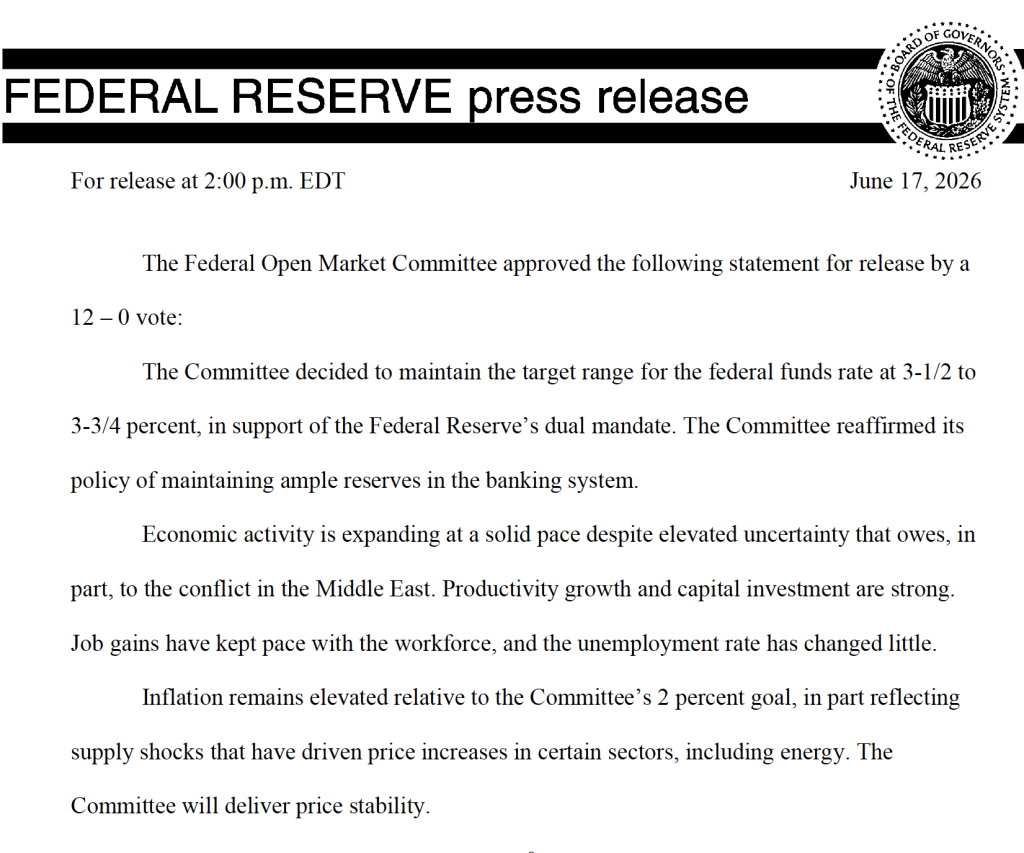

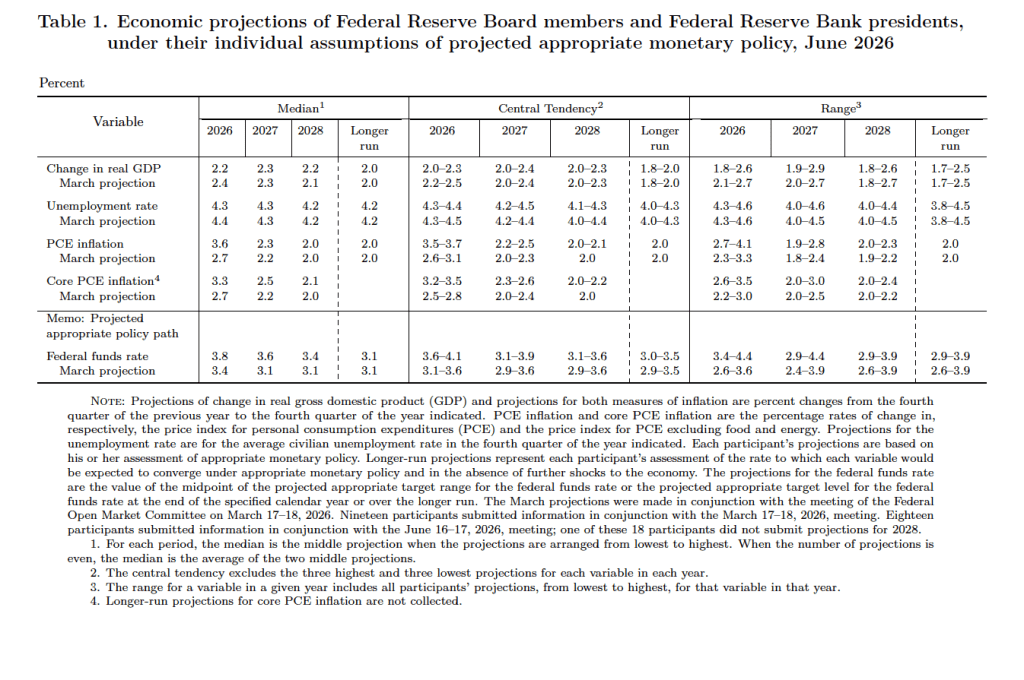

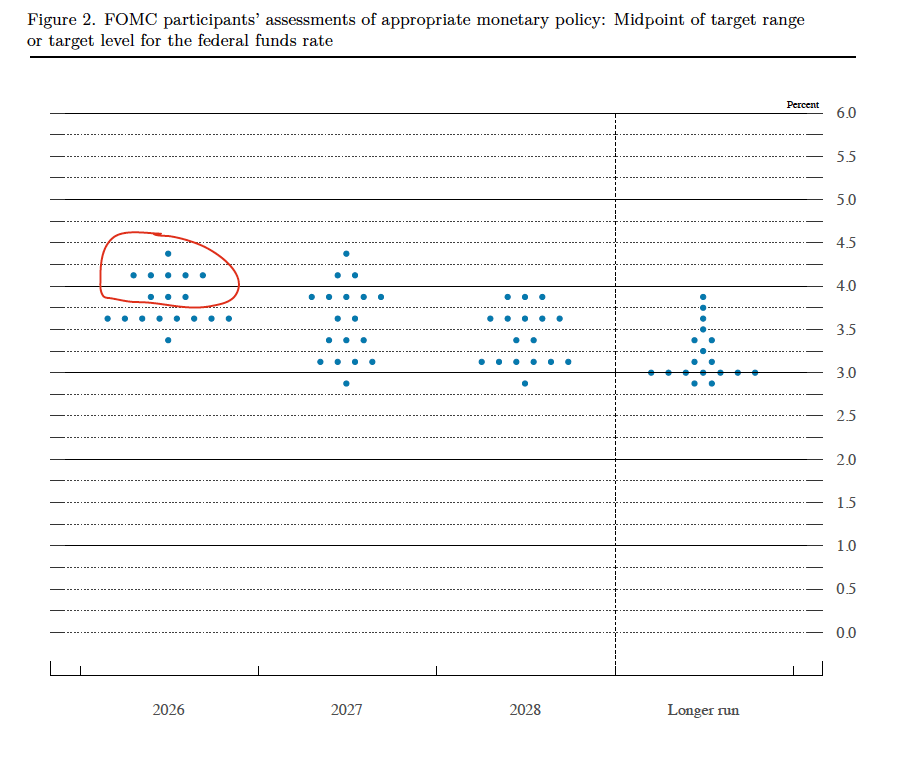

Image created by ChatGPT

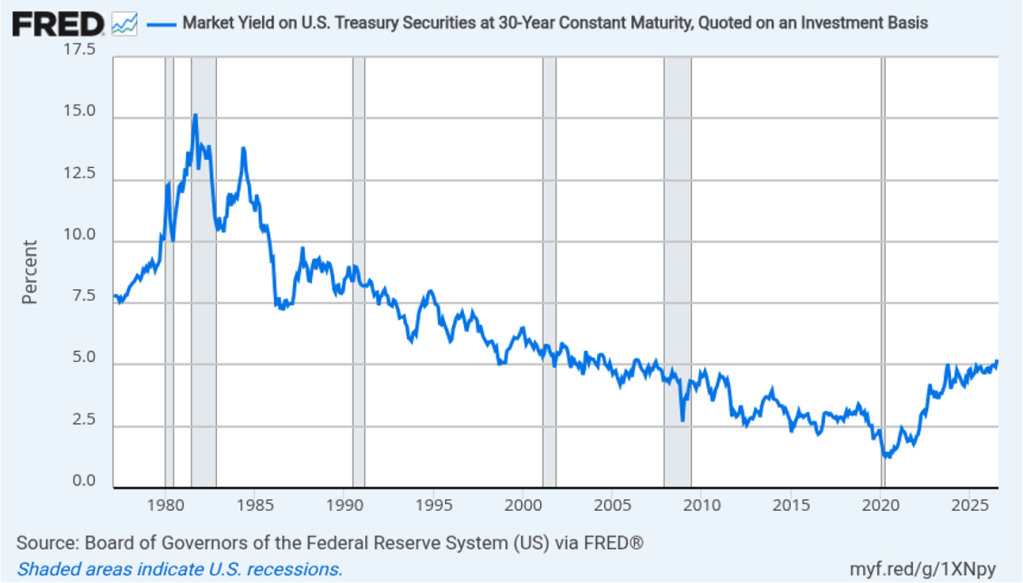

At the close of trading on Friday, July 31, the yield on the 30-year Treasury bond was 5.28 percent. As the following figure shows, that yield was the highest since July 2007, before the Global Financial Crisis and the Great Recession of 2007–2009.

