Senator Elizabeth Warren (Photo from the Associated Press)Lawrence Summers (Photo from harvardmagazine.com)

As we’ve discussed in several previous blog posts, in early 2021 Lawrence Summers, professor of economics at Harvard and secretary of the treasury in the Clinton administration, argued that the Biden administration’s $1.9 trillion American Rescue Plan, enacted in March, was likely to cause a sharp acceleration in inflation. When inflation began to rapidly increase, Summers urged the Federal Reserve to raise its target for the federal funds rate in order to slow the increase in aggregate demand, but the Fed was slow to do so. Some members of the Federal Open Market Committee (FOMC) argued that much of the inflation during 2021 was transitory in that it had been caused by lingering supply chain problems initially caused by the Covid–19 pandemic.

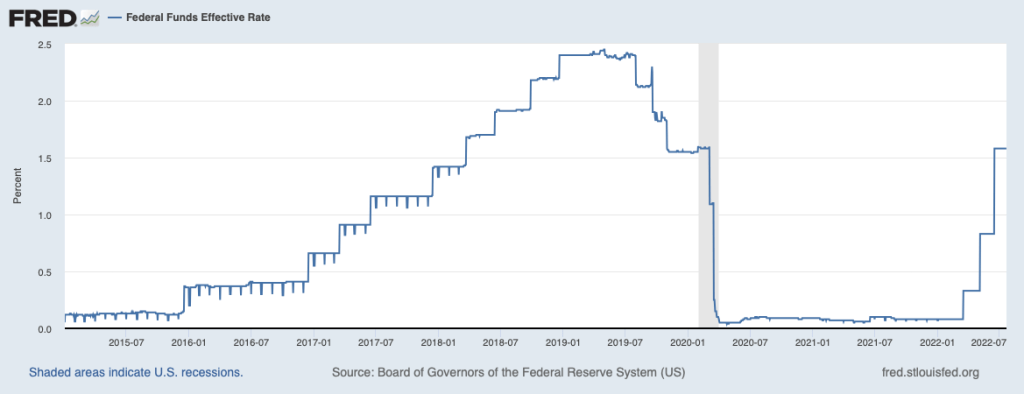

At the beginning of 2022, most members of the FOMC became convinced that in fact increases in aggregate demand were playing an important role in causing high inflation rates. Accordingly, the FOMC began increasing its target for the federal funds rate in March 2022. After two more rate increases, on the eve of the FOMC’s meeting on July 26–27, the federal funds rate target was a range of 1.50 percent to 1.75 percent. The FOMC was expected to raise its target by at least 0.75 percent at the meeting. The following figure shows movements in the effective federal funds rate—which can differ somewhat from the target rate—from January 1, 2015 to July 21, 2022.

In an opinion column in the Wall Street Journal, Massachusetts Senator Elizabeth Warren argued that the FOMC was making a mistake by increasing its target for the federal funds rate. She also criticized Summers for supporting the increases. Warren worried that the rate increases were likely to cause a recession and argued that Congress and President Biden should adopt alternative measures to contain inflation. Warren argued that a better approach to dealing with inflation would be to, among other steps, increase the federal government’s support for child care to enable more parents to work, provide support for strengthening supply chains, and lower prescription drug prices by allowing Medicare to negotiate the prices with pharmaceutical firms. She also urged a “crack down on price gouging by large corporations.” (We discussed the argument that monopoly power is responsible for inflation in this blog post.)

Summers responded to Warren in a Twitter thread. He noted that: “In the 18 months since the massive stimulus policies & easy money that [Senator Warren] has favored & I have opposed, the inflation rate has risen from below 2 to above 9 percent & workers purchasing power has, as a consequence, declined more rapidly than in any year in the last 50.” And “[Senator Warren] opposes restrictive monetary policy or any other measure to cool off total demand. Why does she think at a time when there are twice as many vacancies as jobs that inflation will come down without some drop in total demand?”

Clearly, economists and policymakers continue to hotly debate monetary policy.

Source: Elizabeth Warren, “Jerome Powell’s Fed Pursues a Painful and Ineffective Inflation Cure,” Wall Street Journal, July 24, 2022.

Photo of the Port of Los Anglese from the Wall StreetJournal.

In economics, index numbers play an important role in gauging the state of the economy. For instance, rather than measure inflation by looking at the price of one or a few goods and services, we use the consumer price index (CPI), which combines the prices of many goods and services into a single number. (In Macroeconomics, Chapter 9, Section 9.4 and Economics, Chapter 19, Section 19.4, we discuss how the Bureau of Labor Statistics constructs the consumer price index.) Similarly, the S&P 500 provides an index of stock prices and the Federal Reserve compiles an index of industrial production that measures the output of factories, mines, and utilities.

The advantage of indexes is that they provide broader measures of an economic variable. Important as the price of gasoline is in the average family’s budget, the prices of food, clothing, and other goods and services are also important. So, the CPI is a better measure of inflation than is just the price of gasoline.

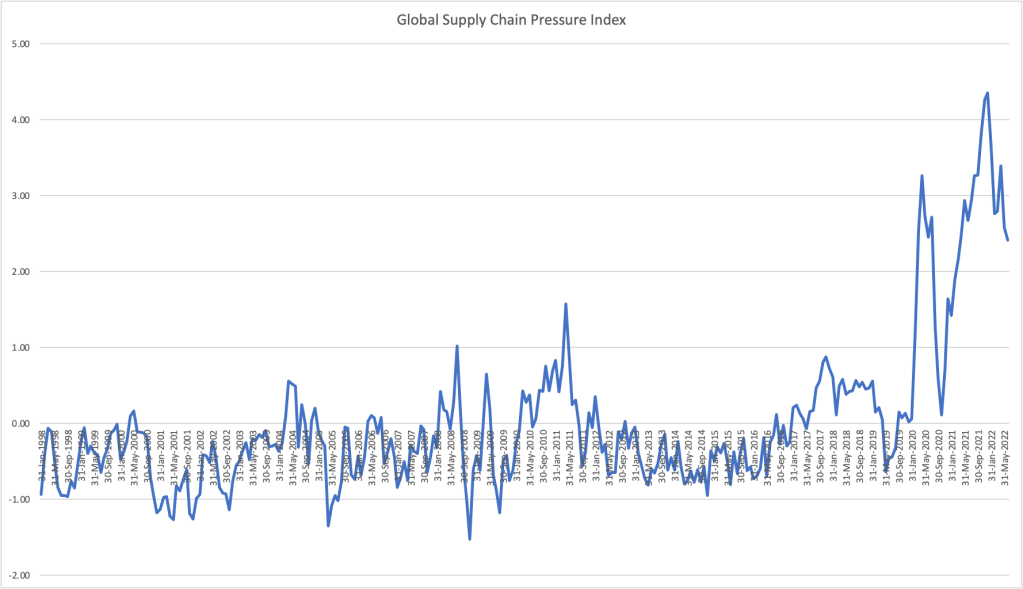

But in some cases it can be difficult for economists to construct an index. This problem is particularly likely when an index would not be comprised of similar data, such as prices of goods and services in the case of the CPI. For example, when the Covid–19 pandemic first began to affect the United States in March 2020, the U.S. economy began to experience “supply chain problems.” News articles reported supply chains problems persisting into the summer of 2022. These reports highlighted specific problems, such as shortages of semiconductors that reduced automobile production and ships being backed up at ports leading to delays in U.S. firms receiving imported products. Just as we don’t want to measure inflation by looking only at gasoline prices, we don’t want to measure supply chain problems by looking only at shortages of semiconductors. It would be better to use an index that summarizes what is happening with supply chains in a way that’s analogous to how the CPI summarizes what is happening with the price level. But the very different aspects of supply chain problems make constructing an index that summarizes these problems more difficult than constructing the CPI.

