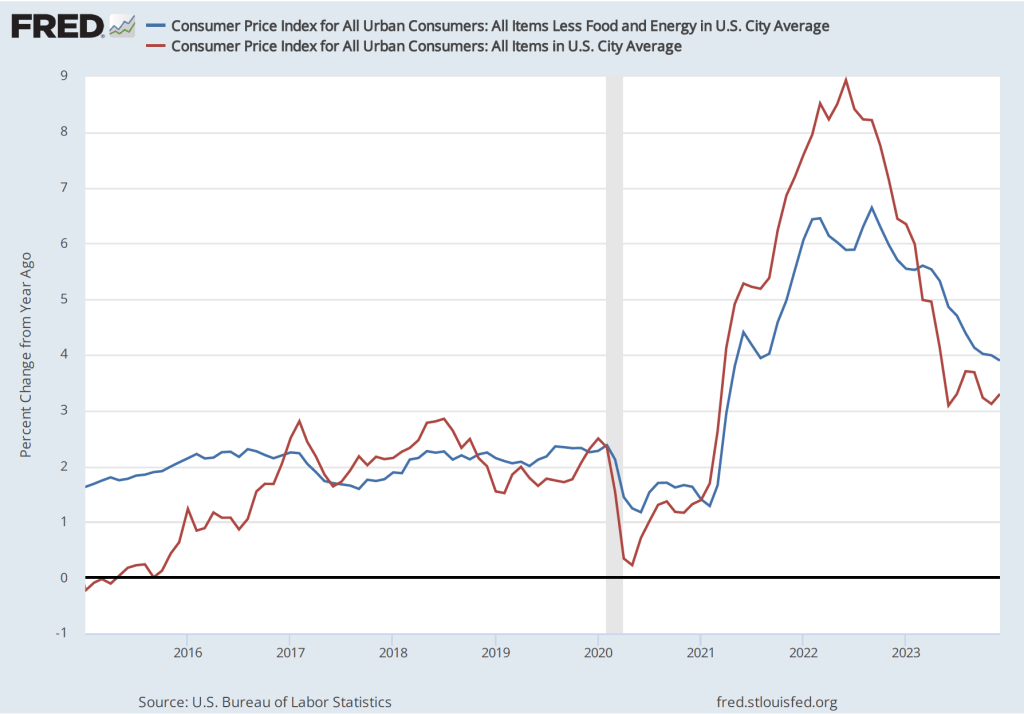

On the morning of January 11, 2024, the Bureau of Labor Statistics released its report on changes in consumer prices during December 2023. The report indicated that over the period from December 2022 to December 2023, the Consumer Price Index (CPI) increased by 3.4 percent (often referred to as year-over-year inflation). “Core” CPI, which excludes prices for food and energy, increased by 3.9 percent. The following figure shows the year-over-year inflation rate since Januar 2015, as measured using the CPI and core CPI.

This report was consistent with other recent reports on the CPI and on the personal consumption expenditures (PCE) price index—the measure the Fed uses to gauge whether it is achieving its target of 2 percent annual inflation—in showing that inflation has declined substantially from its peak in mid-2022 but is still above the Fed’s target.

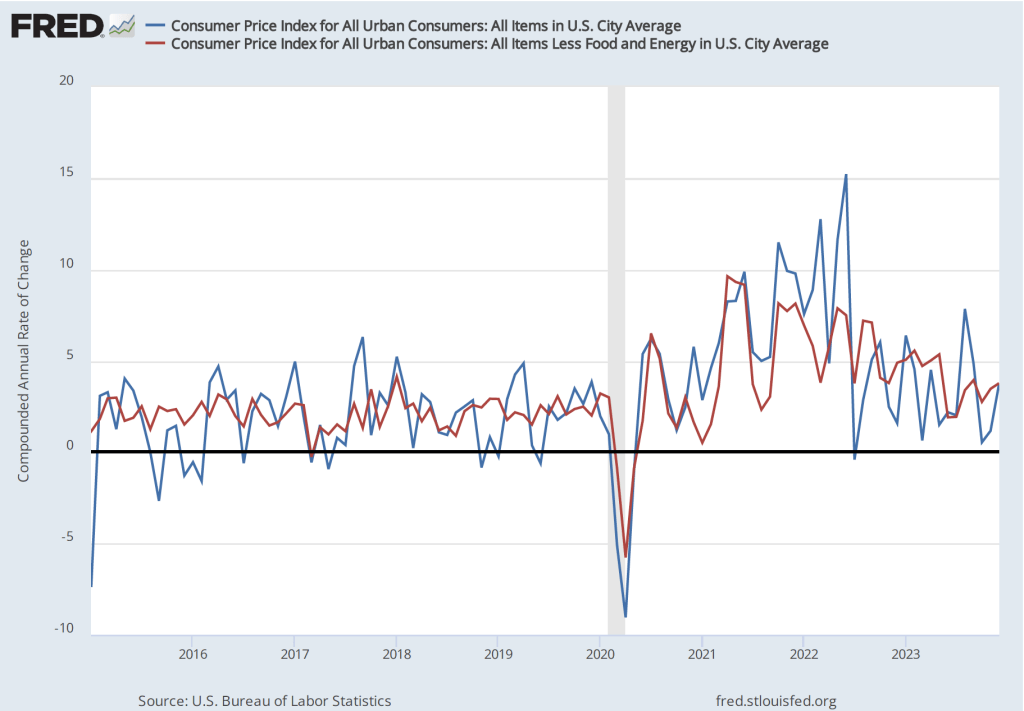

We get a similar result if we look at the 1-month inflation rate—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—as the following figure shows. The 1-month CPI inflation rate has moved erratically but has generally trended down. The 1-month core CPi inflation rate has moved less erratically, making the downward trend since mid-2022 clearer.

