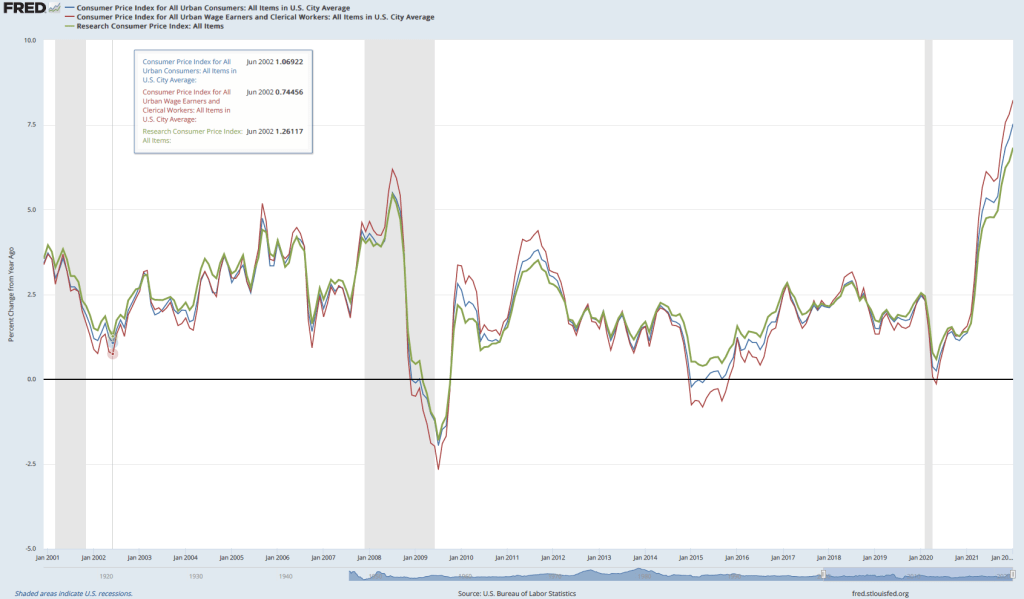

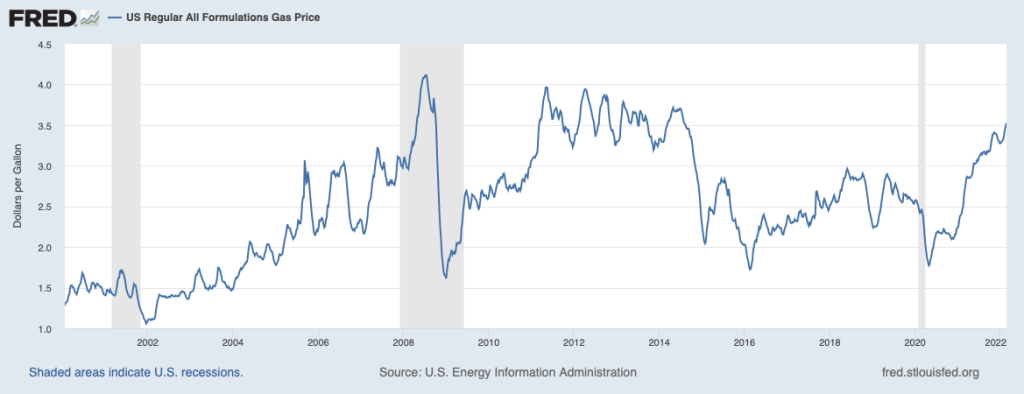

The federal government levies an excise tax of 18.4 cents per gallon of gasoline. (An excise tax is a tax that a government imposes on a particular product. In addition to the tax on gasoline, the federal government imposes excise taxes on tobacco, alcohol, airline tickets, and a few other products.) In February 2022, inflation was running at the highest level in several decades. The average retail price of gasoline across the country had risen to $3.50 per gallon from $2.60 per gallon a year earlier. The following figure shows fluctuations in the retail price of gasoline since January 2000.

