Lawrence Summers, professor of economics at Harvard University and secretary of the Treasury under President Bill Clinton, has been outspoken in arguing that monetary and fiscal have been too expansionary. In February 2021, just before Congress passed the American Rescure Plan, which increased federal government spending by $1.9 trillion, Summers cautioned that “there is a chance that macroeconomic stimulus on a scale closer to World War II levels than normal recession levels will set off inflationary pressures of a kind we have not seen in a generation, with consequences for the value of the dollar and financial stability.”

In a brief CNN interview found at this LINK, Summers indicates that he remains concerned that inflation may persist at high levels for a longer period than many other economists, including policymakers at the Federal Reserve, believe.

Source for quote: Lawrence H. Summers, “The Biden Stimulus Is Admirably Ambitious. But It Brings Some Big Risks, Too,” Washington Post, February 4, 2021.

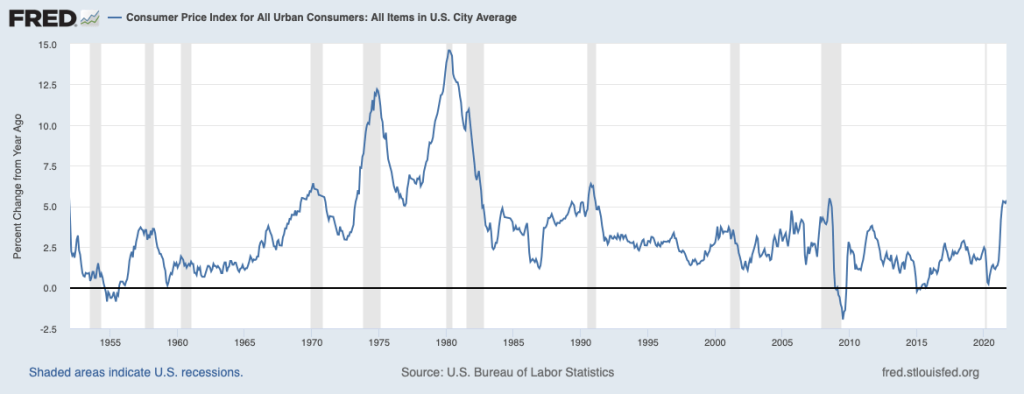

A recent publication by economists Regis Barnichon, Luiz E. Oliveira, and Adam H. Shapiro at the Federal Reserve Bank of San Francisco asks that provocative question. “The ‘60s” is a reference to the events that led to the U.S. economy experiencing more than 10 years of high inflation rates. Below is a graph similar to Chapter 15, Figure 15.1 in Macroeconomics (Economics, Chapter 25, Figure 25.1) that shows the inflation rate in the United States as measured by the percentage change in the Consumer Price Index (CPI) for each year since 1952. Economists call the years from 1968 though 1982 the “Great Inflation” because inflation was greater during that period than during any other period in the history of the United States.

As we discuss in Macroeconomics, Chapter 17, Section 17.2 (Economics, Chapter 27, Section 27.2), many economists believe that the Great Inflation began as a result of the Federal Reserve attempting to keep the unemployment rate below the natural rate of unemployment for a period of several years. As predicted by the Phillips Curve, the inflation rate increased and, as Milton Friedman and Edmund Phelps had argued would likely happen, the expected inflation rate eventually increased. The inflation was made worse during the 1970s by two supply shocks resulting from sharp increases in oil prices.

