For most of human history there was little to no economic growth. Until the nineteenth century, the average person everywhere in the world lived at a subsistence level. For example, although the Roman Empire controlled most of Southern and Western Europe, the Near East, and North Africa for more than 400 years, the living standard of the average citizen of the Empire was no higher at the end of the Empire than it had been at the beginning.

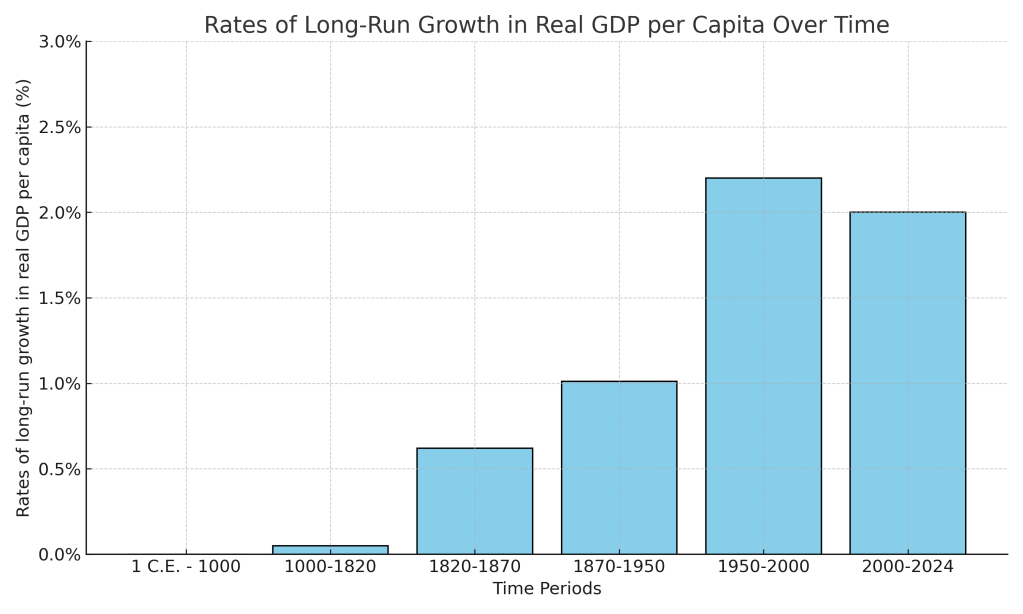

Economists typically measure economic growth by the rate of increase in real GDP per capita. The following figure, updated from Chapter 11 of Macroeconomics (Chapter 21 of Economics), shows the slow pace of growth in real GDP per capita in the world economy from the year 1 to the year 1820 and the much faster rates of growth over the following periods. As discussed in Chapter 11, the figure relies on data compiled by Angus Maddison of University of Groningen in the Netherlands and—for recent years—data from the World Bank.

This year’s three Nobelists have contributed to understanding why economic growth accelerated sharply in the nineteenth century and why England was the first country to experienced sustained increases in real GDP per capita—an event labeled the Industrial Revolution. Joel Mokyr of Northwestern University has conducted decades of research into which innovations were crucial to economic growth and the institutional and economic advantages that allowed entrepreneurs in England to use those innovations to expand production much more rapidly than had happened before. Philippe Aghion of Collège de France and INSEAD and Peter Howitt of Brown University have focused on formally modeling the process of creative destruction that underlies sustained economic growth. The classic discussion of creative destruction appears in Joseph Schumpeter’s book Capitalism, Socialism, and Democracy, published in 1942.

In Macroeconomics Chapter 21, we discuss the process of creative destruction in the context of economic growth. Creative destruction occurs as technological change results in new products that drive firms producing older products out of business. Examples are automobiles driving out of business producers of horse-drawn carriages in the early twentieth century. Or Netflix and other movie streaming sites driving video rental stores out of business in more recent years.

The Nobel Committee’s announcement of the prize can be found here. A longer discussion of the Nobelists’ work can be found here. The scope of their research can be seen by reviewing their curricula vitae, which can be found here, here, and here. The amount of the prize this years is 11 million Swedish kronor (about $1.2 million). Mokyr receives half and Aghion and Howitt receive the other half.

