Nvidia’s headquarters in Santa Clara, California. (Photo from nvidia.com)

Nvidia was founded in 1993 by Jensen Huang, Chris Malachowsky, and Curtis Priem, electrical engineers who started the company with the goal of designing computer chips that would increase the realism of images in video games. The firm achieved a key breakthrough in 1999 when it invented the graphics processing unit, or GPU, which it marketed under the name GeForce256. In 2001, Microsoft used a Nvidia chip in its new Xbox video game console, helping Nvidia to become the dominant firm in the market for GPUs.

The technology behind GPUs has turned out to be usable not just for gaming, but also for powering AI—artificial intelligence—software. The market for Nvidia’s chips exploded witth technology giants Google, Microsoft, Facebook and Amazon, as well as many startups ordering large quantites of Nvidia’s chips.

By 2016, Nvidia CEO Jen-Hsun Huang could state in an interview that: “At no time in the history of our company have we been at the center of such large markets. This can be attributed to the fact that we do one thing incredibly well—it’s called GPU computing.” Earlier this year, an article in the Economist noted that: “Access to GPUs, and in particular those made by Nvidia, the leading supplier, is vital for any company that wants to be taken seriously in artificial intelligence (AI).”

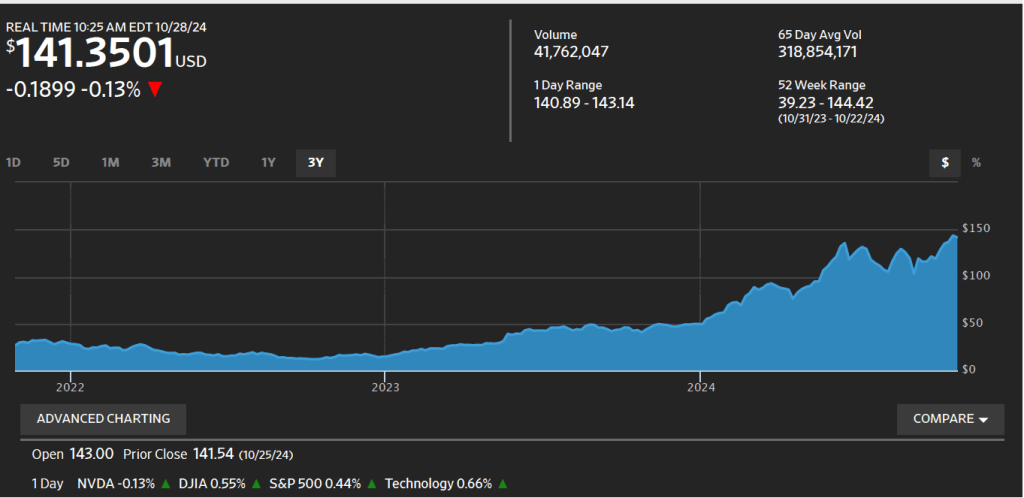

Nvidia’s success has been reflected in its stock price. When Nvidia became a public company in 1999 by undertaking an initial public offering (IPO) of stock, a share of the firm’s stock had a price of $0.04, adjusted for later stock splits. The large profits Nvidia has been earning in recent years have caused its stock price to rise to more than $140 dollars a share.

(With a stock split, a firm reduces the price per share of its stock by giving shareholders additional shares while holding the total value of the shares constant. For example, in June of this year Nvidia carried out a 10 for 1 stock split, which gave shareholders nine shares of stock for each share they owned. The total value of the shares was the same, but each share now had a price that was 10 percent of its price before the split. We discuss the stock market in Microeconomics, Chapter 8, Section 8.2, Macroeconomics, Chapter 6, Section 6.2, and Economics, Chapter 8, Section 8.2.)

The following figure from the Wall Street Journal shows the sharp increase in Nvidia’s stock price over the past three years as AI has become an increasingly important part of the economy.

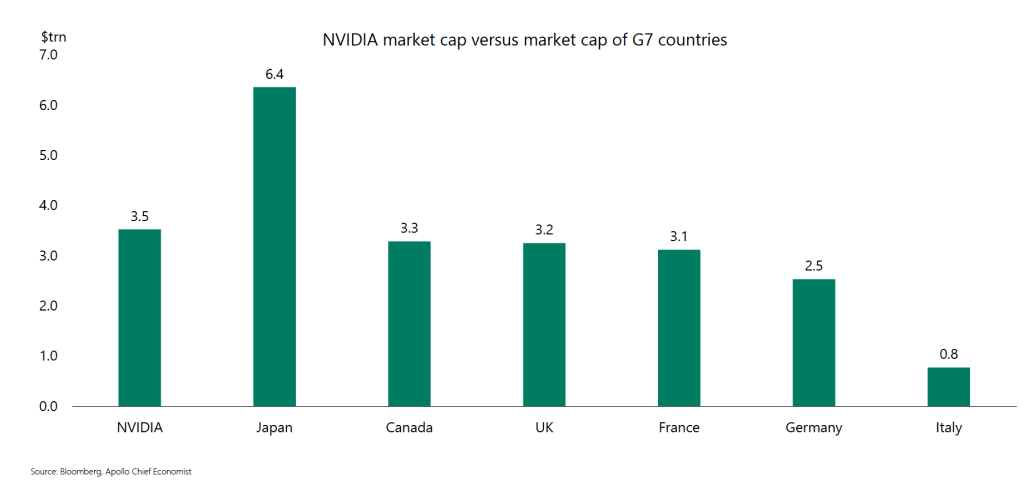

Nvidia’s market capitalization (or market cap)—the total value of all of its outstanding shares of stock—is $3.5 trillion. How large is that? Torsten Sløk, the chief economist at Apollo, an asset management firm, has noted that, as shown in the following figure, Nvidia’s market cap is larger than the total market caps—the total value of all the publicly traded firms—in five large economies.

Can Nvidia’s great success continue? Will it be able to indefinitely dominate the market for AI chips? As we noted in Apply the Concept “Do Large Firms Live Forever?” in Microeconomics Chapter 14, in the long run, even the most successful firms eventually have their positions undermined by competition. That Nvidia has a larger stock market value than the total value of all the public companies in Germany or the United Kingdom is extraordinary and seems impossible to sustain. It may indicate that investors have bid up the price of Nvidia’s stock above the value that can be justified by a reasonable forecast of its future profits.

There are already some significant threats to Nvidia’s dominant position in the market for AI chips. GPUs were originally designed to improve computer displays of graphics rather than to power AI software. So, one way of competing with Nvidia that some startups are trying to exploit is to design chips specifically for use in AI. It’s also possible that larger chips may make it possible to use fewer chips than when using GPUs, possibly reducing the total cost of the chips necessary to run sophisticated AI software. In addition, existing large technology firms, such as Amazon and Microsoft, have been developing chips that may be able to compete with Nvidia.

As with any firm, Nvidia’s continued success requires it to innovate sufficiently to stay ahead of the many competitors that would like to cut into the firm’s colossal profits.

