In the Federal Reserve Act, Congress charged the Federal Reserve with conducting monetary policy so as to achieve both “maximum employment” and “stable prices.” These two goals are referred to as the Fed’s dual mandate. (We discuss the dual mandate in Macroeconomics, Chapter 15, Section 15.1, Economics, Chapter 25, Section 25.1, and Money, Banking, and the Financial System, Chapter 15, Section 15.1.) Accordingly, when Fed chairs give their semiannual Monetary Policy Reports to Congress, they reaffirm that they are acting consistently with the dual mandate. For example, when testifying before the U.S. Senate Committee on Banking, Housing, and Urban Affairs in June 2022, Fed Chair Jerome Powell stated that: “The Fed’s monetary policy actions are guided by our mandate to promote maximum employment and stable prices for the American people.”

Despite statements of that kind, some economists argue that in practice during some periods the Fed’s policymaking Federal Open Market Committee (FOMC) acts as if it were more concerned with one of the two mandates. In particular, in the decades following the Great Inflation of the 1970s, FOMC members appear to have put more emphasis on price stability than on maximum employment. These economists argue that during these years, FOMC members were typically reluctant to pursue a monetary policy sufficiently expansionary to lead to maximum employment if the result would be to cause the inflation rate to rise above the Fed’s target of an annual target of 2 percent. (Although the Fed didn’t announce a formal inflation target of 2 percent until 2012, the FOMC agreed to set a 2 percent inflation target in 1996, although they didn’t publicly announce at the time. Implicitly, the FOMC had been acting as if it had a 2 percent target since at least the mid–1980s.)

In July 2019, the FOMC responded to a slowdown in economic growth in late 2018 and early 2019 but cutting its target for the federal funds rate. It made further cuts to the target rate in September and October 2019. These cuts helped push the unemployment rate to low levels even as the inflation rate remained below the Fed’s 2 percent target. The failure of inflation to increase despite the unemployment rate falling to low levels, provides background to the new monetary policy strategy the Fed announced in August 2020. The new monetary policy, in effect, abandoned the Fed’s previous policy of attempting to preempt a rise in the inflation rate by raising the target for the federal funds rate whenever data on unemployment and real GDP growth indicated that inflation was likely to rise. (We discussed aspects of the Fed’s new monetary policy in previous blog posts, including here, here, and here.)

In particular, the FOMC would no longer see the natural rate of unemployment as the maximum level of employment—which Congress has mandated the Fed to achieve—and, therefore, wouldn’t necessarily begin increasing its target for the federal funds rate when the unemployment rate dropped by below the natural rate. As Fed Chair Powell explained at the time, “the maximum level of employment is not directly measurable and [it] changes over time for reasons unrelated to monetary policy. The significant shifts in estimates of the natural rate of unemployment over the past decade reinforce this point.”

Many economists interpreted the Fed’s new monetary strategy and the remarks that FOMC members made concerning the strategy as an indication that the Fed had turned from focusing on the inflation rate to focusing on unemployment. Of course, given that Congress has mandated the Fed to achieve both stable prices and maximum employment, neither the Fed chair nor other members of the FOMC can state directly that they are focusing on one mandate more than the other.