Note: As we discuss in Money, Banking, and the Financial System, Chapter 3, when economists refer to the interest rate on a bond, they are referring to the bond’s yield to maturity. (A new edition of our textbook is now available.)

The figure shows the nominal yields on the 30-year Treasury bond—the yield not corrected for the effects of inflation. What factors can cause the nominal yield on Treasury bonds to increase? Because investors are interested in the real yield on Treasury bonds—the yield corrected for the effects of inflation—an increase in the expected inflation rate will cause the nominal yield to rise. The Fisher effect refers to the assertion by Yale economist Irving Fisher that the nominal interest rate on a bond rises point-for-point with increases in the expected inflation rate. Although the pure Fisher effect doesn’t typically hold, there’s no doubt that changes in the expected inflation rate are a key driver of changes in nominal bond yields.

The other main driver of nominal bond yields is changes in the demand for credit. The Congressional Budget Office forecasts that, because of continuing federal government budget deficits, the value of publicly held Treasury securities will rise “from 101 percent of GDP in 2026 to 120 percent in 2036, well above the previous record of 106 percent just after World War II.” Such substantial increases in the supply of Treasury bonds will lower their prices, raising their nominal yields.

The market for Treasury bonds is linked to the market for corporate bonds. Although not all investors who buy Treasury bonds also buy corporate bonds and vice versa, many investors participate in both markets. As a result, a surge in the supply of corporate bonds will raise both their yields and the yields on Treasury bonds. As the following figure shows, the yields on high-quality corporate bonds (those rated A, AA, or AAA), have moved roughly in synch with Treasury yields, with recent increases in corporate yields mirroring the increases in Treasury yields.

The surge in the supply of corporate bonds has been driven by so-called hyperscalers, such as Amazon, Google, Oracle, and Microsoft, who have been raising hundreds of billions of dollars to fund the building of data centers to power AI programs.

