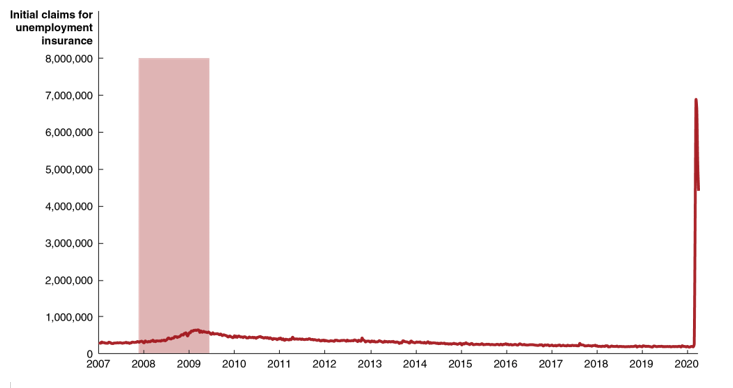

The spike in people losing their jobs and applying for unemployment insurance was primarily due to many mayors and governors ordering the closure of nonessential businesses to fight the spread of the Covid-19 disease caused by the coronavirus. Unemployment insurance payments vary across states but typically last for 26 weeks and are intended to replace about 50 percent of a worker’s wage, subject to a cap. In 2020, Congress and President Donald Trump enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act to provide funds to support firms and businesses suffering from the effects of the coronavirus pandemic. Included in the act was a provision to increase the normal state unemployment insurance payment by $600 per week for up to four months.

Congress and President Franklin Roosevelt created the U.S. unemployment insurance system during the Great Depression as part of the Social Security Act of 1935. The first payments were made in 1939. Congress has had two main goals in establishing and maintaining a system of unemployment insurance: (1) To provide the means for workers who have lost their jobs to continue to buy food, clothing, and other necessities; and (2) to help support the level of total spending in the economy to avoid making recessions worse. From the beginning, some members of Congress and some state legislators were concerned that payments to the unemployed would reduce the recipients’ incentive to quickly find a new job. In establishing the program in the 1930s, policymakers were influenced by the experience in England where high rates of unemployment throughout most of the 1920s had resulted in many people receiving government payments—being “on the dole”—for years. In reaction, most states established 26 weeks as the length of time the unemployed could receive payments and kept the amount of money at roughly half a worker’s previous wage.

Economists believe that any type of insurance results in moral hazard, which refers to the actions people take after they have entered into a transaction. In particular, insurance makes the event being insured against more likely. For instance, once a firm has purchased a fire insurance policy on a warehouse, it may choose not to install an expensive sprinkler system thereby increasing the chance that the warehouse will burn down. People with health insurance may visit a doctor for treatment of a cold or other minor illness, which they would not do if they lacked insurance. Similarly, moral hazard resulting from the unemployment insurance system may result in workers not accepting jobs that they would have taken in the absence of unemployment insurance.

Economists debate the extent to which the moral hazard involved in unemployment insurance has a significant effect on U.S. labor markets. Most studies indicate that unemployment does increase the length of time that workers are unemployed—the duration of spells of unemployment—thereby reducing the efficiency of the economy by decreasing the size of the labor force and the quantity of goods and services produced. But because unemployment insurance reduces the opportunity cost of searching for a job—since workers give up less income during the time they are searching—it may also result in a better fit between workers and jobs, thereby increasing worker productivity and economic efficiency. Most economists conclude that, on balance, unemployment insurance that lasts for only 26 weeks and replaces only 50 percent of previous income probably does not significantly reduce economic efficiency in the United States.

After passage of the CARES, some policymakers and economists again raised the issue of whether the unemployment insurance system provides disincentives for people to work. The additional $600 that an unemployed worker received under the CARES act increased the average unemployment insurance benefit from $378 per week to $978 per week. That income was equivalent to a wage of $24.45 per hour for a 40-hour week and was greater than the wage rate received by more than half of workers in the United States in early 2020, before the coronavirus pandemic began. As a result, some workers were reluctant to return to their previous jobs as some firms began to reopen during May.

A restaurant owner in Oregon noted that one of his cooks was receiving $376 more per week in unemployment insurance than he had earned working: “Why on earth would he want to come back to work?” The restaurant was having difficulty attracting enough workers to provide takeout and delivery services while the restaurant’s dining room was closed. As the head of the National Restaurant Association put it: “It’s not that these workers are lazy, they’re just making the best economic decision for their families.”

Some firms that were unsure whether to continue to employ workers during the period the firms were ordered closed. Retaining workers would make it easier to restart once mayors and governors had lifted restrictions on operating. But the availability of higher unemployment insurance payments made some of these firms decide to lay off workers instead. For example, according to an article in the Wall Street Journal, Macy’s chief executive stated that “the new benefits in the federal stimulus program played a role in the company’s decision to furlough 125,000 workers this past week.”

The supplementary unemployment insurance payments included in the CARES act succeeded in cushioning the income losses workers suffered from the layoffs during the pandemic, but they had also made it more likely that firms would lay off workers and made some workers more reluctant to return to work. Given that the additional $600 payments were scheduled to end after four months, it remained unclear whether the payments would have a lasting effect on the U.S. labor market.

Sources: Kurt Huffman, “Our Restaurants Can’t Reopen Until August,” Wall Street Journal, April 12, 20202; Eric Morath, “Coronavirus Relief Often Pays Workers More Than Work,” Wall Street Journal, April 28, 2020; Patrick Thomas and Chip Cutter, “Companies Cite New Government Benefits in Cutting Workers,” Wall Street Journal, April 7, 2020; Henry S. Farber and Robert G. Valletta, “Do Extended Unemployment Benefits Lengthen Unemployment Spells? Evidence from Recent Cycles in the U.S. Labor Market,” Journal of Human Resources, Vol. 50, No. 4, Fall 2015, pp. 873-909; Congressional Budget Office, “Understanding and Responding to Persistently High Unemployment,” February 2012; Daniel N. Price, “Unemployment Insurance, Then and Now, 1935-85,” Social Security Bulletin, Vol. 48, No. 10, October 1985, pp. 22-32; and Federal Reserve Bank of St. Louis.

Question: An article published in the New York Times during April 2020, quoted a policy analyst as stating that: “I would never two months ago have ever thought of advocating for 100 percent income replacement.”

- What does the analyst mean by “100 percent income replacement”?

- Why during an economic expansion or mild economic recession would most policymakers be reluctant to adopt a policy of 100 percent income replacement?

- Are there benefits to such a policy during an economic expansion or mild economic recessions? How is the desirability of such a policy affected if the economy is in a severe recession?

Source: Ella Koeze, “The $600 Unemployment Booster Shot, State by State,” New York Times, April 23, 2020.