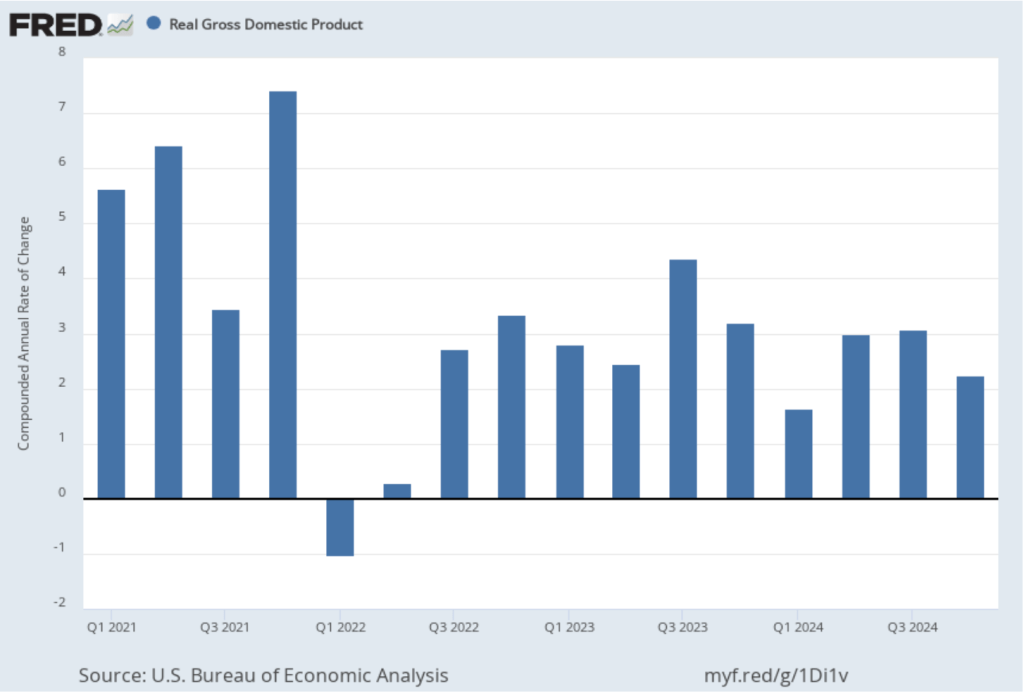

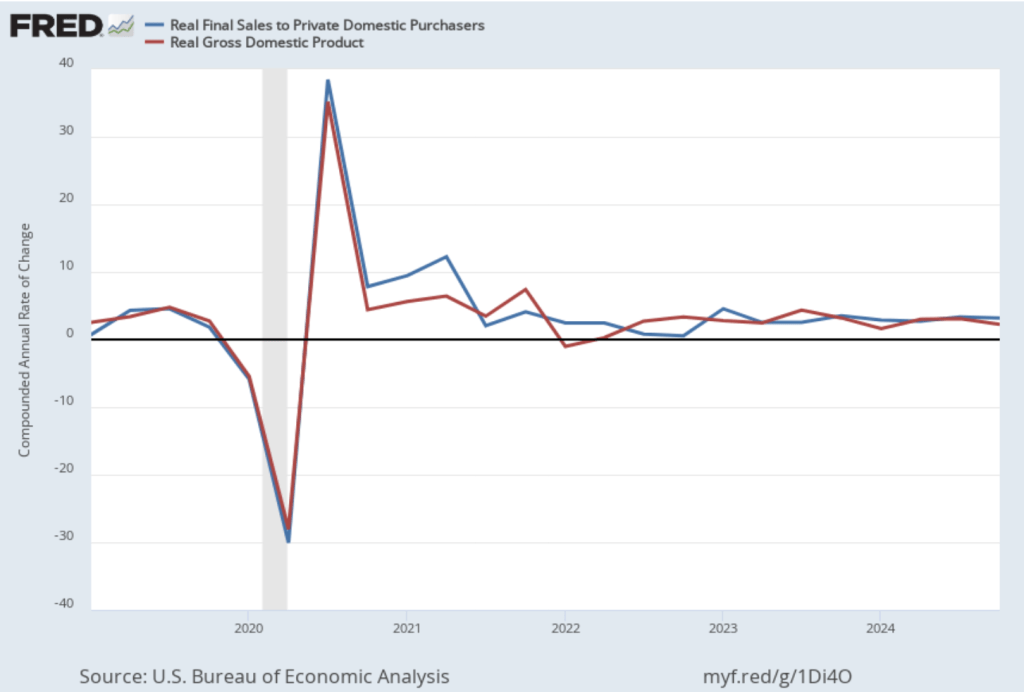

Today (January 30), the Bureau of Economic Analysis (BEA) released its advance estimate of GDP for the fourth quarter of 2024. (The report can be found here.) The BEA estimates that real GDP increased at an annual rate of 2.3 percent in the fourth quarter—October through December. That was down from the 3.1 percent increase in real GDP in the third quarter. On an annual basis, real GDP grew by 2.5 percent in 2024, down from 3.2 percent in 2023. A 2.5 percent growth rate is still well above the Fed’s estimated long-run annual growth rate in real GDP of 1.8 percent. The following figure shows the growth rate of real GDP (calculated as a compound annual rate of change) in each quarter since the first quarter of 2021.

Personal consumption expenditures increased at an annual rate of 4.2 percent in the fourth quarter, while gross private domestic investment fell at a 5.6 annual rate. As we discuss in this blog post, Fed Chair Jerome Powell’s preferred measure of the growth of output is growth in real final sales to private domestic purchasers. This measure of production equals the sum of personal consumption expenditures and gross private fixed investment. By excluding exports, government purchases, and changes in inventories, final sales to private domestic purchasers removes the more volatile components of gross domestic product and provides a better measure of the underlying trend in the growth of output.

The following figure shows growth in real GDP (the blue line) and in real final sales to private domestic purchasers (the red line) with growth measured as compound annual rates of change. Measured this way, in the fourth quarter of 2024, real final sales to private domestic producers increased by 3.2 percent, well above the 2.3 percent increase in real GDP. Growth in real final sales to private domestic producers was down from 3.4 percent in the third quarter, while growth in real GDP was down from 3.1 percent in third quarter. Overall, using Powell’s preferred measure, growth in production seems strong.

