Earlier this month, Sam Bankman-Fried was convicted of fraud connected with the collapse of the FTX cryptocurrency exchange he founded. (We discuss aspects of cryptocurrencies in earlier blog posts here and here.) Bankman-Fried had a reputation for dressing casually and for having bushy, unkempt hair. In preparing for his trial, Bankman-Fried paid another inmate at the Metropolitan Detention Center in New York City to cut his hair short. According to an article in the Wall Street Journal, Bankman-Fried paid the other inmate not with currency but with four packets of mackerels—like the ones shown in the photo above—to cut his hair.

Although using packets of mackerels to buy and sell services may seem strange, in fact, packets of mackerel seem to be widely used in place of currency in the U.S. prison system. We explained the situation in an Apply the Concept in an earlier edition of our principles textbook. We reproduce that feature here. Note that the inmate quoted indicates that the price of a haircut at that time was only two mackerel packets rather than the four that Bankman-Fried paid. (Question to consider: Would we expect that prices of services in terms of mackerel packets would be the same across prisons at a given time or in the same prison over time?)

The Mackerel Economy in the Federal Prison System

Inmates of the federal prison system are not allowed to have money. Funds they earn working in the prison or receive from friends and relatives are placed in an account they can draw on to buy snacks and other items from the prison store. Lacking money, prisoners could barter with each other in exchanging goods and services, but we have seen that barter is inefficient. Since about 2004, in many prisons small plastic packets of mackerel fillets costing about $1 each have been used as money. [According to the Wall Street Journal article linked to earlier, the mackerel packets now sell for $1.30.] The packets are known in prison as “macks.”

Some prisoners have set up small businesses using mackerel packets for money. They sell services such as shoe shines, cell cleaning, or haircuts for macks. According to a prisoner in Lompoc prison in California, “A haircut is two macks.” A former prisoner described a fellow prisoner’s food business: “I knew a guy who would buy ingredients and use the microwaves to cook meals. Then people used mack to buy it from him.” In the Pensacola prison in Florida, the prison commissary was open only one day a week. So, several prisoners would run “prison 7-Elevens” by stocking up on goods and reselling them for macks at a profit. Very few prisoners actually eat the mackerel in the packets. In fact, apart from prison commissaries, the demand for mackerel in the United States is very small.

The mackerel economy is under pressure at some prisons, where rules exist against hoarding goods from the commissary. Prisoners caught dealing in macks can risk no longer being allowed to use the commissary or may be moved to a less desirable cell. In these prisons, the mackerel economy has been pushed underground.

The prison mackerel economy illustrates an important fact about money: Anything can be used as money, as long as people are willing to accept it in exchange for goods and services—even pouches of fish that no one wants to eat.

Source: Justin Scheck, “Mackerel Economics in Prison,” Wall Street Journal, October 2, 2008.

A job fair in Jackson, Mississippi (photo from the Associated Press)

As part of the Social Security Act of 1935,Congress created the unemployment insurance program to make payments to unemployed workers. The program run jointly by the federal government and the state governments. It’s financed primarily by state and federal taxes on employers. States are allowed to determine which workers are eligible, the dollar amount of the unemployment benefit workers will receive, and for how long workers will receive the benefit.

What’s the purpose of the unemployment insurance program? A document published the U.S. Department of Labor explains that: “Unemployment compensation is a social insurance program. It is designed to provide benefits to most individuals out of work, generally through no fault of their own, for periods between jobs…. [Unemployment compensation] ensures that a significant proportion of the necessities of life can be met on a week-to-week basis while a search for work takes place.”

But the same document also notes that unemployment compensation “maintains [unemployed workers’] purchasing power which also acts as an economic stabilizer in times of economic downturn.” By “economic stabilizer,” the Department of Labor is noting that unemployment compensation is what in Macroeconomics, Chapter 16, Section 16.1 (Economics, Chapter 26, Section 26.1) we call an automatic stabilizer. An automatic stabilizer is a government spending or taxing program that automatically increases or decreases along with the business cycle.

As shown in the following figure, when the economy enters a recession, the total amount of unemployment compensation payments increases without the federal government or the state governments having to take any action because eligibility for the payments is already defined in existing law. So, during a recession, the unemployment insurance program helps to keep aggregate demand higher than it would otherwise be, which can lessen the severity of the recession.

As we discuss in Macroeconomics, Chapter 9, Section 9.3 (Economics, Chapter 19, Section 19.3), the unemployment insurance program can have an unintended effect. The higher the unemployment insurance payment a worker receives and the longer the worker receives it, the more likely the worker is to delay searching for another job. In other words, by reducing the opportunity cost of being unemployed, unemployment insurance benefits may unintentionally increase the length of unemployment spells—the amount of time the typical worker is unemployed.

During and immediately after the 2020 recession, the federal government increased the dollar amount of the unemployment insurance payments that workers received and extended the number of months workers could continue to receive these payments. Under the American Rescue Plan, a law which President Biden proposed and Congress passed in March 2021, workers receiving unemployment insurance benefits received an additional $300 weekly from March 2021 until September 6, 2021. Also, under the law, people, such as the self-employed and gig workers, would receive unemployment insurance benefits even though they had previously been ineligible to receive them. (Note the resulting spike during this period in the total dollar amount of unemployment insurance benefits as shown in the above figure.)

Some state governments were concerned that the extended benefits might cause some workers to delay taking jobs, thereby slowing the recovery of these states’ economies from the effects of the pandemic. Accordingly, 18 states stopped participating in the programs in June 2021, meaning that at that time unemployed workers would no longer receive the extra $300 per week and workers who prior to March 2021 hadn’t been eligible to receive unemployment benefits would again be ineligible.

Were unemployed workers in the states that ended the expanded unemployment insurance benefits in June more likely to become employed than were unemployed workers in states that continued the expanded benefits into September? On the one hand, ending the expanded benefits would increase the opportunity cost of not having a job. But, on the other hand, because government payments to workers would decline in these states, the result could be a decline in consumer spending that would decrease the demand for labor. Which of these effects was larger would determine whether employment increased or decreased in the states that ended expanded unemployment benefits early.

Glenn, along with Harry Holzer of Georgetown University and Michael Strain of the American Enterprise Institute, carried out an econometric analysis to explore the effects ending expanded unemployment benefits early had on the labor markets in those states. They find that:

Among unemployed workers ages 25 to 54 (“prime-age workers”), ending the expanded unemployment benefit program increased the number of workers in those states who moved from being unemployed to being employed by 14 percentage points.

Among prime-age workers, the employment-to-population ratio in those states increased by about 1 percentage point.

Among prime-age workers, the unemployment rate in those stated decreased by about 0.9 percentage point.

These estimates indicate that the effect of ending the expanded unemployment benefit program raised the opportunity cost of being unemployed more than it decreased the demand for labor by reducing the incomes of some household. But what about the larger question of whether households were made better or worse off as a result of ending the program early? The authors find that ending the program early decreased the share of households that had no difficulty meeting expenses. They, therefore, conclude that the effects on household well-being of ending the program early are ambiguous.

The paper presenting these results can be found here. Warning! The econometric analysis is quite technical.

Some interesting macro data were released during the past two weeks. On the key issues, the data indicate that inflation continues to run in the range of 3.0 percent to 3.5 percent, although depending on which series you focus on, you could conclude that inflation has dropped to a bit below 3 percent or that it is still in vicinity of 4 percent. On balance, output and employment data seem to be indicating that the economy may be cooling in response to the contractionary monetary policy that the Federal Open Market Committee began implementing in March 2022.

We can summarize the key data releases.

Employment, Unemployment, and Wages

On Friday morning, the Bureau of Labor Statistics (BLS) released its Employment Situation report. (The full report can be found here.) Economists and policymakers—notably including the members of the Federal Reserve’s Federal Open Market Committee (FOMC)—typically focus on the change in total nonfarm payroll employment as recorded in the establishment, or payroll, survey. That number gives what is generally considered to be the best indicator of the current state of the labor market.

The previous month’s report included a surprisingly strong net increase of 336,000 jobs during September. Economists surveyed by the Wall Street Journal last week forecast that the net increase in jobs in October would decline to 170,000. The number came in at 150,000, slightly below that estimate. In addition, the BLS revised down the initial estimates of employment growth in August and September by a 101,000 jobs. The figure below shows the net gain in jobs for each month of 2023.

Although there are substantial fluctuations, employment increases have slowed in the second half of the year. The average increase in employment from January to June was 256,667. From July to October the average increase declined to 212,000. In the household survey, the unemployment rate ticked up from 3.8 percent in September to 3.9 percent in October. The unemployment rate has now increased by 0.5 percentage points from its low of 3.4 percent in April of this year.

Finally, data in the employment report provides some evidence of a slowing in wage growth. The following figure shows wage inflation as measured by the percentage increase in average hourly earnings (AHE) from the same month in the previous year. The increase in October was 4.1 percent, continuing a generally downward trend since March 2022, although still somewhat above wage inflation during the pre-2020 period.

As the following figure shows, September growth in average hourly earnings measured as a compound annual growth rate was 2.5 percent, which—if sustained—would be consistent with a rate of price inflation in the range of the Fed’s 2 percent target. (The figure shows only the months since January 2021 to avoid obscuring the values for recent months by including the very large monthly increases and decreases during 2020.)