The headline on the Wall Street Journalarticle discussing this BLS report was: “Inflation Edged Up in December After Rapid Cooling Most of 2023.” The headline reflected the reaction of Wall Street investors who had hoped that the report would unambiguously show further slowing in inflation.

Overall, the report was middling: It didn’t show a significant acceleration in inflation at the end of 2023 but neither did it show a signficant slowing of inflation. At its next meeting on January 30-31, the Fed’s Federal Open Market Committee (FOMC) is expected to keep its target for the federal funds rate unchanged. There doesn’t appear to be anything in this inflation report that would be likely to affect the committee’s decision.

Agents from the National Transportation Safety Board inspect a piece of the Boeing jetliner found in a backyard in Portland, Oregon. (Photo from the AP via the New York Times.)

What causes movements in stock prices? As we explain in Economics and Microeconomics, Chapter 8, Section 8.2 (Macroeconomics, Essentials of Economics, and Money, Banking, and the Financial System, Chapter 6, Section 6.2): “Shares of stock represent claims on the profits of the firms that issue them. As the fortunes of the firms change and they earn more or less profit, the prices of the stock the firms have issued should also change.”

We also note that: “Many Wall Street investment professionals expend a great deal of effort gathering all possible information about the future profitability of firms, hoping to buy the stocks that are most likely to rise in the future. As a result of the actions of these professional investors, all of the information about a firm that is available on news and financial websites, cable TV business shows, and online discussion sites like X and Reddit is already reflected in the firm’s stock price.” As a consequence, the price of a firm’s stock will change only as a result of new information about the future profitability of the firm issuing the stock.

During the course of a typical week, the new information that becomes available about a large company, like Apple or General Motors, is likely to indicate only minor changes in the future profitability of the firm. Therefore, we wouldn’t expect that the firm’s stock price would change very much. Sometimes, though, investors receive important new information that causes them to significantly revise their expectations of the future profitability of a firm. That’s what happened to Boeing, the jetliner manufacturer, on Friday, January 5. An Alaska Air Boeing 737 Max 9 was taking off from Portland International Airport when a piece of the plane blew out. (A Wall Street Journalarticle gives the details of the incident.)

The accident caused some industry observers to question whether Boeing’s quality control during manufacturing had deficiencies that might lead to other problems being discovered on the firm’s jetliners. Boeing was particularly at risk of having its quality control methods questioned because in 2019 two slightly different models of the 737 Max airliner had crashed, causing the planes to be grounded for almost two years.

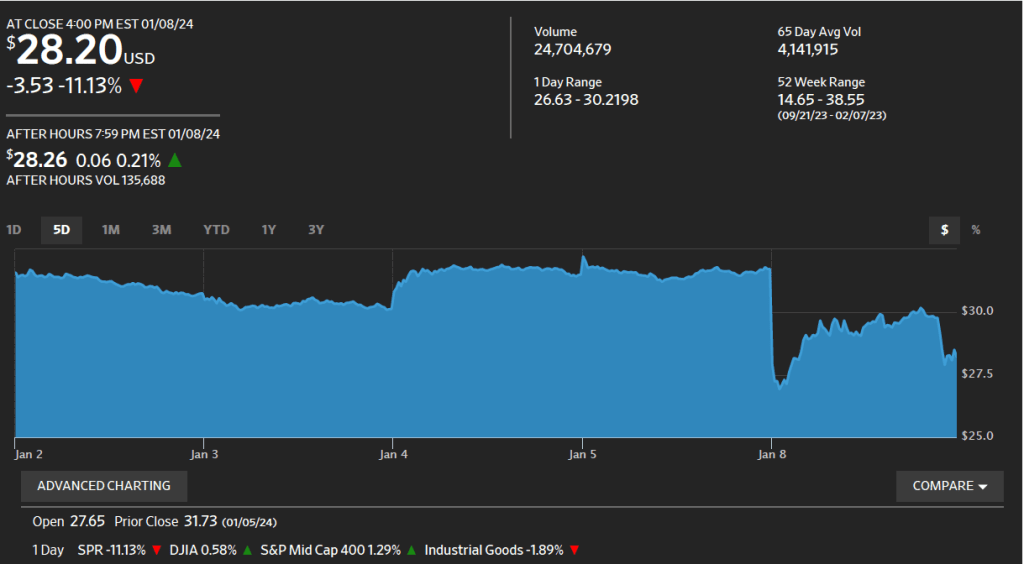

The effect of the Alaska Air incident on Boeing’s stock price can be seen in the following figure, reproduced from the Wall Street Journal. On Friday, January 5 at 4 pm eastern time—the time at which trading on the New York Stock Exchange (NYSE) closes for the day—the price of Boeing’s stock was $249.00 per share. The accident took place at around 7:40 pm eastern time, so it occurred after the close of trading on the NYSE. When trading on the NYSE resumed at 9:30 am on Monday, January 8, Boeing’s stock price had declined to $227.79 per share. The size of the drop in price indicated that investors believed that the Portland accident would have a significantly negative affect on Boeing’s future profitability. Boeing’s profits could fall if the accident leads airlines to reduce their future purchases of 737 Max airliners or if Boeing’s costs rise significantly as a result of making repairs on Max airliners currently in servide or as a result of having to spend more on quality control measures when manufacturing the planes.

