As we’ve discussed in several previous blog posts, in early 2021 Lawrence Summers, professor of economics at Harvard and secretary of the treasury in the Clinton administration, argued that the Biden administration’s $1.9 trillion American Rescue Plan, enacted in March, was likely to cause a sharp acceleration in inflation. When inflation began to rapidly increase, Summers urged the Federal Reserve to raise its target for the federal funds rate in order to slow the increase in aggregate demand, but the Fed was slow to do so. Some members of the Federal Open Market Committee (FOMC) argued that much of the inflation during 2021 was transitory in that it had been caused by lingering supply chain problems initially caused by the Covid–19 pandemic.

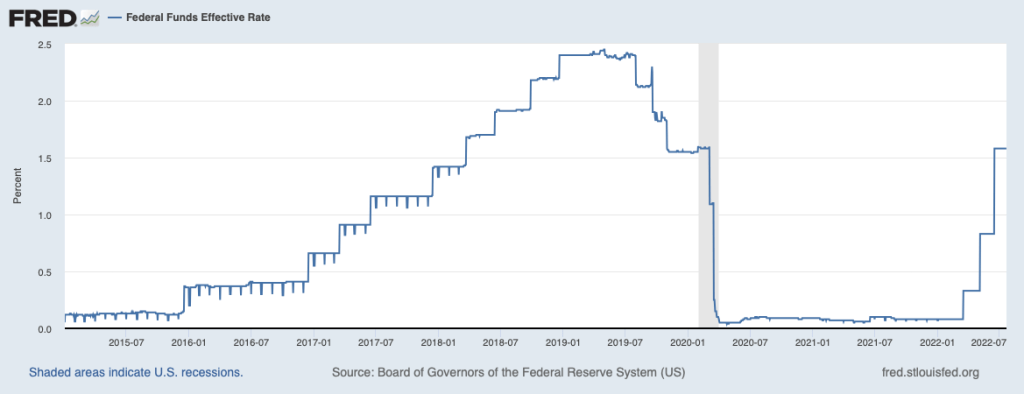

At the beginning of 2022, most members of the FOMC became convinced that in fact increases in aggregate demand were playing an important role in causing high inflation rates. Accordingly, the FOMC began increasing its target for the federal funds rate in March 2022. After two more rate increases, on the eve of the FOMC’s meeting on July 26–27, the federal funds rate target was a range of 1.50 percent to 1.75 percent. The FOMC was expected to raise its target by at least 0.75 percent at the meeting. The following figure shows movements in the effective federal funds rate—which can differ somewhat from the target rate—from January 1, 2015 to July 21, 2022.

In an opinion column in the Wall Street Journal, Massachusetts Senator Elizabeth Warren argued that the FOMC was making a mistake by increasing its target for the federal funds rate. She also criticized Summers for supporting the increases. Warren worried that the rate increases were likely to cause a recession and argued that Congress and President Biden should adopt alternative measures to contain inflation. Warren argued that a better approach to dealing with inflation would be to, among other steps, increase the federal government’s support for child care to enable more parents to work, provide support for strengthening supply chains, and lower prescription drug prices by allowing Medicare to negotiate the prices with pharmaceutical firms. She also urged a “crack down on price gouging by large corporations.” (We discussed the argument that monopoly power is responsible for inflation in this blog post.)

Summers responded to Warren in a Twitter thread. He noted that: “In the 18 months since the massive stimulus policies & easy money that [Senator Warren] has favored & I have opposed, the inflation rate has risen from below 2 to above 9 percent & workers purchasing power has, as a consequence, declined more rapidly than in any year in the last 50.” And “[Senator Warren] opposes restrictive monetary policy or any other measure to cool off total demand. Why does she think at a time when there are twice as many vacancies as jobs that inflation will come down without some drop in total demand?”

Clearly, economists and policymakers continue to hotly debate monetary policy.

Source: Elizabeth Warren, “Jerome Powell’s Fed Pursues a Painful and Ineffective Inflation Cure,” Wall Street Journal, July 24, 2022.