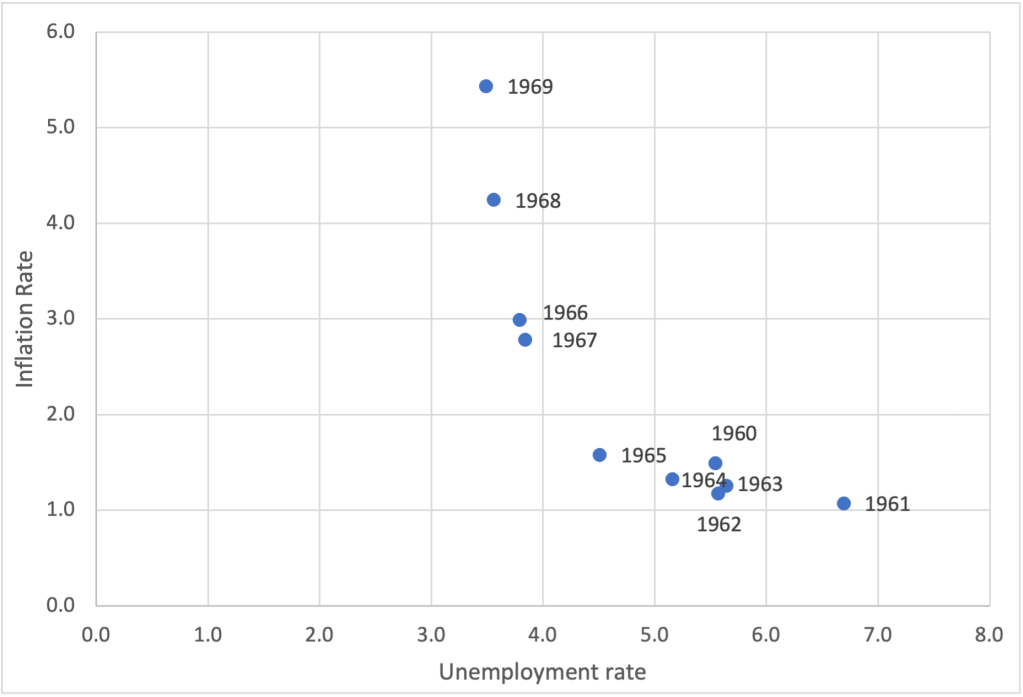

Is the United States on the edge of repeating the experience of the Great Inflation? Earlier this year, Olivier Blanchard of the Peterson Institute for International Economics wrote a paper arguing that the U.S. economy was at significant risk of experiencing a significant acceleration in inflation. His paper included a figure similar to the one below showing the combinations of inflation and unemployment during each year of the 1960s. The figure shows a substantial acceleration in inflation over the course of the decade.

Blanchard notes that:

“The history of the Phillips curve is one of shifts, largely due to the adjustment of expectations of inflation to actual inflation. True, expectations have [currently] been extremely sticky for a long time, apparently not reacting to movements in actual inflation. But, with such overheating, expectations might well deanchor. If they do, the increase in inflation could be much stronger.”

….

“If inflation were to take off, there would be two scenarios: one in which the Fed would let inflation increase, perhaps substantially, and another—more likely—in which the Fed would tighten monetary policy, perhaps again substantially. Neither of these two scenarios is ideal. In the first, inflation expectations would likely become deanchored, cancelling one of the major accomplishments of monetary policy in the last 20 years and making monetary policy more difficult to use in the future. In the second, the increase in interest rates might have to be very large, leading to problems in financial markets.”