Job Openings and Labor Turnover Survey (JOLTS)

On November 1, the BLS released its Job Openings and Labor Turnover Survey (JOLTS) report for September 2023. (The full report can be found here.) The report indicated that the number of unfilled job openings was 9.5 million, well below the peak of 11.8 million job openings in December 2021 but—as shown in the following figure—well above prepandemic levels.

The following figure shows the ratio of the number of job opening to the number of unemployed people. The figure shows that, after peaking at 2.0 job openings per unemployed person in in March 2022, the ratio has decline to 1.5 job opening per unemployed person in September 2022. While high, that ratio was much closer to the ratio of 1.2 that prevailed during the year before the pandemic. In other words, while the labor market still appears to be strong, it has weakened somewhat in recent months.

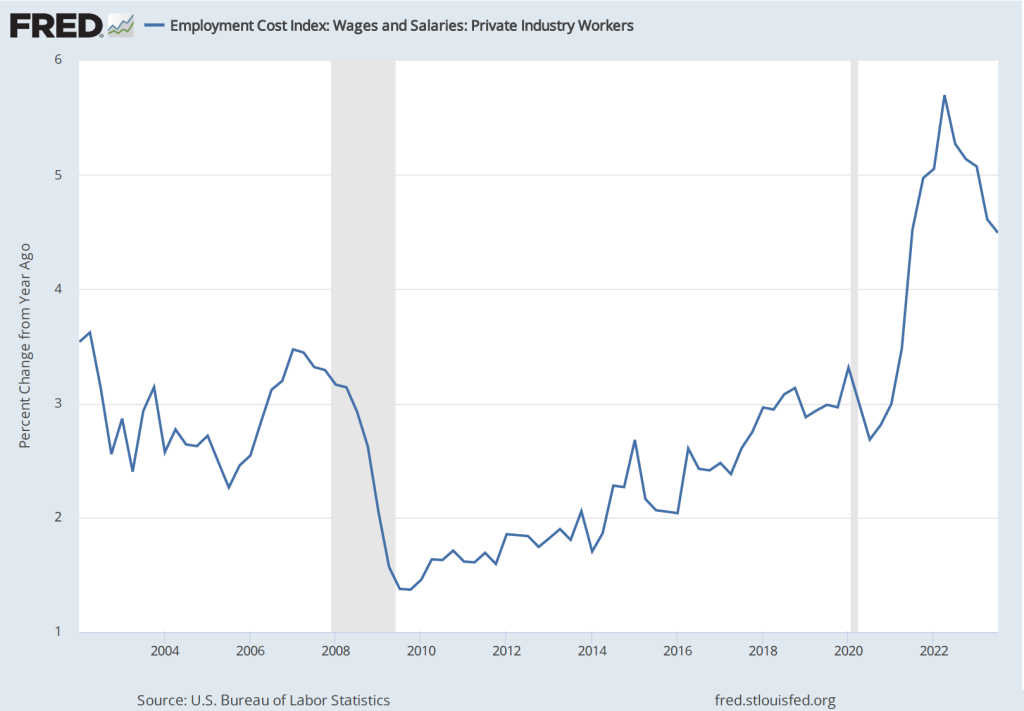

Employment Cost Index

As we note in this blog post, the employment cost index (ECI), published quarterly by the BLS, measures the cost to employers per employee hour worked and can be a better measure than AHE of the labor costs employers face. The BLS released its most recent report on October 31. (The report can be found here.) The first figure shows the percentage change in ECI from the same quarter in the previous year. The second figure shows the compound annual growth rate of the ECI. Both measures show a general downward trend in the growth of labor costs, although compound annual rate of change shows an uptick in the third quarter of 2023. (We look at wages and salaries rather than total compensation because non-wage and salary compensation can be subject to fluctuations unrelated to underlying trends in labor costs.)

The Federal Open Market Committee’s October 31-November 1 Meeting

As was widely expected from indications in recent statements by committee members, the Federal Open Market Committee voted at its most recent meeting to hold constant its targe range for the federal funds rate at 5.25 percent to 5.50 percent. (The FOMC’s statement can be found here.)

At a press conference following the meeting, Fed Chair Jerome Powell remarks made it seem unlikely that the FOMC would raise its target for the federal funds rate at its December 14-15 meeting—the last meeting of 2023. But Powell also noted that the committee was unlikely to reduce its target for the federal funds rate in the near future (as some economists and financial jounalists had speculated): “The fact is the Committee is not thinking about rate cuts right now at all. We’re not talking about rate cuts, we’re still very focused on the first question, which is: have we achieved a stance of monetary policy that’s sufficiently restrictive to bring inflation down to 2 percent over time, sustainably?” (The transcript of Powell’s press conference can be found here.)

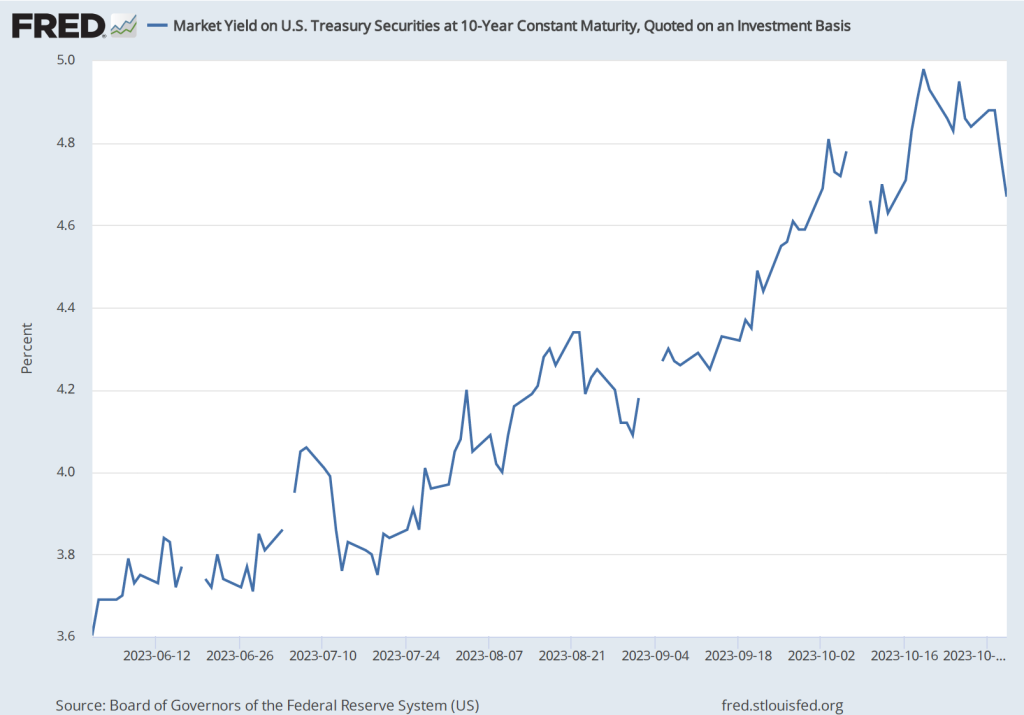

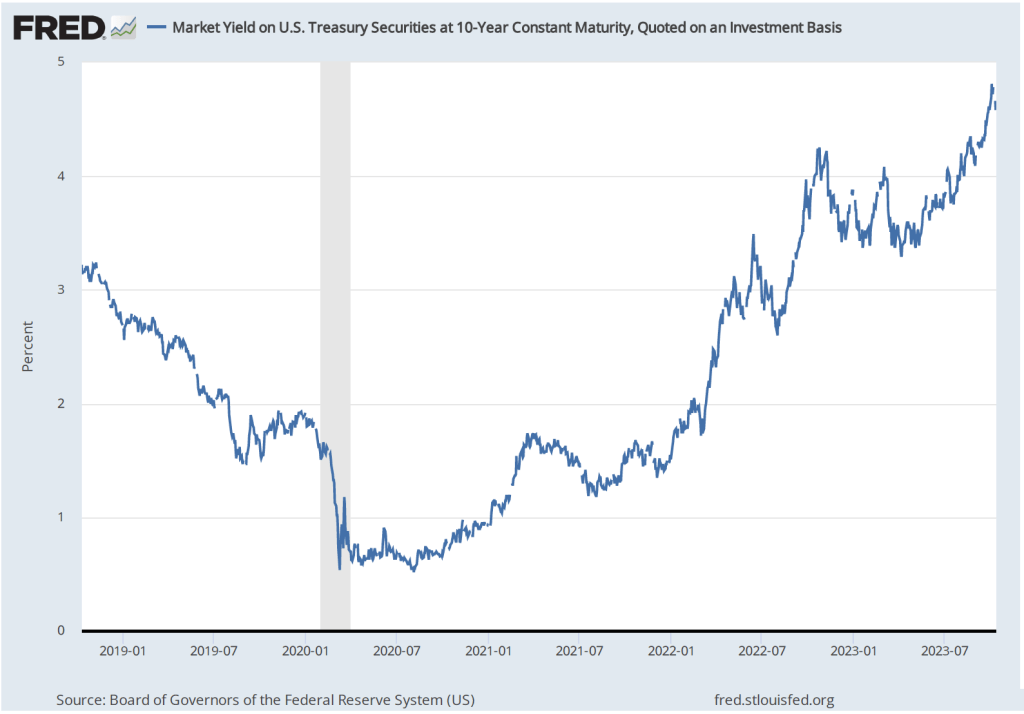

Investors in the bond market reacted to Powell’s press conference by pushing down the interest rate on the 10-year Treasury note, as shown in the following figure. (Note that the figure gives daily values with the gaps representing days on which the bond market was closed) The interest rate on the Treasury note reflects investors expectations of future short-term interest rates (as well as other factors). Investors interpreted Powell’s remarks as indicating that short-term rates may be somewhat lower than they had previously expected.

