Neel Kashkari, president of the Federal Reserve Bank of Minneapolis. Photo from the Wall Street Journal.Pat Toomey, U.S. Senator from Pennsylvania. Photo from http://www.toomey.senate.gov.

As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), the Federal Reserve is unusual among federal government agencies in being able to operate largely independently of Congress and the president. Congress passed the Federal Reserve Act, which established the Federal Reserve System, in 1913, and has amended it several times in the years since. (Note that, as we discuss in the Apply the Concept, “End the Fed?” in this chapter, the U.S. Constitution does not explicitly authorized the federal government to establish a central bank.) Section 2A of the act gives the Federal Reserve System the following charge:

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

Elsewhere in the act, the Fed was given other specified responsibilities, such as supervising commercial banks that are members of the Federal Reserve System and serving on the Financial Stability Oversight Council (FSOC), which is charged with assessing risks to the financial system.

Because Congress can change the structure and operations of the Fed at any time and because Congress has given the Fed only certain specific responsibilities, traditionally the Fed has avoided becoming involved in policy debates that are not directly concerned with its responsibilities. Over the years, most members of the Board of Governors have believed that if the Fed were to become involved in issues beyond monetary policy and the working of the financial system, Congress might decide to revise the Federal Reserve Act to reduce, or even eliminate, Fed independence.

In the spring of 2022, though, there were two instances where some members of Congress argued that the Fed had become involved in policy issues that went beyond the Fed’s responsibilities under the Federal Reserve Act. The first instance involved President Joe Biden’s nomination in January 2022 of Sarah Bloom Raskin to serve on the Fed’s Board of Governors. In 2010, Raskin was nominated to the Board of Governors by President Barack Obama and confirmed by the Senate in a voice vote without significant opposition. (In 2014, she resigned from the Board to accept a position in the Treasury Department.)

Her nomination by President Biden encountered significant opposition, however, largely because in July 2020 she had suggested that when the Fed expanded its lending programs during the Covid-19 pandemic it should have excluded firms in the oil, natural gas, and coal industries: “The Fed is ignoring clear warning signs about the economic repercussions of the impending climate crisis by taking action that will lead to increases in greenhouse gas emissions at a time when even in the short term, fossil fuels are a terrible investment.” Although her supporters argued that in formulating policy the Fed should take into account the threats to financial stability caused by climate change, when it became clear that a majority of the Senate disagreed, Raskin withdrew her nomination.

In April 2022, some members of Congress, including Senator Pat Toomey of Pennsylvania, questioned whether it was appropriate for President Neel Kashkari of the Federal Reserve Bank of Minneapolis to formally support the campaign to amend the Minnesota state constitution to include a provision stating that, “All children have a fundamental right to a quality public education …. It is a paramount duty of the state to ensure quality public schools that fulfill this fundamental right.”

The Bank defended its support for the amendment in a statement on its website: “The Federal Reserve Bank of Minneapolis’ support of the Page amendment is closely linked to the mission of the Federal Reserve. Congress assigned the Federal Reserve the dual goals of achieving (1) stable prices and (2) maximum employment, and one of the greatest determinants of success in the job market is education.”

Senator Toomey strongly disagreed, arguing in a letter of Bank President Kashkari that: “This amendment is highly political, as it wades into an ongoing debate about whether government-run school systems are preferable to parental choice in education.” Toomey asserted that: “These political lobbying efforts by you and other Minneapolis Fed officials … are well beyond the Federal Reserve’s mandate, violate Federal Reserve Bank policies, constitute a misuse of Minneapolis Fed resources, and ultimately undermine the Federal Reserve’s independence and credibility.”

It remains to be seen whether Congress will ultimately accept the arguments of Federal Reserve policymakers such as Kashkari and Raskin that the Fed needs to interpret its mandate from Congress more broadly, or whether Congress will decide to amend the Federal Reserve Act to more explicitly limit the boundaries of Fed action—or to reduce Fed independence in some other ways.

Sources: Sarah Bloom Raskin, “Why Is the Fed Spending So Much Money on a Dying Industry?” New York Times, May 28, 2020; Andrew Ackerman and Ken Thomas, “Sarah Bloom Raskin Withdraws as Biden’s Pick for Top Fed Banking Regulator,” Wall Street Journal, March 15, 2022; Michael S. Derby, “GOP Senator Criticizes Minneapolis Fed Over Education Issue,” Wall Street Journal, April 12, 2022; Federal Reserve Bank of Minneapolis, “Page Amendment: Every Child Deserves a Quality Public Education,” minneapolisfed.org; and Pat Toomey, “Letter to Neel Kashkari,” banking.senate. gov, April 11, 2022.

Authors Glenn Hubbard and Tony O’Brien reconsider the role of inflation in today’s economy. They discuss the Fed’s possible responses by considering responses to similar inflation threats in previous generations – notably the Fed’s response led by Paul Volcker that directly led to the early 1980’s recession. The markets are reflecting stark differences in our collective expectations about what will happen next. Listen to find out more about the Fed’s likely next steps.

It now seems clear that the new monetary policy strategy the Fed announced in August 2020 was a decisive break with the past in one respect: With the new strategy, the Fed abandoned the approach dating to the 1980s of preempting inflation. That is, the Fed would no longer begin raising its target for the federal funds rate when data on unemployment and real GDP growth indicated that inflation was likely to rise. Instead, the Fed would wait until inflation had already risen above its target inflation rate.

Since 2012, the Fed has had an explicit inflation target of 2 percent. As we discussed in a previous blog post, with the new monetary policy the Fed announced in August 2020, the Fed modified how it interpreted its inflation target: “[T]he Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

The Fed’s new approach is sometimes referred to as average inflation targeting (AIT) because the Fed attempts to achieve its 2 percent target on average over a period of time. But as former Fed Vice Chair Richard Clarida discussed in a speech in November 2020, the Fed’s monetary policy strategy might be better called a flexible average inflation target (FAIT) approach rather than a strictly AIT approach. Clarida noted that the framework was asymmetric, meaning that inflation rates higher than 2 percent need not be offset with inflation rates lower than 2 percent: “The new framework is asymmetric. …[T]he goal of monetary policy … is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent.” And: “Our framework aims … for inflation to average 2 percent over time, but it does not make a … commitment to achieve … inflation outcomes that average 2 percent under any and all circumstances ….”

