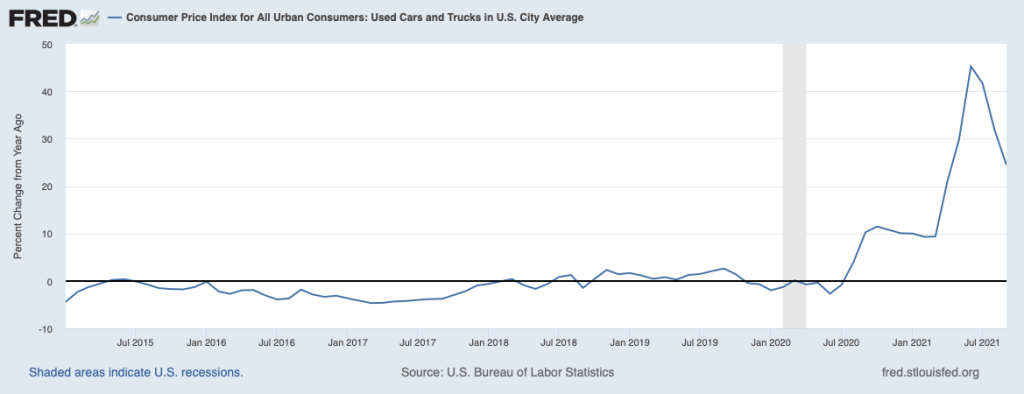

The term “sticker shock” was first used during the 1970s to describe the surprise car buyers experienced when seeing how much car prices had risen. Because inflation during that decade was so high, anyone who hadn’t bought a car for several years was unprepared for the jump in car prices. During 2020 and 2021, sticker shock returned, particularly to the used car market. Prices were increasing so rapidly that even people who had purchased a car a year or two before were surprised by the increases.

The following graph shows U.S. Bureau of Labor Statistics (BLS) data on inflation in the market for used cars in the months since January 2015. Inflation is measured as the percent change from the same month in the previous year in the used cars and trucks component of the Consumer Price Index (CPI). The CPI is the most widely used measure of inflation. Used car prices began rising in August 2020, peaking at a 45 percent increase in June 2021. Inflation at such rates over a period longer than a year is very unusual in any of components of the CPI.

What explains the extraordinary burst of inflation in used car prices during 2020 and 2021? Three factors seem to have been of greatest importance:

A decline in the supply of new cars resulting from a shortage in semiconductors caused an increase in new car prices. Rising new car prices led some consumers who would otherwise have bought a new car to enter the used car market, increasing the demand for used cars.

Because of the Covid-19 pandemic, some people became reluctant to ride buses and other mass transit, increasing the demand for both new and used cars.

As the pandemic increased in severity in the spring of 2020, most rental car companies decided to purchase fewer new cars for their fleets. After keeping a car in its fleet for one year, rental car companies typically sell the car to used car dealers for resale. Because rental car companies were selling them fewer cars, used car dealers had fewer cars on their lots. So the supply of used cars declined.

We can use the demand and supply model to explain the jump in used car prices. As shown in the following figure, the demand curve for used cars shifted to the right from D1 to D2, as some consumers who would otherwise have bought new cars, bought used cars instead, and as some people swithced from public transportation to driving their cars to work. At the same time, the supply of used cars shifted to the left from S1 to S2 because used car dealers were able to buy fewer used cars from rental car companies. The result was that the price of used cars rose from P1 to P2 at the same time that the quantity of used cars sold fell from Q1 to Q2.

Sources: Yueqi Yang, “U.S. Used-Car Prices, Key Inflation Driver, Surge to Record,” bloomberg.com, October 7, 2021; Nora Naughton, “Looking to Buy a Used Car? Expect High Prices, Few Options,” wsj.com, May 10, 2021; Cox Automotive, “13-Month Rolling Used-Vehicle SAAR,” coxautoinc.com, October 15, 2021; and Federal Reserve Bank of St. Louis.

In Economics, Chapter 10, Section 10.4, when discussing behavioral economics, we mentioned Richard Thaler’s idea of nudges, which are small changes that government policymakers or business managers can make that may affect people’s behavior. Underlying the concept of nudges is the assumption that at least some of the time people may not be making fully rational decisions (We discuss in the chapter the reasons why people may not always make fully rational decisions.) An example of a nudge is a business automatically enrolling employees into retirement savings plans to overcome the tendency of many people to be unrealistic about their future behavior.

Once vaccines for the Covid-19 virus became widely available to the general adult population in 2021, some government policymakers were concerned that not enough people were being vaccinated to quickly curb the pandemic. Some people who declined to be vaccinated had carefully thought through the decision and declined the vaccine either because they believed they were at only a small risk of developing a severe case of Covid-19 or for other reasons. But some people who were not vaccinated intended eventually to receive the injection but for various reasons had not yet done so. The second group were potentially candidates for being nudged into becoming vaccinated.

