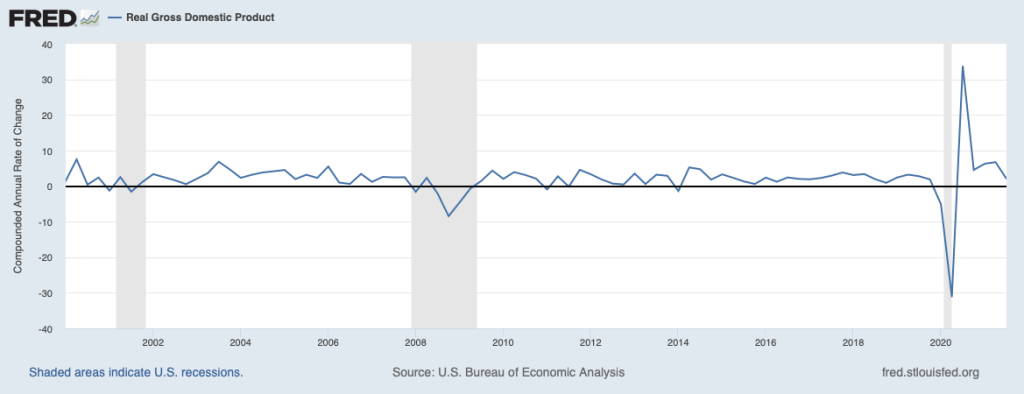

There are a number of ways in which the Covid-19 pandemic was unlike anything the United States has experienced since the 1918 influenza pandemic. Most striking from an economic perspective were the extraordinary swings in real GDP. The following figure shows quarterly changes in real GDP seasonally adjusted and calculated at an annual rate. There were three recessions during this period (shown by the shaded areas).

The first of these recessions occurred during 2001 and was similar to most recessions in the United States since 1950 in being short and relatively mild. Real GDP declined by 1.5 percent during the third quarter of 2001. The recession of 2007–2009 was the most severe to that point since the Great Depression of the 1930s. The worst periods of the 2007–2009 were the fourth quarter of 2008, when real GDP declined by 8.5 percent—the largest decline to that point during any quarter since 1960—and the first quarter of 2009, when real GDP declined by 4.6 percent.

Turning to the 2020 recession, during the first quarter of 2020, only at the end of which did Covid-19 begin to seriously affect the U.S. economy, real GDP declined by 5.1 percent. Then in the second quarter a collapse in production occurred unlike anything previously experienced in the United States over such a short period: Real GDP declined by 31.2 percent. But that collapse was followed in the next quarter by an extraordinary recovery in production when real GDP increased by 33.8 percent—by far the largest increase in a single quarter in U.S. history.