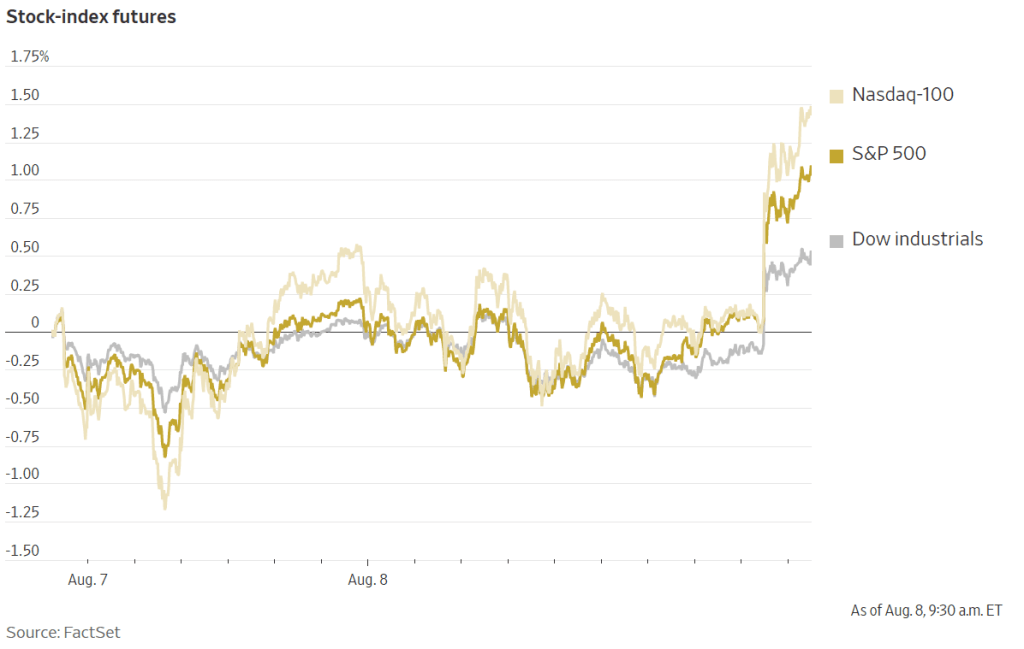

Over the first past few days, the stock and bond markets have gone through substantial swings as investors try to determine whether the U.S. economy is likely to move into a recession soon. (We discussed here the most recent BLS “Employment Situation” report, which was surprisingly weak.)

It’s difficult to determine with certainty why on a particular day stock and bond prices fluctuate. The following two figures from the Wall Street Journal show movements this morning (August 8) in stock prices and bond yields. (Recall that bond yields rise when bond prices fall, a point we discuss in the Appendix to Chapter 6 of Macroeconomics (Chapter 8 of Economics).)

Rising stock prices and falling bond prices (rising bond yields) can be an indication that investors are more optimistic that the U.S. economy will avoid a recession. In a recession, profits decline, which is bad for stock prices. And in a recession, interest rates typically fall both because the Federal Reserve cuts it target range for the federal funds rate and because household and firms borrow less, which reduces the demand for loanable funds. Accordingly, most analysts are attributing the movements in stock and bond prices this morning to investors becoming more optimistic that the U.S. economy will avoid a recession.

Because of the level of uncertainty about the future path of the economy, investors are following very closely the release of new macroeconomic data. The Wall Street Journal and other business publications attributed the increase in investor optimism this morning to the U.S. Employment and Training Administration releasing at 8:30 a.m. its latest report on initial claims for unemployment insurance. The headline in the Wall Street Journal was: “Stocks Rise on Claims Data.” Similalry, the headline on bloomberg.com was: “Stocks Get Relief Rally after Jobless Claims Data.”

What are jobless claims? The first step when you lose a job and wish to receive government unemployment insurance payments is to file a claim, which starts the process by which an agency of the state government determines whether you are eligible to receive unemployment insurance payments.

The data on initial jobless claims are released weekly. As the following figure shows, there is a lot of volatility in this data series. The latest data were favorable—which is thought to have caused the increase in stock prices and decline in bond prices—because new claims declined by 17,000 this week. But the series is so volatile that drawing conclusions from weekly changes seems unwarranted. For instance, the figure shows that weekly claims surged during the summer of 2023, although employment and production continued to expand during that period.

So it appears that people trading in stock and bond markets this morning are overreacting to this macrodata release. But explanations of why stock and bonds prices move as they do over a short period of time often turnout in hindsight to have been incorrect. It may well be the case that investors are acting as they are this morning for reasons that are, in fact, unrelated to the data on jobless claims.

Supports:Macroeconomics, Chapter 5, Section 5.3 or Chapter 6, Section 6.1; Microeconomics and Economics, Chapter 7, Section 7.3 or Chapter 8, Section 8.1.

Image from Reuters via the Wall Street Journal.

A recent paper by Iyah Rahwan, of the Max Planck Institute for Human Development in Berlin Germany, and colleagues raises the possibility that dating apps, like Tinder, OkCupid, and Bumble, may have a principal-agent problem. Dating apps—like nearly all other subscription apps—generate more income if subscribers pay for the app over a longer period of time. Many people use dating apps in the hope of connecting with another app user with whom they can have a long-term relationship.

a. What is the principal-agent problem?

b. Explain whether dating apps may have a principal-agent problem. If they do, who is the principal and who is the agent?

c. How does your answer to part b. affect your estimate of how likely people using dating apps are to find a long-term relationship using these apps?

Solving the Problem

Step 1:Review the chapter material. This problem is about the principal-agent problem, so you may want to review either of the two sections in which the principal-agent problem is discussed: Macroeconomics, Chapter 5, Section 5.3, “Information Problems and Externalities in the Market for Health Care” or Chapter 6, Section 6.1, “Types of Firms” (Microeconomics and Economics, Chapter 7, Section 7.3 or Chapter 8, Section 8.1.)

Step 2:Answer part a. by defining “principal-agent” problem. Principal-agent is defined in the textbook this way: A problem caused by an agent pursuing the agent’s own interests rather than the interests of the principal who hired the agent.

Step 3: Answer part b. by explaining why dating apps may have a principal-agent problem and by identifying who is the principal and who is the agent in this situation. With dating apps, the principal is the app user who, typically, uses the app to help find a partner for a long-term relationship. The owners of the dating app are the agent because they have been hired by the app user to help the user achieve the goal of starting a long-term relationship. Unfortunately, the owners of the dating app have a different goal than does the app user. The goal of the owners is to have users keep subscribing to the app. Anyone who finds a long-term relationship using the app is likely (we hope!) to drop his or her subscription to the app. Therefore, whereas the app user would like to quickly find a partner for a long-term relationship, the owners of the app want the app user to take a long time to find such a partner.

Step 4: Answer part c. by discussing how the principal-agent problem may affect the likelihood of someone using a dating app successfully finding someone for a long-term relationship. The answer to part b. indicates that dating apps may have an incentive to make it somewhat more difficult to find a long-term relationship using the app—perhaps by employing a matching algorithm that doesn’t result in users easily finding good matches. Therefore, it’s likely that the principal-agent problem make it less likely that people using dating apps will successfully find a partner for a long-term relationship.

Source: Iyah Rahwan, et al., “Price of Anarchy in Algorithmic Matching of Romantic Partners,” ACM Transactions on Economics and Computation, Vol. 12, No. 1, pp. 1-25.

Agents from the National Transportation Safety Board inspect a piece of the Boeing jetliner found in a backyard in Portland, Oregon. (Photo from the AP via the New York Times.)

What causes movements in stock prices? As we explain in Economics and Microeconomics, Chapter 8, Section 8.2 (Macroeconomics, Essentials of Economics, and Money, Banking, and the Financial System, Chapter 6, Section 6.2): “Shares of stock represent claims on the profits of the firms that issue them. As the fortunes of the firms change and they earn more or less profit, the prices of the stock the firms have issued should also change.”

We also note that: “Many Wall Street investment professionals expend a great deal of effort gathering all possible information about the future profitability of firms, hoping to buy the stocks that are most likely to rise in the future. As a result of the actions of these professional investors, all of the information about a firm that is available on news and financial websites, cable TV business shows, and online discussion sites like X and Reddit is already reflected in the firm’s stock price.” As a consequence, the price of a firm’s stock will change only as a result of new information about the future profitability of the firm issuing the stock.