A recent National Bureau of Economic Research working paper by Tom Chang of the University of Southern California and colleagues reports an experiment that measured the effect of nudges intended to increase the likelihood of someone becoming vaccinated. The study was conducted in Contra Costa Country in northern California with 2,700 Medicaid (a state run system of health care offered to people with low incomes) recipients who agreed to participate. The study took place between May and July 2021 after all adults in the county had been eligible for several weeks to receive a vaccine. Half the people involved in the experiment received three nudges: 1) a video noting the positive effects of being vaccinated, 2) a financial incentive of either $10 or $50 if they received a vaccination within two weeks, and 3) “a highlighted convenient link to the county’s new public vaccination appointment scheduling system or just a message about getting vaccinated without a link.” The other half of the people involved in the experiment received none of these nudges.

The authors’ statistical analysis of the results of the experiment indicates that none of the nudges individually or in combination significantly raised vaccination rates. Do these results show conclusively that nudges are ineffective in increasing Covid-19 vaccination rates? The authors note that the people involved in this experiment were not representative of the U.S. population. All had low incomes (which made them eligible for Medicaid), they were relatively young, and were more likely to be Black or Hispanic than is true of the overall U.S. population. The study also took place just before the peak in the spread of the Delta variant of Covid-19 at a time when infection rates appeared to be declining. So, while for these reasons the study cannot be called a definitive, it does provide some evidence that nudges may not be effective in changing behavior towards vaccinations.

Source: Tom Chang, Mireille Jacobson, Manisha Shah, Rajiv Pramanik, and Samir B. Shah, “Financial Incentives and other Nudges Do Not Increase Covid-19 Vaccinations among the Vaccine Hesitant,” National Bureau of Economic Research, Working Paper 29403, October 2021.

In 1901, U.S. Steel became the world’s first corporation with a stock market value greater than $1 billion. In October 2021, Tesla joined Alphabet (Google’s corporate parent), Amazon, Apple, and Microsoft as the only U.S. corporations whose stock market value exceeds $1 trillion. (The Saudi Arabian Oil Company is the only non-U.S. firm with a market value above $1 trillion.)

As large U.S. corporations developed in the late nineteenth and early twentieth centuries, a key problem facing them was how to allocate the firms’ scarce financial capital across competing uses. (A thorough—and lengthy!—discussion of the development of the modern U.S. corporation is Alfred Chandler’s book, The Visible Hand: The Managerial Revolution in American Business.) By 1940, many large corporations had formed executive committees comprised of the chief executive officer (CEO), the chief operating officer (COO), and other so-called C-suite executives.

Executive committees typically don’t become involved in the day-to-day operations of the firms, leaving those responsibilities to lower level managers. Instead, executive committees devote most of their time to strategic issues such as whether to introduce new products, where to locate sales and production facilities, and how much of the firm’s resources to devote to research and development and to marketing. The decisions that an executive committee concentrates on involve how best to allocate the firm’s financial capital, funds that come from investors who buy the firm’s stocks and bonds and from the firm’s retained earnings—the firm’s profits that aren’t distributed as dividends to the firm’s shareholders. In allocating these funds, executive committees face trade-offs of the type we discuss in Chapter 2. For instance, if a U.S.-based firm uses funds to build a factory in another country, it may not have the funds to expand its domestic factories.

Allocating the firm’s financial capital will not have much effect on the firm’s profits in the short run but can be the main determinant of the firm’s profitability—and even its survival—in the long run. For instance, the failure of Blockbuster Video to expand into offering rentals of DVDs by mail or to offering a movie streaming service, resulted in the company shrinking from having 4,000 stores in the early 2000s to a single store today. In contrast, the decision in 2018 by U.S. pharmaceutical firm Pfizer to partner with BioNTech, a small German firm, to develop vaccines using messenger RNA (or mRNA) biotechnology proved very profitable for Pfizer (and saved many lives) when the Covid-19 virus led to a worldwide epidemic.

At Tesla, CEO Elon Musk has final say on strategic decisions, a situation typical of many large firms where a single executive, through stock ownership, has control of the company. One of his key decisions has been where to locate his production facilities. In making this decision, Musk faces trade-offs in how to use the scarce funds the firm has available for expanding production capacity. Building a facility in one place means not being able to fund building a facility in another place. In addition, funds used to build new factories is not available to increase research and development on autonomous cars or on other improvements to car design or technology.

Initially, Tesla operated a single factory in Fremont, California. Built in 1962, the factory had been owned by General Motors and then jointly by GM and Toyota before being sold to Tesla in 2010. In 2019, Tesla began construction of a second factory in Shanghai, China and in 2021 was awaiting final governmental approval to build a factory in Grünheide, Germany.

Why would Tesla, or another U.S. firm, decide to build factories in other countries? The simplest answer is that firms expand their operations outside the United States when they expect to increase their profitability by doing so. Today, most large U.S. corporations are multinational firms with factories and other facilities overseas. Firms might expect to increase their profits through overseas operations for five main reasons:

To avoid tariffs or the threat of tariffs. Tariffs are taxes imposed by countries on imports from other countries. Sometimes firms establish factories in other countries to avoid having to pay tariffs.

2. To gain access to raw materials. Some U.S. firms have expanded abroad to secure supplies of raw materials. U.S. oil firms—beginning with Standard Oil in the late nineteenth century—have had extensive overseas operations aimed at discovering, recovering, and refining crude oil.