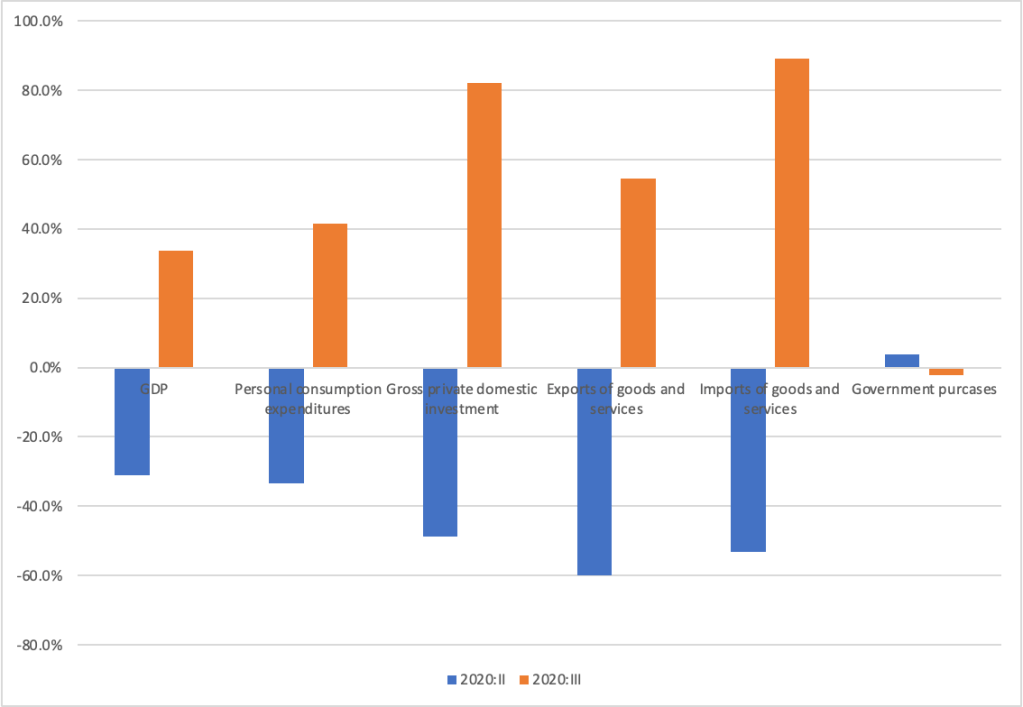

The following figure shows the changes in the components of real GDP during the second and third quarters of 2020. In the second quarter of 2020, consumption spending declined by about the same percentage as GDP, but investment spending declined by more, as many residential and commercial construction projects were closed. Exports declined by nearly 60 percent and imports declined by nearly as much as many ports were temporarily closed. In the third quarter of 2020, many state and local governments relaxed their restrictions on business operations and the components of spending bounced back, although they remained below their levels of late 2019 until mid-2021.

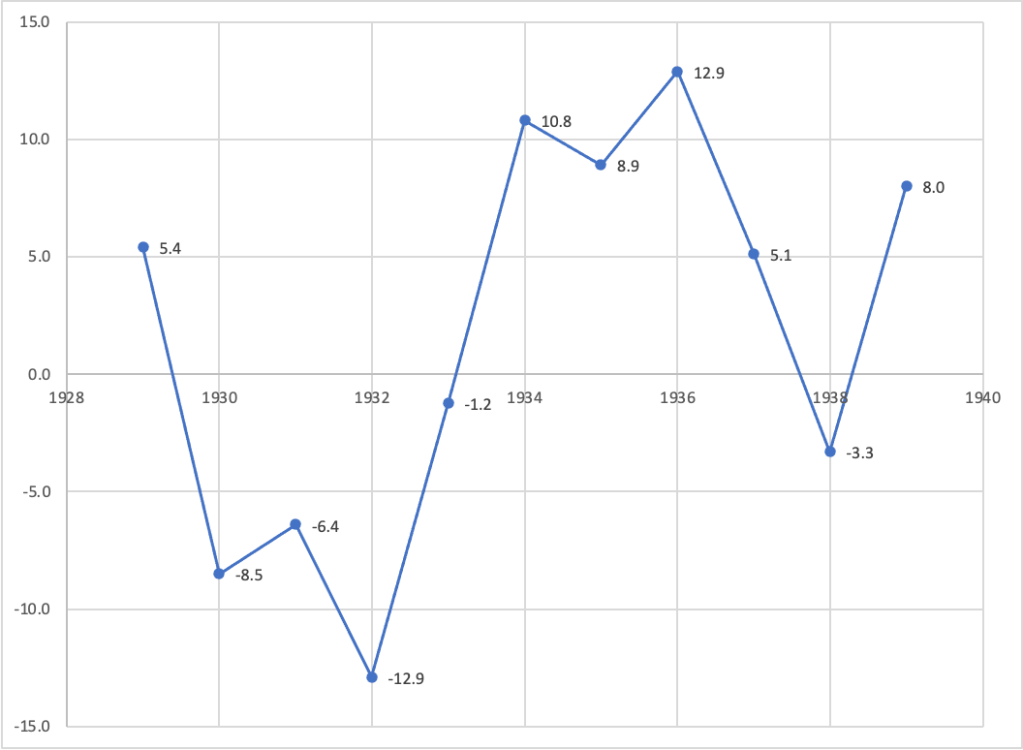

Even when compared with the Great Depression of the 1930s, the movements in real GDP during the Covid-19 pandemic stand out for the size of the fluctuations. The official U.S. Bureau of Economic Analysis data on real GDP are available only annually for the 1930s. The following figure shows the changes in these annual data for the years 1929 to 1939. As severe as the Great Depression was, in 1932, the worst year of the downturn, real GDP declined by less than 13 percent—or only about a third as much as real GDP declined during the worst of the 2020 recession.