Real GDPand the Atlanta Fed’s Real GDPNow Estimate for the Fourth Quarter

On October 26, the Bureau of Economic Analysis (BEA) released its advance estimate of real GDP for the third quarter of 2023. (The full report can be found here.) We discussed the report in this recent blog post. Although, as we note in that post, the estimated increase in real GDP of 4.9 percent is quite strong, there are indications that real GDP may be growing significantly more slowly during the current (fourth) quarter.

The Federal Reserve Bank of Atlanta compiles a forecast of real GDP called GDPNow. The GDPNow forecast uses data that are released monthly on 13 components of GDP. This method allows economists at the Atlanta Fed to issue forecasts of real GDP well in advance of the BEA’s estimates. On November 1, the GDPNow forecast was that real GDP in the fourth quarter of 2023 would increase at a slow rate of 1.2 percent. If this preliminary estimate proves to be accurate, the growth rate of the U.S. economy will have sharply declined from the third to the fourth quarter.

Fed Chair Powell has indicated that economic growth will likely need to slow if the inflation rate is to fall back to the target rate of 2 percent. The hope, of course, is that contractionary monetary policy doesn’t cause aggregate demand growth to slow to the point that the economy slips into a recession.

Join authors Glenn Hubbard & Tony O’Brien as they reflect on the Fed’s efforts to execute the soft landing, ponder if the effect will stick, and wonder if future economies will be tethered to an anchor point above two percent.

Fed Chair Jerome Powell and Fed Vice-Chair Philip Jefferson this summer at the Fed conference in Jackson Hole, Wyoming. (Photo from the AP via the Washington Post.)

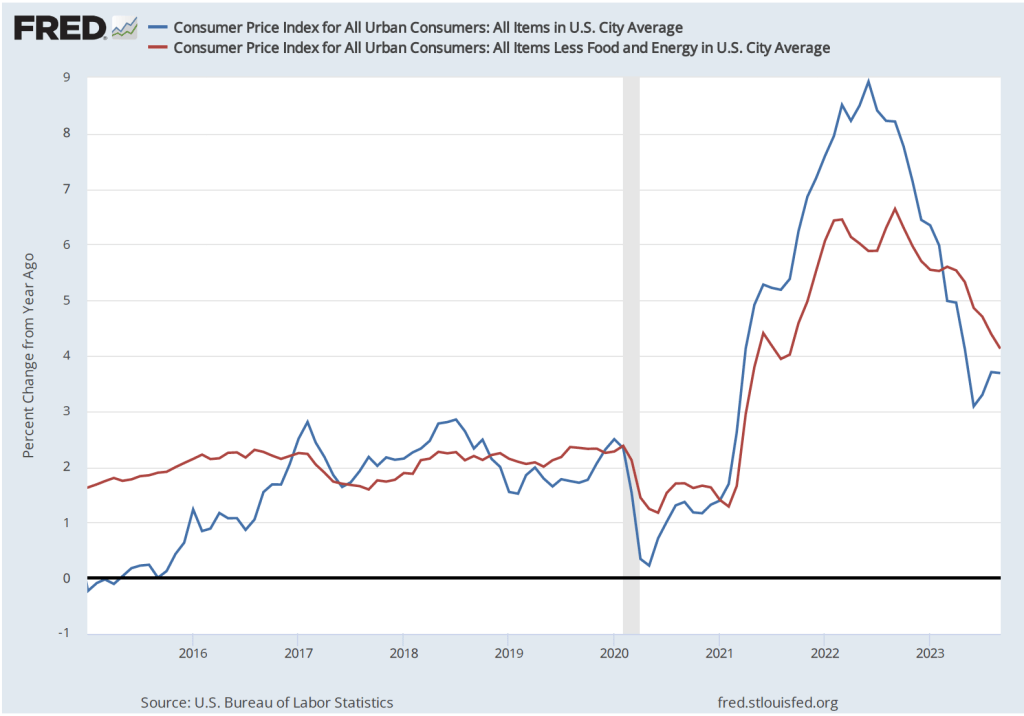

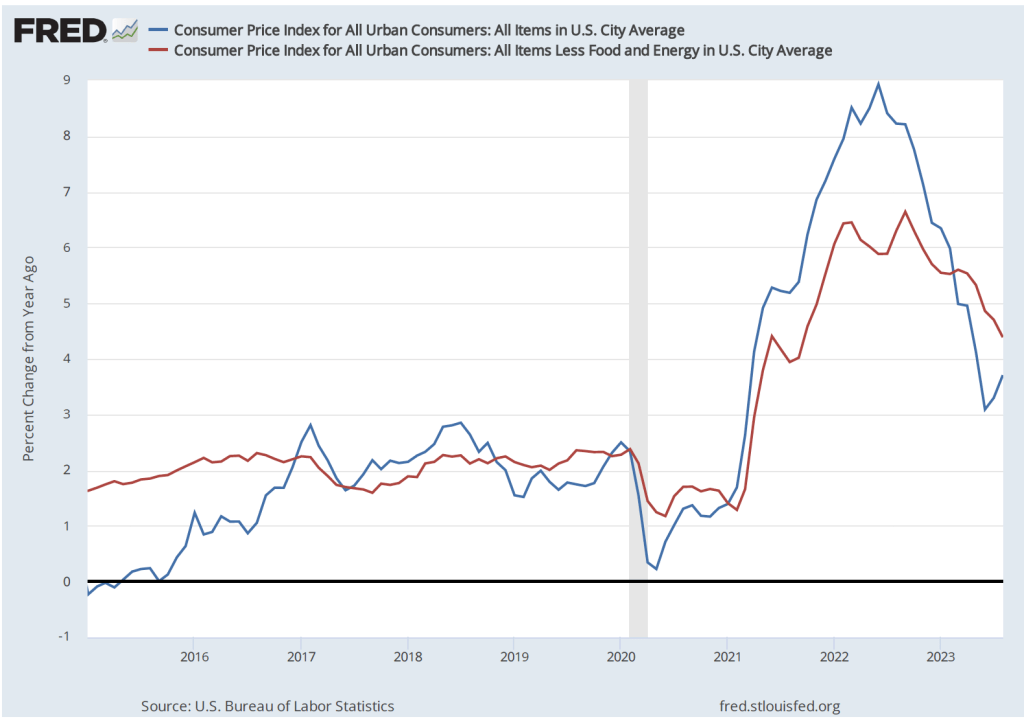

This morning, the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for September. (The full report can be found here.) The report was consistent with other recent data showing that inflation has declined markedly from its summer 2022 highs, but appears, at least for now, to be stuck in the 3 percent to 4 percent range—well above the Fed’s 2 percent inflation target.

The report indicated that the CPI rose by 0.4 percent in September, which was down from 0.6 percent in August. Measured by the percentage change from the same month in the previous year, the inflation rate was 3.7 percent, the same as in August. Core CPI, which excludes the prices of food and energy, increased by 4.1 percent in September, down from 4.4 percent in August. The following figure shows inflation since 2015 measured by CPI and core CPI.

Reporters Gabriel Rubin and Nick Timiraos, writing in the Wall Street Journalsummarized the prevailing interpretation of this report:

“The latest inflation data highlight the risk that without a further slowdown in the economy, inflation might settle around 3%—well below the alarming rates that prompted a series of rapid Federal Reserve rate increases last year but still above the 2% inflation rate that the central bank has set as its target.”

As we discuss in this blog post, some economists and policymakers have argued that the Fed should now declare victory over the high inflation rates of 2022 and accept a 3 percent inflation rate as consistent with Congress’s mandate that the Fed achieve price stability. It seems unlikely that the Fed will follow that course, however. Fed Chair Jerome Powell ruled it out in a speech in August: “It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so.”