Inflation began to increase rapidly in mid-2021. The following figure shows three measure of inflation, each calculated as the percentage change in the series from the same month in the previous year: the consumer price index (CPI), the personal consumption expenditure (PCE) price index, and the core PCE—which excludes the prices of food and energy. Inflation as measured by the CPI is sometimes called headline inflation because it’s the measure of inflation that most often appears in media stories about the economy. The PCE is a broader measure of the price level in that it includes the prices of more consumer goods and services than does the CPI. The Fed’s target for the inflation rate is stated in terms of the PCE. Because prices of food and inflation fluctuate more than do the prices of other goods and services, members of the Fed’s Federal Open Market Committee (FOMC) generally consider changes in the core PCE to be the best measure of the underlying rate of inflation.

The figure shows that for most of the period from 2002 through early 2021, inflation as measured by the PCE was below the Fed’s 2 percent target. Since that time, inflation has been running well above the Fed’s target. In February 2022, PCE inflation was 6.4 percent. (Core PCE inflation was 5.4 percent and CPI inflation was 7.9 percent.) At its March 2022 meeting the FOMC begin raising its target for the federal funds rate—well after the increase in inflation had begun. The Fed increased its target for the federal funds rate by 0.25 percent, which raised the target from 0 to 0.25 percent to 0.25 to 0.50 percent.

Should the Fed have taken action to reduce inflation earlier? To answer that question, it’s first worth briefly reviewing Fed policy during the Great Inflation of 1968 to 1982. In the late 1960s, total federal spending grew rapidly as a result of the Great Society social programs and the war in Vietnam. At the same time, the Fed increased the rate of growth of the money supply. The result was an end to the price stability of the 1952-1967 period during which the annual inflation rate had averaged only 1.6 percent.

The 1973 and 1979 oil price shocks also contributed to accelerating inflation. Between January 1974 and June 1982, the annual inflation rate averaged 9.3 percent. This was the first episode of sustained inflation outside of wartime in U.S. history—until now. Although the oil price shocks and expansionary fiscal policy contributed to the Great Inflation, most economists, inside and outside of the Fed, eventually concluded that Fed policy failures were primarily responsible for inflation becoming so severe.

The key errors are usually attributed to Arthur Burns, who was Fed Chair from January 1970 to March 1978. Burns, who was 66 at the time of his appointment, had made his reputation for his work on business cycles, mostly conducted prior to World War II at the National Bureau of Economic Research. Burns was skeptical that monetary policy could have much effect on inflation. He was convinced that inflation was mainly the result of structural factors such as the power of unions to push up wages or the pricing power of large firms in concentrated industries.

Accordingly, Burns was reluctant to raise interest rates, believing that doing so hurt the housing industry without reducing inflation. Burns testified to Congress that inflation “poses a problem that traditional monetary and fiscal remedies cannot solve as quickly as the national interest demands.” Instead of fighting inflation with monetary policy he recommended “effective controls over many, but by no means all, wage bargains and prices.” (A collection Burns’s speeches can be found here.)

Few economists shared Burns’s enthusiasm for wage and price controls, believing that controls can’t end inflation, they can only temporarily reduce it while causing distortions in the economy. (A recent overview of the economics of price controls can be found here.) In analyzing this period, economists inside and outside the Fed concluded that to bring the inflation rate down, Burns should have increased the Fed’s target for the federal funds rate until it was higher than the inflation rate. In other words, the real interest rate, which equals the nominal—or stated—interest rate minus the inflation rate, needed to be positive. When the real interest rate is negative, a business may, for example, pay 6% on a bond when the inflation rate is 10%, so they’re borrowing funds at a real rate of −4%. In that situation, we would expect borrowing to increase, which can lead to a boom in spending. The higher spending worsens inflation.

Because Burns and the FOMC responded only slowly to rising inflation, workers, firms, and investors gradually increased their expectations of inflation. Once higher expectation inflation became embedded, or entrenched, in the U.S. economy it was difficult to reduce the actual inflation rate without increasing the target for the federal funds rate enough to cause a significant slowdown in the growth of real GDP and a rise in the unemployment rate. As we discuss in Macroeconomics, Chapter 17, Sections 17.2 and 17.3 (Economics, Chapter 27, Sections 27.2 and 27.3), the process of the expected inflation rate rising over time to equal the actual inflation rate was first described in research conducted separately by Nobel Laureates Milton Friedman and Edmund Phelps during the 1960s.

An implication of Friedman and Phelps’s work is that because a change in monetary policy takes more than a year to have its full effect on the economy, if the Fed waits until inflation has already increased, it will be too late to keep the higher inflation rate from becoming embedded in interest rates and long-term labor and raw material contracts.

Paul Volcker, appointed Fed chair by Jimmy Carter in 1979, showed that, contrary to Burns’s contention, monetary policy could, in fact, deal with inflation. By the time Volcker became chair, inflation was above 11%. By raising the target for the federal funds rate to 22%—it was 7% when Burns left office—Volcker brought the inflation rate down to below 4%, but only at the cost of a severe recession during 1981–1982, during which the unemployment rate rose above 10 percent for the first time since the Great Depression of the 1930s. Note that whereas Burns had largely failed to increase the target for the federal funds as rapidly as inflation had increased—resulting in a negative real federal funds rate—Volcker had raised the target for the federal funds rate above the inflation rate—resulting in a positive real federal funds rate.

Because the 1981–1982 recession was so severe, the inflation rate declined from above 11 percent to below 4 percent. In Chapter 17, Figure 17.10 (reproduced below), we plot the course of the inflation and unemployment rates from 1979 to 1989.

Caption: Under Chair Paul Volcker, the Fed began fighting inflation in 1979 by reducing the growth of the money supply, thereby raising interest rates. By 1982, the unemployment rate had risen to 10 percent, and the inflation rate had fallen to 6 percent. As workers and firms lowered their expectations of future inflation, the short-run Phillips curve shifted down. The adjustment in expectations allowed the Fed to switch to an expansionary monetary policy, which by 1987 brought unemployment back to the natural rate of unemployment, with an inflation rate of about 4 percent. The orange line shows the actual combinations of unemployment and inflation for each year from 1979 to 1989.

The Fed chairs who followed Volcker accepted the lesson of the 1970s that it was important to head off potential increases in inflation before the increases became embedded in the economy. For instance, in 2015, then Fed Chair Janet Yellen in explaining why the FOMC was likely to raise to soon its target for the federal funds rate noted that: “A substantial body of theory, informed by considerable historical evidence, suggests that inflation will eventually begin to rise as resource utilization continues to tighten. It is largely for this reason that a significant pickup in incoming readings on core inflation will not be a precondition for me to judge that an initial increase in the federal funds rate would be warranted.”