The effect of the Portland accident on Boeing’s stock price is an example of the efficiency of the stock market in processing information about a firm’s future profitability.

Glenn participated in this session hosted by the Society of Policy Modeling and the American Economic Association of Economic Educators and moderated by Dominick Salvatore of Fordham University. (Link to the page for this session in the ASSA program.)

Also making presentations at the session were Robert Barro of Harvard University, Janice Eberly of Northwestern University, Kenneth Rogoff of Harvard University, and John Taylor of Stanford University.

Here is the abstract for Glenn’s presentation:

Economic growth is foundational for living standards and as an objective for economic policy. The emergence of Artificial Intelligence as a General Purpose Technology, on the one hand, and a number of demographic and budget challenges, on the other hand, generate an unusually wide range of future economic outcomes. I focus on key ‘policy’ and ‘political economy’ considerations that increase the likelihood of a more favorable growth path given pre-existing trends and technological possibilities. By ‘policy,’ I consider mechanisms enabling growth through research, taxation, the scope of regulation, and competition. By ‘political economy’ factors, I consider mechanisms to increase economic participation in support of growth and policies that enhance it. I argue that both sets of mechanisms are necessary for a viable pro-growth economic policy framework.

These slides from the presentation highlight some of Glenn’s key points. (Note the cover of the new 9th edition of the textbook in slide 7!)

Glenn participated in this session hosted by the National Association of Economic Educators and moderated by Kim Holder of the University of West Georgia. Glenn thanks Kim for organizing the session and for inviting him to participate.

Here is the session abstract and the list of participants:

Glenn prepared some slides for his presentation. Note that “B01″ and B02” were the titles when he first taught principles of economics as an assistant professor at Northwestern. (We won’t mention how long ago that was!)

During the last few months of 2023, the macroeconomic data has generally been consistent with the Federal Reserve successfully bringing about a soft landing: Inflation returning to the Fed’s 2 percent target without the economy entering a recession. On the morning of Friday, January 5, the Bureau of Labor Statistics (BLS) issued its latest “Employment Situation Report” for December 2023. The report was generally consistent with the economy still being on course for a soft landing, but because both employment growth and wage growth were stronger than expected, the report makes it somewhat less likely that the Federal Reserve’s Federal Open Market Committee (FOMC) will soon begin reducing its target for the federal funds rate. (The full report can be found here.)

Economists and policymakers—notably including the members of the FOMC—typically focus on the change in total nonfarm payroll employment as recorded in the establishment, or payroll, survey. That number gives what is generally considered to be the best gauge of the current state of the labor market.

The report indicated that during December there had been a net increase of 216,000 jobs. This number was well above the expected gain of 160,000 to 170,000 jobs that several surveys of economists had forecast (see here, here, and here). The BLS revised downward by a total of 71,000 jobs its previous estimates for October and November, somewhat offsetting the surprisingly strong estimated increase in net jobs for December.

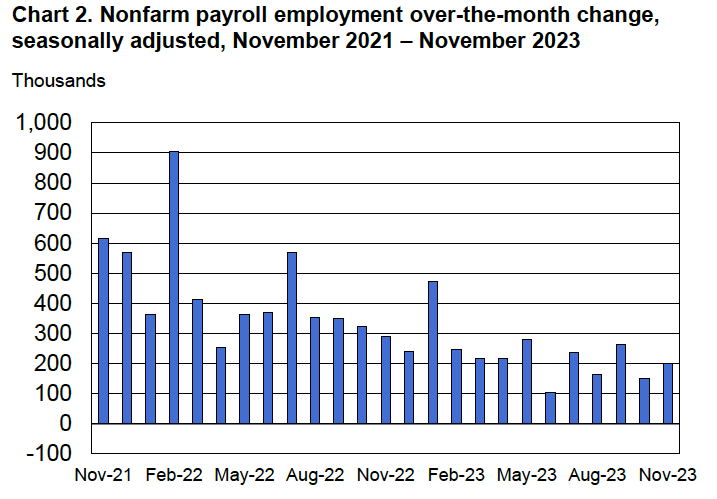

The following figure from the report shows the net increase in jobs each month since December 2021. Although the net number of jobs created has trended up from September to December, the longer run trend has been toward slower growth in employment. In the first half of 2023, an average of 257,000 net jobs were created per month, whereas in the second half of 2023, an average of 193,000 net jobs were created per month. Average weekly hours worked have also been slowly trending down, from 34.6 hours per week in January to 34.3 hours per week in December.

Economists surveyed were also expecting that the unemployment rate—calculated by the BLS from data gathered in the household survey—would increase slightly. Instead, it remained constant at 3.7 percent. As the following figure shows, the unemployment rate has been below 4.0 percent each month since December 2021. The members of the FOMC expect that the unemployment rate during 2024 will be 4.1 percent. (The most recent economic projections of the members of the FOMC can be found here.)

