Image generated by ChatGPT

This morning (July 2)—one day early because tomorrow is a federal holiday—the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for June. The report showed a smaller than expected increase in employment.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

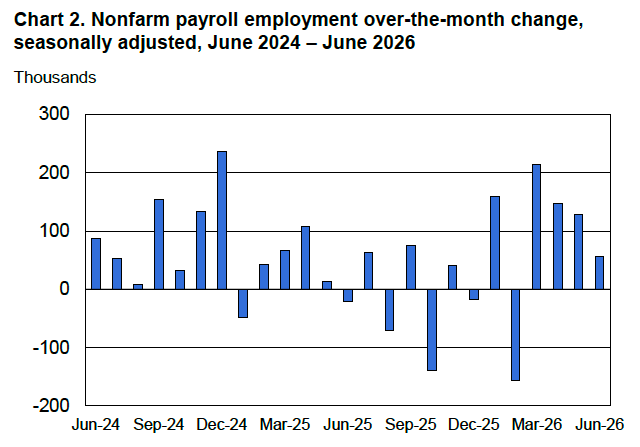

According to the establishment survey, there was a net increase of 57,000 nonfarm jobs during June. Economists surveyed by the Wall Street Journal had forecast an increase of 115,000 jobs. Economists surveyed by FactSet had a lower forecast of a net increase of 100,000 jobs. The BLS revised downward its previous estimates of employment in April and May by a combined 74,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”)

The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years. The figure shows that the relatively strong 137,000 average net increase in jobs over the past four months represents a break from the unusual pattern in that began in the middle of 2025 in which months of declining employment and months of increasing employment had been alternating.

These employment gains conflict with a popular view among economists that slowing labor force growth has driven the break-even rate of employment growth—the rate required to keep the unemployment rate constant—down to nearly zero

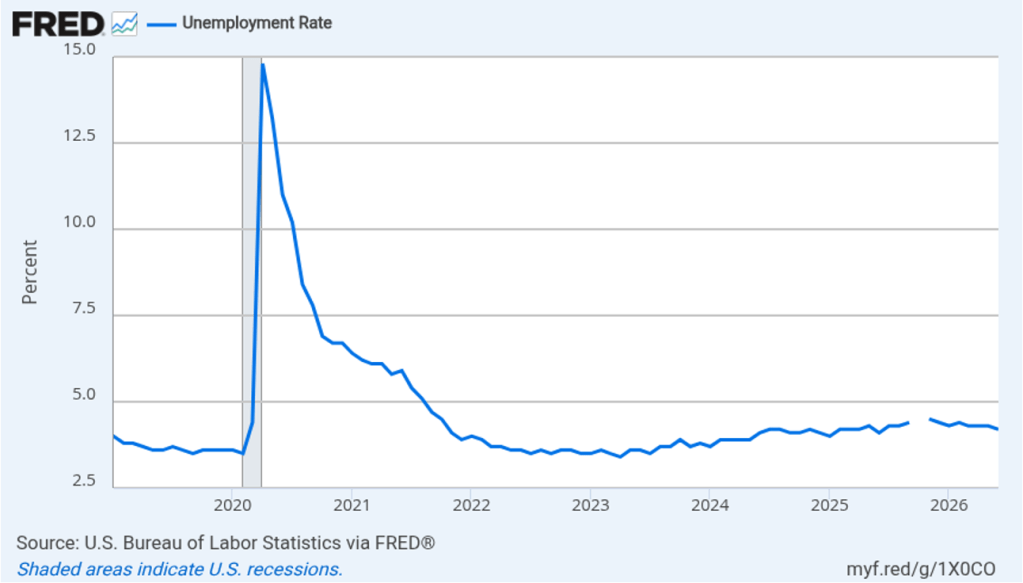

Despite the relatively small increase in employment in June, the unemployment rate, which is calculated from data in the household survey, declined to 4.2 percent from 4.3 percent in May at 4.3. The decline in the unemployment rate was due to a decline in the estimated size of the labor force, an estimate that fluctuates significantly from month to month. Despite that fact, as the following figure shows, the unemployment rate has been remarkably stable over the past year and a half, staying between 4.0 percent and 4.4 percent in each month since May 2024. The Federal Open Market Committee’s current estimate of the natural rate of unemployment—the normal rate of unemployment over the long run—is 4.2 percent. So, currently the unemployment rate is equal to that estimate of the natural rate. (We discuss the natural rate of unemployment in Macroeconomics, Chapter 9 and Economics, Chapter 19.)

