On Tuesday, August 30, 2022, the U.S. Bureau of Labor Statistics (BLS) released its Job Openings and Labor Turnover Survey (JOLTS) report for July 2022. The report indicated that the U.S. labor market remained very strong, even though, according to the Bureau of Economic Analysis (BEA), real gross domestic product (GDP) had declined during the first half of 2022. (In this blog post, we discuss the possibility that during this period the real GDP data may have been a misleading indicator of the actual state of the economy.)

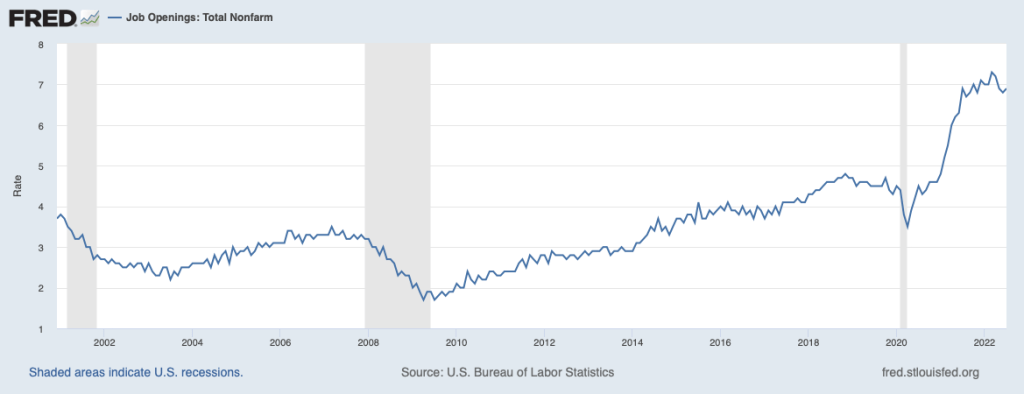

As the following figure shows, the rate of job openings remained very high, even in comparison with the strong labor market of 2019 and early 2020 before the Covid-19 pandemic began disrupting the U.S. economy. The BLS defines a job opening as a full-time or part-time job that a firm is advertising and that will start within 30 days. The rate of job openings is the number of job openings divided by the number of job openings plus the number of employed workers, multiplied by 100.

In the following figure, we compare the total number of job openings to the total number of people unemployed. The figure shows that in July 2022 there were almost two jobs available for each person who was unemployed.

Typically, a strong job market with high rates of job openings indicates that firms are expanding and that they expect their profits to be increasing. As we discuss in Macroeconomics, Chapter 6, Section 6.2 (Microeconomics and Economics, Chapter 8, Section 8.2) the price of a stock is determined by investors’ expectations of the future profitability of the firm issuing the stock. So, we might have expected that on the day the BLS released the July JOLTS report containing good news about the labor market, the stock market indexes like the Dow Jones Industrial Average, the S&P 500, and the Nasdaq Composite Index would rise. In fact, though the indexes fell, with the Dow Jones Industrial Average declining a substantial 300 points. As a column in the Wall Street Journal put it: “A surprisingly tight U.S. labor market is rotten news for stock investors.” Why did good news about the labor market could cause stock prices to decline? The answer is found in investors’ expectations of the effect the news would have on monetary policy.

In August 2022, Fed Chair Jerome Powell and the other members of the Federal Reserve Open Market Committee (FOMC) were in the process of tightening monetary policy to reduce the very high inflation rates the U.S. economy was experiencing. In July 2022, inflation as measured by the percentage change in the consumer price index (CPI) was 8.5 percent. Inflation as measured by the percentage change in the personal consumption expenditures (PCE) price index—which is the measure of inflation that the Fed uses when evaluating whether it is hitting its target of 2 percent annual inflation—was 6.3 percent. (For a discussion of the Fed’s choice of inflation measure, see the Apply the Concept “Should the Fed Worry about the Prices of Food and Gasoline,” in Macroeconomics, chapter 15, Section 15.5 and in Economics, Chapter 25, Section 25.5.)

To slow inflation, the FOMC was increasing its target for the federal funds rate—the interest rate that banks charge each other on overnight loans—which in turn was leading to increases in other interest rates, such as the interest rate on residential mortgage loans. Higher interest rates would slow increases in aggregate demand, thereby slowing price increases. How high would the FOMC increase its target for the federal funds rate? Fed Chair Powell had made clear that the FOMC would monitor economic data for indications that economic activity was slowing. Members of the FOMC were concerned that unless the inflation rate was brought down quickly, the U.S. economy might enter a wage-price spiral in which high inflation rates would lead workers to push for higher wages, which, in turn, would increase firms’ labor costs, leading them to raise prices further, in response to which workers would push for even higher wages, and so on. (We discuss the concept of a wage-price spiral in this earlier blog post.)

In this context, investors interpretated data showing unexpected strength in the economy—particularly in the labor market—as making it likely that the FOMC would need to make larger increases in its target for the federal fund rate. The higher interest rates go, the more likely that the U.S. economy will enter an economic recession. During recessions, as production, income, and employment decline, firms typically experience lower profits or even suffer losses. So, a good JOLTS report could send stock prices falling because news that the labor market was stronger than expected increased the likelihood that the FOMC’s actions would push the economy into a recession, reducing profits. Or as the Wall Street Journal column quoted earlier put it:

“So Tuesday’s [JOLTS] report was good news for workers, but not such good news for stock investors. It made another 0.75-percentage-point rate increase [in the target for the federal funds rate] from the Fed when policy makers meet next month seem increasingly likely, while also strengthening the case that the Fed will keep raising rates well into next year. Stocks sold off sharply following the report’s release.”

Sources: U.S. Bureau of Labor Statistics, “Job Openings and Labor Turnover–July 2022,” bls.gov, August 30, 2022; Justin Lahart, “Why Stocks Got Jolted,” Wall Street Journal, August 30, 2022; Jerome H. Powell, “Monetary Policy and Price Stability,” speech at “Reassessing Constraints on the Economy and Policy,” an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, August 26, 2022; and Federal Reserve Bank of St. Louis.

The Federal Reserve building in Washington, DC. Photo from the Wall Street Journal.

Four times per year, the members of the Federal Reserve’s Federal Open Market Committee (FOMC) publish their projections, or forecasts, of the values of the inflation rate, the unemployment, and changes in real gross domestic product (GDP) for the current year, each of the following two years, and for the “longer run.” The following table, released following the FOMC meeting held on March 15 and 16, 2022, shows the forecasts the members made at that time.

Median Forecast

Meidan Forecast

Median Forecast

2022

2023

2024

Longer run

Actual values, March 2022

Change in real GDP

2.8%

2.2%

2.2%

1.8%

3.5%

Unemployment rate

3.5%

3.5%

3.6%

4.0%

3.6%

PCE inflation

4.3%

2.7%

2.3%

2.0%

6.6%

Core PCE inflation

4.1%

2.6%

2.3%

No forecast

5.2%

Recall that PCE refers to the consumption expenditures price index, which includes the prices of goods and services that are in the consumption category of GDP. Fed policymakers prefer using the PCE to measure inflation rather than the consumer price index (CPI) because the PCE includes the prices of more goods and services. The Fed uses the PCE to measure whether it is hitting its target inflation rate of 2 percent. The core PCE index leaves out the prices of food and energy products, including gasoline. The prices of food and energy products tend to fluctuate for reasons that do not affect the overall long-run inflation rate. So Fed policymakers believe that core PCE gives a better measure of the underlying inflation rate. (We discuss the PCE and the CPI in the Apply the Concept “Should the Fed Worry about the Prices of Food and Gasoline?” in Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5)).