Economists at the Federal Reserve Bank of New York have tried to overcome these technical difficulties in devising an index of supply chain problems: the Global Supply Chain Pressure Index (GSCPI). Here’s the New York Fed’s description of the economic data included in the index:

“The GSCPI integrates a number of commonly used metrics with the aim of providing a comprehensive summary of potential supply chain disruptions. Global transportation costs are measured by employing data from the Baltic Dry Index (BDI)and the Harpex index, as well as airfreight cost indices from the U.S. Bureau of Labor Statistics. The GSCPI also uses several supply chain-related components from Purchasing Managers’ Index (PMI) surveys, focusing on manufacturing firms across seven interconnected economies: China, the euro area, Japan, South Korea, Taiwan, the United Kingdom, and the United States.”

Some more detail on components of the index that may be unfamiliar: The Baltic Dry Index (BDI) and the Harpex indexes both measure rates shippers charge firms to move cargo by sea. (Note that the name “Baltic” has historical significance but doesn’t mean that the index covers only the price of shipping in the Baltic Sea.) The Purchasing Managers’ Index (PMI) is derived from surveying purchasing managers at firms around the world about such aspects of their businesses as order backlogs, new orders, delivery time of goods from suppliers, inventories, and costs.

The following figure shows movements in the GSCPI from January 1998 through June 2022 and is derived from data on the New York Fed site. Higher values indicate more supply chain problems in the world economy. Movements in the index indicate that supply chain problems reached a peak in April 2020 during the height of the initial disruptions caused by the pandemic. Supply chains then improved through September 2020 before worsening again. The worst reading for the index occurred in December 2021. Supply problems then eased during the first half of 2022, although the index still remained high in June 2022. (Note that the values on the vertical axis are standard deviations from the average values of the index over the whole period. The standard deviation is a statistical measure of how spread out values of a series are relative to the series’ average value. That the value for the index during the first half of 2022 was two to four standards deviations above the average of the index indicates that supply chain problems were much more severe than normal.)

Sources: Liz Young, “Companies Face Rising Supply-Chain Costs Amid Inventory Challenges,” Wall Street Journal, June 21, 2022; Ana Monteiro, “Supply Constrainst a Headache for U.S. Firms as Outlook Dims,” bloomberg.com, June 2, 2022; and Federal Reserve Bank of New York, Global Supply Chain Pressure Index, https://www.newyorkfed.org/research/gscpi.html.

On Friday, July 8, the Bureau of Labor Statistics (BLS) released its monthly “Employment Situation” report for June 2022. The BLS estimated that nonfarm employment had increased by 372,000 during the month. That number was well above what economic forecasters had expected and seemed inconsistent with other macroeconomic data that showed the U.S. economy slowing. (Note that the increase in employment is from the establishment survey, sometimes called the payroll survey, which we discuss in Macroeconomics, Chapter 9, Section 9.1 and Economics, Chapter 19, Section 19.1.)

Data indicating that the economy was slowing during the first half of 2022 include the Bureau of Economic Analysis’s (BEA) estimate that real GDP had declined by 1.6 percent in the first quarter of 2022. The BEA’s advance estimate—the agency’s first estimate for the quarter—for the change in real GDP during the second quarter of 2022 won’t be released until July 28, but there are indications that real GDP will have declined again during the second quarter. For instance, the Federal Reserve Bank of Atlanta compiles a forecast of real GDP called GDPNow. The GDPNow forecast uses data that are released monthly on 13 components of GDP. This method allows economists at the Atlanta Fed to issue forecasts of real GDP well in advance of the BEA’s estimates. On July 8, the GDPNow forecast was that real GDP in the second quarter of 2022 would decline by 1.2 percent.

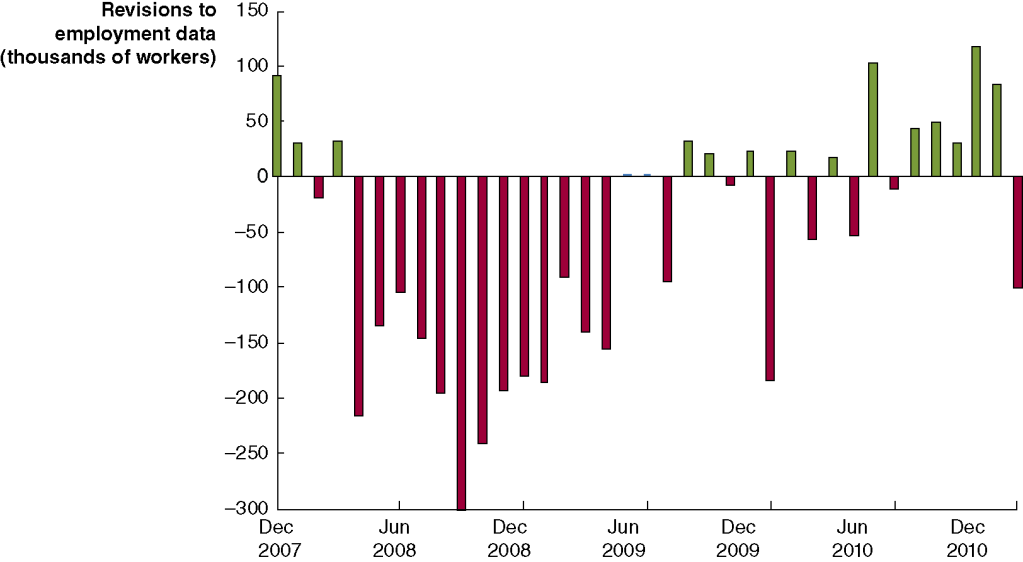

Two consecutive quarters of declining real GDP seems inconsistent with employment strongly growing. At a basic level, if firms are producing fewer goods and services—which is what causes a decline in real GDP—we would expect the firms to be reducing, rather than increasing, the number of people they employ. How can we reconcile the seeming contradiction between rising employment and falling output? One possibility is that either the real GDP data or the employment data—or, possibly, both—are inaccurate. Both GDP data and employment data from the establishment survey are subject to potentially substantial future revisions. (Note that because they are constructed from a survey of households, the employment data in the household survey aren’t revised. As we discuss in the text, economists and policymakers typically rely more on the establishment survey than on the household survey in gauging the current state of the labor market.) Substantial revisions are particularly likely for data released during the beginning of a recession.

In Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), we give an example of substantial revisions in the employment data. Figure 9.5 (reproduced below) shows that the declines in employment during the 2007–2009 recession were initially greatly underestimated. For example, the BLS initially reported that employment declined by 159,000 during September 2008. But after additional data became available, the BLS revised its estimate to a much larger decline of 460,000.