We have to hope that we will never again experience a pandemic as severe as the Covid-19 pandemic or fluctuations in the economy as severe as those of 2020.

Source: U.S. Bureau of Economic Analysis. Note: Because the BEA doesn’t provide an estimate of real GDP in 1928, our value for the change in real GDP during 1929 is the percentage change in real GDP per capita from 1928 to 1929 using the data on real GDP per capita compiled by Robert J. Barro and José F. Ursúa. LINK

During 2020, Congress and President Donald Trump responded to the Covid-19 pandemic with very aggressive fiscal policy initiatives. First, in March 2020, Congress enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The CARES Act increased the federal government’s expenditures by $1.9 trillion. Then, in December 2020, in response to the continuing effects of the pandemic, Congress and President Trump included an additional $915 billion in expenditures related to Covid-19 in the Consolidated Appropriations Act. These two fiscal policy actions included payments directly to households and supplemental unemployment insurance payments. Higher income households were not eligible for the direct payments (often referred to as “stimulus payments”). Higher income households were also less likely to be unemployed and so were less likely to receive the supplemental unemployment insurance payments.

In Chapter 17, Section 17.4, we discuss the unequal distribution of income in the United States. Because the federal payments were targeted toward lower and middle income households, did the payments result in a decline in income inequality? Table 17.6 in Chapter 17, shows a common measure of the distribution of income: Households in the United States are divided into five income quintiles, from the 20 percent with the lowest incomes to the 20 percent with the highest incomes, along with the fraction of total income received by each of the five groups. The following table displays the distribution of income using this measure for 2019 and 2020. (We also include the data for the share of income received by the 5 percent of households with the highest incomes.) Note that the definition of income used in the table includes tax payments households make in that year in addition to payments—including the stimulus payments—received from the government. The income is also “equivalence adjusted,” which means that income is adjusted to account for how many adults and children are in a household.

Year

Lowest 20%

Second 20%

Middle 20%

Fourth 20%

Highest 20%

Highest 5%

2019

4.7%

10.4%

15.7%

22.6%

46.6%

19.9%

2020

5.1%

10.9%

16.0%

22.8%

45.2%

18.9%

Percentage change in income share

8.7%

4.8%

2.1%

0.8%

−3.0%

−5.1%

The table shows that the distribution of income in the United States became somewhat more equal during 2020, with the share of income going to each of the first four quintiles increasing, while the income of the highest quintile declined. The income share of the lowest quintile increased the most—by 8.7 percent—while the income share of the top 5 percent of households decreased by 5.1%. In that section of Chapter 17, we discuss the Gini coefficient, which is a measure of how unequal the distribution of income is. The Gini coefficient ranges between 0 and 1 with higher values indicating a more unequal distribution. Between 2019 and 2020, the Gini coefficient decline from 0.416 to 0.399, or by 4.1 percent, which measure the extent to which the income distribution became more equal.

Will the reduction in income inequality the United States experienced during 2020 persist? It seems likely to, at least through 2021, given that in March 2021, Congress and President Joe Biden enacted the American Rescue Plan, which included payments to households of up to $1,400 per eligible household member. As with the payments to households made during 2020, high-income households were not eligible. Congress also extended supplemental unemployment insurance payments through early September 2021 in states that were willing to accept the payments.

What about after federal stimulus payments to households end? (As of late 2021, it appeared unlikely that Congress and President Biden planned on enacting any further payments.) One indication that some of the reduction in inequality might be sustained comes from the sharp increases in the wages of many low-skilled workers. For instance, in October 2021, the wages (as measured by their average hourly earnings) of workers in the leisure and hospitality industry, which includes workers in restaurants and hotels, increased by nearly 12 percent over the previous year. For all workers in the private sector, wages increased by about 5 percent over the same period. Many of the workers in this industry have low incomes. So, the fact that their wages were increasing more than twice as fast as wages in the overall economy indicates that at least some low-income workers were closing the earnings gap with other workers.

