According to the Federal Reserve Act, the Fed must conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” Neither “maximum employment” nor “stable prices” are defined in the act.

The Fed has interpreted “stable prices” to mean a low rate of inflation. Since 2012, the Fed has had an explicit inflation target of 2 percent. When the Fed announced its new monetary policy strategy in August 2020, it modified its inflation target by stating that it would attempt to achieve an average inflation rate of 2 percent over time. As Fed Chair Jerome Powell stated: “Our approach can be described as a flexible form of average inflation targeting.” (Note that although the consumer price index (CPI) is the focus of many media stories on inflation, the Fed’s preferred measure of inflation is changes in the core personal consumption expenditures (PCE) price index. The PCE is a broader measure of the price level than is the CPI because it includes the prices of all the goods and services included in consumption category of GDP. “Core” means that the index excludes food and energy prices. For a further discussion see, Economics, Chapter 25, Section 15.5 and Macroeconomics, Chapter 15, Section 15.5.)

There is more ambiguity about how to determine whether the economy is at maximum employment. For many years, a majority of members of the Federal Open Market Committee (FOMC) focused on the natural rate of unemployment (also called the non-accelerating rate of unemployment (NAIRU)) as the best gauge of when the U.S. economy had attained maximum employment. The lesson many economists and policymakers had taken from the experience of the Great Inflation that lasted from the late 1960s to the early 1980s was if the unemployment rate was persistently below the natural rate of unemployment, inflation would begin to accelerate. Because monetary policy affects the economy with a lag, many policymakers believed it was important for the Fed to react before inflation begins to significantly increase and a higher inflation rate becomes embedded in the economy.

At least until the end of 2018, speeches and other statements by some members of the FOMC indicated that they continued to believe that the Fed should pay close attention to the relationship between the natural rate of unemployment and the actual rate of unemployment. But by that time some members of the FOMC had concluded that their decision to begin raising the target for the federal funds rate in December 2015 and continuing raising it through December 2018 may have been a mistake because their forecasts of the natural rate of unemployment may have been too high. For instance, Atlanta Fed President Raphael Bostic noted in a speech that: “If estimates of the NAIRU are actually too conservative, as many would argue they have been … unemployment could have averaged one to two percentage points lower” than it actually did.

Accordingly, when the Fed announced its new monetary policy strategy in August 2020, it indicated that it would consider a wider range of data—such as the employment-population ratio—when determining whether the labor market had reached maximum employment. At the time, Fed Chair Powell noted that: “the maximum level of employment is not directly measurable and [it] changes over time for reasons unrelated to monetary policy. The significant shifts in estimates of the natural rate of unemployment over the past decade reinforce this point.”

