Fed Chair Kevin Warsh and colleagues discuss policy at the June FOMC meeting (Photo from federalreserve.gov.)

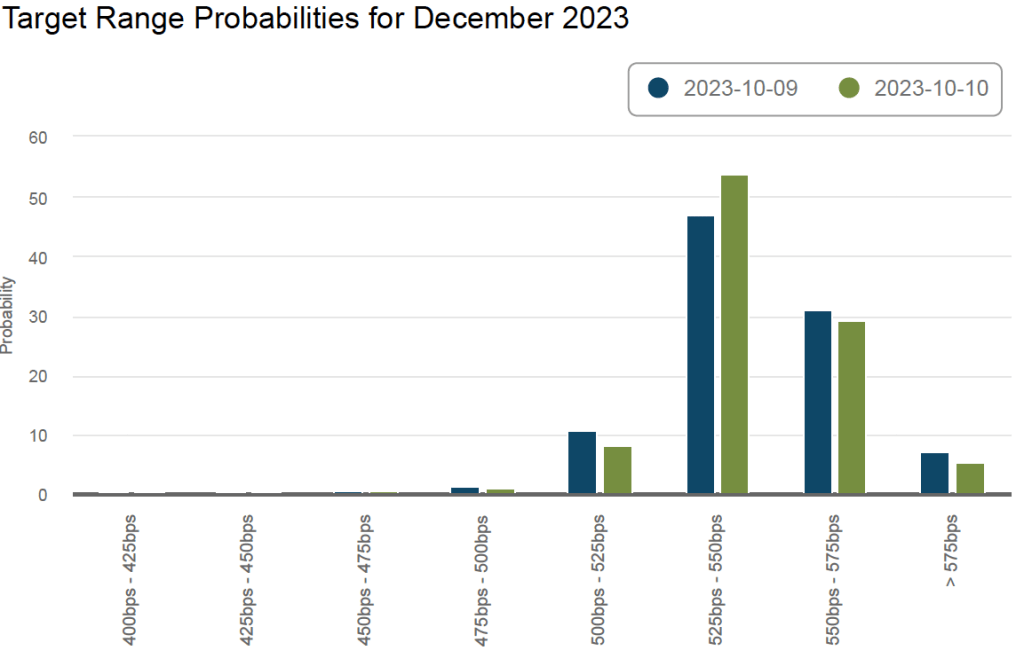

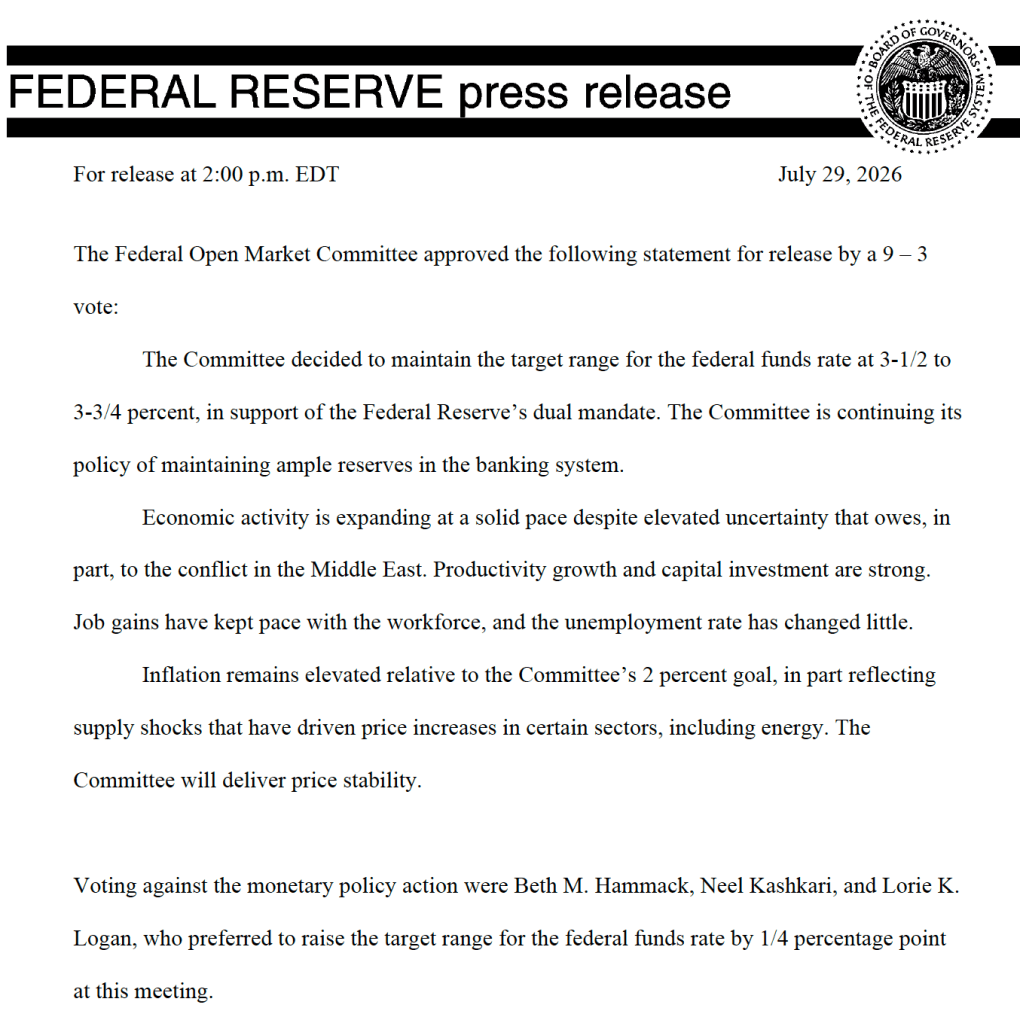

There was some uncertainty as to whether at its meeting that ended today, the Federal Open Market Committee (FOMC) would leave unchanged its target range for the federal funds rate at 3.50 percent to 3.75 percent. As of yesterday, trading in the federal funds rate futures market had given a 31 percent probability to the committee raising its target by 0.25 percentage points (25 basis points). The committee voted 9–3 to keep the target range unchanged, with Beth Hammack, president of the Federal Reserve Bank of Cleveland, Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, and Lorie Logan, president of the Federal Reserve Bank of Dallas, voting to raise the target range by 25 basis points.

