The Bureau of Labor Statistics is housed in the U.S. Department of Labor. (Photo from don.gov site.)

In a blog post at the end of August, we noted that real GDP declined during the first two quarters of 2022. On September 29, the Bureau of Economic Analysis (BEA) slightly revised the real GDP data, but after the revisions the BEA’s estimates still showed real GDP declining during those quarters.

A popular definition of a recession is two consecutive quarters of declining real GDP. But, as we noted in the earlier blog post, most economists do not follow this definition. Instead, for most purposes, economists rely on the National Bureau of Economic Research’s business cycle dating, which is based on a number of macroeconomic data series. The NBER defines a recession as “a significant decline in activity spread across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.” The NBER discusses its approach to business cycle dating here.

The Federal Reserve Bank of St. Louis’s invaluable FRED economic data site has collected the data series that the NBER’s Business Cycle Dating Committee relies on when deciding when a recession began. The FRED page collecting these data can be found here.

Note that although the Business Cycle Dating Committee analyzes a variety of data series, “In recent decades, the two measures we have put the most weight on are real personal income less transfers and nonfarm payroll employment.” The following figures show movements in those two data series. These data series don’t give a strong indication that the economy was in recession during the first half of 2022. Real personal income minus transfer payments did decline by 0.4 percent between January and June 2022 (before increasing during July and August), but nonfarm payroll employment increased by 1.4 percent during the same period (and increased further in July and August).

As we noted in our earlier blog post, the message from most data series other than real GDP seems to be that the U.S. economy was not in a recession during the first half of 2022.

The Bureau of Economic Analysis (BEA) publishes data on gross domestic product (GDP) each quarter. Economists and media reports typically focus on changes in real GDP as the best measure of the overall state of the U.S. economy. But, as we discuss in Macroeconomics, Chapter 8, Section 8.4 (Economics, Chapter 18, Section 18.4), the BEA also publishes quarterly data on gross domestic income (GDI). As we discuss in Chapter 8, Section 8.1 when discussing the circular-flow diagram, the value of every final good and services produced in the economy (GDP) should equal the value of all the income in the economy resulting from that production (GDI). The BEA has designed the two measures to be identical by including in GDI some non-income items, such as sales taxes and depreciation. But as we discuss in the Apply the Concept, “Should We Pay More Attention to Gross Domestic Income?” GDP and GDI are compiled by the BEA from different data sources and can sometimes significantly diverge.

A large divergence between the two measures occurred in the first half of 2022. During this period real GDP declined—as shown by the blue line in the following figure—after which some stories in the media indicated that the U.S. economy was in a recession. But real GDI—as shown by the red line in the figure—increased during the same two quarters. So, was the U.S. economy still in the expansion that began in the third quarter of 2020, rather than in a recession? Or, as an article in the Wall Street Journal put it: “A Different Take on the U.S. Economy: Maybe It Isn’t Really Shrinking.”

In fact, most economists do not follow the popular definition of a recession as being two consecutive quarters of declining real GDP. Instead, as we discuss in Chapter 10, Section 10.3, economists typically follow the definition of a recession used by the National Bureau of Economic Research: “A recession is a significant decline in activity spread across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.”

During the first half of 2022, most measures of economic activity were expanding, rather than contracting. For example, the first of the following figures shows payroll employment increasing in each month in the first half of 2022. The second figure shows industrial production also increasing during most months in the first half of 2022, apart from a very slight decline from April to May after which it continued to increase.

Taken together, these data indicate that the U.S. economy was likely not in a recession during the first half of 2022. The BEA revises the data on real GDP and real GDI over time as various government agencies gather more information on the different production and income measures included in the series. Jeremy Nalewaik of the Federal Reserve Board of Governors has analyzed the BEA’s adjustments to its initial estimates of real GDP and real GDI. He has found that when there are significant differences between the two series, the BEA revisions usually result in the GDP values being revised to be closer to the GDI values. Put another way, the initial GDI estimates may be more accurate than the initial GDP estimates.

If that generalization holds true in 2022, then the BEA may eventually revise its estimates of GDP upward, which would show that the U.S. economy was not in a recession in the first of half of 2022 because economic activity was increasing rather than decreasing.

Sources: Jon Hilsenrath, “A Different Take on the U.S. Economy: Maybe It Isn’t Really Shrinking,” Wall Street Journal, August 28, 2022; Reade Pickert, “Key US Growth Measures Diverge, Complicating Recession Debate,” bloomberg.com, August 25, 2022; Jeremy L. Nalewaik, “The Income- and Expenditure-Side Estimates of U.S. Output Growth,” Brookings Papers on Economic Activity, Spring 2010, pp. 71-127; and Federal Reserve Bank of St. Louis.

Glenn Hubbard and Tony O’Brien continue their podcast series by spending just under 15 minutes discussing why it was so difficult for economists to see this pandemic and the associated economic downturn coming. Just as scientists lacked the indicators to see the pandemic coming, economists also didn’t have the tools available to see where the economy was headed even though some early signs were present. Please listen and SHARE with your students.