The values in the table are the median forecasts of the FOMC members, meaning that the forecasts of half the members were higher and half were lower. The members do not make a longer run forecast for core PCE. The final column shows the actual values of each variable in March 2022. The values in that column represent the percentage in each variable from the corresponding month (or quarter in the case of real GDP) in the previous year. Links to the FOMC’s economic projections can be found on this page of the Federal Reserve’s web site.

At its March 2022 meeting, the FOMC began increasing its target for the federal funds rate with the expectation that a less expansionary monetary policy would slow the high rates of inflation the U.S. economy was experiencing. Note that in that month, inflation measured by the PCE was running far above the Fed’s target inflation rate of 2 percent.

In raising its target for the federal funds rate and by also allowing its holdings of U.S. Treasury securities and mortgage-backed securities to decline, Fed Chair Jerome Powell and the other members of the FOMC were attempting to achieve a soft landing for the economy. A soft landing occurs when the FOMC is able to reduce the inflation rate without causing the economy to experience a recession. The forecast values in the table are consistent with a soft landing because they show inflation declining towards the Fed’s target rate of 2 percent while the unemployment rate remains below 4 percent—historically, a very low unemployment rate—and the growth rate of real GDP remains positive. By forecasting that real GDP would continue growing while the unemployment rate would remain below 4 percent, the FOMC was forecasting that no recession would occur.

Some economists see an inconsistency in the FOMC’s forecasts of unemployment and inflation as shown in the table. They argued that to bring down the inflation rate as rapidly as the forecasts indicated, the FOMC would have to cause a significant decline in aggregate demand. But if aggregate demand declined significantly, real GDP would either decline or grow very slowly, resulting in the unemployment rising above 4 percent, possibly well above that rate. For instance, writing in the Economist magazine, Jón Steinsson of the University of California, Berkeley, noted that the FOMC’s “combination of forecasts [of inflation and unemployment] has been dubbed the ‘immaculate disinflation’ because inflation is seen as falling rapidly despite a very tight labor market and a [federal funds] rate that is for the most part negative in real terms (i.e., adjusted for inflation).”

Similarly, writing in the Washington Post, Harvard economist and former Treasury secretary Lawrence Summers noted that “over the past 75 years, every time inflation has exceeded 4 percent and unemployment has been below 5 percent, the U.S. economy has gone into recession within two years.”

In an interview in the Financial Times, Olivier Blanchard, senior fellow at the Peterson Institute for International Economics and former chief economist at the International Monetary Fund, agreed. In their forecasts, the FOMC “had unemployment staying at 3.5 percent throughout the next two years, and they also had inflation coming down nicely to two point something. That just will not happen. …. [E]ither we’ll have a lot more inflation if unemployment remains at 3.5 per cent, or we will have higher unemployment for a while if we are actually to inflation down to two point something.”

While all three of these economists believed that unemployment would have to increase if inflation was to be brought down close to the Fed’s 2 percent target, none were certain that a recession would occur.

What might explain the apparent inconsistency in the FOMC’s forecasts of inflation and unemployment? Here are three possibilities:

Fed policymakers are relatively optimistic that the factors causing the surge in inflation—including the economic dislocations due to the Covid-19 pandemic and the Russian invasion of Ukraine and the surge in federal spending in early 2021—are likely to resolve themselves without the unemployment rate having to increase significantly. As Steinsson puts it in discussing this possibility (which he believes to be unlikely) “it is entirely possible that inflation will simply return to target as the disturbances associated with Covid-19 and the war in Ukraine dissipate.”

Fed Chair Powell and other members of the FOMC were convinced that business managers, workers, and investors still expected that the inflation rate would return to 2 percent in the long run. As a result, none of these groups were taking actions that might lead to a wage-price spiral. (We discussed the possibility of a wage-price spiral in earlier blog post.) For instance, at a press conference following the FOMC meeting held on May 3 and 4, 2022, Powell argued that, “And, in fact, inflation expectations [at longer time horizons] come down fairly sharply. Longer-term inflation expectations have been reasonably stable but have moved up to—but only to levels where they were in 2014, by some measures.” If Powell’s assessment was correct that expectations of future inflation remained at about 2 percent, the probability of a soft landing was increased.

We should mention the possibility that at least some members of the FOMC may have expected that the unemployment rate would increase above 4 percent—possibly well above 4 percent—and that the U.S. economy was likely to enter a recession during the coming months. They may, however, have been unwilling to include this expectation in their published forecasts. If members of the FOMC state that a recession is likely, businesses and households may reduce their spending, which by itself could cause a recession to begin.

Sources: Martin Wolf, “Olivier Blanchard: There’s a for Markets to Focus on the Present and Extrapolate It Forever,” ft.com, May 26, 2022; Lawrence Summers, “My Inflation Warnings Have Spurred Questions. Here Are My Answers,” Washington Post, April 5, 2022; Jón Steinsson, “Jón Steinsson Believes That a Painless Disinflation Is No Longer Plausible,” economist.com, May 13, 2022; Federal Open Market Committee, “Summary of Economic Projections,” federalreserve.gov, March 16, 2022; and Federal Open Market Committee, “Transcript of Chair Powell’s Press Conference May 4, 2022,” federalreserve.gov, May 4, 2022.

On Thursday morning, April 28, the Bureau of Economic Analysis (BEA) released its “advance” estimate for the change in real GDP during the first quarter of 2022. As shown in the first line of the following table, somewhat surprisingly, the estimate showed that real GDP had declined by 1.4 percent during the first quarter. The Federal Reserve Bank of Atlanta’s “GDP Now” forecast had indicated that real GDP would increase by 0.4 percent in the first quarter. Earlier in April, the Wall Street Journal’s panel of academic, business, and financial economists had forecast an increase of 1.2 percent. (A subscription may be required to access the forecast data from the Wall Street Journal’s panel.)

Do the data on real GDP from the first quarter of 2022 mean that U.S. economy may already be in recession? Not necessarily, for several reasons:

First, as we note in the Apply the Concept, “Trying to Hit a Moving Target: Making Policy with ‘Real-Time’ Data,” in Macroeconomics, Chapter 15, Section 15.3 (Economics, Chapter 25, Section 25.3): “The GDP data the BEA provides are frequently revised, and the revisions can be large enough that the actual state of the economy can be different for what it at first appears to be.”

Second, even though business writers often define a recession as being at least two consecutive quarters of declining real GDP, the National Bureau of Economic Research has a broader definition: “A recession is a significant decline in activity across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.” Particularly given the volatile movements in real GDP during and after the pandemic, it’s possible that even if real GDP declines during the second quarter of 2022, the NBER might not decide to label the period as being a recession.

