At the close of stock trading on Friday, January 24 at 4 pm EST, Nvidia’s stock had a price of $142.62 per share. When trading reopened at 9:30 am on Monday, January 27, Nvidia’s stock price plunged to $127.51. The total value of all Nvidia’s stock (the firm’s market capitalization or market cap) dropped by $589 billion—the largest one day drop in market cap in history. The following figure from the Wall Street Journal shows movements in Nvidia’s stock price over the past six months.

What happened to cause should a dramatic decline in Nvidia’s stock price? As we discuss in Macroeconomics, Chapter 6 (Economics, Chapter 8, and Money, Banking, and the Financial System, Chapter 6), Nividia’s price of $142.62 at the close of trading on January 24—like the price of any publicly traded stock—reflected all the information available to investors about the company. For the company’s stock to have declined so sharply at the beginning of the next trading day, important new information must have become available—which is exactly what happened.

As we discussed in this blog post from last October, Nvidia has been very successful in producing state-of-the-art computer chips that power the most advanced generative artificial intelligence (AI) software. Even after Monday’s plunge in the value of its stock, Nvidia still had a market cap of nearly $3.5 trillion at the end of the day. It wasn’t news that DeepSeek, a Chinese AI company had produced AI software called R1 that was similar to ChatGTP and other AI software produced by U.S. companies. The news was that R1—the latest version of the software is called V3—appeared to be comparable in many ways to the AI software produced by U.S. firms, but had been produced by DeepSeek despite not using the state-of-the-art Nvidia chips used in those AI programs.

The Biden administration had barred export to China of the newest Navidia chips to keep Chinese firms from surging ahead of U.S. firms in developing AI. DeepSeek claimed to have developed its software using less advanced chips and have trained its software at a much lower cost than U.S. firms have been incurring to train their software. (“Training” refers to the process by which engineers teach software to be able to accurately solve problems and answer questions.) Because DeepSeek’s costs are lower, the company charges less than U.S. AI firms do to use its computer infrastructure to handle business tasks like responding to consumer inquiries.

If the claims regarding DeepSeek’s software are accurate, then AI firms may no longer require the latest Nvidia chips and may be forced to reduce the prices they can charge firms for licensing their software. The demand for electricity generation may also decline if it turns out that the demand for AI data centers, which use very large amounts of power, will be lower than expected.

But on Monday it wasn’t yet clear whether the claims being made about DeepSeek’s software were accurate. Some industry observers speculated that, despite the U.S. prohibition on exporting the latest Nvidia chips to China, DeepSeek had managed to obtain them but was reluctant to admit that it had. There were also questions about whether DeepSeek had actually spent as little as it claimed in training its software.

What happens to the price of Nvidia’s stock during the rest of the week will indicate how investors are evaluating the claims DeepSeek made about its AI software.

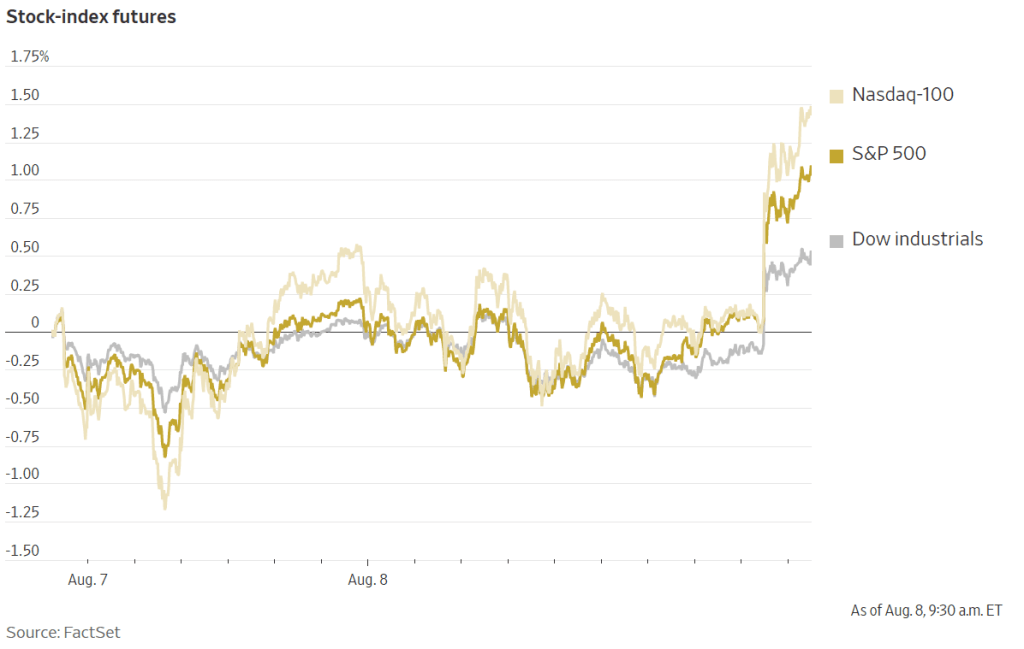

Over the first past few days, the stock and bond markets have gone through substantial swings as investors try to determine whether the U.S. economy is likely to move into a recession soon. (We discussed here the most recent BLS “Employment Situation” report, which was surprisingly weak.)