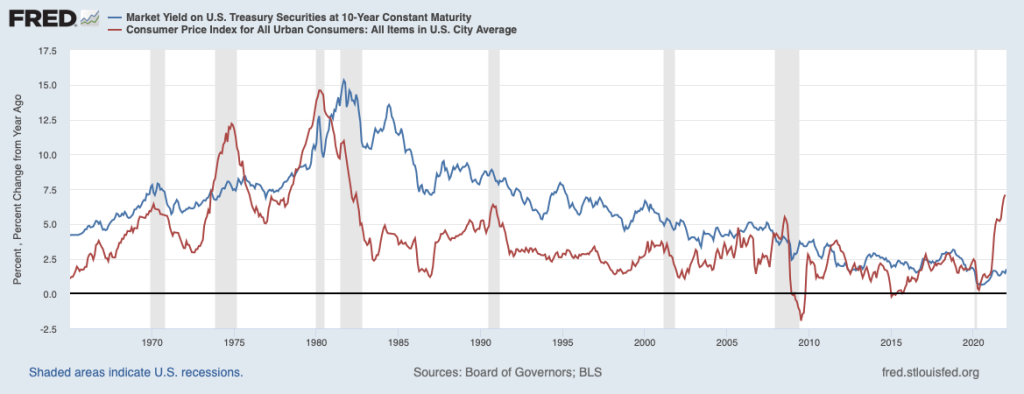

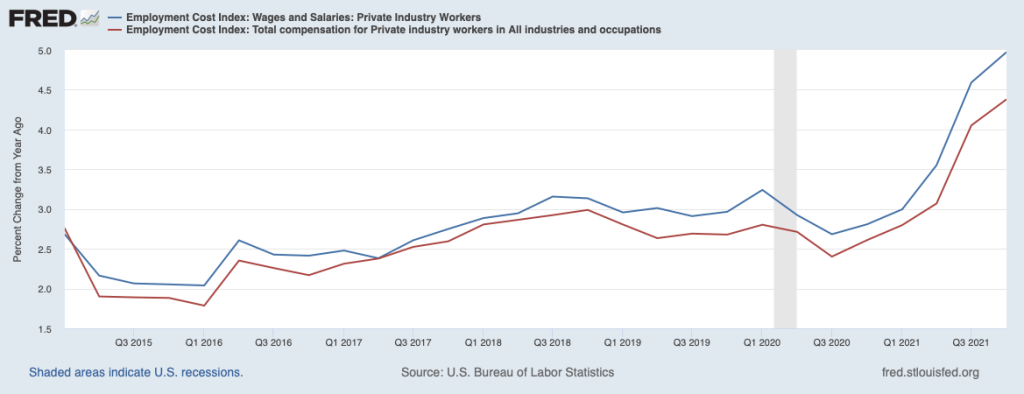

The sharp acceleration in inflation that began in the spring of 2021 and continued into the fall of 2022 (shown in the following figure) has caused members of the FOMC to speak more forcefully about the need for monetary policy to bring inflation back to the Fed’s target rate of 2 percent. For example, in a speech at the Federal Reserve Bank of Kansas City’s annual monetary policy conference held in Jackson Hole, Wyoming, Fed Chair Powell spoke very directly: “The Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal.” According to an article in the Wall Street Journal, Powell had originally planned a longer speech discussing broader issues concerning monetary policy and the state of the economy—typical of the speeches that Fed chairs give at this conference—before deciding to deliver a short speech focused directly on inflation.

Members of the FOMC were concerned that a prolonged period of high inflation rates might lead workers, firms, and investors to no longer expect that the inflation rate would return to 2 percent in the near future. If the expected inflation rate were to increase, the U.S. economy might enter a wage–price spiral in which high inflation rates would lead workers to push for higher wages, which, in turn, would increase firms’ labor costs, leading them to raise prices further, in response to which workers would push for even higher wages, and so on. (We discuss the concept of a wage–price spiral in earlier blog posts here and here.)

With Powell noting in his Jackson Hole speech that the Fed would be willing to run the risk of pushing the economy into a recession if that was required to bring down the inflation rate, it seemed clear that the Fed was giving priority to its mandate for price stability over its mandate for maximum employment. An article in the Wall Street Journal quoted Richard Clarida, who served on the Fed’s Board of Governors from September 2018 until January 2022, as arguing that: “Until inflation comes down a lot, the Fed is really a single mandate central bank.”

This view was reinforced by the FOMC’s meeting on September 21, 2022 at which it raised its target for the federal funds rate by 0.75 percentage points to a range of 3 to 3.25 percent. The median projection of FOMC members was that the target rate would increase to 4.4 percent by the end of 2022, up a full percentage point from the median projection at the FOMC’s June 2022 meeting. The negative reaction of the stock market to the announcement of the FOMC’s decision is an indication that the Fed is pursuing a more contractionary monetary policy than many observers had expected. (We discuss the relationship between stock prices and economic news in this blog post.)