Third, and most importantly, there are indications in the underlying data that the U.S. economy performed better during the first quarter of 2022 than the estimate of declining real GDP would indicate. In a blog post in January discussing the BEA’s advance estimate of real GDP during the fourth quarter of 2021, we noted that the majority of the 6.9 percent increase in real GDP that quarter was attributable to inventory accumulation. The earlier table indicates that the same was true during the first quarter of 2022: 60 percent of the decline in real GDP during the quarter was the result of a 0.84 decline in inventory investment.

We don’t know whether the decline in inventories indicates that firms had trouble meeting demand for goods from current inventories or whether they decided to reverse some of the increases in inventories from the previous quarter. With supply chain disruptions continuing as China grapples with another wave of Covid-19, firms may be having difficulty gauging how easily they can replace goods sold from their current inventories. Note the corresponding point that the decline in sales of domestic product (line 2 in the table) was smaller than the decline in real GDP.

The table below shows changes in the components of real GDP. Note the very large decline exports and in purchases of goods and services by the federal government. (Recall from Macroeconomics, Chapter 16, Section 16.1, the distinction between government purchases of goods and services and total government expenditures, which include transfer payments.) The decline in federal defense spending was particularly large. It seems likely from media reports that the escalation of Russia’s invasion of Ukraine will lead Congress and President Biden to increase defense spending.

Notice also that increases in the non-government components of aggregate demand remained fairly strong: personal consumption expenditures increased 2.7 percent, gross private domestic investment increased 2.3 percent, and imports surged by 17.7 percent. These data indicate that private demand in the U.S. economy remains strong.

So, should we conclude that the economy will shrug off the decline in real GDP during the first quarter and expand during the remainder of the year? Unfortunately, there are still clouds on the horizon. First, there are the difficult to predict effects of continuing supply chain problems and of the war in Ukraine. Second, the Federal Reserve has begun tightening monetary policy. Whether Fed Chair Jerome Powell will be able to bring about a soft landing, slowing inflation significantly while not causing a large jump in unemployment, remains the great unknown of economic policy. Finally, if high inflation rates persist, households and firms may respond in ways that are difficult to predict and, may, in particular decide to reduce their spending from the current strong levels.

It now seems clear that the new monetary policy strategy the Fed announced in August 2020 was a decisive break with the past in one respect: With the new strategy, the Fed abandoned the approach dating to the 1980s of preempting inflation. That is, the Fed would no longer begin raising its target for the federal funds rate when data on unemployment and real GDP growth indicated that inflation was likely to rise. Instead, the Fed would wait until inflation had already risen above its target inflation rate.

Since 2012, the Fed has had an explicit inflation target of 2 percent. As we discussed in a previous blog post, with the new monetary policy the Fed announced in August 2020, the Fed modified how it interpreted its inflation target: “[T]he Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

The Fed’s new approach is sometimes referred to as average inflation targeting (AIT) because the Fed attempts to achieve its 2 percent target on average over a period of time. But as former Fed Vice Chair Richard Clarida discussed in a speech in November 2020, the Fed’s monetary policy strategy might be better called a flexible average inflation target (FAIT) approach rather than a strictly AIT approach. Clarida noted that the framework was asymmetric, meaning that inflation rates higher than 2 percent need not be offset with inflation rates lower than 2 percent: “The new framework is asymmetric. …[T]he goal of monetary policy … is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent.” And: “Our framework aims … for inflation to average 2 percent over time, but it does not make a … commitment to achieve … inflation outcomes that average 2 percent under any and all circumstances ….”

Inflation began to increase rapidly in mid-2021. The following figure shows three measure of inflation, each calculated as the percentage change in the series from the same month in the previous year: the consumer price index (CPI), the personal consumption expenditure (PCE) price index, and the core PCE—which excludes the prices of food and energy. Inflation as measured by the CPI is sometimes called headline inflation because it’s the measure of inflation that most often appears in media stories about the economy. The PCE is a broader measure of the price level in that it includes the prices of more consumer goods and services than does the CPI. The Fed’s target for the inflation rate is stated in terms of the PCE. Because prices of food and inflation fluctuate more than do the prices of other goods and services, members of the Fed’s Federal Open Market Committee (FOMC) generally consider changes in the core PCE to be the best measure of the underlying rate of inflation.

The figure shows that for most of the period from 2002 through early 2021, inflation as measured by the PCE was below the Fed’s 2 percent target. Since that time, inflation has been running well above the Fed’s target. In February 2022, PCE inflation was 6.4 percent. (Core PCE inflation was 5.4 percent and CPI inflation was 7.9 percent.) At its March 2022 meeting the FOMC begin raising its target for the federal funds rate—well after the increase in inflation had begun. The Fed increased its target for the federal funds rate by 0.25 percent, which raised the target from 0 to 0.25 percent to 0.25 to 0.50 percent.

Should the Fed have taken action to reduce inflation earlier? To answer that question, it’s first worth briefly reviewing Fed policy during the Great Inflation of 1968 to 1982. In the late 1960s, total federal spending grew rapidly as a result of the Great Society social programs and the war in Vietnam. At the same time, the Fed increased the rate of growth of the money supply. The result was an end to the price stability of the 1952-1967 period during which the annual inflation rate had averaged only 1.6 percent.

The 1973 and 1979 oil price shocks also contributed to accelerating inflation. Between January 1974 and June 1982, the annual inflation rate averaged 9.3 percent. This was the first episode of sustained inflation outside of wartime in U.S. history—until now. Although the oil price shocks and expansionary fiscal policy contributed to the Great Inflation, most economists, inside and outside of the Fed, eventually concluded that Fed policy failures were primarily responsible for inflation becoming so severe.

The key errors are usually attributed to Arthur Burns, who was Fed Chair from January 1970 to March 1978. Burns, who was 66 at the time of his appointment, had made his reputation for his work on business cycles, mostly conducted prior to World War II at the National Bureau of Economic Research. Burns was skeptical that monetary policy could have much effect on inflation. He was convinced that inflation was mainly the result of structural factors such as the power of unions to push up wages or the pricing power of large firms in concentrated industries.

Accordingly, Burns was reluctant to raise interest rates, believing that doing so hurt the housing industry without reducing inflation. Burns testified to Congress that inflation “poses a problem that traditional monetary and fiscal remedies cannot solve as quickly as the national interest demands.” Instead of fighting inflation with monetary policy he recommended “effective controls over many, but by no means all, wage bargains and prices.” (A collection Burns’s speeches can be found here.)

Few economists shared Burns’s enthusiasm for wage and price controls, believing that controls can’t end inflation, they can only temporarily reduce it while causing distortions in the economy. (A recent overview of the economics of price controls can be found here.) In analyzing this period, economists inside and outside the Fed concluded that to bring the inflation rate down, Burns should have increased the Fed’s target for the federal funds rate until it was higher than the inflation rate. In other words, the real interest rate, which equals the nominal—or stated—interest rate minus the inflation rate, needed to be positive. When the real interest rate is negative, a business may, for example, pay 6% on a bond when the inflation rate is 10%, so they’re borrowing funds at a real rate of −4%. In that situation, we would expect borrowing to increase, which can lead to a boom in spending. The higher spending worsens inflation.

