Supports:Microeconomics and Economics, Chapter 15, Section 15.5, and Essentials of Economics, Chapter 10, Section 10.5

Image generated by ChatGTP 03

According to a recent article in the Economist, some U.S. airlines have “started charging higher per-person fares for single-passenger bookings than for identical itineraries with two people.” However, the difference in fares held only for round-trip tickets that included a weekday return flight. For round-trip tickets with a return flight on Saturday, the per-ticket price was the same whether booking for two people or for one person. Briefly explain why an airline might expect to increase its profit using this pricing strategy.

Step 1: Review the chapter material. This problem is about firms using price discrimination, so you may want to review Chapter 15, Sections 15.5

Step 2: Answer the question by explaining why an airline might expect to increase its profit by charging people traveling alone a higher ticket price than the price it charges per ticket to two people traveling together. The airline is attempting to increase its profit by using price discrimination. Price discrimination involves charging different prices to different customers for the same good or service when the price difference isn’t due to differences in cost. Firms who able to price discriminate increase their profits by doing so.

In Chapter 15, Section 15.5, we call the airlines the “kings of price discrimination” because they often charge many different prices for tickets on the same flight. One key way that airlines practice price discrimination is by charging higher prices to business travelers—who are likely to have a lower price elasticity of demand—than to leisure travelers—who are likely to have a higher price elasticity of demand. To employ this strategy, airlines have to successfully identify which flyers are business travelers. Someone flying alone is more likely than someone flying in a group of two or more people to be a business traveler. In addition, business travelers often attempt to complete their trips before the weekend. Therefore, people returning from a trip on a Saturday or Sunday are more likely to be leisure travelers.

We can conclude that an airline can expect to increase its profit using the pricing strategy discussed in the Economist article because the strategy helps the airline to better identify business travelers.

Wendy’s management intends to begin using dynamic pricings in its fast-food restaurants. As we discuss in Microeconomics and Economics, Chapter 15, Section 15.5 (Essentials of Economics, Chapter 10, Section 10.5), dynamic pricing is a form of price discrimination, which is the business practice of charging different prices to different customers for the same good or service. The ability of firms to analyze customer data using machine learning models has increased the ability to price discriminate.

One form of price discrimination involves charging customers different prices at different times, as, for instance, when movie theaters charge a lower price during afternoon showings than during evening showings. As a group, people who can choose whether to attend either an afternoon or an evening showing are more sensitive to changes in the price of a ticket—that is, their demand for tickets is more price elastic—than are people who can only attend an evening showing. Price discrimination with respect to movie tickets results in movie theaters earning a greater profit than if they charged the same price for all showings.

In a conference call with investors in February, Wendy’s CEO Kirk Tanner indicated that next year the firm would begin using dynamic pricing of its hamburgers and other menu items by charging different prices at different times of the day. Tanner didn’t provide details on how prices would differ in high demand times, such as during lunch and dinner, and low demand times, such as the middle of the afternoon. Some business commentators, though, assumed that Wendy’s dynamic pricing strategy would resemble Uber’s surge pricing strategy. As we discuss in Microeconomics, Economics, and Essentials of Economics, Chapter 4, Section 4.1, Uber increases prices during periods of high demand, such as on New Year’s Eve.

The idea that Wendy’s would increase prices at peak times sparked a strong reaction on social media with many people criticizing the firm for “price gouging.” Rival fast-food restaurants joined the criticism. Burger King posted on X (formerly Twitter) that “we don’t believe in charging people more when they’re hungry.” As we note in Microeconomics and Economics, Chapter 10, Section 10.3 (Essentials of Econmics, Chapter 7, Section 7.3), surveys indicate that many people believe that it is fair for firms to raise prices following an increase in the firms’ costs, but unfair to raise prices following an increase in demand.

One way for firms to avoid this reaction from consumers while still price discriminating is to frame the issue by stating that they charge regular prices during times of peak demand and discount prices during times of low demand. For example, recently one AMC theater was charging $13.99 for a 7:15 PM showing of Dune: Part Two, but a “Matinee Discount Price” of $10.39 for a 1:oo PM showing of the film. Note that there is no real economic difference between AMC calling the evening price the normal price and the afternoon price the discoung price and the firm calling the afternoon price the normal price and the evening price a “surge price.” But one of the lessons of behavioral economics is that firms should pay attention to how consumers intepret a policy. Many consumers clearly see the two pricing strategies as different even though economically they aren’t. (We discuss behavioral economics in Microeconomics and Economics, Chapter 10, Section 10.4, and in Essentials of Economics, Chapter 7, Section 7.4.)