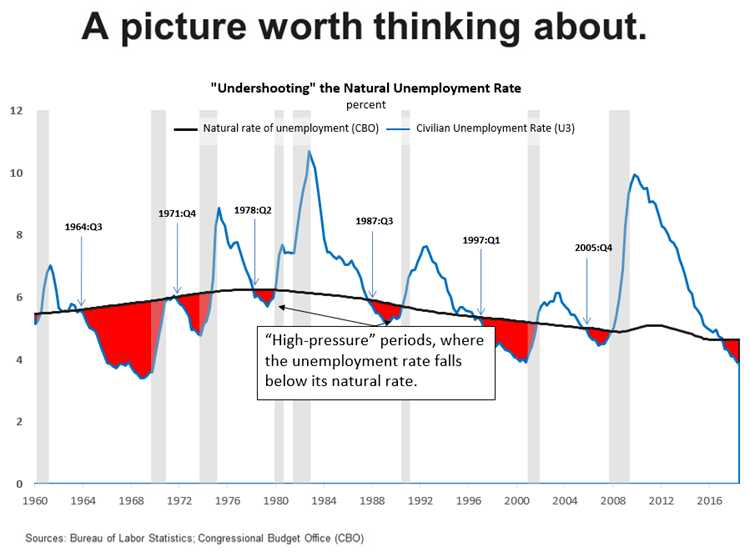

Between 2015 and 2018, the FOMC increased its target for the federal funds rate nine times, raising the target from a range of 0 to 0.25 percent to a range of 2.25 to 2.50 percent. In 2018, Raphael Bostic, president of the Federal Reserve Bank of Atlanta justified these rate increases by noting that “… we shouldn’t forget that [the Fed’s] credibility [with respect to keeping inflation low] was hard won. Inflation expectations are reasonably stable for now, but we know little about how far the scales can tip before it is no longer so.”

He used the following figure to illustrate his point.

Bostic interpreted the figure as follows:

“[The red areas in the figure are] periods of time when the actual unemployment rate fell below what the U.S. Congressional Budget Office now estimates as the so-called natural rate of unemployment. I refer to these episodes as “high-pressure” periods. Here is the punchline. Dating back to 1960, every high-pressure period ended in a recession. And all but one recession was preceded by a high-pressure period….

I think a risk management approach requires that we at least consider the possibility that unemployment rates that are lower than normal for an extended period are symptoms of an overheated economy. One potential consequence of overheating is that inflationary pressures inevitably build up, leading the central bank to take a much more “muscular” stance of policy at the end of these high-pressure periods to combat rising nominal pressures. Economic weakness follows [resulting typically, as indicated in the figure by the gray band, in a recession].”

By July 2019, a majority of the members of the FOMC, including Chair Powell, had come to believe that with no sign of inflation accelerating, they could safely cut the federal funds rate. But they had not yet explicitly abandoned the view that the FOMC should act to preempt increases in inflation. The formal change came in August 2020 when, as discussed earlier, the FOMC announced the new FAIT.

At the time the FOMC adopted its new monetary policy strategy, most members expected that any increase in inflation owing to problems caused by the Covid-19 pandemic—particularly the disruptions in supply chains—would be transitory. Because inflation has proven to be more persistent than Fed policymakers and many economists expected, two aspects of the FAIT approach to monetary policy have been widely discussed: First, the FOMC did not explicitly state by how much inflation can exceed the 2 percent target or for how long it needs to stay there before the Fed will react. The failure to elaborate on this aspect of the policy has made it more difficult for workers, firms, and investors to gauge the Fed’s likely reaction to the acceleration in inflation that began in the spring of 2021. Second, the FOMC’s decision to abandon the decades-long policy of preempting inflation may have made it more difficult to bring inflation down to the 2 percent target without causing a recession.

Federal Reserve Governor Lael Brainard recently remarked that “it is of paramount importance to get inflation down” and some Fed policymakers believe that the FOMC will have to begin increasing its target for the federal funds rate more aggressively. (The speech in which Governor Brainard discusses her current thinking on monetary policy can be found here.) For instance James Bullard, president of the Federal Reserve Bank of St. Louis, has argued in favor of raising the target to above 3 percent this year. With the Fed’s preferred measure of inflation running above 5 percent, it would take substantial increases int the target to achieve a positive real federal funds rate.

It is an open question whether Jerome Powell finds himself in a position similar to that of Paul Volcker in 1979: Rapid increases in interest rates may be necessary to keep inflation from accelerating, but doing so risks causing a recession. In a recent speech (found here), Powell pledged that: “We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

But Powell argued that the FOMC could achieve “a soft landing, with inflation coming down and unemployment holding steady” even if it is forced to rapidly increase its target for the federal funds rate:

“Some have argued that history stacks the odds against achieving a soft landing, and point to the 1994 episode as the only successful soft landing in the postwar period. I believe that the historical record provides some grounds for optimism: Soft, or at least softish, landings have been relatively common in U.S. monetary history. In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession.”

Some economists have been skeptical that a soft landing is likely. Harvard economist and former Treasury Secretary Lawrence Summers has been particularly critical of Fed policy, as in this Twitter thread. Summers concludes that: “I am apprehensive that we will be disappointed in the years ahead by unemployment levels, inflation levels, or both.” (Summers and Harvard economist Alex Domash provide an extended discussion in a National Bureau of Economic Research Working Paper found here.)

Clearly, we are in a period of great macroeconomic uncertainty.

Ernie Banks of the Chicago Cubs poses for a portrait circa 1963. (Photo by Louis Requena/MLB Photos)

With the owners of the Major Labor Baseball teams and the Major League Players Association having finally settled on a new collective bargaining agreement, the baseball season will soon begin. Ernie Banks, the late Hall of Fame shortstop for the Chicago Cubs, was known for his upbeat personality. However bad the weather might be at Chicago’s Wrigley Field, Banks would run on the field and say, “What a great day for baseball! Let’s play two.”

In honor of Ernie Banks, today let’s do two Solved Problems in macro. They both involve errors that students in principles courses often make. So, in that sense they would also work as Don’t Let This Happen to You features.

Solved Problem 1.: Bond Yields and Bond Prices

An article in the Financial Times had the following headline: “U.S. Government Bond Prices Drop Ahead of Federal Reserve Meeting.” The first sentence of the article reads: “U.S. government bond yields rose to multiyear highs on Monday ahead of this week’s Federal Reserve meeting ….”

a. When a media article mentions “U.S. government bonds,” what type of bonds are they referring to?

b. Is there a contradiction between the headline and the first sentence of the article? Is the article telling us that U.S. government bonds went up or down? Briefly explain.