During the course of a typical week, the new information that becomes available about a large company, like Apple or General Motors, is likely to indicate only minor changes in the future profitability of the firm. Therefore, we wouldn’t expect that the firm’s stock price would change very much. Sometimes, though, investors receive important new information that causes them to significantly revise their expectations of the future profitability of a firm. That’s what happened to Boeing, the jetliner manufacturer, on Friday, January 5. An Alaska Air Boeing 737 Max 9 was taking off from Portland International Airport when a piece of the plane blew out. (A Wall Street Journalarticle gives the details of the incident.)

The accident caused some industry observers to question whether Boeing’s quality control during manufacturing had deficiencies that might lead to other problems being discovered on the firm’s jetliners. Boeing was particularly at risk of having its quality control methods questioned because in 2019 two slightly different models of the 737 Max airliner had crashed, causing the planes to be grounded for almost two years.

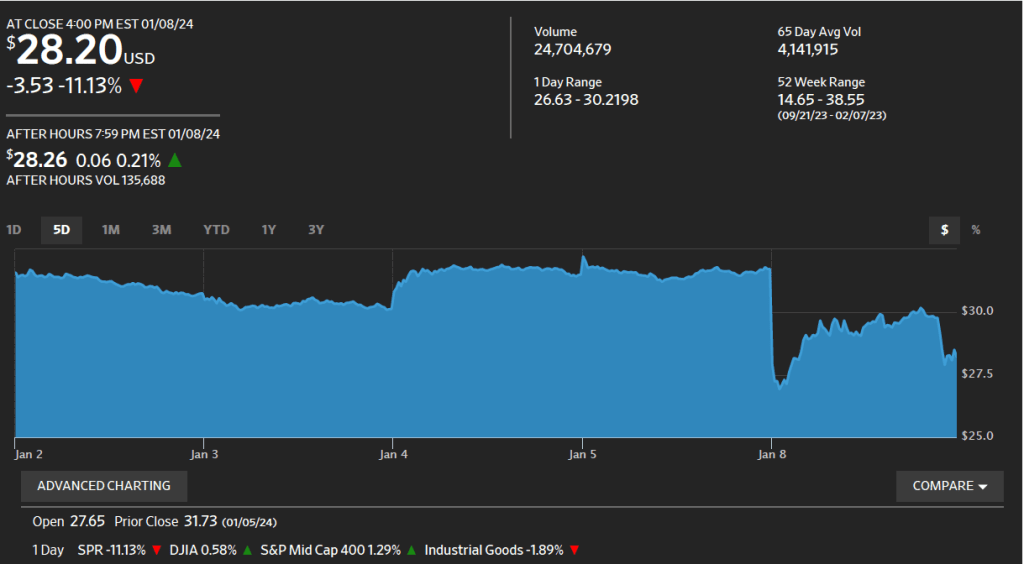

The effect of the Alaska Air incident on Boeing’s stock price can be seen in the following figure, reproduced from the Wall Street Journal. On Friday, January 5 at 4 pm eastern time—the time at which trading on the New York Stock Exchange (NYSE) closes for the day—the price of Boeing’s stock was $249.00 per share. The accident took place at around 7:40 pm eastern time, so it occurred after the close of trading on the NYSE. When trading on the NYSE resumed at 9:30 am on Monday, January 8, Boeing’s stock price had declined to $227.79 per share. The size of the drop in price indicated that investors believed that the Portland accident would have a significantly negative affect on Boeing’s future profitability. Boeing’s profits could fall if the accident leads airlines to reduce their future purchases of 737 Max airliners or if Boeing’s costs rise significantly as a result of making repairs on Max airliners currently in servide or as a result of having to spend more on quality control measures when manufacturing the planes.

The effect of the Portland accident on Boeing’s stock price is an example of the efficiency of the stock market in processing information about a firm’s future profitability.

A trader on the New York Stock Exchange listtening to Fed Chair Jerome Powell (from Reuters via the New York Times)

Accounting for movements in the market prices of stocks and bonds is not an exact exercise. Accounts in the Wall Street Journal and on other business web sites often attribute movements in stock and bond prices to the Fed having acted in a way that investors didn’t expect.

The decision by the Fed’s Federal Open Market Committee (FOMC) at its meeting on September 20-21, 2023 to hold its target for the federal funds rate constant at a range of 5.25 percent to 5.50 percent wasn’t a surprise. Fed Chair Jerome Powell had signaled during his press conference on July 26 following the FOMC’s previous meeting that the FOMC was likely to pause further increases in the federal funds rate target. (A transcript of Powell’s July 26 press conference can be found here.)

In advance of the September meeting, some other members of the FOMC had also signaled that the committee was unlikely to increase its target. For instance, an article in the Wall Street Journal quoted Susan Collins, president of the Federal Reserve Bank of Boston, as stating that: “The risk of inflation staying higher for longer must now be weighed against the risk that an overly restrictive stance of monetary policy will lead to a greater slowdown than is needed to restore price stability.” And in a speech in August, Raphael Bostic, president of the Federal Reserve Bank of Atlanta, explained his position on future rate increases: “Based on current dynamics in the macroeconomy, I feel policy is appropriately restrictive. I think we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain.”

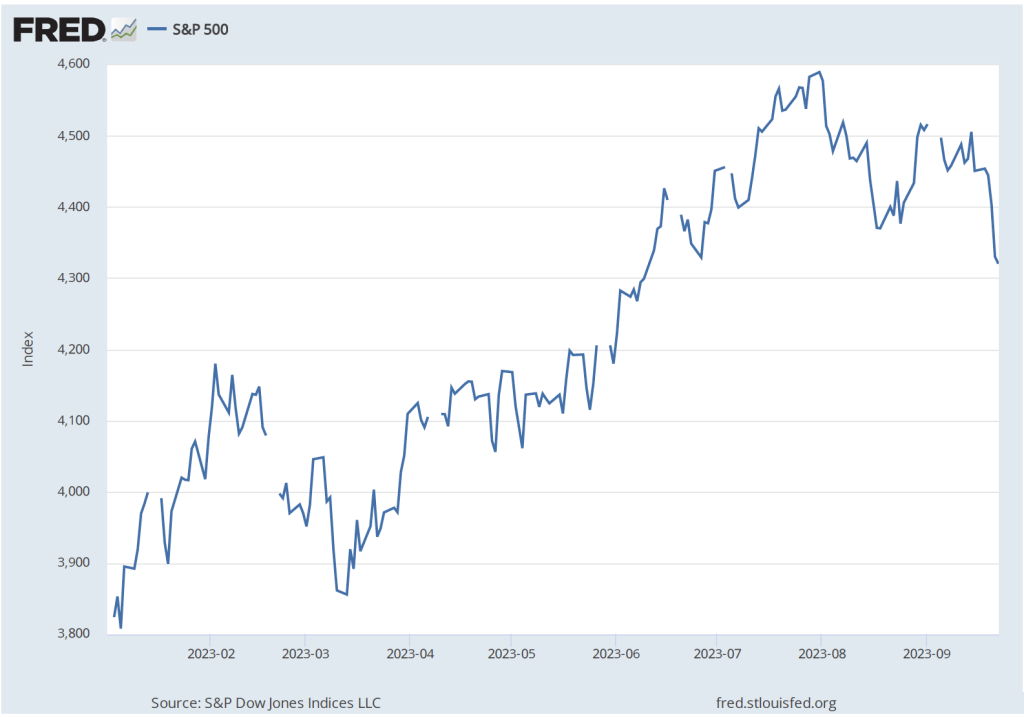

Although it wasn’t a surprise that the FOMCdecided to hold its target for the federal funds rate constant, after the decision was announced, stock and bond prices declined. The following figure shows the S&P 500 index of stock prices. The index declined 2.8 percent from September 19—the day before the FOMC meeting—to September 22—two days after the meeting. (We discuss indexes of stock prices in Macroeconomics, Chapter 6, Section 6.2; Economics, Chapter 8, Section 8.2; and Essentials of Economics, Chapter 8, Section 8.2.)

