Image created by ChatGPT of Alan Greenspan as a maestro

Earlier this week, Alan Greenspan, former chair of the Federal Reserve passed away at the age of 100. Greenspan may have been the best-known Fed chair in history. People who follow the economics and business news know who Jerome Powell and Kevin Warsh are. But many people who don’t follow the news likely have never heard of them. During his term as Fed chair from 1987 to 2006, Greenspan achieved a level of celebrity that made him one of the best known public officials of the past 50 years.

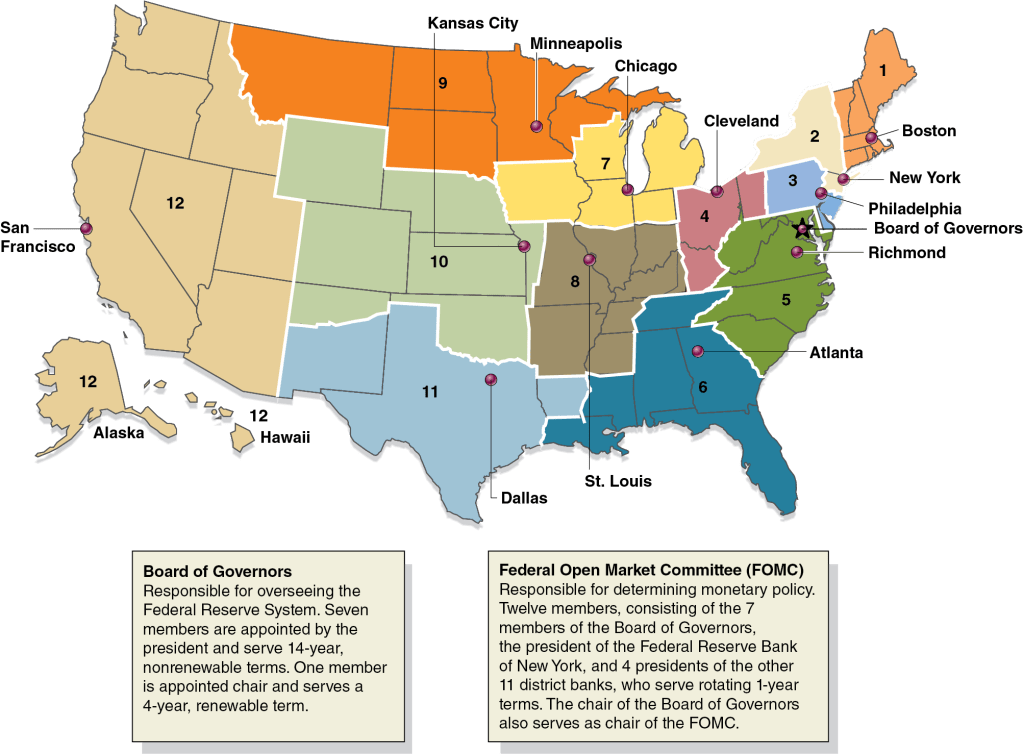

Greenspan served as Fed chair for 18 years and 5 months, a term in office exceeded only by William McChesney Martin who served as chair for 5 months longer. The Federal Reserve Act requires that the president choose as chair a member of the Fed’s Board of Governors. As we discuss in Macroeconomics, Chapter 14, Section 14.4 (Economics, Chapter 24, Section 24.4, and Money, Banking, and the Financial System, Chapter 13, Section 13.1), after being nominated by the president and confirmed by the Senate, members of the Board of Governors serve 14-year, nonrenewable terms. The following figure, reproduced from Chapter 14, illustrates the structure of the Fed.

If members of the Board of Governs serve a single 14-year term, how did both Greenspan and Martin serve for more than 18 years? The answer is that, although a member of the Board of Governors cannot be nominated to a second term, someone who serves out the remainder of the term of a member who has left the board can be nominated by the president to a full term. In August 1987, Greenspan was nominated by President Ronald Reagan to fill the remainder of Paul Volcker’s term on the Board of Governors and to replace Volcker as chair. Volcker had been nominated by President Jimmy Carter in 1979 to the unexpired term of G. William Miller. When the Miller/Volcker/Greenspan term expired in 1992, President George H. W. Bush nominated Greenspan to a new 14-year term. Volcker stepped down from the Board of Governors in 1987 after deciding that he would not ask President Reagan to nominate him to a third term as chair. (In this oral history, Volcker discusses the somewhat ambiguous circumstances under which he came to his decision.)