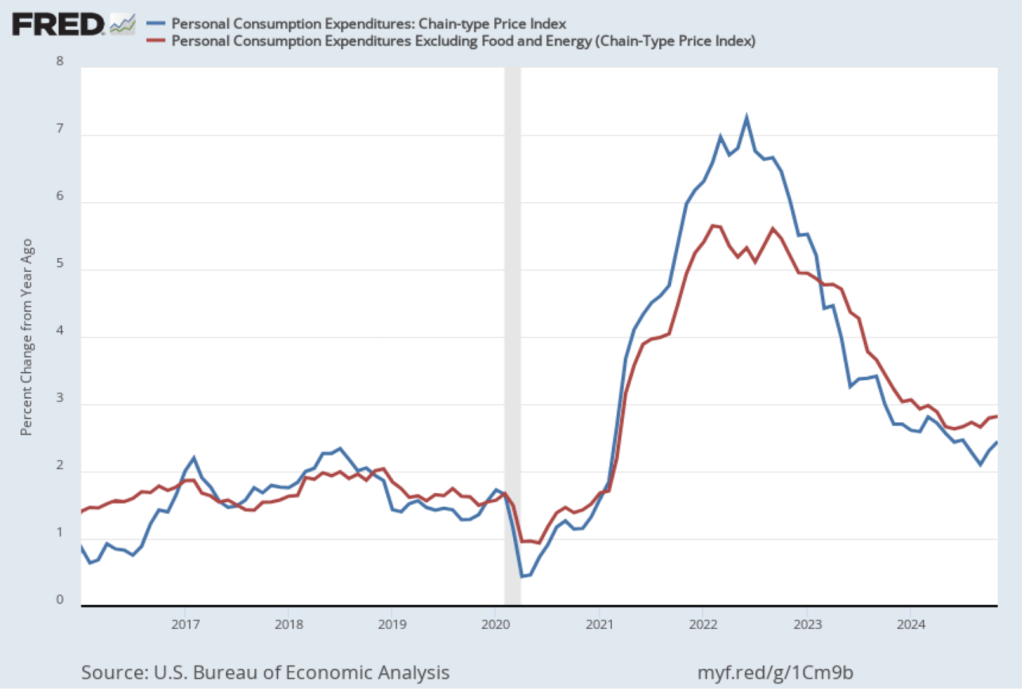

This BEA report also includes data on the private consumption expenditure (PCE) price index, which the FOMC uses to determine whether it is achieving its goal of a 2 percent inflation rate. The following figure shows inflation as measured using the PCE (the blue line) and the core PCE (the red line)—which excludes food and energy prices—since the beginning of 2016. (Note that these inflation rates are measured using quarterly data and as percentage changes from the same quarter in the previous year to match the way the Fed measures inflation relative to its 2 percent target.) Inflation as measured by PCE was 2.4 percent, up slightly from 2.3 percent in the third quarter. Core PCE, which may be a better indicator of the likely course of inflation in the future, was 2.8 percent in the fourth quarter, unchanged since the third quarter. As has been true of other inflation data in recent months, these data show that inflation has declined greatly from its mid-2022 peak while remaining above the Fed’s 2 percent target.

This latest BEA report doesn’t change the consensus view of the overall macroeconomic situation: Production and employment are growing at a steady pace, while inflation remains stubbornly above the Fed’s target.

Treasury Secretary nominee Scott Bessent. (Photo from Progect Syndicate.)

By setting an ambitious 3% growth target, U.S. Treasury Secretary nominee Scott Bessent has provided the Trump administration a North Star to follow in devising its economic policies. The task now is to focus on productivity growth and avoiding any unforced errors that would threaten output.

U.S. Treasury Secretary nominee Scott Bessent is right to emphasize faster economic growth as a touchstone of Donald Trump’s second presidency. More robust growth not only implies higher incomes and living standards—surely the basic objective of economic policy—but also can reduce America’s yawning federal budget deficit and debt-to-GDP ratio, and ease the sometimes difficult trade-offs across defense, social, and education and research spending.

But faster growth must be more than just a wish. Achieving it calls for a carefully constructed agenda, based on a recognition of the channels through which economic policies can raise or reduce output. While a pro-investment tax policy might boost capital accumulation, productivity, and GDP, higher interest rates from deficit-financed tax or spending changes might have the opposite effect. Similarly, since growth in hours worked is a component of growth in output or GDP, the new administration should avoid anti-work policies that hinder full labor-force participation, as well as sudden adverse changes to legal immigration.

While recognizing that some policy shifts that increase output might adversely affect other areas of social interest (such as the distribution of income) or even national security, policymakers should focus squarely on increasing productivity. The three pillars of any productivity policy are support for research, investment-friendly tax provisions, and more efficient regulation.

Ideas drive prospects in modern economies. Basic research in the sciences, engineering, and medicine power the innovation that advances technology, improvements in business organization, and gains in health and well-being. It makes perfect sense for the federal government to support such research. Since private firms cannot appropriate all the gains from their own outlays for basic research, they have less of an incentive to invest in it. Moreover, government support in this area produces valuable spillovers, as demonstrated by the earlier Defense Department research expenditures that became catalysts for today’s digital revolution.

This being the case, cuts in federal support for basic research are inconsistent with a growth agenda. Still, policymakers should review how research funds are distributed to ensure scientific merit, and they should encourage a healthy dose of risk-taking on newer ideas and researchers.

In addition to encouraging commercialization of spillovers from basic research and defense programs, federal support for applied research centers around the country would accelerate the dissemination of new productivity-enhancing technologies and ideas. Such centers also tend to distribute the economy’s prosperity more widely, by making new ideas broadly accessible—as agricultural- and manufacturing-extension services have done historically.