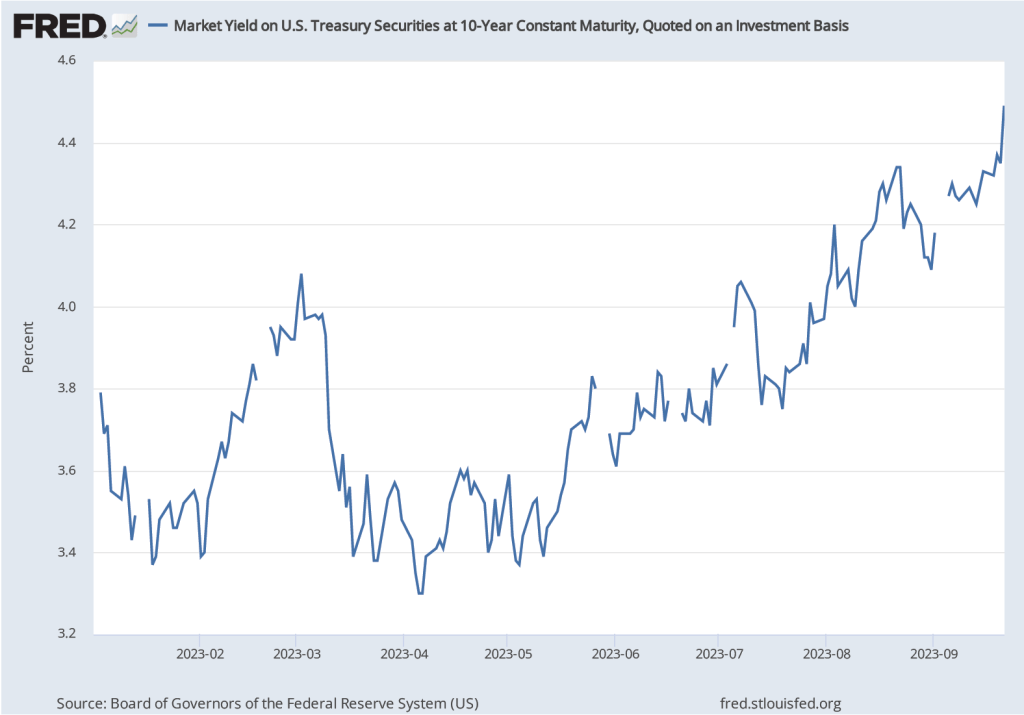

We see a similar pattern in the bond market. Recall that when the price of bonds declines in the bond market, the interest rates—or yields—on the bonds increase. As the following figure shows, the interest rate on the 10-year Treasury note rose from 4.37 percent on September 19 to 4.49 percent on September 21. The 10-year Treasury note plays an important role in the financial system, influencing interest rates on mortgages and corporate bonds. So, the yield on the 10-year Treasury note increasing from 3.3 percent in the spring of 2023 to 4.5 percent following the FOMC meeting has the effect of increasing long-term interest rates throughout the U.S. economy.

What explains the movements in the prices of stocks and bonds following the September FOMC meeting? Investors seem to have been surprised by: 1) what Chair Powell had to say in his news conference following the meeting; and 2) the committee members’ Summary of Economic Projections (SEP), which was released after the meeting.

Powell’s remarks were interpreted as indicating that the FOMC was likely to increase its target for the federal funds rate at least once more in 2023 and was unlikely to cut its target before late 2024. For instance, in response to a question Powell said: “We need policy to be restrictive so that we can get inflation down to target. Okay. And we’re going to need that to remain to be the case for some time.” Investors often disagree in their interpretations of what a Fed chair says. Fed chairs don’t act unilaterally because the 12 voting members of the FOMC decide on the target for the federal funds rate. So chairs tend to speak cautiously about future policy. Still, their seemed to be a consensus among investors that Powell was indicating that Fed policy would be more restrictive (or contractionary) than had been anticipated prior to the meeting.

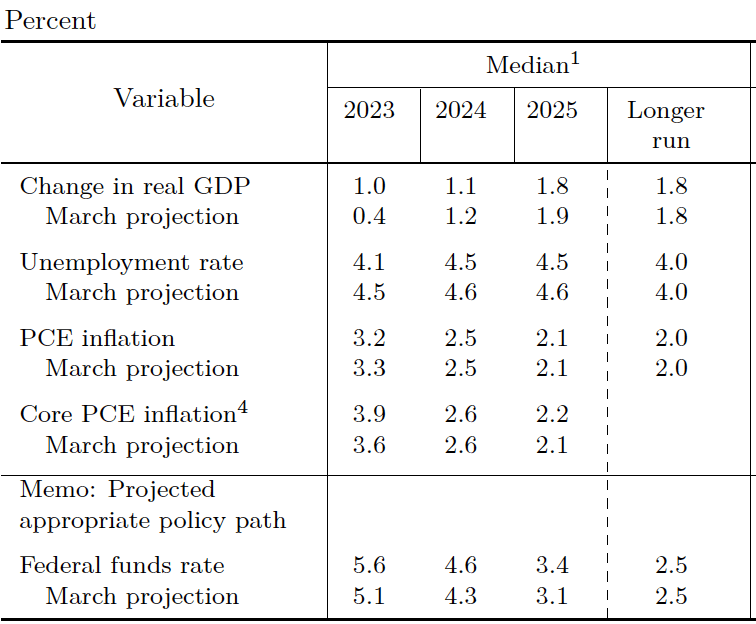

The FOMC releases the SEP four times per year. The most recent SEP before the September meeting was from the June meeting. The table below shows the median of the projections, or forecasts, of key economic variables made by the members of the FOMC at the June meeting. Note the second row from the bottom, which shows members’ median forecast of the federal funds rate.

The following table shows the median values of members’ forecast at the September meeting. Look again at the next to last row. The members’ forecast of the federal funds rate at the end of 2023 was unchanged. But their forecasts for the federal funds rate at the end of 2024 and 2025 were both 0.50 percent higher.

Why were members of the FOMC signaling that they expected to hold their target for the federal funds rate higher for a longer period? The other economic projections in the tables provide a clue. In September, the members expected that real GDP growth would be higher and the unemployment rate would be lower than they had expected in June. Stronger economic growth and a tighter labor market seemed likely to require them to maintain a contractionary monetary policy for a longer period if the inflation rate was to return to their 2.0 percent target. Note that the members didn’t expect that the inflation rate would return to their target until 2026.

Photo of a Walmart store from the Associated Press via the Wall Street Journal.

Many people are familiar with Fortune magazine’s list of the 500 largest U.S.-based firms, measured by their revenue in 2022. (Note: It’s easy to confuse the Fortune 500 with the S&P 500. Firms are included in the S&P 500 on the basis of their market capitalization—the value of all of their outstanding shares of stock—rather than on the basis of their revenue. The S&P 500 is used to compute the most widely followed stock market index. See Microeconomics and Economics, Chapter 8, Section 8.2, and Macroeconomics and Essentials of Economics, Chapter 6, Section 6.2.)

Fortune also compiles a global 500 list, which includes firms based anywhere in the world. The table below shows the top 10 firms on this Fortune list. With more than $600 billion in revenue in 2022, Walmart tops the list. Five of the ten largest firms are in the oil industry. The three firms based in China are owned by the Chinese government. The Saudi government owns more than half of Saudi Aramco.

Firm

Industry

Country

Walmart

Retailing

United States

Saudi Aramco

Oil

Saudi Arabia

State Grid

Public utility

China

Amazon

Retailing

United States

China National Petroleum

Oil

China

Sinopec Group

Oil

China

Exxon Mobil

Oil

United States

Apple

Consumer electronics

United States

Shell

Oil

United Kingdom

UnitedHealth Group

Health insurance

United States

The following table shows how many firms among the top 100 are headquartered in the listed countries. All countries that have more than one firm located in them are included. Far more of these large firms are located in the United States and China than in any of the other countries. Germany, Japan, France, and South Korea are the only other countries that are the headquarters for more than two firms.