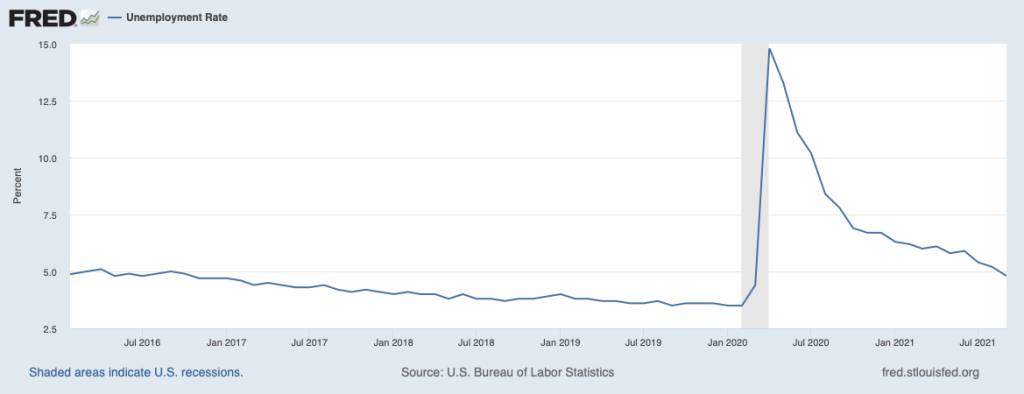

The authors of the San Francisco Fed publication are more optimistic. They begin their discussion by observing that because of the pandemic, the state of the labor market is more difficult to assess than in most years. They note that the unemployment rate of 4.8 percent in September 2021 was only slightly below the average unemployment rate over the past 30 years and well above the low unemployment rates of 2019 and early 2021. So, on the basis of the unemployment rate, policymakers at the Fed and in Congress might conclude that the inflation the U.S. economy is experiencing is not the result of overly tight labor markets such as those of the late 1960s. But the job openings rate(sometimes called the vacancy rate) is telling a different story. Job openings are positions that are both available to be filled within the next 30 days and for which firms are actively recruiting applicants from outside the firm. (According to the BLS: “The job openings rate is computed by dividing the number of job openings by the sum of employment and job openings and multiplying that quotient by 100.”)

The authors of the San Francisco Fed study note that “the vacancy rate is well above its 30-year average … and has surpassed its historic highs from the late 1960s … indicating that employers are having a difficult time filling positions. Confirming this high vacancy rate, the fraction of small businesses reporting that job openings are hard to fill is at historic highs ….” The figures below show the vacancy rate and the unemployment rate since January 2016.

The authors combine the unemployment rate and the vacancy rate into a statistic—the vacancy-to-unemployment ratio—that they demonstrate has historically done a better job of explaining movements in inflation than has the unemployment rate. They expect that expansionary fiscal policy will result in an increase in vacancy-to-unemployment ratio and, therefore, an increase in the inflation rate. But they share the view of Blanchard and many other economists that a key issue is “the stability of longer-run inflation expectations.”

We know that in the 1960s, several years of rising inflation made long-run inflation expectations unstable—in terms of the discussion in Chapter 17, the short-run Phillips curve shifted up. We don’t yet know what will happen to inflation expectations in late 2021 and in 2022, so we can’t yet tell how persistent current rates of inflation will be.

Sources: Regis Barnichon, Luiz E. Oliveira, and Adam H. Shapiro, “Is the American Rescue Plan Taking Us Back to the ’60s?,” FRBSF Economic Letter, No. 2021-27, October 18, 2021; Olivier Blanchard, “In Defense of Concerns over the $1.9 Trillion relief Plan,” piie.com, February 18, 2021; and Federal Reserve Bank of St. Louis.

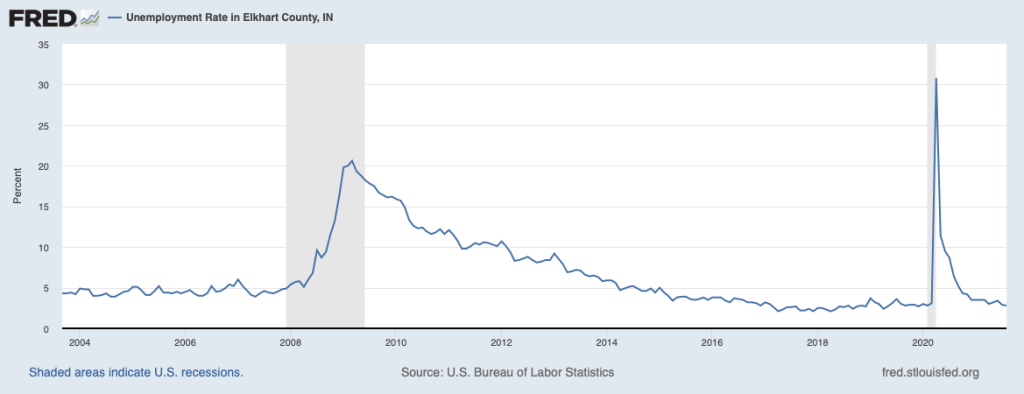

More than 80 percent of the recreational vehicles (RV) sold in the United States are manufactured in Elkhart County, Indiana. As we discuss in the opener to Chapter 22 in Economics (Chapter 12 in Macroeconomics), being dependent on sales of expensive durable goods like RVs means that the county is particularly vulnerable to the business cycle, with local firms experiencing rising sales during economic expansions and sharply falling sales during economic recessions. Accordingly, the unemployment rate in the county fluctuates much more during the business cycle than is typical—as shown in the above graph.

