Authors Glenn Hubbard and Tony O’Brien reconsider the role of inflation in today’s economy. They discuss the Fed’s possible responses by considering responses to similar inflation threats in previous generations – notably the Fed’s response led by Paul Volcker that directly led to the early 1980’s recession. The markets are reflecting stark differences in our collective expectations about what will happen next. Listen to find out more about the Fed’s likely next steps.

Category: Money. Banking, and the Financial System

Did the Fed Make a Mistake by Not Preempting Inflation?

Warning: Long post!

It now seems clear that the new monetary policy strategy the Fed announced in August 2020 was a decisive break with the past in one respect: With the new strategy, the Fed abandoned the approach dating to the 1980s of preempting inflation. That is, the Fed would no longer begin raising its target for the federal funds rate when data on unemployment and real GDP growth indicated that inflation was likely to rise. Instead, the Fed would wait until inflation had already risen above its target inflation rate.

Since 2012, the Fed has had an explicit inflation target of 2 percent. As we discussed in a previous blog post, with the new monetary policy the Fed announced in August 2020, the Fed modified how it interpreted its inflation target: “[T]he Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

The Fed’s new approach is sometimes referred to as average inflation targeting (AIT) because the Fed attempts to achieve its 2 percent target on average over a period of time. But as former Fed Vice Chair Richard Clarida discussed in a speech in November 2020, the Fed’s monetary policy strategy might be better called a flexible average inflation target (FAIT) approach rather than a strictly AIT approach. Clarida noted that the framework was asymmetric, meaning that inflation rates higher than 2 percent need not be offset with inflation rates lower than 2 percent: “The new framework is asymmetric. …[T]he goal of monetary policy … is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent.” And: “Our framework aims … for inflation to average 2 percent over time, but it does not make a … commitment to achieve … inflation outcomes that average 2 percent under any and all circumstances ….”

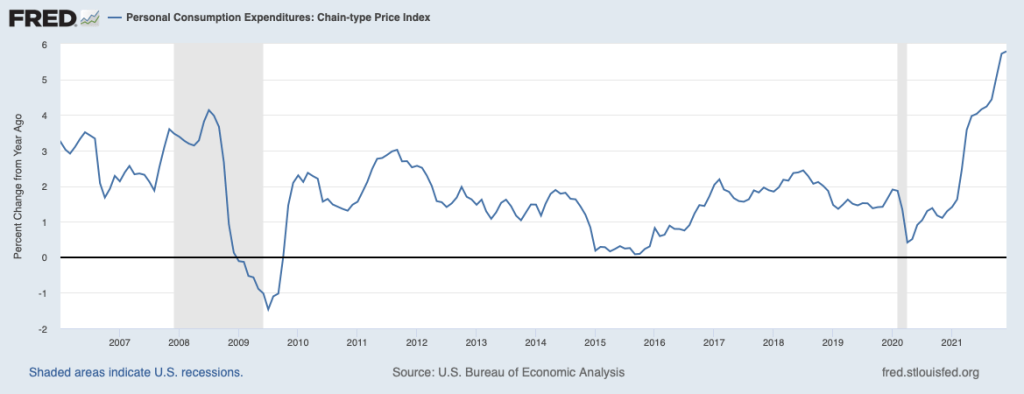

Inflation began to increase rapidly in mid-2021. The following figure shows three measure of inflation, each calculated as the percentage change in the series from the same month in the previous year: the consumer price index (CPI), the personal consumption expenditure (PCE) price index, and the core PCE—which excludes the prices of food and energy. Inflation as measured by the CPI is sometimes called headline inflation because it’s the measure of inflation that most often appears in media stories about the economy. The PCE is a broader measure of the price level in that it includes the prices of more consumer goods and services than does the CPI. The Fed’s target for the inflation rate is stated in terms of the PCE. Because prices of food and inflation fluctuate more than do the prices of other goods and services, members of the Fed’s Federal Open Market Committee (FOMC) generally consider changes in the core PCE to be the best measure of the underlying rate of inflation.

The figure shows that for most of the period from 2002 through early 2021, inflation as measured by the PCE was below the Fed’s 2 percent target. Since that time, inflation has been running well above the Fed’s target. In February 2022, PCE inflation was 6.4 percent. (Core PCE inflation was 5.4 percent and CPI inflation was 7.9 percent.) At its March 2022 meeting the FOMC begin raising its target for the federal funds rate—well after the increase in inflation had begun. The Fed increased its target for the federal funds rate by 0.25 percent, which raised the target from 0 to 0.25 percent to 0.25 to 0.50 percent.

Should the Fed have taken action to reduce inflation earlier? To answer that question, it’s first worth briefly reviewing Fed policy during the Great Inflation of 1968 to 1982. In the late 1960s, total federal spending grew rapidly as a result of the Great Society social programs and the war in Vietnam. At the same time, the Fed increased the rate of growth of the money supply. The result was an end to the price stability of the 1952-1967 period during which the annual inflation rate had averaged only 1.6 percent.

The 1973 and 1979 oil price shocks also contributed to accelerating inflation. Between January 1974 and June 1982, the annual inflation rate averaged 9.3 percent. This was the first episode of sustained inflation outside of wartime in U.S. history—until now. Although the oil price shocks and expansionary fiscal policy contributed to the Great Inflation, most economists, inside and outside of the Fed, eventually concluded that Fed policy failures were primarily responsible for inflation becoming so severe.

The key errors are usually attributed to Arthur Burns, who was Fed Chair from January 1970 to March 1978. Burns, who was 66 at the time of his appointment, had made his reputation for his work on business cycles, mostly conducted prior to World War II at the National Bureau of Economic Research. Burns was skeptical that monetary policy could have much effect on inflation. He was convinced that inflation was mainly the result of structural factors such as the power of unions to push up wages or the pricing power of large firms in concentrated industries.

Accordingly, Burns was reluctant to raise interest rates, believing that doing so hurt the housing industry without reducing inflation. Burns testified to Congress that inflation “poses a problem that traditional monetary and fiscal remedies cannot solve as quickly as the national interest demands.” Instead of fighting inflation with monetary policy he recommended “effective controls over many, but by no means all, wage bargains and prices.” (A collection Burns’s speeches can be found here.)

Few economists shared Burns’s enthusiasm for wage and price controls, believing that controls can’t end inflation, they can only temporarily reduce it while causing distortions in the economy. (A recent overview of the economics of price controls can be found here.) In analyzing this period, economists inside and outside the Fed concluded that to bring the inflation rate down, Burns should have increased the Fed’s target for the federal funds rate until it was higher than the inflation rate. In other words, the real interest rate, which equals the nominal—or stated—interest rate minus the inflation rate, needed to be positive. When the real interest rate is negative, a business may, for example, pay 6% on a bond when the inflation rate is 10%, so they’re borrowing funds at a real rate of −4%. In that situation, we would expect borrowing to increase, which can lead to a boom in spending. The higher spending worsens inflation.

Because Burns and the FOMC responded only slowly to rising inflation, workers, firms, and investors gradually increased their expectations of inflation. Once higher expectation inflation became embedded, or entrenched, in the U.S. economy it was difficult to reduce the actual inflation rate without increasing the target for the federal funds rate enough to cause a significant slowdown in the growth of real GDP and a rise in the unemployment rate. As we discuss in Macroeconomics, Chapter 17, Sections 17.2 and 17.3 (Economics, Chapter 27, Sections 27.2 and 27.3), the process of the expected inflation rate rising over time to equal the actual inflation rate was first described in research conducted separately by Nobel Laureates Milton Friedman and Edmund Phelps during the 1960s.