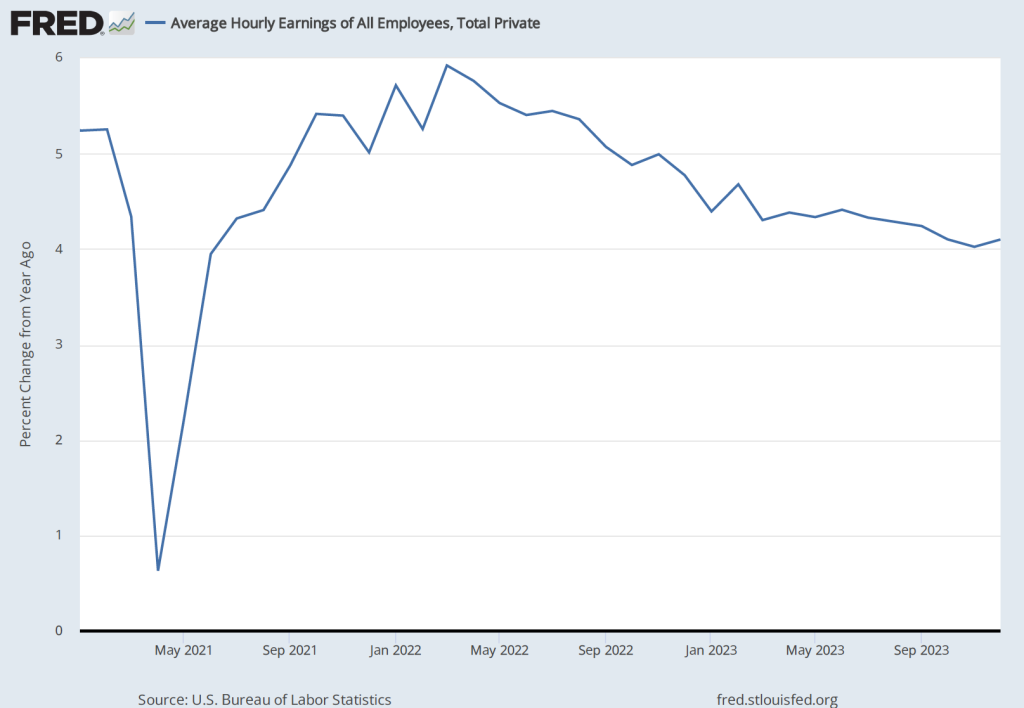

Although the employment data indicate that conditions in the labor market are easing in a way that may be consistent with inflation returning to the Fed’s 2 percent target, the data on wage growth are so far sending a different message. Average hourly earnings—data on which are collected in the establishment survey—increased by 4.1 percent in December compared with the same month in 2022. This rate of increase was slightly higher than the 4.0 percent increase in November. The following figure shows movements in the rate of increase in average hourly earnings since January 2021.

In his press conference following the FOMC’s December 13, 2023 meeting, Fed Chair Jerome Powell noted that increases in wages at 4 percent or higher were unlikely to result in inflation declining to the Fed’s 2 percent goal:

“So wages are still running a bit above what would be consistent with 2 percent inflation over a long period of time. They’ve been gradually cooling off. But if wages are running around 4 percent, that’s still a bit above, I would say.”

The FOMC’s next meeting is on January 30-31. At this point it seems likely that the committee will maintain its current target for the federal funds. The data in the latest employment report make it somewhat less likely that the committee will begin reducing its target at its meeting on March 19-20, as some economists and some Wall Street analysts had been expecting. (The calendar of the FOMC’s 2024 meetings can be found here.)

In recent months, the macroeconomic data has generally been consistent with the Federal Reserve successfully bringing about a soft landing: Inflation returning to the Fed’s 2 percent target without the economy entering a recession. The Bureau of Labor Statistics’ latest Employment Situation Report, released on the morning of Friday, December 8, was consistent with this trend. (The full report can be found here.)

Economists and policymakers—notably including the members of the Federal Reserve’s Federal Open Market Committee (FOMC)—typically focus on the change in total nonfarm payroll employment as recorded in the establishment, or payroll, survey. That number gives what is generally considered to be the best gauge of the current state of the labor market.

The report indicated that during November there had been a net increase of 199,000 jobs. This number was somewhat above the expected gain of 153,000 jobs Reuters news service reported from its survey of economists and just slightly above an expected gain of 190,000 jobs the Wall Street Journal reported from a separate survey of economists. The BLS revised downward by 35,000 jobs its previous estimate for September. It left its estimate for October unchanged. The following figure from the report shows the net increase in jobs each month since November 2021.

Because the BLS often substantially revises its preliminary estimates of employment from the establishment survey, it’s important not to overinterpret data for a single month or even for a few months. But general trends in the data can give useful information on changes in the state of the labor market. The estimate for November is the fourth time in the past six months that employment has increased by less than 200,000. Prior to that, employment had increased by more than 200,000 every month since January 2021.

Although the rate of job increases is slowing, it’s still above the rate at which new entrants enter the labor market, which is estimated to be roughly 90,000 people per month. The additional jobs are being filled in part by increased employment among people aged 25 to 54—so-called prime-age workers. (We discuss the employment-population ratio in Macroeconomics, Chapter 9, Section 9.1, Economics, Chapter 19, Section 9.1, and Essentials of Economics, Chapter 13, Section 13.1.) As the following figure shows, the employment-population ratio for prime-age workers remains above its level in early 2020, just before the spread of the Covid–19 pandemic in the United States.