Because Burns and the FOMC responded only slowly to rising inflation, workers, firms, and investors gradually increased their expectations of inflation. Once higher expectation inflation became embedded, or entrenched, in the U.S. economy it was difficult to reduce the actual inflation rate without increasing the target for the federal funds rate enough to cause a significant slowdown in the growth of real GDP and a rise in the unemployment rate. As we discuss in Macroeconomics, Chapter 17, Sections 17.2 and 17.3 (Economics, Chapter 27, Sections 27.2 and 27.3), the process of the expected inflation rate rising over time to equal the actual inflation rate was first described in research conducted separately by Nobel Laureates Milton Friedman and Edmund Phelps during the 1960s.

An implication of Friedman and Phelps’s work is that because a change in monetary policy takes more than a year to have its full effect on the economy, if the Fed waits until inflation has already increased, it will be too late to keep the higher inflation rate from becoming embedded in interest rates and long-term labor and raw material contracts.

Paul Volcker, appointed Fed chair by Jimmy Carter in 1979, showed that, contrary to Burns’s contention, monetary policy could, in fact, deal with inflation. By the time Volcker became chair, inflation was above 11%. By raising the target for the federal funds rate to 22%—it was 7% when Burns left office—Volcker brought the inflation rate down to below 4%, but only at the cost of a severe recession during 1981–1982, during which the unemployment rate rose above 10 percent for the first time since the Great Depression of the 1930s. Note that whereas Burns had largely failed to increase the target for the federal funds as rapidly as inflation had increased—resulting in a negative real federal funds rate—Volcker had raised the target for the federal funds rate above the inflation rate—resulting in a positive real federal funds rate.

Because the 1981–1982 recession was so severe, the inflation rate declined from above 11 percent to below 4 percent. In Chapter 17, Figure 17.10 (reproduced below), we plot the course of the inflation and unemployment rates from 1979 to 1989.

Caption: Under Chair Paul Volcker, the Fed began fighting inflation in 1979 by reducing the growth of the money supply, thereby raising interest rates. By 1982, the unemployment rate had risen to 10 percent, and the inflation rate had fallen to 6 percent. As workers and firms lowered their expectations of future inflation, the short-run Phillips curve shifted down. The adjustment in expectations allowed the Fed to switch to an expansionary monetary policy, which by 1987 brought unemployment back to the natural rate of unemployment, with an inflation rate of about 4 percent. The orange line shows the actual combinations of unemployment and inflation for each year from 1979 to 1989.

The Fed chairs who followed Volcker accepted the lesson of the 1970s that it was important to head off potential increases in inflation before the increases became embedded in the economy. For instance, in 2015, then Fed Chair Janet Yellen in explaining why the FOMC was likely to raise to soon its target for the federal funds rate noted that: “A substantial body of theory, informed by considerable historical evidence, suggests that inflation will eventually begin to rise as resource utilization continues to tighten. It is largely for this reason that a significant pickup in incoming readings on core inflation will not be a precondition for me to judge that an initial increase in the federal funds rate would be warranted.”

Between 2015 and 2018, the FOMC increased its target for the federal funds rate nine times, raising the target from a range of 0 to 0.25 percent to a range of 2.25 to 2.50 percent. In 2018, Raphael Bostic, president of the Federal Reserve Bank of Atlanta justified these rate increases by noting that “… we shouldn’t forget that [the Fed’s] credibility [with respect to keeping inflation low] was hard won. Inflation expectations are reasonably stable for now, but we know little about how far the scales can tip before it is no longer so.”

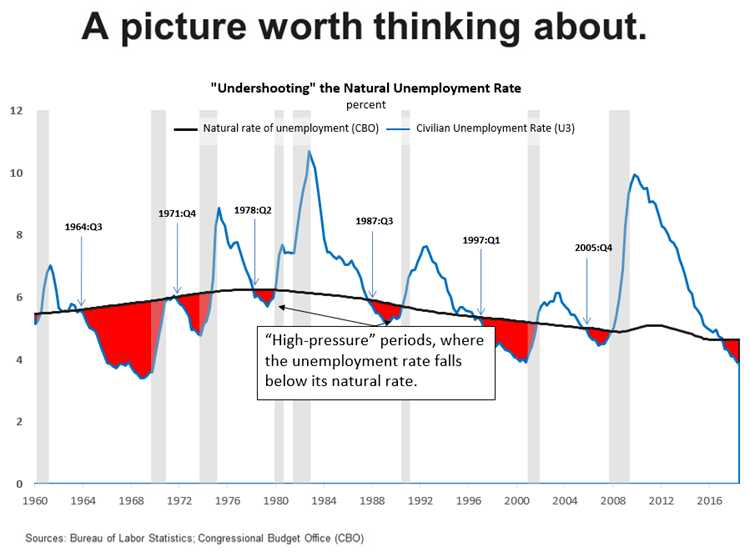

He used the following figure to illustrate his point.

Bostic interpreted the figure as follows:

“[The red areas in the figure are] periods of time when the actual unemployment rate fell below what the U.S. Congressional Budget Office now estimates as the so-called natural rate of unemployment. I refer to these episodes as “high-pressure” periods. Here is the punchline. Dating back to 1960, every high-pressure period ended in a recession. And all but one recession was preceded by a high-pressure period….

I think a risk management approach requires that we at least consider the possibility that unemployment rates that are lower than normal for an extended period are symptoms of an overheated economy. One potential consequence of overheating is that inflationary pressures inevitably build up, leading the central bank to take a much more “muscular” stance of policy at the end of these high-pressure periods to combat rising nominal pressures. Economic weakness follows [resulting typically, as indicated in the figure by the gray band, in a recession].”

By July 2019, a majority of the members of the FOMC, including Chair Powell, had come to believe that with no sign of inflation accelerating, they could safely cut the federal funds rate. But they had not yet explicitly abandoned the view that the FOMC should act to preempt increases in inflation. The formal change came in August 2020 when, as discussed earlier, the FOMC announced the new FAIT.

At the time the FOMC adopted its new monetary policy strategy, most members expected that any increase in inflation owing to problems caused by the Covid-19 pandemic—particularly the disruptions in supply chains—would be transitory. Because inflation has proven to be more persistent than Fed policymakers and many economists expected, two aspects of the FAIT approach to monetary policy have been widely discussed: First, the FOMC did not explicitly state by how much inflation can exceed the 2 percent target or for how long it needs to stay there before the Fed will react. The failure to elaborate on this aspect of the policy has made it more difficult for workers, firms, and investors to gauge the Fed’s likely reaction to the acceleration in inflation that began in the spring of 2021. Second, the FOMC’s decision to abandon the decades-long policy of preempting inflation may have made it more difficult to bring inflation down to the 2 percent target without causing a recession.