Sources: Emily A. Shrider, Melissa Kollar, Frances Chen, and Jessica Semega, U.S. Census Bureau, Current Population Reports, P60-270, Income and Poverty in the United States: 2020, Washington, DC, U.S. Government Printing Office, September 2021, Table C-3; and U.S. Bureau of Labor Statistics.

Northampton County Community College in Pennsylvania

People who graduate from college earn significantly more and have lower unemployment rates than do people who have only a high school degree. (We discuss this issue in Chapter 16, Section 16.3.) As the following table shows, in 2020, people with a bachelor’s degree had average weekly earnings of $1,305 and had an unemployment rate of 5.5 percent, while people who had only a high school degree had weekly earnings of $781 and an unemployment rate of 9.0 percent. People with an associate’s degree from a two-year community college were in between the other two groups.

Educational attainment

Median usual weekly earnings ($)

Unemployment rate (%)

Doctoral degree

1,885

2.5

Professional degree

1,893

3.1

Master’s degree

1,545

4.1

Bachelor’s degree

1,305

5.5

Associate’s degree

938

7.1

Some college, no degree

877

8.3

High school diploma

781

9

Less than a high school diploma

619

11.7

Total

1,029

7.1

Not surprisingly, attempts to reduce income inequality have often included plans to increase the number of low-income people who attend college. In 2021, President Joe Biden proposed a plan that would cover the tuition of most first-time students attending community college in states that agreed to participate in the plan. The plan was estimated to cost $109 billion over 10 years and would potentially cover 5.5 million students. As of late 2021, it appeared unlikely that Congress would enact the plan but similar plans have been proposed in the past making the economic payoff to free community college an important policy issue.

There are many federal, state, and local programs that already cover some or all of the tuition and fees for some community college students. The state and local programs are often called “promise programs.” The name refers to what is usually considered the first such program, which began in Kalamazoo, Michigan in 2005. There are now more than 200 promise programs in 41 states. The programs differ in the percentage of a student’s tuition and fees that are covered and on which students are eligible. The plan proposed by President Biden would have differed from existing programs in being more comprehensive—covering community college tuition for all high school graduates who had not previously attended college.

We can’t offer here a full assessment of the economic effects that might result from a nationwide free community college, but we can briefly summarize some of the very large number of economic studies of community colleges. Hieu Nguyen of Illinois Wesleyan University has studied the effects of the Tennessee Promise program, which beginning in fall 2015, has covered that part of the tuition not covered by federal or other state programs for any Tennessee high school graduate who enrolls in a public two-year college in the state. Nguyen’s analysis finds that the program had a very large effect, increasing “full-time first-time undergraduate enrollment at the state’s community colleges by at least 40%.” Some policymakers and economists are concerned that promise programs may divert some students into attending community college who would otherwise have enrolled in a four-year college. As the table shows, on average, people who graduate from a four-year college have higher incomes and lower unemployment rates than people who graduate from a two-year college. Nguyen analysis indicates that this problem was not significant in Tennessee. He finds that the Tennessee Promise program resulted in only a 2 percent decline in enrollment in Tennessee’s public four-year colleges.

Oded Gurantz of the University of Missouri studied the Oregon Promise program, which like the Tennessee Promise program, covers the part of tuition at Oregon two-year colleges not covered by federal or other state programs with the difference that it awards $1,000 per year to students whose tuition is completely covered from other sources. The program began in 2016. Guarantz finds that although the program did increase the enrollment in two-year colleges by four to five percent, initially nearly all of the increase was the result of students shifting away from four-year colleges. He finds that in later years the program was effective in increasing enrollment in both two-year and four-year colleges.

Elizabeth Bell of Miami University finds that a narrowly focused Oklahoma program that covers tuition and fees at a single two-year college—Tulsa Community College—succeeds in substantially increasing the number of students who transfer to a four-year college and, to a lesser extent, increasing the fraction of students who receive degrees from four-year colleges.