Not surprisingly, following the adverse reaction to its annoucement that it would begin using dynamic pricing, Wendy’s responded with a blog post in which it stated that its new pricing strategy was “misconstrued in some media reports as an intent to raise prices when demand is highest at our restaurants. We have no plans to do that and would not raise prices when our customers are visiting us most.” And that: “Digital menuboards could allow us to change the menu offerings at different times of day and offer discounts and value offers to our customers more easily, particularly in the slower times of day.” In effect, Wendy’s was framing its pricing strategy the way movie theaters do rather than the way Uber does.

Wendy’s CEO probably realizes now that how a pricing strategy is presented to consumers can affect how successful the strategy will be.

The Magic Kingdom in Walt Disney World in Florida. Photo by the AP via the Wall Street Journal.

Elasticity is near the top of the list of topics that students struggle with in the principles course. Some students struggle with the arithmetic of calculating elasticities, while others have difficulty understanding the basic concept. The importance and difficulty of elasticity led us to devote an entire chapter to it: Chapter 6 in both Microeconomics and Economics. (We include a briefer discussion in Chapter 7, Sections 7.5 and 7.6 in Essentials of Economics.)

When the Walt Disney Company released its 2023 second quarter earnings report on May 10, it turned out that Disney CEO Bob Iger is also a little shaky on the concept of price elasticity. During Iger’s previous time as Disney CEO he had started the Disney+ subscription streaming service. Like some other streaming services during the past year, Disney+ has struggled to earn a profit. Disney’s announcement in November 2022 that Disney+ had lost $1.47 billion during the previous quarter contributed to Bob Chapek, Iger’s predecessor as CEO, being fired by Disney’s board of directors.

For this quarter, Iger was able to announce that losses at Disney+ had been reduced to $659 million, although skepticism among investors about whether the service would turn a profit by next year as Iger indicated contributed to a sharp decline in Disney’s stock price. The smaller loss at Disney+ was largely the result of Disney having raised the price of the service in December 2022 from $7.99 per month to $10.99 per month. According to an article in the Wall Street Journal, Iger noted that the price increase had caused only a very small decline in subscribers. Iger was quoted as concluding: “That leads us to believe that we, in fact, have pricing elasticity” with respect to Disney+.

Taken literally, Iger has the concept of elasticity backwards. If “having pricing elasticity” means having price elastic demand, then Disney would have experienced a large loss of Disney+ subscribers after the price increase, not a small loss. To use the concept correctly, Iger should have said something like “we have price inelastic demand.” If we give Iger the benefit of the doubt and assume that he knows the definitions of price elastic and price inelastic, then we can interpret what he said as meaning “we have favorable price elasticity.” Favorable in this case would mean demand is price inelastic.

In any case, this episode is a good example of why many students–and CEOs!–can struggle with the concept of price elasticity.

Supports: Microeconomics, Chapter 6, Section 6.3 and Chapter 10, Section 10.3, Economics Chapter 6, Section 6.3 and Chapter 10, Section 10.3, and Essentials of Economics, Chapter 7, Section 7.4 and Section 7.7.

In August 2022, an article in the Wall Street Journal discussed the Disney Company increasing the prices it charges for admission to its Disneyland and Walt Disney World theme parks. As a result of the price increases, “For the quarter that ended July 2 [2022], the business unit that includes the theme parks … posted record revenue of $5.42 billion and record operating income of $1.65 billion.” The increase in revenue occurred even though “attendance at Disney’s U.S. parks fell by 17% compared with the previous year….”

The article also contains the following observations about Disney’s ticket price increases:

“Disney’s theme-park pricing is determined by ‘pure supply and demand,’ said a company spokeswoman.”

“[T]he changes driving the increases in revenue and profit have drawn the ire of what Disney calls ‘legacy fans,’ or longtime parks loyalists.”