Federal Reserve Governor Lael Brainard recently remarked that “it is of paramount importance to get inflation down” and some Fed policymakers believe that the FOMC will have to begin increasing its target for the federal funds rate more aggressively. (The speech in which Governor Brainard discusses her current thinking on monetary policy can be found here.) For instance James Bullard, president of the Federal Reserve Bank of St. Louis, has argued in favor of raising the target to above 3 percent this year. With the Fed’s preferred measure of inflation running above 5 percent, it would take substantial increases int the target to achieve a positive real federal funds rate.

It is an open question whether Jerome Powell finds himself in a position similar to that of Paul Volcker in 1979: Rapid increases in interest rates may be necessary to keep inflation from accelerating, but doing so risks causing a recession. In a recent speech (found here), Powell pledged that: “We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

But Powell argued that the FOMC could achieve “a soft landing, with inflation coming down and unemployment holding steady” even if it is forced to rapidly increase its target for the federal funds rate:

“Some have argued that history stacks the odds against achieving a soft landing, and point to the 1994 episode as the only successful soft landing in the postwar period. I believe that the historical record provides some grounds for optimism: Soft, or at least softish, landings have been relatively common in U.S. monetary history. In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession.”

Some economists have been skeptical that a soft landing is likely. Harvard economist and former Treasury Secretary Lawrence Summers has been particularly critical of Fed policy, as in this Twitter thread. Summers concludes that: “I am apprehensive that we will be disappointed in the years ahead by unemployment levels, inflation levels, or both.” (Summers and Harvard economist Alex Domash provide an extended discussion in a National Bureau of Economic Research Working Paper found here.)

Clearly, we are in a period of great macroeconomic uncertainty.

In respect to its mandate to achieve price stability, the Federal Open Market Committee focuses on data for the personal consumption expenditure (PCE) price index and the core PCE price index. (The core PCE price index omits food and energy prices, as does the core consumer price index.) After the March, June, September, and December FOMC meetings, each committee member projects future values of these price indexes. The projections, which are made public, provide a means for investors, businesses, and households to understand what the Fed expects to happen with future inflation.

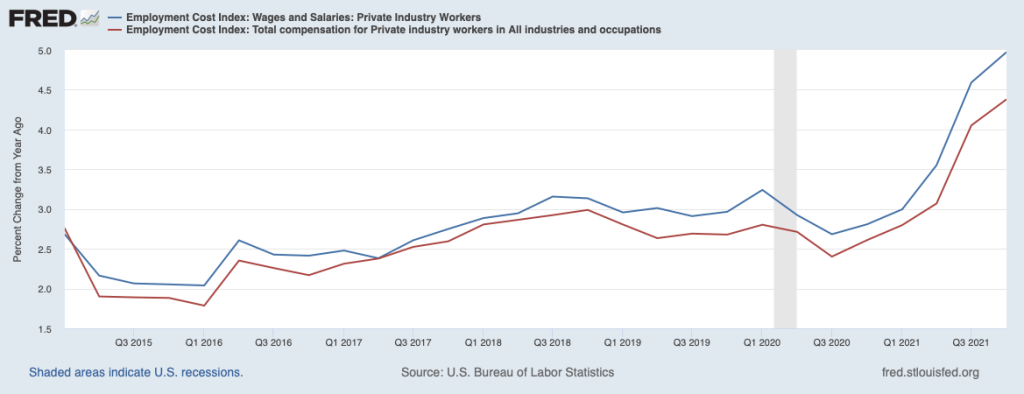

In his press conference following the December 2021 FOMC meeting, Chair Jerome Powell surprised some economists by discussing the importance of the employment cost index (ECI) in the committee’s evaluation of the current state of inflation. Powell was asked this question by a journalist: “I wonder if you could talk a little bit about what prompted your recent pivot toward greater wariness around inflation.” He responded, in part:

“We got the ECI reading on the eve of the November meeting—it was the Friday before the November meeting—and it was very high, 5.7 percent reading for the employment compensation index for the third quarter … That’s really what happened [that resulted in FOMC deciding to focus more on inflation]. It was essentially higher inflation and faster—turns out much faster progress in the labor market.”

The ECI is compiled by the Bureau of Labor Statistics and is published quarterly. It measures the cost to employers per employee hour worked. The BLS publishes data that includes only wages and salaries and data that includes, in addition to wages and salaries, non-wage benefits—such as contributions to retirement accounts or health insurance—that firms pay workers. The figure below shows the ECI including just wages and salaries (red line) and including all compensation (blue line). The difference between the two lines shows that wages and salaries have been increasing more rapidly than has total compensation.

A focus on the labor market when analyzing inflation is unsurprising. In Macroeconomics, Chapter 17, Section 17.1 (Economics, Chapter 27, Section 27.1) we discuss how the Phillips curve links the state of the labor market—as measured by the unemployment rate—to the inflation rate. The link between the unemployment rate and the inflation rate operates through the labor market: When the unemployment rate is low, firms raise wages as they attempt to attract the relatively small number of available workers and to keep their own workers from leaving. (As first drawn by economist A.W. Phillips, the Phillips curve showed the relationship between the unemployment rate and the rate of wage inflation, rather than the relationship between the unemployment rate and the rate of price inflation.) As firms’ wage costs rise, they increase prices. So, as Powell noted, we would expect that if wages are rising rapidly, the rate of price inflation will also increase.

Powell noted that the FOMC is concerned that rising wages might eventually lead to a wage-price spiral in which higher wages lead to higher prices, which, in turn, cause workers to press for higher nominal wages to keep their real wages from falling, which then leads firms to increases their prices even more, and so on. Some economists interpret the inflation rates during the Great Inflation for 1968–1982 as resulting from a wage-price spiral. One condition for a wage-price spiral to begin is that workers and firms cease to believe that the Fed will be able to return to its target inflation rate—which is currently 2 percent.

In terms of the Phillips curve analysis of Chapter 17, a wage-price spiral can be interpreted as a shifting up of the short-run Phillips curve. The Phillips curve shifts up when households, firms, and investors increase their expectations of future inflation. We discuss this process in Chapter 17, Section 17.2. As the short-run Phillips curve shifts up the tradeoff between inflation and unemployment becomes worse. That is, the inflation rate is higher at every unemployment rate. For the Fed to reduce the inflation rate—bring it back down to the Fed’s target—becomes more difficult without causing a recession. The Great Inflation was only ended after the Fed raised its target for the federal funds rate to levels that helped cause the severe recession of 1981–1982.

The FOMC has been closely monitoring movements in the ECI to make sure that it heads off a wage-price spiral before it begins.

Sources: The transcript of Chair Powell’s press conference can be found here; the most recent economic projections of FOMC members can be found here; and a news article discussing Powell’s fears of a wage-price spiral can be found here (subscription may be required).

Fed Chair Jerome Powell (Photo from the Associated Press)

The results of the meeting were largely as expected: The FOMC statement indicated that the Fed remained concerned about “elevated levels of inflation” and that “the Committee expects it will soon be appropriate to raise the target range for the federal funds rate.”

In a press conference following the meeting, Fed Chair Jerome Powell suggested that the FOMC would begin raising its target for the federal funds at its March meeting. He also noted that it was possible that the committee would have to raise its target more quickly than previously expected: “We will remain attentive to risks, including the risk that high inflation is more persistent than expected, and are prepared to respond as appropriate.”