Solving the Problem

Step 1:Review the chapter material. This problem is about the inverse relationship between bond yields and bond prices, so you may want to review Macroeconomics, Chapter 6, Appendix, “Using Present Value” (Economics, Chapter 8, Appendix, “Using Present Value”). You may also want to review the discussion of U.S. Treasury bonds in Macroeconomics, Chapter 16, Section 16.6, “Deficits, Surpluses, and Federal Government Debt” (Economics, Chapter 26, Section 26.6, “Deficits, Surpluses, and Federal Government Debt”).

Step 2:Answer part a. by explaining what media articles are referring to when they use the phrase “U.S. government bonds.” As discussed in Chapter 16, Section 16.6, most of the bonds issued by the federal government of the United States are U.S. Treasury bonds. The Treasury sells these bonds to investors when the federal government doesn’t collect enough in tax revenues to pay for all of its spending. So, when the media refers to U.S. government bonds, without further explanation, the reference is always to U.S. Treasury bonds.

Step 3: Answer part b. by explaining that there is no contradiction between the headline and the first sentence of the article. An important fact about bond markets is that when the price of a bond falls, the yield—or interest rate—on the bond rises. The reverse is also true: When the price of a bond rises, the yield on the bond falls. The reason why this relationship holds is explained in the Appendix to Chapter 6: The price of a bond (or other financial asset) should be equal to the present value of the payments an investor receives from owning that asset. If you buy a U.S. Treasury bond, the price will equal the present value of the coupon payments the Treasury sends you during the life of the bond and the final payment to you by the Treasury of the principal, or face value of the bond. Remember that present value is the value in today’s dollars of funds to be received in the future. The higher the interest rate, the lower the present value of a payment to be received in the future. So a higher yield, or interest rate, on a bond results in a lower price of the bond because the higher yield reduces the present value of the payments to be received from the bond.

Therefore, whenever the yield on a bond rises, the price of the bond must fall (and whenever the yield on a bond falls, the price of the bond must rise. So, we can conclude that the headline of the Financial Times article and the first sentence of the article are consistent, not contradictory: Because the prices of Treasury bonds fell, the yields on the bonds must have risen.

Source: Nicholas Megaw, Naomi Rovnick, George Steer, and Hudson Lockett, “U.S. Government Bond Prices Drop Ahead of Federal Reserve Meeting,” ft.com, March 14, 2022.

Solved Problem 2: Being Careful about the Definition of Inflation

An article in the New York Times contrasted inflation during the 1970s with inflation today:

“Price increases had run high for more than a decade by the time Mr. Volcker became chair [of the Federal Reserve Board of Governors] in 1979 …. Shopper expected prices to go up, businesses knew that, and both acted accordingly. This time, inflation has been anemic for years (until recently), and most consumers and investors expect costs to return to lower levels before long, survey and market data show.”

a. What does the article mean by “inflation has been anemic for years”?

b. In the last sentence what “costs” is the article referring to?

c. Is the article correctly using the definition of inflation in the last sentence? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the definition of inflation, so you may want to review Macroeconomics, Chapter 9, Section 9.4, “Measuring Inflation” (Economics, Chapter 20, Section 20.4, “Measuring Inflation”).

Step 2:Answer part a. by explaining what the phrase “inflation has been anemic for years” means. Anemia is a medical disorder that usually has the symptom of fatigue. So, the word “anemic” is often used to mean weak. The article is arguing that until recently, the inflation rate had been weak, or slow.

Step 3: Answer part b. by explaining what the article is referring to by “costs.” Economists typically use the word costs for the amount that firm pays to produce a good—labor costs, raw material costs, and so on. Here, though, the article is using “costs” to mean “prices.” Costs is often used this way in everyday conversation: “I didn’t buy a new car because they cost too much.” Or: “Has the cost of a movie ticket increased?”

Step 4: Answer part c. by explaining whether the article is correctly using the definition of inflation. In writing “consumers and investors expect costs to return to lower levels” the article is making a common mistake. The article seems to mean that consumers and investors expect that the rate of inflation will be lower in the future. But even if the rate of inflation declines from nearly 8 percent in early 2022 to, say, 3 percent in 2023, prices will still be increasing. So, prices (“costs” in the sentence) will still be higher next year even if the rate of inflation is lower. In other words, even if the rate of increase in prices—inflation—declines, the price level will still be higher.

It’s a common mistake to think that a decline in the inflation rate means that prices will be lower, when actually prices will still be increasing, just more slowly.

Source: Jeanna Smialek, “Powell Admires Volcker. He May Have to Act Like Him,” New York Times, March 14, 2022.

Inflation as measured by the percentage change in the consumer price index (CPI) from the same month in the previous year was 7.9 percent in February 2022, the highest rate since January 1982—near the end of the Great Inflation that began in the late 1960s. The following figure shows inflation in the new motor vehicle component of the CPI. The 12.4 percent increase in new car prices was the largest since April 1975.

The increase in new car prices was being driven partly by increases in aggregate demand resulting from the highly expansionary monetary and fiscal policies enacted in response to the economic disruptions caused by the Covid-19 pandemic, and partly from shortages of semiconductors and some other car components, which reduced the supply of new cars.

As the following figure shows, inflation in used car prices was even greater. With the exception of June and July of 2021, the 41.2 percent increase in used car prices in February 2022 was the largest since the Bureau of Labor Statistics began publishing these data in 1954.

Because used cars are a substitute of new cars, rising prices of new cars caused an increase in demand for used cars. In addition, the supply of used cars was reduced because car rental firms, such as Enterprise and Hertz, had purchased fewer new cars during the worst of the pandemic and so had fewer used cars to sell to used car dealers. Increased demand and reduced supply resulted in the sharp increase in the price of used cars.

Another factor increasing the prices consumers were paying for cars was a reduction in bargaining—or haggling—over car prices. Traditionally, most goods and services are sold at a fixed price. For example, some buying a refrigerator usually pays the posted price charged by Best Buy, Lowes, or another retailer. But houses and cars have been an exception, with buyers often negotiating prices that are lower than the seller was asking.

In the case of automobiles, by federal law, the price of a new car has to be posted on the car’s window. The posted price is called the Manufacturer’s Suggested Retail Price (MSRP), often referred to as the sticker price. Typically, the sticker price represents a ceiling on what a consumer is likely to pay, with many—but not all—buyers negotiating for a lower price. Some people dislike the idea of bargaining over the price of a car, particularly if they get drawn into long negotiations at a car dealership. These buyers are likely to pay the sticker price or something very close to it.

