On Friday, July 8, the Bureau of Labor Statistics (BLS) released its monthly “Employment Situation” report for June 2022. The BLS estimated that nonfarm employment had increased by 372,000 during the month. That number was well above what economic forecasters had expected and seemed inconsistent with other macroeconomic data that showed the U.S. economy slowing. (Note that the increase in employment is from the establishment survey, sometimes called the payroll survey, which we discuss in Macroeconomics, Chapter 9, Section 9.1 and Economics, Chapter 19, Section 19.1.)

Data indicating that the economy was slowing during the first half of 2022 include the Bureau of Economic Analysis’s (BEA) estimate that real GDP had declined by 1.6 percent in the first quarter of 2022. The BEA’s advance estimate—the agency’s first estimate for the quarter—for the change in real GDP during the second quarter of 2022 won’t be released until July 28, but there are indications that real GDP will have declined again during the second quarter. For instance, the Federal Reserve Bank of Atlanta compiles a forecast of real GDP called GDPNow. The GDPNow forecast uses data that are released monthly on 13 components of GDP. This method allows economists at the Atlanta Fed to issue forecasts of real GDP well in advance of the BEA’s estimates. On July 8, the GDPNow forecast was that real GDP in the second quarter of 2022 would decline by 1.2 percent.

Two consecutive quarters of declining real GDP seems inconsistent with employment strongly growing. At a basic level, if firms are producing fewer goods and services—which is what causes a decline in real GDP—we would expect the firms to be reducing, rather than increasing, the number of people they employ. How can we reconcile the seeming contradiction between rising employment and falling output? One possibility is that either the real GDP data or the employment data—or, possibly, both—are inaccurate. Both GDP data and employment data from the establishment survey are subject to potentially substantial future revisions. (Note that because they are constructed from a survey of households, the employment data in the household survey aren’t revised. As we discuss in the text, economists and policymakers typically rely more on the establishment survey than on the household survey in gauging the current state of the labor market.) Substantial revisions are particularly likely for data released during the beginning of a recession.

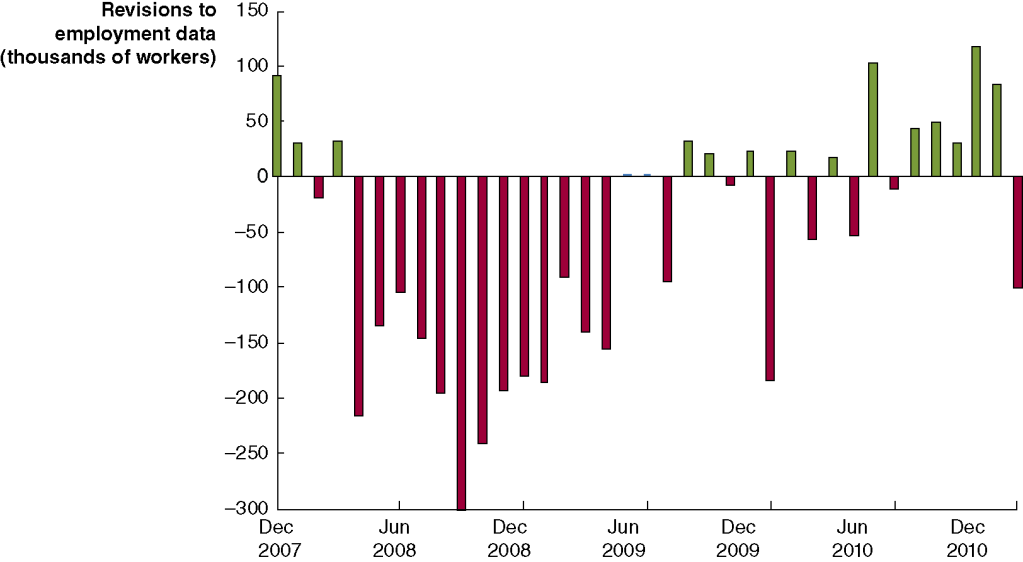

In Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), we give an example of substantial revisions in the employment data. Figure 9.5 (reproduced below) shows that the declines in employment during the 2007–2009 recession were initially greatly underestimated. For example, the BLS initially reported that employment declined by 159,000 during September 2008. But after additional data became available, the BLS revised its estimate to a much larger decline of 460,000.

Similarly, in Macroeconomics, Chapter 15, Section 15,3, in the Apply the Concept “Trying to Hit a Moving Target: Making Policy with ‘Real-Time Data’,” we show the BEA’s estimates of the change in real GDP during the first quarter of 2008 have been revised substantially over time. The BEA’s advance estimate of the change in real GDP during the first quarter of 2008 was an increase of 0.6 percent at an annual rate. But that estimate of real GDP growth has been revised a number of times over the years, mostly downward. Currently, BEA data indicate that real GDP actually declined by 1.6 percent at an annual rate during the first quarter of 2008. This swing of more than 2 percentage points from the advance estimate is a large difference, which changes the picture of what happened during the first quarter of 2008 from one of an economy experiencing slow growth to one of an economy suffering a sharp downturn as it fell into the worst recession since the Great Depression of the 1930s.

The changes to the estimates of both employment and real GDP during the beginning of the 2007–2009 recession are not surprising. The initial estimates of employment and real GDP rely on incomplete data. The estimates are revised as additional data are collected by government agencies. During the beginning of a recession, these additional data are likely to show lower levels of employment and output than were indicated by the initial estimates. If the U.S. economy is in a recession in the second quarter of 2022, we can expect that the BLS and BEA will revise their initial estimates of employment and real GDP downward, which—depending on the relative magnitudes of the revisions to the two series—may resolve the paradox of rising employment and falling output.

Or it’s possible that the U.S. economy is not in a recession. In that case, the employment data may be correct in showing an increase in the number of people working, and the real GDP data may be revised upward to show that output has actually been expanding during the first six months of 2022. Economists and policymakers will have to wait to see which of these alternatives turns out to be the case.