Screenshot of Fed Chair Jerome Powell at his FOMC press conference on April 29

Today’s meeting of the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) had the expected result with the committee deciding to leave unchanged its target for the federal funds rate at its current range of 3.50 percent to 3.75 percent. The members of the committee voted 8 to 4 in favor of the decision. Fed Governor Stephen Miran voted against the decision, preferring to lower the target range for the federal funds rate by 0.25 percentage point (25 basis points). Beth Hammack, president of the Federal Reserve Bank of Cleveland; Neel Kashkari, president of the Federal Reserve Bank of Minneapolis; and Lorie Logan, president of the Federal Reserve Bank of Dallas; supported keeping the target rate unchanged but “but did not support inclusion of an easing bias in the statement at this time.”

Perhaps the most significant news came at Chair Powell’s press conference at the conclusion of the meeting. Powell noted that Kevin Warsh’s nomination to be Fed chair had advanced out of the Senate Banking Committee this morning. Powell expected that Warsh would assume the role of chair by the time Powell’s term as chair ends on May 15. However, Powell announced that he would break with decades of tradition and remain on the Board of Governors. He noted that: “I have said that I will not leave the Board until this investigation [into his testimony before Congress concerning the renovations of the Fed’s headquarters building] is well and truly over, with transparency and finality, and I stand by that…. After my term as Chair ends on May 15, I will continue to serve as a governor for a period of time, to be determined. I plan to keep a low profile as a governor.” Powell’s term on the Board expires on January 31, 2028.

Powell will be the first Fed chair to remain on the Board after the end of his term as chair since Marriner Eccles continued to serve for three years after the end of his term as chair in 1948. The person whom the president has nominated as chair of the Board of Governors, once confirmed by the Senate, by tradition also serves as the chair of the FOMC. However, the Federal Reserve Act allows the FOMC to select its own chair. To head off any speculation that he might attempt to remain as chair of the FOMC, Powell stated at his press conference that: “When Kevin Warsh is confirmed and sworn, he will be that Chair. Once sworn in as Board Chair, his new colleagues will elect him to chair the FOMC as well.”