Greenspan served out the 4 years and 5 months that remained in the Miller/Volcker term and then served the 14 years of his own term. When his term expired in January 2006, President George W. Bush nominated Ben Bernanke to take Greenspan’s place as chair. One other institutional note: It’s sometimes written that the chair of the Board of Governors is automatically the chair of the Federal Open Market Committee. In fact, under the Federal Reserve Act, the FOMC chooses its own chair. In practice, though, the chair of the Board of Governors has always been elected chair by the members of the FOMC, as happened in May when Warsh began his term of chair of the Board of Governors and was voted chair by the members of the FOMC.

Photo of Paul Volcker from federalreserve.gov

During his time as chair, economists, Fed watchers on Wall Street, and members of Congress generally commended Greenspan’s performance. In particular, Greenspan received praise for his handling of the 1987 stock market crash, the failure of the Long-Term Capital Management hedge fund in 1997, and the foreign debt crises in the 1990s and early 2000s involving Mexico, several Asian countries, Russia, and Argentina. In July 1995, Greenspan began the modern procedure of explicitly stating the FOMC’s target for the federal funds rate after each meeting. Prior to that time, financial analysts and economists tried to determine the target federal funds rate by observing the size of the Fed’s New York Trading Desk transactions with primary dealers and by determining how much banks were charging each other for short-term loans in the federal funds market. In 2001, journalist Bob Woodward wrote a very favorable account of Greenspan’s role as Fed chair in the book Maestro: Greenspan’s Fed and the American Boom.

Photo from Amazon.com

Greenspan’s reputation was dimmed by the severity of the Global Financial Crisis of 2007–2009, which began nearly two years after his term of office. Greenspan was criticized for having kept the target for the federal funds rate too low in the years following the 2001 recession. Critics argue that low borrowing costs increased the amount of speculation in financial markets. Greenspan was also criticized for the Fed’s failure to use its legal authority to more closely regulate the mortgage market, which might have stopped mortgage lenders from weakening credit standards, thereby increasing the number of borrowers who would have difficulty making payments on their mortgages if housing prices declined. Greenspan also resisted increased regulation of financial derivatives, particularly those not traded on financial markets. During the financial crisis, the rapidly falling prices of some derivatives undermined the solvency of some financial firms. (In Money, Banking, and the Financial System, we discuss derivative markets in Chapter 7.)

A brief biography of Greenspan can be found here. A useful overview of Greenspan’s career is given in this article by Nick Timiraos in the Wall Street Journal. (A subscription may be required.)

When Kevin Warsh was sworn in as Fed chair, Greenspan was the only one of his predecessors that he mentioned by name, despite Warsh having served several years on the Board of Governors when Ben Bernanke was Fed chair. On several occasions, Warsh has praised Greenspan for resisting pressure during the 1990s to raise the target for the federal funds rate. During that period, Greenspan believed, correctly, that the information revolution resulting from the spread of personal computers and the greater use of the internet meant that real GDP and employment could increase rapidly without leading to an increase in inflation. Warsh believes that the AI revolution has put the Fed in a similar situation today. According to an article in the Financial Times, “Warsh predicts the AI boom will upend the world of work quickly, with the best companies doing ‘things that are unimaginable’ within a year.”