To address the second pillar of productivity growth, the administration should seek to extend the pro-investment provisions of the Tax Cuts and Jobs Act that Trump signed into law in 2017. While the TCJA’s lower tax rates on corporate profits remain in place, the expensing of business investment – a potent tool for boosting capital accumulation, productivity, and incomes – was set to be phased out over the 2023-26 period. This provision could be restored and made permanent by reducing spending on credits under the Inflation Reduction Act, or by rolling back the spending – such as $175 billion to forgive student loans – associated with outgoing President Joe Biden’s executive orders.

If the new administration wanted to go further with tax policy, it could build on the 2016 House Republican blueprint for tax reform that shifted the business tax regime from an income tax to a cashflow tax. By permitting immediate expensing of investment, but not interest deductions for nonfinancial firms, this reform would stimulate investment and growth, remove tax incentives that favor debt over equity, and simplify the tax system.

That brings us to the third pillar of a successful growth strategy: efficient regulation. The issue is not “more” versus “less.” What really matters for growth is how changes in regulation can improve the prospects for growth through innovation, investment, and capital allocation, while focusing on trade-offs in risks. Those shaping the agenda should start with basic questions like: Why can’t we build better infrastructure faster? Why can’t capital markets and bank lending be nimbler? Not only do such questions identify a specific goal; they also require one to identify trade-offs.

Fortunately, financial regulation under the new administration is likely to improve capital allocation and the prospects for growth, given the leadership appointments already announced at the Securities and Exchange Commission and the Federal Reserve. But policymakers also will need to improve the climate for building infrastructure and enhancing the country’s electricity grids to support the data centers needed for generative artificial intelligence. This will require a sharper focus on cost-benefit analysis at the federal level, as well as better coordination with state and local authorities on permitting. Using federal financial support programs as carrots or sticks can be part of such a strategy.

Bessent’s emphasis on economic growth is spot on. By setting an ambitious 3% target for annual growth, he has provided the new administration a North Star to follow in devising its economic policies.

Image generated by GTP-4o illustrating labor productivity

Several articles in the business press have discussed the recent increases in labor productivity. For instance, this article appeared in this morning’s Wall Street Journal (a subscription may be required).

The most widely used measure of labor productivity is output per hour of work in the nonfarm business sector. The BLS calculates output in the nonfarm business sector by subtracting from GDP production in the agricultural, government, and nonprofit sectors. (The definitions used by the Bureau of Labor Statistics (BLS) in estimating labor productivity are discussed in the “Technical Notes” that appear at the end of the BLS’s quarterly “Productivity and Costs” releases.) The blue line in the following figure shows the annual growth rate in labor productivity in the nonfarm business sector as measured by the percentage change from the same quarter in the previous year. The green line shows labor productivity growth in manufacturing.

As the figure shows, both labor productivity growth in the nonfarm business sector and labor productivity growth in manufacturing are volatile. The business press has focused on the growth of productivity in the nonfarm business sector during the period from the third quarter of 2023 through the third quarter of 2024. During this time, labor productivity has grown at an average annual rate of 2.5 percent. That growth rate is notably higher than the growth rate that many economists are expecting over the next 10 years. For instance, the Congressional Budget Office (CBO) has forecast that labor productivity will grow at an average annual rate of only 1.6 percent over the period from 2025 to 2034.

The CBO forecasts that the total numbers of hours worked in the economy will grow at an average annual rate of 0.5 percent. Combining that estimate with a 2.5 percent annual rate of growth of labor productivity results in output per person—a measure of the standard of living—increasing by 34 percent by 2034. If labor productivity increases at a rate of only 1.6 percent, then output per person will have increased by only 23 percent by 2034.

The standard of living of the average person in United States increasing 11 percent more would make a noticeable difference in people’s lives by allowing them to consume and save more. Higher rates of labor productivity growth leading to a faster growth rate of income and output would also increase the federal government’s tax revenues, helping to decrease federal budget deficits that are currently forecast to be historically large. (We discuss the components of long-run economic growth in Macroeconomics, Chapter 16, Section 16.7; Economics, Chapter 26, Section 26.7, and the economics of long-run growth in Macroeconomics, Chapter 11; Economics, Chapter 21.)

Can the recent growth rates in labor productivity be maintained over the next 10 years? There is an historical precedent. Labor productivity in the nonfarm business sector grew at an average annual rate of 2.6 percent between 1950 and 1973. But growth rates that high have proven difficult to achieve in more recent years. For instance, from 2008 to 2023, labor productivity grew at an average annual rate of only 1.5 percent. (We discuss the debate over future growth rates in Macroeconomics, Chapter 11, Section 11.3; Economics, Chapter 21, Section 21.3.)

The Wall Street Journal article we cited earlier provides an overview of some of the factors that may account for the recent increase in labor productivity growth rates. The 2020 Covid pandemic may have led to some increases in labor productivity. Workers who temporarily or permanently lost their jobs as businesses closed during the height of the pandemic may have found new jobs that better matched their skills, making them more productive. Similarly, businesses that were forced to operate with fewer workers, may have found ways to restore their previous levels of output with lower levels of employment. These changes may have led to one-time increases in labor productivity at some firms, but are unlikely to result in increased rates of labor productivity growth in the future.

Some businesses have used newly available generative artificial intelligence (AI) software to increase labor productivity by, for instance, using software to replace workers who previously produced marketing materials or responded to customer questions or complaints. It will take at least several years before generative AI software spreads throughout the economy, so it seems too early for it to have had a broad enough effect on the economy to be visible in the productivity data.