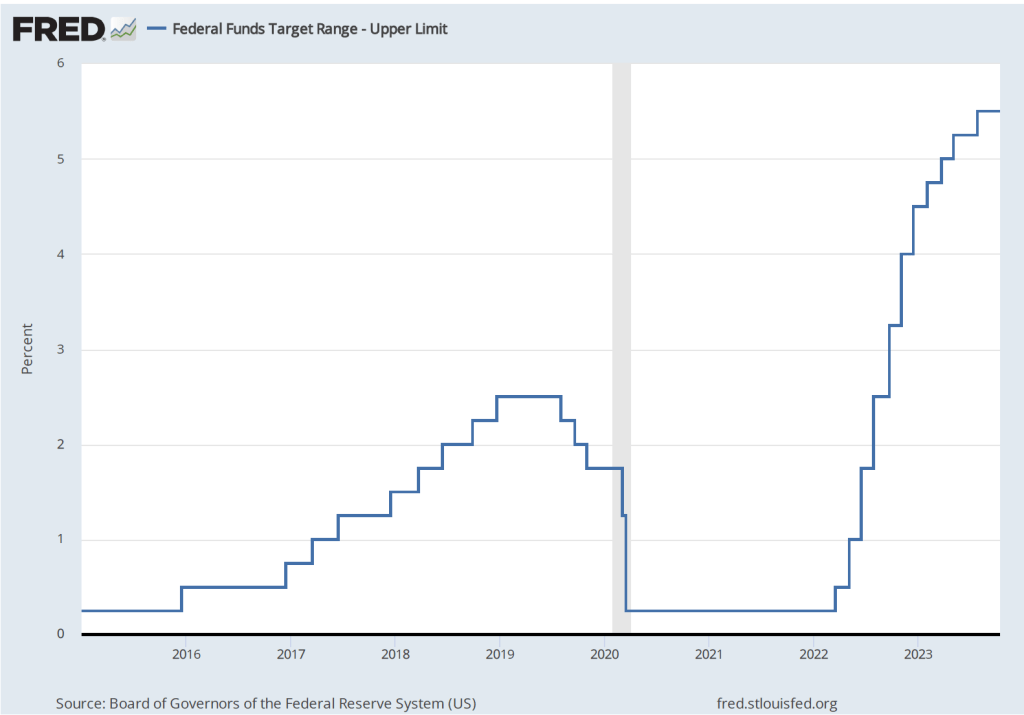

To achieve its goal of bringing inflation back to its 2 percent targer, it seems likely that economic growth in the United States will have to slow, thereby reducing upward pressure on wages and prices. Will this slowing require another increase in the Federal Open Market Committe’s target range for the federal funds rate, which is currently 5.25 to 5.50 percent? The following figure shows changes in the upper bound for the FOMC’s target range since 2015.

Several members of the FOMC have raised the possibility that financial markets may have already effectively achieved the same degree of policy tightening that would result from raising the target for the federal funds rate. The interest rate on the 10-year Treasury note has been steadily increasing as shown in the following figure. The 10-year Treasury note plays an important role in the financial system, influencing interest rates on mortgages and corporate bonds. In fact, the main way in which monetary policy works is for the FOMC’s increases or decreases in its target for the federal funds rate to result in increases or decreases in long-run interest rates. Higher long-run interest rates typically result in a decline in spending by consumrs on new housing and by businesses on new equipment, factories computers, and software.

Federal Reserve Bank of Dallas President Lorie Logan, who serves on the FOMC, noted in a speech that “If long-term interest rates remain elevated … there may be less need to raise the fed funds rate.” Similarly, Fed Vice-Chair Philip Jefferson stated in a speech that: “I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

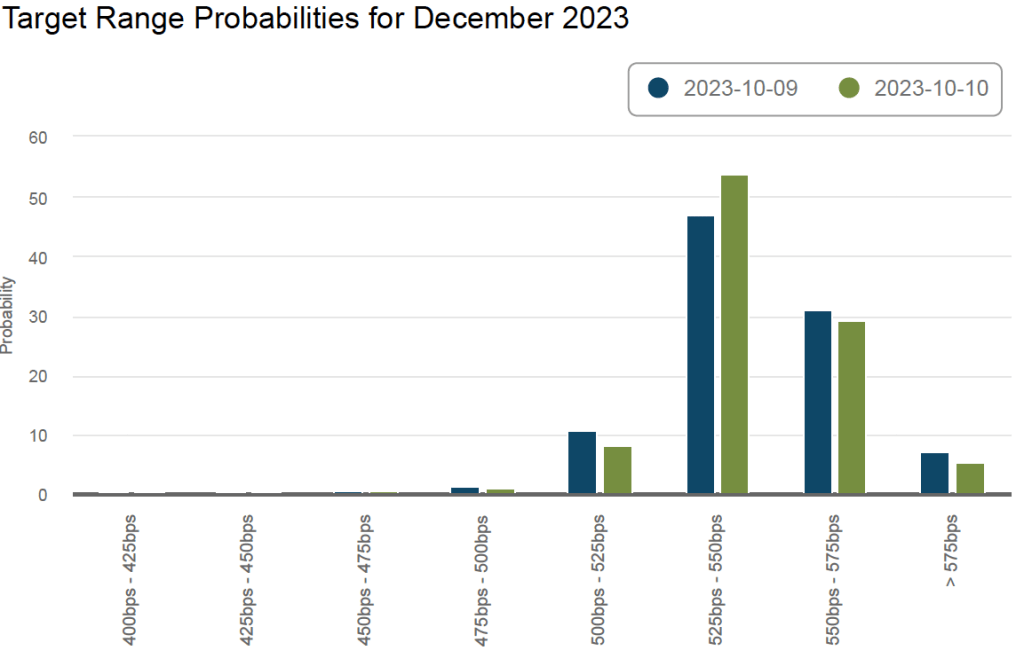

The FOMC has two more meetings scheduled for 2023: One on October 31-November 1 and one on December 12-13. The following figure from the web site of the Federal Reserve Bank of Atlanta shows financial market expectations of the FOMC’s target range for the federal funds rate in December. According to this estimate, financial markets assign a 35 percent probability to the FOMC raising its target for the federal funds rate by 0.25 or more. Following the release of the CPI report, that probability declined from about 38 percent. That change reflects the general expectation that the report didn’t substantially affect the likelihood of the FOMC raising its target for the federal funds rate again by the end of the year.

A trader on the New York Stock Exchange listtening to Fed Chair Jerome Powell (from Reuters via the New York Times)

Accounting for movements in the market prices of stocks and bonds is not an exact exercise. Accounts in the Wall Street Journal and on other business web sites often attribute movements in stock and bond prices to the Fed having acted in a way that investors didn’t expect.

The decision by the Fed’s Federal Open Market Committee (FOMC) at its meeting on September 20-21, 2023 to hold its target for the federal funds rate constant at a range of 5.25 percent to 5.50 percent wasn’t a surprise. Fed Chair Jerome Powell had signaled during his press conference on July 26 following the FOMC’s previous meeting that the FOMC was likely to pause further increases in the federal funds rate target. (A transcript of Powell’s July 26 press conference can be found here.)

In advance of the September meeting, some other members of the FOMC had also signaled that the committee was unlikely to increase its target. For instance, an article in the Wall Street Journal quoted Susan Collins, president of the Federal Reserve Bank of Boston, as stating that: “The risk of inflation staying higher for longer must now be weighed against the risk that an overly restrictive stance of monetary policy will lead to a greater slowdown than is needed to restore price stability.” And in a speech in August, Raphael Bostic, president of the Federal Reserve Bank of Atlanta, explained his position on future rate increases: “Based on current dynamics in the macroeconomy, I feel policy is appropriately restrictive. I think we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain.”

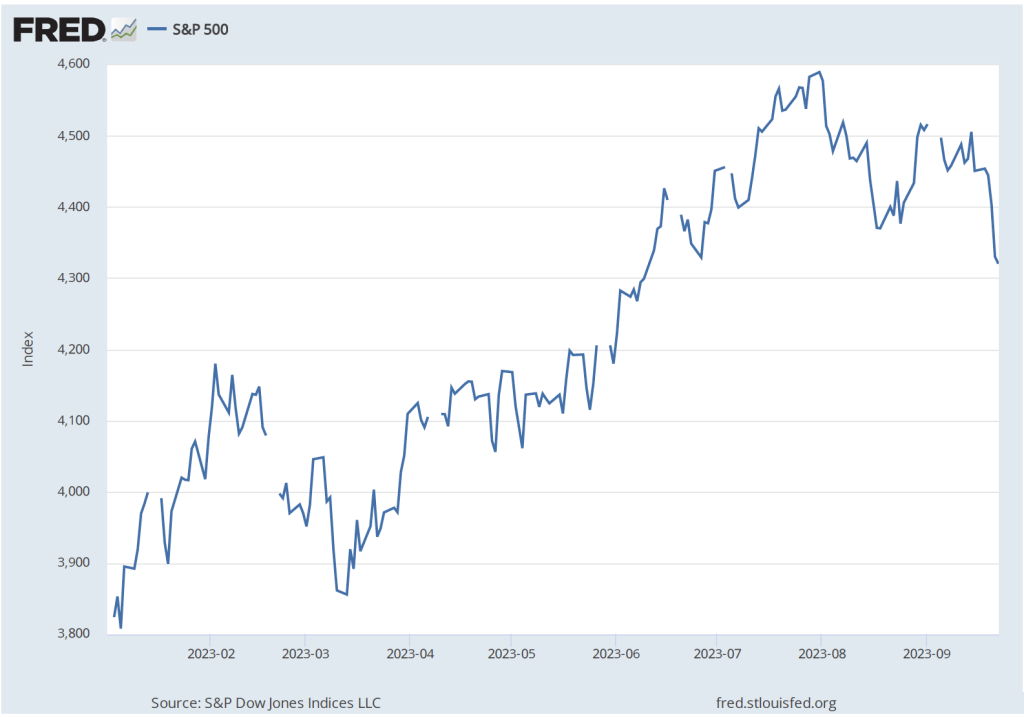

Although it wasn’t a surprise that the FOMCdecided to hold its target for the federal funds rate constant, after the decision was announced, stock and bond prices declined. The following figure shows the S&P 500 index of stock prices. The index declined 2.8 percent from September 19—the day before the FOMC meeting—to September 22—two days after the meeting. (We discuss indexes of stock prices in Macroeconomics, Chapter 6, Section 6.2; Economics, Chapter 8, Section 8.2; and Essentials of Economics, Chapter 8, Section 8.2.)