A number of researchers have studied the returns to individuals from attending community college. As with the returns from four-year colleges, choice of major can be very important. Michael Grosz of the Federal Trade Commission found that, controlling for the individual characteristics of students, receiving a degree in nursing from a California community college “increases earnings by 44 percent and the probability of working in the health care industry by 19 percentage points.”

Jack Mountjoy of the University of Chicago has compiled a large data set for the state of Texas that links enrollment in all public and private universities in the state to students’ earnings later in life. Mountjoy uses the data to analyze the effects of community college on upward mobility. The upward mobility of students who attend a community college is increased if the students would otherwise not have attended college but hindered if they attend a community college rather a four-year college they were qualified to attend. Mountjoy notes that survey evidence indicates that 81 percent of students enrolling in two-year colleges intend to ultimately receive a degree from a four-year college, buy only 33 percent transfer to a four-year college within six years and only 14 percent ultimately earn a bachelor’s degree.

Because so few students who enroll in a two-year college ultimately receive a degree from a four-college, promise programs run the risk of actually reducing the number of students who receive bachelor’s degrees by diverting some students from four-year colleges to two-year colleges. Mountjoy’s analysis of the Texas data indicates that “broad expansions of 2-year college access are likely to boost the upward mobility of students ‘democratized’ into higher education from non-attendance, but more targeted policies that avoid significant 4-year diversion may generate larger net benefits.” He notes that for low-income students, “2-year college enrollment may involve other labor market benefits … beyond modest increases in formal educational attainment, such as better access to employer networks, short course sequences teaching readily-employable skills, and improved job matching.”

Mountjoy’s results reinforce a point made by some other economists and policymakers: Programs that provide free community college for all students may be a less effective way for governments to spend scarce funds than are programs that focus on boosting the ability of low-income students to attend and complete both two-year and four-year colleges. Many low-income students face barriers beyond difficulty affording tuition, including the lost earnings from time spent in class and studying rather than working, child care expenses, and paying for textbooks and other learning materials. In addition, providing free tuition at community colleges to all students may end up subsidizing college attendance for some middle and high-income students who would have attended college without the subsidy and may provide an incentive for some students to enroll in two-year colleges who would have been better off enrolling in four-year colleges.

Sources: Julie Bykowicz and Douglas Belkin, “Why Biden’s Plan for Free Community College Likely Will Be Cut From Budget Package,” wsj.com, October 21, 2021; Michel Grosz, “The Returns to a Large Community College Program: Evidence from Admissions Lotteries,” American Economic Journal: Economic Policy; Vol. 12, No. 1, February 2020; 226-253; Hieu Nguyen, “Free College? Assessing Enrollment Responses to the Tennessee Promise Program,” Labour Economics, Vol. 66, October 2020; Oded Guarantz, “What Does Free Community College Buy? Early Impacts from the Oregon Promise,” Journal of Policy Analysis and Management, Vol. 39, No. 1 October 2020, pp. 11-35; Elizabeth Bell, “Does Free Community College Improve Student Outcomes? Evidence From a Regression Discontinuity Design,” Educational Evaluation and Policy Analysis, Vol. 43, No. 2, June 2021, pp. 329-350; Michael Grosz, “The Returns to a Large Community College Program: Evidence from Admissions Lotteries,” American Economic Journal: Economic Policy, Volume 12, No. 1, February 2020; pp. 225-253; Jack Mountjoy, “Community Colleges and Upward Mobility,” National Bureau of Economic Research, Working Paper 29254, September 2021; Allison Pohle, “What Does Biden’s Plan for Families Mean for Community College, Pre-K?” wsj.com, April 28, 2021; Meredith Billings, “Understanding the Design of College Promise Programs, and Where to Go from Here,” brookings.edu, September 18, 2018; and U.S. Bureau of Labor Statistics, “Employment Projections: Education Pays,” Table 5.1, September 8, 2021.