The estimated unemployment rate, which is collected in the household survey, was down slightly from 3.9 percent to 3.7 percent. A shown in the following figure, the unemployment rate has been below 4 percent every month since February 2022.

The Employment Situation Report also presents data on wages, as measured by average hourly earnings. The growth rate of average hourly earnings, measured as the percentage change from the same month in the previous year, continued its gradual decline, as shown in the following figure. As a result, upward pressure on prices from rising labor costs is easing. (Keep in mind, though, as we note in this blog post, changes in average hourly earnings have shortcomings as a measure of changes in the costs of labor to businesses.)

Taken together, the data in the latest employment report indicate that the labor market is becoming less tight, reflecting a gradual slowing in U.S. economic growth. The data are consistent with the U.S. economy approaching a soft landing. It’s still worth bearing in mind, of course, that, as Fed Chair Jerome Powell continues to caution, there’s no certainty that inflation won’t surge again or that the U.S. economy won’t enter a recession.

The meeting room of the FOMC in the Federal Reserve building in Washington, DC.

As we’ve noted in several recent posts, the inflation rate has fallen significantly from its peak in mid-2022, as U.S. economic growth has been slowing and the labor market appears to be less tight, slowing the growth of wages. Some economists and policymakers now believe that by early 2024, inflation will approach the Fed Reserve’s 2 percent inflation target. At that point, the Fed’s Federal Open Market Committee (FOMC) is likely to turn its attention from inflation to making sure that the U.S. economy doesn’t slip into a recession.

Accordingly, both economists and financial market participants have begun to anticipate the point at which the FOMC will begin to cut its target for the federal funds rate. (One note of caution: Fed Chair Jerome Powell has made clear that the FOMC stands ready to further increase its target for the federal funds rate if the inflation rate shows signs of increasing. He made this point most recently on December 1 in a speech at Spelman College in Atlanta.) There is currently an interesting disagreement between economists and investors over when the FOMC is likely to cut interest rates and by how much. We can see the views of investors reflected in the futures market for federal funds.

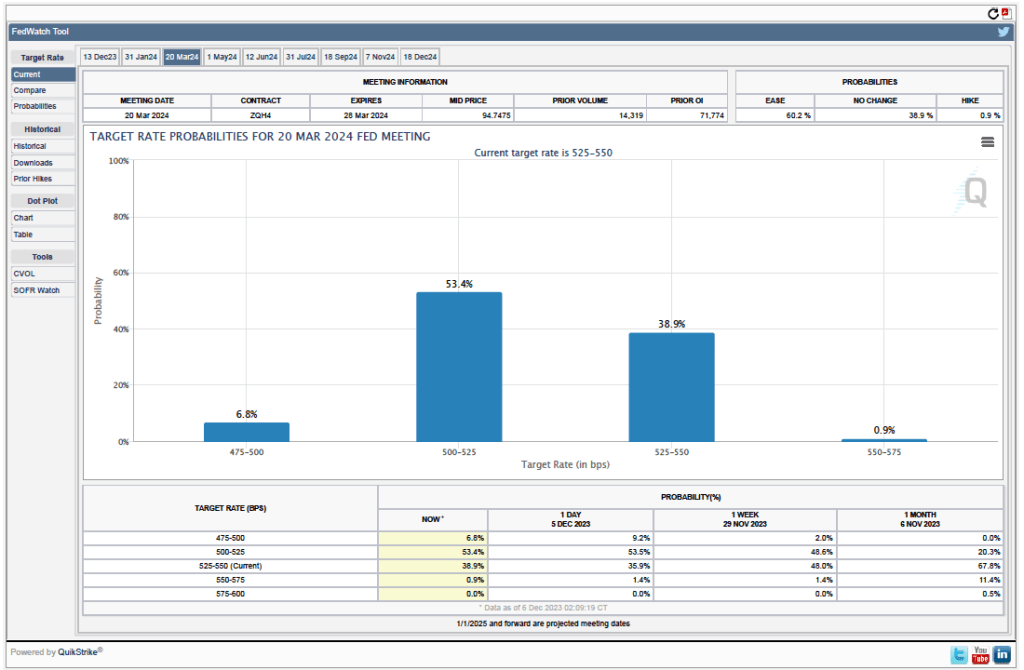

Futures markets allow investors to buy and sell futures contracts on commodities–such as wheat and oil–and on financial assets. Investors can use futures contracts both to hedge against risk—such as a sudden increase in oil prices or in interest rates—and to speculate by, in effect, betting on whether the price of a commodity or financial asset is likely to rise or fall. (We discuss the mechanics of futures markets in Chapter 7, Section 7.3 of Money, Banking, and the Financial System.) The CME Group was formed from several futures markets, including the Chicago Mercantile Exchange, and allows investors to trade federal funds futures contracts. The data that result from trading on the CME indicate what investors in financial markets expect future values of the federal funds rate to be. The following chart from the CME’s FedWatch Tool shows values after trading of federal funds futures on December 5, 2023.

The probabilities in the chart reflects investors’ predictions of what the FOMC’s target for the federal funds rate will be after the committee’s meeting on March 20, 2024. This meeting is the first after which investors currently expect that the target is likely to be lowered. The target range is currently 5.25 percent to 5.50 percent. The chart indicates that investors assign a probability of 60.2 percent to the FOMC making at least a 0.25 percentage cut in the target rate at the March meeting.