An implication of Friedman and Phelps’s work is that because a change in monetary policy takes more than a year to have its full effect on the economy, if the Fed waits until inflation has already increased, it will be too late to keep the higher inflation rate from becoming embedded in interest rates and long-term labor and raw material contracts.

Paul Volcker, appointed Fed chair by Jimmy Carter in 1979, showed that, contrary to Burns’s contention, monetary policy could, in fact, deal with inflation. By the time Volcker became chair, inflation was above 11%. By raising the target for the federal funds rate to 22%—it was 7% when Burns left office—Volcker brought the inflation rate down to below 4%, but only at the cost of a severe recession during 1981–1982, during which the unemployment rate rose above 10 percent for the first time since the Great Depression of the 1930s. Note that whereas Burns had largely failed to increase the target for the federal funds as rapidly as inflation had increased—resulting in a negative real federal funds rate—Volcker had raised the target for the federal funds rate above the inflation rate—resulting in a positive real federal funds rate.

Because the 1981–1982 recession was so severe, the inflation rate declined from above 11 percent to below 4 percent. In Chapter 17, Figure 17.10 (reproduced below), we plot the course of the inflation and unemployment rates from 1979 to 1989.

The Fed chairs who followed Volcker accepted the lesson of the 1970s that it was important to head off potential increases in inflation before the increases became embedded in the economy. For instance, in 2015, then Fed Chair Janet Yellen in explaining why the FOMC was likely to raise to soon its target for the federal funds rate noted that: “A substantial body of theory, informed by considerable historical evidence, suggests that inflation will eventually begin to rise as resource utilization continues to tighten. It is largely for this reason that a significant pickup in incoming readings on core inflation will not be a precondition for me to judge that an initial increase in the federal funds rate would be warranted.”

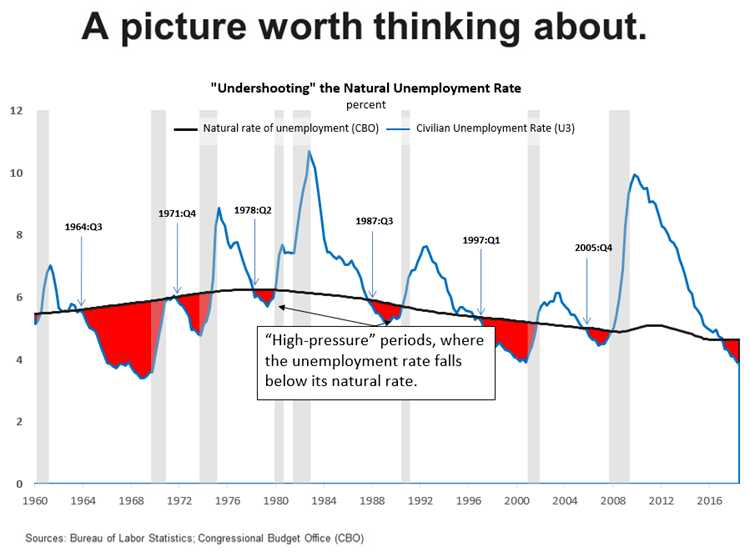

Between 2015 and 2018, the FOMC increased its target for the federal funds rate nine times, raising the target from a range of 0 to 0.25 percent to a range of 2.25 to 2.50 percent. In 2018, Raphael Bostic, president of the Federal Reserve Bank of Atlanta justified these rate increases by noting that “… we shouldn’t forget that [the Fed’s] credibility [with respect to keeping inflation low] was hard won. Inflation expectations are reasonably stable for now, but we know little about how far the scales can tip before it is no longer so.”

He used the following figure to illustrate his point.

Bostic interpreted the figure as follows:

“[The red areas in the figure are] periods of time when the actual unemployment rate fell below what the U.S. Congressional Budget Office now estimates as the so-called natural rate of unemployment. I refer to these episodes as “high-pressure” periods. Here is the punchline. Dating back to 1960, every high-pressure period ended in a recession. And all but one recession was preceded by a high-pressure period….

I think a risk management approach requires that we at least consider the possibility that unemployment rates that are lower than normal for an extended period are symptoms of an overheated economy. One potential consequence of overheating is that inflationary pressures inevitably build up, leading the central bank to take a much more “muscular” stance of policy at the end of these high-pressure periods to combat rising nominal pressures. Economic weakness follows [resulting typically, as indicated in the figure by the gray band, in a recession].”

By July 2019, a majority of the members of the FOMC, including Chair Powell, had come to believe that with no sign of inflation accelerating, they could safely cut the federal funds rate. But they had not yet explicitly abandoned the view that the FOMC should act to preempt increases in inflation. The formal change came in August 2020 when, as discussed earlier, the FOMC announced the new FAIT.

At the time the FOMC adopted its new monetary policy strategy, most members expected that any increase in inflation owing to problems caused by the Covid-19 pandemic—particularly the disruptions in supply chains—would be transitory. Because inflation has proven to be more persistent than Fed policymakers and many economists expected, two aspects of the FAIT approach to monetary policy have been widely discussed: First, the FOMC did not explicitly state by how much inflation can exceed the 2 percent target or for how long it needs to stay there before the Fed will react. The failure to elaborate on this aspect of the policy has made it more difficult for workers, firms, and investors to gauge the Fed’s likely reaction to the acceleration in inflation that began in the spring of 2021. Second, the FOMC’s decision to abandon the decades-long policy of preempting inflation may have made it more difficult to bring inflation down to the 2 percent target without causing a recession.

Federal Reserve Governor Lael Brainard recently remarked that “it is of paramount importance to get inflation down” and some Fed policymakers believe that the FOMC will have to begin increasing its target for the federal funds rate more aggressively. (The speech in which Governor Brainard discusses her current thinking on monetary policy can be found here.) For instance James Bullard, president of the Federal Reserve Bank of St. Louis, has argued in favor of raising the target to above 3 percent this year. With the Fed’s preferred measure of inflation running above 5 percent, it would take substantial increases int the target to achieve a positive real federal funds rate.

It is an open question whether Jerome Powell finds himself in a position similar to that of Paul Volcker in 1979: Rapid increases in interest rates may be necessary to keep inflation from accelerating, but doing so risks causing a recession. In a recent speech (found here), Powell pledged that: “We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

But Powell argued that the FOMC could achieve “a soft landing, with inflation coming down and unemployment holding steady” even if it is forced to rapidly increase its target for the federal funds rate:

“Some have argued that history stacks the odds against achieving a soft landing, and point to the 1994 episode as the only successful soft landing in the postwar period. I believe that the historical record provides some grounds for optimism: Soft, or at least softish, landings have been relatively common in U.S. monetary history. In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession.”

Some economists have been skeptical that a soft landing is likely. Harvard economist and former Treasury Secretary Lawrence Summers has been particularly critical of Fed policy, as in this Twitter thread. Summers concludes that: “I am apprehensive that we will be disappointed in the years ahead by unemployment levels, inflation levels, or both.” (Summers and Harvard economist Alex Domash provide an extended discussion in a National Bureau of Economic Research Working Paper found here.)

Clearly, we are in a period of great macroeconomic uncertainty.