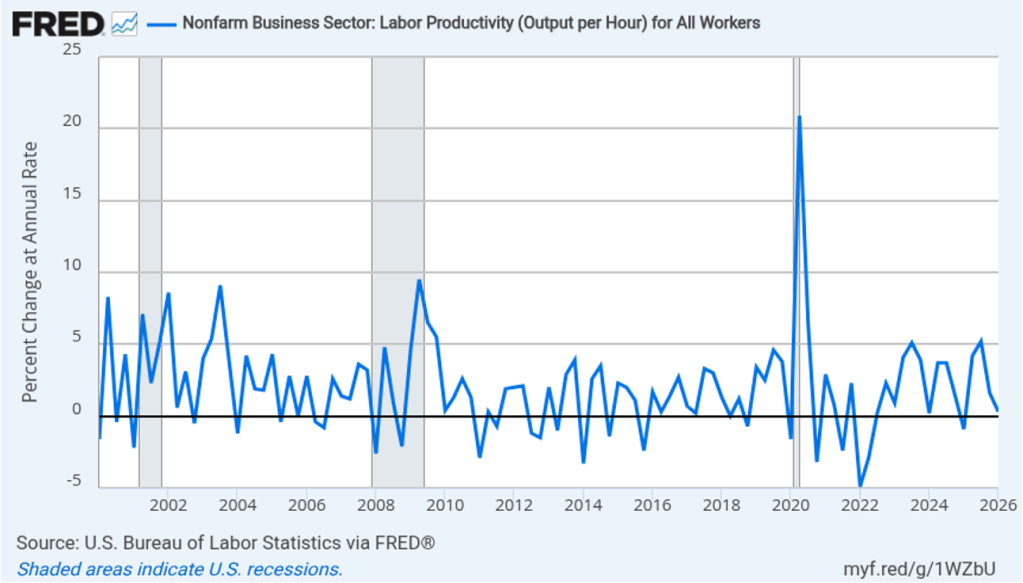

Warsh argues that rising productivity from the spread of AI will allow the Fed to keep the target for the federal funds rate lower without risking rising inflation in a way similar to Greenspan’s policy in the 1990s. The following figure shows productivity growth, as measured by the annual rate of change of output per hour worked for the nonfarm business sector, during the period from the first quarter of 2000 through the first quarter of 2026. Productivity has grown at an annual rate of 2.6 percent since the first quarter of 2023 as opposed to a rate of 2.0 percent for the whole period since 2000.

Productivity moves erratically over short periods, so it’s not yet clear whether AI, in fact, will cause a sustained increase in output per hour worked. Many economists argue that over the short run, AI may be increasing demand more than it is increasing supply. The most important effect of AI to this point might be the surge in demand for data centers, which accounts for more than a third of new capital investment. In addition, Warsh’s remarks at his press conference following the last FOMC meeting made it clear that his top priority is to bring inflation back to the Fed’s 2 percent target. Investors trading in the federal funds futures market now assign a 60 percent probability to the FOMC raising its target for the federal funds rate at its September meeting.

If Warsh intends to follow Greenspan’s strategy of keeping interest rates low to facilitate rapid economic growth during a surge in productivity, he likely won’t begin doing so until well into 2027.

An image generated by ChatGTP-4o of a hypothetical meeting between President Richard Nixon and Fed Chair Arthur Burns in the White House.

In a speech on April 15 at the Economic Club of Chicago, Federal Reserve Chair Jerome Powell discussed how the Fed might react to President Donald Trump’s tariff increases: “Tariffs are highly likely to generate at least a temporary rise in inflation. The inflationary effects could also be more persistent…. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.”

Powell’s remarks were interpreted as indicating that the Fed’s policymaking Federal Open Market Committee (FOMC) was unlikely to cut its target for the federal funds rate anytime soon. President Trump, who has stated several times that the FOMC should cut its target, was displeased with Powell’s position and posted on social media that “Powell’s termination cannot come fast enough!” Stock prices declined sharply on the possibility that Trump might try to fire Powell because many economists and market participants believed that move would increase uncertainty and possibly undermine the FOMC’s continuing attempts to bring inflation down to the Fed’s 2 percent target. Trump, possibly responding to the fall in stock prices, stated to reporters that he had “no intention” of firing Powell. In this recent blog post we discuss the debate over whether presidents can legally fire Fed chairs.