3. To gain access to low-cost labor. In recent decades, some U.S. firms have located factories or other facilities in countries such as China, India, Malaysia, and El Salvador to take advantage of the lower wages paid to workers in those countries.

4. To reduce exchange-rate risk. The exchange rate tells us how many units of foreign currency are received in exchange for a unit of domestic currency. Fluctuations in exchange rates can reduce the profits of a firm that exports goods to other countries. (We discuss this point in more detail in Economics, Chapter 28, Section 28.3 and in Macroeconomics, Chapter 18, Section 18.3.)

5. To respond to industry competition. In some instances, companies expand overseas as a competitive response to an industry rival. The worldwide competition for markets between Pepsi and Coke is an example of this kind of expansion.

All of these reasons, apart from 2., likely played a role in Tesla’s decision to build factories in China and Germany.

In 2021, Tesla was building a factory in Austin, Texas. It was also moving its corporate headquarters from California to Texas. With these actions, the firm may have been responding to lower taxes in Texas and lower housing costs for its workers.

In October 2021, Tesla’s $1 trillion stock market value seemed very high relative to the profits it was currently earning and also because it made Tesla’s value greater than the values of the next nine largest car makers combined. The price of its stock reflected the expectation among investors that Tesla’s profits would increase in future years. Tesla’s decisions about locating its new factories would play a key role in determining whether that expectation turns out to be correct.

Sources: Rebecca Elliott and Dave Sebastian, “Tesla Surpasses $1 Trillion in Market Value as Hertz Orders 100,000 Vehicles,” wsj.com, October 25, 2021; Al Root, “How Tesla Gained $175 Billion in Value From Hertz’s $4 Billion Order. It Makes Perfect Sense,” barrons.com, October 26, 2021; Bojan Pancevski and Jared S. Hopkins, “How Pfizer Partner BioNTech Became a Leader in Coronavirus Vaccine Race,” wsj.com, October 22, 2020; William Boston, “Tesla Awaits Green Light for Production in Germany,” wsj.com, October 12, 2021; Niraj Chokshi, “Tesla Will Move Its Headquarters to Austin, Texas, in Blow to California,” nytimes.com, October 13, 2021; and Alfred D. Chandler, Jr., The Visible Hand: The Managerial Revolution in American Business, Cambridge: Harvard University Press, 1977; and Tesla.com.

In 2021, SPACs were the hottest trend on the stock market and had become the leading way for companies to go public. A public company is one with shares that trade on the stock market. Private firms make up more than 95 percent of all firms in the United States. Most will never become public firms because they will never grow large enough for investors to have sufficient information on the firms’ financial health to be willing to buy the firms’ stocks and bonds.

But some firms, particularly technology firms, grow rapidly enough that they are able to become public firms. Apple, Microsoft, Google, Uber, Facebook, Snap, and other firms have followed this path. When these firms went public, they did so using an initial public offering (IPO). (We briefly discuss IPOs in Economics and Microeconomics, Chapter 8, Section 8.2 and in Macroeconomics, Chapter 6, Section 6.2.) With an IPO, a firm uses one or more investment banks to underwrite the firm’s sales of new stocks or bonds to the public. In underwriting,investment banks typically guarantee a price for stocks or bonds to the issuing firm, sell the stocks or bonds in financial markets or directly to investors at a higher price, and keep the difference, known as the spread.

Beginning in 2020 and continuing through 2021, an increasing number of firms have used a different means of going public—merging with a SPAC. SPAC stands for special-purpose acquisition company and is a firm that holds only cash—it doesn’t sell a good or service—and only has the purpose of merging with another firm that wants to go public. Once a merger takes place, the acquired firm takes the place of the SPAC in the stock market. For instance, a SPAC named Diamond Eagle Acquisition merged with online sports betting site DraftKings in April 2020. Once the merger had been completed, DraftKings took Diamond Eagle’s place on the stock market, trading under the stock symbol DKNG. By 2021, the value of SPAC mergers had risen to being three times as much as the value of IPOs.

Some firms intending to go public prefer SPACs to traditional IPOs because they can bargain directly with the managers of the SPAC in determining the value of the firm. In addition, IPOs are closely regulated by the federal government’s Securities and Exchange Commission (SEC). In particular, the SEC monitors whether an investment bank is accurately stating the financial prospects of a firm whose IPO the bank is underwriting. The claims that SPACs make when attracting investors are less closely monitored. SPAC mergers can also be finalized more quickly than can traditional IPOs.

The experience of WeWork illustrates how some firms that have struggled to go public through an IPO have been able to do so by merging with a SPAC. Adam Neumann and Miguel McLevey founded WeWork in 2010 as a firm that would rent office space in cities, renovate the space, and then sub-lease it to other firms. In 2019, the firm prepared for an IPO that would have given the firm a total value of more than $40 billion. But doubts about the firm’s business model led to an indefinite postponement of the IPO and Neumann was forced out as CEO.

WeWork was reorganized under new CEO Sandeep Mathrani and went public in October 2021 by merging with BowX Acquisition Corporation, a SPAC. Although WeWork’s stock began trading (under stock symbol WE) at a price that put the firm’s value at about $9 billion—far below the value it expected at the time of its postponed IPO two years before—investors seemed optimistic about the firm’s future because its stock price rose sharply during the first two days it traded on the stock market.