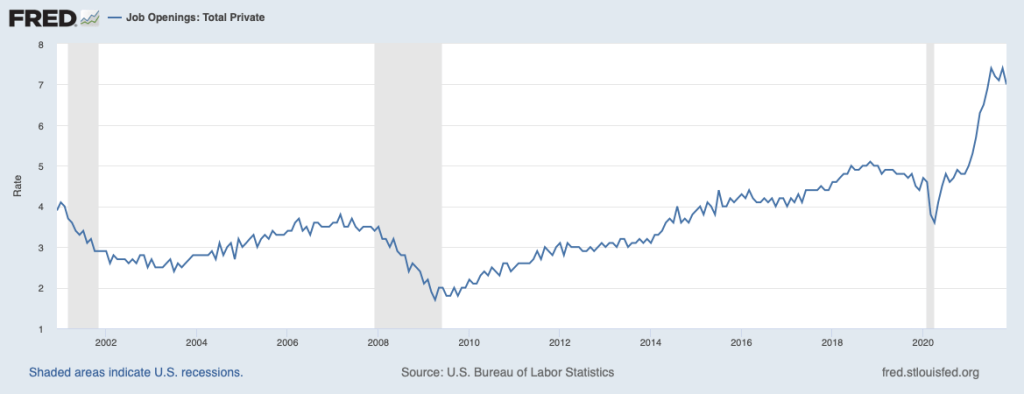

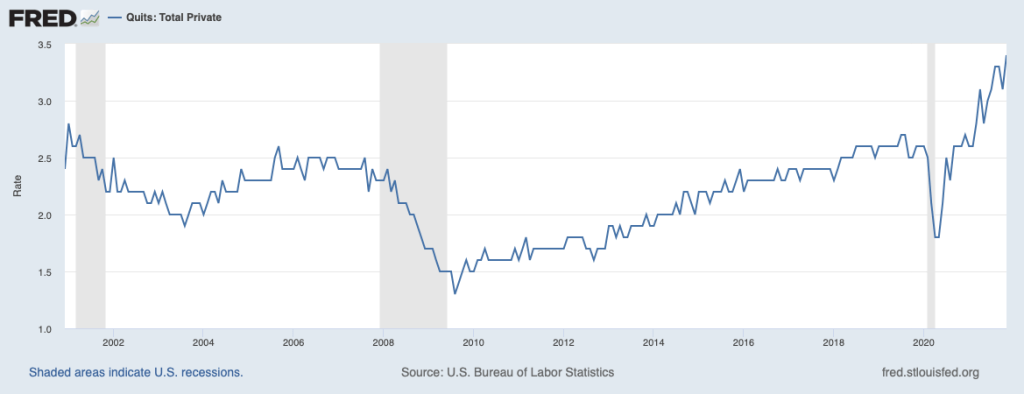

As the economy recovered from the effects of the Covid-19 pandemic, the Fed faced particular difficulty in assessing the state of the labor market. Some labor market indicators appeared to show that the economy was close to maximum employment while other indicators showed that the labor market recovery was not complete. For instance, in December 2021, the unemployment rate was 3.9 percent, slightly below the average of the FOMC members estimates of the natural rate of unemployment, which was 4.0 percent. Similarly, as the first figure below shows, job vacancy rates were very high at the end of 2021. (The BLS calculates job vacancy rates, also called job opening rates, by dividing the number of unfilled job openings by the sum of total employment plus job openings.) As the second figure below shows, job quit rates were also unusually high, indicating that workers saw the job market as being tight enough that if they quit their current job they could find easily another job. (The BLS calculates job quit rates by dividing the number of people quitting jobs by total employment.) By those measures, the labor market seemed close to maximum employment.