Note also that, as the green line in the figure above shows, manufacturing productivity has been lagging recently. From the third quarter of 2023 to the third quarter of 2024, labor productivity in manufacturing has increased at an annual average rate of only 0.4 percent. This slowdown is surprising given that over the long run productivity in manufacturing has typically increased faster than has productivity in the overall economy. It seems unlikely that labor productivity in the overall economy can sustain its recent growth rates if labor productivity growth in manufacturing continues to lag.

Finally, the productivity data are subject to revision as better estimates of output and of hours worked become available. It’s possible that what appear to be rapid rates of productivity growth during the last five quarters may turn out to have been less rapid following data revisions.

So, while the recent increase in the growth rate of labor productivity is an encouraging sign of the strength of the U.S. economy, it’s too soon to tell whether we have entered a sustained period of higher productivity growth.

Image showing scientific research generated by GTP-4o

Note: The following op-ed first appeared in the Wall Street Journal.

The Trump Economic Awakening

Traditional policies like tax cuts, targeted aid and responsible spending can deliver stronger growth.

Political scientists will debate the forces that shaped Donald Trump’s victory, but one thing is clear: Americans yearn for a change in economic policy. Voters have rejected the interventionist policies that brought inflation and high deficits. They want an economic awakening, a new way forward that uses traditional economic policies to achieve Mr. Trump’s goal of more jobs for Americans whose fortunes have been harmed by technological change and globalization.

Any economic path to a successful awakening begins with growth: the engine that powers individual income and our collective ability to support the nation’s defense, economy, education and healthcare industry. To pursue this growth, the new administration should consider at least three measures:

First, by working with Congress, it should build on the successes of the Tax Cuts and Jobs Act of 2017 to make permanent the expensing of business investment. Second, it should increase support for science and defense research, which would have significant spillover to the commercial sector, particularly in space exploration. Third, it should build on this research by constructing applied research centers around the country, linked to regional university and city hubs. Like the land-grant colleges of the 19th century, these centers would generate and distribute knowledge, improving local capabilities in manufacturing and services.

Opportunity is also a pillar of the awakening. Community colleges are an underfunded source of skill-building and mobility. As Austan Goolsbee, Amy Ganz and I proposed in a 2019 report, a modest federal block grant to support community colleges on the supply side—rather than a demand-side emphasis on financial aid—can help these schools push more Americans toward better jobs by working with local employers on skill needs and curriculum development. Targeted aid to places with depressed economic activity can help distribute opportunity to communities better than one-size-fits-all Washington-directed programs.

Corporate tax reform can play a role, too, by improving incentives for companies to settle and invest in the U.S. This can magnify opportunities for Americans, all without having to rely on costly tariffs.

Working a job doesn’t merely generate income; it also promotes human dignity. Enlisting more people into the workforce is thus another element of the economic-policy awakening. While growth and opportunity policies can boost labor-force participation, strengthening the earned-income tax credit to boost the incomes of childless workers can help attract younger people to the workforce. Maintaining the child tax credit can also provide parents with easier pathways toward economic participation.

These ideas share several important themes with Mr. Trump’s campaign and the traditional conservative playbook. They emphasize that policy ideas should be practical and workable, not merely rhetorical. Each makes use of America’s federalist system and innovative ethos. Making a priority of strong local involvement in applied research centers and community colleges and as tailoring place-based aid are more effective approaches than Washington diktats. Programs need to be held accountable for results, not simply allocated money.

This economic-policy awakening requires a clear-eyed assessment of budget trade-offs. Profligate spending with little regard for debt and inflation—à la the American Rescue Plan—contributed to Mr. Trump’s victory. It is possible to accomplish the steps above in a fiscally responsible way by offsetting spending and tax changes.

Organizing for the policy awakening’s success will be essential. Lack of communication among cabinet agencies can stymie creative ideas for expanding the economic pie for American workers. Like the president’s Working Group on Financial Markets, created by Ronald Reagan in 1988 to convene disparate agencies, the new administration would benefit from a senior executive team that can coordinate economic ideas and learn from leaders in business, labor and social services. Such a body, unlike the National Economic Council, could more adeptly cut across silos related to tax, trade, regulatory and industrial policy.

Voters have signaled they’re ready for an economic awakening. The president-elect, equipped with a new playbook and vision, should seize the opportunity.

Daron Acemoglu and Simon Johnson (Credit: Acemoglu, Adam Glanzman; Johnson, courtesy of MIT, from news.mit.edu)

James Robinson (photo from news.uchicago.edu)

Many economic studies have a relatively limited objective. For instance, estimating the price elasticity of demand for soda in order to determine the incidence of a soda tax. Or estimating a Keynesian fiscal policy multiplier in order to determine the effects of a change in federal spending or taxes. (We consider the first topic in Microeconomics, Chapter 6, and the second topic in Macroeconomics, Chapter 16.)

Other economic studies consider much broader questions, such as why are some countries rich and other countries poor? As the late Nobel laureate Robert Lucas once wrote: “The consequences for human welfare involved in questions like these are simply staggering: Once one starts to think about them, it is hard to think about anything else.”