Similarly, in Macroeconomics, Chapter 15, Section 15,3, in the Apply the Concept “Trying to Hit a Moving Target: Making Policy with ‘Real-Time Data’,” we show the BEA’s estimates of the change in real GDP during the first quarter of 2008 have been revised substantially over time. The BEA’s advance estimate of the change in real GDP during the first quarter of 2008 was an increase of 0.6 percent at an annual rate. But that estimate of real GDP growth has been revised a number of times over the years, mostly downward. Currently, BEA data indicate that real GDP actually declined by 1.6 percent at an annual rate during the first quarter of 2008. This swing of more than 2 percentage points from the advance estimate is a large difference, which changes the picture of what happened during the first quarter of 2008 from one of an economy experiencing slow growth to one of an economy suffering a sharp downturn as it fell into the worst recession since the Great Depression of the 1930s.

The changes to the estimates of both employment and real GDP during the beginning of the 2007–2009 recession are not surprising. The initial estimates of employment and real GDP rely on incomplete data. The estimates are revised as additional data are collected by government agencies. During the beginning of a recession, these additional data are likely to show lower levels of employment and output than were indicated by the initial estimates. If the U.S. economy is in a recession in the second quarter of 2022, we can expect that the BLS and BEA will revise their initial estimates of employment and real GDP downward, which—depending on the relative magnitudes of the revisions to the two series—may resolve the paradox of rising employment and falling output.

Or it’s possible that the U.S. economy is not in a recession. In that case, the employment data may be correct in showing an increase in the number of people working, and the real GDP data may be revised upward to show that output has actually been expanding during the first six months of 2022. Economists and policymakers will have to wait to see which of these alternatives turns out to be the case.

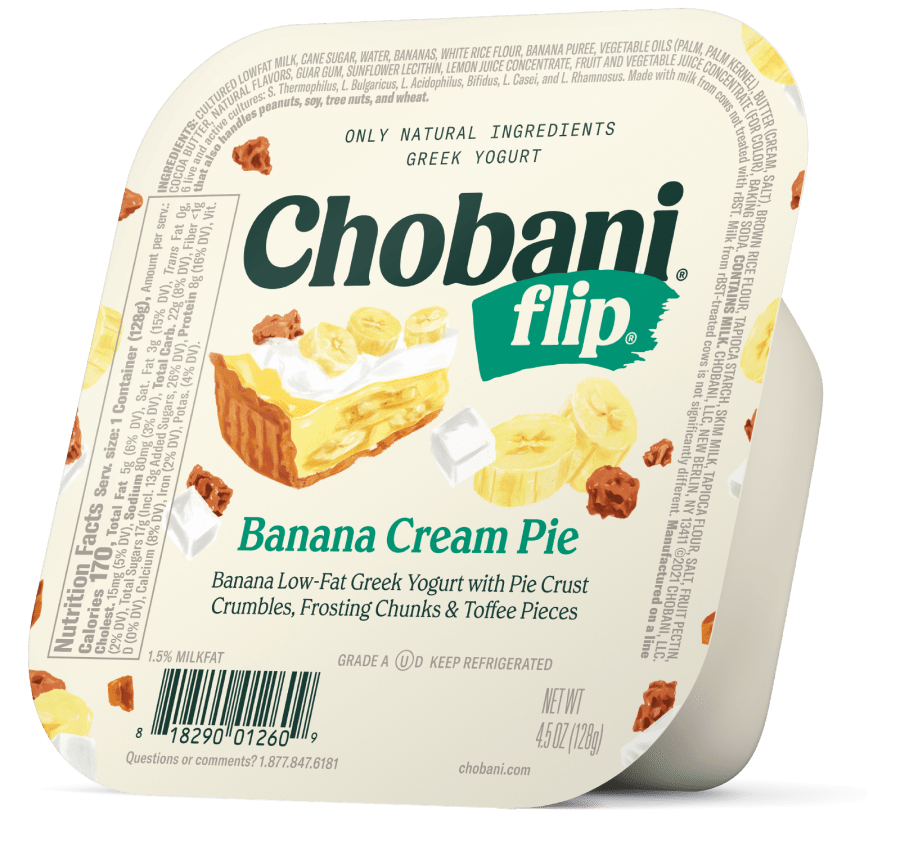

This yogurt remained the same price although the container shrank from 5.3 ounces to 4.5 ounces.

Each month, hundreds of employees of the Bureau of Labor Statistics (BLS) gather data on prices of goods and services from stores in 87 cities and from websites. The BLS constructs the consumer price index (CPI) by giving each price a weight equal to the fraction of a typical family’s budget spent on that good or service. (CPI is discussed in Macroeconomics, Chapter 9, Section 9.4 and in Economics, Chapter 19, Section 19.4.) Ideally, the BLS tracks prices of the same product over time. But sometimes a particular brand and style of shirt, for example, is discontinued. In that case, the BLS will instead use the price of a shirt that is a very close substitute.

A more difficult problem arises when the price of a good increases at the same time that the quality of the good improves. For instance, a new model iPhone may have both a higher price and a better battery than the model it replaces, so the higher price partly reflects the improvement in the quality of the phone. The BLS has long been aware of this problem and has developed statistical techniques that attempt to identify which part of the price increases are due to increases in quality. Economists differ in their views on how successfully the BLS has dealt with this quality bias to the measured inflation rate. Because of this bias in constructing the CPI, it’s possible that the published values of inflation may overstate the actual annual rate of inflation by 0.5 percentage point. For instance, the BLS might report an inflation rate of 3.5 percent when the actual inflation rate—if the BLS could determine it—was 4.0 percent. As the inflation rate increased beginning in the spring of 2021, a number of observers pointed to hidden inflation that was occurring. There were two main types of hidden inflation:

The quality of some services was declining

Some packaged goods contained smaller quantities at the same price

Here’s one example of the deteriorating quality of some services. Because during 2021 and 2022 many restaurants were having difficulty hiring servers, it was often taking longer for customers to have their orders taken and to have their food brought to the table. Because restaurants were also having difficulty hiring enough cooks, they also limited the items available on their menus. In other words, the service these restaurants were offering was not as good as it had been prior to the pandemic. So even if the restaurants kept their prices unchanged, their customers were paying the same price, but receiving less. Alan Cole, a former senior economist with the Congressional Joint Economic Committee, discussed these other examples on his blog: “hotels clean rooms less frequently on multi-night stays, shipping delays are longer, and phone hold times at airlines are worse.” In a column in the New York Times, economics writer Neil Irwin made similar points: “Complaints have been frequent about the cleanliness of [restaurant] tables, floors and bathrooms.” And: “People trying to buy appliances and other retail goods are waiting longer.”

A column in the Wall Street Journal on business travel by Scott McCartney was headlined “The Incredible Disappearing Hotel Breakfast.” McCartney noted that many hotels continue to advertise free hot breakfasts on their websites and apps but have stopped providing them. He also noted that hotels “have suffered from labor shortages that have made it difficult to supply services such as daily housekeeping or loyalty-group lounges,” in addition to hot breakfasts. In all of these cases, the actual prices of the services had increased more than had the listed prices because the deterioration in quality meant that people were receiving less for their money.