Some other points:

The Federal Reserve Act gives the Federal reserve the dual mandate of “maximum employment” and “price stability.” Neither policy goal is defined in the act. In its new monetary policy strategy announced in August 2020, the Fed stated that it would consider the goal of price stability to have been achieved if annual inflation measured by the change in the core personal consumption expenditures (PCE) price index averaged 2 percent over time. The Fed was less clear about defining the meaning of maximum employment, as we discussed in this blog post.

As we noted in the post, as of December, some labor market indicators—notably, the unemployment rate and the job vacancy rate—appeared to show that the labor market’s recovery from the effects of the pandemic was largely complete. But both total employment and employment of prime age workers remained significantly below the levels of early 2020, just before the effects of the pandemic began to be felt on the labor market.

In his press conference, Powell indicated that despite these conflicting labor market indicators: “Most FOMC participants agree that labor market conditions are consistent with maximum employment in the sense of the highest level of employment that is consistent with price stability. And that is my personal view.”

In March 2020, as the target for the federal funds rate reached the zero lower bound, the Fed turned to quantitative easing (QE), just as it had in November 2008 during the Great Financial Crisis. To carry out its policy of QE, the Fed purchased large quantities of long-term Treasury securities with maturities of 4 to 30 years and mortgage backed securities guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae—so-called agency MBS. As a result of these purchases, the Fed’s asset holdings (often referred to as its balance sheet) soared to nearly $9 trillion.

In addition to raising its target for the federal funds rate, the Fed intends to gradually shrink the size of this asset holdings. Some economists refer to this process as quantitative tightening (QT). Following its January meeting, the FOMC issued a statement on “Principles for Reducing the Size of the Federal Reserve’s Balance Sheet.” The statement indicated that increases in the federal funds rate, not QT, would be the focus of its shift to a less expansionary monetary policy: “The Committee views changes in the target range for the federal funds rate as its primary means of adjusting the stance of monetary policy.” The statement also indicated that as the process of QT continued the Fed would eventually hold primarily Treasury securities, which means that the Fed would eventually stop holding agency MBS. Some economists have speculated that the Fed’s exiting the market for agency MBS might have a significant effect on that market, potentially causing mortgage interest rates to increase.

Finally, Powell indicated that the FOMC would likely raise its target for the federal funds more rapidly than it had during the 2015 to 2018 period. Financial market are expecting three or four 0.25 percent increases during 2022, but Powell would not rule out the possibility that the target could be raised during each remaining meeting of the year—which would result in seven increases. The FOMC’s long-run target for the federal funds rate—sometime referred to as the neutral rate—is 2.5 percent. With the target for the federal funds rate currently near zero, four rate increases during 2022 would still leave the target well short of the neutral rate.

Sources: The statements issued by the FOMC at the close of the meeting can be found here; Christopher Rugaber, “Fed Plans to Raise Rates Starting in March to Cool Inflation,” apnews.com, January 26, 2022; Nick Timiraos, “Fed Interest-Rate Decision Tees Up March Increase,” Wall Street Journal, January 26, 2022; Olivia Rockeman and Craig Torres, “Powell Back March Liftoff, Won’t Rule Out Hike Every Meeting,” bloomberg.com, January 26, 2022; and Olivia Rockeman and Reade Pickett, “Powell Says U.S. Labor Market Consistent with Maximum Employment,” bloomberg.com, January 26, 2022.

According to the Federal Reserve Act, the Fed must conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” Neither “maximum employment” nor “stable prices” are defined in the act.

The Fed has interpreted “stable prices” to mean a low rate of inflation. Since 2012, the Fed has had an explicit inflation target of 2 percent. When the Fed announced its new monetary policy strategy in August 2020, it modified its inflation target by stating that it would attempt to achieve an average inflation rate of 2 percent over time. As Fed Chair Jerome Powell stated: “Our approach can be described as a flexible form of average inflation targeting.” (Note that although the consumer price index (CPI) is the focus of many media stories on inflation, the Fed’s preferred measure of inflation is changes in the core personal consumption expenditures (PCE) price index. The PCE is a broader measure of the price level than is the CPI because it includes the prices of all the goods and services included in consumption category of GDP. “Core” means that the index excludes food and energy prices. For a further discussion see, Economics, Chapter 25, Section 15.5 and Macroeconomics, Chapter 15, Section 15.5.)

There is more ambiguity about how to determine whether the economy is at maximum employment. For many years, a majority of members of the Federal Open Market Committee (FOMC) focused on the natural rate of unemployment (also called the non-accelerating rate of unemployment (NAIRU)) as the best gauge of when the U.S. economy had attained maximum employment. The lesson many economists and policymakers had taken from the experience of the Great Inflation that lasted from the late 1960s to the early 1980s was if the unemployment rate was persistently below the natural rate of unemployment, inflation would begin to accelerate. Because monetary policy affects the economy with a lag, many policymakers believed it was important for the Fed to react before inflation begins to significantly increase and a higher inflation rate becomes embedded in the economy.

At least until the end of 2018, speeches and other statements by some members of the FOMC indicated that they continued to believe that the Fed should pay close attention to the relationship between the natural rate of unemployment and the actual rate of unemployment. But by that time some members of the FOMC had concluded that their decision to begin raising the target for the federal funds rate in December 2015 and continuing raising it through December 2018 may have been a mistake because their forecasts of the natural rate of unemployment may have been too high. For instance, Atlanta Fed President Raphael Bostic noted in a speech that: “If estimates of the NAIRU are actually too conservative, as many would argue they have been … unemployment could have averaged one to two percentage points lower” than it actually did.

Accordingly, when the Fed announced its new monetary policy strategy in August 2020, it indicated that it would consider a wider range of data—such as the employment-population ratio—when determining whether the labor market had reached maximum employment. At the time, Fed Chair Powell noted that: “the maximum level of employment is not directly measurable and [it] changes over time for reasons unrelated to monetary policy. The significant shifts in estimates of the natural rate of unemployment over the past decade reinforce this point.”