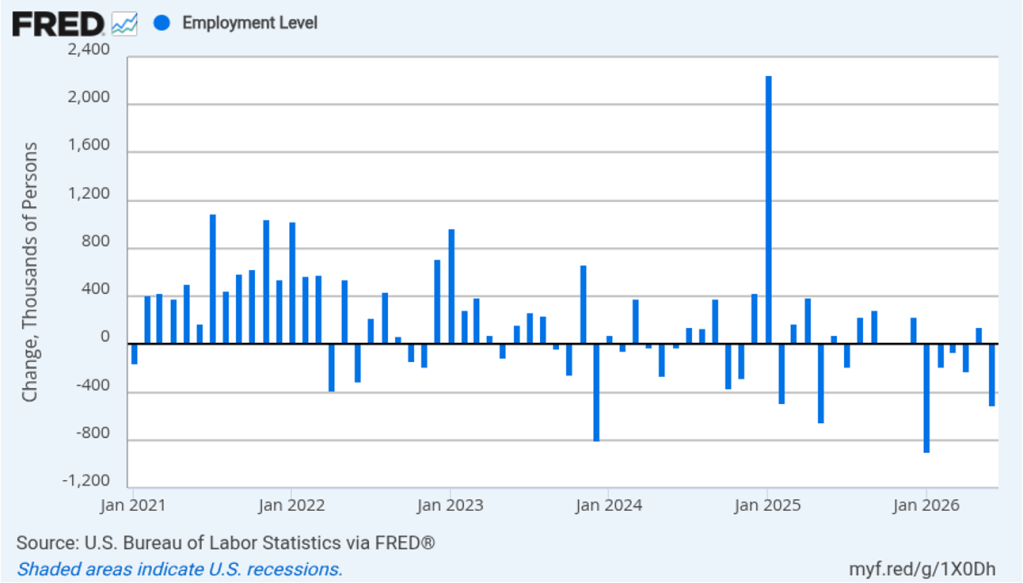

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net decrease of 507,000 jobs in June, as compared to the net increase in employment shown in the establishment survey. In addition, the household survey shows a significant net decline in jobs during the past six months, in contrast to the significant net increase in jobs shown in the establishment survey. (Note that because of last year’s shutdown of the federal government, there are no data for October or November.)

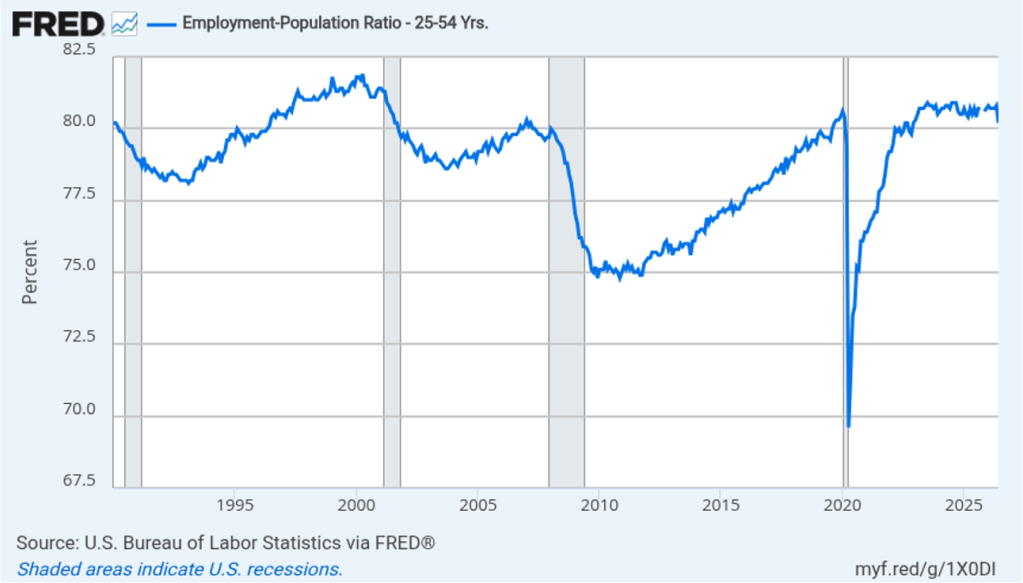

The household survey has another important labor market indicator: the employment-population ratio for prime age workers—those workers aged 25 to 54. In June. the ratio declined sharply to 80.2 percent from 80.8 percent in May, the lowest value since December 2022. The decline in the prime-age population ratio is difficult to reconcile with the net increase in employment shown in the payroll survey. The state of the labor market in June seemed significantly weaker in household survey data than in establishment survey data.