In addition to deterioration in the quality of services, hidden inflation during this period also took the form of consumers buying some packaged goods in which the quantities had been reduced, although the price was unchanged. For example, in June 2022, an article by the Associated Press noted that:

• “A small box of Kleenex now has 60 tissues; a few months ago, it had 65.” • “Chobani Flips yogurts have shrunk from 5.3 ounces to 4.5 ounces.” • “Earth’s Best Organic Sunny Days Snack Bars went from eight bars per box to seven, but the price listed at multiple stores remains $3.69.”

An article in the Wall Street Journal observed that: “Shrinkflation, as economists call it, tends to be easier for companies to pass on to consumers. Despite labels that show price by weight, research shows that most customers look at only the overall price.”

The BLS does try to adjust the measurement of the CPI for shrinkflation, which it can do because the BLS keeps careful track of the quantities included in the packaged goods that are included in its survey.

But the BLS makes no attempt to adjust the CPI for the deterioration in the quality of services because doing so would be very difficult. As Irwin observes: “Customer service preferences—particularly how much good service is worth—varies highly among individuals and is hard to quantify. How much extra would you pay for a fast-food hamburger from a restaurant that cleans its restroom more frequently than the place across the street?” And an economist at the BLS noted that, “We do not capture the decrease in service quality associated with cleaning a [hotel] room every two days rather than one.”

As we noted earlier, most economists believe that the failure of the BLS to fully account for improvements in the quality of goods results in changes in the CPI overstating the true inflation rate. This bias may have been more than offset during 2021–2022 by deterioration in the quality of services resulting in the CPI understating the true inflation rate. As the dislocations caused by the pandemic gradually resolve themselves, it seems likely that the deterioration in services will be reversed. But it’s possible that the deterioration in the provision of some services may persist. Fortunately, unless the deterioration increases over time, it would not continue to distort the measurement of the inflation rate because the same lower level of service would be included in every period’s prices.

Sources: Dee-Ann Durbin, “No, You’re Not Imagining It—Package Sizes Are Shrinking,” apnews.com, June 8, 2022; Annie Gasparro and Gabriel T. Rubin, “The Hidden Ways Companies Raise Prices,” Wall Street Journal, February 12, 2022; Alan Cole, “How I Reluctantly Became an Inflation Crank,” fullstackeconomics.com, September 8, 2021; Scott McCartney, “The Incredible Disappearing Hotel Breakfast—and Other Amenities Travelers Miss,” Wall Street Journal, October 20, 2021; and Neil Irwin, “There Is Shadow Inflation Taking Place All Around Us,” New York Times, October 14, 2021.

Emily Mascitis checks prices at an auto-repair shop in Philadelphia. (Photo from the Wall StreetJournal.)

As we discuss in Macroeconomics, Chapter 9, Section 9.4, (Economics, Chapter 19, Section 19.4) in calculating the consumer price index (CPI) each month, the Bureau of Labor Statistics sends hundreds of employees to gather price data from stores and offices. A reporter for the Wall Street Journal followed a price checker as she visited an auto-repair shop, a grocery store, and other businesses.

The article provides an excellent discussion of the care with which prices are collected, particularly with respect to making sure that the prices are for the same good or service each month. For instance, while in a grocery, the price checker almost made the mistake of recording the price of a can of low sodium chicken noodle soup, rather than the price of regular chicken noodle soup as in previous months.

At one point, the price checker noted that the price of clementines had been increasing rapidly and remarked that when buying fruit for her own family “We need to pick a less expensive fruit.” Switching from buying a fruit, in this case clementines, with a price that is increasing rapidly to a fruit with a price that is increasing more slowly, say regular oranges, is an example of the substitution bias. That’s one of the four biases discussed in Section 9.4 that can cause the measured increase in the CPI to overstate the true rate of inflation.

The article can be found here. (A subscription may be required.)

Source: Rachel Wolfe, “How the Inflation Rate Is Measured: 477 Government Workers at Grocery Stores,” Wall Street Journal, May 10, 2022.

On Thursday morning, April 28, the Bureau of Economic Analysis (BEA) released its “advance” estimate for the change in real GDP during the first quarter of 2022. As shown in the first line of the following table, somewhat surprisingly, the estimate showed that real GDP had declined by 1.4 percent during the first quarter. The Federal Reserve Bank of Atlanta’s “GDP Now” forecast had indicated that real GDP would increase by 0.4 percent in the first quarter. Earlier in April, the Wall Street Journal’s panel of academic, business, and financial economists had forecast an increase of 1.2 percent. (A subscription may be required to access the forecast data from the Wall Street Journal’s panel.)

Do the data on real GDP from the first quarter of 2022 mean that U.S. economy may already be in recession? Not necessarily, for several reasons:

First, as we note in the Apply the Concept, “Trying to Hit a Moving Target: Making Policy with ‘Real-Time’ Data,” in Macroeconomics, Chapter 15, Section 15.3 (Economics, Chapter 25, Section 25.3): “The GDP data the BEA provides are frequently revised, and the revisions can be large enough that the actual state of the economy can be different for what it at first appears to be.”

Second, even though business writers often define a recession as being at least two consecutive quarters of declining real GDP, the National Bureau of Economic Research has a broader definition: “A recession is a significant decline in activity across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.” Particularly given the volatile movements in real GDP during and after the pandemic, it’s possible that even if real GDP declines during the second quarter of 2022, the NBER might not decide to label the period as being a recession.

Third, and most importantly, there are indications in the underlying data that the U.S. economy performed better during the first quarter of 2022 than the estimate of declining real GDP would indicate. In a blog post in January discussing the BEA’s advance estimate of real GDP during the fourth quarter of 2021, we noted that the majority of the 6.9 percent increase in real GDP that quarter was attributable to inventory accumulation. The earlier table indicates that the same was true during the first quarter of 2022: 60 percent of the decline in real GDP during the quarter was the result of a 0.84 decline in inventory investment.

We don’t know whether the decline in inventories indicates that firms had trouble meeting demand for goods from current inventories or whether they decided to reverse some of the increases in inventories from the previous quarter. With supply chain disruptions continuing as China grapples with another wave of Covid-19, firms may be having difficulty gauging how easily they can replace goods sold from their current inventories. Note the corresponding point that the decline in sales of domestic product (line 2 in the table) was smaller than the decline in real GDP.

The table below shows changes in the components of real GDP. Note the very large decline exports and in purchases of goods and services by the federal government. (Recall from Macroeconomics, Chapter 16, Section 16.1, the distinction between government purchases of goods and services and total government expenditures, which include transfer payments.) The decline in federal defense spending was particularly large. It seems likely from media reports that the escalation of Russia’s invasion of Ukraine will lead Congress and President Biden to increase defense spending.

Notice also that increases in the non-government components of aggregate demand remained fairly strong: personal consumption expenditures increased 2.7 percent, gross private domestic investment increased 2.3 percent, and imports surged by 17.7 percent. These data indicate that private demand in the U.S. economy remains strong.