Macro Solved Problems on Treasury Bonds and Defining Inflation

With the owners of the Major Labor Baseball teams and the Major League Players Association having finally settled on a new collective bargaining agreement, the baseball season will soon begin. Ernie Banks, the late Hall of Fame shortstop for the Chicago Cubs, was known for his upbeat personality. However bad the weather might be at Chicago’s Wrigley Field, Banks would run on the field and say, “What a great day for baseball! Let’s play two.”

In honor of Ernie Banks, today let’s do two Solved Problems in macro. They both involve errors that students in principles courses often make. So, in that sense they would also work as Don’t Let This Happen to You features.

Solved Problem 1.: Bond Yields and Bond Prices

An article in the Financial Times had the following headline: “U.S. Government Bond Prices Drop Ahead of Federal Reserve Meeting.” The first sentence of the article reads: “U.S. government bond yields rose to multiyear highs on Monday ahead of this week’s Federal Reserve meeting ….”

a. When a media article mentions “U.S. government bonds,” what type of bonds are they referring to?

b. Is there a contradiction between the headline and the first sentence of the article? Is the article telling us that U.S. government bonds went up or down? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the inverse relationship between bond yields and bond prices, so you may want to review Macroeconomics, Chapter 6, Appendix, “Using Present Value” (Economics, Chapter 8, Appendix, “Using Present Value”). You may also want to review the discussion of U.S. Treasury bonds in Macroeconomics, Chapter 16, Section 16.6, “Deficits, Surpluses, and Federal Government Debt” (Economics, Chapter 26, Section 26.6, “Deficits, Surpluses, and Federal Government Debt”).

Step 2: Answer part a. by explaining what media articles are referring to when they use the phrase “U.S. government bonds.” As discussed in Chapter 16, Section 16.6, most of the bonds issued by the federal government of the United States are U.S. Treasury bonds. The Treasury sells these bonds to investors when the federal government doesn’t collect enough in tax revenues to pay for all of its spending. So, when the media refers to U.S. government bonds, without further explanation, the reference is always to U.S. Treasury bonds.

Step 3: Answer part b. by explaining that there is no contradiction between the headline and the first sentence of the article. An important fact about bond markets is that when the price of a bond falls, the yield—or interest rate—on the bond rises. The reverse is also true: When the price of a bond rises, the yield on the bond falls. The reason why this relationship holds is explained in the Appendix to Chapter 6: The price of a bond (or other financial asset) should be equal to the present value of the payments an investor receives from owning that asset. If you buy a U.S. Treasury bond, the price will equal the present value of the coupon payments the Treasury sends you during the life of the bond and the final payment to you by the Treasury of the principal, or face value of the bond. Remember that present value is the value in today’s dollars of funds to be received in the future. The higher the interest rate, the lower the present value of a payment to be received in the future. So a higher yield, or interest rate, on a bond results in a lower price of the bond because the higher yield reduces the present value of the payments to be received from the bond.

Therefore, whenever the yield on a bond rises, the price of the bond must fall (and whenever the yield on a bond falls, the price of the bond must rise. So, we can conclude that the headline of the Financial Times article and the first sentence of the article are consistent, not contradictory: Because the prices of Treasury bonds fell, the yields on the bonds must have risen.

Source: Nicholas Megaw, Naomi Rovnick, George Steer, and Hudson Lockett, “U.S. Government Bond Prices Drop Ahead of Federal Reserve Meeting,” ft.com, March 14, 2022.

Solved Problem 2: Being Careful about the Definition of Inflation

An article in the New York Times contrasted inflation during the 1970s with inflation today:

“Price increases had run high for more than a decade by the time Mr. Volcker became chair [of the Federal Reserve Board of Governors] in 1979 …. Shopper expected prices to go up, businesses knew that, and both acted accordingly. This time, inflation has been anemic for years (until recently), and most consumers and investors expect costs to return to lower levels before long, survey and market data show.”

a. What does the article mean by “inflation has been anemic for years”?

b. In the last sentence what “costs” is the article referring to?

c. Is the article correctly using the definition of inflation in the last sentence? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the definition of inflation, so you may want to review Macroeconomics, Chapter 9, Section 9.4, “Measuring Inflation” (Economics, Chapter 20, Section 20.4, “Measuring Inflation”).

Step 2: Answer part a. by explaining what the phrase “inflation has been anemic for years” means. Anemia is a medical disorder that usually has the symptom of fatigue. So, the word “anemic” is often used to mean weak. The article is arguing that until recently, the inflation rate had been weak, or slow.

Step 3: Answer part b. by explaining what the article is referring to by “costs.” Economists typically use the word costs for the amount that firm pays to produce a good—labor costs, raw material costs, and so on. Here, though, the article is using “costs” to mean “prices.” Costs is often used this way in everyday conversation: “I didn’t buy a new car because they cost too much.” Or: “Has the cost of a movie ticket increased?”

Step 4: Answer part c. by explaining whether the article is correctly using the definition of inflation. In writing “consumers and investors expect costs to return to lower levels” the article is making a common mistake. The article seems to mean that consumers and investors expect that the rate of inflation will be lower in the future. But even if the rate of inflation declines from nearly 8 percent in early 2022 to, say, 3 percent in 2023, prices will still be increasing. So, prices (“costs” in the sentence) will still be higher next year even if the rate of inflation is lower. In other words, even if the rate of increase in prices—inflation—declines, the price level will still be higher.

It’s a common mistake to think that a decline in the inflation rate means that prices will be lower, when actually prices will still be increasing, just more slowly.

Source: Jeanna Smialek, “Powell Admires Volcker. He May Have to Act Like Him,” New York Times, March 14, 2022.

Solved Problem: U.S. Treasury Bonds and the Russian Invasion of Ukraine

Supports: Macroeconomics, Chapter 10, Section 10.5, Economics Chapter 20, Section 20.5, and Essentials of Economics, Chapter 14, Section 14.2.

On March 2, 2022, as the conflict between Russia and Ukraine intensified, an article in the Wall Street Journal had the headline “Investors Pile Into Treasurys as Growth Concerns Flare.” The article noted that: “The 10-year Treasury yield just recorded its largest two-day decline since March 2020, while two-year Treasury yields plunged the most since 2008.”

a. What does it mean for investors to “pile into” Treasury bonds?

b. Why would investors piling into Treasury bonds cause their yields to fall?

c. What are “growth concerns”? What kind of growth are investors concerned about?

d. Why might growth concerns cause investors to buy Treasury bonds?

Solving the Problem

Step 1: Review the chapter material. This problem is about the effects of slowing economic growth on interest rates, so you may want to review Chapter 10, Section 10.5, “Saving, Investment and the Financial System.” You may also want to review Chapter 6, Appendix A (in Economics, Chapter 8, Appendix A), which explains the inverse relationship between bond prices and interest rates.

Step 2: Answer part a. by explaining what the article meant by the phrase “pile into” Treasury bonds. The article is using a slang phrase that means that investors are buying a lot of Treasury bonds.

Step 3: Answer part b. by explaining why investors piling into Treasury bonds will cause the yields on the bonds to fall. As the Appendix to Chapter 6 explains, the price of a bond represents the present value of the payments that an investor will receive over the life of the bond. Lower interest rates result in a higher present value of the payments received and, therefore, higher bond prices or—which is restating the same point—higher bond prices result in lower interest rates. If investors are increasing their demand for Treasury bonds, the increased demand will cause the prices of the bonds to increase and cause the yields—or the interest rates—on the bonds to fall.

Step 4: Answer part c. by explaining the phrase “growth concerns.” In this context, the growth being discussed is economic growth—changes in real GDP. The headline indicates that investors were concerned that the Russian invasion of Ukraine might lead to slower economic growth in the United States.