For example, during the Great Recession of 2007-2009, the unemployment rate in the country rose from a low of 3.9 percent in May 2007 to a high of 20 percent in March 2009, before declining during the following economic recovery. Just before the start of the Covid-19 recession of 2020, the unemployment rate in Elkhart was 2.8 percent. It then soared to 30.8 percent in April.

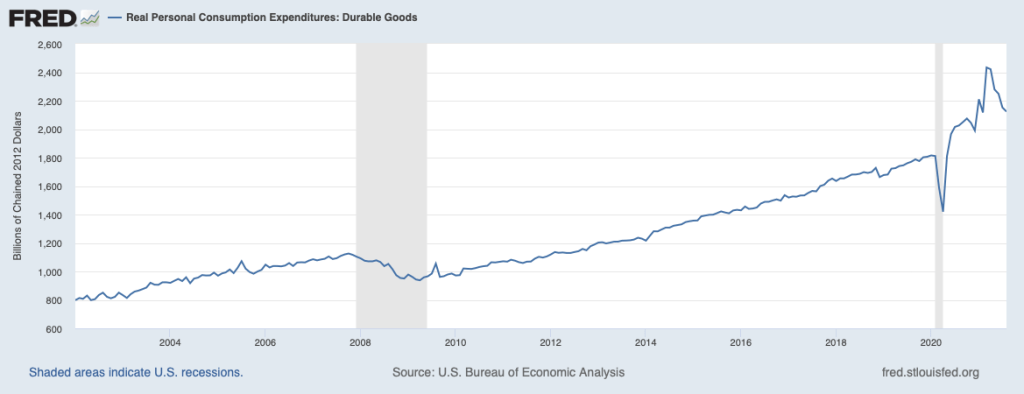

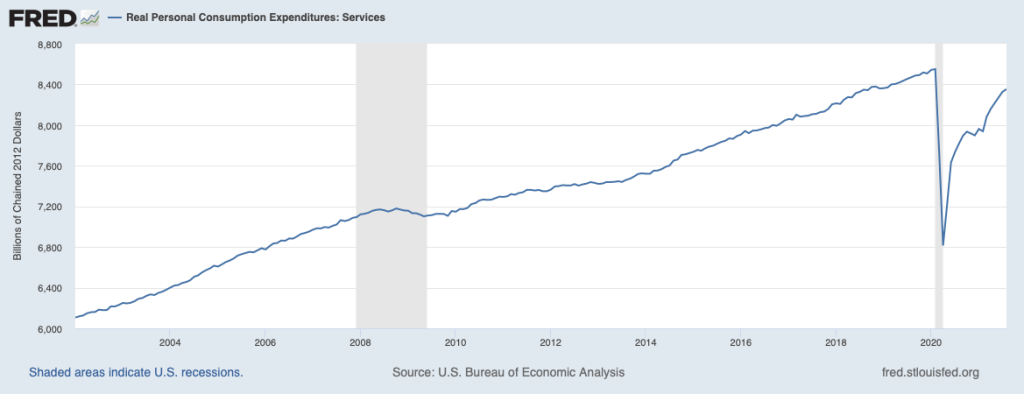

But, as we discuss in the chapter, the recovery from the 2020 recession was unusually rapid, although uneven. Many services industries, such as restaurants, gyms, and movie theaters continued to struggle well into 2021 as firms had difficulty attracting workers and as some consumers remained reluctant to spend time inside in close contact with other people. In contrast, consumer spending on durable goods was far above its pre-pandemic level, as well as being above the rate at which it had been growing during the years before the pandemic. The two graphs below show real consumer spending on durables and on services up through August 2021.

During 2021, sales of RVs through August were 50 percent higher than in the same period in 2020 and were on a pace to reach record annual sales. The success of the RV industry has led to rising incomes in Elkhart County, which, in turn, has allowed the area to attract other industries, including a logistics center that when completed will be the largest industrial building in Indiana and an Amazon warehouse that when completed will provide 1,000 new jobs. Rising incomes have also supported other businesses, such as community theaters, art galleries, and a recently reopened 1920s-era hotel.