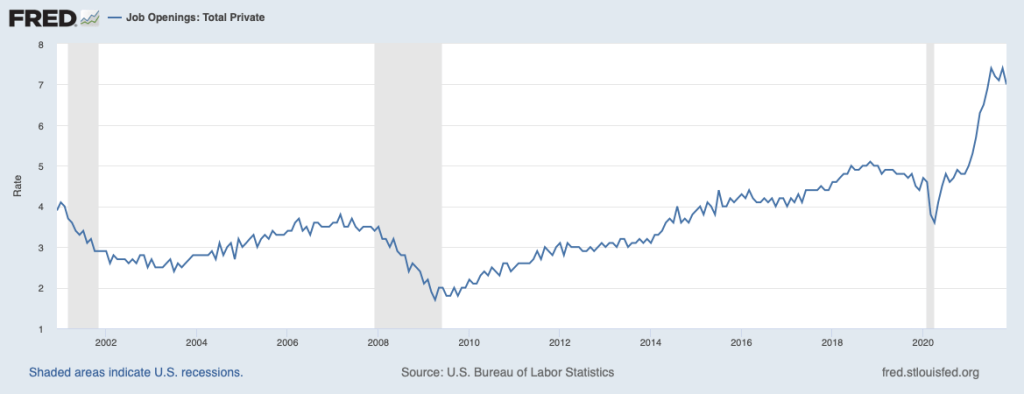

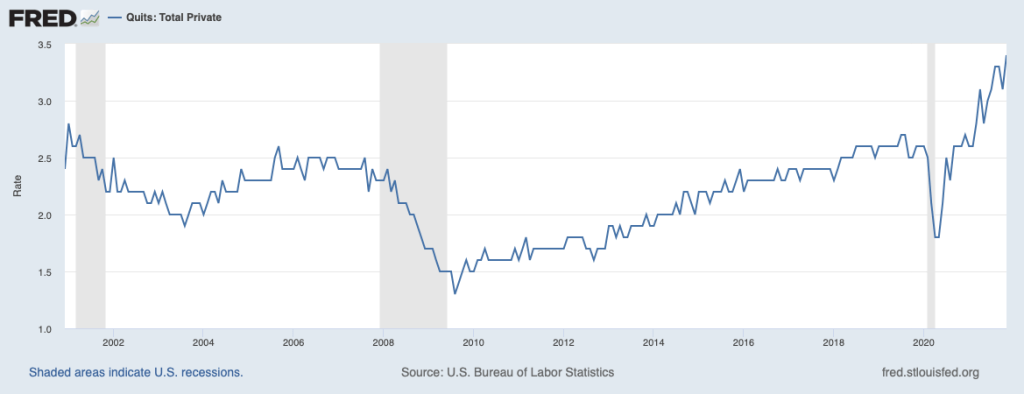

As the economy recovered from the effects of the Covid-19 pandemic, the Fed faced particular difficulty in assessing the state of the labor market. Some labor market indicators appeared to show that the economy was close to maximum employment while other indicators showed that the labor market recovery was not complete. For instance, in December 2021, the unemployment rate was 3.9 percent, slightly below the average of the FOMC members estimates of the natural rate of unemployment, which was 4.0 percent. Similarly, as the first figure below shows, job vacancy rates were very high at the end of 2021. (The BLS calculates job vacancy rates, also called job opening rates, by dividing the number of unfilled job openings by the sum of total employment plus job openings.) As the second figure below shows, job quit rates were also unusually high, indicating that workers saw the job market as being tight enough that if they quit their current job they could find easily another job. (The BLS calculates job quit rates by dividing the number of people quitting jobs by total employment.) By those measures, the labor market seemed close to maximum employment.

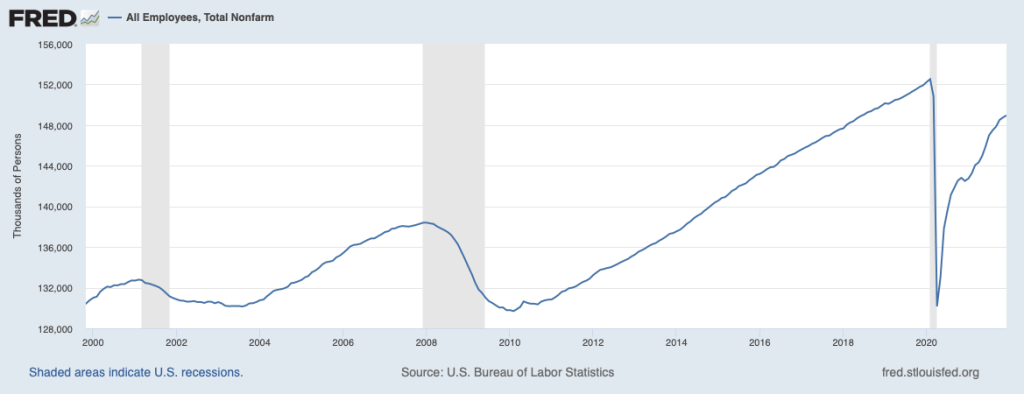

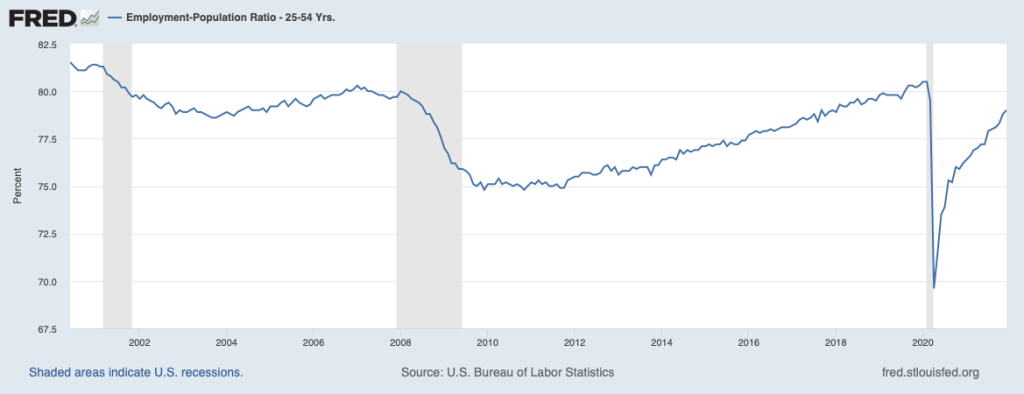

But as the first figure below shows, total employment in December 2021 was still 3.5 million below its level of early 2020, just before the U.S. economy began to experience the effects of the pandemic. Some of the decline in employment can be accounted for by older workers retiring, but as the second figure below indicates, employment of prime-age workers (those between the ages of 25 and 54), had not recovered to pre-pandemic levels.

How to reconcile these conflicting labor market indicators? In January 2022, Fed Chair Powell testified before the Senate Banking Committee as the Senate considered his nomination for a second four-year term as chair. In discussing the state of the economy he offered the opinion that: “We’re very rapidly approaching or at maximum employment.” He noted that inflation as measured by changes in the CPI had been running above 5 percent since June 2021: “If these high levels of inflation get entrenched in our economy, and in people’s thinking, then inevitably that will lead to much tighter monetary policy from us, and it could lead to a recession.” In that sense, “high inflation is a severe threat to the achievement of maximum employment.”

At the time of Powell’s testimony, the FOMC had already announced that it was moving to a less expansionary monetary policy by reducing its purchases of Treasury bonds and mortgage-backed securities and by increasing its target for the federal funds rate in the near future. He argued that these actions would help the Fed achieve its dual mandate by reducing the inflation rate, thereby heading off the need for larger increases in the federal funds rate that might trigger a recession. Avoiding a recession would help achieve the goal of maximum employment.

Powell’s remarks did not make explicit which labor market indicators the Fed would focus on in determining whether the goal of maximum employment had been obtained. It did make clear that the Fed’s new policy of average inflation targeting did not mean that the Fed would accept inflation rates as high as those of the second half of 2021 without raising its target for the federal funds rate. In that sense, the Fed’s monetary policy of 2022 seemed consistent with its decades-long commitment to heading off increases in inflation before they lead to a significant increase in the inflation rate expected by households, businesses, and investors.