Briefly explain what must be true of the demand for tickets to Disney’s theme parks if its revenue from ticket sales increased even though 17 percent fewer tickets were sold. [For the sake of simplicity, ignore any other sources of revenue Disney earns from its theme parks apart from ticket sales.]

In Chapter 10, Section 10.3 the textbook discusses social influences on decision making, in particular, the business implications of fairness. Briefly discuss whether the analysis in that section is relevant as Disney determines the prices for tickets to its theme parks.

Solving the Problem

Step 1: Review the chapter material. This problem is about the effects of price increases on firms’ revenues and on whether firms should pay attention the possibility that consumers might be concerned about fairness when making their consumption decisions, so you may want to review Chapter 6, Section 6.3, “The Relationship between Price Elasticity of Demand and Total Revenue” and Chapter 10, Section 10.3, “Social Influences on Decision Making,” particularly the topic “Business Implications of Fairness.”

Step 2: Answer part a. by explaining what must be true of the demand for tickets to Disney’s theme parks if revenue from ticket sales increased even though Disney sold fewer tickets. Assuming that the demand curve for tickets to Disney’s theme parks is unchanged, a decline in the quantity of tickets sold will result in a move up along the demand curve for tickets, raising the price of tickets. Only if the demand curve for theme park tickets is price inelastic will the revenue Disney receives from ticket sales increase when the price of tickets increases. Revenue increases in this situation because with an inelastic demand curve, the percentage increase in price is greater than the percentage decrease in quantity demanded.

Step 3: Answer part b. by explaining whether the textbook’s discussion of the business implications of fairness is relevant as Disney as determines ticket prices. Section 10.3 may be relevant to Disney’s decisions because the section discusses that firms sometimes take consumer perceptions of fairness into account when deciding what prices to charge. Note that ordinarily economists assume that the utility consumers receive from a good or service depends only on the attributes of the good or service and is not affected by the price of the good or service. Of course, in making decisions on which goods and services to buy with their available income, consumers take price into account. But consumers take price into account by comparing the marginal utilities of products realtive to their prices, with the marginal utilities assumed not to be affected by the prices.

In other words, a consumer considering buying a ticket to Disney World will compare the marginal utility of visiting Disney World relative to the price of the ticket to the marginal utility of other goods and services relative to their prices. The consumer’s marginal utility from spending a day in Disney World will not be affected by whether he or she considers the price of the ticket to be unfairly high.

The textbook gives examples, though, of cases where a business may fail to charge the price that would maximize short-run profit because the business believes consumers would see the price as unfair, which might cause them to be unwilling to buy the product in the future. For instance, restaurants frequently don’t increase their prices during a particularly busy night, even though doing so would increase the profit they earn on that night. They are afraid that if they do so, some customers will consider the restaurants to have acted unfairly and will stop eating in the restaurants. Similarly, the National Football League doesn’t charge a price that would cause the quantity of Super Bowl tickets demanded to be equal to the fixed supply of seats available at the game because it believes that football fans would consider it unfair to do so.

The Wall Street Journal article quotes a Disney spokeswomen as saying that the company sets the price of tickets according to demand and supply. That statement seems to indicate that Disney is charging the price that will maximize the short-run profit the company earns from selling theme park tickets. But the article also indicates that many of Disney’s long-time ticket buyers are apparently upset at the higher prices Disney has been charging. If these buyers consider Disney’s prices to be unfair, they may in the future stop buying tickets.

In other words, it’s possible that Disney might find itself in a situation in which it has increased its profit in the short run at the expense of its profit in the long run. The managers at Disney might consider sacrificing some profit in the long run to increase profit in the short run an acceptable trade-off, particularly because it’s difficult for the company to know whether in fact many of its customers will in the future stop buying admission tickets because they believe current ticket prices to be unfairly high.

Sources: Robbie Whelan and Jacob Passy, “Disney’s New Pricing Magic: More Profit From Fewer Park Visitors,” Wall Street Journal, August 27, 2022.

Production line for Ford F-series trucks. Photo from the Wall Street Journal.

Supports: Microeconomics, Chapter 6, Section 6.3 and Chapter 15, Section 15.6,Economics Chapter 6, Section 6.3 and Chapter 15, Section 15.6, and Essentials of Economics, Chapter 7, Section 7.7 and Chapter 10, Section 10.5.