Rumors spread about the financial state of a bank. Some depositors begin to withdraw funds from their accounts. Suddenly a wave of withdrawals occurs and regulators step in and close the bank. A description of a run on a bank in New York City in the fall of 1930? No. This happened to Silicon Valley Bank, headquartered in Santa Clara, California and the sixteenth largest bank in the United States, on Friday, March 10, 2023.

Background on Bank Runs

In Macroeconomics, Chapter 14, Section 14.4 (Economics, Chapter 24, Section 24.4) we describe the basic reasons why a run on a bank may occur. We describe bank runs in greater detail in Money, Banking, and the Financial System, Chapter 12. We reproduce here a key paragraph on the underlying fragility of commercial banking from Chapter 12 of the money and banking text:

The basic activities of commercial banks are to accept short-term deposits, such as checking account deposits, and use the funds to make loans—including car loans, mortgages, and business loans—and to buy long-term securities, such as municipal bonds. In other words, banks borrow short term from depositors and lend, often long term, to households, firms, and governments. As a result, banks have a maturity mismatch because the maturity of their liabilities—primarily deposits—is much shorter than the maturity of their assets—primarily loans and securities. Banks are relatively illiquid because depositors can demand their money back at any time, while banks may have difficulty selling the loans in which they have invested depositors’ money. Banks, therefore, face liquidity risk because they can have difficulty meeting their depositors’ demands to withdraw their money. If more depositors ask to withdraw their money than a bank has money on hand, the bank has to borrow money, usually from other banks. If banks are unable to borrow to meet deposit withdrawals, then they have to sell assets to raise the funds. If a bank has made loans and bought securities that have declined in value, the bank may be insolvent, which means that the value of its assets is less than the value of its liabilities, so its net worth, or capital, is negative. An insolvent bank may be unable to meet its obligations to pay off its depositors.

The Founding of the Fed and the Establishment of the FDIC as a Response to Bank Runs

The instability of the banking system led to a number of financial crises during the 1800s and early 1900s, culminating in the Panic of 1907. Congress responded by passing the Federal Reserve Act in 1913, establishing the Federal Reserve System. The Fed was given the role of lender of last resort, making discount loans to banks that were experiencing deposit runs but that remained solvent. The failure of the Fed to stop the bank panics of the early 1930s led Congress to establish the Federal Deposit Insurance Corporation (FDIC) to ensure deposits in commercial banks, originally up to a limit of $2,500 per deposit, per bank. The current limit is $250,000.

Deposit insurance reduced the likelihood of runs but increased moral hazard in the banking system by eliminating the incentive insured depositors had to monitor the actions of bank managers. In principle, bank managers still have an incentive to avoid making risky loans and other investments for fear of withdrawals by households and firms with deposits that exceed the dollar deposit limit.

Contagion, Moral Hazard, and the Too-Big-to-Fail Policy

But if these depositors fail to monitor risk taking by bank managers or if a bank’s loans and investments decline in price even though they weren’t excessively risky at the time they were made, the FDIC and the Fed face a dilemma. Allowing banks to fail and large depositors to be only partially paid back may set off a process of contagion that results in runs spreading to other banks. Problems in the banking system can affect the wider economy by making it more difficult for households and firms that depend on bank loans to finance their spending. (We discuss the process of contagion in this post on the Diamond-Dybvig model.)

The Fed and the FDIC can stop the process of contagion if they are willing to ensure that large depositors don’t suffer losses. One mechanism to achieve this result is facilitating a merger between an insolvent bank and another bank that agrees to assume responsibility for meeting depositors withdrawals from the insolvent bank. But stopping contagion in this manner with no depositors suffering losses can be interpreted as amounting to deposit insurance having no dollar limit. The result is a further increase in moral hazard in the banking system. When the federal government does not allow large financial firms to fail for fear of damaging the financial system, it is said to be following a too-big-to-fail policy.

Silicon Valley Bank and VCs

Runs on commercial banks have been rare in recent decades, which is why the run on Silicon Valley Bank (SVB) took many people by surprise. As its name indicates, SVB is located in the heart of California’s Silicon Valley and the bank played an important role in the financing of many startups in the area. As such, SVB provided banking services to many venture capital (VC) firms. As we note in Chapter 9, Section 9.2 of the money and banking text, venture capital firms play an important role in providing funding to startup firms:

VCs such as Sequoia Capital, Accel, and Andreessen Horowitz raise funds from investors and invest in small startup firms, often in high-technology industries. In recent years, VCs have raised large amounts from institutional investors, such as pension funds and university endowments. A VC frequently takes a large ownership stake in a startup firm, often placing its own employees on the board of directors or even having them serve as managers. These steps can reduce principal–agent problems because the VC has a greater ability to closely monitor the managers of the firm it’s investing in. The firm’s managers are likely to be attentive to the wishes of a large investor because having a large investor sell its stake in the firm may make it difficult to raise funds from new investors. In addition, a VC avoids the free-rider problem when investing in a firm that is not publicly traded because other investors cannot copy the VC’s investment strategy.

An article on bloomberg.com summarized SVB’s role in Silicon Valley. SVB is

the single most critical financial institution for the nascent tech scene, serving half of all venture-backed companies in the US and 44% of the venture-backed technology and health-care companies that went public last year. And its offerings were vast — ranging from standard checking accounts, to VC investment, to loans, to currency risk management.

Note from this description that SVB acted as a VC—that is, it made investments in startup firms—as well as engaging in conventional commercial banking activities, such as making loans and accepting deposits. The CEO of one startup was quoted in an article in the Wall Street Journal as saying, “For startups, all roads lead to Silicon Valley Bank.” (The Wall Street Journal article describing the run on SVB can be found here. A subscription may be required.)

SVB’s Vulnerability to a Run

As with any commercial bank, the bulk of SVB’s liabilities were short-term deposits whereas the bulk of its assets were long-term loans and other investments. We’ve discussed above that this maturity mismatch means that SVB—like other commercial banks—was vulnerable to a run if depositors withdraw their funds. We’ve also seen that in practice bank runs are very rare in the United States. Why then did SVB experience a run? SVB was particularly vulnerable to a run for two related reasons:

1. Its deposits are more concentrated than is true of a typical bank. Many startups and VCs maintain large checking account balances with SVB. According to the Wall Street Journal, at the end of 2022, SVB had $157 billion in deposits, the bulk of which were in just 37,000 accounts. Startups often initially generate little or no revenue and rely on VC funding to meet their expenses. Most Silicon Valley VCs advised the startups they were invested in to establish checking accounts with SVB.

2. Accordingly, the bulk of the value of deposits at SVB was greater than the $250,000 FDIC insurance limit. Apparently 93 percent to 97 percent of deposits were above the deposit limit as opposed to about 50 percent for most commercial banks.

Economics writer Noah Smith notes that SVB required that startups it was lending to keep their deposits with SVB as a condition for receiving a loan. (Smith’s discussion of SVB can be found on his Substack blog here. A subscription may be required.)

The Reasons for the Run on SVB

When the Fed began increasing its target for the federal funds rate in March 2022 in response to a sharp increase in inflation, longer term interest rates, including interest rates on U.S. Treasury securities, also increased. For example the interest rate on the 10-year Treasury note increased from less than 2 percent in March 2022 to more than 4 percent in March 2023. The interest rate on the 2-year Treasury note increased even more, from 1.5 percent in March 2022 to around 5 percent in March 2023.