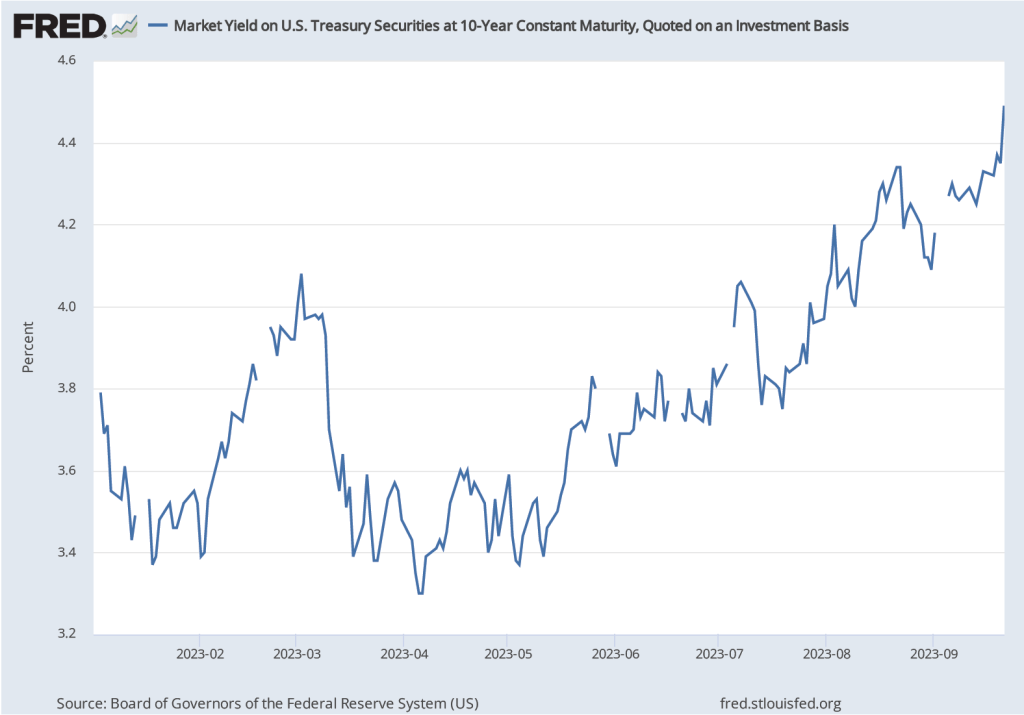

We see a similar pattern in the bond market. Recall that when the price of bonds declines in the bond market, the interest rates—or yields—on the bonds increase. As the following figure shows, the interest rate on the 10-year Treasury note rose from 4.37 percent on September 19 to 4.49 percent on September 21. The 10-year Treasury note plays an important role in the financial system, influencing interest rates on mortgages and corporate bonds. So, the yield on the 10-year Treasury note increasing from 3.3 percent in the spring of 2023 to 4.5 percent following the FOMC meeting has the effect of increasing long-term interest rates throughout the U.S. economy.

What explains the movements in the prices of stocks and bonds following the September FOMC meeting? Investors seem to have been surprised by: 1) what Chair Powell had to say in his news conference following the meeting; and 2) the committee members’ Summary of Economic Projections (SEP), which was released after the meeting.

Powell’s remarks were interpreted as indicating that the FOMC was likely to increase its target for the federal funds rate at least once more in 2023 and was unlikely to cut its target before late 2024. For instance, in response to a question Powell said: “We need policy to be restrictive so that we can get inflation down to target. Okay. And we’re going to need that to remain to be the case for some time.” Investors often disagree in their interpretations of what a Fed chair says. Fed chairs don’t act unilaterally because the 12 voting members of the FOMC decide on the target for the federal funds rate. So chairs tend to speak cautiously about future policy. Still, their seemed to be a consensus among investors that Powell was indicating that Fed policy would be more restrictive (or contractionary) than had been anticipated prior to the meeting.

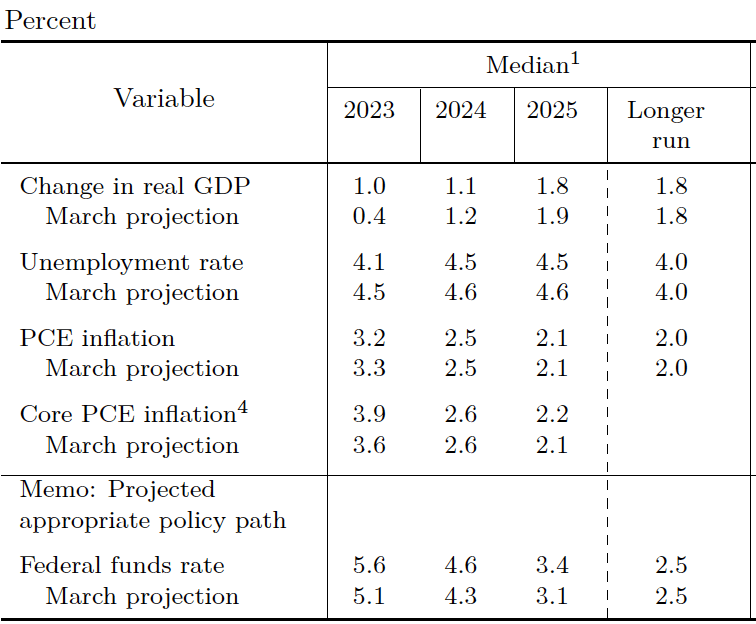

The FOMC releases the SEP four times per year. The most recent SEP before the September meeting was from the June meeting. The table below shows the median of the projections, or forecasts, of key economic variables made by the members of the FOMC at the June meeting. Note the second row from the bottom, which shows members’ median forecast of the federal funds rate.

The following table shows the median values of members’ forecast at the September meeting. Look again at the next to last row. The members’ forecast of the federal funds rate at the end of 2023 was unchanged. But their forecasts for the federal funds rate at the end of 2024 and 2025 were both 0.50 percent higher.

Why were members of the FOMC signaling that they expected to hold their target for the federal funds rate higher for a longer period? The other economic projections in the tables provide a clue. In September, the members expected that real GDP growth would be higher and the unemployment rate would be lower than they had expected in June. Stronger economic growth and a tighter labor market seemed likely to require them to maintain a contractionary monetary policy for a longer period if the inflation rate was to return to their 2.0 percent target. Note that the members didn’t expect that the inflation rate would return to their target until 2026.

Join authors Glenn Hubbard & Tony O’Brien as they discuss the economic landscape of inflation, soft-landings, and the green economy. This conversation occurred on Saturday, 9/16/23, prior to the FOMC meeting on September 19th-20th.

Inflation has declined, although many consumers are skeptical. What explains consumer skepticism? First we can look at what’s happened to inflation in the period since the beginning of 2015. The figure below shows inflation measured as the percentage change in the consumer price index (CPI) from the same month in the previous year. We show both so-called headline inflation, which includes the prices of all goods and services in the index, and core inflation, which excludes energy and food prices. Because energy and food prices can be volatile, most economists believe that the core inflation provides a better indication of underlying inflation.

Both measures show inflation following a similar path. The inflation rate begins increasing rapidly in the spring of 2021, reaches a peak in the summer of 2022, and declines from there. Headline CPI peaks at 8.9 percent in June 2022 and declines to 3.7 percent in August 2023. Core inflation reaches a peak of 6.6 percent in September 2022 and declines to 4.4 percent in August 2022.

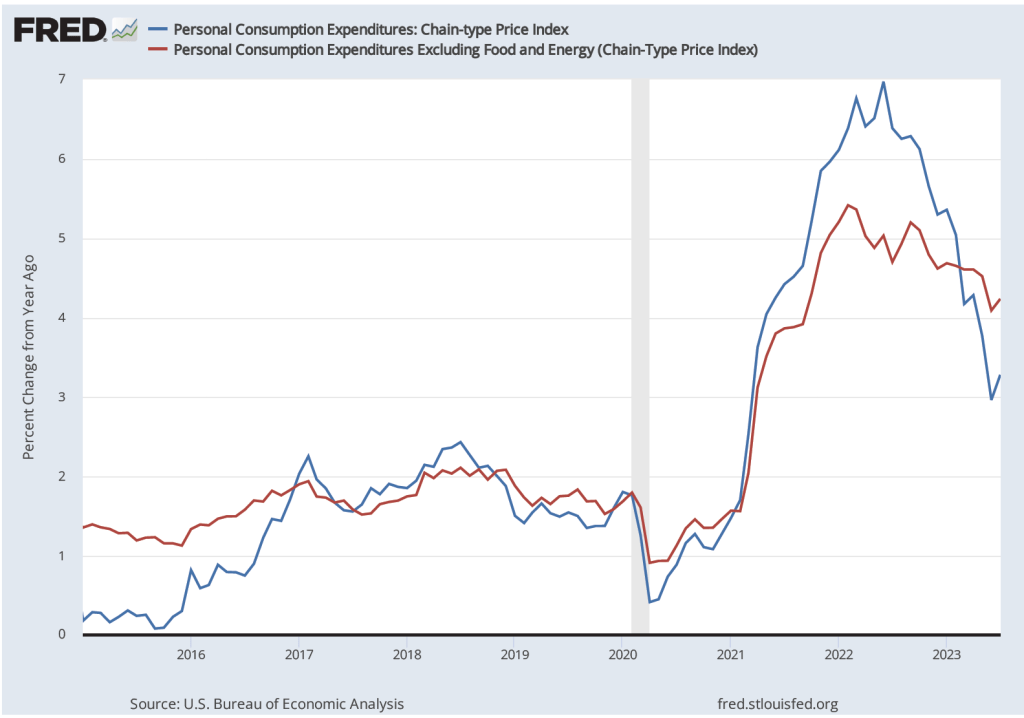

As we discuss in Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5, and Essentials of Economics, Chapter 17, Section 17.5), the Fed’s inflation target is stated in terms of the personal consumption expenditure (PCE) price index, not the CPI. The PCE includes the prices of all the goods and services included in the consumption component of GDP. Because the PCE includes the prices of more goods and services than does the CPI, it’s a broader measure of inflation. The following figure shows inflation as measured by the PCE and by the core PCE, which excludes energy and food prices.