It’s difficult to determine with certainty why on a particular day stock and bond prices fluctuate. The following two figures from the Wall Street Journal show movements this morning (August 8) in stock prices and bond yields. (Recall that bond yields rise when bond prices fall, a point we discuss in the Appendix to Chapter 6 of Macroeconomics (Chapter 8 of Economics).)

Rising stock prices and falling bond prices (rising bond yields) can be an indication that investors are more optimistic that the U.S. economy will avoid a recession. In a recession, profits decline, which is bad for stock prices. And in a recession, interest rates typically fall both because the Federal Reserve cuts it target range for the federal funds rate and because household and firms borrow less, which reduces the demand for loanable funds. Accordingly, most analysts are attributing the movements in stock and bond prices this morning to investors becoming more optimistic that the U.S. economy will avoid a recession.

Because of the level of uncertainty about the future path of the economy, investors are following very closely the release of new macroeconomic data. The Wall Street Journal and other business publications attributed the increase in investor optimism this morning to the U.S. Employment and Training Administration releasing at 8:30 a.m. its latest report on initial claims for unemployment insurance. The headline in the Wall Street Journal was: “Stocks Rise on Claims Data.” Similalry, the headline on bloomberg.com was: “Stocks Get Relief Rally after Jobless Claims Data.”

What are jobless claims? The first step when you lose a job and wish to receive government unemployment insurance payments is to file a claim, which starts the process by which an agency of the state government determines whether you are eligible to receive unemployment insurance payments.

The data on initial jobless claims are released weekly. As the following figure shows, there is a lot of volatility in this data series. The latest data were favorable—which is thought to have caused the increase in stock prices and decline in bond prices—because new claims declined by 17,000 this week. But the series is so volatile that drawing conclusions from weekly changes seems unwarranted. For instance, the figure shows that weekly claims surged during the summer of 2023, although employment and production continued to expand during that period.

So it appears that people trading in stock and bond markets this morning are overreacting to this macrodata release. But explanations of why stock and bonds prices move as they do over a short period of time often turnout in hindsight to have been incorrect. It may well be the case that investors are acting as they are this morning for reasons that are, in fact, unrelated to the data on jobless claims.

Agents from the National Transportation Safety Board inspect a piece of the Boeing jetliner found in a backyard in Portland, Oregon. (Photo from the AP via the New York Times.)

What causes movements in stock prices? As we explain in Economics and Microeconomics, Chapter 8, Section 8.2 (Macroeconomics, Essentials of Economics, and Money, Banking, and the Financial System, Chapter 6, Section 6.2): “Shares of stock represent claims on the profits of the firms that issue them. As the fortunes of the firms change and they earn more or less profit, the prices of the stock the firms have issued should also change.”

We also note that: “Many Wall Street investment professionals expend a great deal of effort gathering all possible information about the future profitability of firms, hoping to buy the stocks that are most likely to rise in the future. As a result of the actions of these professional investors, all of the information about a firm that is available on news and financial websites, cable TV business shows, and online discussion sites like X and Reddit is already reflected in the firm’s stock price.” As a consequence, the price of a firm’s stock will change only as a result of new information about the future profitability of the firm issuing the stock.