Step 5: Answer part d. by explaining why investors might purchase Treasury bonds if they were concerned about economic growth slowing. Using the model of the loanable funds markets discussed in Chapter 10, Section 10.5, we know that if economic growth slows, firms are likely to engage in fewer new investment projects, which would shift the demand curve for loanable funds to the left and result in a lower equilibrium interest rate. Investors who have purchased Treasury bonds will gain from a lower interest rate because the price of the Treasury bonds they own will increase. In addition, stock prices depend on investors’ expectations of the future profitability of firms issuing the stock. Typically, if investors believe that economic growth is likely to be slower in the future than they had previously expected, stock prices will fall, which would make Treasury bonds a more attractive investment. Finally, investors believe there is no chance that the U.S. Treasury will default on its bonds by not making the interest payments on the bonds. During an economic slowdown, investors may come to believe that the default risk on corporate bonds has increased because some corporations may run into financial problems. An increase in the default risk on corporate bonds increases the relative attractiveness of Treasury bonds as an investment.

Source: Gunjan Banerji, “Investors Pile Into Treasurys as Growth Concerns Flare,” Wall Street Journal, March 2, 2022.

3/01/22 Podcast – Authors Glenn Hubbard & Tony O’Brien discuss Russia’s Invasion of Ukraine.

Authors Glenn Hubbard & Tony O’Brien reflect on the global economic effects of Russia’s invasion of Ukraine last week. They consider the impact on the global commodity market, US monetary policy, and the impact on the financial markets in the US. Impact touches Introductory Economics, Money & Banking, International Economics, and Intermediate Macroeconomics as the effects of Russia’s aggression moves into its second week.

A map of Europe with Ukraine in the middle right below Belarus and to the east of Poland.

Should the Federal Reserve Issue a Digital Currency?

The Problem with Bitcoin as Money

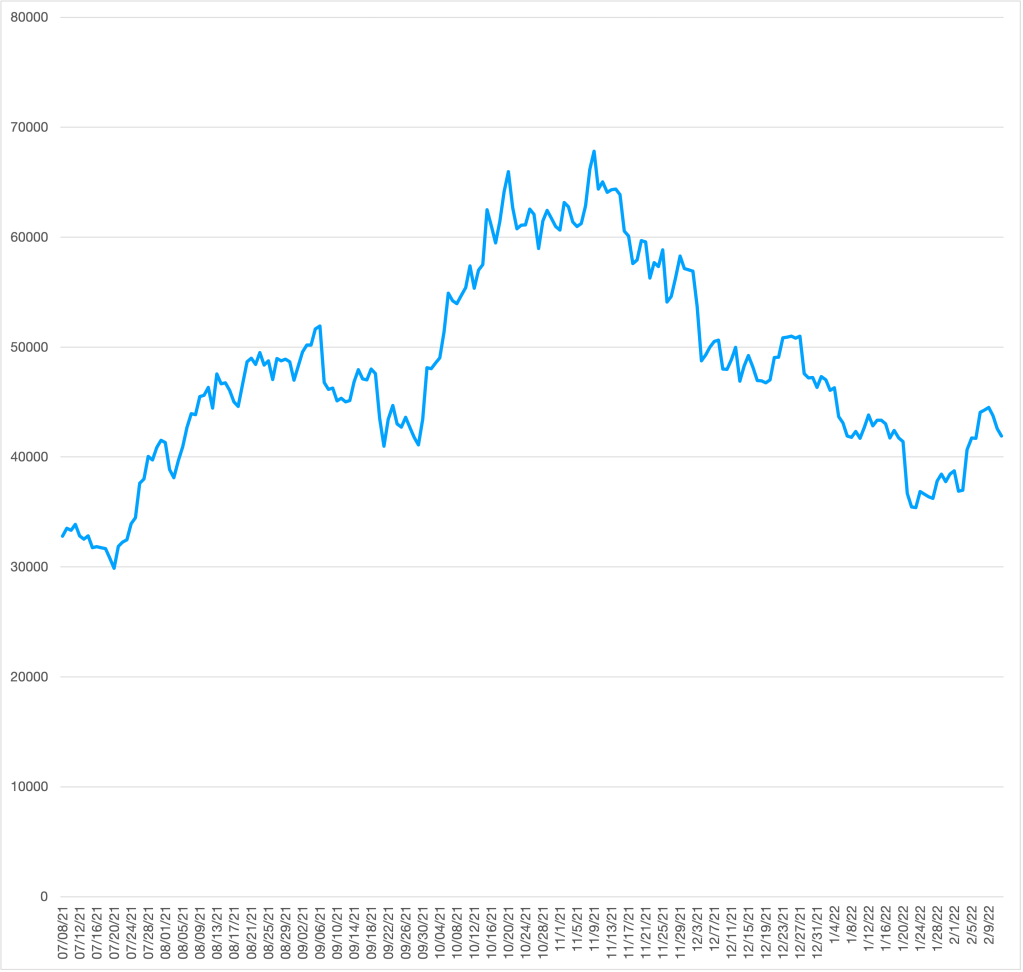

Bitcoin has failed in their original purpose of providing a digital currency that could be used in everyday transactions like buying lunch and paying a cellphone bill. As the following figure shows, swings in the value of bitcoin have been too large to make useful as a medium of exchange like dollar bills. During the period shown in the figure—from July 2021 to February 2022—the price of bitcoin has increased by more than $30,000 per bitcoin and then fallen by about the same amount. Bitcoin has become a speculative asset like gold. (We discuss bitcoin in the Apply the Concept, “Are Bitcoins Money?” which appears in Macroeconomics, Chapter 14, Section 14.2 and in Economics, Chapter 24, Section 24.2. In an earlier blog post found here we discussed how bitcoin has become similar to gold.)

The vertical axis measures the price of bitcoin in dollars per bitcoin.

The Slow U.S. Payments Increases the Appeal of a Digital Currency

Some economists and policymakers argue that there is a need for a digital currency that would do what bitcoin was originally intended to do—serve as a medium of exchange. Digital currencies hold the promise of providing a real-time payments system, which allow payments, such as bank checks, to be made available instantly. The banking systems of other countries, including Japan, China, Mexico, and many European countries, have real-time payment systems in which checks and other payments are cleared and funds made available in a few minutes or less. In contrast, in the United States, it can two days or longer after you deposit a check for the funds to be made available in your account.

The failure of the United States to adopt a real-time payments system has been costly to many lower-income people who are likely to need paychecks and other payments to be quickly available. In practice, many lower-income people: 1) incur bank overdraft fees, when they write checks in excess of the funds available in their accounts, 2) borrow money at high interest rates from payday lenders, or 3) pay a fee to a check cashing store when they need money more quickly than a bank will clear a check. Aaron Klein of the Brookings Institution estimates that lower-income people in the United States spend $34 billion annually as a result of relying on these sources of funds. (We discuss the U.S. payments system in Money, Banking, and the Financial System, 4th edition, Chapter 2, Section 2.3.)

The Problem with Stablecoins as Money

Some entrepreneurs have tried to return to the original idea of using cryptocurrencies as a medium of exchange by introducing stablecoins that can be bought and sold for a constant number of dollars—typically one dollar for one stablecoin. The issuers of stablecoins hold in reserve dollars, or very liquid assets like U.S. Treasury bills, to make credible the claim that holders of stablecoins will be able to exchange them one-for-one for dollars. Tether and Circle Internet Financial are the leading issuers of stablecoins.