Inflation measured using the PCE or the core PCE shows the same pattern as inflation measured using the CPI: A sharp increase in inflation in the spring of 2021, a peak in the summer of 2022, and a decline thereafter.

Although it has yet to return to the Fed’s 2 percent target, the inflation rate has clearly fallen substantially during the past year. Yet surveys of consumers show that majorities are unconvinced that inflation has been declining. A Pew Research Center poll from June found that 65 percent of respondents believe that inflation is “a very big problem,” with another 27 percent believing that inflation is “a moderately big problem.” A Gallup poll from earlier in the year found that 67 percent of respondents thought that inflation would go up, while only 29 percent thought it would go down. Perhaps not too surprisingly, another Gallup poll found that only 4 percent of respondents had a “great deal” of confidence in Federal Reserve Chair Jerome Powell, with another 32 percent having a “fair amount” of confidence. Fifty-four percent had either “only a little” confidence in Powell or “almost none.”

There are a couple of reasons why most consumers might believe that the Fed is doing worse in its fight against inflation than the data indicate. First, few people follow the data releases as carefully as economists do. As a result, there can be a lag between developments in the economy—such as declining inflation—and when most people realize that the development has occurred.

Probably more important, though, is the fact that most people think of inflation as meaning “high prices” rather than “increasing prices.” Over the past year the U.S. economy has experienced disinflation—a decline in the inflation rate. But as long as the inflation rate is positive, the price level continues to increase. Only deflation—a declining price level—would lead to prices actually falling. And an inflation rate of 3 percent to 4 percent, although considerably lower than the rates in mid-2022, is still significantly higher than the inflation rates of 2 percent or below that prevailed during most of the time since 2008.

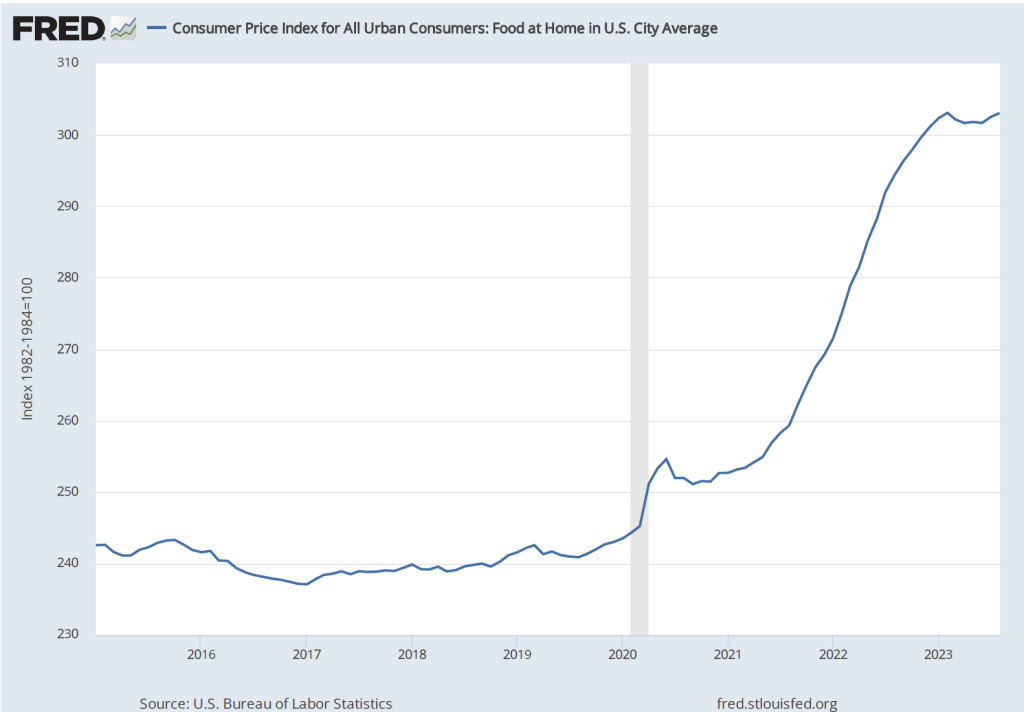

Although, core CPI and core PCE exclude energy and food prices, many consumers judge the state of inflation by what’s happening to gasoline prices and the price of food in supermarkets. These are products that consumers buy frequently, so they are particularly aware of their prices. The figure below shows the component of the CPI that represents the prices of food consumers buy in groceries or supermarkets and prepare at home. The price of food rose rapidly beginning in the spring of 2021. Althought increases in food prices leveled off beginning in early 2023, they were still about 24 percent higher than before the pandemic.

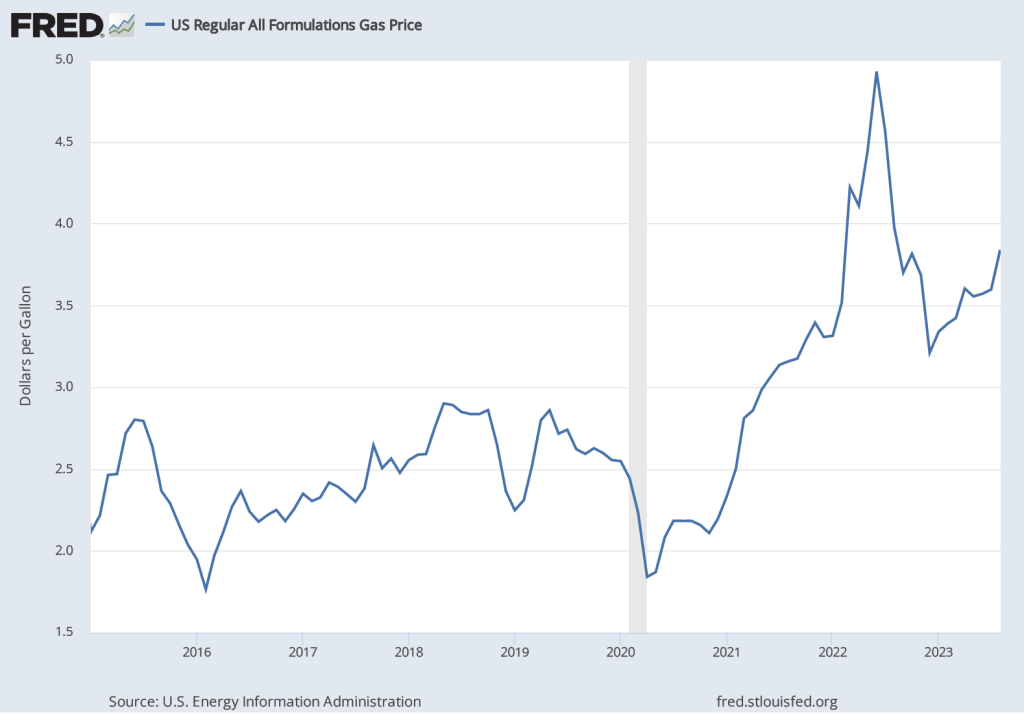

There is a similar story with respect to gasoline prices. Although the average price of gasoline in August 2023 at $3.84 per gallon is well below its peak of nearly $5.00 per gallon in June 2022, it is still well above average gasoline prices in the years leading up to the pandemic.

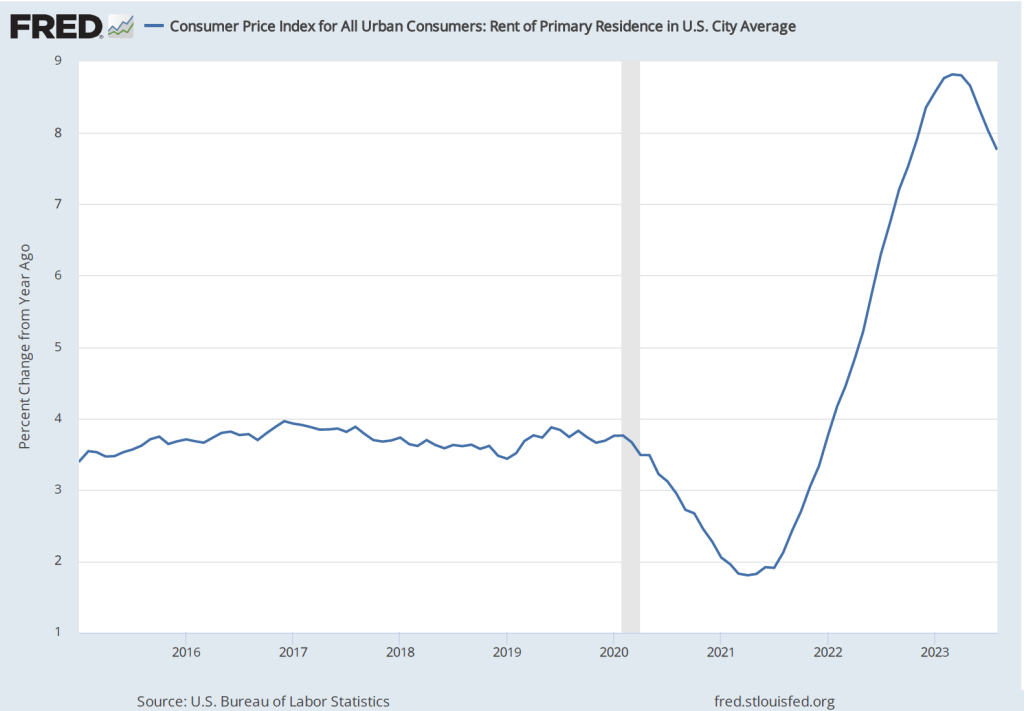

Finally, the figure below shows that while percentage increases in rent are below their peak, they are still well above the increases before and immediately after the recession of 2020. (Note that rents as included in the CPI include all rents, not just rental agreements that were entered into that month. Because many rental agreements, particularly for apartments in urban areas, are for one year or more, in any given month, rents as measured in the CPI may not accurately reflect what is currently happening in rental housing markets.)