Looking at the values for federal funds futures after the FOMC’s December 18, 2024 meeting, investors assign a 66.3 percent probability of the committee having reduced its target for the federal funds rate to 4.00 to 4.25 percent of lower. In other words, investors expect that during 2024, the FOMC will have cut its target for the federal funds rate by at least 1.25 percentage points.

Interesingly, according to a survey by the Financial Times, economists disagree with investors’ forecasts of the federal funds rate. According to the survey, which was conducted between December 1 and December 4, nearly two-thirds of economists believe that the FOMC won’t cut its target for the federal funds rate until July 2024 or later. Three-quarters of the economists surveyed believe that the FOMC will cut its target by 0.5 percent point or less during 2024. Fewer than 10 percent of the economists surveyed believe that during 2024 the FOMC will cut its target for the federal funds rate by 1.25 percent or more. (The Financial Times article describing the results of the survey can be found here. A subscription may be requred to read the article.)

So, at least among the economists surveyed by the Financial Times, the consensus is that the FOMC will cut its target for the federal funds rate later and by less than financial markets are indicating. What explains the discrepancy? The main explanation is that economists see inflation being persistently above the Fed’s 2 percent target for longer than do financial market participants. The economists surveyed are also more optimistic that the U.S. economy will avoid a recession in 2024. If a recession occurs, the FOMC is more likely to significantly cut its target than if the economy during 2024 experiences moderate growth in real GDP and the unemployment rate remains low.

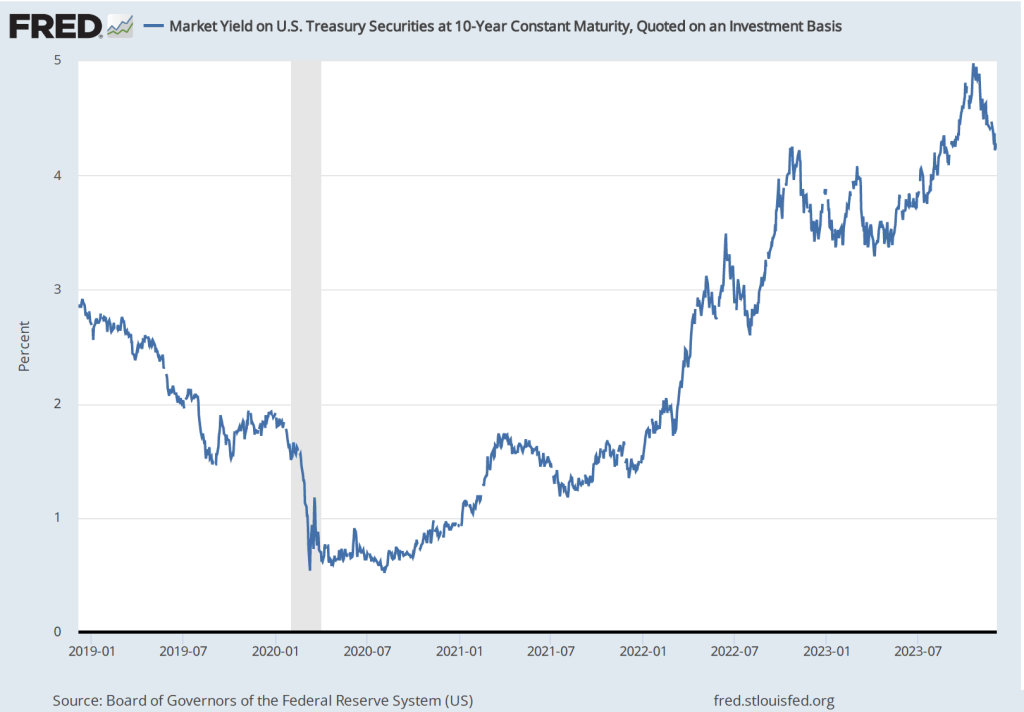

One other indication from financial markets that investors expect that the U.S. economy is likely to slow during 2024 is given by movements in the interest rate on the 10-year U.S. Treasury note. As shown in the following figure, from August to October of this year, the interest rate on the 10-year Treasury note rose from less than 4 percent to nearly 5 percent—an unusually large change in such a short period of time. Since then, most of that increase has been reversed with the interest rate on the 10-year Treasury note having fallen below 4.2 percent in early December

The movements in the interest rate on the 10-year Treasury note typically reflect investors’ expectations of future short-term interest rates. (We discuss the relationship between short-term and long-term interests rates—which economists call the term structure of interest rates—in Money, Banking, and the Financial System, Chapter 5, Section 5.2.) The increase in the 10-year interest rate between August and October reflected investors’ expectation that short-term interest rates were likely to remain persistently high for a considerable period—perhaps several years or more. The decline in the 10-year rate from late October to early December reflects investors changing their expectations toward future short-term interest rates being lower than they had previously thought. Again, as in the data on federal funds rate futures, investors seem to be expecting either slower economic growth or slower inflation than do economists.

One other complication about the interest rate on the 10-year Treasury note should be mentioned. Some of the increase in the rate from August to October may also have represented concern among investors that large federal budget deficit would cause the Treasury to issue more Treasury notes than investors would be willing to buy without the Treasury increasing the interest rate investors would receive on the newly issued notes. This concern may have been reinforced by data showing that foreign investors, particularly in China and Japan, appeared to have slowed or stopped adding to their holdings of Treasury notes. Part of the recent decline in the interest rate on the Treasury note may reflect investors becoming less concerned about these two factors.