Today, the Royal Swedish Academy of Sciences awarded the 2024 Nobel Prize in Economic Sciences to Daron Acemoglu and Simon Johnson of MIT, and to James Robinson of the University of Chicago for “for studies of how institutions are formed and affect prosperity.” Acemoglu, Johnson, and Robinson (AJR) have published work highlighting the key importance of a country’s institutions in explaining whether the country has experienced sustained economic growth. Their work builds on earlier studies by the late Douglas North of Washington University in St. Louis, who received the Nobel Prize in 1993.

The institutional approach to economic growth differs from other approaches that focus on variables such as temperature, prevalence of disease, ethnic fragmentation, resource endowments, or governments adopting flawed development strategies in explaining differences in growth rates in per capita income across countries.

Two of AJR’s most discussed papers are “The Colonial Origins of Comparative Development: An Empirical Investigation,” which was published in the American Economic Review in 2001 (free download here), “Reversal of Fortune: Geography and Institutions in the Making of the Modern World Income Distribution,” which was published in the Quarterly Journal of Economics in 2002 (available here). In these papers, the authors argue that the institutions European countries established in their colonies helped determine economic growth in those countries even decades after colonization.

As with any analysis that covers many countries over long periods of time, AJR’s analysis of the effect of colonialism on economic growth has attracted critiques focused on whether the authors have gathered data properly and whether their data may be better explained with a different approach.

The authors, writing both separately and jointly, have explored many issues beyond the effects of colonialism on economic growth. The wide scope of their research can be seen by reviewing their curricula vitae, which can be found here, here, and here. The announcement by the Nobel committee can be found here.

Glenn serves on the the Grand Bargain Committee, chaired by Michael Strain of the American Enterprise Institute and Isabel Sawhill of the Brookings Institution. The committee, whose members span the political spectrum, have prepared a report that addresses some of the country’s most pressing economic and social problems.

Glenn and Michael Strain prepared the following introduction to the report. Below there is a link to the whole report.

The views expressed in this report are those of the individual authors who collectively constitute the Grand Bargain Committee, co-chaired by Michael R. Strain and Isabel V. Sawhill. This report was sponsored by the Center for Collaborative Democracy and was prepared independent of influence from the center and from any other outside party or institution. It is being published by the Bipartisan Policy Center as an example of how people with diverse views and political leanings can find common ground. The recommendations are strictly those of the policy experts and do not necessarily reflect the views of any organization or those of the BPC. All data are current as of November 2023.

By: Eric Hanushek, G. William Hoagland, Douglas Holtz-Eakin, R. Glenn Hubbard, Maya MacGuineas, Richard V. Reeves, Robert D. Resichauer, Gerard Robinson, Isabel V. Sawhill, Diane Schanzenbach, Richard Schmalensee, Michael R. Strain, and C. Eugene Steuerle.

Introduction

The United States faces serious economic and social challenges, including:

The underlying economic growth rate has slowed, as have opportunities for people to move up the economic ladder.

Our education system fails too many children and leaves many more with fewer opportunities than they deserve.

The nation is not rising to the challenge of addressing climate change.

Both our health care system and the health of our population need improvement.

Our income tax system is broken, generating tax revenue in an inefficient and unfair manner.

And the national debt is growing at an unsustainable pace, threatening long-term economic growth, crowding out needed investments in economic opportunity, and placing the nation’s ability to respond to a future crisis at risk.

To address these problems, the Center for Collaborative Democracy commissioned subject matter experts—progressives, centrists, and conservatives—to develop a “Grand Bargain” encompassing all six issues. The policy debate typically puts these problems into silos, and within each silo, powerful forces support the status quo. This report seeks to break down these silos. Dealing with them all at once—in a Grand Bargain—is a more promising strategy than dealing with them individually, because it allows for different parties to strike deals across policy issues, not just within a single issue.

For example, implementing a carbon tax to address climate change seems impossibly difficult. So does increasing accountability for teacher performance. Trading one for the other might be easier than pursuing both in isolation. Fixing the structural budget deficit by reducing entitlement spending is an enormous political challenge. So is increasing spending on programs that advance economic opportunity. Doing both at the same time could be more politically feasible than addressing them separately.

In this context, the group of experts met for several months in 2023 to share perspectives and ideas and to come up with sensible policies in each of these areas: economic growth and mobility; education; environment; health; taxes; and the federal budget. The end result is this report, which is being published by the Bipartisan Policy Center as an example of how people with diverse views and political leanings can find common ground.

This report is short, consisting of less than 30 pages of text. Its brevity is by design. This constraint forced the group to stay focused on issues and recommendations that matter the most. The focus of the report is on concepts. It is designed to answer such questions as, “How should the nation’s approach to education or to the federal budget change? What fundamental reforms are required to increase the underlying rates of economic growth and upward mobility?” Focusing on concepts means not focusing on policy details, including the details of implementing our recommendations and of transitioning across policy regimes. Our lack of attention to policy details does not mean we do not recognize their importance. Of course, we do, and many members of the group have spent much of their careers studying and designing public policies. Instead, we focus on concepts because we believe the United States needs to return to a discussion of first principles. This report advances that objective.

Not every member of the group agrees with every recommendation in this report. That is not surprising given the diversity of views in the group, and the difficulty and complexity of many of the issues we address. Despite this disagreement, we were able to have an informed and constructive discussion about these economic issues, to find compromises, and to come up with a set of recommendations that we believe, on balance, would greatly strengthen the country and improve people’s lives.