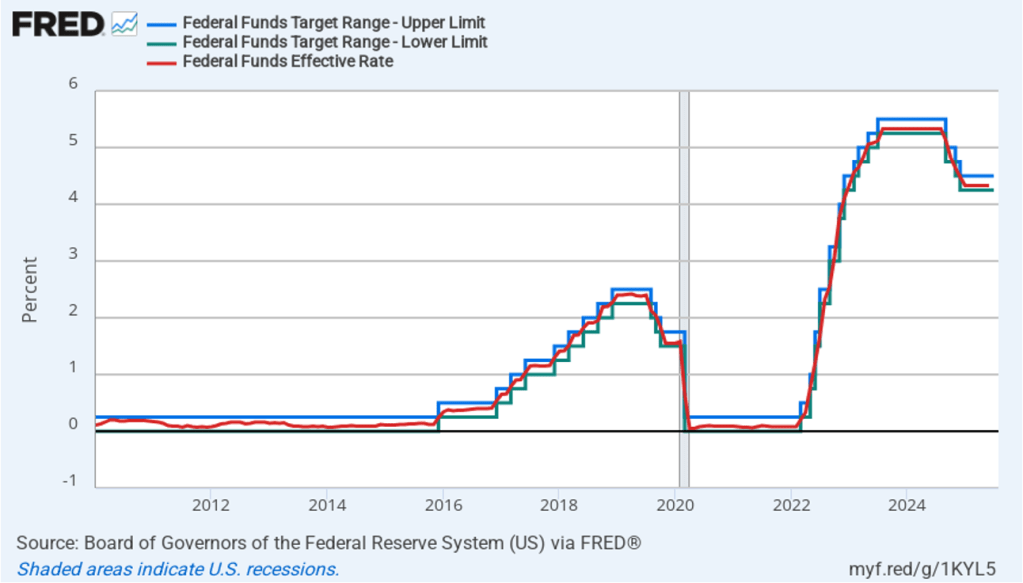

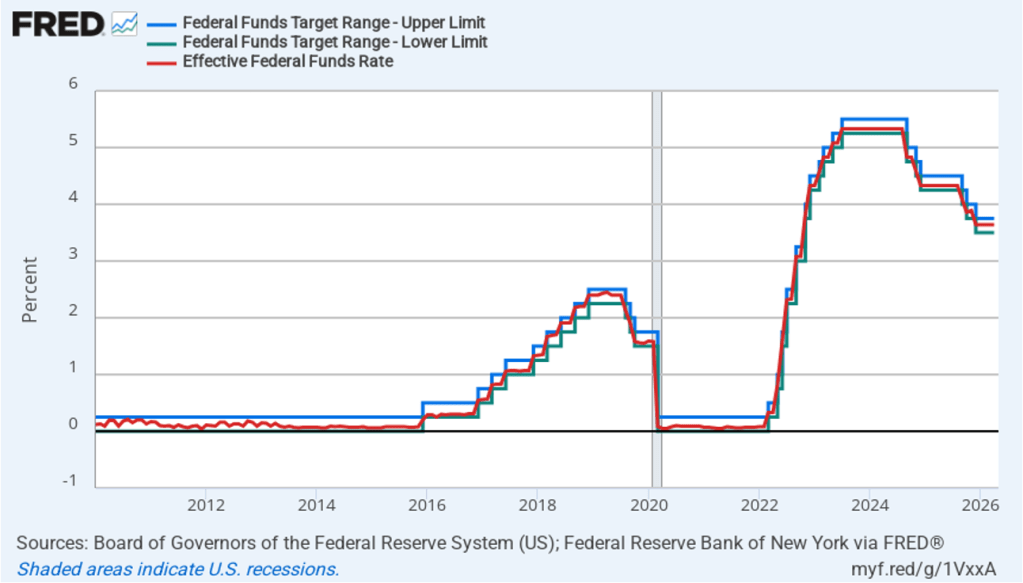

The FOMC has left its target for federal funds rate unchanged since lowering it by 25 basis points on December 10 of last year. The following figure shows for the period since January 2010, the upper bound (the blue line) and the lower bound (the green line) for the FOMC’s target range for the federal funds rate, as well as the actual values for the federal funds rate (the red line). Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate within its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

During his press conference, Powell discussed the reasons for the dissenting votes by Hammack, Kashkari, and Logan. The area of disagreement has to do with this sentence from the committee’s statement: “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” The three dissenters believe that the statement implies that the next change would likely be to lower the target range for the federal funds. They wished the language to be changed to communicate that the next change might also be to raise the target range. The four dissents were the most at an FOMC meeting since 1992.

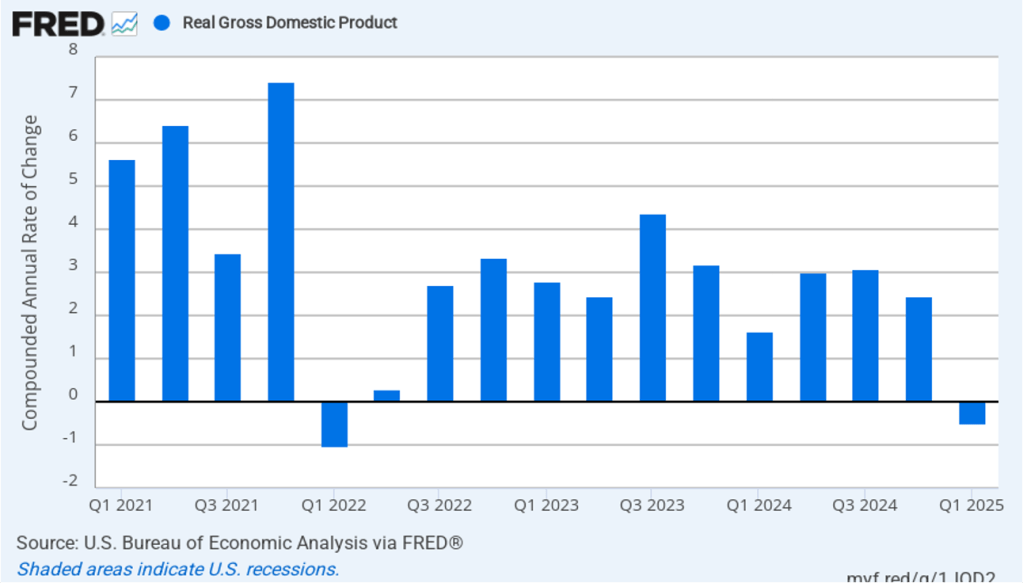

Powell stated that he believed the current target range was mildly restrictive, which he believed was appropriate given that the economy was still experiencing strong output growth and that the labor market appears to be stable, while tariffs and rising oil prices are putting upward pressure on the price level.