So, should we conclude that the economy will shrug off the decline in real GDP during the first quarter and expand during the remainder of the year? Unfortunately, there are still clouds on the horizon. First, there are the difficult to predict effects of continuing supply chain problems and of the war in Ukraine. Second, the Federal Reserve has begun tightening monetary policy. Whether Fed Chair Jerome Powell will be able to bring about a soft landing, slowing inflation significantly while not causing a large jump in unemployment, remains the great unknown of economic policy. Finally, if high inflation rates persist, households and firms may respond in ways that are difficult to predict and, may, in particular decide to reduce their spending from the current strong levels.

Adam Smith bronze statue on Royal Mile Market square in front of Saint Gilles Cathedral in Edinburgh, Scotland.

Growth matters. A lot. A slightly higher rate of economic growth, sustained over time, can make the difference between a big increase in living standards and relative stagnation. Whether we can still generate strong and steady growth is a “$64,000 question” for the economy — the question. Nobel Prize–winning economist Robert Lucas famously observed that once economists think of long-term growth, it is hard to think of anything else. A pro-growth policy agenda is a good idea because growth is a good idea.

But a deeper question remains: Is public support for growth guaranteed? Oren Cass of American Compass refers to growth and economists’ fealty to economic participation for all as “economic piety.” This critique resonates for a simple reason: Forces that propel growth invariably leave a wake of economic disruption for people in many places and political disruption for the nation. A serious discussion of pro-growth policy must account for that disruption.

A conventional pro-growth policy agenda can be enhanced by support for openness to markets, ideas, and new ways of doing things, and for the ability of firms to adapt to change. Such an enhanced agenda would center on infrastructure broadly defined, development and dissemination of better management practices, and reduced barriers to competition.

Yet the political process, and even many a conservative, is openly skeptical of such an agenda. This skepticism is rooted not in disagreement over the future of scientific advances or of organizational adaptation — but in a concern that growth’s benefits be shared broadly. Addressing this skepticism head-on is essential for rebuilding social support for growth and for countering well-meaning but potentially harmful policies.

The system that needs defending is a mature and successful one. Adam Smith, the great proponent of the “invisible hand” (not the visible hand of a state-directed economy), saw openness and competition as worth the candle. His 1776 publication of The Wealth of Nations came before what we would recognize today as industrial capitalism, though technological change and globalization were features of economic debates in the aftermath of Smith’s ideas.

Smith’s radical insight is central to economic policy today: National prosperity (the “wealth of a nation”) is represented by consumption of goods and services by its people — i.e., their living standards. The goal of the economy in Smith’s telling was to make the economic pie as large as possible. His advocacy of free markets and competition rested on their ability to boost consumption possibilities.

Two centuries later, Nobel laureates Kenneth Arrow and Gérard Debreu added the jargon and mathematics of contemporary economics to formalize Smith’s intuition. While individuals and firms act independently, competitive markets lead to an efficient allocation of resources and a maximized economic pie. Friedrich Hayek, another Nobel laureate, hailed the virtue of a decentralized competitive price system in maximizing economic activity.

Smith’s radicalism draws from his attack on mercantilism—the economic orthodoxy of the day—which stressed a zero-sum view of trade and state intervention to promote and protect certain firms and industries. (Sound familiar?) His second radical insight was that the “nation” did not mean the sovereign and the well-connected. In Smith’s view, individuals as consumers—all people—were kings. Finally, channeling the sympathetic concern espoused in his earlier classic, The Theory of Moral Sentiments, Smith championed mass participation in the productive economy as a precondition for human flourishing.

It is fair to say that Smith lacked a theory of per capita growth in the economy over time; indeed, he wrote before the massive increase in living standards attendant upon the Industrial Revolution. After 1800, per capita income in the United Kingdom — and the United States — witnessed a 30-fold increase. There have also been major improvements in the quality of goods and services that such a statistic doesn’t quite capture. And, of course, many of today’s offerings — from smartphones to computers to air-conditioning — were not available even in 1900, let alone 1800.

That lacuna in Smith’s theory partly reflects technical difficulties in modeling growth. Higher output can come from growth in inputs such as labor and capital, but what determines their growth? Today’s economists highlight population growth and society’s willingness to work, save, and invest. Still more important is growth in productivity, or the efficiency with which inputs are used to produce goods and services.

Smith’s pin-factory example — in which output rose with the specialization of tasks — links how things are done with the level of productivity. But what factors determine productivity growth over time? Today’s economic analysis focuses on technology and the process of generating ideas. Since economic growth is still crucial for people seemingly marginalized by capitalism, it’s worth asking whether the economic foundations expressed in The Wealth of Nations are still relevant today. Where does growth come from now? And do those sources still require openness and competition?

The short answer is that they do, but to see why, we need to focus on the ideas of two prominent economists after 1800: Edmund Phelps and Deirdre Nansen McCloskey.

Phelps, a Nobel laureate, has done much to connect growth to Smith’s foundational ideas. He starts with Smith’s emphasis on a great many individuals (not the state or privileged firms) searching for new and better ways of doing things. This relentless search produces innovative ideas, processes, and goods that drive growth — but only if the political economy allows openness. Smith’s messy, “bottom up” version of the market therefore puts mass innovation at the heart of economic growth. Phelps’s argument reflects how Smithian societies committed to openness are best able to prosper and promote growth.

This argument has two important applications. The first is to debunk the sometimes fashionable view of secular productivity decline — that we have run short of new things to discover and exploit. The second is to give an answer to economies struggling with growth in a period of structural changes from technology and globalization. Slowdowns in innovation are likely not due to scientific barrenness but to walls against openness and change — that is, fears of disruption.

Phelps’s concern with economic dynamism draws him to Smith’s arguments against mercantilist tinkering in the economy. Like Smith, he worries about the hidden costs of tinkering with competition by blocking change from the outside and by enabling rent-seeking on the inside. These “corporatist” policies — fashionable among some conservatives at present — inevitably embolden vested interests and cronyism, slowing change and growth. Even seemingly small interventions can subtly diminish innovation, a point to which I’ll return.

Yet such a critique must acknowledge the political consequences of disruption. Dynamism is messy. It creates growth in the aggregate, but with many individual losers as well as individual gainers.

McCloskey, an economic historian, has similarly identified the continuous, large-scale, voluntary, and unfocused search for betterment as the source of new ideas that can produce economic growth. She sees this “innovism” as primarily a cultural force, preferring the term to the more familiar “capitalism,” and connects innovism to economic liberalism. Echoing Smith, she emphasizes how an open economy allows individuals—from the moderately to the spectacularly talented—to “have a go.” This economic liberalism allows competition to enshrine liberty and mass flourishing.

In McCloskey’s telling, growth depends on a liberal tolerance and openness to change, which encourage many people to be alert to opportunity. Sustaining that tolerance as structural shifts bring economic misfortune to many individuals, however, requires more than devotion to Smith.

Therein lies the current economic-policy rub. Economists’ theories of growth bring to mind a coin: Sunny descriptions of growth and dynamism are “heads,” and hand-wringing over disruption is “tails.” As I observed earlier, growth is messy. It can push some individuals, firms, and even industries off well-worn and comfortable paths.