In October 2021, the Wall Street Journal ranked Elkhart County first in its rating of metropolitan areas as measured by the index it compiles with realtor.com. The index “identifies the top metro areas for home buyers seeking an appreciating housing market and appealing lifestyle amenities.” If consumers continue to buy more goods and fewer services, it could be bad news for restaurants and other service industries, but good news for places like Elkhart that depend on goods-producing industries.

Sources: Nicole Friedman, “RV Capital of America Tops WSJ/Realtor.com Housing Index in Third Quarter,” wsj.com, October 19, 2021; Business Wire, “Amazon Announces New Robotics Fulfillment Center and Delivery Station in Elkhart County, Creating More Than 1,000 New, Full-Time Jobs,” businesswire.com, October 7, 2021; Construction Review Online, “Hotel Elkhart Grand Opening Celebrated in Elkhart, Indiana,” constructionreviewonline.com, October 4, 2021; Construction Review Online, “Elkhart County Logistics Facility to Bring about 1,000 jobs in Indiana,” constructionreviewonline.com, August 16, 2021; Federal Reserve Bank of St. Louis; and RV Industry Association.

If the price of your meal is the same, but the service is slow and the menu is limited you have experienced hidden inflation.

Each month, hundreds of employees of the Bureau of Labor Statistics gather data on prices of goods and services from stores in 87 cities and from websites. The BLS constructs the consumer price index (CPI) by giving each price a weight equal to the fraction of a typical family’s budget spent on that good or service. (We discuss the construction of the CPI in Chapter 9, Section 9.4 of Macroeconomics and Chapter 19, Section 19.4 of Economics.) Ideally, the BLS tracks prices of the same product over time. But sometimes a particular brand and style of shirt, for example, is discontinued. In that case, the BLS will use instead the price of a shirt that is a very close substitute.

A more difficult problem arises when the price of a good increases at the same time that the quality of the good improves. For instance, a new model iPhone may have both a higher price and a better battery than the model it replaces, so the higher price partly reflects the improvement in the quality of the phone. The BLS has long been aware of this problem and has developed statistical techniques that attempt to identify that part of price increases that are due to increases in quality. Economists differ in their views on how successfully the BLS has dealt with this quality bias to the measured inflation rate. Because of this bias in constructing the CPI, it’s possible that the published values of inflation may overstate the actual annual rate of inflation by 0.5 percentage point. So, for instance, the BLS might report an inflation rate of 3.5 percent when the actual inflation rate—if the BLS could determine it—was 4.0 percent.

During 2021, a number of observers pointed to a hidden type of inflation occurring, particularly in some service industries. For example, because many restaurants were having difficulty hiring servers, it was often taking longer for customers to have their orders taken and to have their food brought to the table. Because restaurants were also having difficulty hiring enough cooks, they also limited the items available on their menus. In other words, the service these restaurants were offering was not as good as it had been prior to the pandemic. So even if the restaurants kept their prices unchanged, their customers were paying the same price but receiving less.

Alan Cole, who was formerly a senior economist with the Congressional Joint Economic Committee, noted on his blog that “goods and services are getting worse faster than the official statistics acknowledge, suggesting that our inflation problem has actually been bigger than the official statistics suggest.” As examples, he noted that “hotels clean rooms less frequently on multi-night stays,” “shipping delays are longer, and phone hold times at airlines are worse.” In a column in the New York Times, economics writer Neil Irwin made similar points: “Complaints have been frequent about the cleanliness of [restaurant] tables, floors and bathrooms.” And: “People trying to buy appliances and other retail goods are waiting longer.”

A column in the Wall Street Journal on business travel by Scott McCartney was headlined “The Incredible Disappearing Hotel Breakfast.” McCartney noted that many hotels continue to advertise free hot breakfasts on their websites and apps but have stopped providing them. He also noted that hotels “have suffered from labor shortages that have made it difficult to supply services such as daily housekeeping or loyalty-group lounges,” in addition to hot breakfasts.

The BLS makes no attempt to adjust the CPI for these types of deterioration in the quality of services because doing so would be very difficult. As Irwin notes: “Customer service preferences—particularly how much good service is worth—varies highly among individuals and is hard to quantify. How much extra would you pay for a fast-food hamburger from a restaurant that cleans its restroom more frequently than the place across the street?”