So far, stablecoins have been used primarily to buy bitcoin and other cryptocurrencies rather than for day-to-day buying and selling of goods and services in stores or online. Financial regulators, including the U.S. Treasury and the Federal Reserve, are concerned that stablecoins could be a risk to the financial system. These regulators worry that issuers of stablecoins may not, in fact, keep sufficient assets in reserve to redeem them. As a result, stablecoins might be susceptible to runs similar to those that plagued the commercial banking system prior to the establishment of the Federal Deposit Insurance Corporation in the 1930s or that were experienced by some financial firms during the 2008 financial crisis. In a run, issuers of stablecoins might have to sell financial assets, such as Treasury bills, to be able to redeem the stablecoins they have issued. The result could be a sharp decline in the prices of these assets, which would reduce the financial strength of other firms holding the assets.

In 2019, Facebook (whose corporate name is now Meta Platforms) along with several other firms, including PayPal and credit card firm Visa, began preparations to launch a stablecoin named Libra—the name was later changed to Diem. In May 2021, the firms backing Diem announced that Silvergate Bank, a commercial bank in California, would issue the Diem stablecoin. But according to an article in the Wall Street Journal, the Federal Reserve had “concerns about [the stablecoin’s] effect on financial stability and data privacy and worried [it] could be misused by money launderers and terrorist financiers.” In early 2022, Diem sold its intellectual property to Silvergate, which hoped to still issue the stablecoin at some point.

A Federal Reserve Digital Currency?

If private firms or individual commercial banks have not yet been able to issue a digital currency that can be used in regular buying and selling in stores and online, should central banks do so? In January 2022, the Federal Reserve issued a report discussing the issues involved with a central bank digital currency (CBCD). As we discuss in Macroeconomics, Chapter 14, Section 14.2, most of the money supply of the United States consists of bank deposits. As the Fed’s report points out, because bank deposits are computer entries on banks’ balance sheets, most of the money in the United States today is already digital. As we discuss in Section 14.3, bank deposits are liabilities of commercial banks. In contrast, a CBCD would be a liability of the Fed or other central bank.

The Fed report lists the benefits of a CBCD:

“[I]t could provide households and businesses [with] a convenient, electronic form of central bank money, with the safety and liquidity that would entail; give entrepreneurs a platform on which to create new financial products and services; support faster and cheaper payments (including cross-border payments); and expand consumer access to the financial system.”

Importantly, the Fed indicates that it won’t begin issuing a CBCD without the backing of the president and Congress: “The Federal Reserve does not intend to proceed with issuance of a CBDC without clear support from the executive branch and from Congress, ideally in the form of a specific authorizing law.”

The Fed report acknowledges that “a significant number of Americans currently lack access to digital banking and payment services. Additionally, some payments—especially cross-border payments—remain slow and costly.” By issuing a CBDC, the Fed could help to reduce these problems by making digital banking services available to nearly everyone, including lower-income people who currently lack bank checking accounts, and by allowing consumers to have payments instantly available rather than having to wait for a check to clear.

The report notes that: “A CBDC would be the safest digital asset available to the general public, with no associated credit or liquidity risk.” Credit risk is the risk that the value of the currency might decline. Because the Fed would be willing to redeem a dollar of CBDC currency for a dollar or paper money, a CBDC has no credit risk. Liquidity risk is the risk that, particularly during a financial crisis, someone holding CBDC might not be able to use it to buy goods and services or financial assets. Fed backing of the CBDC makes it unlikely that someone holding CBDC would have difficulty using it to buy goods and services or financial assets.

But the report also notes several risks that may result from the Fed issuing a CBDC:

- Banks rely on deposits for the funds they use to make loans to households and firms. If large numbers of households and firms switch from using checking accounts to using CBDC, banks will lose deposits and may have difficulty funding loans.

- If the Fed pays interest on the CBDC it issues, households, firms, and investors may switch funds from Treasury bills, money market mutual funds, and other short-term assets to the CBDC, which might potentially disrupt the financial system. Money market mutual funds buy significant amounts of corporate commercial paper. Some corporations rely heavily on the funds they raise from selling commercial paper to fund their short-term credit needs, including paying suppliers and financial inventories.

- In a financial panic, many people may withdraw funds from commercial bank deposits and convert the funds into CBDC. These actions might destabilize the banking system.

- A related point: A CBDC might result in large swings in bank reserves, particularly during and after a financial panic. As we discuss in Macroeconomics, Chapter 14, Section 14.4 (Economics, Chapter 24, Section 24.4), increasing and decreasing bank reserves is one way in which the Fed carries out monetary policy. So fluctuations in bank reserves may make it more difficult for the Fed to conduct monetary policy, particularly during a financial panic. (This consideration is less important during times like the present when banks hold very large reserves.)

- Because the Fed has no experience in operating a retail banking operation, it would be likely that if it began issuing a CBDC, it would do so through commercial banks or other financial firms rather than doing so directly. These financial firms would then hold customers CBDC accounts and carry out the actual flow of payments in CBDC among households and firms.

The report notes that the Fed is only beginning to consider the many issues that would be involved in issuing a CBDC and still needs to gather feedback from the general public, financial firms, nonfinancial firms, and investors, as well as from policymakers in Washington.

Sources: Peter Rudegeair and Liz Hoffman, “Facebook’s Cryptocurrency Venture to Wind Down, Sell Assets,” Wall Street Journal, January 26, 2022; Liana Baker, Jesse Hamilton, and Olga Kharif, “Mark Zuckerberg’s Stablecoin Ambitions Unravel with Diem Sale Talks,” bloomberg.com, January 25, 2022; Amara Omeokwe, “U.S. Regulators Raise Concern With Stablecoin Digital Currency,” Wall Street Journal, December 17, 2022; Jeanna Smialek, “Fed Opens Debate over a U.S. Central Bank Digital Currency with Long-Awaited Report,”, January 20, 2022; Board of Governors of the Federal Reserve System, Money and Payments: The U.S. Dollar in the Age of Digital Transformation, January 2022; and Aaron Klein, “The Fastest Way to Address Income Inequality? Implement a Real Time Payments System,” brookings.edu, January 2, 2019.

Inflation, Interest Rates, and Stock Prices

Caution: Long post!

An article in the Wall Street Journal quoted an economist at a financial services firm as noting that strong growth in wages could lead to sustained inflation. The article stated that as a result “the yield on the 10-year U.S. Treasury note [rose to] within reach of 2%” and that: “Rising [bond] yields this year have rattled markets and hurt tech stocks in particular ….”

What are the links between wage inflation and price inflation, inflation and bond yields, and bond yields and stock prices—particularly the prices of tech stocks?