Some policymakers are concerned that individual investors may not have sufficient information on firms that go public through a merger with a SPAC. Under one proposal being considered by Congress, financial advisers would only be allowed to recommend investing in SPACs to wealthy investors. The SEC is also considering whether new regulations governing SPACS were needed. Testifying before Congress, SEC Chair Gary Gensler sated: “There’s real questions about who’s benefiting [from firms going public using SPACs] and [about] investor protection.”

It remains to be seen whether SPACs will retain their current position as being the leading way for firms to go public.

Sources: Dave Sebastian, “WeWork Shares Rise on First Day of Trading, Two Years After Failed IPO,” wsj.com, October 21, 2021; Peter Santilli and Amrith Ramkumar, “SPACs Are the Stock Market’s Hottest Trend. Here’s How They Work,” wsj.com, March 29, 2021; Benjamin Bain, “SPAC Marketing Heavily Curtailed in House Democrats’ Draft Bill,” bloomberg.com, October 4, 2021; and Dave Michaels, “SEC Weighs New Investor Protections for SPACs,” wsj.com, May 26, 2021.

Beginning in the 1950s, several companies pioneered in developing modern shipping containers that once arrived at docks can be lifted by cranes and directly attached to trucks or loaded on to trains for overland shipping. As economist Marc Levinson was the first to discuss in detail in his 2004 book, The Box, container shipping, by greatly reducing transportation costs, helped to make the modern global economy possible. (We discuss globalization in Economics, Chapter 9, Section 9.1 and Chapter 21, Section 21.4, and in Macroeconomics, Chapter 7, Section 7.1 and Chapter 11, Section 11.4.)

Lower transportation costs meant that small manufacturing firms and other small businesses that depended on selling in local markets faced much greater competition, including from firms located thousands of miles away. The number of dockworkers declined dramatically as the loading and unloading of cargo ships became automated. Ports such as New York City, San Francisco, and Liverpool that were not well suited for handling containers because they lacked sufficient space for the automated equipment and the warehouses, lost most of their shipping business to other ports, such as Los Angeles, Seattle, and London. Consumers in all countries benefited because lower transportation costs meant they were able to buy cheaper imported goods and had a much greater variety of goods to choose from.

In the decades since the 1950s, shipping firms have continued to exploit economies of scale in container ships. (We discuss the concept of economies of scale in Econimics and Microeconomics, Chapter 11, Section 11.6.) Today, shipping containers have been standardized at either 20 feet or 40 feet long and the largest ships can haul thousands of containers. Levinson explains why economies of scale are important in this industry:

“A vessel to carry 3,000 containers did not require twice as much steel or twice as large an engine as a vessel to carry 1,500. [Because of automation, a] larger ship did not require a larger crew, so crew wages per container were much lower. Fuel consumption did not increase proportionally with the vessel’s size.”

To take advantage of these economies of scale, the ships needed to sail fully loaded. The largest ships can sail fully loaded only on routes where shipping volumes are highest, such as between Asia and the United States or between the United States and Europe. As a result, as Levinson notes, the largest ships are “uneconomic to run on most of the world’s shipping lanes” because on most routes the costs per container are higher for the largest ships for smaller ships. (Note that even these “smaller ships” are still very large in absolute size, being able to haul 1,000 containers.)

Large U.S. retail firms, such as Walmart, Home Depot, and Target rely on imported goods from Asian countries, including China, Japan, and Vietnam. Ordinarily, they are importing goods in sufficient quantities that the goods are shipped on the largest vessels, which today have the capacity to haul 20,000 containers. But during the pandemic, a surge in demand for imported goods combined with disruptions caused by Covid outbreaks in some Asian ports and a shortage of truck drivers and some other workers in the United States, resulted in a backlog of ships waiting to disembark their cargoes at U.S. ports. The ports of Los Angeles and Long Beach in southern California were particularly affected. By October 2021, it was taking an average of 80 days for goods to be shipped across the Pacific, compared with an average of 40 days before the pandemic.

Some large U.S. firms responded to the shipping problems by chartering smaller ships that ordinarily would only make shorter voyages. According to an article in the Wall Street Journal, “the charters provide the big retailers with a way to work around bottlenecks at ports such as Los Angeles, by rerouting cargo to less congested docks such as Portland, Ore., Oakland, Calif., or the East Coast.” Unfortunately, because the smaller ships lacked the economies of scale of the larger ships, the cost the U.S. firms were paying per container were nearly twice as high. (Note that this result is similar to the cost difference between a large and a small automobile factory, which we illustrated in Economics and Microeconomics, Figure 11.6.)

Unfortunately for U.S. consumers, the higher costs U.S. retailers paid for transporting goods across the Pacific Ocean resulted in higher prices on store shelves. Shopping for presents during the 2021 holiday season turned out to be more expensive than in previous years.

Sources: Marc Levinson, The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger, Second edition, Princeton, NJ: Princeton University Press, 2016; Sarah Nassauer and Costas Paris, “Biggest U.S. Retailers Charter Private Cargo Ships to Sail Around Port Delays,” wsj.com, October 10, 2021; and Melissa Repko, “How Bad Are Global Shipping Snafus? Home Depot Contracted Its Own Container Ship as a Safeguard,” cnbc.com, June 13, 2021.