We believe in the importance of a market economy. Free markets have led to unprecedented growth and innovation, along with rising incomes, over the past three centuries. But government also has a role to play. To unleash more growth, we need to curtail unneeded or overly costly regulations and to create a tax system that encourages investment spending and innovation. To bring prosperity to more people, we need policies that will enable more people to benefit from economic growth through investment in their education and skills. For this reason, we put a great deal of emphasis on improving education for children, on training or retraining for adult workers, and on subsidizing the earnings of low-wage workers when necessary while maintaining a safety net for those who cannot work.

Our proposals are designed to advance certain underlying values and themes: Work and savings should be rewarded, investment should be encouraged over consumption, public assistance should be better targeted to those most in need, the tax system should be more progressive, and the nation should invest relatively more in the young and spend relatively less on the elderly.

Our specific proposals in each area are as follows:

On economic growth and mobility, we recommend investing in the education and training of workers, through community colleges and apprenticeships. We call for a more skill-based immigration system and for more immigrants; for encouraging innovation by investing more in basic research; for reducing taxes on new investment; for curbing unneeded regulation; for reducing the national debt; and for encouraging participation in economic life by increasing the generosity of earnings subsidies for low-wage workers.

On education, we recommend improving the teacher workforce at the K-12 level; paying teachers more but strengthening the link between pay and performance; maintaining educational standards and accountability while narrowing gaps by race and class; expanding school choice; and recognizing the role that parents and families must play in students’ learning.

On the environment, our main recommendation is to adopt a carbon tax. We also call for reducing methane emissions; expanding federal authority in the planning, siting, and permitting of the national electric transmission system; and repealing the renewable fuel standard that requires refiners to blend corn ethanol into the fuel they sell.

On health, we call for giving more attention to the social determinants of poor health with a focus on the need for better nutrition, for rationalizing existing subsidies for health care, and for reducing health care costs.

On taxes, we call for increasing tax revenue as a share of annual gross domestic product (GDP), and for that revenue to be raised in a manner that is more progressive, efficient, and simple than under current law, while also increasing the incentive to save and invest. For the business sector, that means allowing the expensing of investment expenditures and moving toward equal treatment of the corporate and noncorporate sectors.

On the federal budget, we recommend putting the debt as a share of annual GDP on a sustainable trajectory with a comprehensive package of reforms made up of a rough balance between tax increases and spending cuts in the initial years, phasing into a much larger share of the savings coming from spending cuts over time.

Most of these recommendations are at the federal level, but some are at the state and local level, particularly our education recommendations.

In the spirit of a Grand Bargain, these recommendations advance common goals and values through compromises both within and across policy areas. For example, one of our values is reflected in the goal of refocusing government spending on those who truly need it, and another is to restore fiscal responsibility. To accomplish this, we call for slower growth in Social Security and Medicare benefits for affluent seniors to reduce the major driver of the national debt, but we also protect vulnerable seniors and spend more on the education of children and on earnings subsidies for the working poor. We recommend adopting a carbon tax because it will simultaneously advance our goals of supporting the environment, increasing tax revenue, and boosting dynamism by encouraging innovation in the energy sector.

We believe the analysis and recommendations in this report point a path forward for the nation, but we offer them in a spirit of humility, understanding that others will disagree. We hope that this report catalyzes a much needed debate about the future of our nation.

Glenn discusses Fed policy, the state of the U.S economy, economic growth, China in the world economy, industrial policy, protectionism, and other topics in this episode of the Political Economy podcast from the American Enterprise Institute.

This op-ed orginally appeared in the Wall Street Journal.

Put Growth Back on the Political Agenda

In a campaign season dominated by the past, a central economic topic is missing: growth. Rapid productivity growth raises living standards and incomes. Resources from those higher incomes can boost support for public goods such as national defense and education, or can reconfigure supply chains or shore up social insurance programs. A society without growth requires someone to be worse off for you to be better off. Growth breaks that zero-sum link, making it a political big deal.

So why is the emphasis on growth fading? More than economics is at play. While progress from technological advances and trade generally is popular, the disruption that inevitably accompanies growth and hits individuals, firms and communities has many politicians wary. Such concerns can lead to excessive meddling via industrial policy.

As we approach the next election, the stakes for growth are high. Regaining the faster productivity that prevailed before the global financial crisis requires action. The nonpartisan Congressional Budget Office estimates potential gross domestic product growth of 1.8% over the coming decade, and somewhat lower after that. Those figures are roughly 1 percentage point lower than the growth rate over the three decades before the pandemic. Many economists believe productivity gains from generative artificial intelligence can raise growth in coming decades. But achieving those gains requires an openness to change that is rare in a political climate stuck in past grievances about disruption—the perennial partner of growth.

Traditionally, economic policy toward growth emphasized support for innovation through basic research. Growth also was fostered by reducing tax burdens on investment, streamlining regulation (which has proliferated during the Biden administration) and expanding markets. These important actions have flagged in recent years. But such attention, while valuable, masks inattention to adverse effects on some individuals and communities, raising concerns about whether open markets advance broad prosperity.

This opened a lane for backward-looking protectionism and industrial policy from Democrats and Republicans alike. Absent strong national-defense arguments (which wouldn’t include tariffs on Canadian steel or objections to Japanese ownership of a U.S. steel company), protectionism limits growth. According to polls by the Chicago Council on Global Affairs, roughly three-fourths of Americans say international trade is good for the economy. Finally, protectionism belies ways in which gains from openness may be preserved, such as by simultaneously offering support for training and work for communities of individuals buffeted by trade and technological change.