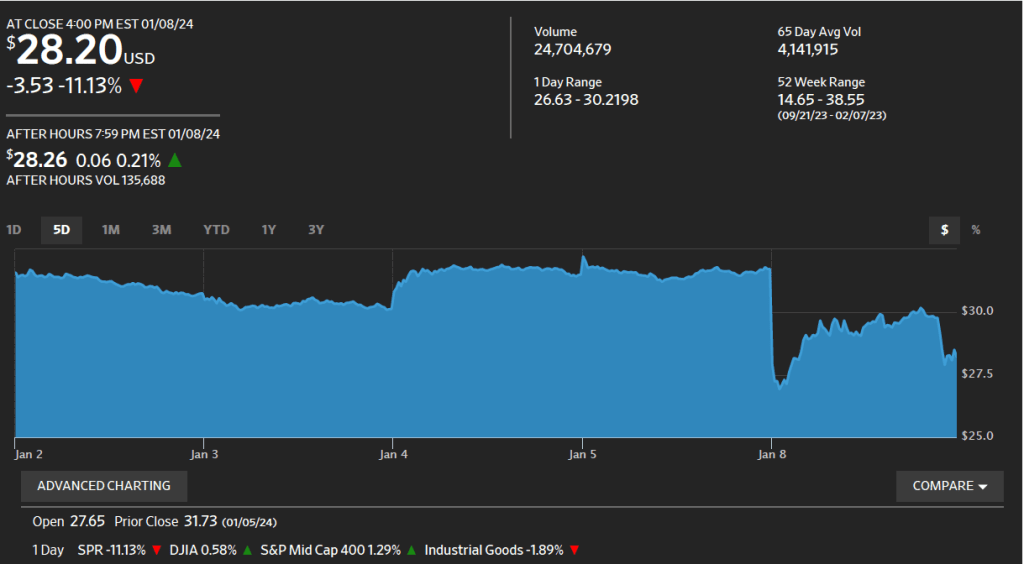

During the course of a typical week, the new information that becomes available about a large company, like Apple or General Motors, is likely to indicate only minor changes in the future profitability of the firm. Therefore, we wouldn’t expect that the firm’s stock price would change very much. Sometimes, though, investors receive important new information that causes them to significantly revise their expectations of the future profitability of a firm. That’s what happened to Boeing, the jetliner manufacturer, on Friday, January 5. An Alaska Air Boeing 737 Max 9 was taking off from Portland International Airport when a piece of the plane blew out. (A Wall Street Journalarticle gives the details of the incident.)

The accident caused some industry observers to question whether Boeing’s quality control during manufacturing had deficiencies that might lead to other problems being discovered on the firm’s jetliners. Boeing was particularly at risk of having its quality control methods questioned because in 2019 two slightly different models of the 737 Max airliner had crashed, causing the planes to be grounded for almost two years.

The effect of the Alaska Air incident on Boeing’s stock price can be seen in the following figure, reproduced from the Wall Street Journal. On Friday, January 5 at 4 pm eastern time—the time at which trading on the New York Stock Exchange (NYSE) closes for the day—the price of Boeing’s stock was $249.00 per share. The accident took place at around 7:40 pm eastern time, so it occurred after the close of trading on the NYSE. When trading on the NYSE resumed at 9:30 am on Monday, January 8, Boeing’s stock price had declined to $227.79 per share. The size of the drop in price indicated that investors believed that the Portland accident would have a significantly negative affect on Boeing’s future profitability. Boeing’s profits could fall if the accident leads airlines to reduce their future purchases of 737 Max airliners or if Boeing’s costs rise significantly as a result of making repairs on Max airliners currently in servide or as a result of having to spend more on quality control measures when manufacturing the planes.

The effect of the Portland accident on Boeing’s stock price is an example of the efficiency of the stock market in processing information about a firm’s future profitability.

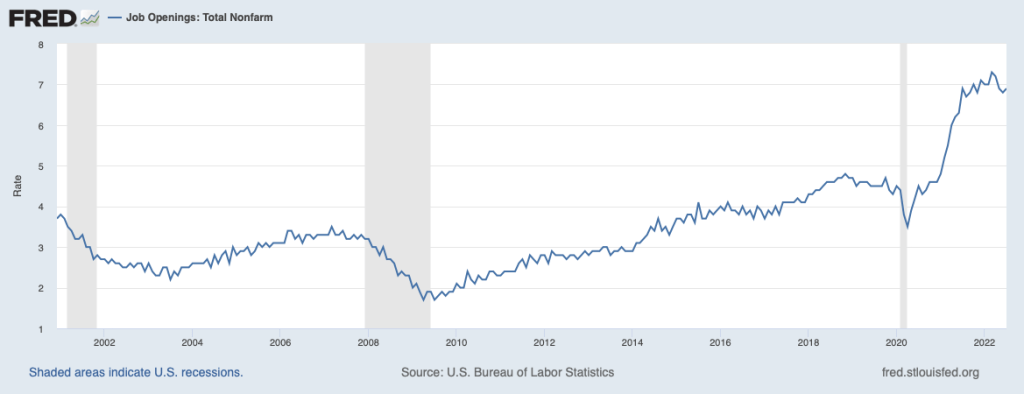

On Tuesday, August 30, 2022, the U.S. Bureau of Labor Statistics (BLS) released its Job Openings and Labor Turnover Survey (JOLTS) report for July 2022. The report indicated that the U.S. labor market remained very strong, even though, according to the Bureau of Economic Analysis (BEA), real gross domestic product (GDP) had declined during the first half of 2022. (In this blog post, we discuss the possibility that during this period the real GDP data may have been a misleading indicator of the actual state of the economy.)

As the following figure shows, the rate of job openings remained very high, even in comparison with the strong labor market of 2019 and early 2020 before the Covid-19 pandemic began disrupting the U.S. economy. The BLS defines a job opening as a full-time or part-time job that a firm is advertising and that will start within 30 days. The rate of job openings is the number of job openings divided by the number of job openings plus the number of employed workers, multiplied by 100.