Glenn Hubbard and Tony O’Brien continued their podcast series by spending about 15 minutes discussing the impact of the Pandemic on the Mom and Pop Businesses across the country. Much of the stimulus package has been developed to save small business but might it be too late or just not enough? Please listen and SHARE with your students.

Supports: Econ (Chapter 20) & Macro (Chapter 10): Economics Growth, the Financial System, and Business Cycles; Essentials: Chapter 14.

Why Do Economists Have Trouble Predicting Recessions?

During the 2008 financial crisis,Queen Elizabeth of England visited the London School of Economics and famously asked the economists present, “Why did nobody notice it?” The queen is not alone in wondering why economists seem unable to predict when an economic crisis or financial crisis will hit.

There are three main reasons recessions are difficult for economists to predict:

Business Cycles are Not Uniform Although economists and policymakers often refer to the “business cycle,” in fact the recurring periods of economic expansion and economic contraction are not of uniform length or severity, so they do not resemble a sine wave from mathematics or other regular pattern. Because economic expansions have no set length, there is no reason to predict that an economic expansion that has lasted for a particular period of time will soon end in a recession.

Leading Economic Indicators are Not Reliable Economists haven’t found a consistent relationship between changes in any economic variable and later changes in real GDP and employment that would allow them to predict when a recession might begin. There are some variables, called leading economic indicators, that usually begin to decline before real GDP and employment decline. But those leading indicators are not completely reliable. For example, stock prices usually decline before a recession begins as investors anticipate the reduction in profits that occur during a recession. But although the largest one-day percentage decline in the S&P 500 stock index occurred on October 19, 1987, the next recession did not begin until nearly three years later. The late Nobel laureate Paul Samuelson of the Massachusetts Institute of Technology once joked that the stock market had predicted nine of the last five recessions.

Events That Trigger a Recession are Hard to Predict Perhaps most importantly, there are many different events that can trigger a recession and these triggering events are typically difficult to predict. For example, the answer to the Queen of England’s question about why economists failed to predict the financial crisis and recession of 2007-2009 is that very few economists recognized how vulnerable the U.S. financial system—and, therefore, the U.S. economy—was to a decline in housing prices.

Many economists believed that the doubling of housing prices between 2000 and 2006 was unsustainable. But few economists or policymakers realized that falling housing prices would lead many homeowners to default on their mortgages, particularly so-called subprime borrowers who had poor credit histories. Economists also didn’t realize these defaults would lead to falling prices of mortgage-backed and severe problems for financial firms that owned these securities. In a speech given in 2007, a few months before the Great Recession began, Federal Reserve Chair Ben Bernanke stated that: “We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of economy or to the financial system.” Bernanke’s opinion was shared by many other economists inside and outside the Fed. Because they didn’t fully understand that, given changes in the financial system over the previous 20 years, falling housing prices would lead to a financial crisis, most economists failed to predict the financial crisis that led to the Great Recession.

Similarly, most economists and policymakers underestimated the effects of Covid-19 when the disease first appeared in China at the end of 2019. In the past 20 years, the world has seen four similar viruses:

2002: Severe Acute Respiratory Syndrome (SARS)

2009: Swine flu

2012: Middle East Respiratory Syndrome (MERS)

2014: Ebola

For various reasons, none of these viruses reached the levels in the United States that required widespread quarantines or the closing of schools and other social distancing measures, although more than 12,000 people may have died of swine flu in the United States.

This experience led many economists, policymakers, firms, and investors to believe that the United States was unlikely to experience a significant economic disruption as a result of the coronavirus. From mid-December 2019 to mid-January 2020, none of the most widely followed forecasts of U.S. real GDP growth for the year 2020 indicated that a recession was likely. The real GDP forecasts from the Congressional Budget Office, the Federal Reserve’s Federal Open Market Committee, the Goldman Sachs investment bank, and 60 economists surveyed by the Wall Street Journal were all between 1.9 percent and 2.3 percent—comparable to the 2.3 percent increase in real GDP that the U.S. had experienced during 2019. The S&P 500 stock index reached a record high on February 19, 2020, despite China already having more than 50,000 cases of infection from the virus.

By mid-March, as cases of Covid-19 became common in the United States and most cities and states were announcing social distancing policies that included closing many non-essential businesses, the S&P 500 had declined by more than 30 percent and economists and policymakers all realized that the U.S. economy would be experiencing a substantial recession

That economists failed to predict the recessions of 2007-2009 and 2020 should probably not have been surprising. Economists Zidong An, João Tovar Jalles, and Prakash Loungani of the International Monetary Fund (IMF) studied how accurate economists were in forecasting recessions in 63 countries over the period from 1990 to 2014. They found that both economists in the private sector as well as the IMF’s own economists rarely succeeded in forecasting a recession before it had begun. On average during this period, real GDP declined by 2.8 percent during the first year of a recession. But in April of the year prior to the start of a recession, the average forecast from private sector economists and economists at the IMF was for an increase in real GDP of 3 percent. By October of the year prior to a recession, private economists had reduced their forecasts of real GDP for the following year on average to an increase of 2 percent and economists at the IMF had reduced their forecast to 2.5 percent but these forecasts were still well above the actual decline in real GDP of 2.8 percent.