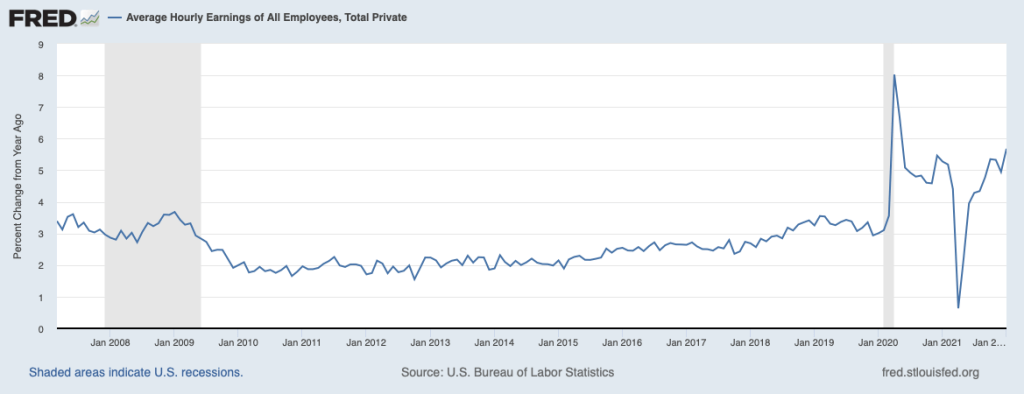

The link between wage inflation and price inflation. The monthly “Employment Situation” reports from the Bureau of Labor Statistics (BLS), in addition to providing data on payroll employment and the unemployment rate, also provide data on average hourly earnings (AHE). AHE are the wages and salaries per hour worked that private, nonfarm business pay workers. AHE don’t include the value of benefits that firms provide workers, such as contributions to 401(k) retirement accounts or health insurance. The following figure shows changes in AHE from the same month in the previous year. The figure shows that since the Covid-19 pandemic first began to affect the U.S. economy in March 2020, AHE have moved erratically. But since the fall of 2021, growth in AHE has been consistently above the 2 percent to 4 percent range that prevailed in the years after the end of the Great Recession of 2007–2009.

Employee compensation is the largest cost for most firms. For the economy as whole, employee compensation is about 80 percent of total costs. When firms pay higher wages per hour, their costs per unit of output don’t rise unless the wage increases are greater than the rate of growth of labor productivity, or output per hour worked. Increases in wages in the range of 5 percent to 6 percent are well above the rate of growth of labor productivity and, so, firms are likely to pass through the wage increases by raising prices. Note that the higher prices may prompt workers to push for higher wage increases to offset the decline in the real purchasing power of their wages, potentially setting off a wage-price spiral. (We discussed the possibility of a wage-price spiral in a recent post here.)

The link between inflation and bond yields. When investors lend money by, for instance, buying a bond, they are concerned with the interest rate they will receive after correcting for the effects of inflation. In other words, they focus on the real interest rate, which is equal to the nominal interest rate, or the stated interest rate on the loan or bond, minus the expected inflation rate:

Real interest rate = Nominal interest rate – Expected inflation rate.

We can rewrite this relationship as:

Nominal interest rate = Real interest rate + Expected inflation rate.

The second equation indicates that if investors expect the inflation rate to increase, then, unless the real interest rate changes, the nominal interest rate will increase. The Fisher effect is the idea associated with Yale economist Irving Fisher that the nominal interest rate rises or falls by the same number of percentage points as the expected inflation rate. So, for instance, if investors expect that the inflation rate will increase from 3 percent to 5 percent, then the nominal interest rate will also increase by two percentage points.

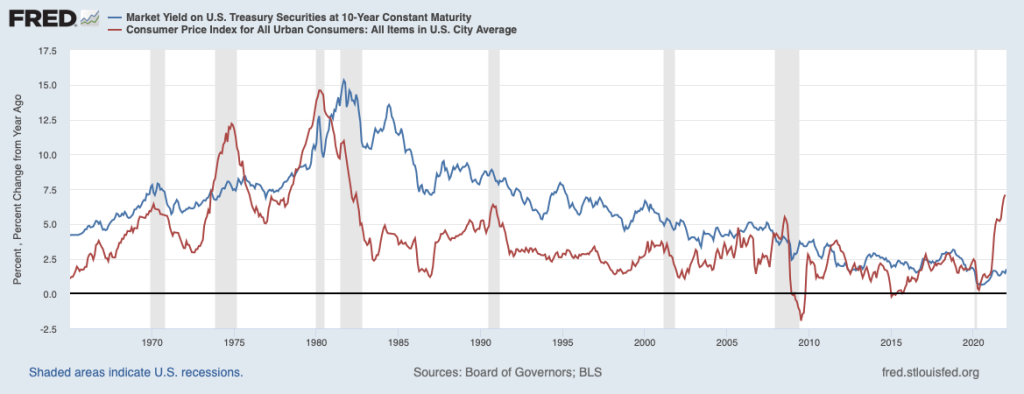

Because of real-world frictions, such as the broker fees that investors pay when buying and selling bonds and the taxes investors pay when they sell a bond that has increased in price, the Fisher effect doesn’t hold exactly. Still, most economists agree that an increase in the expected inflation rate will cause an increase in nominal interest rates. The following figure shows movements in the interest rate on 10-year Treasury notes (blue line) and in inflation (red line). Note that, roughly speaking, the interest rate on the 10-year Treasury note is higher when inflation is higher and lower when inflation is lower. (We discuss real and nominal interest rates in Macroeconomics, Chapter 9, Section 9.6 and in Economics, Chapter 19, Section 19.6. We discuss the Fisher effect in Money, Banking, and the Financial System, Chapter 4, Section 4.3.)

The link between bond yields and stock prices. As wage inflation leads to price inflation and price inflation leads to higher interest rates on bonds—particularly U.S. Treasury bonds—why might stock prices be affected? First, investors consider U.S. Treasury bonds to be default risk free, which means that investors are certain that the Treasury will make the interest and principal payments on the bonds. Stock investments are much riskier because they depend on the future profits of the firms issuing the stocks and those profits may fluctuate in ways that are difficult for investors to anticipate. So as interest rates on Treasury bonds increase, some investors will decide to sell stocks and buy bonds, which will cause a decline in stock prices.

Second, most people value funds they will receive now or soon more highly than funds they will receive in the more distant future. For instance, if someone offered to pay you $1,000 today or $1,000 one year from now, you will prefer to receive the money today. In other words, the present value, or value today, of a payment you won’t receive until the future is worth less than the face value of the payment. For instance, the present value of $1,000 you won’t receive for a year is worth less than $1,000 in present value. The higher the interest rate is, the lower the present value of payments, such as dividends, that you will receive in the future.

Economists believe that price of a financial investment, like a bond or a stock, is equal to the present value of the payments you will receive from owning the asset. If you own a bond, you will receive interest payments and payment of the bond’s principal when the bond matures. If you own a stock, you will receive dividends, which are the payments that firms make to shareholders from the firms’ profits. Therefore stock prices should reflect the present value of the dividends that investors expect to receive from owning the stock. (We discuss present value and the relationship between interest rates and stock and bond prices in Macroeconomics, Chapter 6, Appendix, in Economics, Chapter 8, Appendix, and, more completely, in Money, Banking, and the Financial System, Chapter 3, Section 3.2 and Chapter 6, Section 6.2.)

The Wall Street Journal article we quoted above notes that the rising interest rate on the 10-year Treasury note was causing price declines in tech stocks in particular. The explanation is that tech firms often go through an initial period in which they may make very low profits or even suffer losses. Investors may still be willing to buy stock in tech firms because they expect the firms eventually to increase their profits and the dividends they pay. But because those profits will be earned in the future—often after a period of losses that may stretch for years—the present value of the profits and, therefore, the price of the stock depends more on the interest rate than would be true of a firm making breakfast cereal or frozen pizza that will be steadily earning profits through the years. Therefore, we would expect, as the article indicates, that the prices of tech firms are more likely to decline—or to decline more—when interest rates rise than is true of other firms.