As a result, car dealers have an opportunity to practice price discrimination: They charge buyers whose demand for cars is more price elastic lower prices and buyers whose demand is less price elastic higher prices. The car dealers are able to separate the two groups on the basis of the buyers willingness to haggle over the price of a car. (We discuss price discrimination in Microeconomics and Economics, Chapter 15, Section 15.5.) Prior to the Covid-19 pandemic, the ability of car dealers to practice this form of price discrimination had been eroded by the availability of online car buying services, such as Consumer Reports’ “Build & Buy Service,” which allow buyers to compare competing price offers from local car dealers. There aren’t sufficient data to determine whether using an online buying service results in prices as low as those obtained by buyers willing to haggle over price face-to-face with salespeople in dealerships.

In any event, in 2022 most car buyers were faced with a different situation: Rather than serving as a ceiling on the price, the MSRP, had become a floor. That is, many buyers found that given the reduced supply of new cars, they had to pay more than the MSRP. As one buyer quoted in a Wall Street Journal article put it: “The rules have changed so dramatically…. [T]he dealer’s position is ‘This is kind of a take-it-or-leave-it proposition.’” According to the website Edmunds.com, in January 2021, only about 3 percent of cars were sold in the United States for prices above MSRP, but in January 2022, 82 percent were.

Car manufacturers are opposed to dealers charging prices higher than the MSRP, fearing that doing so will damage the car’s brand. But car manufacturers don’t own the dealerships that sell their cars. The dealerships are independently owned businesses, a situation that dates back to the beginning of the car industry in the early 1900s. Early automobile manufacturers, such as Henry Ford, couldn’t raise sufficient funds to buy and operate a nationwide network of car dealerships. The manufacturers often even had trouble financing the working capital—or the funds used to finance the daily operations of the firm—to buy components from suppliers, pay workers, and cover the other costs of manufacturing automobiles.

The manufacturers solved both problems by relying on a network of independent dealerships that would be given franchises to be the exclusive sellers of a manufacturer’s brand of cars in a given area. The local businesspeople who owned the dealerships raised funds locally, often from commercial banks. Manufacturers generally paid their suppliers 30 to 90 days after receiving shipments of components, while requiring their dealers to pay a deposit on the cars they ordered and to pay the balance due at the time the cars were delivered to the dealers. One historian of the automobile industry described the process:

The great demand for automobiles and the large profits available for [dealers], in the early days of the industry … enabled the producers to exact substantial advance deposits of cash for all orders and to require cash payment upon delivery of the vehicles …. The suppliers of parts and materials, on the other hand, extended book-account credit of thirty to ninety days. Thus the automobile producer had a month or more in which to assemble and sell his vehicles before the bills from suppliers became due; and much of his labor costs could be paid from dealers’ deposits.

The franchise system had some drawbacks for car manufacturers, however. A car dealership benefits from the reputation of the manufacturer whose cars it sells, but it has an incentive to free ride on that reputation. That is, if a local dealer can take an action—such as selling cars above the MSRP—that raises its profit, it has an incentive to do so even if the action damages the reputation of Ford, General Motors, or whichever firm’s cars the dealer is selling. Car manufacturers have long been aware of the problem of car dealers free riding on the manufacturer’s reputation. For instance, in the 1920s, Ford sent so-called road men to inspect Ford dealers to check that they had clean, well-lighted showrooms and competent repair shops in order to make sure the dealerships weren’t damaging Ford’s brand.

As we discuss in Microeconomics and Economics, Chapter 10, Section 10.3, consumers often believe it’s unfair of a firm to raise prices—such as a hardware store raising the prices of shovels after a snowstorm—when the increases aren’t the result of increases in the firm’s costs. Knowing that many consumers have this view, car manufacturers in 2022 wanted their dealers not to sell cars for prices above the MSRP. As an article in the Wall Street Journal put it: “Historically, car companies have said they disapprove of their dealers charging above MSRP, saying it can reflect poorly on the brand and alienate customers.”

But the car manufacturers ran into another consequence of the franchise system. Using a franchise system rather than selling cars through manufacturer owned dealerships means that there are thousands of independent car dealers in the United States. The number of dealers makes them an effective lobbying force with state governments. As a result, most states have passed state franchise laws that limit the ability of car manufacturers to control the actions of their dealers and sometimes prohibit car manufacturers from selling cars directly to consumers. Although Tesla has attained the right in some states to sell directly to consumers without using franchised dealers, Ford, General Motors, and other manufacturers still rely exclusively on dealers. The result is that car manufacturers can’t legally set the prices that their dealerships charge.

Will the situation of most people paying the sticker price—or more—for cars persist after the current supply chain problems are resolved? AutoNation is the largest chain of car dealerships in the United States. Recently, Mike Manley, the firm’s CEO, argued that the substantial discounts from the sticker price that were common before the pandemic are a thing of the past. He argued that car manufacturers were likely to keep production of new cars more closely in balance with consumer demand, reducing the number of cars dealers keep in inventory on their lots: “We will not return to excessively high inventory levels that depress new-vehicle margins.”

Only time will tell whether the situation facing car buyers in 2022 of having to pay prices above the MSRP will persist.

Sources: Mike Colias and Nora Eckert, “A New Brand of Sticker Shock Hits the Car Market,” Wall Street Journal, February 26, 2022; Nora Eckert and Mike Colias, “Ford and GM Warn Dealers to Stop Charging So Much for New Cars,” Wall Street Journal, February 9, 2022; Gabrielle Coppola, “Car Discounts Aren’t Coming Back After Pandemic, AutoNation Says,” bloomberg.com, February 9, 2022; cr.org/buildandbuy; Lawrence H. Seltzer, A Financial History of the American Automobile Industry, Boston: Houghton-Mifflin, 1928; and Federal Reserve Bank of St. Louis.

Glenn published the following opinion column in the Wall Street Journal. Link here and full text below.

NATO Needs More Guns and Less Butter

Russia’s unprovoked invasion of Ukraine has challenged Western assumptions about security, economics and the postwar world order. In Europe and the U.S., public finances have long favored social spending over public goods such as defense. While President Biden doubled down on his proposal to increase social spending during his State of the Union address, Russia’s aggression highlights the shortcomings of this model. Western democracies now face a more uncertain and dangerous world than they did two weeks ago. Navigating it will require significantly higher levels of defense and security spending.