But Smith offers more in defense of growth than paeans to laissez-faire. Though he is sometimes caricatured as being anti-government in all cases, Smith was principally opposed to mercantilist privileges for specific businesses and industries and to the governmentalization of social affairs. He wanted government to provide what economists today call “public goods,” such as national defense, the criminal-justice system, and enforcement of property rights and contracts the institutional underpinnings of commerce and trade. He also favored support for infrastructure to keep commerce flowing freely.

But Smith went further: To prepare workers and enrich their lives, he called for government to provide universal education, and he drew a connection between education and liberty as well as work in a free society. But boosting participation in today’s economy—participation that provides support for growth—will require a bit more.

Not surprisingly, political reaction to economic disruption brings about — pardon the econ-speak—a “demand” for and “supply” of policy actions. Job losses, firm failures, and diminished industry fortunes bring about a demand for help, for adaptation. The political process responds with a supply of ideas in one of two forms: walls or bridges. Walls are protections against disruption or change. Bridges, ways to get somewhere or back, prepare individuals for the changed economy and help those whose economic participation has been disrupted reenter the workforce.

Proposals for walls are familiar. They can be physical, of course, but they needn’t be. Conservative populists advocate limits on trade and technology, in order to advance industrial policy. Some progressives advocate universal basic income. All these policies would diminish the prospects for economic advances.

The most prominent sort of wall today is what I call “modern corporatism.” It assumes that Smith was wrong: The “wealth of a nation” lies not in consumption or living standards (and so ultimately in growth) but in jobs, good jobs, even particular good jobs, with good manufacturing jobs the very paradigm. The sort of tinkering with the market that drew Smith’s ire may actually be a necessary way of recentering economic policy on jobs, so the theory goes. Opportunities for work, and for the dignity it can bring, are surely important.

A gentle industrial policy devised by social scientists who are worried about jobs is not the answer. It results in state tinkering for special interests, precisely the kind of thing that prompted Smith’s criticism of mercantilism. Moreover, as University of Chicago economist Luigi Zingales argues in A Capitalism for the People, it risks a vicious cycle: A little bit of tinkering becomes a lot of tinkering—and anyone who cannot justify special privileges is left out, calling into question social support for growth. Nevertheless, industrial policy has caught the attention of elected officials on the right, from Donald Trump to Josh Hawley to Marco Rubio. While national security and the border can be exceptions as concerns, advice from Milton Friedman to the party of Ronald Reagan this is not.

That said, economists’ invocation of Smith as a proponent of let-’er-rip laissez-faire is neither faithful to Smith nor particularly helpful to individuals and communities buffeted by disruption. With today’s rapid and long-lasting technological change and globalization, “having a go” requires support for acquiring new skills when they are needed.

That is why we need more bridges. Bridges take us somewhere and bring us back. The journey to somewhere is about preparation for new opportunities. The journey back is about reconnecting to the productive economy when economic forces beyond our control have knocked us away.

Economic bridges have three features. The first is that they help people overcome a specific challenge on their way to economic flourishing — they don’t provide that outcome directly. The second is that wider society builds the bridge, through private organizations, governments, or public–private partnerships, as globalization and technological change have introduced significant risks that individuals by themselves cannot avoid. The third feature is that they avoid restraints on openness to changes in markets and ideas.

We once did better, much better. During the Civil War, President Abraham Lincoln worked with Congress to pass the Morrill Act, directing resources to the development of land-grant colleges around the country, extending higher education to citizens of modest means, and enabling workers to develop skills for new industries, particularly in manufacturing. As World War II drew to a close, President Franklin D. Roosevelt and Congress came together to enact the G.I. Bill, helping to educate returning troops for a changing economy.

Supporting economic growth and undergirding broad participation in the economy require similarly bold ideas. To begin, community colleges are the logical workhorses of skill development and retraining, and their presence in regional economies makes them attractive partners for employers. Yet community colleges have seen their state-level public support wither. The Biden administration calls for free tuition, which would boost demand but provide no support for community college to offer a practical education and an emphasis on completion. Amy Ganz, Austan Goolsbee, Melissa Kearney, and I proposed an alternative approach based on the land-grant-college model. We proposed a supply-side program of federal grants to strengthen community colleges — contingent on improved degree-completion rates and labor-market outcomes. To further encourage training, the federal government could offer a tax credit to compensate firms for the risk of losing trained workers. It could also increase the earned-income tax credit for workers with or without children.

New ideas are also needed to promote workers’ reentry into the workforce. Personal reemployment accounts, for example, would support dislocated workers and offer them a reemployment bonus if they found a new job within a certain period of time. The “personal” refers to individuals’ choosing from a range of training and support services. Another idea is to beef up support for place-based assistance to areas with stubbornly high rates of long-term nonemployment. Such support could be integrated with an increase in the earned-income tax credit and the supply-side investment in community colleges. Building on the decentralized approach in the land-grant colleges and grants to community colleges, expanded place-based aid would be delivered via flexible block grants encouraging business and employment.

Broad public support required for growth and dynamism requires both bridge-building and a political language that frames it. Growth, opportunity, and participation are good, and we do not need a new economics. But phrases like “transition cost” and “inevitable economic forces” must give way to bridges of preparation and reconnection.

‘Why did nobody see it coming?” a quizzical Queen of England questioned a quorum of economists at the London School of Economics about the global financial crisis as it emerged in late 2008. How could major disruptive forces build up over time and yet escape the attention of experts and leaders?

Of the disruptive structural changes accompanying economic dynamism, one might ask a similar question. Growth matters. But that growth is one side of a coin whose flip side is disruption is known, certainly to economists. Why has our political discourse not emphasized this basic point?

Why did we not see fatigue with change coming among the people who most had to bear its ill effects?

However foolishly, we did not. Some so-called conservatives today have responded by saying that we should limit change. Surely a better response is that we should seek ever more growth by allowing unfettered change, but also facilitate the establishing of ever more connections in a growing economy. That classical-liberal answer has the better place in American conservatism — and in American economic life.

— This essay is sponsored by National Review Institute.Originally published here.

Lawrence Summers (Photo from harvardmagazine.com.)John Cochrane (Photo from hoover.org.)

In several of our blog posts and podcasts, we’ve discussed Lawrence Summers’s forecasts of inflation. Beginning in February 2021, Summers, an economist at Harvard who served as Treasury secretary in the Clinton administration, argued that the United States was likely to experience rates of inflation that would be higher and persist longer than Federal Reserve policymakers were forecasting. In March 2021, the members of the Fed’s Federal Open Market Committee had an average forecast of inflation of 2.4 percent in 2021, falling to 2.0 percent in 2022. (The FOMC projections can be found here.)

In fact, inflation measured by the CPI has been above 5 percent every month since June 2021; the Fed’s preferred measure of inflation—the percentage change in the price index for personal consumption expenditures—has been above 5 percent every month since October 2021. Summers’s forecasts of inflation have turned out to be more accurate than those of the members of the Federal Open Committee.