As we discuss in the appendix to Macroeconomics, Chapter 6 (Economics, Chapter 8) and in greater detail in Money, Banking, and the Financial System, Chapter 3, the price of a bond or other security equals the present value of the payments the owner of the security will receive. When market interest rates rise, as happened during 2022 and early 2023, the value of the payments received on existing securities—and therefore the prices of these securities—fall. Treasury securities are free from default risk, which is the risk that the Treasury won’t make the interest and principal payments on the security, but are subject to interest-rate risk, which is the risk that the price of security will decrease as market interest rates rise.

As interest rates rose, the value of bonds and other long-term assets that SVB owned fell. The price of an asset on the balance sheet of a firm is said to be marked to market if the price is adjusted to reflect fluctuations in the asset’s market price. However, banking law allows a bank to keep constant the prices of bonds on its balance sheets if it intends to hold the bonds until they mature, at which point the bank will receive a payment equal to the principal of the bond. But if a bank needs to sell bonds, perhaps to meet its liquidity needs as depositors make withdrawals, then the losses on the bonds have to be reflected on the bank’s balance sheet.

SVB’s problems began on Wednesday, March 8 when it surprised Wall Street analysts and the bank’s Silicon Valley clients by announcing that to raise funds it had sold $21 billion in securities at a loss of $1.8 billion. It also announced that it was selling stock to raise additional funds. (SVB’s announcement can be found here.) SVB’s CEO also announced that the bank would borrow an additional $15 billion. Although the CEO stated that the bank was solvent, as an article on fortune.com put it, “Investors didn’t buy it.” In addition to the news that SVB had suffered a loss on its bond sales and had to raise funds, some analysts raised the further concern that the downturn in the technology sector meant that some of the firms that SVB had made loans to might default on the loans.

Problems for SVB compounded the next day, Thursday, March 9, when Peter Theil, a co-founder of PayPal and Founders Fund, a leading VC, advised firms Founders Fund was invested in to withdraw their deposits from SVB. Other VCs began to pull their money from SVB and advised their firms to do the same and a classic bank run was on. Because commercial banks lack the funds to pay off a significant fraction of their depositors over a short period of time, in a run, depositors with funds above the $250,000 deposit insurance limit know that they need to withdraw their funds before other depositors do and the bank is forced to close. This fact makes it difficult for a bank to stop a run once it gets started.

According to an article in the Wall Street Journal, by the end of business on Thursday, depositors had attempted to withdraw $42 billion from SVB. The FDIC took control of SVB the next day, Friday, March 10, before the bank could open for business.

The Government Response to the Collapse of SVB

The FDIC generally handles bank failures in one of two ways: (1) It closes the bank and pays off depositors, or (2) it purchases and assumes control of the bank while finding another bank that is willing to purchase the failed bank. If the FDIC closes a bank, it pays off the insured depositors immediately, using the bank’s assets. If those funds are insufficient, the FDIC makes up the difference from its insurance reserves, which come from payments insured banks make to the FDIC. After the FDIC has compensated insured depositors, any remaining funds are paid to uninsured depositors.

As we write this on Sunday, March 12, leaders of the Fed, the FDIC, and the Treasury Department, were considering what steps to take to avoid a process of contagion that would cause the failure of SVB to lead to deposit withdrawals and potential failures of other banks—in other words, a bank panic like the one that crippled the U.S. economy in the early 1930s, worsening the severity of the Great Depression. These agencies hoped to find another bank that would purchase SVB and assume responsibility for meeting further deposit withdrawals.

Another possibility was that the FDIC would declare that closing SVB, selling the bank’s assets, and forcing depositors above the $250,000 deposit limit to suffer losses would pose a systemic risk to the financial system. In that circumstance, the FDIC could provide insurance to all depositors however large their deposits might be. As discussed earlier, this approach would increase moral hazard in the banking system because it would, in effect, waive the limit on deposit insurance. Although the waiver would apply directly only to this particular case, large depositors in other banks might conclude that if their bank failed, the FDIC would waive the deposit limit again. Under current law, the FDIC could only announce they were waiving the deposit limit if two-thirds of the FDIC’s Board of Directors, two-thirds of the Fed’s Board of Governors, and Treasury Secretary Janet Yellen agreed that failure of SVB would pose a systemic risk to the financial system.

According to an article on wsj.com posted at 4 pm on Sunday afternoon, bank regulators were conducting an auction for SVB in the hopes that a buyer could be found that would assume responsibility for the bank’s uninsured deposits. [Update evening of Monday March 13: The Sunday auction failed when no U.S. banks entered a bid. Late Monday, the FDIC was planning on holding another auction, with potentially better terms available for the acquiring bank.]

Update: At 6:15 pm Sunday, the Treasury, the Fed, and the FDIC issued a statement (you can read it here). As we noted might occur above, by invoking a situation of systemic risk, the FDIC was authorized to allow all depositors–including those with funds above the deposit limit of $250,000–to access their funds on Monday morning. Here is an excerpt from the statement:

“After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.”

[Update Monday morning March 13] As we discussed above, one of the problems SVB faced was a decline in the prices of its bond holdings. As a result, when it sold bonds to help meet deposit outflows, it suffered a $2.1 billion loss. Most commercial banks have invested some of their deposits in Treasury bonds and so potentially face the same problem of having to suffer losses if they need to sell the bonds to meet deposit outflows.

To deal with this issue, Sunday night the Fed announced that it was establishing the Bank Term Funding Program (BTFP). Banks and other depository institutions, such as savings and loans and credit unions, can use the BTFP to borrow against their holdings of Treasury and mortgage-backed securities and agency debt. (Agency debt consists of bonds issued by any federal government agency other than the U.S. Treasury. Most agency debt is bonds issued by the Government Sponsored Agencies (GSEs) involved in the mortgage market: Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and the Federal Home Loan Mortgage (Freddie Mac).) The Fed explained its reasons for setting up the BTFP: “The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.” You can read the Fed’s statement here.

On Sunday, Signature Bank was closed by New York state banking officials and the FDIC. As with SVB, the Fed, FDIC, and Treasury announced that all depositors, including those whose deposits were above the $250,000 deposit limit, would be able to withdraw the full amount of their deposits.

Shareholders in SVB and Signature Bank lost their investments when the FDIC took control of the banks. On Monday morning, investors were selling shares of a number of regional banks who might also face runs, fearing that their investments would be lost if the FDIC were to seize these banks.

President Biden, speaking from the White House, attempted to reassure the public that the banking system was safe. He stated that he would ask Congress to explore changes in banking regulations to reduce the likelihood of future bank failures.

On Tuesday, August 30, 2022, the U.S. Bureau of Labor Statistics (BLS) released its Job Openings and Labor Turnover Survey (JOLTS) report for July 2022. The report indicated that the U.S. labor market remained very strong, even though, according to the Bureau of Economic Analysis (BEA), real gross domestic product (GDP) had declined during the first half of 2022. (In this blog post, we discuss the possibility that during this period the real GDP data may have been a misleading indicator of the actual state of the economy.)