But change will be difficult, and the magnitude of what needs to be done is sobering. The U.S. currently spends 3.2% of gross domestic product on defense—roughly half of Cold War spending levels relative to GDP. An increase in spending of even 1% of GDP would amount to about $210 billion. That’s about 5% of the total federal spending level using a 2019 pre-Covid baseline. While Covid spending was large, it was transitory. Defense outlays would be much longer-lasting, an insurance premium or transaction cost for dealing with a more dangerous world.

The U.S. is not alone. Germany’s announcement of €100 billion in additional defense spending this year represents an increase of just over 0.25% of GDP, leaving Berlin still under the 2% commitment agreed to by North Atlantic Treaty Organization allies. Increasing Europe’s defense spending merely to the agreed-on level would require significant outlays. Such spending increases would occur against the backdrop of elevated public debt relative to GDP, brought on in part by heightened borrowing during the Covid pandemic and the earlier global financial crisis. High levels of public debt make it unlikely that countries will want to pay to increase their defense spending with new borrowing.

Paying for higher levels of defense spending will force most governments either to raise taxes or cut spending. Tax increases raise risks to growth. The larger non-U.S. NATO economies are already taxed to the hilt. Tax revenue relative to the size of the economy in France (45%), Germany (38%), Canada (34%) and the U.K. (32%) doesn’t leave much room to tax more without depressing economic activity. The U.S. has a lower tax share of GDP—about 17.5% at the federal level and 25.5% in total—but its patchwork quilt of income and payroll taxes makes tax increases more costly by distorting household and business decisions about consumption and investment.

A significant tax increase in the U.S. would need to be accompanied by fundamental tax reform, dialing back income taxes (as with the 2017 reduction in corporate tax rates) and increasing reliance on consumption taxes. A broad-based consumption tax could be implemented by imposing a tax at the business level on revenue minus purchases from other firms (a “subtraction method” value-added tax). Alternatively, the tax system could impose a broad-based wage and business cash-flow tax, with a progressive wage surtax on high earners. These consumption-tax alternatives would be efficient and equitable in a revenue-neutral tax reform. And they are crucial in avoiding decreases in savings, investment and entrepreneurship that accompany a tax increase.

Since the 1960s, spending on Social Security, Medicare and Medicaid has come to dominate the federal budget. Outlays for these programs have almost doubled since then as a share of GDP to 10.2% today, and the Congressional Budget Office projects they will consume about another 5% of GDP annually by 2040. Spending offsets to accommodate higher defense spending would surely require slowing the growth in social-insurance spending. As with tax increases, there are trade-offs. It is possible to slow the growth of this spending while preserving access to such support for lower-income Americans. Accomplishing that will require focusing net taxpayer subsidies on lower-income Americans, along with undertaking market-oriented health reforms. Such changes require serious attention.

The U.S. and its NATO allies will face a challenging set of economic trade-offs and political realities in achieving higher defense spending. The challenge will be exacerbated by additional private investment needs in a more dangerous world of investment risks, skepticism about globalization, and cybersecurity threats.

In the U.S., the failure of the 2010 Simpson-Bowles Commission’s proposed spending and tax reforms to spark a serious discussion is a warning sign. So, too, is the antipathy of Democratic and Republican officials alike toward creating the fiscal space necessary to accommodate greater defense spending. Such challenges don’t cause threats to vanish. They require leadership—now.

Supports: Macroeconomics, Chapter 10, Section 10.5, Economics Chapter 20, Section 20.5, and Essentials of Economics, Chapter 14, Section 14.2.

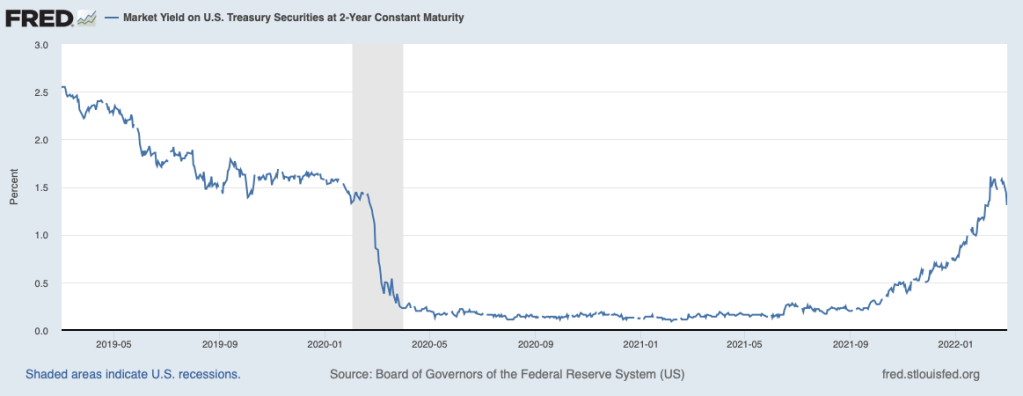

On March 2, 2022, as the conflict between Russia and Ukraine intensified, an article in the Wall Street Journal had the headline “Investors Pile Into Treasurys as Growth Concerns Flare.” The article noted that: “The 10-year Treasury yield just recorded its largest two-day decline since March 2020, while two-year Treasury yields plunged the most since 2008.”

a. What does it mean for investors to “pile into” Treasury bonds?

b. Why would investors piling into Treasury bonds cause their yields to fall?

c. What are “growth concerns”? What kind of growth are investors concerned about?

d. Why might growth concerns cause investors to buy Treasury bonds?

Solving the Problem

Step 1: Review the chapter material. This problem is about the effects of slowing economic growth on interest rates, so you may want to review Chapter 10, Section 10.5, “Saving, Investment and the Financial System.” You may also want to review Chapter 6, Appendix A (in Economics, Chapter 8, Appendix A), which explains the inverse relationship between bond prices and interest rates.

Step 2: Answer part a. by explaining what the article meant by the phrase “pile into” Treasury bonds. The article is using a slang phrase that means that investors are buying a lot of Treasury bonds.

Step 3: Answer part b. by explaining why investors piling into Treasury bonds will cause the yields on the bonds to fall. As the Appendix to Chapter 6 explains, the price of a bond represents the present value of the payments that an investor will receive over the life of the bond. Lower interest rates result in a higher present value of the payments received and, therefore, higher bond prices or—which is restating the same point—higher bond prices result in lower interest rates. If investors are increasing their demand for Treasury bonds, the increased demand will cause the prices of the bonds to increase and cause the yields—or the interest rates—on the bonds to fall.