In the following figure, we compare the total number of job openings to the total number of people unemployed. The figure shows that in July 2022 there were almost two jobs available for each person who was unemployed.

Typically, a strong job market with high rates of job openings indicates that firms are expanding and that they expect their profits to be increasing. As we discuss in Macroeconomics, Chapter 6, Section 6.2 (Microeconomics and Economics, Chapter 8, Section 8.2) the price of a stock is determined by investors’ expectations of the future profitability of the firm issuing the stock. So, we might have expected that on the day the BLS released the July JOLTS report containing good news about the labor market, the stock market indexes like the Dow Jones Industrial Average, the S&P 500, and the Nasdaq Composite Index would rise. In fact, though the indexes fell, with the Dow Jones Industrial Average declining a substantial 300 points. As a column in the Wall Street Journal put it: “A surprisingly tight U.S. labor market is rotten news for stock investors.” Why did good news about the labor market could cause stock prices to decline? The answer is found in investors’ expectations of the effect the news would have on monetary policy.

In August 2022, Fed Chair Jerome Powell and the other members of the Federal Reserve Open Market Committee (FOMC) were in the process of tightening monetary policy to reduce the very high inflation rates the U.S. economy was experiencing. In July 2022, inflation as measured by the percentage change in the consumer price index (CPI) was 8.5 percent. Inflation as measured by the percentage change in the personal consumption expenditures (PCE) price index—which is the measure of inflation that the Fed uses when evaluating whether it is hitting its target of 2 percent annual inflation—was 6.3 percent. (For a discussion of the Fed’s choice of inflation measure, see the Apply the Concept “Should the Fed Worry about the Prices of Food and Gasoline,” in Macroeconomics, chapter 15, Section 15.5 and in Economics, Chapter 25, Section 25.5.)

To slow inflation, the FOMC was increasing its target for the federal funds rate—the interest rate that banks charge each other on overnight loans—which in turn was leading to increases in other interest rates, such as the interest rate on residential mortgage loans. Higher interest rates would slow increases in aggregate demand, thereby slowing price increases. How high would the FOMC increase its target for the federal funds rate? Fed Chair Powell had made clear that the FOMC would monitor economic data for indications that economic activity was slowing. Members of the FOMC were concerned that unless the inflation rate was brought down quickly, the U.S. economy might enter a wage-price spiral in which high inflation rates would lead workers to push for higher wages, which, in turn, would increase firms’ labor costs, leading them to raise prices further, in response to which workers would push for even higher wages, and so on. (We discuss the concept of a wage-price spiral in this earlier blog post.)

In this context, investors interpretated data showing unexpected strength in the economy—particularly in the labor market—as making it likely that the FOMC would need to make larger increases in its target for the federal fund rate. The higher interest rates go, the more likely that the U.S. economy will enter an economic recession. During recessions, as production, income, and employment decline, firms typically experience lower profits or even suffer losses. So, a good JOLTS report could send stock prices falling because news that the labor market was stronger than expected increased the likelihood that the FOMC’s actions would push the economy into a recession, reducing profits. Or as the Wall Street Journal column quoted earlier put it:

“So Tuesday’s [JOLTS] report was good news for workers, but not such good news for stock investors. It made another 0.75-percentage-point rate increase [in the target for the federal funds rate] from the Fed when policy makers meet next month seem increasingly likely, while also strengthening the case that the Fed will keep raising rates well into next year. Stocks sold off sharply following the report’s release.”

Sources: U.S. Bureau of Labor Statistics, “Job Openings and Labor Turnover–July 2022,” bls.gov, August 30, 2022; Justin Lahart, “Why Stocks Got Jolted,” Wall Street Journal, August 30, 2022; Jerome H. Powell, “Monetary Policy and Price Stability,” speech at “Reassessing Constraints on the Economy and Policy,” an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, August 26, 2022; and Federal Reserve Bank of St. Louis.

Jerome Powell (photo from the Wall Street Journal)

Most economists believe that monetary policy actions, such as changes in the Fed’s pace of buying bonds or in its target for the federal funds rate, affect real GDP and employment only with a lag of several months or longer. But monetary policy actions can have a more immediate effect on the prices of financial assets like stocks and bonds.

Investors in financial markets are forward looking because the prices of financial assets are determined by investors’ expectations of the future. (We discuss this point in Economics and Microeconomics, Chapter 8, Section 8.2, Macroeconomics, Chapter 6, Section 6.2, and Money, Banking and the Financial System, Chapter 6.) For instance, stock prices depend on the future profitability of firms, so if investors come to believe that future economic growth is likely to be slower, thereby reducing firms’ profits, the investors will sell stocks causing stock prices to decline.