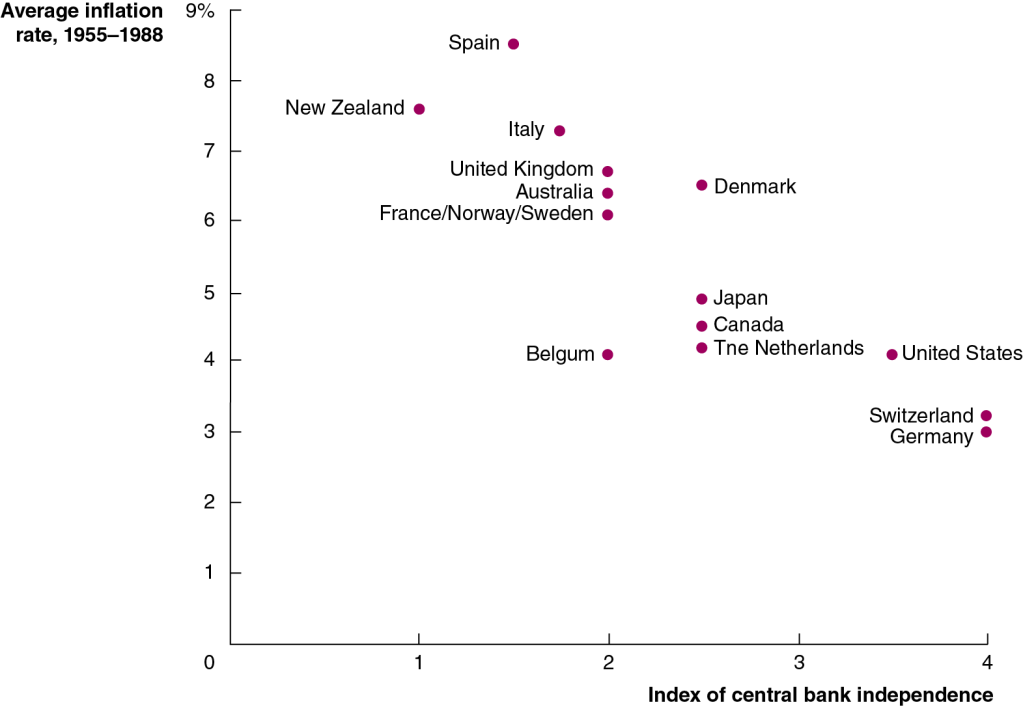

Leaving aside the legal issue of whether a president can fire a Fed chair, would it be better or worse for the conduct of monetary if the presdient did have that power? We review the arguments for and against the Fed conducting monetary policy independently of the president and Congress in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4). One key point that’s often made in favor of Fed independence is illustrated in Figure 17.12, which is reproduced below.

The figure is from a classic study by Alberto Alesina and Lawrence Summers, who were both economists at Harvard University at the time. Alesina and Summers tested the assertion that the less independent a country’s central bank, the higher the country’s inflation rate will be by comparing the degree of central bank independence and the inflation rate for 16 high-income countries during the years from 1955 to 1988. As the figure shows, countries with highly independent central banks, such as the United States, Switzerland, and Germany, had lower inflation rates than countries whose central banks had little independence, such as New Zealand, Italy, and Spain. In the following years, New Zealand and Canada granted their banks more independence, at least partly to better fight inflation.

Debates over Fed independence didn’t start with President Trump and Fed Chair Powell; they date all the way back to the passage of the Federal Reserve Act in 1913. The background to the passage of the Act is the political struggle over establishing a central bank during the early years of the country. In 1791, Congress established the Bank of the United States, at the urging of the country’s first Treasury secretary, Alexander Hamilton. When the bank’s initial 20-year charter expired in 1811, political opposition kept the charter from being renewed, and the bank went out of existence. The bank’s opponents believed that the bank’s actions had the effect of reducing loans to farmers and owners of small businesses and that Congress had exceeded its constitutional authority in establishing the bank. Financial problems during the War of 1812 led Congress to charter the Second Bank of the United States in 1816. But, again, political opposition, this time led by President Andrew Jackson, resulted in the bank’s charter not being renewed in 1836.

As we discuss in Chapter 14, Section 14.4, Congress established the Federal Reserve as a lender of last resort to bring an end to bank panics. In 1913, Congress was less concerned aboout making the Fed independent from Congress and the president than it was in overcoming political opposition to establishing a central bank located in Washington, DC. Accordingly, Congress established a decentralized system by having 12 District Banks that would be owned by the member banks in the district. Congress gave the responsibility for overseeing the system to the Federal Reserve Board, which was the forerunner of the current Board of Governors. The president had a greater influence on the Federal Reserve Board than presidents today have on the Board of Governors because the Federal Reserve Board included the secretary of the Treasury and the comptroller of the currency as members. Then as now, the president is free to replace the secretary of the Treasury and the comptroller of the currency at any time.

When the United States entered World War I in April 1917, the Fed came under pressure to help the Treasury finance the war by making loans to banks to help the banks purchase Treasury securities—Liberty Bonds—and by lending funds to banks that banks could loan to households to purchase bonds. In 1919, a ruling by the attorney general clarified that Congress had intended in the Federal Reserve Act to give the Federal Reserve Board the power to set the discounts rate the 12 District Banks charged member banks on loans.

Despite this ruling, authority within the Fed remained much more divided than is true today. Divided authority proved to be a serious problem when the Fed had to deal with the Great Depression, which began in August 1929 and worsened as the result of a series of bank panics. As we’ve seen, the secretary of the Treasury and the comptroller of the currency, both of whom report directly to the president of the United States, served on the Federal Reserve Board. So, the Fed had less independence from the executive branch of the government than it does today.

In addition, the heads of the 12 District Banks operated much more independently than they do today, with the head of the Federal Reserve Bank of New York having nearly as much influence within the system as the head of the Federal Reserve Board. At the time of the bank panics, George Harrison, the head of the Federal Reserve Bank of New York, served as chair of the Open Market Policy Conference, the predecessor of the current Federal Open Market Committee. Harrison frequently acted independently of Roy Young and Eugene Meyer, who served as heads of the Federal Reserve Board during those years. Important decisions could be made only with the consensus of these different groups. During the early 1930s, consensus proved hard to come by, and taking decisive policy actions was difficult.