Step 4: Answer part c. by explaining the phrase “growth concerns.” In this context, the growth being discussed is economic growth—changes in real GDP. The headline indicates that investors were concerned that the Russian invasion of Ukraine might lead to slower economic growth in the United States.

Step 5: Answer part d. by explaining why investors might purchase Treasury bonds if they were concerned about economic growth slowing. Using the model of the loanable funds markets discussed in Chapter 10, Section 10.5, we know that if economic growth slows, firms are likely to engage in fewer new investment projects, which would shift the demand curve for loanable funds to the left and result in a lower equilibrium interest rate. Investors who have purchased Treasury bonds will gain from a lower interest rate because the price of the Treasury bonds they own will increase. In addition, stock prices depend on investors’ expectations of the future profitability of firms issuing the stock. Typically, if investors believe that economic growth is likely to be slower in the future than they had previously expected, stock prices will fall, which would make Treasury bonds a more attractive investment. Finally, investors believe there is no chance that the U.S. Treasury will default on its bonds by not making the interest payments on the bonds. During an economic slowdown, investors may come to believe that the default risk on corporate bonds has increased because some corporations may run into financial problems. An increase in the default risk on corporate bonds increases the relative attractiveness of Treasury bonds as an investment.

Source: Gunjan Banerji, “Investors Pile Into Treasurys as Growth Concerns Flare,” Wall Street Journal, March 2, 2022.

Authors Glenn Hubbard & Tony O’Brien reflect on the global economic effects of Russia’s invasion of Ukraine last week. They consider the impact on the global commodity market, US monetary policy, and the impact on the financial markets in the US. Impact touches Introductory Economics, Money & Banking, International Economics, and Intermediate Macroeconomics as the effects of Russia’s aggression moves into its second week.

A map of Europe with Ukraine in the middle right below Belarus and to the east of Poland.

On Tuesday, March 1, Glenn and Tony will record a podcast on the economic consequences of the Russian invasion of Ukraine. The recording will be posted to this blog and also available through iTunes.

Some useful links

General information on developments (political and military, as well as economic):

Updates on the website of the Financial Times (note that the FT has dropped its paywall to allow non-subscribers to read this content). This article on the possible effects on the global economy is particularly worth reading.

The Twitter feed of Max Seddon, the FT’s Moscow bureau chief, is here.

The website of the New York Times has an extensive series of updates focused on military and political developments (subscription may be required).

Streaming updates on the website of the Wall Street Journal (subscription may be required).

A Twitter feed that provides timely updates on the military situation.

An article in the New Yorker discussing Russian President Vladimir Putin’s claims about the historical relationship between Russia and Ukraine.

A pessimistic blog post by a retired U.S. Army Colonel on whether the U.S. military is equipped to fight a war in Europe.

Discussions focused on economics:

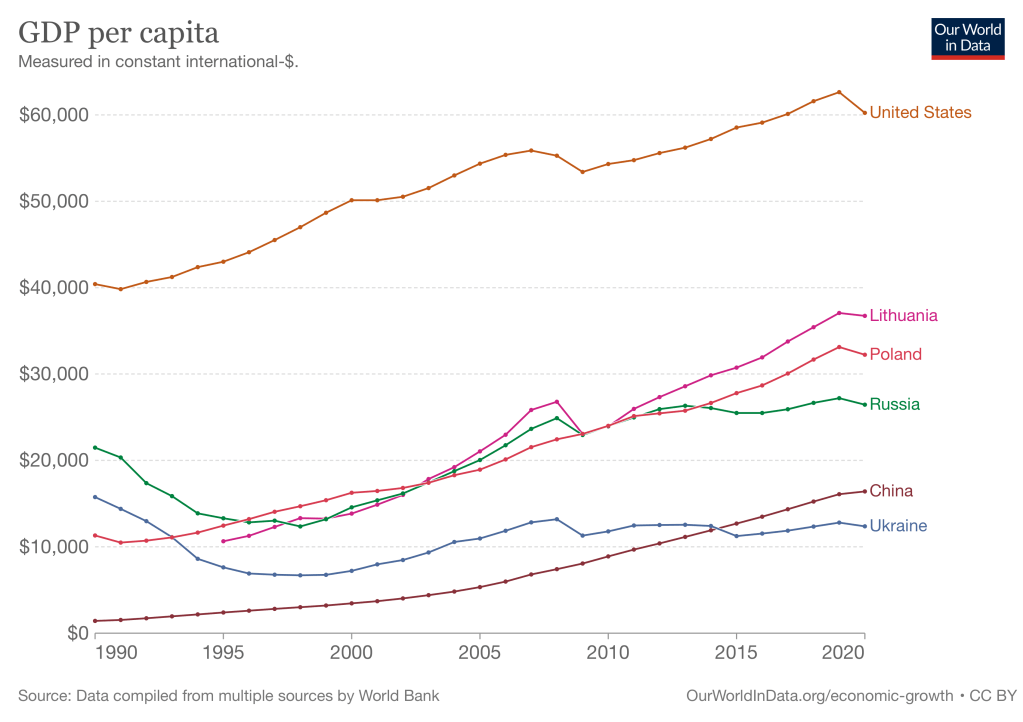

As background, the following figure from the Our World in Data site shows the growth in real GDP per capita for several countries. The underlying data were compiled by the World Bank and are measured in constant international dollars, which means that they are corrected for inflation and for variations across countries in the purchasing power of the domestic currency.

In 2020, Russian GDP per capita was less than half that of U.S. GDP per capita although about 50 percent greater than GDP per capita in China. GDP per capita in Lithuania, part of the Soviet Union until 1991, and Poland, part of the Soviet bloc until 1989, are significantly higher than in Russia. These two countries have become integrated into the European economy and have grown more rapidly than has Russia, which continues to rely heavy on exports of oil, natural gas, and other commodities. Ukraine is not as well integrated into the European economy as are Poland and Lithuania and Ukraine experienced little economic growth since attaining independence in 1991. In fact, Ukraine’s real GDP per capita was lower in 2020 than it had been in 1991.

Here is a transcript of President Joe Biden’s speech imposing sanctions on Russia.

Informative Full Stack Economics blog post by Alan Cole explaining the likely reasons why U.S. and European sanctions on Russia excluded energy. Useful explanation of the role of correspondent banking in international trade.

An article in the Economist discussing sanctions (subscription may be required).