Note: For a discussion of the background to Fed policy, see Economics, Chapter 25, Section 25.5 and Chapter 27, Section 17.4, and Macroeconomics, Chapter 15, Section 15.5 and Chapter 17, Section 17.4.

Sources: Jeanna Smialek, “Jerome Powell Says the Fed is Prepared to Raise Rates to Tame Inflation,” New York Times, January 11, 2022; Nick Timiraos, “Fed’s Powell Says Economy No Longer Needs Aggressive Stimulus,” Wall Street Journal, January 11, 2022; and Federal Open Market Committee, “Meeting Calendars, Statements, and Minutes,” federalreserve.gov, January 5, 2022.

Jerome Powell (photo from the Wall Street Journal)

Most economists believe that monetary policy actions, such as changes in the Fed’s pace of buying bonds or in its target for the federal funds rate, affect real GDP and employment only with a lag of several months or longer. But monetary policy actions can have a more immediate effect on the prices of financial assets like stocks and bonds.

Investors in financial markets are forward looking because the prices of financial assets are determined by investors’ expectations of the future. (We discuss this point in Economics and Microeconomics, Chapter 8, Section 8.2, Macroeconomics, Chapter 6, Section 6.2, and Money, Banking and the Financial System, Chapter 6.) For instance, stock prices depend on the future profitability of firms, so if investors come to believe that future economic growth is likely to be slower, thereby reducing firms’ profits, the investors will sell stocks causing stock prices to decline.

Similarly, holders of existing bonds will suffer losses if the interest rates on newly issued bonds are higher than the interest rates on existing bonds. Therefore, if investors come to believe that future interest rates are likely to be higher than they had previously expected them to be, they will sell bonds, thereby causing their prices to decline and the interest rates on them to rise. (Recall that the prices of bonds and the interest rates (or yields) on them move in opposite directions: If the price of a bond falls, the interest rate on the bond will increase; if the price of a bond rises, the interest rate on the bond will decrease. To review this concept, see the Appendix to Economics and Microeconomics Chapter 8, the Appendix to Macroeconomics Chapter 6, and Money, Banking, and the Financial System, Chapter 3.)

Because monetary policy actions can affect future interest rates and future levels of real GDP, investors are alert for any new information that would throw light on the Fed’s intentions. When new information appears, the result can be a rapid change in the prices of financial assets. We saw this outcome on January 5, 2022, when the Fed released the minutes of the Federal Open Market Committee meeting held on December 14 and 15, 2021. At the conclusion of the meeting, the FOMC announced that it would be reducing its purchases of long-term Treasury bonds and mortgage-backed securities. These purchases are intended to aid the expansion of real GDP and employment by keeping long-term interest rates from rising. The FOMC also announced that it intended to increase its target for the federal funds rate when “labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment.”

When the minutes of this FOMC meeting were released at 2 pm on January 5, 2022, many investors realized that the Fed might increase its target for the federal funds rate in March 2022—earlier than most had expected. In this sense, the release of the FOMC minutes represented new information about future Fed policy and the markets quickly reacted. Selling of stocks caused the S&P 500 to decline by nearly 100 points (or about 2 percent) and the Nasdaq to decline by more than 500 points (or more than 3 percent). Similarly, the price of Treasury securities fell and, therefore, their interest rates rose.

Investors had concluded from the FOMC minutes that economic growth was likely to be slower during 2022 and interest rates were likely to be higher than they had previously expected. This change in investors’ expectations was quickly reflected in falling prices of stocks and bonds.

Sources: An Associated Press article on the reaction to the release of the FOMC minutes can be found HERE; the FOMC’s statement following its December 2021 meeting can be found HERE; and the minutes of the FOMC meeting can be found HERE.

When Congress established the Federal Reserve System in 1913, it intended to make the Fed independent of the rest of the federal government. (We discuss this point in the opener to Macroeconomics, Chapter 15 and to Economics, Chapter 25. We discuss the structure of the Federal Reserve System in Macroeconomics, Chapter 14, Section 14.4 and in Economics, Chapter 24, Section 24.4.) The ultimate responsibility for operating the Fed lies with the Board of Governors in Washington, DC. Members of the Board of Governors are nominated by the president and confirmed by the Senate to 14-year nonrenewable terms. Congress intentionally made the terms of Board members longer than the eight years that a president serves (if the president is reelected to a second term).

The president is still able to influence the Board of Governors in two ways:

The terms of members of the Board of Governors are staggered so that one term expires on January 31 of each even-number year. Although this approach means that it’s unlikely that a president will be able to appoint all seven members during the president’s time in office, in practice, many members do not serve their full 14-year terms. So, a president who serves two terms will typically have an opportunity to appoint more than four members of the Board.

The president nominates one member of the Board to serve a renewable four-year term as chair, subject to confirmation by the Senate.

The terms of Fed chairs end in the year after the year a president begins either the president’s first or second term. As a result, presidents are often faced with what is at times a difficult decision as to whether to reappoint a Fed chair who was first appointed by a president of the other party.

For example, after taking office in January 2009, President Barack Obama, a Democrat, faced the decision of whether to nominate Fed Chair Ben Bernanke to a second term to begin in 2010. Bernanke had originally been appointed by President George W. Bush, a Republican. Partly because the economy was still suffering the aftereffects of the financial crisis and the Great Recession, President Obama decided that it would potentially be disruptive to financial markets to replace Bernanke, so he nominated him for a second term.

After taking office in January 2017, President Donald Trump, a Republican, had to decide whether to nominate Fed Chair Janet Yellen, who had been appointed by Obama, to another term that would begin in 2018. He decided not to reappoint Yellen and instead nominated Jerome Powell, who was already serving on the Board of Governors. Although a Republican, Powell had been appointed to the Board in 2014 by Obama.

President Biden’s reasons for nominating Powell to a second term to begin in 2022 were similar to Obama’s reasons for nominating Bernanke to a second term: The U.S. economy was still recovering from the effects of the Covid-19 pandemic, including the strains the pandemic had inflicted on the financial system. He believed that replacing Powell with another nominee would have been potentially disruptive to the financial system.

There had been speculation that Biden would choose Lael Brainard, who has served on the Board of Governors since 2014 following her appointment by Obama, to succeed Powell as Fed chair. Instead, Biden appointed Brainard as vice chair of the Board. In announcing the appointments, Biden stated: “America needs steady, independent, and effective leadership at the Federal Reserve. That’s why I will nominate Jerome Powell for a second term as Chair of the Board of Governors of the Federal Reserve System and Dr. Lael Brainard to serve as Vice Chair of the Board of Governors.”

Sources: Nick Timiraos and Andrew Restuccia, “Biden Will Tap Jerome Powell for New Term as Fed Chairman,” wsj.com, November 22, 2021; and Jeff Cox and Thomas Franck, “Biden Picks Jerome Powell to Lead the Fed for a Second Term as the U.S. Battles Covid and Inflation,” cnbc.com, November 22, 2021.