Because consumers continue to pay prices that are much higher than the prices they were paying prior to the pandemic, many consider inflation to still be a problem. Which is to say, consumers appear to frequently equate inflation with high prices, even when the inflation rate has markedly declined and prices are increasing more slowly than they were.

A food market in Mexico. (Photo from mexperience.com)

Supports:Macroeconomics, Chapter 18, Economics, Chapter 28, and Essentials of Economics, Chapter 19.

In September 2023, an article in the Los Angeles Times discussed the effects on Mexico of the “’super-peso,’ as the Mexican currency has been dubbed since steadily gaining 18% on the dollar during the last 12 months.” The article focused on the effects of the rising value of the peso on people in Mexico who receive U.S. dollars from relatives and friends working in the United States. Many of the people who receive these payments rely on them to buy basic necessities, such as food and clothing. An article in the Wall Street Journal on the effects of the rising value of the peso noted that: “The peso’s strength has helped curtail inflation ….”

Briefly explain what the Los Angeles Times article means by the peso “gaining” on the U.S. dollar? Does the peso gaining on the dollar mean that someone exchanging dollars for pesos would receive more pesos or fewer pesos?

As a result of the rising value of the peso would people in Mexico receiving dollar payments from relatives in the United States be better off or worse off? Briefly explain.

Why would the increasing strength of the peso reduce the inflation rate in Mexico?

The Los Angeles Times article also noted that: “The Bank of Mexico’s benchmark interest rate of 11.25% is more than double the U.S. Federal Reserve target …” Does this fact have anything to do with the increase in the value of the peso in exchange for the dollar? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the effect of fluctuations in the exchange rate and the relationship between interest rates and exchange rates, so you may want to review Macroeconomics, Chapter 18, Section 8.2, “The Foreign Exchange Market and Exchange Rates,” or the corresponding sections in Economics, Chapter 28 or Essentials of Economics, Chapter 19.

Step 2:Answer part a. by explaining what it means for the peso to be “gaining” on the U.S. dollar. The peso gaining on the dollar means that someone can exchange fewer pesos to receive a dollar. Or, alternatively, someone exchanging dollars for pesos will receive fewer pesos.

Step 3: Answer part b. by explaining why people in Mexico receiving dollar payments from relatives in the United States will be worse off because of the rising value of the peso. People living in Mexico needs pesos to buy food and clothing from Mexican stores. Because people will receive fewer pesos in exchange for the dollars they receive from relatives in the United States, these people will have been made worse off by the rising value of the peso.

Step 4: Answer part c. by explaining why the increasing strength of the peso will reduce inflation in Mexico. A country’s inflation rate includes the prices of imported goods as well as the prices of domestically produced goods. A stronger peso means that fewer pesos are needed to buy the same quantity of a foreign currency, which reduces the peso price of imports from that country. For example, a stronger peso reduces the number of pesos Mexican consumers pay to buy $10 worth of cucumbers imported from the United States. Falling prices of imported goods will reduce the inflation rate in Mexico.

Step 5: Answer part d. by explaining why higher interest rates in Mexico relative to interest rates in the United States will increase the value of the peso in exchange for the U.S. dollar. If interest rates in Mexico rise relative to interest rates in the United States, Mexican financial assets, such as Mexican government bonds, will be more desirable, causing investors to increase their demand for the pesos they need to buy Mexican financial assets. The resulting shift to the right in the demand curve for pesos will cause the equilibrium exchange rate between the peso and the dollar to increase.

Sources: Patrick J. McDonnell, “Mexico’s Peso Is Soaring. That’s Bad News for People Who Rely on Dollars Sent from the U.S.,” Los Angeles Times, September 5, 2023; and Anthony Harrup, “Mexico’s Peso Surges to Strongest Level Since 2015,” Wall Street Journal, July 13, 2023.

During 2023, GDP and employment have continued to expand. Between the second quarter of 2022 and the second quarter of 2023, nominal GDP increased by 6.1 percent. From July 2022 to July 2023, total employment increased by 3.3 million as measured by the establishment (or payroll) survey and by 3.0 as measured by the household survey. (In this post, we discuss the differences between the employment measures in the two surveys.)

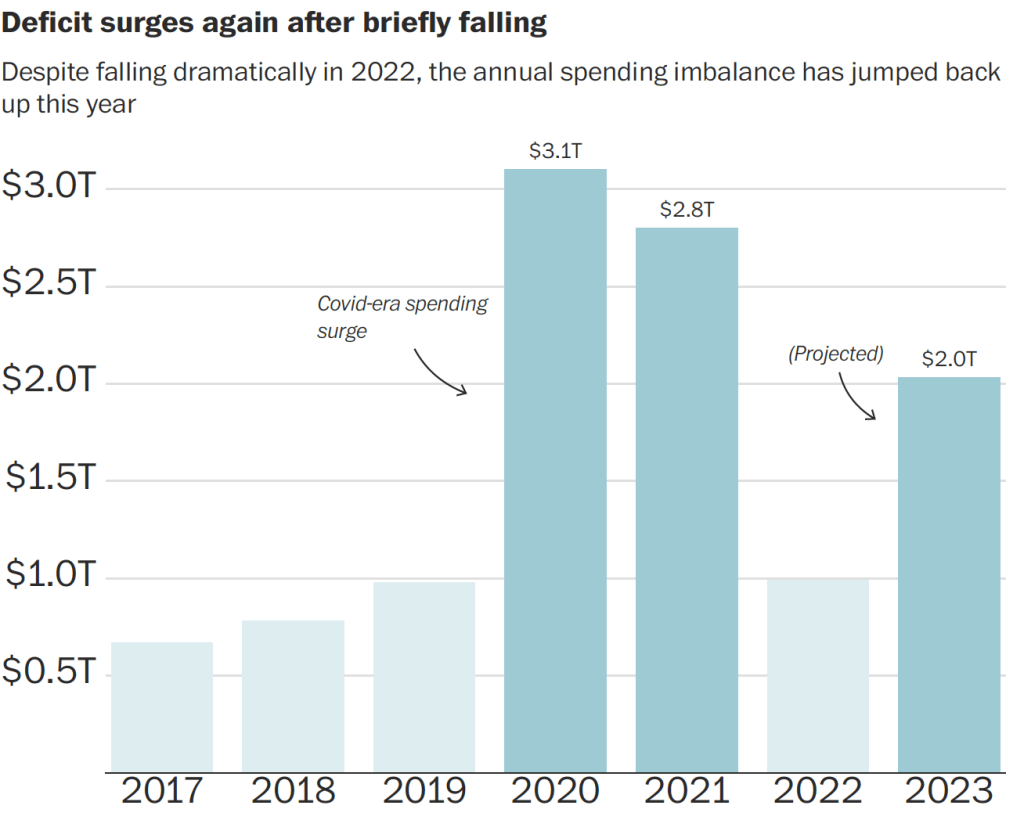

We would expect that with an expanding economy, federal tax revenues would rise and federal expenditures on unemployment insurance and other transfer programs would decline, reducing the federal budget deficit. (We discuss the effects of the business cycle on the federal budget deficit in Macroeconomics, Chapter 16, Section 16.6, Economics, Chapter 26, Section 26.6, and Essentials of Economics, Chapter 18, Section 18.6.) In fact, though, as the figure from the Congressional Budget Office (CBO) at the top of this post shows, the federal budget deficit actually increased substantially during 2023 in comparison with 2022. The federal budget deficit from the beginning of government’s fiscal year on October 1, 2022 through July 2023 was $1,617 billion, more than double the $726 billion deficit during the same period in fiscal 2022.

The following figure from an article in the Washington Post uses data from the Committee for a Responsible Federal Budget to illustrate changes in the federal budget deficit in recent years. The figure shows the sharp decline in the federal budget deficit in 2022 as the economic recovery from the Covid–19 pandemic increased federal tax receipts and reduced federal expenditures as emergency spending programs ended. Given the continuing economic recovery, the surge in the deficit during 2023 was unexpected.