Policymakers were looking for ways to lessen the effects of inflation on consumers. An article in the Wall Street Journalreported that several Democratic members of the U.S. Senate, including Mark Kelly of Arizona, Maggie Hassan of New Hampshire, and Raphael Warnock of Georgia proposed that the federal excise tax on gasoline be suspended for the remainder of 2022. The sponsors of the proposal believed that cutting the tax would reduce the price of gasoline that consumers pay at the pump. Other members of the Senate weren’t so sure, with one quoted as saying that cutting the tax was “not going to change anything” and another arguing that oil companies would receive most of the benefit of the tax cut.

Some members of Congress were opposed to suspending the gasoline tax because the revenue raised from the tax is placed in the highway trust fund, which helps to pay for federal contributions to highway building and repair and for mass transit. In that sense, the gasoline tax follows the benefits-received principle, under which people who receive benefits from a government program—in this case, highway maintenance—should help pay for the program. (We discuss the principles for evaluating taxes in Microeconomics, Chapter 17, Section 17.2 and in Economics, Chapter 17, Section 17.2) Other members of Congress were opposed to suspending the tax because they believe that the tax helps to reduce the quantity of gasoline consumed, thereby helping to slow climate change.

Focusing just on the question of the effect of suspending the tax on the retail price of gasoline, what can we conclude? The question is one of tax incidence, which looks at the actual division of the burden of a tax between buyers and sellers in a market. In other words, tax incidence looks beyond the fact that gasoline stations collect the tax and send the revenue to federal government to the issue of who actually pays the tax. As we note in Chapter 17, Section 17.3:

When the demand for a product is less elastic than supply, consumers pay the majority of the tax on the product. When the demand for a product is more elastic than supply, firms pay the majority of the tax on the product.

Consumers would receive all of the tax cut—that is, the retail price of gasoline would fall by 18.4 cents—only in the polar case where the demand for gasoline were perfectly price inelastic. Similarly, consumers would receive none of the tax cut and the price of gasoline would remain unchanged—so oil companies would receive all of the tax cut—only in the polar case where the demand for gasoline is perfectly price inelastic. (It’s a worthwhile exercise to show these two cases using demand and supply graphs.)

In the real world, we would expect to be somewhere in between these two cases, with consumers receiving some of the benefit of suspending the tax and producers receiving the remainder of the benefit. The short-run price elasticity of demand for gasoline is quite small; according to one estimate it is only −.06. The short-run price elasticity of supply of gasoline is likely to be somewhat larger than that in absolute value, which means that we would expect that consumers would receive the majority of the tax cut. (Note that we would expect the long-run price elasticities of demand and supply to both be larger for reasons we discuss in Chapter 6, Section 6.2 and 6.6.) In other words, the retail price of gasoline would fall, holding all other factors constant, but not by the full tax cut of 18.4 cents.

Joseph Doyle of MIT and Krislert Samphantharak of the University of California, San Diego studied the effect of suspension in the state excise tax on gasoline in Indiana and Illinois in 2000. In that year, Indiana suspended collecting its gasoline excise tax for 120 days and Illinois suspended its tax for 184 days. The authors estimate that consumers received about 70 percent of the tax cut in the form of lower gasoline prices. If we apply that estimate to the federal gasoline tax, then suspending the tax would lower the price of gasoline by about 12.9 cents per gallon, holding all other factors that affect the price of gasoline constant. As the above figure shows, the retail price of gasoline frequently fluctuates up and down by more than 12.9 cents, even over fairly brief periods of time. In that sense, the effect on the gasoline market of suspending the federal excise tax on gasoline would be relatively small.

Sources: Andrew Duehren and Richard Rubin, “Some Lawmakers Want to Halt Gas Tax Amid High Inflation. Others See a Gimmick,” Wall Street Journal, February 16, 2022; Tony Romm and Jeff Stein, “White House, Congressional Democrats Eye Pause of Federal Gas Tax as Prices Remain High, Election Looms,” Washington Post, February 15, 2022; Joseph J. Doyle, Jr., Krislert Samphantharak, “$2.00 Gas! Studying the Effects of a Gas Tax Moratorium,” Journal of Public Economics, Vol. 92, No.s 3-4, April 2008, pp. 869-884; and Federal Reserve Bank of St. Louis.