In July 2022, an article in the Wall Street Journal noted that “The chip shortage and broader supply constraints have hampered vehicle production … Many major car companies on Friday reported U.S. sales declines of 15% or more for the first half of the year.” But the Wall Street Journal also reported that car makers were experiencing increases in revenues. For example, Ford Motor Company reported an increase in revenue even though it had sold fewer cars than during the same period in 2021.

Briefly explain what must be true of the demand for new cars if car makers can sell 15 percent fewer cars while increasing their revenue.

Eventually, the chip shortage and other supply problems facing car makers will end. At that point, would we expect that car makers will expand production to prepandemic levels or will they continue to produce fewer cars in order to maintain higher levels of profits? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the effects of price increases on firms’ revenues and on the ability of firms to restrict output in order increase profits, so you may want to review Chapter 6, Section 6.3, “The Relationship between Price Elasticity of Demand and Total Revenue” and Chapter 15, Section 15.6, “Government Policy toward Monopoly.”

Step 2: Answer part a. by explaining what must be true of the demand for new cars if car makers are increasing their profits while selling fewer cars. Assuming that the demand curve for cars is unchanged, a decline in the quantity of cars sold will result in a move up along the demand curve for cars, raising the price of cars. Only if the demand curve for new cars is price inelastic will the revenue car markers receive increase when the price increases. Revenue increases in this situation because with an inelastic demand curve, the percentage increase in price is greater than the percentage decrease in quantity demanded.

Step 3: Answer part b. by explaining whether we should expect that once the car industry’s supply problems are resolved, car makers will continue to produce fewer cars. Although as a group car makers would be better off if they could continue to reduce the supply of cars, they are unlikely to be able to do so. Any one car maker that decided to keep producing fewer cars would lose sales to other car makers who increased their production to prepandemic levels. Because this increased production would result in a movement down along the demand curve for new cars, the price would fall. So a car maker that reduced output would receive a lower price on its reduced output, causing its profit to decline. (Note that this situation is effectively a prisoner’s dilemma as discussed in Chapter 14, Section 14.2.)

The firms could attempt to keep output of new cars at a low level by explicitly agreeing to do so. But colluding in this way would violate the antitrust laws, and executives at the firms would risk being fined or even imprisoned. The firms could attempt to implicitly collude by producing lower levels of output without explicitly agreeing to do so. (We discus implicit collusion in Chapter 14, Section 14.2.) But implicit collusion is unlikely to succeed because firms have an incentive to break an implicit agreement by increasing output.

We can conclude that once the chip and other supply problems facing car makers are resolved, production of cars is likely to increase.

Sources: Mike Colias and Nora Eckert, “GM Says Unfinished Cars to Hurt Quarterly Results,” Wall Street Journal, July 1, 2022; and Nora Eckert, “Ford’s U.S. Sales Increase 32% in June, Outpacing Broader Industry,” Wall Street Journal, July 5, 2022.

Photo of Russian oil refinery from the New York Times.

On March 8, 2022, President Joe Biden announced that the United States would no longer allow new shipments of oil from Russia to the United States. Russian oil made up about 8 percent of total U.S. oil imports and about 2 percent of U.S. oil consumption. European countries, which are much more heavily dependent on oil imports from Russia, announced plans to gradually reduce Russian oil imports.

The point of these policy actions was to reduce the revenues Russia would receive from oil exports as retaliation for Russia’s invasion of Ukraine. Beyond the effect of direct action against Russian oil imports, Russian oil exports were reduced further as a result of other sanctions imposed on the Russian economy by the United States and other countries. These sanctions made it difficult for Russia to access shipping services and the international payments system.