The difficulties the Fed had in responding to the Great Depression led Congress to reorganize the system with the passage of the Banking Act of 1935. Most of the current structure of the Fed was put in place by that law. Power was concentrated in the hands of the Board of Governors. The removal of the secretary of the Treasury and the comptroller of the currency from the Board reduced the ability of the president to influence the Fed’s decisions.

During World War II, the Fed again came under pressure to help the federal government finance the war. The Fed agreed to hold interest rates on Treasury securities at low levels: 0.375% on Treasury bills and 2.5% on Treasury bonds. The Fed could keep interest rates at these low levels only by buying any bonds that were not purchased by private investors, thereby fixing, or pegging, the rates.

When the war ended in 1945, the Treasury and President Harry Truman wanted to continue this policy, but the Fed didn’t agree. The Fed’s concern was inflation: Larger purchases of Treasury securities by the Fed could increase the growth rate of the money supply and the rate of inflation. Fed Chair Marriner Eccles strongly objected to the policy of fixing interest rates. His opposition led President Truman to not reappoint him as chair in 1948,although Eccles continued to fight for Fed independence during the remainder of his time as a governor. On March 4, 1951, the federal government formally abandoned the wartime policy of fixing the interest rates on Treasury securities with the Treasury–Federal Reserve Accord. This agreement was important in eestablishing the Fed’s ability to operate independently of the Treasury.

Conflicts between the Treasury and the Fed didn’t end with that agreement, however. Thomas Drechsel of the University of Maryland has analyzed the daily schedules of presidents during the period from 1933 to 2016 and finds that during these years presidents met with Fed officials on more than 800 occasions. Of course, not all of these interactions involved attempts by a president to influence the actions of a Fed Chair, but some seem to have. For example, research by Helen Fessenden of the Federal Reserve Bank of Richmond has shown that in 1967, President Lyndon Johnson, who was facing reelection in 1968, was anxious that Fed Chair William McChesney Martin adopt a more expansionary monetary policy. There is some evidence that Johnson and Martin came to an agreement that if Johnson agreed to push Congress to increase taxes, Martin would pursue an expansionary monetary policy.

An image generated by ChatGTP-4o of a hypothetical meeting between President Lyndon Johnson and Fed Chair William McChesney Martin in the White House.

Similarly, in late 1971, President Richard Nixon was concerned that the unemployment rate was at 6%, which he believed would, if it persisted, endanger his chance of reelection in 1972. Dreschel finds that Nixon met with Fed Chair Arthur Burns 34 times during the second half of 1971. Evidence from tape recordings of Nixon’s conversations with Burns at the White House and from Burns’s diary entries indicate that Nixon pressured Burns to increase the rate of growth of the money supply and that Burns agreed to do so.

President Ronald Reagan and Federal Reserve Chair Paul Volcker argued over who was at fault for the severe economic recession of the early 1980s. Reagan blamed the Fed for soaring interest rates. Volcker held that the Fed could not take action to bring down interest rates until the budget deficit—which results from policy actions of the president and Congress—was reduced. Similar conflicts occurred during the administrations of George H.W. Bush and Bill Clinton, with the Treasury frequently pushing for lower short-term interest rates than the Fed considered advisable.

During the financial crisis of 2007–2009 and during the 2020 Covid pandemic, the Fed worked closely with the Treasury. The relationship was so close, in fact, that some economists and policymakers worried that the Fed might be sacrificing some of its independence. The frequent consultations between Fed Chair Ben Bernanke and Treasury Secretary Henry Paulson in the fall of 2008, during the height of the crisis, were a break with the tradition of Fed chairs formulating policy independently of a presidential administration. During the 2020 pandemic, Fed Chair Jerome Powell and Treasury Secretary Steven Mnuchin also frequently consulted on policy.

These examples from the Fed’s history indicate that presidents have persistently attempted to influence Fed policy. Most economists believe that central bank independence is an important check on inflation. But, given the importance of monetary policy, it’s probably inevitable that presidents and members of Congress will continue to attempt to sway Fed policy.

Authors Glenn Hubbard and Tony O’Brien reconsider the role of inflation in today’s economy. They discuss the Fed’s possible responses by considering responses to similar inflation threats in previous generations – notably the Fed’s response led by Paul Volcker that directly led to the early 1980’s recession. The markets are reflecting stark differences in our collective expectations about what will happen next. Listen to find out more about the Fed’s likely next steps.