As we noted earlier, most economists believe that the failure of the BLS to fully account for improvements in the quality of goods results in changes in the CPI overstating the true inflation rate. This bias may have been more than offset since the beginning of the pandemic by deterioration in the quality of services resulting in the CPI understating the true inflation rate. As the dislocations caused by the pandemic gradually resolve themselves, it seems likely that the deterioration in services will be reversed. But it’s possible that the deterioration in the provision of some services may persist. Fortunately, unless the deterioration increases over time, it would not continue to distort the measurement of the inflation rate because the same lower level of service would be included in every period’s prices.

Sources: Alan Cole, “How I Reluctantly Became an Inflation Crank,” fullstackeconomics.com, September 8, 2021; Scott McCartney, “The Incredible Disappearing Hotel Breakfast—and Other Amenities Travelers Miss,” wsj.com, October 20, 2021; and Neil Irwin, “There Is Shadow Inflation Taking Place All Around Us,” nytimes.com, October 14, 2021.

It’s customary for textbook authors to note that “much has happened in the economy” since the last edition of their book appeared. To say that much has happened since we prepared our last edition in 2019 would be a major understatement. Never in the lifetimes of today’s students and instructors have events like those of 2020 and 2021 occurred. The U.S. and world economies had experienced nothing like the Covid-19 pandemic since the influenza pandemic of 1918. In the spring of 2020, the U.S. economy suffered an unprecedented decline in the supply of goods and services as a majority of businesses in the country shut down to reduce spread of the virus. Many businesses remained closed or operated at greatly reduced capacity well into 2021. Most schools, including most colleges, switched to remote learning, which disrupted the lives of many students and their parents.

During the worst of the pandemic, total spending in the economy declined as the unemployment rate soared to levels not seen since the Great Depression of the 1930s. Reduced spending and closed businesses resulted in by far the largest decline in total production in such a short period in the history of the U.S. economy. Congress, the Trump and Biden administrations, and the Federal Reserve responded with fiscal and monetary policies that were also unprecedented.

Our updated Eighth Edition covers all of these developments as well as the policy debates they initiated. As with previous editions, we rely on extensive digital resources, including: author-created application videos and audio recordings of the chapter openers and Apply the Concept features; figure animation videos; interactive real-time data graphs animations; and Solved Problem whiteboard videos.

Glenn and Tony discuss the updated edition in this video:

Sample chapters will be available by October 15.

The full Macroeconomics text will available in early to mid December.

The full Microeconomics text will be available in mid to late December.

If you would like to view the sample chapters or are considering adopting the updated Eighth Edition for the spring semester, please contact your local Pearson representative. You can use this LINK to find and contact your representative.

Authors Glenn Hubbard and Tony O’Brien discuss the recent jobs report falling short of expectations. They also discuss the comments of Fed Chairman Powell’s comments at the Federal Reserve’s recent Jackson Hole conference. They also get to some of the recommendations of a Brookings Task Force, co-chaired by Glenn Hubbard, on ways to address financial stability. Use the links below to see more information about these timely topics: Powell’s Jackson Hole speech:

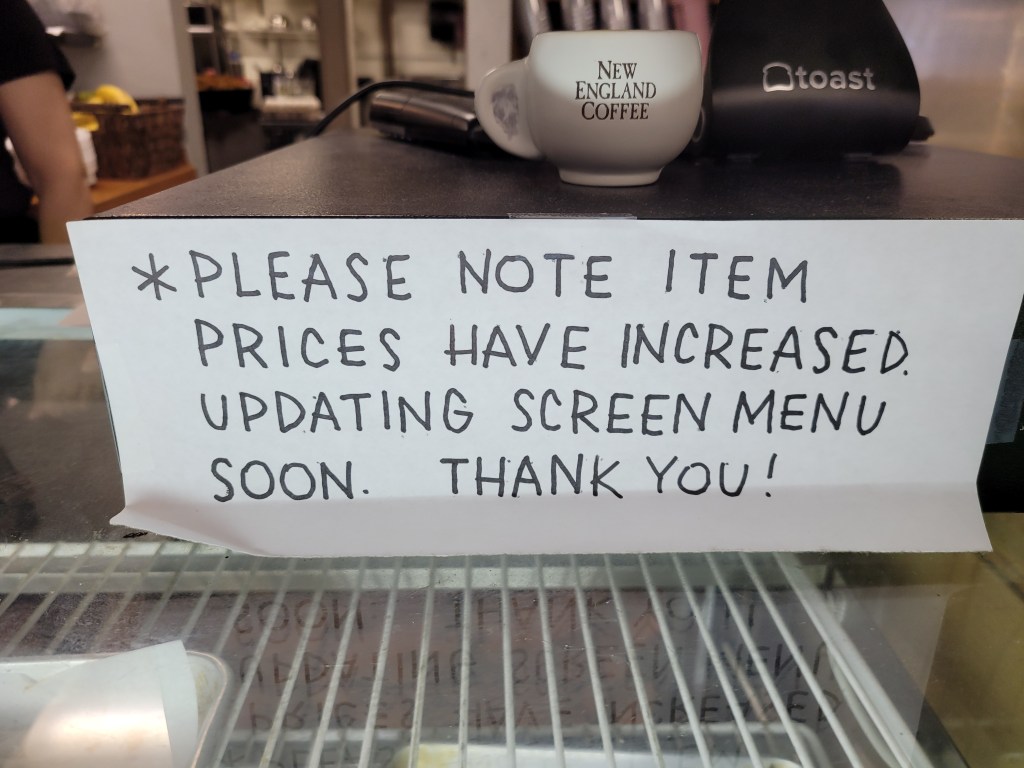

Inflation imposes a number of costs on households and firms (see our discussion in Economics, Chapter 19, Section 19.7 and Macroeconomics, Chapter 19, Section 19.7). Economists call the costs to firms of changing prices menu costs. For instance, when supermarkets raise prices, employees have to spend time changing the prices posted on shelves.

When restaurants raise prices, they have to print new menus (hence the general name economists give to these costs). Particularly during the Covid-19 pandemic, the trend toward having digital menus rather than paper ones increased. But even with digital menus, a restaurant incurs some costs, as this sign in a coffee shop indicates. An employee has to update the digital menu to reflect the new prices and, in the meantime, the shop may experience friction from customers who see one price on the digital menu and are charged a higher price when they pay at the register.

Join authors Glenn Hubbard and Tony O’Brien as they return for a new academic year! The issues have evolved but the importance of these issues has not waned. We discuss the impact of closures related to the delta variant has on the economy. The discussion extends to the active fiscal and monetary policy that has reintroduced inflation as a topic facing our economy. Many students have little or no experience with inflation so it is a learning opportunity. Check back regularly where Glenn & Tony will continue to wrestle with these important economic concepts and relate them to the classroom!

Glenn wrote the following opinion column for the New York Times.

How to Keep the Economy Booming — And Meet the Demand for Workers

In recent economic news, optimists and pessimists could both find evidence to support their outlooks.

The May jobs report showed a gain of 559,000 jobs in May and a decline in the unemployment rate to 5.8 percent. It also showed a marked improvement from last month’s weaker showing across a number of sectors, and average hourly earnings continued to rise. Ahead of the monthly report, the unemployment insurance weekly claims report on Thursday showed the number of new unemployment insurance claims fell from 405,000 the week before to 385,000 — lower than levels typically indicative of a recession (400,000). This is the first time this has happened since the pandemic-induced closures began. Further wage growth should help draw more workers back to the labor force.

Yet at the same time, the recent jobs report showed a big miss relative to the expected gain of 650,000 jobs. Constraints in supply chains and business reopenings still complicate the return to work. And workers still aren’t out of the woods: Thursday’s report indicated the total number of already unemployed individuals claiming benefits hasn’t dropped since mid-March. If job creation is robust, that contrast between falling new claims and those still on the jobless rolls is odd.

What explains these confounding tensions? To unpack them, consider the legacies of the economists John Maynard Keynes and Friedrich Hayek.