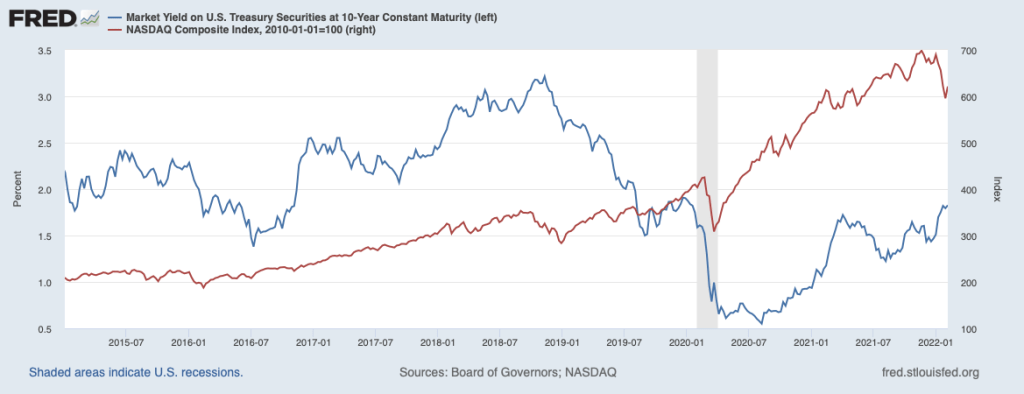

The following figure shows the interest rate on the 10-year Treasury note (blue line with scale given on the left) and the values of the Nasdaq composite stock index (red line with the value for January 1, 2010 set equal to 100 and the scale given on the right). The Nasdaq includes the stocks of more tech firms than is true of the other widely followed stock market indexes—the S&P 500 and the Dow Jones Industrial Average. The figure shows that the declining interest rate on 10-year Treasury notes that began in late 2018 and continued through mid-2020 coincided with increases in the prices of the stocks in the Nasdaq index—apart from the spring of 2020 during the beginning of the Covid-19 pandemic. The most recent period shows that increases in the interest rate on the 10-year Treasury note have corresponded with a decline in the Nasdaq, as noted in the article.

Source: Sam Goldfarb, “Elevated Bond Yields Approach Key Milestone,” Wall Street Journal, February 7, 2022; U.S. Bureau of Economic Analysis, “Prices, Costs, and Profit per Unit of Real Gross Value Added of Nonfinancial Domestic Corporate Business,” January 27, 2022; and Federal Reserve Bank of St. Louis.

The Controversy over Modern Monetary Theory (MMT)

On Sunday, February 6, the New York Times ran an article on Modern Monetary Theory (MMT) on the front page of its business section with the title, “Time for a Victory Lap.” Link here, subscription may be required. (Note: The title of the article was later changed on the nytimes.com site to “Is This What Winning Looks Like?” perhaps because of the controversy linked to below.)

The article led to a controversy on Twitter (but, then, what topic doesn’t lead to a controversy on Twitter?). Social media is, obviously, not always the best place to discuss economic theory and policy, but instructors and students interested in the debate may find the following links useful both because of the substantive issues raised and as an example of how debates over economic policy can sometimes become heated.

Harvard economist Lawrence Summers reacts negatively to the content of the New York Times article (and to MMT) here.

Economics blogger Noah Smith also reacts negatively to the article here. Smith’s blog post discussing the article at length is here, subscription may be required.

Former Fed economist Claudia Sahm defends the article (and MMT) here.

Jeanna Smialek, the author of the New York Times article, reacts to critics of the article here and to Noah Smith’s blog post here. Smith responds to her response here.

Jason Furman of Harvard’s Kennedy School provides a brief discussion of whether MMT has had much influence on monetary policy here.

We discuss MMT in the Apply the Concept, “Modern Monetary Theory: Should We Stop Worrying and Love the Debt?” in Macroeconomics, Chapter 16, Section 16.6 and in Economics, Chapter 26, Section 26.6.

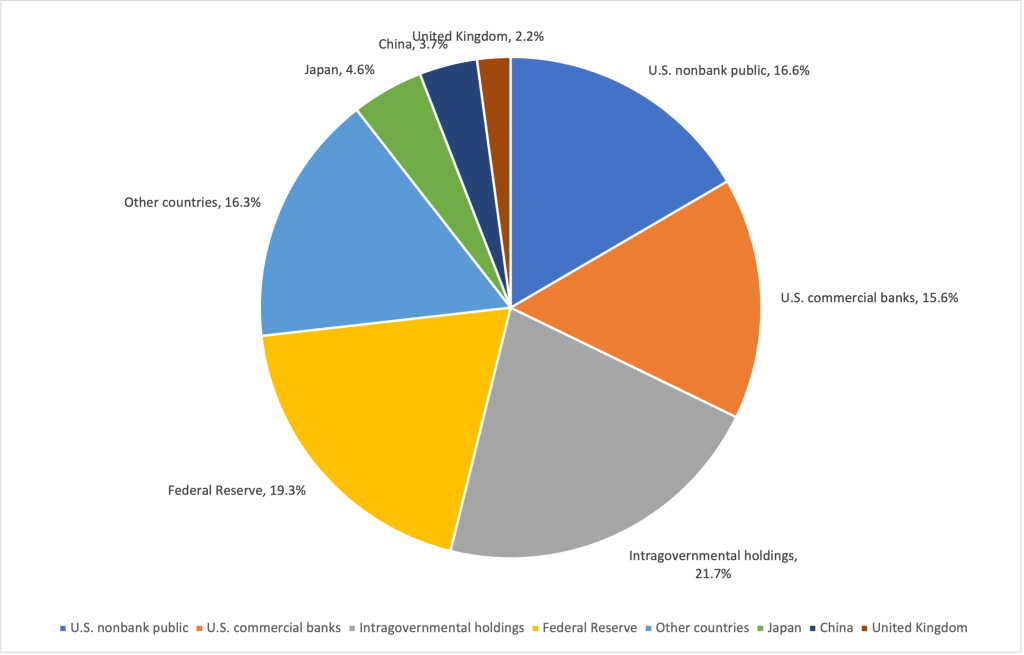

The National Debt Just Hit $30 Trillion. Who Owns It?

On February 1, 2022, a headline in the Wall Street Journal noted that: “U.S. National Debt Exceeds $30 Trillion for the First Time.” The national debt—or, more formally, the federal government debt—is the value of all U.S. Treasury securities outstanding. Treasury securities include Treasury bills, which mature in one year or less; Treasury notes, which mature between 2 years and 10 years; Treasury bonds, which mature in 30 years; U.S. savings bonds purchased by individual investors; and Treasury Inflation-Protected Securities (TIPS), which, unlike other Treasury securities, have their principal amounts adjusted every six months to reflect changes in the consumer price index (CPI).

With a value of $30 trillion, the federal government debt in early February is about 120 percent of GDP, a record that exceeds the ratio of government debt to GDP during World War II. In 2007, at the beginning of the Great Recession of 2007–2009, the ratio of government debt to GDP was only 35 percent. (We discuss the federal government debt in Macroeconomics, Chapter 16, Section 16.6 and in Economics, Chapter 26, Section 26.6.)

There are many important economic issues involved with the federal government debt, but in this blog post we’ll focus just on the question of who owns the debt.