Similarly, holders of existing bonds will suffer losses if the interest rates on newly issued bonds are higher than the interest rates on existing bonds. Therefore, if investors come to believe that future interest rates are likely to be higher than they had previously expected them to be, they will sell bonds, thereby causing their prices to decline and the interest rates on them to rise. (Recall that the prices of bonds and the interest rates (or yields) on them move in opposite directions: If the price of a bond falls, the interest rate on the bond will increase; if the price of a bond rises, the interest rate on the bond will decrease. To review this concept, see the Appendix to Economics and Microeconomics Chapter 8, the Appendix to Macroeconomics Chapter 6, and Money, Banking, and the Financial System, Chapter 3.)

Because monetary policy actions can affect future interest rates and future levels of real GDP, investors are alert for any new information that would throw light on the Fed’s intentions. When new information appears, the result can be a rapid change in the prices of financial assets. We saw this outcome on January 5, 2022, when the Fed released the minutes of the Federal Open Market Committee meeting held on December 14 and 15, 2021. At the conclusion of the meeting, the FOMC announced that it would be reducing its purchases of long-term Treasury bonds and mortgage-backed securities. These purchases are intended to aid the expansion of real GDP and employment by keeping long-term interest rates from rising. The FOMC also announced that it intended to increase its target for the federal funds rate when “labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment.”

When the minutes of this FOMC meeting were released at 2 pm on January 5, 2022, many investors realized that the Fed might increase its target for the federal funds rate in March 2022—earlier than most had expected. In this sense, the release of the FOMC minutes represented new information about future Fed policy and the markets quickly reacted. Selling of stocks caused the S&P 500 to decline by nearly 100 points (or about 2 percent) and the Nasdaq to decline by more than 500 points (or more than 3 percent). Similarly, the price of Treasury securities fell and, therefore, their interest rates rose.

Investors had concluded from the FOMC minutes that economic growth was likely to be slower during 2022 and interest rates were likely to be higher than they had previously expected. This change in investors’ expectations was quickly reflected in falling prices of stocks and bonds.

Sources: An Associated Press article on the reaction to the release of the FOMC minutes can be found HERE; the FOMC’s statement following its December 2021 meeting can be found HERE; and the minutes of the FOMC meeting can be found HERE.

In 2021, SPACs were the hottest trend on the stock market and had become the leading way for companies to go public. A public company is one with shares that trade on the stock market. Private firms make up more than 95 percent of all firms in the United States. Most will never become public firms because they will never grow large enough for investors to have sufficient information on the firms’ financial health to be willing to buy the firms’ stocks and bonds.

But some firms, particularly technology firms, grow rapidly enough that they are able to become public firms. Apple, Microsoft, Google, Uber, Facebook, Snap, and other firms have followed this path. When these firms went public, they did so using an initial public offering (IPO). (We briefly discuss IPOs in Economics and Microeconomics, Chapter 8, Section 8.2 and in Macroeconomics, Chapter 6, Section 6.2.) With an IPO, a firm uses one or more investment banks to underwrite the firm’s sales of new stocks or bonds to the public. In underwriting,investment banks typically guarantee a price for stocks or bonds to the issuing firm, sell the stocks or bonds in financial markets or directly to investors at a higher price, and keep the difference, known as the spread.

Beginning in 2020 and continuing through 2021, an increasing number of firms have used a different means of going public—merging with a SPAC. SPAC stands for special-purpose acquisition company and is a firm that holds only cash—it doesn’t sell a good or service—and only has the purpose of merging with another firm that wants to go public. Once a merger takes place, the acquired firm takes the place of the SPAC in the stock market. For instance, a SPAC named Diamond Eagle Acquisition merged with online sports betting site DraftKings in April 2020. Once the merger had been completed, DraftKings took Diamond Eagle’s place on the stock market, trading under the stock symbol DKNG. By 2021, the value of SPAC mergers had risen to being three times as much as the value of IPOs.

Some firms intending to go public prefer SPACs to traditional IPOs because they can bargain directly with the managers of the SPAC in determining the value of the firm. In addition, IPOs are closely regulated by the federal government’s Securities and Exchange Commission (SEC). In particular, the SEC monitors whether an investment bank is accurately stating the financial prospects of a firm whose IPO the bank is underwriting. The claims that SPACs make when attracting investors are less closely monitored. SPAC mergers can also be finalized more quickly than can traditional IPOs.

The experience of WeWork illustrates how some firms that have struggled to go public through an IPO have been able to do so by merging with a SPAC. Adam Neumann and Miguel McLevey founded WeWork in 2010 as a firm that would rent office space in cities, renovate the space, and then sub-lease it to other firms. In 2019, the firm prepared for an IPO that would have given the firm a total value of more than $40 billion. But doubts about the firm’s business model led to an indefinite postponement of the IPO and Neumann was forced out as CEO.