On industrial policy, it is true that markets can’t solve every allocation problem. But such concerns underpin arguments for greater federal support of research for new technologies in defense, climate-change mitigation, and private activity, not micromanaged subsidies to firms and industries. If a specific defense activity merits assistance, it could be subsidized. These alternatives mitigate the problems in conventional industrial policy of “winner picking” and, just as important, the failure to abandon losers. It is policymakers’ hyperattention to those buffeted by change that hampers policy effectiveness and, worse, invites rent-seeking behavior and costly regulatory micromanagement.

Examples abound. Appending child-care requirements to the Chips Act and the inaptly named Inflation Reduction Act has little to do with those laws’ industrial policy purpose. The Biden administration’s opposition to Nippon Steel’s acquisition of U.S. Steel raises questions amid the current wave of industrial policy. How is a strong American ally’s efficient operation of an American steel company with U.S. workers an industrial-policy problem? Flip-flops on banning TikTok fuel uncertainty about business operations in the name of industrial policy.

The wrongly focused hyperattention is supposedly grounded in putting American workers first. But it raises three problems. First, the interventions raise the cost of investments, and the jobs they are to create or protect, by using mandates and generating policy uncertainty. Second, they contradict the economic freedom in market economies of voluntary transactions. Absent a strong national-security foundation, why is public policy directing investment in or ownership of assets? Such policies threaten the nation’s long-term prosperity by discouraging investment and invite rent-seeking in a way that voluntary market transactions don’t. Both problems hamstring growth.

Third, and perhaps most important, such micromanagement misses the economic and political mark of actually helping individuals and communities disrupted by growth-enhancing openness. A more serious agenda would focus on training suited to current markets (through, for example, more assistance to community colleges), on work (through expanding the Earned Income Tax Credit), and on aid to communities hit by prolonged employment loss (through services that enhance business formation and job creation). The federal government could also establish research centers around the country to disseminate ideas for businesses.

Growth matters—for individual livelihoods, business opportunities and public finances. Pro-growth policies that account for disruption’s effects while encouraging innovation, saving, capital formation, skill development and limited regulation must return to the economic agenda. A shift to prospective, visionary thinking would reorient the bipartisan, backward-looking protectionism and industrial policy that weaken growth and fail to address disruption.

Glenn participated in this session hosted by the Society of Policy Modeling and the American Economic Association of Economic Educators and moderated by Dominick Salvatore of Fordham University. (Link to the page for this session in the ASSA program.)

Also making presentations at the session were Robert Barro of Harvard University, Janice Eberly of Northwestern University, Kenneth Rogoff of Harvard University, and John Taylor of Stanford University.

Here is the abstract for Glenn’s presentation:

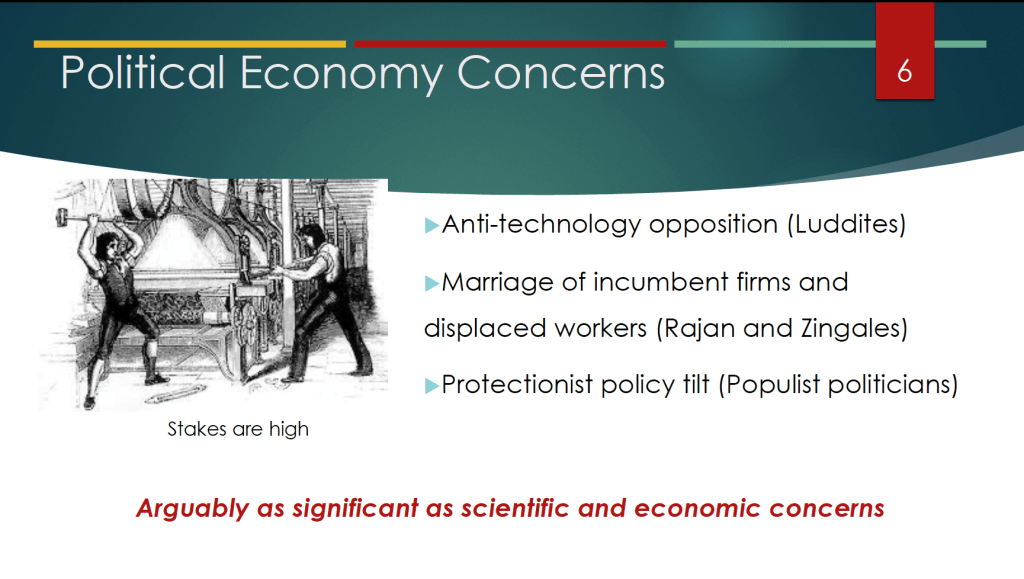

Economic growth is foundational for living standards and as an objective for economic policy. The emergence of Artificial Intelligence as a General Purpose Technology, on the one hand, and a number of demographic and budget challenges, on the other hand, generate an unusually wide range of future economic outcomes. I focus on key ‘policy’ and ‘political economy’ considerations that increase the likelihood of a more favorable growth path given pre-existing trends and technological possibilities. By ‘policy,’ I consider mechanisms enabling growth through research, taxation, the scope of regulation, and competition. By ‘political economy’ factors, I consider mechanisms to increase economic participation in support of growth and policies that enhance it. I argue that both sets of mechanisms are necessary for a viable pro-growth economic policy framework.

These slides from the presentation highlight some of Glenn’s key points. (Note the cover of the new 9th edition of the textbook in slide 7!)