It now seems clear that the new monetary policy strategy the Fed announced in August 2020 was a decisive break with the past in one respect: With the new strategy, the Fed abandoned the approach dating to the 1980s of preempting inflation. That is, the Fed would no longer begin raising its target for the federal funds rate when data on unemployment and real GDP growth indicated that inflation was likely to rise. Instead, the Fed would wait until inflation had already risen above its target inflation rate.

Since 2012, the Fed has had an explicit inflation target of 2 percent. As we discussed in a previous blog post, with the new monetary policy the Fed announced in August 2020, the Fed modified how it interpreted its inflation target: “[T]he Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

The Fed’s new approach is sometimes referred to as average inflation targeting (AIT) because the Fed attempts to achieve its 2 percent target on average over a period of time. But as former Fed Vice Chair Richard Clarida discussed in a speech in November 2020, the Fed’s monetary policy strategy might be better called a flexible average inflation target (FAIT) approach rather than a strictly AIT approach. Clarida noted that the framework was asymmetric, meaning that inflation rates higher than 2 percent need not be offset with inflation rates lower than 2 percent: “The new framework is asymmetric. …[T]he goal of monetary policy … is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent.” And: “Our framework aims … for inflation to average 2 percent over time, but it does not make a … commitment to achieve … inflation outcomes that average 2 percent under any and all circumstances ….”

Inflation began to increase rapidly in mid-2021. The following figure shows three measure of inflation, each calculated as the percentage change in the series from the same month in the previous year: the consumer price index (CPI), the personal consumption expenditure (PCE) price index, and the core PCE—which excludes the prices of food and energy. Inflation as measured by the CPI is sometimes called headline inflation because it’s the measure of inflation that most often appears in media stories about the economy. The PCE is a broader measure of the price level in that it includes the prices of more consumer goods and services than does the CPI. The Fed’s target for the inflation rate is stated in terms of the PCE. Because prices of food and inflation fluctuate more than do the prices of other goods and services, members of the Fed’s Federal Open Market Committee (FOMC) generally consider changes in the core PCE to be the best measure of the underlying rate of inflation.

The figure shows that for most of the period from 2002 through early 2021, inflation as measured by the PCE was below the Fed’s 2 percent target. Since that time, inflation has been running well above the Fed’s target. In February 2022, PCE inflation was 6.4 percent. (Core PCE inflation was 5.4 percent and CPI inflation was 7.9 percent.) At its March 2022 meeting the FOMC begin raising its target for the federal funds rate—well after the increase in inflation had begun. The Fed increased its target for the federal funds rate by 0.25 percent, which raised the target from 0 to 0.25 percent to 0.25 to 0.50 percent.

Should the Fed have taken action to reduce inflation earlier? To answer that question, it’s first worth briefly reviewing Fed policy during the Great Inflation of 1968 to 1982. In the late 1960s, total federal spending grew rapidly as a result of the Great Society social programs and the war in Vietnam. At the same time, the Fed increased the rate of growth of the money supply. The result was an end to the price stability of the 1952-1967 period during which the annual inflation rate had averaged only 1.6 percent.

The 1973 and 1979 oil price shocks also contributed to accelerating inflation. Between January 1974 and June 1982, the annual inflation rate averaged 9.3 percent. This was the first episode of sustained inflation outside of wartime in U.S. history—until now. Although the oil price shocks and expansionary fiscal policy contributed to the Great Inflation, most economists, inside and outside of the Fed, eventually concluded that Fed policy failures were primarily responsible for inflation becoming so severe.

The key errors are usually attributed to Arthur Burns, who was Fed Chair from January 1970 to March 1978. Burns, who was 66 at the time of his appointment, had made his reputation for his work on business cycles, mostly conducted prior to World War II at the National Bureau of Economic Research. Burns was skeptical that monetary policy could have much effect on inflation. He was convinced that inflation was mainly the result of structural factors such as the power of unions to push up wages or the pricing power of large firms in concentrated industries.

Accordingly, Burns was reluctant to raise interest rates, believing that doing so hurt the housing industry without reducing inflation. Burns testified to Congress that inflation “poses a problem that traditional monetary and fiscal remedies cannot solve as quickly as the national interest demands.” Instead of fighting inflation with monetary policy he recommended “effective controls over many, but by no means all, wage bargains and prices.” (A collection Burns’s speeches can be found here.)