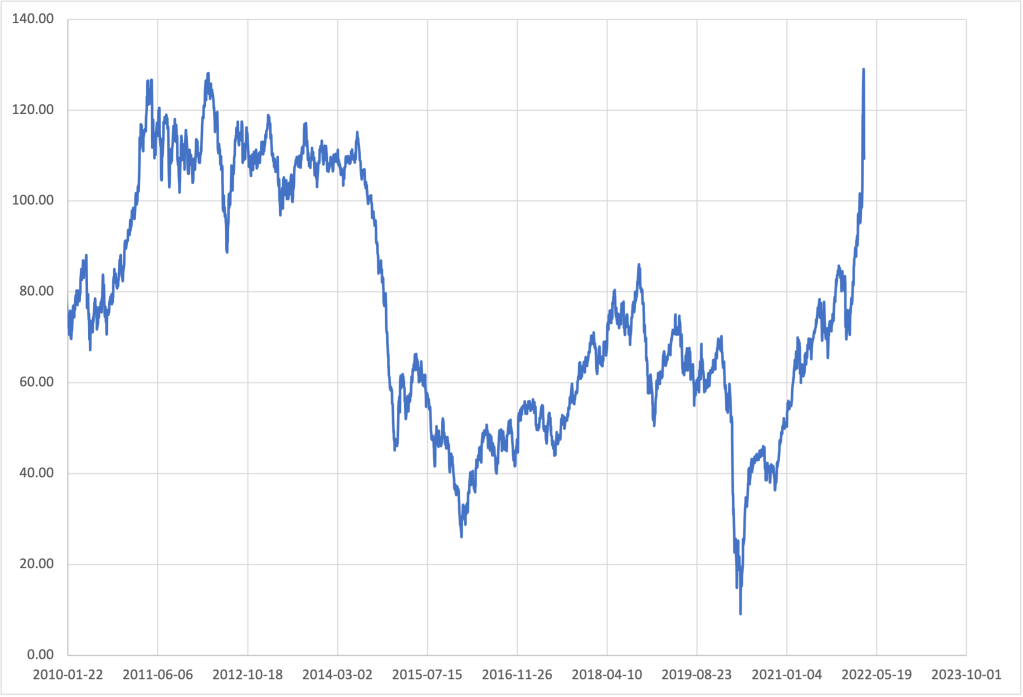

The decline in Russian oil exports reduced the total supply of oil on the international oil market, pushing up the price of the oil. The following figure shows the daily price in dollars per barrel of Brent crude oil, which is the most commonly used benchmark price of oil.

Will the actions taken by the United States and other countries reduce Russian oil revenues? As we discuss in Microeconomics, Chapter 6, Section 6.3, whether a seller’s total revenue will decrease as a result of a decrease in the quantity sold depends on the price elasticity of demand for the seller’s product. If demand is price elastic, the revenue the seller receives will fall. If demand is price inelastic, the revenue the seller receives will rise.

In this case, Russia’s oil revenue will decline if the percentage increase in the price of oil is less than the percentage decrease in the quantity of oil Russia is selling. The energy information firm Energy Intelligence has estimated that Russian oil exports have declined by about one-third. On the day before the Russian invasion of Ukraine, the price of Brent crude oil was about $99 per barrel. It then rose to $129 per barrel on March 7 before falling to $109 per barrel on March 10. Based on these values, the price Russia received per barrel of oil increased between 9 and 29 percent or by less than the 33 percent decline in the quantity of oil Russia sold.

Because the percentage decline in quantity was greater than the percentage increase in price, we can conclude that the actions taken by the United States and other countries reduced Russian oil revenue. In fact, the reduction in revenue is probably larger than indicated by the change in the price of Brent crude oil. Media reports indicate that to find buyers Russia is having to discount its oil by more than $10 per barrel from the Brent price. In addition, the countries of the European Union have pledged to reduce Russian oil imports by two-thirds by the end of 2022 and the United Kingdom has pledged to end them entirely. Although Russia might be able to redirect to other countries some oil it had been exporting to Europe and the United States, it seems likely that Russia’s total oil exports will eventually decline by more than the initial one-third.

Sources: Andrew Restuccia and Josh Mitchell, “Biden Bans Imports of Russian Oil, Natural Gas, Wall Street Journal, March 8, 2022; Stanley Reed, “The Future Turns Dark for Russia’s Oil Industry,” New York Times, March 8, 2022; Collin Eaton, “How Much Oil Does the U.S. Import From Russia and Why Is Biden Banning It?” Wall Street Journal, March 9, 2022; “Russian Oil Exports Fall by One-Third,” energyintel.com, March 2, 2022; and Tsuyoshi Inajima and Serene Cheong, “More Russian Oil Deeply Discounted as Ban Risk Alarms Buyers,” bloomberg.com, March 7, 2022. Brent crude oil price data from the Federal Reserve Bank of St. Louis and the Wall Street Journal.