In this chapter, we have studied several types of elasticities, starting with the price elasticity of demand. Elasticity is a general concept that economists use to measure the effect of a change in one variable on another variable. An example of a more general use of elasticity, beyond the uses we discussed in this chapter, appears in a new academic paper written by Anne Sofie Tegner Anker of the University of Copenhagen, Jennifer L. Doleac of Texas A&M University, and Rasmus LandersØ of Aarshus University.

The authors are interested in studying the effects of crime deterrence. They note that rational offenders will be deterred by government policies that increase the probability that an offender will be arrested. Even offenders who don’t respond rationally to an increase in the probability of being arrested will still commit fewer crimes because they are more likely to be arrested. Governments have different policies available to reduce crime. Given that government resources are scarce, efficient allocation of resources requires policymakers to choose policies that provide the most deterrence per dollar of cost.

The authors note “we currently know very little about precisely how much deterrence we achieve for any given increase in the likelihood that an offender is apprehended.” They attempt to increase knowledge on this point by analyzing the effects of a policy change in Denmark in 2005 that made it much more likely that an offender would have his or her DNA entered into a DNA database: “The goal of DNA registration is to deter offenders and increase the likelihood of detection of future crimes by enabling matches of known offenders with DNA from crime scene evidence.”

The authors find that the expansion of Denmark’s DNA database had a substantial effect on recidivism—an offender committing additional crimes—and on the probability that an offender who did commit additional crimes would be caught. They estimate that “a 1 percent higher detection probability reduces crime by more than 2 percent.” In other words, the elasticity of crime with respect to the detection probability is −2.

Just as the price elasticity of demand gives a business manager a useful way to summarize the responsiveness of the quantity demanded of the firm’s product to a change in its price, the elasticity the authors estimated gives a policymaker a useful way to summarize the responsiveness of crime to a policy that increases the probability of catching offenders.

Source: Anne Sofie Tegner Anker, Jennifer L. Doleac, and Rasmus LandersØ, “The Effects of DNA Databases on the Deterrence and Detection of Offenders,” American Economic Journal: Applied Economics, Vol. 13, No. 4, October 2021, pp. 194-225.

David Card of the University of California, Berkeley; Joshua Angrist of the Massachusetts Institute of Technology; and Guido Imbens of Stanford University shared the 2021 Nobel Prize in Economics (formally, the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel). Card received half of the prize of 10 million Swedish kronor (about 1.14 million U.S. dollars) “for his empirical contributions to labor economics,” and Angrist and Imbens shared the other half “for their methodological contributions to the analysis of causal relationships.” (In the work for which they received the prize, all three had collaborated with the late Alan Krueger of Princeton University. Card was quoted in the Wall Street Journal as stating that: “I’m sure that if Alan was still with us that he would be sharing this prize with me.”)

The work of the three economists is related in that all have used natural experiments to address questions of economic causality. With a natural experiment, economists identify some variable of interest—say, an increase in the minimum wage—that has changed for one group of people—say, fast-food workers in one state—while remaining unchanged for another similar group of people—say, fast-food workers in a neighboring state. Researchers can draw an inference about the effects of the change by looking at the difference between the outcomes for the two groups. In this example, the difference between changes in employment at fast-food restaurants in the two states can be used to measure the effect of an increase in the minimum wage.

Using natural experiments is an alternative to the traditional approach that had dominated empirical economics from the 1940s when the increased availability of modern digital computers made it possible to apply econometric techniques to real-world data. With the traditional approach to empirical work, economists would estimate structural models to answer questions about causality. So, for instance, a labor economist might estimate a model of the demand and supply of labor to predict the effect of an increase in the minimum wage on employment.

Over the years, many economists became dissatisfied with using structural models to address questions of economic causality. They concluded that the information requirements to reliably estimate structural models were too great. For instance, structural models require assumptions about the functional form of relationships, such as the demand for labor, that are not inferable directly from economic theory. Theory also did not always identify all variables that should be included in the model. Gathering data on the relevant variables was sometimes difficult. As a result, answers to empirical questions, such as the employment effects of the minimum wage, differed substantially across studies. In such cases, policymakers began to see empirical economics as an unreliable guide to economic policy.

In a famous study of the effect of the minimum wage on employment published in 1994 in the American Economic Review, Card and Krueger pioneered the use of natural experiments. In that study, Card and Krueger analyzed the effect of the minimum wage on employment in fast-food restaurants by comparing what happened to employment in New Jersey when it raised the state minimum wage from $4.25 to $5.05 per hour with employment in eastern Pennsylvania where the minimum wage remained unchanged. They found that, contrary to the usual analysis that increases in the minimum wage lead to decreases in the employment of unskilled workers, employment of fast-food workers in New Jersey actually increased relative to employment of fast-food workers in Pennsylvania.

The following graphic from Nobel Prize website summarizes the study. (Note that not all economists have accepted the results of Card and Krueger’s study. We briefly summarize the debate over the effects of the minimum wage in Chapter 4, Section 4.3 of our textbook.)