Few economists shared Burns’s enthusiasm for wage and price controls, believing that controls can’t end inflation, they can only temporarily reduce it while causing distortions in the economy. (A recent overview of the economics of price controls can be found here.) In analyzing this period, economists inside and outside the Fed concluded that to bring the inflation rate down, Burns should have increased the Fed’s target for the federal funds rate until it was higher than the inflation rate. In other words, the real interest rate, which equals the nominal—or stated—interest rate minus the inflation rate, needed to be positive. When the real interest rate is negative, a business may, for example, pay 6% on a bond when the inflation rate is 10%, so they’re borrowing funds at a real rate of −4%. In that situation, we would expect borrowing to increase, which can lead to a boom in spending. The higher spending worsens inflation.

Because Burns and the FOMC responded only slowly to rising inflation, workers, firms, and investors gradually increased their expectations of inflation. Once higher expectation inflation became embedded, or entrenched, in the U.S. economy it was difficult to reduce the actual inflation rate without increasing the target for the federal funds rate enough to cause a significant slowdown in the growth of real GDP and a rise in the unemployment rate. As we discuss in Macroeconomics, Chapter 17, Sections 17.2 and 17.3 (Economics, Chapter 27, Sections 27.2 and 27.3), the process of the expected inflation rate rising over time to equal the actual inflation rate was first described in research conducted separately by Nobel Laureates Milton Friedman and Edmund Phelps during the 1960s.

An implication of Friedman and Phelps’s work is that because a change in monetary policy takes more than a year to have its full effect on the economy, if the Fed waits until inflation has already increased, it will be too late to keep the higher inflation rate from becoming embedded in interest rates and long-term labor and raw material contracts.

Paul Volcker, appointed Fed chair by Jimmy Carter in 1979, showed that, contrary to Burns’s contention, monetary policy could, in fact, deal with inflation. By the time Volcker became chair, inflation was above 11%. By raising the target for the federal funds rate to 22%—it was 7% when Burns left office—Volcker brought the inflation rate down to below 4%, but only at the cost of a severe recession during 1981–1982, during which the unemployment rate rose above 10 percent for the first time since the Great Depression of the 1930s. Note that whereas Burns had largely failed to increase the target for the federal funds as rapidly as inflation had increased—resulting in a negative real federal funds rate—Volcker had raised the target for the federal funds rate above the inflation rate—resulting in a positive real federal funds rate.

Because the 1981–1982 recession was so severe, the inflation rate declined from above 11 percent to below 4 percent. In Chapter 17, Figure 17.10 (reproduced below), we plot the course of the inflation and unemployment rates from 1979 to 1989.

Caption: Under Chair Paul Volcker, the Fed began fighting inflation in 1979 by reducing the growth of the money supply, thereby raising interest rates. By 1982, the unemployment rate had risen to 10 percent, and the inflation rate had fallen to 6 percent. As workers and firms lowered their expectations of future inflation, the short-run Phillips curve shifted down. The adjustment in expectations allowed the Fed to switch to an expansionary monetary policy, which by 1987 brought unemployment back to the natural rate of unemployment, with an inflation rate of about 4 percent. The orange line shows the actual combinations of unemployment and inflation for each year from 1979 to 1989.

The Fed chairs who followed Volcker accepted the lesson of the 1970s that it was important to head off potential increases in inflation before the increases became embedded in the economy. For instance, in 2015, then Fed Chair Janet Yellen in explaining why the FOMC was likely to raise to soon its target for the federal funds rate noted that: “A substantial body of theory, informed by considerable historical evidence, suggests that inflation will eventually begin to rise as resource utilization continues to tighten. It is largely for this reason that a significant pickup in incoming readings on core inflation will not be a precondition for me to judge that an initial increase in the federal funds rate would be warranted.”