WeWork was reorganized under new CEO Sandeep Mathrani and went public in October 2021 by merging with BowX Acquisition Corporation, a SPAC. Although WeWork’s stock began trading (under stock symbol WE) at a price that put the firm’s value at about $9 billion—far below the value it expected at the time of its postponed IPO two years before—investors seemed optimistic about the firm’s future because its stock price rose sharply during the first two days it traded on the stock market.

Some policymakers are concerned that individual investors may not have sufficient information on firms that go public through a merger with a SPAC. Under one proposal being considered by Congress, financial advisers would only be allowed to recommend investing in SPACs to wealthy investors. The SEC is also considering whether new regulations governing SPACS were needed. Testifying before Congress, SEC Chair Gary Gensler sated: “There’s real questions about who’s benefiting [from firms going public using SPACs] and [about] investor protection.”

It remains to be seen whether SPACs will retain their current position as being the leading way for firms to go public.

Sources: Dave Sebastian, “WeWork Shares Rise on First Day of Trading, Two Years After Failed IPO,” wsj.com, October 21, 2021; Peter Santilli and Amrith Ramkumar, “SPACs Are the Stock Market’s Hottest Trend. Here’s How They Work,” wsj.com, March 29, 2021; Benjamin Bain, “SPAC Marketing Heavily Curtailed in House Democrats’ Draft Bill,” bloomberg.com, October 4, 2021; and Dave Michaels, “SEC Weighs New Investor Protections for SPACs,” wsj.com, May 26, 2021.

Supports: Hubbard/O’Brien, Chapter 8, Firms, the Stock Market, and Corporate Governance; Macroeconomics Chapter 6; Essentials of Economics Chapter 6; Money, Banking, and the Financial System, Chapter 6.

We’ve seen that a firm’s stock price should represent the best estimates of investors as to how profitable the firm will be in the future. How, then, can we explain the following graph of the price of shares of GameStop, the retail chain that primarily sells video game cartridges and video game systems? The graph shows the price of the stock from December 1, 2020 through February 9, 2021. If the main reason the price of a stock changes is that investors have become more or less optimistic about the profitability of the firm, is it plausible that opinions on GameStop’s profitability changed so much in such a short period of time?.

Sometimes investors do abruptly change their minds about the profitability of a firm but typically this happens when the firm’s profitability is heavily dependent on the success of a single product. For instance, the price of the stock a biotech firm might soar as investors believe that a new drug therapy the firm is developing will succeed and then the price of the stock might crash when the drug is unable to gain regulatory approval. But it wasn’t news about its business that was driving the price of GameStop’s stock from $15 per share during December 2020 to a high of $347 per share on January 27, 2021 and then down to $49 per share on February 9.

To understand these prices swings, first we need to take into account that not all people buying stock do so because they are making long-term investments to accumulate funds to purchase a house, pay for their children’s educations, or for their retirement. Some people who buy stock are speculators who hope to profit by buying and selling stock during a short period—perhaps as short as a few minutes or less. The availability of online stock trading apps, such as Robinhood, that don’t charge commissions for buying and selling stock, and online stock discussion groups on sites like Reddit, have made it easier for some individual investors to become day traders, frequently buying and selling stocks in the hopes of making a short-term profit.

Many day traders engage in momentum investing, which means they buy stocks that have increasing prices and sell stocks that have falling prices, ignoring other aspects of the firm’s situation, including the firm’s likely future profitability. Momentum investing is an example of what economists call noise trading, or buying and selling stocks on the basis of factors not directly related to a firm’s profitability. Noise trading can result in a bubble in a firm’s stock, which means that the price rises above the fundamental value of the stock as indicated by the firm’s profitability. Once a bubble begins, a speculator may buy a stock to resell it quickly for a profit, even if the speculator knows that the price is greater than the stock’s fundamental value. Some economists explain a bubble in the price of a stock by the greater fool theory: An investor is not a fool to buy an overvalued stock as long as there’s a greater fool willing to buy it later for a still higher price.

Although the factors mentioned played a role in explaining the volatility in GameStop’s stock price, there was another important factor that involved hedge funds and short selling. Hedge funds are similar to mutual funds in that they use money from savers to make investments. But unlike mutual funds, by federal regulation only wealthy individuals or institutional investors such as pension funds or university endowment funds are allowed to invest in hedge funds. Hedge funds frequently engage in short selling, which means that when they identify a firm whose stock they consider to be overvalued, they borrow shares of the firm’s stock from a broker or dealer and sell them in the stock market, planning to make a profit by buying the shares back after their prices have fallen.