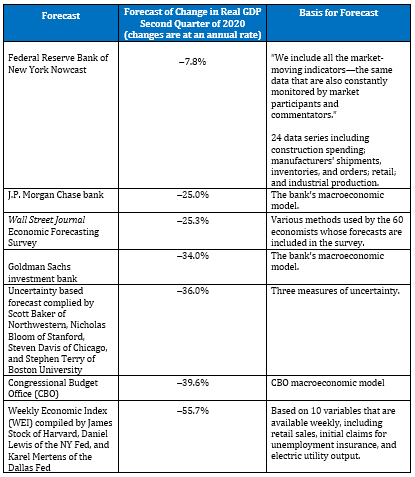

In recent years, economists have devoted resources to forecasting how real GDP will change during the current quarter. This nowcasting, if accurate, can provide policymakers and economists information on how a recession is progressing while it is occurring. Nowcasting generally relies on identifying relationships between economic variables that have data available monthly or weekly and real GDP, which in the United States is calculated by the BEA quarterly. Because economists disagree on which data provide the most accurate forecasts of real GDP during the current quarter, their nowcasts can be strikingly different.

The following table shows seven nowcasts issued during mid-April 2020 of real GDP during the second quarter of 2020, during the recession caused by the coronavirus pandemic. The data are given as changes expressed at an annual rate, which means they should be interpreted as indicating what the change in real GDP would be if the rate at which GDP changed in that quarter were sustained for a year. (Note that the Weekly Economic Index (WEI) and the uncertainty based forecast were originally presented as the percentage change from the same quarter in the previous year and have been converted to an annual rate.) Six of the forecasts agree in predicting that real GDP would decline during the quarter at a very high rate of more than 25 percent. As a standard of comparison, before the second quarter of 2020, the largest two quarterly declines in real GDP since 1947 were the decline of 10.0 percent in the first quarter of 1958 and the decline of 8.4 percent in the fourth quarter of 2008. Even the more moderate decline predicted by the New York Fed’s Nowcast would be among the largest in the past 75 years.

Ultimately, the difficulty that macroeconomists encounter in forecasting changes in real GDP indicates the complexity of the macroeconomy. Economists have not yet succeeded in reducing this complexity to a statistical model that can reliably forecast changes in real GDP—particularly whether a recession is likely to occur.

Sources: Scott Baker, Nicholas Bloom, Steven Davis, and Stephen Terry, “Covid-Induced Economic Uncertainty,” National Bureau of Economic Research Working Paper 26983, April 2020; Zidong An, João Tovar Jalles, and Prakash Loungani, “How Well Do Economists Forecast Recessions?” IMF Working Paper, March 2018; Board of Governors of the Federal Reserve System, “Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, under Their Individual Assumptions of Projected Appropriate Monetary Policy,” federalreserve.gov, December 11, 2019; Goldman Sachs, “What’s the Outlook for the U.S. Stock Market in 2020?” January 6, 2020; “Economic Forecasting Survey,” wsj.com; Lisa Beilfuss, “Why a 50% Drop in U.S. GDP Isn’t as Bad as It Seems, barrons.com, April 14, 2020; Andrew Pierce, “The Queen Asks Why No One Saw the Credit Crunch Coming,” telegraph.com.uk, November 5, 2008; Brian Domitrovic, “The Stock Market Has Predicted Nine of the Past Five Recessions,” forbes.com, November 22, 2018; and Federal Reserve Bank of St. Louis.

Question: During the coronavirus pandemic, some people wondered why biologists seemed unable to answer many questions about the virus, including why children appeared rarely to become ill, why men were more likely than women to die from the virus, and why there was great uncertainty about whether some existing pharmaceuticals would be effective in treating the disease. Briefly discuss similarities and differences between the problem biologists faced in understanding the coronavirus and the problem economists face in predicting recessions.

For Economics Instructors that would like the approved answers to the above questions, please email Christopher DeJohn from Pearson at christopher.dejohn@pearson.com and list your Institution and Course Number.

On April 24th, Glenn Hubbard and Tony O’Brien continued their podcast series by spending about 18 minutes discussing the role of uncertainty in how quickly the economy can rebound once things open back up. A very good discussion about business cycles occurs. Instructors – Please consider sharing these podcasts with your students. A lot of URL dropping in today’s conversation so we’re providing some show notes from today’s episodes if you’d like to explore them further: