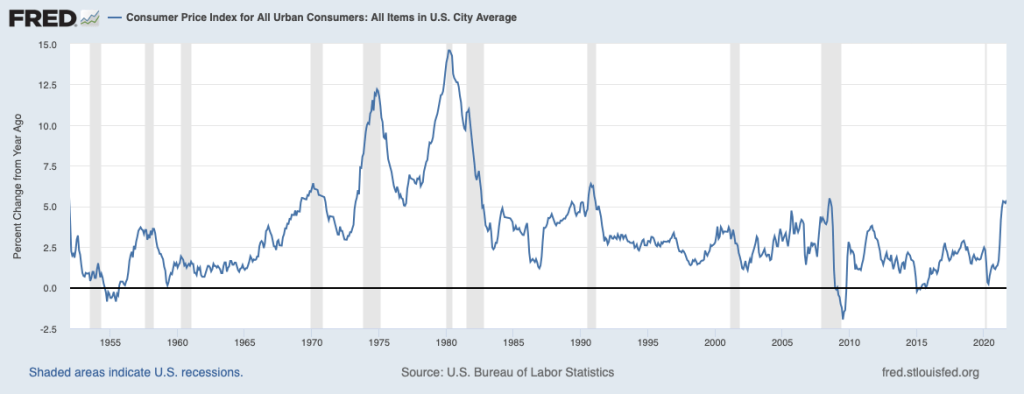

A recent publication by economists Regis Barnichon, Luiz E. Oliveira, and Adam H. Shapiro at the Federal Reserve Bank of San Francisco asks that provocative question. “The ‘60s” is a reference to the events that led to the U.S. economy experiencing more than 10 years of high inflation rates. Below is a graph similar to Chapter 15, Figure 15.1 in Macroeconomics (Economics, Chapter 25, Figure 25.1) that shows the inflation rate in the United States as measured by the percentage change in the Consumer Price Index (CPI) for each year since 1952. Economists call the years from 1968 though 1982 the “Great Inflation” because inflation was greater during that period than during any other period in the history of the United States.

As we discuss in Macroeconomics, Chapter 17, Section 17.2 (Economics, Chapter 27, Section 27.2), many economists believe that the Great Inflation began as a result of the Federal Reserve attempting to keep the unemployment rate below the natural rate of unemployment for a period of several years. As predicted by the Phillips Curve, the inflation rate increased and, as Milton Friedman and Edmund Phelps had argued would likely happen, the expected inflation rate eventually increased. The inflation was made worse during the 1970s by two supply shocks resulting from sharp increases in oil prices.

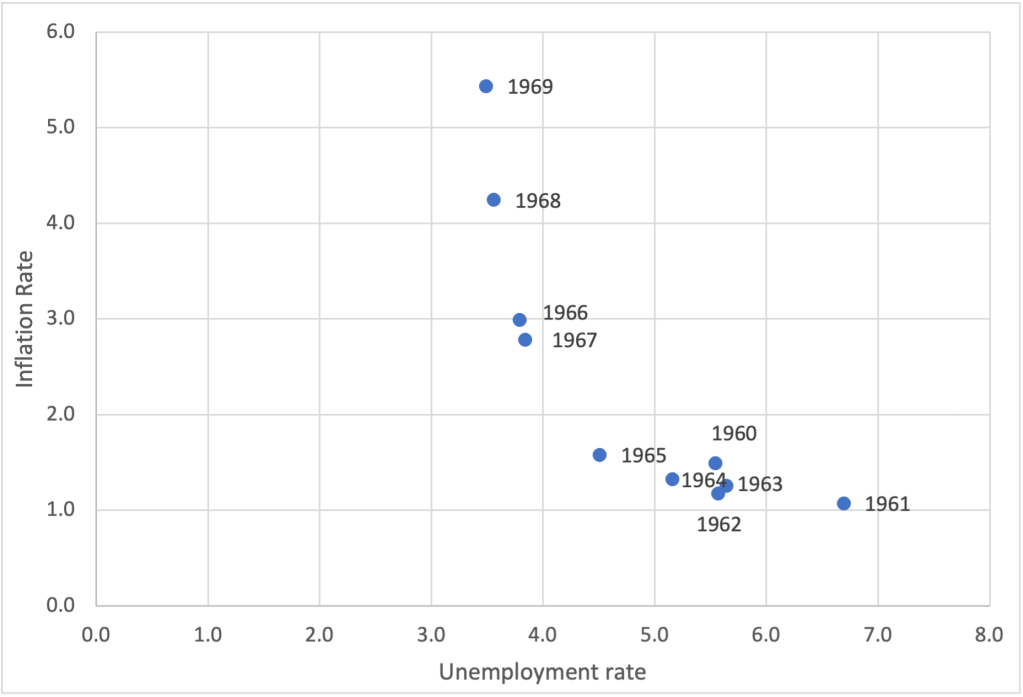

Is the United States on the edge of repeating the experience of the Great Inflation? Earlier this year, Olivier Blanchard of the Peterson Institute for International Economics wrote a paper arguing that the U.S. economy was at significant risk of experiencing a significant acceleration in inflation. His paper included a figure similar to the one below showing the combinations of inflation and unemployment during each year of the 1960s. The figure shows a substantial acceleration in inflation over the course of the decade.

Blanchard notes that:

“The history of the Phillips curve is one of shifts, largely due to the adjustment of expectations of inflation to actual inflation. True, expectations have [currently] been extremely sticky for a long time, apparently not reacting to movements in actual inflation. But, with such overheating, expectations might well deanchor. If they do, the increase in inflation could be much stronger.”

….

“If inflation were to take off, there would be two scenarios: one in which the Fed would let inflation increase, perhaps substantially, and another—more likely—in which the Fed would tighten monetary policy, perhaps again substantially. Neither of these two scenarios is ideal. In the first, inflation expectations would likely become deanchored, cancelling one of the major accomplishments of monetary policy in the last 20 years and making monetary policy more difficult to use in the future. In the second, the increase in interest rates might have to be very large, leading to problems in financial markets.”

The authors of the San Francisco Fed publication are more optimistic. They begin their discussion by observing that because of the pandemic, the state of the labor market is more difficult to assess than in most years. They note that the unemployment rate of 4.8 percent in September 2021 was only slightly below the average unemployment rate over the past 30 years and well above the low unemployment rates of 2019 and early 2021. So, on the basis of the unemployment rate, policymakers at the Fed and in Congress might conclude that the inflation the U.S. economy is experiencing is not the result of overly tight labor markets such as those of the late 1960s. But the job openings rate(sometimes called the vacancy rate) is telling a different story. Job openings are positions that are both available to be filled within the next 30 days and for which firms are actively recruiting applicants from outside the firm. (According to the BLS: “The job openings rate is computed by dividing the number of job openings by the sum of employment and job openings and multiplying that quotient by 100.”)

The authors of the San Francisco Fed study note that “the vacancy rate is well above its 30-year average … and has surpassed its historic highs from the late 1960s … indicating that employers are having a difficult time filling positions. Confirming this high vacancy rate, the fraction of small businesses reporting that job openings are hard to fill is at historic highs ….” The figures below show the vacancy rate and the unemployment rate since January 2016.

The authors combine the unemployment rate and the vacancy rate into a statistic—the vacancy-to-unemployment ratio—that they demonstrate has historically done a better job of explaining movements in inflation than has the unemployment rate. They expect that expansionary fiscal policy will result in an increase in vacancy-to-unemployment ratio and, therefore, an increase in the inflation rate. But they share the view of Blanchard and many other economists that a key issue is “the stability of longer-run inflation expectations.”

We know that in the 1960s, several years of rising inflation made long-run inflation expectations unstable—in terms of the discussion in Chapter 17, the short-run Phillips curve shifted up. We don’t yet know what will happen to inflation expectations in late 2021 and in 2022, so we can’t yet tell how persistent current rates of inflation will be.

Sources: Regis Barnichon, Luiz E. Oliveira, and Adam H. Shapiro, “Is the American Rescue Plan Taking Us Back to the ’60s?,” FRBSF Economic Letter, No. 2021-27, October 18, 2021; Olivier Blanchard, “In Defense of Concerns over the $1.9 Trillion relief Plan,” piie.com, February 18, 2021; and Federal Reserve Bank of St. Louis.