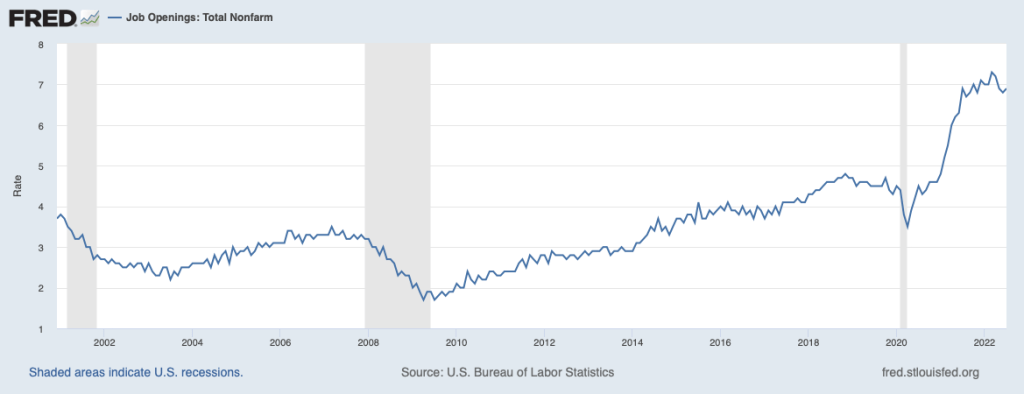

As the following figure shows, the rate of job openings remained very high, even in comparison with the strong labor market of 2019 and early 2020 before the Covid-19 pandemic began disrupting the U.S. economy. The BLS defines a job opening as a full-time or part-time job that a firm is advertising and that will start within 30 days. The rate of job openings is the number of job openings divided by the number of job openings plus the number of employed workers, multiplied by 100.

In the following figure, we compare the total number of job openings to the total number of people unemployed. The figure shows that in July 2022 there were almost two jobs available for each person who was unemployed.

Typically, a strong job market with high rates of job openings indicates that firms are expanding and that they expect their profits to be increasing. As we discuss in Macroeconomics, Chapter 6, Section 6.2 (Microeconomics and Economics, Chapter 8, Section 8.2) the price of a stock is determined by investors’ expectations of the future profitability of the firm issuing the stock. So, we might have expected that on the day the BLS released the July JOLTS report containing good news about the labor market, the stock market indexes like the Dow Jones Industrial Average, the S&P 500, and the Nasdaq Composite Index would rise. In fact, though the indexes fell, with the Dow Jones Industrial Average declining a substantial 300 points. As a column in the Wall Street Journal put it: “A surprisingly tight U.S. labor market is rotten news for stock investors.” Why did good news about the labor market could cause stock prices to decline? The answer is found in investors’ expectations of the effect the news would have on monetary policy.

In August 2022, Fed Chair Jerome Powell and the other members of the Federal Reserve Open Market Committee (FOMC) were in the process of tightening monetary policy to reduce the very high inflation rates the U.S. economy was experiencing. In July 2022, inflation as measured by the percentage change in the consumer price index (CPI) was 8.5 percent. Inflation as measured by the percentage change in the personal consumption expenditures (PCE) price index—which is the measure of inflation that the Fed uses when evaluating whether it is hitting its target of 2 percent annual inflation—was 6.3 percent. (For a discussion of the Fed’s choice of inflation measure, see the Apply the Concept “Should the Fed Worry about the Prices of Food and Gasoline,” in Macroeconomics, chapter 15, Section 15.5 and in Economics, Chapter 25, Section 25.5.)

To slow inflation, the FOMC was increasing its target for the federal funds rate—the interest rate that banks charge each other on overnight loans—which in turn was leading to increases in other interest rates, such as the interest rate on residential mortgage loans. Higher interest rates would slow increases in aggregate demand, thereby slowing price increases. How high would the FOMC increase its target for the federal funds rate? Fed Chair Powell had made clear that the FOMC would monitor economic data for indications that economic activity was slowing. Members of the FOMC were concerned that unless the inflation rate was brought down quickly, the U.S. economy might enter a wage-price spiral in which high inflation rates would lead workers to push for higher wages, which, in turn, would increase firms’ labor costs, leading them to raise prices further, in response to which workers would push for even higher wages, and so on. (We discuss the concept of a wage-price spiral in this earlier blog post.)

In this context, investors interpretated data showing unexpected strength in the economy—particularly in the labor market—as making it likely that the FOMC would need to make larger increases in its target for the federal fund rate. The higher interest rates go, the more likely that the U.S. economy will enter an economic recession. During recessions, as production, income, and employment decline, firms typically experience lower profits or even suffer losses. So, a good JOLTS report could send stock prices falling because news that the labor market was stronger than expected increased the likelihood that the FOMC’s actions would push the economy into a recession, reducing profits. Or as the Wall Street Journal column quoted earlier put it:

“So Tuesday’s [JOLTS] report was good news for workers, but not such good news for stock investors. It made another 0.75-percentage-point rate increase [in the target for the federal funds rate] from the Fed when policy makers meet next month seem increasingly likely, while also strengthening the case that the Fed will keep raising rates well into next year. Stocks sold off sharply following the report’s release.”

Sources: U.S. Bureau of Labor Statistics, “Job Openings and Labor Turnover–July 2022,” bls.gov, August 30, 2022; Justin Lahart, “Why Stocks Got Jolted,” Wall Street Journal, August 30, 2022; Jerome H. Powell, “Monetary Policy and Price Stability,” speech at “Reassessing Constraints on the Economy and Policy,” an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, August 26, 2022; and Federal Reserve Bank of St. Louis.

Buying athletic shoes and reselling them for a higher price has become a popular way for some people to make money. The mostly young entrepreneurs involved in this business are often called sneakerheads. Note that economists call buying a product at a low price and reselling it at a high price arbitrage. The profits received from engaging in arbitrage are called arbitrage profits. One estimate puts the total value of sneakers being resold at $2 billion per year.

Why would anybody buy sneakers from a sneakerhead that they could buy at a lower price online or from a retail store? Most people wouldn’t, which is why most sneakerheads resell only shoes that shoe manufacturers like Nike or Adidas produce in limited quantities—typically fewer than 50,000 pairs. To obtain the shoes, shoe resellers use two main strategies: (1) waiting in line at retail stores on the day that a new limited quantity shoe will be introduced, or (2) buying shoes online using a software application called a bot. A bot speeds up a buyer’s checkout process for an online sale. Typical customers buying at an online shoe site take a few minutes to choose a size, fill in their addresses, and provide their credit card information. But a few minutes is enough time for shoe resellers using bots to buy all of the newly-released shoes available on the site.

In addition to reselling shoes on their own sites, many sneakerheads use dedicated resale sites like StockX and GOAT. These sites have greatly increased the liquidity of sneakers, or the ease with which sneakers can be resold. In effect, limited-edition sneakers have become an asset like stocks, bonds, or gold because they can be bought and sold in the secondary market that exists on the online resale sites. (We discuss the concepts of primary and secondary markets for assets in Macroeconomics, Chapter 6, Section 6.2 and in Microeconomics and Economics, Chapter 8, Section 8.2.)

An article in the New York Times gives an example of the problems that bots can cause for retail shoe stores. Bodega, a shoe store in Boston, offered the limited-edition New Balance 997S sneaker on its online site. Ten minutes later, the shoe was sold out. One of the store’s owner was quoted as saying: “We got destroyed by bots. It was making it impossible for our average customers to even have a shot at the shoes.” Although the store had a policy of allowing customers to buy a maximum of three pairs of shoes, shoe resellers were able to get around the policy by having shoes shipped to their friends’ addresses or by having a group of people coordinate their purchases. An article on bloomberg.com described how one reseller along with 15 of his friends used bots to buy 600 pairs of Adidas’s Yeezy sneakers from an online site on the morning the sneakers were released. Adidas has a rule that each customer can buy only one pair of its limited-edition shoes, but the company has trouble enforcing the rule.

Shopify and other firms have developed software that retailers can use to make it difficult for resellers to use bots on the retailers’ sites. But the developers of bot software have often been able to modify the bots to get around the defenses used by the anti-bot software.