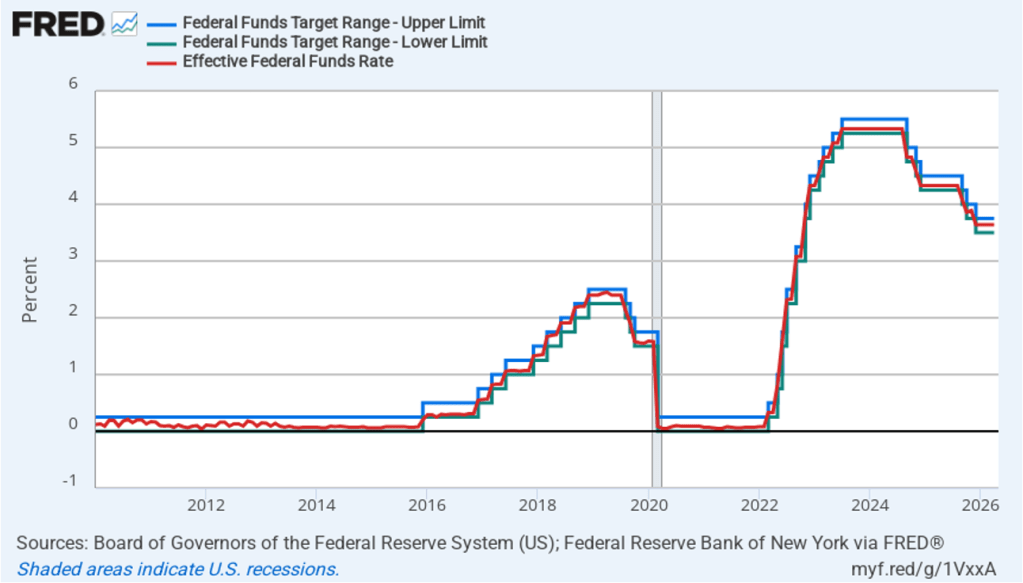

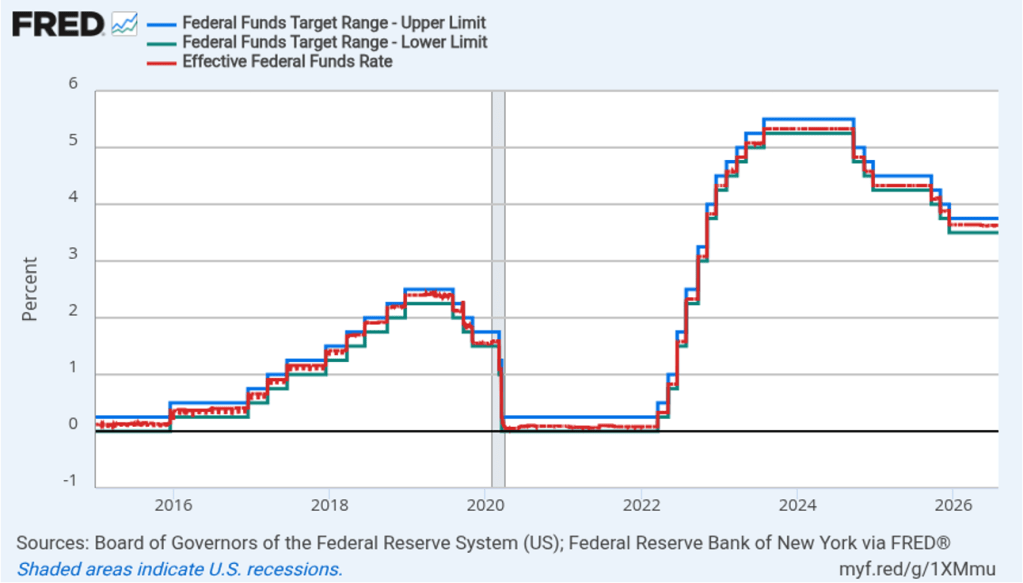

The FOMC has left its target for federal funds rate unchanged since lowering it by 25 basis points on December 10 of last year. The following figure shows for the period since January 2015, the upper bound (the blue line) and the lower bound (the green line) for the FOMC’s target range for the federal funds rate, as well as the actual values for the federal funds rate (the red line). Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate within its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

As with the policy statement issued following Fed Chair Kevin Warsh’s first FOMC meeting in June, today’s policy statement was short and did not include any discussion of the circumstances under which policy might change in the future—so-called forward guidance. We discuss forward guidance in Macroeconomics, Chapter 15 (Economics, Chapter 25).

In his press conference following the meeting, Warsh expanded on his approach to monetary policy, highlighting differences with previous Fed chairs. He noted that he believed that FOMC policy statements should present “just the facts,” providing only a brief summary of current economic conditions and avoiding mention of future monetary policy apart from the assertion—which also closed the policy statement following the June meeting—that “The Committee will deliver price stability.”

He stressed that the committee was in the process of reassessing its approach to monetary policy. The reassessment will rely in part on the findings of the five committees he has formed, although he noted that the FOMC would not feel bound by the recommendations of the five committees. He emphasized that the committee would focus more on trends in economic data and wouldn’t be “holding our breath” waiting for any particular data release. In reply to questions from reporters, he noted that despite the committee leaving its target for the federal funds rate unchanged, there hadn’t been a “pause” in policy because the committee had continued its “rigorous review of big, hard questions.”

Warsh noted that by avoiding forward guidance, the committee wasn’t attempting to surprise financial markets when at some point it announces a policy change. Instead, he argued that prices in financial markets would now better reflect the opinions of market participants, which will provide the committee with useful information.

On two issues, Warsh noted continuity with committee procedures under previous Fed chairs. First, at his June press conference, Warsh had indicated that he would only hold press conferences after FOMC meetings if there was new information to convey. Today, he stated that, through at least the end of the year, he would continue the recent tradition of holding a press conference after each FOMC meeting. Second, when asked about his statements that new measures of inflation were needed, Warsh indicated that, at least through the end of the year, the committee would continue to measure progress toward its 2 percent annual inflation goal using the inflation rate as measured by the personal consumption expenditures (PCE) price index.

Finally, this afternoon, investors in the federal funds rate futures market assigned a 63.4 percent probability to the committee increasing its target range by 25 basis points at its next meeting on September 15–16, a decrease from 76.0 percent yesterday.