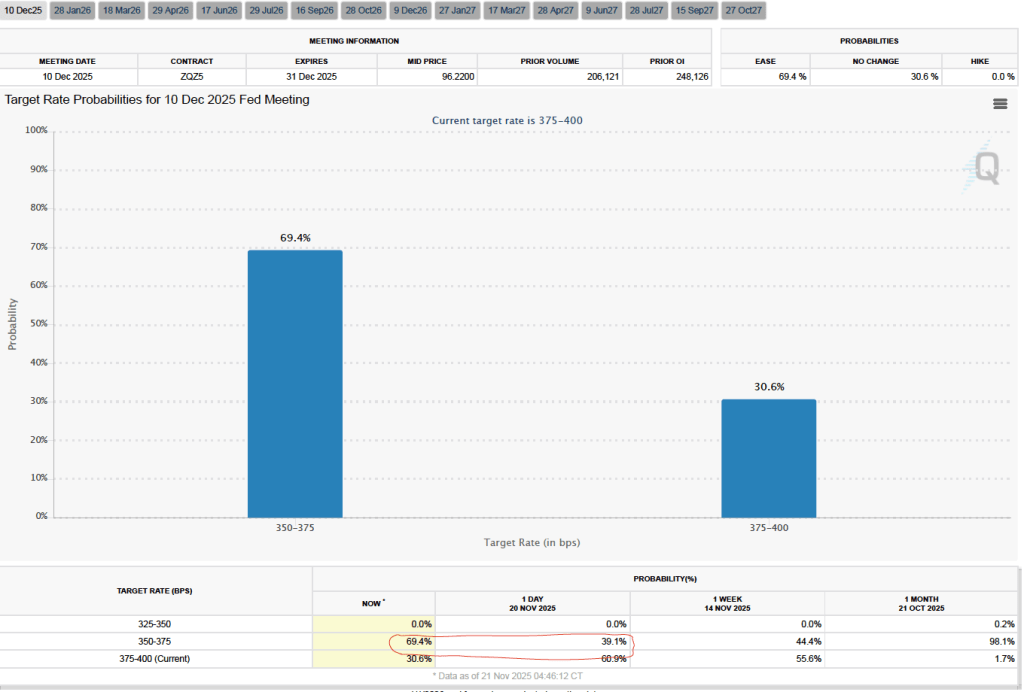

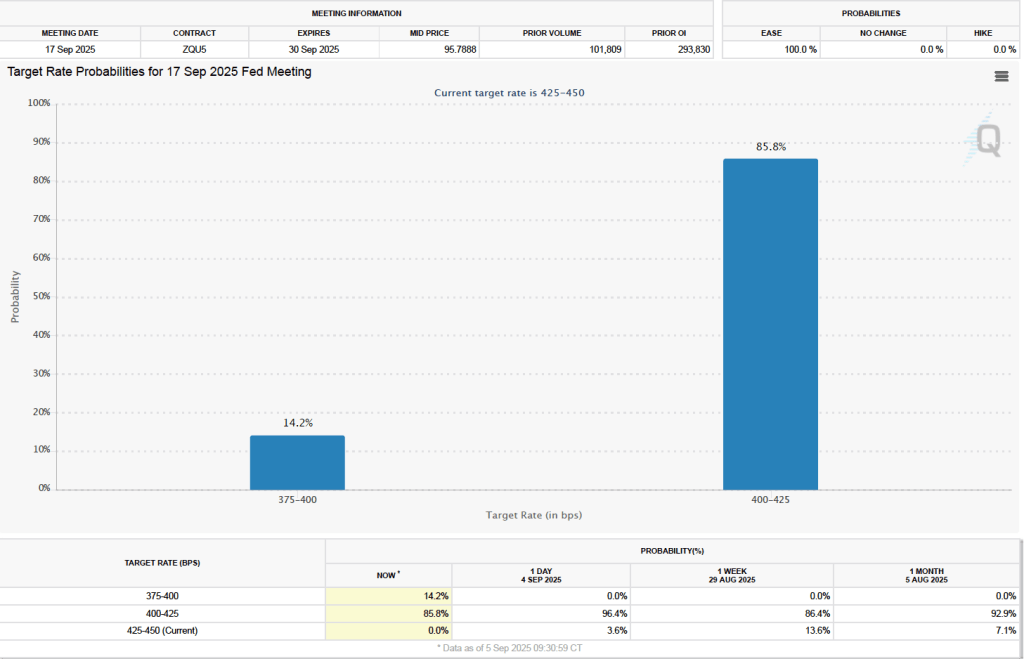

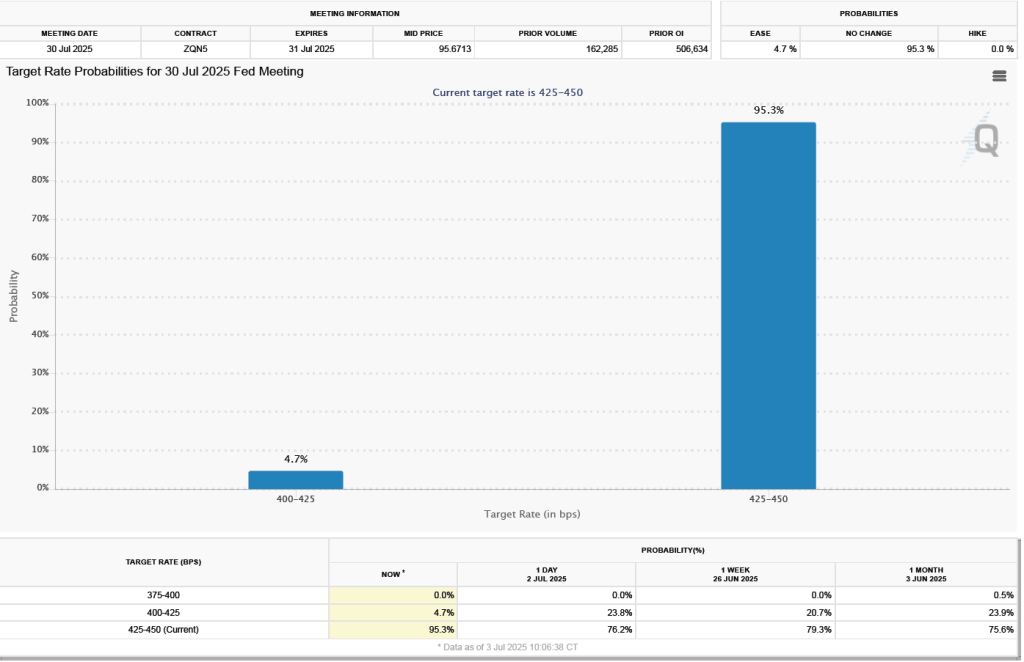

When might the FOMC lower its target range for the federal funds rate? One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. There are four more FOMC meeting scheduled for this year and for each meeting investors assign a probability of greater than 98 percent that the committee will either keep its target constant or raise it. For each meeting in 2027 until the last one on December 17–18, investors assign a probability of greater than 70 percent that the committee will keep its target constant or raise it. In other words, investors don’t believe that the target rate will be cut until the end of next year.

The next FOMC meeting will be on June 16–17. At that meeting, the committee is scheduled to release its quarterly Summary of Economic Projections (SEP), which includes a “dot plot” that represents each member’s expectations of future values of the federal funds rate. Warsh has questioned whether the SEP and the dot plot serve a good purpose and he may attempt to persuade the committee to abandon them. He has also questioned whether the chair should hold a press conference after every FOMC meeting as Powell has done since January 2019.

If Warsh does hold a press conference after the June meeting, his responses to questions will be closely analyzed for clues about the direction he intends to take the committee.