In this podcast, Summers discusses his analysis of inflation with four scholars from the Hoover Institution, including economist John Cochrane. Summers explains why he came to believe in early 2021 that inflation was likely to be much higher than generally expected, how long he believes high rates of inflation will persist, and whether the Fed is likely to be able to achieve a soft landing by bringing inflation back to its 2 percent target without causing a recession. The first half of the podcast, in particular, should be understandable to students who have completed the monetary and fiscal policy chapters (Macroeconomics, Chapters 15 and 16; Economics, Chapters 25 and 26). Background useful for understanding the podcast discussion of monetary policy during the 1970s can be found in Chapter 17, Sections 17.2 and 17.3.

Authors Glenn Hubbard and Tony O’Brien reconsider the role of inflation in today’s economy. They discuss the Fed’s possible responses by considering responses to similar inflation threats in previous generations – notably the Fed’s response led by Paul Volcker that directly led to the early 1980’s recession. The markets are reflecting stark differences in our collective expectations about what will happen next. Listen to find out more about the Fed’s likely next steps.

It now seems clear that the new monetary policy strategy the Fed announced in August 2020 was a decisive break with the past in one respect: With the new strategy, the Fed abandoned the approach dating to the 1980s of preempting inflation. That is, the Fed would no longer begin raising its target for the federal funds rate when data on unemployment and real GDP growth indicated that inflation was likely to rise. Instead, the Fed would wait until inflation had already risen above its target inflation rate.

Since 2012, the Fed has had an explicit inflation target of 2 percent. As we discussed in a previous blog post, with the new monetary policy the Fed announced in August 2020, the Fed modified how it interpreted its inflation target: “[T]he Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

The Fed’s new approach is sometimes referred to as average inflation targeting (AIT) because the Fed attempts to achieve its 2 percent target on average over a period of time. But as former Fed Vice Chair Richard Clarida discussed in a speech in November 2020, the Fed’s monetary policy strategy might be better called a flexible average inflation target (FAIT) approach rather than a strictly AIT approach. Clarida noted that the framework was asymmetric, meaning that inflation rates higher than 2 percent need not be offset with inflation rates lower than 2 percent: “The new framework is asymmetric. …[T]he goal of monetary policy … is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent.” And: “Our framework aims … for inflation to average 2 percent over time, but it does not make a … commitment to achieve … inflation outcomes that average 2 percent under any and all circumstances ….”

Inflation began to increase rapidly in mid-2021. The following figure shows three measure of inflation, each calculated as the percentage change in the series from the same month in the previous year: the consumer price index (CPI), the personal consumption expenditure (PCE) price index, and the core PCE—which excludes the prices of food and energy. Inflation as measured by the CPI is sometimes called headline inflation because it’s the measure of inflation that most often appears in media stories about the economy. The PCE is a broader measure of the price level in that it includes the prices of more consumer goods and services than does the CPI. The Fed’s target for the inflation rate is stated in terms of the PCE. Because prices of food and inflation fluctuate more than do the prices of other goods and services, members of the Fed’s Federal Open Market Committee (FOMC) generally consider changes in the core PCE to be the best measure of the underlying rate of inflation.

The figure shows that for most of the period from 2002 through early 2021, inflation as measured by the PCE was below the Fed’s 2 percent target. Since that time, inflation has been running well above the Fed’s target. In February 2022, PCE inflation was 6.4 percent. (Core PCE inflation was 5.4 percent and CPI inflation was 7.9 percent.) At its March 2022 meeting the FOMC begin raising its target for the federal funds rate—well after the increase in inflation had begun. The Fed increased its target for the federal funds rate by 0.25 percent, which raised the target from 0 to 0.25 percent to 0.25 to 0.50 percent.

Should the Fed have taken action to reduce inflation earlier? To answer that question, it’s first worth briefly reviewing Fed policy during the Great Inflation of 1968 to 1982. In the late 1960s, total federal spending grew rapidly as a result of the Great Society social programs and the war in Vietnam. At the same time, the Fed increased the rate of growth of the money supply. The result was an end to the price stability of the 1952-1967 period during which the annual inflation rate had averaged only 1.6 percent.

The 1973 and 1979 oil price shocks also contributed to accelerating inflation. Between January 1974 and June 1982, the annual inflation rate averaged 9.3 percent. This was the first episode of sustained inflation outside of wartime in U.S. history—until now. Although the oil price shocks and expansionary fiscal policy contributed to the Great Inflation, most economists, inside and outside of the Fed, eventually concluded that Fed policy failures were primarily responsible for inflation becoming so severe.

The key errors are usually attributed to Arthur Burns, who was Fed Chair from January 1970 to March 1978. Burns, who was 66 at the time of his appointment, had made his reputation for his work on business cycles, mostly conducted prior to World War II at the National Bureau of Economic Research. Burns was skeptical that monetary policy could have much effect on inflation. He was convinced that inflation was mainly the result of structural factors such as the power of unions to push up wages or the pricing power of large firms in concentrated industries.

Accordingly, Burns was reluctant to raise interest rates, believing that doing so hurt the housing industry without reducing inflation. Burns testified to Congress that inflation “poses a problem that traditional monetary and fiscal remedies cannot solve as quickly as the national interest demands.” Instead of fighting inflation with monetary policy he recommended “effective controls over many, but by no means all, wage bargains and prices.” (A collection Burns’s speeches can be found here.)

Few economists shared Burns’s enthusiasm for wage and price controls, believing that controls can’t end inflation, they can only temporarily reduce it while causing distortions in the economy. (A recent overview of the economics of price controls can be found here.) In analyzing this period, economists inside and outside the Fed concluded that to bring the inflation rate down, Burns should have increased the Fed’s target for the federal funds rate until it was higher than the inflation rate. In other words, the real interest rate, which equals the nominal—or stated—interest rate minus the inflation rate, needed to be positive. When the real interest rate is negative, a business may, for example, pay 6% on a bond when the inflation rate is 10%, so they’re borrowing funds at a real rate of −4%. In that situation, we would expect borrowing to increase, which can lead to a boom in spending. The higher spending worsens inflation.

Because Burns and the FOMC responded only slowly to rising inflation, workers, firms, and investors gradually increased their expectations of inflation. Once higher expectation inflation became embedded, or entrenched, in the U.S. economy it was difficult to reduce the actual inflation rate without increasing the target for the federal funds rate enough to cause a significant slowdown in the growth of real GDP and a rise in the unemployment rate. As we discuss in Macroeconomics, Chapter 17, Sections 17.2 and 17.3 (Economics, Chapter 27, Sections 27.2 and 27.3), the process of the expected inflation rate rising over time to equal the actual inflation rate was first described in research conducted separately by Nobel Laureates Milton Friedman and Edmund Phelps during the 1960s.

An implication of Friedman and Phelps’s work is that because a change in monetary policy takes more than a year to have its full effect on the economy, if the Fed waits until inflation has already increased, it will be too late to keep the higher inflation rate from becoming embedded in interest rates and long-term labor and raw material contracts.