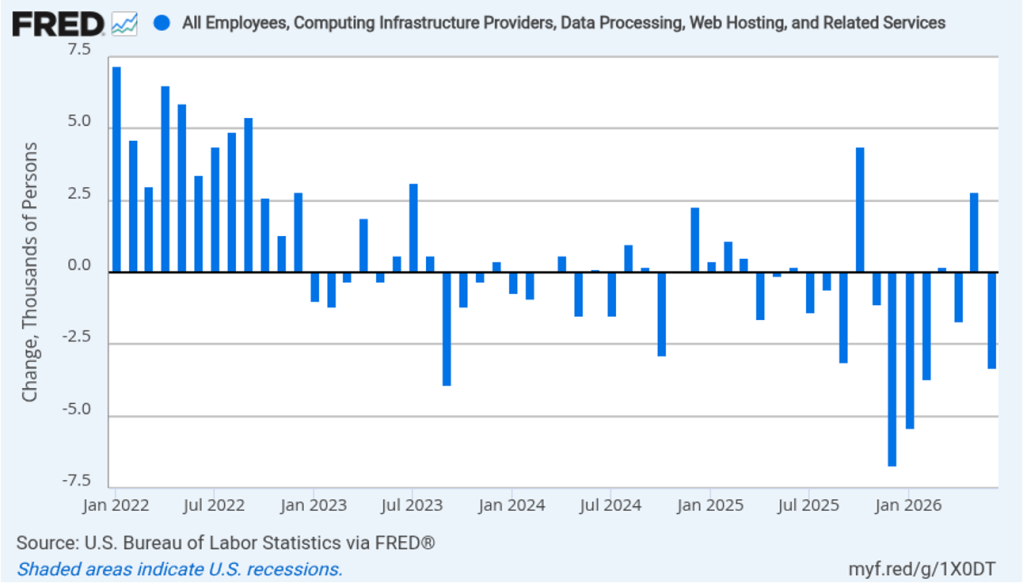

There have been media reports of firms, including Salesforce, Cloudflare, Coinbase, Cisco Systems, and Meta Platforms, laying off workers in information systems. The following figure shows net employment changes in the BLS employment category of “computing infrastructure providers, data processing, web hosting, and related services.” Employment in this sector has been declining during most months since the beginning of 2023. June was no exception with a net decrease of 3,300 jobs.

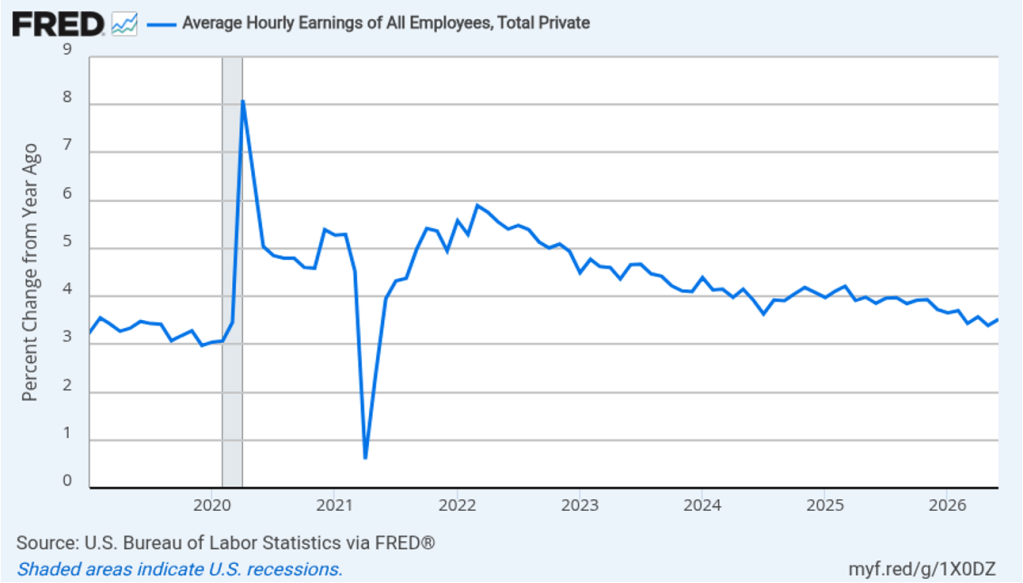

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.5 percent in June, up slightly from 3.4 percent in May.

What effect is this jobs report likely to have on the decisions of the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) at its next meeting on July 28–19? The slowdown in employment growth reduces the chance that the FOMC will increase its target range for the federal funds rate. The probability that investors in the federal funds futures market assign to the FOMC increasing its target range at that meeting fell from 28.9 percent yesterday to 17.6 percent this morning. Investors still assign a 54.0 percent probability to the FOMC raising its target range at its September meeting, but that was down from 64.1 percent yesterday.