The pie chart below shows the shares of the debt held by different groups. The largest slice shown is for “intragovernmental holdings,” which represent ownership of Treasury securities by government trust funds, notably the Social Security trust funds. The Social Security system makes payments to retired or disabled workers. The system operates on a pay-as-you-go basis, which means that the payroll taxes collected from today’s workers are used to make payments to retired workers. Because of slowing population growth, Congress authorized an increase in payroll taxes above the level necessary to make current payments. The Social Security system has invested the surplus in special Treasury securities that the Treasury redeems when the funds are necessary to make payments to retired workers. (In the Apply the Concept “Is Spending on Social Security and Medicare a Fiscal Time Bomb?” in Macroeconomics, Chapter 16, Section 16.1, we discuss the long-term funding problems of the Social Security and Medicare systems.)

Some economists argue that the value of these Treasury securities should not be counted as part of the federal government debt because the securities are not marketable in the way that Treasury bills, notes, and bonds are and because the securities represent a flow of funds from one federal agency to another federal agency. If we exclude the value of these securities, the national debt on February 1, 2022 was $23.5 trillion rather than $30.0 trillion.

The Federal Reserve System holds about 19 percent of federal government debt. The Fed buys and sells Treasury securities as part of its normal conduct of monetary policy. In addition, the Fed accumulated large holdings of Treasury securities as part of its quantitative easing operations during and following the 2007–2009 financial crisis and from 2020 to 2022 during the worst of the Covid-19 pandemic. (We discuss quantitative easing in Macroeconomics, Chapter 15, Section 15.3.)

About 27 percent of the debt is held by foreign central banks, foreign commercial banks, and foreign investors. The largest amount of Treasury debt is held by Japan, followed by China and the United Kingdom. All other countries combined hold about 16 percent of the debt.

U.S. commercial banks hold more than 15 percent of the debt. Banks hold Treasury securities partly because since the 2007–2009 financial crisis most interest rates, including those on loans and on corporate and municipal bonds, have been very low compared with historic averages. The interest rates on these assets are in some cases too low to compensate banks for the risk of owning the assets rather than default-risk free Treasury securities. In addition, large banks are required to meet a liquidity coverage ratio, which means that they have to hold sufficient liquid assets—those that can be easily converted into cash—to meet their need for funds in a financial crisis. Many banks meet their liquidity requirements, in part, by owning Treasury securities.

The remaining Treasury securities—about 16.5 percent of the total federal government debt—are held by the U.S. nonbank public. The nonbank public includes financial firms—such as investment banks, insurance companies, and mutual funds—as well as individual investors.

Sources: Amara Omeokwe, “U.S. National Debt Exceeds $30 Trillion for First Time,” Wall Street Journal, February 1, 2022; “Debt to the Penny,” fiscaldata.treasury.gov; “Major Foreign Holders of Treasury Securities,” ticdata.treasury.gov; and Federal Reserve Bank of St. Louis.

AIT or FAIT: How Will the Fed’s New Monetary Policy Strategy Deal with High Inflation Rates?

Congress has given the Fed a mandate to achieve the goal of price stability. Until 2012, the Fed had never stated explicitly how they would measure whether they had achieved this goal. One interpretation of price stability is that the price level remains constant. But a constant price level would be very difficult to achieve in practice and the Fed has not attempted to do so. In 2012, the Fed, under then Chair Ben Bernanke, announced that it was targeting an inflation rate of 2 percent, which it believed was low enough to be consistent with price stability: “When households and businesses can reasonably expect inflation to remain low and stable, they are able to make sound decisions regarding saving, borrowing, and investment, which contributes to a well-functioning economy.” (We discuss inflation targeting in Macroeconomics, Chapter 15, Section 15.5 and Economics, Chapter 25, Section 25.5.)

In August 2020, the Fed announced a new monetary policy strategy that modified how it interpreted its inflation target: “[T]he Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.” The Fed’s new approach is sometimes referred to as average inflation targeting (AIT) because the Fed attempts to achieve its 2 percent target on average over a period of time, although the Fed has not explicitly stated how long the period of time may be. In other words, the Fed hasn’t indicated the time horizon during which it intends inflation to average 2 percent.

The Fed uses changes in the personal consumption expenditure (PCE) price index to measure inflation, rather than using changes in the consumer price index (CPI). The Fed prefers the PCE to the CPI because the PCE is a broader measure of the price level in that it includes the prices of more consumer goods and services than does the CPI. The following figure shows inflation for the period since 2006 measured by percentage changes in the PCE from the corresponding month in the previous year. (Members of the Fed’s Federal Open Market Committee generally consider changes in the core PCE—which excludes the prices of food and energy—to be the best measure of the underlying rate of inflation. But because the Fed’s inflation target is stated in terms of the PCE rather than the core PCE, we are looking here only at the PCE.) The figure shows that for most of the period from 2012 to early 2021, inflation was less than the Fed’s target of 2 percent.

The figure also shows that since March 2021, inflation has been running above 2 percent and has steadily increased, reaching a rate of 5.8 percent in December 2021. Note that a strict interpretation of AIT would mean that the Fed would have to balance these inflation rates far above 2 percent with future inflation rates well below 2 percent. As Ricardo Reis, an economist at the London School of Economics, noted recently: “If the [Fed’s time] horizon is 3 years, the Fed … will [have to] pursue monetary policy to achieve annual inflation of… −0.5% over the next year and a half. If the horizon is 5 years, the Fed … will [have to] pursue policy to achieve annual inflation of 0.9% over the next 3.5 years.” It seems unlikely that the Fed would want to bring about inflation rates that low because doing so would require raising its target for the federal funds rate to levels likely to cause a recession.

Another interpretation of the Fed’s monetary policy strategy is that involves a flexible average inflation target (FAIT) approach rather than a strictly AIT approach. Former Fed Vice Chair Richard Clarida discussed this interpretation of the Fed’s strategy in a speech in November 2020. He noted that the framework was asymmetric, meaning that inflation rates higher than 2 percent need not be offset with inflation rates lower than 2 percent: “The new framework is asymmetric. …[T]he goal of monetary policy … is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent.” And: “Our framework aims … for inflation to average 2 percent over time, but it does not make a … commitment to achieve … inflation outcomes that average 2 percent under any and all circumstances ….”

Under this interpretation, particularly if Fed policymakers believe that the high inflation rates of 2021 were the result of temporary supply chain problems and other factors caused by the pandemic, it would not need to offset them by forcing inflation to very low levels in order to make the average inflation rate over time equal 2 percent. Critics of the FAIT approach to monetary policy note that the approach doesn’t provide investors, household, and firms with much guidance on what inflation rates the Fed may find acceptable over the short-term of a year or so. In that sense, the Fed is moving away from a rules-based policy, such as the Taylor rule that we discuss in Chapter 15. Or, as a columnist for the Wall Street Journal wrote with respect to FAIT: “Of course, the word ‘flexible’ is there because the Fed doesn’t want to be tied down, so it can do anything.”

The Fed’s actions during 2022 will likely provide a better understanding of how it intends to implement its new monetary policy strategy during conditions of high inflation.

Sources: Board of Governors of the Federal Reserve, “Why does the Federal Reserve aim for inflation of 2 percent over the longer run?” federalreserve.gov, August 27, 2020; Board of Governors of the Federal Reserve, “2020 Statement on Longer-Run Goals and Monetary Policy Strategy,” federalreserve.gov, January 14, 2021; Ricardo Reis’s comments are from this Twitter thread: https://mobile.twitter.com/R2Rsquared/status/1488552608981827590, Richard H. Clarida, “The Federal Reserve’s New Framework: Context and Consequences,” federalreserve.gov, November 16, 2020; and James Mackintosh, “On Inflation Surge, the Fed Is Running Out of Excuses,” Wall Street Journal, November 14, 2021.