Paul Volcker, appointed Fed chair by Jimmy Carter in 1979, showed that, contrary to Burns’s contention, monetary policy could, in fact, deal with inflation. By the time Volcker became chair, inflation was above 11%. By raising the target for the federal funds rate to 22%—it was 7% when Burns left office—Volcker brought the inflation rate down to below 4%, but only at the cost of a severe recession during 1981–1982, during which the unemployment rate rose above 10 percent for the first time since the Great Depression of the 1930s. Note that whereas Burns had largely failed to increase the target for the federal funds as rapidly as inflation had increased—resulting in a negative real federal funds rate—Volcker had raised the target for the federal funds rate above the inflation rate—resulting in a positive real federal funds rate.

Because the 1981–1982 recession was so severe, the inflation rate declined from above 11 percent to below 4 percent. In Chapter 17, Figure 17.10 (reproduced below), we plot the course of the inflation and unemployment rates from 1979 to 1989.

Caption: Under Chair Paul Volcker, the Fed began fighting inflation in 1979 by reducing the growth of the money supply, thereby raising interest rates. By 1982, the unemployment rate had risen to 10 percent, and the inflation rate had fallen to 6 percent. As workers and firms lowered their expectations of future inflation, the short-run Phillips curve shifted down. The adjustment in expectations allowed the Fed to switch to an expansionary monetary policy, which by 1987 brought unemployment back to the natural rate of unemployment, with an inflation rate of about 4 percent. The orange line shows the actual combinations of unemployment and inflation for each year from 1979 to 1989.

The Fed chairs who followed Volcker accepted the lesson of the 1970s that it was important to head off potential increases in inflation before the increases became embedded in the economy. For instance, in 2015, then Fed Chair Janet Yellen in explaining why the FOMC was likely to raise to soon its target for the federal funds rate noted that: “A substantial body of theory, informed by considerable historical evidence, suggests that inflation will eventually begin to rise as resource utilization continues to tighten. It is largely for this reason that a significant pickup in incoming readings on core inflation will not be a precondition for me to judge that an initial increase in the federal funds rate would be warranted.”

Between 2015 and 2018, the FOMC increased its target for the federal funds rate nine times, raising the target from a range of 0 to 0.25 percent to a range of 2.25 to 2.50 percent. In 2018, Raphael Bostic, president of the Federal Reserve Bank of Atlanta justified these rate increases by noting that “… we shouldn’t forget that [the Fed’s] credibility [with respect to keeping inflation low] was hard won. Inflation expectations are reasonably stable for now, but we know little about how far the scales can tip before it is no longer so.”

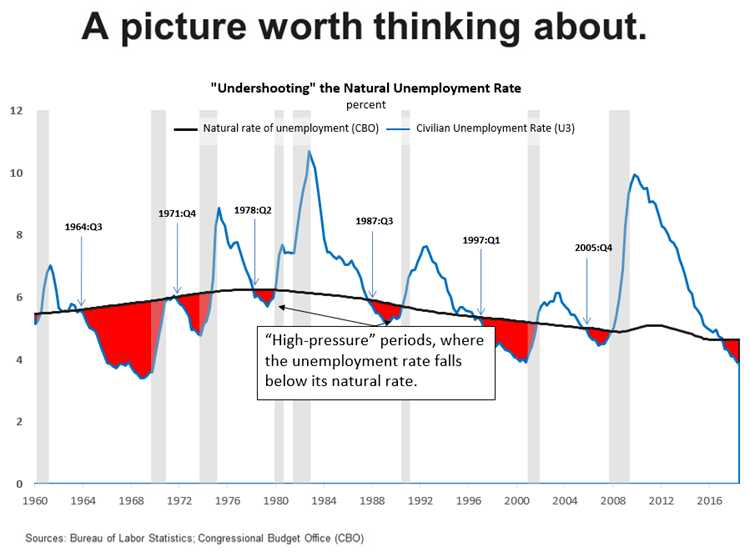

He used the following figure to illustrate his point.

Bostic interpreted the figure as follows:

“[The red areas in the figure are] periods of time when the actual unemployment rate fell below what the U.S. Congressional Budget Office now estimates as the so-called natural rate of unemployment. I refer to these episodes as “high-pressure” periods. Here is the punchline. Dating back to 1960, every high-pressure period ended in a recession. And all but one recession was preceded by a high-pressure period….

I think a risk management approach requires that we at least consider the possibility that unemployment rates that are lower than normal for an extended period are symptoms of an overheated economy. One potential consequence of overheating is that inflationary pressures inevitably build up, leading the central bank to take a much more “muscular” stance of policy at the end of these high-pressure periods to combat rising nominal pressures. Economic weakness follows [resulting typically, as indicated in the figure by the gray band, in a recession].”

By July 2019, a majority of the members of the FOMC, including Chair Powell, had come to believe that with no sign of inflation accelerating, they could safely cut the federal funds rate. But they had not yet explicitly abandoned the view that the FOMC should act to preempt increases in inflation. The formal change came in August 2020 when, as discussed earlier, the FOMC announced the new FAIT.

At the time the FOMC adopted its new monetary policy strategy, most members expected that any increase in inflation owing to problems caused by the Covid-19 pandemic—particularly the disruptions in supply chains—would be transitory. Because inflation has proven to be more persistent than Fed policymakers and many economists expected, two aspects of the FAIT approach to monetary policy have been widely discussed: First, the FOMC did not explicitly state by how much inflation can exceed the 2 percent target or for how long it needs to stay there before the Fed will react. The failure to elaborate on this aspect of the policy has made it more difficult for workers, firms, and investors to gauge the Fed’s likely reaction to the acceleration in inflation that began in the spring of 2021. Second, the FOMC’s decision to abandon the decades-long policy of preempting inflation may have made it more difficult to bring inflation down to the 2 percent target without causing a recession.

Federal Reserve Governor Lael Brainard recently remarked that “it is of paramount importance to get inflation down” and some Fed policymakers believe that the FOMC will have to begin increasing its target for the federal funds rate more aggressively. (The speech in which Governor Brainard discusses her current thinking on monetary policy can be found here.) For instance James Bullard, president of the Federal Reserve Bank of St. Louis, has argued in favor of raising the target to above 3 percent this year. With the Fed’s preferred measure of inflation running above 5 percent, it would take substantial increases int the target to achieve a positive real federal funds rate.

It is an open question whether Jerome Powell finds himself in a position similar to that of Paul Volcker in 1979: Rapid increases in interest rates may be necessary to keep inflation from accelerating, but doing so risks causing a recession. In a recent speech (found here), Powell pledged that: “We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

But Powell argued that the FOMC could achieve “a soft landing, with inflation coming down and unemployment holding steady” even if it is forced to rapidly increase its target for the federal funds rate:

“Some have argued that history stacks the odds against achieving a soft landing, and point to the 1994 episode as the only successful soft landing in the postwar period. I believe that the historical record provides some grounds for optimism: Soft, or at least softish, landings have been relatively common in U.S. monetary history. In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession.”

Some economists have been skeptical that a soft landing is likely. Harvard economist and former Treasury Secretary Lawrence Summers has been particularly critical of Fed policy, as in this Twitter thread. Summers concludes that: “I am apprehensive that we will be disappointed in the years ahead by unemployment levels, inflation levels, or both.” (Summers and Harvard economist Alex Domash provide an extended discussion in a National Bureau of Economic Research Working Paper found here.)

Clearly, we are in a period of great macroeconomic uncertainty.