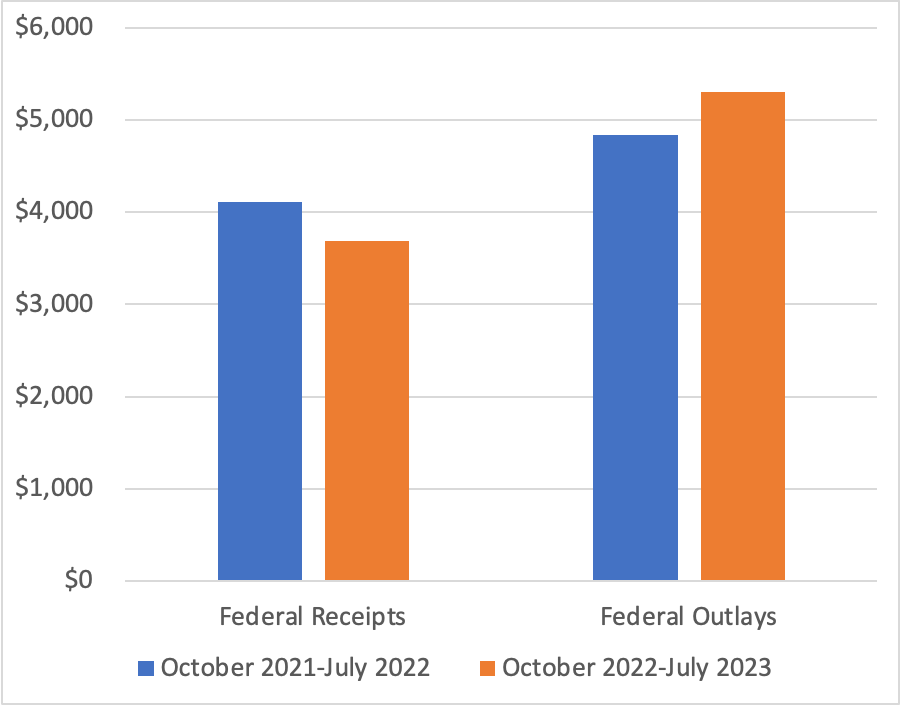

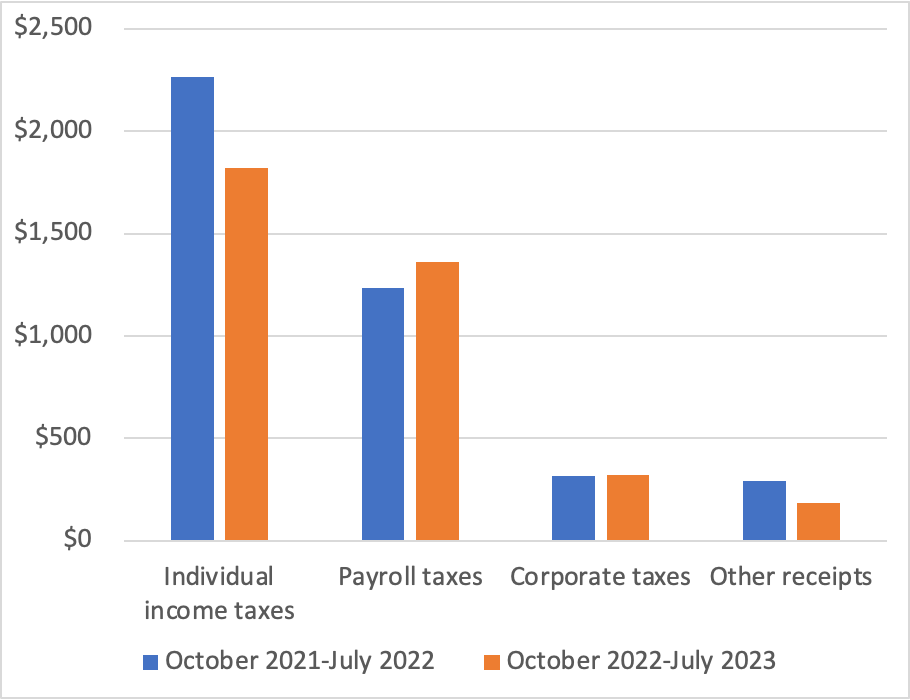

As the following figure shows, using CBO data, federal receipts—mainly taxes—are 10 percent lower this year than last year, and federal outlays—including transfer payments—are 11 percent higher. For receipts to fall and outlays to increase during an economic expansion is very unusual. As an article in the Wall Street Journal put it: “Something strange is happening with the federal budget this year.”

Note: The values on the vertical axis are in billions of dollars.

The following figure shows a breakdown of the decline in federal receipts. While corporate taxes and payroll taxes (primarily used to fund the Social Security and Medicare systems) increased, personal income tax receipts fell by 20 percent, and “other receipts” fell by 37 percent. The decline in other receipts is largely the result of a decline in payments from the Federal Reserve to the U.S. Treasury from $99 billion in 2022 to $1 billion in 2023. As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), Congress intended the Federal Reserve to be independent of the rest of the government. Unlike other federal agencies and departments, the Fed is self-financing rather than being financed by Congressional appropriations. Typically, the Fed makes a profit because the interest it earns on its holdings of Treasury securities is more than the interest it pays banks on their reserve deposits. After paying its operating costs, the Fed pays the rest of its profit to the Treasury. But as the Fed increased its target for the federal funds rate beginning in March 2022, it also increased the interest rate it pays banks on their reserve deposits. Because most of the securities it holds pay low interest rates, the Fed has begun running a deficit, reducing the payments it makes to the Treasury.

Note: The values on the vertical axis are in billions of dollars.

The reasons for the sharp decline in individual income taxes are less clear. The decline was in the “nonwithheld category” of individual income taxes; federal income taxes withheld from worker paychecks increased. People who are self-employed or who receive substantial income from sources such as capital gains from selling stocks, make quarterly estimated income tax payments. It’s these types of personal income taxes that have been unexpectedly low. Accordingly, smaller capital gains may be one explanation for the shortfall in federal revenues, but a more complete explanation won’t be possible until more data become available later in the year.

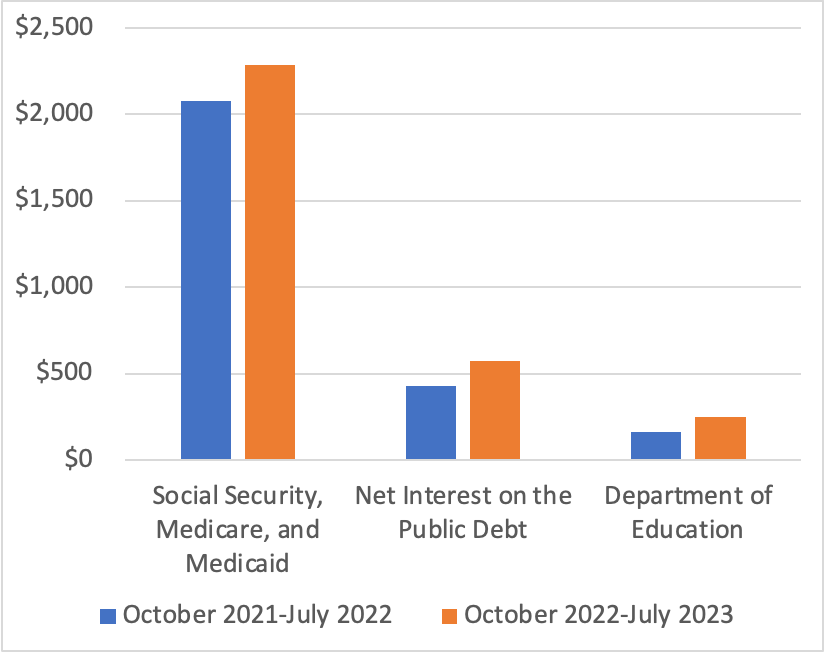

The following figure shows the categories of federal outlays that have increased the most from 2022 to 2023. The largest increase is in spending on Social Security, Medicare, and Medicaid, with spending on Social Security alone increasing by $111 billion. This increase is due partly to an increase in the number of retired workers receiving benefits and partly to the sharp rise in inflation, because Social Security is indexed to changes in the consumer price index (CPI). Spending on Medicare increased by $66 billion or a surprisingly large 18 percent. Interest payments on the public debt (also called the federal government debt or the national debt) increased by $146 billion or 34 percent because interest rates on newly issued Treasury securities rose as nominal interest rates adjusted to the increase in inflation and because the public debt had increased significantly as a result of the large budget deficits of 2020 and 2021. The increase in spending by the Department of Education reflects the effects of the changes the Biden administration made to student loans eligible for the income-driven repayment plan. (We discuss the income-driven repayment plan for student loans in this blog post.)

Note: The values on the vertical axis are in billions of dollars.

The surge in federal government outlays occurred despite a $120 billion decline in refundable tax credits, largely due to the expiration of the expansion of the child tax credit Congress enacted during the pandemic, a $98 billion decline in Treasury payments to state and local governments to help offset the financial effects of the pandemic, and $59 billion decline in federal payments to hospitals and other medical facilities to offset increased costs due to the pandemic.

In this blog post from February, we discussed the challenges posed to Congress and the president by the CBO’s forecasts of rising federal budget deficits and corresponding increases in the federal government’s debt. The unexpected expansion in the size of the federal budget deficit for the current fiscal year significantly adds to the task of putting the federal government’s finances on a sound basis.