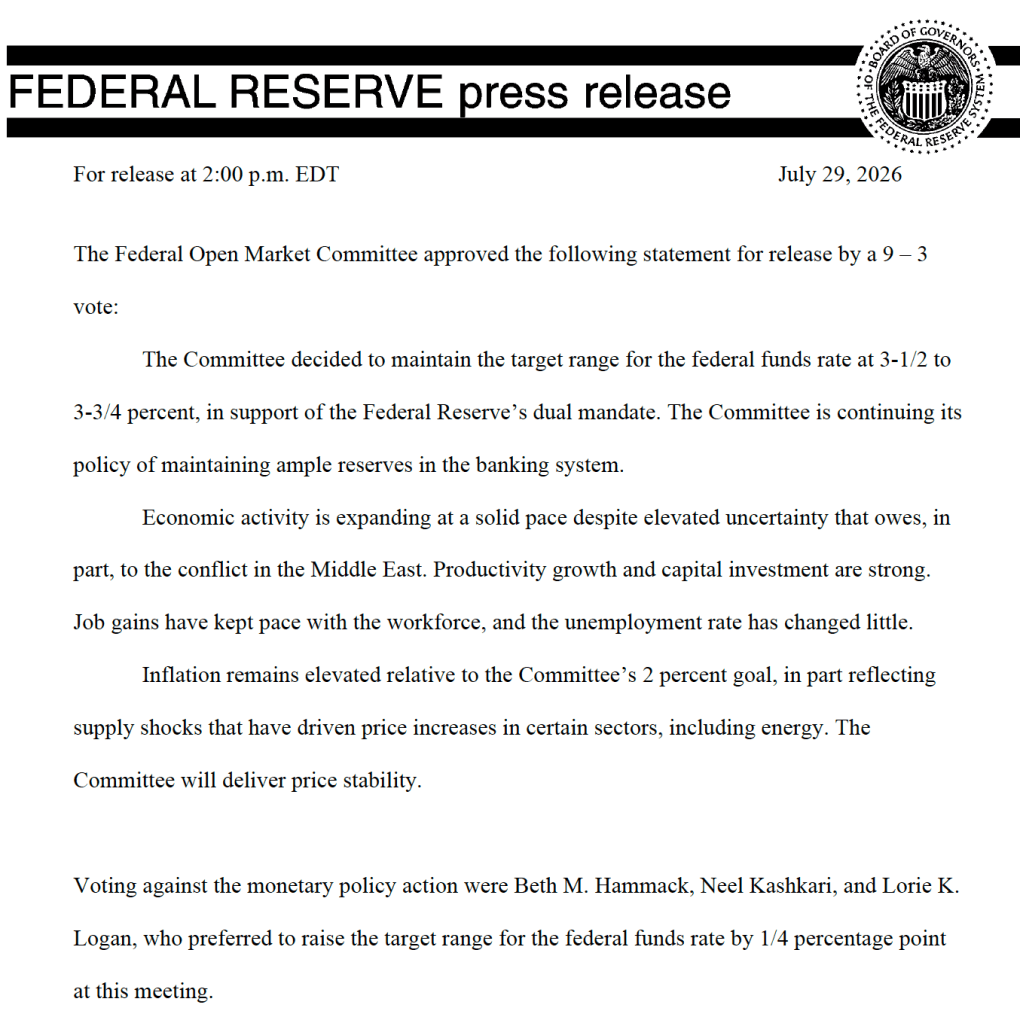

In recent days, there has been much discussion as to whether the increased supply of bonds or rising expectations of future inflation have been behind the surge in Treasury yields. Following the latest meeting of the Federal Open Market Committee (FOMC) on Wednesday, July 29, Fed Chair Kevin Warsh’s press conference left many industry analysts believing that Warsh would be willing to tolerate higher rates of inflation. If, on the other hand, Warsh had been interpreted as willing to raise the FOMC’s target for the federal funds rate in the near future, that may have reassured investors that future rates of inflation would be lower, which would have brought down Treasury yields. An article in the Wall Street Journal quoted Mark Cabana, head of U.S. rates strategy at Bank of America as saying: “If you actually want to get long-end rates down, there’s an argument that you need to raise front-end rates [that is, the target for the federal funds rate] right now in order to establish that credibility.”

The following figure from the Wall Street Journal shows that during Warsh’s press conference, the yield on the 30-year Treasury bond rose sharply.

Despite the immediate reaction of bond investors to Warsh’s press conference, there isn’t much indication that in recent weeks a significant rise in investors’ expectations of inflation has been the key driver of increases in the Treasury bond rate.

In January 1997, the U.S. Treasury started issuing indexed bonds to address investors’ concerns about the effects of inflation on real interest rates. With these bonds, called TIPS (Treasury Inflation-Protected Securities), the Treasury increases the principal, or face value, as the price level increases, as measured by the CP. The stated interest rate on a TIPS remains fixed once issued, but because it is applied to a principal amount that increases with inflation, the effective interest rate increases with inflation. For example, suppose that when issued, a 30-year TIPS has a principal of $1,000 and a coupon rate of 3%. (The coupon rate equals the coupon payment divided by the face value, or par value, of a bond.) If the inflation rate during the year is 2%, then the principal increases to $1,020. So, the investor would receive the coupon rate of 3% plus the 2% increase in the principal, or 5%. In the rare case in which the economy experiences deflation, with the price level falling, the principal of a TIPS will decrease.

If we compare the yield on a TIPS of a given maturity to the yield on a non-TIPS Treasury security of the same maturity, we have an estimate of the annual inflation rate investors expect over that time period. For example, if the yield on a non-TIPS 30-Year Treasury bond is 5% and the yield on a 30-year TIPS is 2%, investors expect an annual inflation rate of 3% over the next 30 years. The difference between the yield on the non-TIPS 30-year Treasury bond and the yield on the 30-year TIPS is called the 30-year breakeven inflation rate because at that inflation rate, an investor would expect the same real yield from buying either the TIPS or the non-TIPS bond.

The following figure shows, for the period beginning in January 2022, the daily yield to maturity on the 30-year Treasury bond (the blue line), the yield on the 30-year TIPS (the orange line), and the implied 30-year breakeven inflation rate (the green line). Note that values for the green line are usually close to 2%, which is the Fed’s long-run inflation target. Even during 2022, when inflation as measured by the CPI reached 9%, this measure of expected inflation never rose above 2.7%. When the expected inflation rate changes relatively little during a period when the actual inflation rate is fluctuating, expectations of inflation are said to be well anchored.

A reasonable conclusion is that, to this point, the rise in long-term bond yields appears to be driven more by the increasing supply of Treasury and corporate bonds than by higher expected inflation.

(We should note that some economists question the accuracy of using breakeven inflation as a measure of expected inflation for two reasons: (1) An investor buying a TIPS is protected against the possibility that the inflation rate might turn out to be higher than expected. As a result, investors may be willing to accept a slightly lower interest rate on TIPS, which would lead to an

overestimate of the expected inflation rate. (2) The volume of TIPS traded on any given day is much smaller than volume of non-TIPS Treasury securities traded, which make TIPS slightly less liquid—meaning they are slightly more difficult to sell. Investors typically require a higher interest rate to buy a less liquid asset. So, this outcome might have the opposite effect of the first one—an underestimate of the expected inflation rate.)