Drawing inferences from natural experiments is not as straightforward as it might seem from our brief description. Angrist and Imbens helped develop the techniques that many economists rely on when analyzing data from natural experiments.

Taken together, the work of these three economists represent a revolution in empirical economics. They have provided economists with an approach and with analytical techniques that have been applied to a wide range of empirical questions.

For the annoucement from the Nobel website click HERE.

For the article in the Wall Street Journal on the prize click HERE (note that a subscription may be required).

For the orignal Card and Krueger paper on the minimum wage click HERE.

Supports: Econ Chapter 12, Section 12.4, “Deciding Whether to Produce or Shut Down in the Short Run,” and Section 12.5, “‘If Everyone Can Do It, You Can’t Make Money at It’: The Entry and Exit of Firms in the Long Run”; and Essentials: Chapter 9, Section 9.4 and Section 9.5.

Photo from the Associated Press.

Solved Problem: Why Is Starbucks Closing Stores in New York City?

In May 2021, many businesses in the United States began fully reopening as local governments eased restrictions on capacity imposed to contain the spread of Covid-19. An article on crainsnewyork.com discussed the decisions Starbucks was making with respect to its stores in New York City. Starbucks intended to keep some stores open, some stores would be permanently closed, and “about 20 others that are currently in business will shutter when their leases end in the next year.” Analyze the relationship between cost and revenue for each of these three categories of Starbucks stores: 1) the stores that will remain permanently open; 2) the stores that will not reopen; and 3) the stores that will remain open only until their leases expire. In particularly, be sure to explain why Starbucks didn’t close the stores in category 3) immediately rather than waiting until the their leases expire.

Source: Cara Eisenpress, “Starbucks Closing Some City Locations as It Moves to a Smaller, Pickup Model,” crainsnewyork.com, May 19, 2021.

Solving the Problem

Step 1: Review the chapter material. This problem is about the break-even price for a firm in the short run and in the long run, so you may want to review Chapter 12, Section 12.4, “Deciding Whether to Produce or to Shut Down in the Short Run,” and Section 12.5, “‘If Everyone Can Do It, You Can’t Make Money at It’: The Entry and Exit of Firms in the Long Run.”

Step 2: Explain why stores in category 1) will remain permanently open. We know that firms will continue to operate a store if the revenue from the store is greater than or equal to all of the store’s costs—both its fixed costs and its variable costs. So, Starbucks must expect this relationship between revenue and cost to hold for the stores that it will keep permanently open.

Step 3: Explain why Starbucks will not reopen stores in category 2). Firms will close a store in the short run if the loss from operating the store is greater than the store’s fixed costs. Put another way, the firm won’t be willing to lose more than the store’s fixed costs. We can conclude that Starbucks believes that if it reopens stores in category 2) its loss from operating those stores will be greater than the stores’ fixed costs.

Step 4: Explain why Starbucks will operate some stores only until their leases expire and then will shut them down. If a firm’s revenue from operating a store is greater than the store’s variable costs, the firm will operate the store even though it is incurring an economic loss. If it closed the store, it would still have to pay the fixed costs of the store, the most important of which in this case is the rent it has to pay the owner of the building the store is in. By operating the store, Starbucks will incur a smaller loss than by immediately closing the store. But recall that there are no fixed costs in the long run. The stores’ leases will eventually expire, eliminating that fixed cost. So, in the long run, a firm will close a store that is incurring a loss. Because Starbucks doesn’t believe that in the long run it can cover all the costs of operating stores in category 3, it intends to operate them until their leases expire and then shut them down.

Eva is an Associate Teaching Professor at the University of Notre Dame, where she is also a fellow of the Kellogg Institute for International Studies, the Liu Institute for Asia and Asian Studies, and the Pulte Institute for Global Development. She received her PhD from the University of Illinois, Chicago in 2014.

Last June, we interviewed Eva on our podcast. That podcast can be found HERE.

Can a Behavioral Nudge with Small Commitment Lead to Better Exam Scores?

So Covid brought challenges…. we can’t really even count them. In the world of education, it meant switching to online delivery and while that may be hard on us professors, it also requires a lot more from students. Learning from home requires more discipline, there is a degree of freedom (statistics pun intended). There is also a lack of accountability that typically comes with attending an in-person class where the professor can call you out for not being prepared. This is what non-traditional students who have a job, a family, go through on a regular basis even without Covid. The often opt for online classes in the first place. It can also be a tougher adjustment for students who come from traditionally underrepresented groups in higher education, as they may not grow up watching their parents make lists, prioritize, and manage time that would promote college success. Is there something that could help alter students’ behavior and overcome this inequality?

In all of our introductory economic models, we assume that agents are rational. If that assumption is violated, we cannot really predict how they will respond to incentives and our models would lose their predictive power. The 2017 Nobel Prize in Economics was awarded to Richard Thaler for his contributions to behavioral economics. The art and science of “irrationality”. Well, about time as we seem to violate rationality a lot! We know we should study, we know we should not procrastinate, yes we know but… These choices can have serious long-term consequences, so it is important to study our behaviors and why we make decisions that perhaps do not appear rational. And it is important to study how we could alter certain behaviors. Research has shown that simply nudging students with a text message doesn’t really lead to improvements in academic performance. A 2019 NBER working paper summarized it pretty well: “The Remarkable Unresponsiveness of College Students to Nudging and What We Can Learn from It.” [The paper can be found HERE.]