In early 2021, several large hedge funds were shorting GameStop’s stock believing that the market for video game cassettes would continue to decline as more gamers switched to downloading games. Some people in online forums—notably the WallStreetBets forum on Reddit—dedicated to discussing investing strategies argued that if enough day traders bought GameStop’s stock they could make money through a short squeeze. A short squeeze happens when a heavily shorted stock increases in price. The speculators who shorted the stock may then have to buy back the stock to avoid large losses or having to pay very high fees to dealers who had loaned them the shares they were shorting. As the short sellers buy stock, the price of the stock is bid up further, earning a profit for day traders who had bought the stock in anticipation of the short squeeze. One MIT graduate student made a profit of more than $200,000 on a $500 investment in GameStop stock. Some hedge funds that had been shorting GameStop lost billions of dollars.

Some of the day traders involved saw this episode as one of David defeating Goliath because the people executing the short squeeze were primarily young with moderate incomes whereas the people running the hedge funds taking substantial losses in the short squeeze were older with high incomes. The reality was more complex because as the price of GameStop stock declined from $347 on to $54 on February 4, some day traders who bought the stock after its price had already substantially risen lost money. And all the winners from the short squeeze weren’t day traders; some were hedge funds. For instance, by early February, the hedge fund Senvest Management had earned $700 million from its trading in GameStop’s stock.

Economists had differing opinions about whether the GameStop episode had a wider significance for understanding how the stock market works or for how it was likely to work in the future. Some economists and investment professionals argued that what happened with GameStop’s stock price was not very different from previous episodes in which speculators buying and selling a stock will for a time cause increased volatility in the stock’s price. In the long run, they believe that stock prices return to their fundamental values. Other economists and investors thought that the increased number of day traders combined with the availability of no-commission stock buying and selling meant that stock prices might be entering a new period of increased volatility. They noted that similar, if less spectacular, price swings had happened at the same time in other stocks such as AMC, the movie theater chain, and Express, the clothing store chain. An article on bloomberg.com quoted one analyst as saying, “We’ve made gambling on the stock market cheaper than gambling on sports and gambling in Vegas.”

Federal regulators, including Treasury Secretary Janet Yellen, were evaluating what had happened and whether they needed to revise existing government regulations of financial markets.

Sources: Misyrlena Egkolfopoulou and Sarah Ponczek, “Robinhood Crisis Reveals Hidden Costs in Zero-Fee Trading Model,” bloomberg.com, February 3, 2021; Gunjan Banerji, Juliet Chung, and Caitlin McCabe, “GameStop Mania Reveals Power Shift on Wall Street—and the Pros Are Reeling,”Wall Street Journal, January 27, 2021; Gregory Zuckerman, “For One GameStop Trader, the Wild Ride Was Almost as Good as the Enormous Payoff,” Wall Street Journal, February 3, 2021; Juliet Chung, “Wall Street Hedge Funds Stung by Market Turmoil,” Wall Street Journal, January 28, 2021; and Juliet Chung, “This Hedge Fund Made $700 Million on GameStop,” Wall Street Journal, February 3, 2021.

Questions

During the same week that the price of GameStop’s stock was soaring to a record high, an article in the Wall Street Journal noted the following: “Analysts expect GameStop to post its fourth consecutive annual decline in revenue in its latest fiscal year amid declines in its core operations [of selling video game cartridges and video game consoles in retail stores].” Don’t stock prices reflect the expected profitability of the firms that issue the stock? If so, why in January 2021 was the price of GameStop’s stock greatly increasing when it seemed unlikely that the firm would become more profitable in the future?

Source: Sarah E. Needleman, “GameStop and AMC’s Stocks Are on a Tear, but Their Businesses Aren’t,” Wall Street Journal, January 31, 2021

2. In early 2021, as the stock price of GameStop was soaring, a columnist in the New York Times advised that: “A better option [than buying stock in GameStop] would be salting away money in dull, well-diversified stock and bond portfolios, these days preferably in low-cost index funds.”

a. What does the columnist mean by “salting money away”?

b. are index funds and why might they be considered dull when compared to investing in an individual stock like GameStop?

c. Why would the columnist consider investing in an index mutual fund to be a better option than investing money in an individual stock like GameStop?

Source: Jeff Sommer, “How to Keep Your Cool in the GameStop Market,” New York Times, January 29, 2021.

Instructors can access the answers to these questions by emailing Pearson at christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.

Apply the Concept: If the Economy Is Down, Why Is the Stock Market Up?

Here’s the Key Point: In determining a firm’s stock price, the firm’s current profitability is less important than its expected future profitability.

The price of a share of stock reflects the profitability of the firm that issued it. During economic recessions, firms experience declining sales and profits and the prices of their stocks fall. We saw such a decline at the beginning of the downturn caused by the Covid-19 pandemic in 2020. As the following figure shows, the S&P 500 stock market price index reached a high the week ending on February 14. By the week ending on March 20, this index had declined by 29 percent.