Some economists and policymakers have raised a broader issue concerning the Fed’s mandate: Should Congress amend the Federal Reserve Act to give the Fed the single mandate of achieving price stability? As we’ve already noted, one interpretation of the FOMC’s actions from the mid–1980s until 2019 is that it was already implicitly acting as if price stability were a more important goal than maximum employment. Or as Stanford economist John Cochrane has put it, the Fed was following “its main mandate, which is to ensure price stability.”

The main argument for the Fed having price stability as its only mandate is that most economists believe that in the long run, the Fed can affect the inflation rate but not the level of potential real GDP or the level of employment. In the long run, real GDP is equal to potential GDP, which is determined by the quantity of workers, the capital stock—including factories, office buildings, machinery and equipment, and software—and the available technology. (We discuss this point in Macroeconomics, Chapter 13, Section 13.2 and in Economics, Chapter 23, Section 23.2.) Congress and the president can use fiscal policy to affect potential GDP by, for example, changing the tax code to increase the profitability of investment, thereby increasing the capital stock, or by subsidizing apprentice programs or taking other steps to increase the labor supply. But most economists believe that the Fed lacks the tools to achieve those results.

Economists who support the idea of a single mandate argue that the Fed would be better off focusing on an economic variable they can control in the long run—the inflation rate—rather than on economic variables they can’t control—potential GDP and employment. In addition, these economists point out that some foreign central banks have a single mandate to achieve price stability. These central banks include the European Central Bank, the Bank of Japan, and the Reserve Bank of New Zealand.

Economists and policymakers who oppose having Congress revise the Federal Reserve Act to give the Fed the single mandate to achieve price stability raise several points. First, they note that monetary policy can affect the level of real GDP and employment in the short run. Particularly when the U.S. economy is in a severe recession, the Fed can speed the return to full employment by undertaking an expansionary policy. If maximum employment were no longer part of the Fed’s mandate, the FOMC might be less likely to use policy to increase the pace of economic recovery, thereby avoiding some unemployment.

Second, those opposed to the Fed having single mandate argue that the Fed was overly focused on inflation during some of the period between the mid–1980s and 2019. They argue that the result was unnecessarily low levels of employment during those years. Giving the Fed a single mandate for price stability might make periods of low employment more likely.

Finally, because over the years many members of Congress have stated that the Fed should focus more on maximum employment than price stability, in practical terms it’s unlikely that the Federal Reserve Act will be amended to give the Fed the single mandate of price stability.

In the end, the willingness of Congress to amend the Federal Reserve Act, as it has done many times since initial passage in 1914, depends on the performance of the U.S. economy and the U.S. financial system. It’s possible that if the high inflation rates of 2021–2022 were to persist into 2023 or beyond, Congress might revise the Federal Reserve Act to change the Fed’s approach to fighting inflation either by giving the Fed a single mandate for price stability or in some other way.

Sources: Board of Governors of the Federal Reserve System, “Federal Reserve Issues FOMC Statement,” federalreserve.gov, September 21, 2022; Board of Governors of the Federal Reserve System, “Summary of Economic Projections,” federalreserve.gov, September 21, 2022; Nick Timiraos, “Jerome Powell’s Inflation Whisperer: Paul Volcker,” Wall Street Journal, September 19, 2022; Matthew Boesler and Craig Torres, “Powell Talks Tough, Warning Rates Are Going to Stay High for Some Time,” bloomberg.com, August 26, 2022; Jerome H. Powell, “Semiannual Monetary Policy Report to the Congress,” June 22, 2022, federalreserve.gov; Jerome H. Powell, “Monetary Policy and Price Stability,” speech delivered at “Reassessing Constraints on the Economy and Policy,” an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, federalreserve.gov, August 26, 2022; John H. Cochrane, “Why Isn’t the Fed Doing its Job?” project-syndicate.org, January 19, 2022; Board of Governors of the Federal Reserve System, “Minutes of the Federal Open Market Committee Meeting on July 2–3, 1996,” federalreserve.gov; and Federal Reserve Bank of St. Louis.