In our paper “Microcommitments: The Effect of Small Commitments on Academic Performance,” we set out to test whether a text message nudge accompanied by a small commitment can “push” students in the right direction. In economics, the gold standard of answering questions like this is a randomized controlled trial. If assignment is not random and students are selected into treatment and control groups, then we would not be able to identify the role of the intervention, as these groups may be responding differently in the first place. For example, imagine we tested the nudge with commitment on a group of women and men served as the “placebo” control group. If we find higher exam scores for women, then it may be because of the nudge with commitment but it is also entirely possible that women could have scored higher regardless, this is referred to as a selection bias. We overcome this by randomly assigning almost 1,000 students from the University of Notre Dame, Florida Atlantic University, and University of Illinois into two groups, which after close examination of observable characteristics look very similar. This is called a balance test. After randomization, the two groups have a similar proportion of women, similar average SAT, GPA, age, family structure, their procrastination tendencies, self-efficacy, study habits, etc. Some of the students are enrolled in regular in-person classes, and some are enrolled in a hybrid/online classes.

After the first exam of the semester, which will serve as a baseline comparison, the experiment begins! Both groups receive text messages in the morning with content related to material covered in class. Students know they are not required to submit their answers and it is not mandatory, these messages are just extra practice on how to think as an economist. The control group received the content as a simple text message. The treatment group’s text message also had “I commit” to click. Then at 4pm, they also got a follow up text with “I did it” click. This is the commitment device we are testing and it is the only difference between the treatment and control groups, everything else is identical. The research question is: Does a small commitment (really to yourself, as it is not required) compel you to complete the task and does this engagement then improve your future exam score? The regression estimation allows us to hold everything else constant, so we are adhering to our ceteris paribus condition.

It turns out that the small commitment does make a difference! In fact, the positive results on the exam which followed the experiment is driven by students in hybrid and online classes who scored 3.5 percentage points higher than students in the control group which received the same message content but did not receive the commitment! We find no effect on the academic performance among students in regular in-person classes. It appears that this simple intervention partially substitutes for the lack of instructor contact for students in hybrid and online classes. We also find that students who tend to procrastinate and those with lower GPA benefit from the commitment device more, which then acts as an equalizing force in terms of academic performance and could have positive implications for social mobility and economic equity. Who would have thought that making a small promise to yourself could actually make a difference!!!

References: Felkey, Amanda J, Eva Dziadula, Eric P Chiang, and Jose Vazquez. 2021. “Microcommitments: The Effect of Small Commitments on Academic Performance.” AEA Papers and Proceedings 111: 1–6. [The paper can be found HERE.]

Oreopoulos, Philip, and Uros Petronijevic. 2019. “The Remarkable Unresponsiveness of College Students to Nudging and What We Can Learn from It.” [The paper can be found HERE.]

Supports: Hubbard/O’Brien, Chapter 8, Firms, the Stock Market, and Corporate Governance; Macroeconomics Chapter 6; Essentials of Economics Chapter 6; Money, Banking, and the Financial System, Chapter 6.

We’ve seen that a firm’s stock price should represent the best estimates of investors as to how profitable the firm will be in the future. How, then, can we explain the following graph of the price of shares of GameStop, the retail chain that primarily sells video game cartridges and video game systems? The graph shows the price of the stock from December 1, 2020 through February 9, 2021. If the main reason the price of a stock changes is that investors have become more or less optimistic about the profitability of the firm, is it plausible that opinions on GameStop’s profitability changed so much in such a short period of time?.

Sometimes investors do abruptly change their minds about the profitability of a firm but typically this happens when the firm’s profitability is heavily dependent on the success of a single product. For instance, the price of the stock a biotech firm might soar as investors believe that a new drug therapy the firm is developing will succeed and then the price of the stock might crash when the drug is unable to gain regulatory approval. But it wasn’t news about its business that was driving the price of GameStop’s stock from $15 per share during December 2020 to a high of $347 per share on January 27, 2021 and then down to $49 per share on February 9.

To understand these prices swings, first we need to take into account that not all people buying stock do so because they are making long-term investments to accumulate funds to purchase a house, pay for their children’s educations, or for their retirement. Some people who buy stock are speculators who hope to profit by buying and selling stock during a short period—perhaps as short as a few minutes or less. The availability of online stock trading apps, such as Robinhood, that don’t charge commissions for buying and selling stock, and online stock discussion groups on sites like Reddit, have made it easier for some individual investors to become day traders, frequently buying and selling stocks in the hopes of making a short-term profit.

Many day traders engage in momentum investing, which means they buy stocks that have increasing prices and sell stocks that have falling prices, ignoring other aspects of the firm’s situation, including the firm’s likely future profitability. Momentum investing is an example of what economists call noise trading, or buying and selling stocks on the basis of factors not directly related to a firm’s profitability. Noise trading can result in a bubble in a firm’s stock, which means that the price rises above the fundamental value of the stock as indicated by the firm’s profitability. Once a bubble begins, a speculator may buy a stock to resell it quickly for a profit, even if the speculator knows that the price is greater than the stock’s fundamental value. Some economists explain a bubble in the price of a stock by the greater fool theory: An investor is not a fool to buy an overvalued stock as long as there’s a greater fool willing to buy it later for a still higher price.