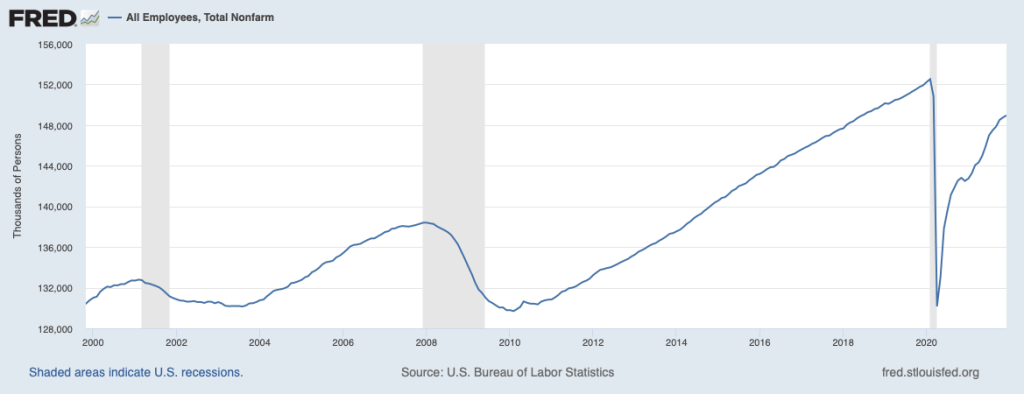

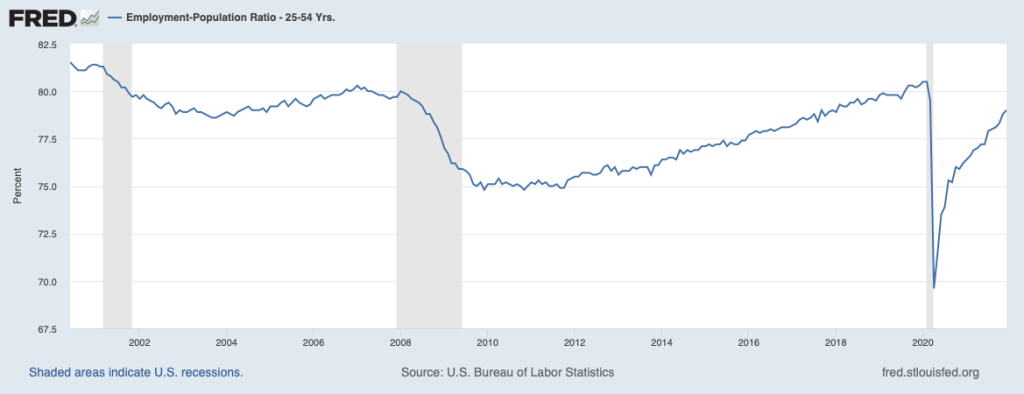

But as the first figure below shows, total employment in December 2021 was still 3.5 million below its level of early 2020, just before the U.S. economy began to experience the effects of the pandemic. Some of the decline in employment can be accounted for by older workers retiring, but as the second figure below indicates, employment of prime-age workers (those between the ages of 25 and 54), had not recovered to pre-pandemic levels.

How to reconcile these conflicting labor market indicators? In January 2022, Fed Chair Powell testified before the Senate Banking Committee as the Senate considered his nomination for a second four-year term as chair. In discussing the state of the economy he offered the opinion that: “We’re very rapidly approaching or at maximum employment.” He noted that inflation as measured by changes in the CPI had been running above 5 percent since June 2021: “If these high levels of inflation get entrenched in our economy, and in people’s thinking, then inevitably that will lead to much tighter monetary policy from us, and it could lead to a recession.” In that sense, “high inflation is a severe threat to the achievement of maximum employment.”

At the time of Powell’s testimony, the FOMC had already announced that it was moving to a less expansionary monetary policy by reducing its purchases of Treasury bonds and mortgage-backed securities and by increasing its target for the federal funds rate in the near future. He argued that these actions would help the Fed achieve its dual mandate by reducing the inflation rate, thereby heading off the need for larger increases in the federal funds rate that might trigger a recession. Avoiding a recession would help achieve the goal of maximum employment.

Powell’s remarks did not make explicit which labor market indicators the Fed would focus on in determining whether the goal of maximum employment had been obtained. It did make clear that the Fed’s new policy of average inflation targeting did not mean that the Fed would accept inflation rates as high as those of the second half of 2021 without raising its target for the federal funds rate. In that sense, the Fed’s monetary policy of 2022 seemed consistent with its decades-long commitment to heading off increases in inflation before they lead to a significant increase in the inflation rate expected by households, businesses, and investors.

Note: For a discussion of the background to Fed policy, see Economics, Chapter 25, Section 25.5 and Chapter 27, Section 17.4, and Macroeconomics, Chapter 15, Section 15.5 and Chapter 17, Section 17.4.

Sources: Jeanna Smialek, “Jerome Powell Says the Fed is Prepared to Raise Rates to Tame Inflation,” New York Times, January 11, 2022; Nick Timiraos, “Fed’s Powell Says Economy No Longer Needs Aggressive Stimulus,” Wall Street Journal, January 11, 2022; and Federal Open Market Committee, “Meeting Calendars, Statements, and Minutes,” federalreserve.gov, January 5, 2022.

One thought on “How Do We Know When the Economy Is at Maximum Employment?”