Federal Reserve Chair Jerome Powell (photo from bloomberg.com)

In a blog post from February of this year, we discussed three possible outcomes of the contractionary monetary policy that the Federal Reserve has been pursuing since March 2022, when the Federal Open Market Committee (FOMC) began raising its target range for the federal funds rate:

A soft landing. The Fed’s preferred outcome; inflation returns to the Fed’s target of 2 percent without the economy falling into recession.

A hard landing. Inflation returns to the Fed’s 2 percent target, but the economy falls into a recession.

No landing. At the beginning of 2023, the unemployment remained very low and inflation, as measured by the percentage change in the personal consumption expenditures (PCE) price index from the same month in the previous year, was still above 5 percent. So, some observers, particularly in Wall Street financial firms, began discussing the possibility that low unemployment and high inflation might persist indefinitely, resulting an outcome of no landing.

At the end of 2023, the economy appears to be slowing: Retail sales declined in October; real disposable personal income increased in October, but it has been trending down, as have real personal consumption expenditures; while the increase in third quarter real GDP was recently revised upward from 4.9 percent to 5.2 percent, forecasts of growth in real GDP during the fourth quarter show a marked slowing—for instance, GDPNow, compiled by the Atlanta Fed, estimates fourth quarter growth at 2.1 percent; and while employment continues to expand, average weekly hours have been slowly declining and initial claims for unemployment insurance have been increasing.

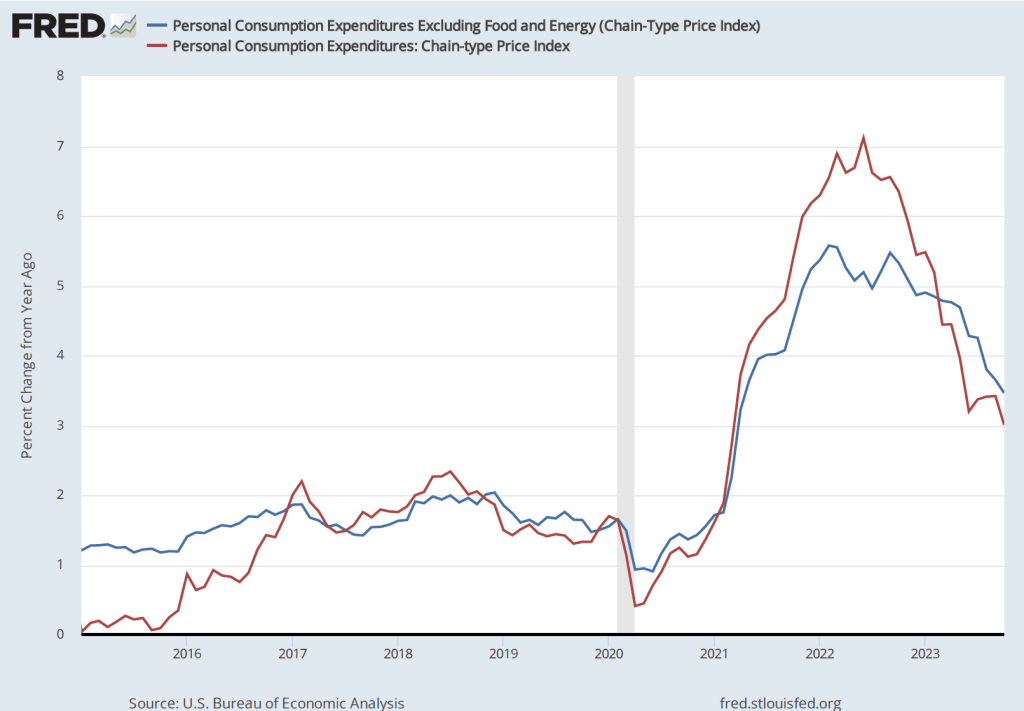

The slowing in the growth of output, income, and employment are reflected in a falling inflation rate. The following figure show the percentage change since the same month in the previous year in PCE price index, which is the measure the Fed uses to gauge whether it is hitting its 2 percent inflation target. (We discuss the reasons for the Fed preferring the PCE price index to the consumer price index (CPI) in Macroeconomics, Chapter 15, Section 15.5 and Economics, Chapter 25, Section 25.5.) The figure also shows core PCE, which excludes the prices of food and energy. Core PCE inflation typically gives a better measure of the underlying inflation rate than does PCE inflation.

PCE inflation declined from 3.4 percent in September to 3.0 percent in October. Core PCE inlation declined from 3.8 percent in September to 3.5 percent in September. Although inflation has been declining from its peak in mid-2022, both of these measures of inflation remain above the Fed’s 2 percent target.

But if we look at the 1-month inflation rate—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—we see a much sharper decline in inflation, as the following figure shows.

The 1-month inflation rate is naturally more volatile than the 12-month inflation rate. In this case, the 1-month rate shows a sharp decline in PCE inflation from 3.8 percent in September to 0.6 percent in October. Core PCE inflation declined less sharply from 3.9 percent in September to 2.0 percent in October.

The continuing decline in inflation has caused some economists and Wall Street analysts to predict that the FOMC will not implement further increases in its target for the federal funds rate and will likely begin cutting its target by mid-2024.