In contrast with owners of retail stores, Nike, Adidas, New Balance, and the other shoe manufacturers have a more mixed reaction to sneakerheads using bots scooping up most pairs of limited-edition shoes shortly after the shoes are released. Like the owners of retail stores, the shoe manufacturers know that they risk upsetting the typical customer if the customer can only buy hot new shoe releases from resellers at prices well above the original retail price. But an active resale market increases the demand for shoes, just as individual investors increased their demand for individual stocks when it became possible to easily buy and sell stocks online using sites like TD Ameritrade, E*Trade, and Fidelity. So manufacturers benefit from knowing that most of their limited-edition shoes will sell out. One industry analyst singled out “The durability of Nike’s … ability to fuel the sneaker resale ecosystem ….” as a particular strength of the company. In addition, manufacturers may believe that the publicity about limited edition shoes rapidly selling out may spill over to increased demand for other shoes the manufacturers sell. (In Microeconomics and Economics, Chapter 10, Section 10.3 we note that some consumers may receive utility from buying goods that are widely seen as popular and fashionable.)

In the long run, is it possible for sneakerheads to make a profit reselling shoes? It seems unlikely for the reasons we discuss in Microeconomics and Economics, Chapter 12, Section 12.5. The barriers to entry in reselling sneakers are very low. Anyone can list shoes for sale on StockX or one of the other resale sites. Waiting in line in front of a retail store on the day a new shoe is released is something that anyone who is willing to accept the opportunity cost of the time lost can do. Similarly, bots that can be used to scoop up newly released shoes from online sites are widely available for sale. So, we would expect that in the long run entry into sneaker reselling will compete away any economic profit that sneakerheads were earning.

In fact, by the summer of 2022, prices on reselling sites were falling. In just the month of June, the average price of sneakers listed on StockX declined by 20 percent. Resellers who had stockpiled shoes waiting for prices to increase were instead selling them because they feared that prices would go even lower. And new limited-edition shoes were taking longer to sell out. According to an article in the Wall Street Journal, “A pair of Air Jordans released on July 13 [2022] that might have once vanished in minutes took days to sell out from Nike Inc.’s virtual shelves.” One reseller quoted in the Wall Street Journal article indicated that entry was the reason that prices were falling: “You don’t want prices to go down, but they’re going down anyways, just because of how many people are selling in general.”

Although a seemingly unusual market, sneaker reselling is subject to the same rules of competition that we see in other markets.

Sources: Inti Pacheco, “Flipping Air Jordans Is No Longer a Slam Dunk,” Wall Street Journal, July 23, 2022; Shoshy Ciment, “Sneaker Reselling Side Hustle: Your Guide to Making Thousands Flipping Hyped Pairs of Dunks, Jordans, and Yeezys,” businessinsider.com, May 3, 2022; Teresa Rivas, “A Strong Sneaker-Resale Market Is Another Boon for Nike,” barrons.com, May 24, 2022; Curtis Bunn, “Sneakers Are So Hot, Resellers Are Making a Living Off of Coveted Models,” nbcnews.com, October 23, 2021; Daisuke Wakabayashi, “The Fight for Sneakers,” New York Times, October 15, 2021; and Joshua Hunt, “Sneakerheads Have Turned Jordans and Yeezys Into a Bona Fide Asset Class,” bloomberg.com, February 15, 2021.

That’s what Elon Musk did in April 2022. In early April, Musk purchased about 9% of Twitter’s shares. On April 25, he became the owner of Twitter by buying the roughly 90% remaining shares for $54.20 per share. The total he paid for these remaining shares came to $44 billion. Following his often unorthodox style, Musk announced his plans in a tweet on Twitter. Where did he get the money to fund such a large purchase?

According to Forbes magazine, in March 2022, Musk was by far the richest person in the world with total wealth of about $270 billion—nearly $100 billion more than Amazon founder Jeff Bezos, who is the second-richest person. While it appears that Musk could afford to buy Twitter without having to borrow any money, Bloomberg estimated that in April 2022 Musk had only $3 billion in cash. Much of his wealth was in Tesla stock or his ownership shares in SpaceX and the Boring Company, both of which are private companies that, therefore, don’t have publicly traded stock. Musk was reluctant to fund all of his offer for Twitter by selling Tesla stock or finding investors willing to buy into SpaceX and Boring.

Musk turned to investment banks to help him raise the necessary funds. Investment banks, such as Goldman Sachs, differ from commercial banks in that they don’t accept deposits, and they rarely lend directly to households. Instead, investment banks have traditionally concentrated on providing advice to firms issuing stocks and bonds or to firms (and billionaires!) who are looking for ways to finance mergers or acquisitions. A syndicate of investment banks, including Morgan Stanley (which served as Musk’s lead adviser), Bank of America, Barclays, and what an article in the Wall Street Journal described as “nearly every global blue-chip investment bank aside from the two [Goldman Sachs and JP Morgan Chase] advising Twitter,” put together the following financing package. Initially, Musk wanted to raise $46.5 billion in financing—more than in the end he needed. Of that amount, Musk would provide $21 billion and the investment banks would provide loans for the remaining $25.5 billion. As collateral for the loans, Musk pledged $60 billion of his Tesla stock.

Musk’s financing was a combination of equity—the $21 billion in cash—and debt—the $25.5 billion in loans from investment banks. To fund his equity investment, he was considering selling some of his stock in Tesla but hoped to attract other equity investors who would put up cash in exchange for part ownership of Twitter. According to press reports, Apollo Global Management, a private equity firm was considering becoming an equity investor. (As we saw in Chapter 9, Section 9.2, private equity firms raise equity capital to invest in other firms.) Musk’s purchase is called a leveraged buyout (LBO) because (1) he relied on borrowing for a substantial part of his purchase of Twitter and (2) he intended to take the company private—the company would no longer have publicly traded stock.

Why would Musk want to buy Twitter? He shared the view of some industry analysts that Twitter’s management had failed to take advantage of opportunities to increase the firm’s profit. The actions of Musk and the investment banks were part of the market for corporate control. As we discuss in Microeconomics, Chapter 8, Section 8.1 (Macroeconomics, Chapter 6, Section 6.1), in large corporations there is often a separation of ownership from control. Although the shareholders legally own the firm, the firm’s top management controls the firm’s day-to-day operations. The result can be a principal-agent problem with the management of a large firm failing to act in the best interests of the firm’s shareholders. The existence of a market for corporate control in which outsiders buy stakes in firms that appear to be poorly managed can make firms more efficient by overcoming these moral hazard problems.

But Musk had another reason for buying Twitter. As he stated in an interview, “Having a public platform that is maximally trusted and broadly inclusive is extremely important to the future of civilization.” It was unclear whether this and similar statements meant that after gaining control of Twitter he might take actions that won’t necessarily increase the firm’s profitability.

Elon Musk’s purchase of Twitter is a high profile example of the role that investment banks can play in determining control of large corporations.

Sources: Kurt Wagner, “Elon Musk Lands Deal to Take Twitter Private for $44 Billion,” bloomberg.com, April 25, 2022; Cara Lombardo and Liz Hoffman, “How Elon Musk Won Twitter,” Wall Street Journal, April 25, 2022; Michele F. Davis, “Elon Musk Vets Potential Equity Partners for Twitter Bid,” bloomberg.com, April 21, 2022; Sabrina Escobar, “Elon Musk Isn’t Twitter’s Only Problem. It Faces a Number of Short-Term Headwinds,” barrons.com, April 21, 2022; Cara Lombardo and Liz Hoffman, “Elon Musk Says He Has $46.5 Billion in Funding for Twitter Bid,” Wall Street Journal, April 21, 2022; Andrew Ross Sorkin, Jason Karaian, Vivian Giang, Stephen Gandel, Lauren Hirsch, Ephrat Livni, and Anna Schaverien, “Elon Musk Wants All of Twitter,” New York Times, April 14, 2022; Rob Copeland, Rebecca Elliott, and Cara Lombardo, “Elon Musk Makes $43 Billion Bid for Twitter, Says ‘Civilization’ At Stake,” Wall Street Journal, April 14, 2022; “The World’s Real-Time Billionaires,” forbes.com, April 24, 2022; Musk’s tweet announcing his offer to buy Twitter can be found here.