An article in the New York Times discussing the SWIFT (Society for Worldwide Interbank Financial Telecommunications) service, which is based in Belgium, and is a key component of the international financial system. Some policymakers have proposed cutting Russia off from SWIFT. The article discusses why some countries have been opposed to taking that step (subscription may be required).

An opinion column by Justin Fox on bloomberg.com examines in what sense the United States is energy independent and the economic reasons that the U.S. still imports some oil from Russia (subscription may be required).

Blog post by economic writer Noah Smith on the possible effects of the invasion on the post-World War II international economic system.

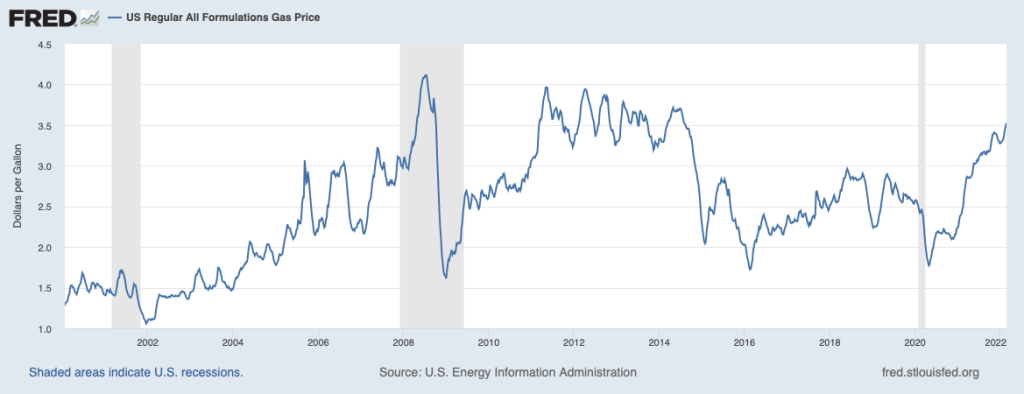

The federal government levies an excise tax of 18.4 cents per gallon of gasoline. (An excise tax is a tax that a government imposes on a particular product. In addition to the tax on gasoline, the federal government imposes excise taxes on tobacco, alcohol, airline tickets, and a few other products.) In February 2022, inflation was running at the highest level in several decades. The average retail price of gasoline across the country had risen to $3.50 per gallon from $2.60 per gallon a year earlier. The following figure shows fluctuations in the retail price of gasoline since January 2000.

Policymakers were looking for ways to lessen the effects of inflation on consumers. An article in the Wall Street Journalreported that several Democratic members of the U.S. Senate, including Mark Kelly of Arizona, Maggie Hassan of New Hampshire, and Raphael Warnock of Georgia proposed that the federal excise tax on gasoline be suspended for the remainder of 2022. The sponsors of the proposal believed that cutting the tax would reduce the price of gasoline that consumers pay at the pump. Other members of the Senate weren’t so sure, with one quoted as saying that cutting the tax was “not going to change anything” and another arguing that oil companies would receive most of the benefit of the tax cut.

Some members of Congress were opposed to suspending the gasoline tax because the revenue raised from the tax is placed in the highway trust fund, which helps to pay for federal contributions to highway building and repair and for mass transit. In that sense, the gasoline tax follows the benefits-received principle, under which people who receive benefits from a government program—in this case, highway maintenance—should help pay for the program. (We discuss the principles for evaluating taxes in Microeconomics, Chapter 17, Section 17.2 and in Economics, Chapter 17, Section 17.2) Other members of Congress were opposed to suspending the tax because they believe that the tax helps to reduce the quantity of gasoline consumed, thereby helping to slow climate change.

Focusing just on the question of the effect of suspending the tax on the retail price of gasoline, what can we conclude? The question is one of tax incidence, which looks at the actual division of the burden of a tax between buyers and sellers in a market. In other words, tax incidence looks beyond the fact that gasoline stations collect the tax and send the revenue to federal government to the issue of who actually pays the tax. As we note in Chapter 17, Section 17.3:

When the demand for a product is less elastic than supply, consumers pay the majority of the tax on the product. When the demand for a product is more elastic than supply, firms pay the majority of the tax on the product.

Consumers would receive all of the tax cut—that is, the retail price of gasoline would fall by 18.4 cents—only in the polar case where the demand for gasoline were perfectly price inelastic. Similarly, consumers would receive none of the tax cut and the price of gasoline would remain unchanged—so oil companies would receive all of the tax cut—only in the polar case where the demand for gasoline is perfectly price inelastic. (It’s a worthwhile exercise to show these two cases using demand and supply graphs.)

In the real world, we would expect to be somewhere in between these two cases, with consumers receiving some of the benefit of suspending the tax and producers receiving the remainder of the benefit. The short-run price elasticity of demand for gasoline is quite small; according to one estimate it is only −.06. The short-run price elasticity of supply of gasoline is likely to be somewhat larger than that in absolute value, which means that we would expect that consumers would receive the majority of the tax cut. (Note that we would expect the long-run price elasticities of demand and supply to both be larger for reasons we discuss in Chapter 6, Section 6.2 and 6.6.) In other words, the retail price of gasoline would fall, holding all other factors constant, but not by the full tax cut of 18.4 cents.

Joseph Doyle of MIT and Krislert Samphantharak of the University of California, San Diego studied the effect of suspension in the state excise tax on gasoline in Indiana and Illinois in 2000. In that year, Indiana suspended collecting its gasoline excise tax for 120 days and Illinois suspended its tax for 184 days. The authors estimate that consumers received about 70 percent of the tax cut in the form of lower gasoline prices. If we apply that estimate to the federal gasoline tax, then suspending the tax would lower the price of gasoline by about 12.9 cents per gallon, holding all other factors that affect the price of gasoline constant. As the above figure shows, the retail price of gasoline frequently fluctuates up and down by more than 12.9 cents, even over fairly brief periods of time. In that sense, the effect on the gasoline market of suspending the federal excise tax on gasoline would be relatively small.

Sources: Andrew Duehren and Richard Rubin, “Some Lawmakers Want to Halt Gas Tax Amid High Inflation. Others See a Gimmick,” Wall Street Journal, February 16, 2022; Tony Romm and Jeff Stein, “White House, Congressional Democrats Eye Pause of Federal Gas Tax as Prices Remain High, Election Looms,” Washington Post, February 15, 2022; Joseph J. Doyle, Jr., Krislert Samphantharak, “$2.00 Gas! Studying the Effects of a Gas Tax Moratorium,” Journal of Public Economics, Vol. 92, No.s 3-4, April 2008, pp. 869-884; and Federal Reserve Bank of St. Louis.