On December 1 in a speech at Spelman College in Atlanta, Fed Chair Jerome Powell urged caution in assuming that the Fed has succeeded in putting inflation on a course back to its 2 percent target:

“The FOMC is strongly committed to bringing inflation down to 2 percent over time, and to keeping policy restrictive until we are confident that inflation is on a path to that objective. It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so.”

In terms of the three policy outcomes listed at the beginning of this post, the third—no landing, with the unemployment rate remaining very low while the inflation rate remains above the Fed’s 2 percent target—now seems unlikely. The labor market appears to be weakening, which will likely result in increases in the unemployment rate. The next “Employment Report” from the Bureau of Labor Statistics, which will be released on December 8, will provide additional data on the state of the labor market.

Although we can’t entirely rule out the possibility of a no landing outcome, it seems more likely that the economy will either make a soft landing—if output and employment continue to increase, although at a slower rate, while inflation continues to decline—or a hard landing—if output and employment begin to fall as the economy enters a recession. Although a consensus seems to be building among economists, policymakers, and Wall Street analysts that a soft landing is the likeliest outcome, Powell has provided a reminder that that outcome is far from certain.

Federal Reserve Governor Christopher J. Waller (photo from the Associated Press via the Wall Street Journal)

Fed Governor Christopher Waller has a reputation for being a policy hawk, which means that since the spring of 2022 he has been a forceful advocate of multiple increases in the target for the federal funds rate as the Fed attempts to slow the economy and bring inflation back to the Fed’s 2 percent target. (Waller’s biography on the Fed’s web site can be found here.)

So, it was notable that in a speech at the American Enterprise Institute (AEI) on November 28, he said that “I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2 percent.” Although he also stressed that “there is still significant uncertainty about the pace of future activity, and so I cannot say for sure whether the [Federal Open Market Committee] FOMC has done enough to achieve price stability” his remarks were interpreted as reinforcing the growing view among non-Fed economists and investors that the FOMC is unlikely to increase its target for the federal funds rate further and is likely to reduce the target at some point during 2024. The text of Waller’s speech can be found here.

AEI economist Michael Strain interviewed Waller following his speech. In the interview (which can be found here), Strain made the case for believing that the Fed’s ability to achieve a soft landing—returning inflation to the 2 percent target without pushing the economy into a recession—would be more difficult than Waller seems to believe. Included in the interview are discussions of whether expecting a soft landing is consistent with the historical record, what guidance the Taylor rule can give to monetary policymakers (we discuss the Taylor rule in Macroeconomics, Chapter 15, Section 15.5, Economics, Chapter 25, Section 15.5, and Essentials of Economics, Chapter 17, Section 17.5), the significance of rising labor force participation rates among prime-age workers, and the implications large federal budget deficits have for monetary policy.

Earlier this month, Sam Bankman-Fried was convicted of fraud connected with the collapse of the FTX cryptocurrency exchange he founded. (We discuss aspects of cryptocurrencies in earlier blog posts here and here.) Bankman-Fried had a reputation for dressing casually and for having bushy, unkempt hair. In preparing for his trial, Bankman-Fried paid another inmate at the Metropolitan Detention Center in New York City to cut his hair short. According to an article in the Wall Street Journal, Bankman-Fried paid the other inmate not with currency but with four packets of mackerels—like the ones shown in the photo above—to cut his hair.

Although using packets of mackerels to buy and sell services may seem strange, in fact, packets of mackerel seem to be widely used in place of currency in the U.S. prison system. We explained the situation in an Apply the Concept in an earlier edition of our principles textbook. We reproduce that feature here. Note that the inmate quoted indicates that the price of a haircut at that time was only two mackerel packets rather than the four that Bankman-Fried paid. (Question to consider: Would we expect that prices of services in terms of mackerel packets would be the same across prisons at a given time or in the same prison over time?)

The Mackerel Economy in the Federal Prison System

Inmates of the federal prison system are not allowed to have money. Funds they earn working in the prison or receive from friends and relatives are placed in an account they can draw on to buy snacks and other items from the prison store. Lacking money, prisoners could barter with each other in exchanging goods and services, but we have seen that barter is inefficient. Since about 2004, in many prisons small plastic packets of mackerel fillets costing about $1 each have been used as money. [According to the Wall Street Journal article linked to earlier, the mackerel packets now sell for $1.30.] The packets are known in prison as “macks.”

Some prisoners have set up small businesses using mackerel packets for money. They sell services such as shoe shines, cell cleaning, or haircuts for macks. According to a prisoner in Lompoc prison in California, “A haircut is two macks.” A former prisoner described a fellow prisoner’s food business: “I knew a guy who would buy ingredients and use the microwaves to cook meals. Then people used mack to buy it from him.” In the Pensacola prison in Florida, the prison commissary was open only one day a week. So, several prisoners would run “prison 7-Elevens” by stocking up on goods and reselling them for macks at a profit. Very few prisoners actually eat the mackerel in the packets. In fact, apart from prison commissaries, the demand for mackerel in the United States is very small.

The mackerel economy is under pressure at some prisons, where rules exist against hoarding goods from the commissary. Prisoners caught dealing in macks can risk no longer being allowed to use the commissary or may be moved to a less desirable cell. In these prisons, the mackerel economy has been pushed underground.

The prison mackerel economy illustrates an important fact about money: Anything can be used as money, as long as people are willing to accept it in exchange for goods and services—even pouches of fish that no one wants to eat.

Source: Justin Scheck, “Mackerel Economics in Prison,” Wall Street Journal, October 2, 2008.