On the figure, the shaded area shows the weeks during this period when the economy was in a recession. We are dating the beginning of the recession using the Weekly Economic Index published by the New York Federal Reserve and compiled by James Stock of Harvard, Daniel Lewis of the New York Federal Reserve, and Karel Mertens of the Dallas Federal Reserve. The index is comprised of 10 economic variables including sales in retail stores, claims by laid off workers for government unemployment insurance payments, steel production, and railroad freight traffic.

Notice two things about the figure:

Stock prices began to fall in mid-February 2020, about a month before the recession began in mid-March. This result is not surprising because the stock market is often a leading indicator, that is, stock prices tend to decline before production and employment fall. The incomes of professional stock traders and managers of mutual funds and exchange-traded funds (ETFs) depend in part on their ability to sell stocks before their prices decline and buy them before their prices increase. So these finance professionals have a strong incentive to attempt to anticipate changes in the economy before they occur.

Stock prices began to rise in mid-March while the economy was still in recession. In fact, the S&P 500 stock index increased more than 20 percent between mid-March and early May even though, as measured by the WEI, the economic recession was becoming worse as production and employment were rapidly declining. This result surprised many people who had trouble understanding how, as the headline of an article in the New York Times put it: “The Bad News Won’t Stop, but Markets Keep Rising.”

Both these points reflect the same key fact about the stock market: Although a firm’s stock price depends on the firm’s profitability, the firm’s current profitability is less important than its expected future profitability. You wouldn’t pay much for the stock of a firm that was making a profit today but that you expect will be driven out of business in the future by another firm about to introduce a superior competing product. Even though the profitability of most firms in the United States had yet to decline in mid-February, many investors were beginning to fear that Covid-19 would have a major effect on the U.S. economy, so stock prices began to decline.

Why then did stock prices turnaround and begin to rise only a month later, and why did they rise and fall significantly on many days? Those swings in stock prices reflected a key result of investors interacting in financial markets: Buying and selling of financial assets like stocks results in the prices of those assets fully reflecting all the available information relevant to the value of the assets. In the case of the stock market, buying and selling stock results in stock prices reflecting all available information on the future profitability of the firms issuing the stock. New information that is favorable to the future profitability of a firm—for instance, Apple announces that iPhone sales have been higher than investors expected—will lead investors to increase demand for the firm’s stock, raising its price. The opposite happens when new information becomes available that is unfavorable to the future profitability of a firm.

Because new information becomes available continually, we would expect stock prices to change day-to-day, hour-to-hour, and minute-to-minute. Stock prices for the market as a whole, as reflected in stock price indexes like the S&P 500, will rise and fall as new information becomes available on the future strength of the economy. During the Covid-19 pandemic, investors were particularly concerned with the following four issues:

The development of new medical treatments for the disease, particularly vaccines.

The effectiveness of government programs, such as loans to businesses, that were intended to help the economy recover from the effects of the lockdowns used to reduce the spread of the virus.

The ability of the economy to adjust to the possibility that the virus might persist in some form for years.

The willingness of consumers to resume buying goods and services, such as restaurant meals and movie tickets, that seemed particularly affected by the virus.

Optimistic news about these factors, such as successful early trials of a vaccine for use against Covid-19, caused sharp increases in stock prices and pessimistic news caused prices to fall. For example, here are the percentage changes in the S&P 500 stock price index for consecutive trading days in mid-March (the stock market is closed on Saturdays and Sundays):

Stock prices are rarely this volatile. Wall Street investment professionals spend a great deal of effort gathering all possible information about the future profitability of firms, but in this period they had difficulty interpreting the importance of new information. No investor had experienced a pandemic as severe as Covid-19, so it was particularly challenging for them to determine the implications of new information for the likely future strength of the economy and, therefore, to the profitability of firms.

The large fluctuations in stock prices were another indication of how unusual an event the Covid-19 pandemic was and the difficulty that investors had in understanding its likely long-run effects on the U.S. economy.

Sources: Matt Phillips, “The Bad News Won’t Stop, but Markets Keep Rising,” New York Times, April 29, 2020; and Federal Reserve Bank of St. Louis.

Question:

In May 2020, an article in New York Magazine noted that, “The stock market zoomed on Monday in response to very preliminary positive news about a vaccine” being tested by the pharmaceutical firm Moderna. Positive news about one of its products might be expected to increase Moderna’s future profits and the price of its stock, but why would prices of many other stocks increase on this news?

For Economics Instructors that would like the approved answers to the above questions, please email Christopher DeJohn from Pearson at christopher.dejohn@pearson.com and list your Institution and Course Number.