In his day, Keynes argued for boosting aggregate demand during a recession to keep workers afloat — a prescription that has clearly shaped the ultra-stimulative fiscal and monetary policies from both the Trump and the Biden administrations. His influence also resonates in the recent jobs reports: The coming rebound in the consumption of services — restaurant meals, entertainment and travel — will lift demand above its prepandemic level, and reopening and abundant consumer cash, bolstered by policy, will increase the demand for workers.

While Keynes may have lit the path to recovery after last spring’s cataclysmic job loss, he offers little to guide us through the coming labor-supply crunch. If policy actively disincentivizes the unemployed from returning to the fold, as recent reports suggest, there will be no one in place to meet the coming surge in demand, imperiling our economic rehabilitation.

To preserve the still-shaky recovery, we must now turn to Hayek, the godfather of free-market thinking. He argued that policy should allow workers to adjust to changes in the economy. Looking ahead, policymakers must consider curbing elevated unemployment benefits and a focus on old, prepandemic jobs in order to let workers and the economy adjust to new activities and new jobs that are more promising in the postpandemic world. We don’t want unemployed workers to find the postpandemic economy has passed them by.

As demand revives, supply will need to keep pace. Those in some industries, like carmakers, can simply sell off excess inventories, something that is already happening. Tool and machinery makers can increase imports to keep up. But eventually, demand must be met by higher domestic production from workers. Once businesses are freed from pandemic restrictions, we can expect to see some improvements in supply.

But holding back a faster improvement in employment and output are the very challenges Hayek identifies, including slowing down the process of matching dislocated workers to new, postpandemic jobs. That is to say, demand growth with supply constraints won’t produce the sustainable jobs recovery we need.

Many workers are taking their time to find a new job or are choosing to work less, thanks to their generous pandemic unemployment insurance benefits. These benefits provided extra income for those who lost their jobs early in the crisis. As a result, the economy’s adjustment to a postpandemic paradigm will be slow. These benefits also slow future gains in the form of higher wages workers might earn from a new and better job. But as Hayek tells us, the longer it takes for these workers to rejoin the work force, the longer it will take for them to gain these benefits.

In the coming months, we will be able to assess the potency of dealing with these forces of supply and demand by comparing employment gains in the 25 states choosing to end federal pandemic benefit supplements with the 25 states retaining them. While employment is likely to rise quickly as the pandemic fades and extra unemployment insurance benefits fall away, unemployment rates are still likely to remain high relative to prepandemic levels for another year.

If we look ahead, wage gains should be robust for those employed, particularly for lower-skilled service-sector workers — especially if some employees delay returning to work. Those higher real wages are good news for recipients.

A less welcome wild card would be inflationary pressures, fueled by demand outstripping supply. Those pressures could be a brief blip in an adjusting economy. Or they could suggest a reduction in purchasing power from higher inflation for an extended period. Higher recent inflation readings in consumer prices are a cause for concern.

Whether this happens hinges on whether the federal government and the Federal Reserve dial back their extra Keynesian demand support in time to avoid increases in expected inflation. Inflation risks robbing them of purchasing power gains from their higher wages.

The latest jobs report, then, favors a more Hayekian solution — with a nudge: Policy should support returning to work and matching workers to jobs by supporting re-employment and training for new skills, not just boosting demand. That shift offers the best chance for a sustained lift in jobs as well as demand as the pandemic recedes. In the matter Keynes v. Hayek, then: Let Hayek now prevail.

The current debate over monetary and fiscal policy has been particularly wide-ranging, touching on many of the issues we discuss in the policy chapters of the principles textbook.

Here are links to recent contributions to the debate.

Glenn and Tony discuss fiscal policy in a podcast HERE.

We discuss the Fed’s new monetary policy strategy HERE.

We discuss the current state of the labor market HERE.

The President’s Council of Economic Advisers discusses the need for additional fiscal policy measures in this POST on their blog.

An article on politico.com summarizes the debate HERE.

Harvard economist and former Treasury secretary Larry Summers has argued that fiscal and monetary policy have been too expansionary. A recent op-ed by Summers appears in the Washington PostHERE (subscription may be required).

Jason Furman, who was chair of the Council of Economic Advisers under President Obama gives his take on the division of opinion among academic economists in this Twitter THREAD.