Although the factors mentioned played a role in explaining the volatility in GameStop’s stock price, there was another important factor that involved hedge funds and short selling. Hedge funds are similar to mutual funds in that they use money from savers to make investments. But unlike mutual funds, by federal regulation only wealthy individuals or institutional investors such as pension funds or university endowment funds are allowed to invest in hedge funds. Hedge funds frequently engage in short selling, which means that when they identify a firm whose stock they consider to be overvalued, they borrow shares of the firm’s stock from a broker or dealer and sell them in the stock market, planning to make a profit by buying the shares back after their prices have fallen.

In early 2021, several large hedge funds were shorting GameStop’s stock believing that the market for video game cassettes would continue to decline as more gamers switched to downloading games. Some people in online forums—notably the WallStreetBets forum on Reddit—dedicated to discussing investing strategies argued that if enough day traders bought GameStop’s stock they could make money through a short squeeze. A short squeeze happens when a heavily shorted stock increases in price. The speculators who shorted the stock may then have to buy back the stock to avoid large losses or having to pay very high fees to dealers who had loaned them the shares they were shorting. As the short sellers buy stock, the price of the stock is bid up further, earning a profit for day traders who had bought the stock in anticipation of the short squeeze. One MIT graduate student made a profit of more than $200,000 on a $500 investment in GameStop stock. Some hedge funds that had been shorting GameStop lost billions of dollars.

Some of the day traders involved saw this episode as one of David defeating Goliath because the people executing the short squeeze were primarily young with moderate incomes whereas the people running the hedge funds taking substantial losses in the short squeeze were older with high incomes. The reality was more complex because as the price of GameStop stock declined from $347 on to $54 on February 4, some day traders who bought the stock after its price had already substantially risen lost money. And all the winners from the short squeeze weren’t day traders; some were hedge funds. For instance, by early February, the hedge fund Senvest Management had earned $700 million from its trading in GameStop’s stock.

Economists had differing opinions about whether the GameStop episode had a wider significance for understanding how the stock market works or for how it was likely to work in the future. Some economists and investment professionals argued that what happened with GameStop’s stock price was not very different from previous episodes in which speculators buying and selling a stock will for a time cause increased volatility in the stock’s price. In the long run, they believe that stock prices return to their fundamental values. Other economists and investors thought that the increased number of day traders combined with the availability of no-commission stock buying and selling meant that stock prices might be entering a new period of increased volatility. They noted that similar, if less spectacular, price swings had happened at the same time in other stocks such as AMC, the movie theater chain, and Express, the clothing store chain. An article on bloomberg.com quoted one analyst as saying, “We’ve made gambling on the stock market cheaper than gambling on sports and gambling in Vegas.”

Federal regulators, including Treasury Secretary Janet Yellen, were evaluating what had happened and whether they needed to revise existing government regulations of financial markets.

Sources: Misyrlena Egkolfopoulou and Sarah Ponczek, “Robinhood Crisis Reveals Hidden Costs in Zero-Fee Trading Model,” bloomberg.com, February 3, 2021; Gunjan Banerji, Juliet Chung, and Caitlin McCabe, “GameStop Mania Reveals Power Shift on Wall Street—and the Pros Are Reeling,”Wall Street Journal, January 27, 2021; Gregory Zuckerman, “For One GameStop Trader, the Wild Ride Was Almost as Good as the Enormous Payoff,” Wall Street Journal, February 3, 2021; Juliet Chung, “Wall Street Hedge Funds Stung by Market Turmoil,” Wall Street Journal, January 28, 2021; and Juliet Chung, “This Hedge Fund Made $700 Million on GameStop,” Wall Street Journal, February 3, 2021.

Questions

During the same week that the price of GameStop’s stock was soaring to a record high, an article in the Wall Street Journal noted the following: “Analysts expect GameStop to post its fourth consecutive annual decline in revenue in its latest fiscal year amid declines in its core operations [of selling video game cartridges and video game consoles in retail stores].” Don’t stock prices reflect the expected profitability of the firms that issue the stock? If so, why in January 2021 was the price of GameStop’s stock greatly increasing when it seemed unlikely that the firm would become more profitable in the future?

Source: Sarah E. Needleman, “GameStop and AMC’s Stocks Are on a Tear, but Their Businesses Aren’t,” Wall Street Journal, January 31, 2021

2. In early 2021, as the stock price of GameStop was soaring, a columnist in the New York Times advised that: “A better option [than buying stock in GameStop] would be salting away money in dull, well-diversified stock and bond portfolios, these days preferably in low-cost index funds.”

a. What does the columnist mean by “salting money away”?

b. are index funds and why might they be considered dull when compared to investing in an individual stock like GameStop?

c. Why would the columnist consider investing in an index mutual fund to be a better option than investing money in an individual stock like GameStop?

Source: Jeff Sommer, “How to Keep Your Cool in the GameStop Market,” New York Times, January 29, 2021.

Instructors can access the answers to these questions by emailing Pearson at christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.