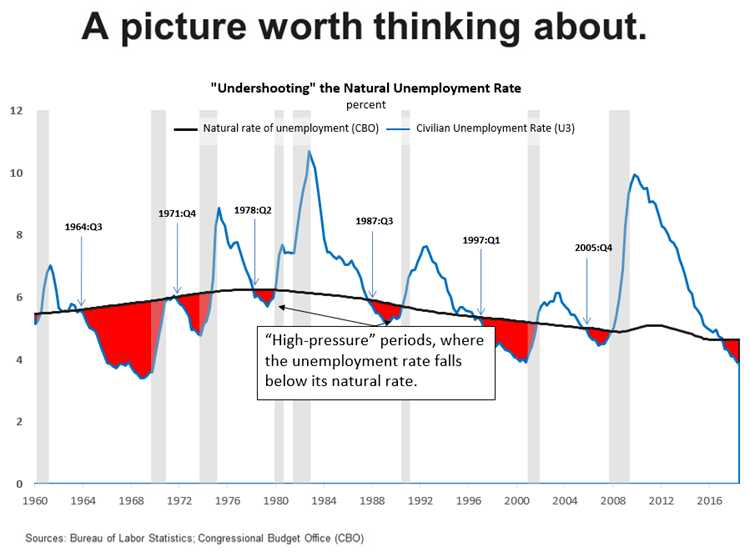

Between 2015 and 2018, the FOMC increased its target for the federal funds rate nine times, raising the target from a range of 0 to 0.25 percent to a range of 2.25 to 2.50 percent. In 2018, Raphael Bostic, president of the Federal Reserve Bank of Atlanta justified these rate increases by noting that “… we shouldn’t forget that [the Fed’s] credibility [with respect to keeping inflation low] was hard won. Inflation expectations are reasonably stable for now, but we know little about how far the scales can tip before it is no longer so.”

He used the following figure to illustrate his point.

Bostic interpreted the figure as follows:

“[The red areas in the figure are] periods of time when the actual unemployment rate fell below what the U.S. Congressional Budget Office now estimates as the so-called natural rate of unemployment. I refer to these episodes as “high-pressure” periods. Here is the punchline. Dating back to 1960, every high-pressure period ended in a recession. And all but one recession was preceded by a high-pressure period….

I think a risk management approach requires that we at least consider the possibility that unemployment rates that are lower than normal for an extended period are symptoms of an overheated economy. One potential consequence of overheating is that inflationary pressures inevitably build up, leading the central bank to take a much more “muscular” stance of policy at the end of these high-pressure periods to combat rising nominal pressures. Economic weakness follows [resulting typically, as indicated in the figure by the gray band, in a recession].”

By July 2019, a majority of the members of the FOMC, including Chair Powell, had come to believe that with no sign of inflation accelerating, they could safely cut the federal funds rate. But they had not yet explicitly abandoned the view that the FOMC should act to preempt increases in inflation. The formal change came in August 2020 when, as discussed earlier, the FOMC announced the new FAIT.

At the time the FOMC adopted its new monetary policy strategy, most members expected that any increase in inflation owing to problems caused by the Covid-19 pandemic—particularly the disruptions in supply chains—would be transitory. Because inflation has proven to be more persistent than Fed policymakers and many economists expected, two aspects of the FAIT approach to monetary policy have been widely discussed: First, the FOMC did not explicitly state by how much inflation can exceed the 2 percent target or for how long it needs to stay there before the Fed will react. The failure to elaborate on this aspect of the policy has made it more difficult for workers, firms, and investors to gauge the Fed’s likely reaction to the acceleration in inflation that began in the spring of 2021. Second, the FOMC’s decision to abandon the decades-long policy of preempting inflation may have made it more difficult to bring inflation down to the 2 percent target without causing a recession.

Federal Reserve Governor Lael Brainard recently remarked that “it is of paramount importance to get inflation down” and some Fed policymakers believe that the FOMC will have to begin increasing its target for the federal funds rate more aggressively. (The speech in which Governor Brainard discusses her current thinking on monetary policy can be found here.) For instance James Bullard, president of the Federal Reserve Bank of St. Louis, has argued in favor of raising the target to above 3 percent this year. With the Fed’s preferred measure of inflation running above 5 percent, it would take substantial increases int the target to achieve a positive real federal funds rate.

It is an open question whether Jerome Powell finds himself in a position similar to that of Paul Volcker in 1979: Rapid increases in interest rates may be necessary to keep inflation from accelerating, but doing so risks causing a recession. In a recent speech (found here), Powell pledged that: “We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

But Powell argued that the FOMC could achieve “a soft landing, with inflation coming down and unemployment holding steady” even if it is forced to rapidly increase its target for the federal funds rate:

“Some have argued that history stacks the odds against achieving a soft landing, and point to the 1994 episode as the only successful soft landing in the postwar period. I believe that the historical record provides some grounds for optimism: Soft, or at least softish, landings have been relatively common in U.S. monetary history. In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession.”

Some economists have been skeptical that a soft landing is likely. Harvard economist and former Treasury Secretary Lawrence Summers has been particularly critical of Fed policy, as in this Twitter thread. Summers concludes that: “I am apprehensive that we will be disappointed in the years ahead by unemployment levels, inflation levels, or both.” (Summers and Harvard economist Alex Domash provide an extended discussion in a National Bureau of Economic Research Working Paper found here.)

Clearly, we are in a period of great macroeconomic uncertainty.