Few diseases affect all demographic groups equally. For example, the 1918–1919 influenza pandemic killed an unusually large number of young adults. Estimates are that half of deaths in the United States during that pandemic occurred among people aged 20 to 40. In recent flu seasons, the elderly have much higher mortality rates than do other age groups. For instance, during the 2018–2019 flu season, people 65 and older died at a rate more than 10 times greater than people 18 to 49 years old. The very young also have comparatively high mortality rates from the flu. In 2018–2019, children 0 to 4 years-old died at a rate six times higher than children 5 to 17 years-old.

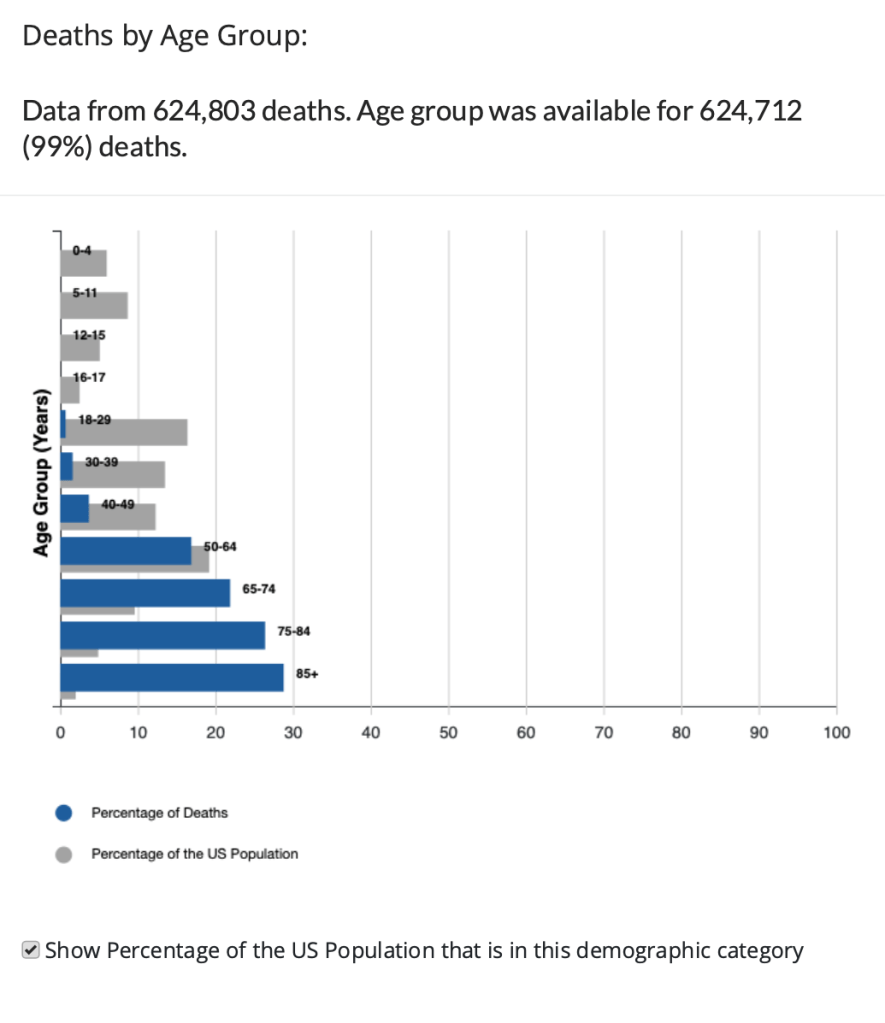

When the Covid-19 virus began to spread widely in the United States in the spring of 2020, some epidemiologists expected that it would affect different demographic groups in about the same way that the flu does. In fact, though, while people 65 and older were particularly at risk, young children were less affected by Covid-19 than they are by the flu. The following chart prepared by the Centers for Disease Control and Prevention (CDC) displays for the United States data on Covid deaths by age group as of early November 2021.

The blue bars show the percentage of total deaths from Covid since the beginning of the pandemic represented by that age group and the gray bars show the percentage that group makes up of the total U.S. population. Therefore, an age group that has a gray bar longer than its blue bar was proportionally less affected by the virus and an age group that has a blue bar longer its gray bar was proportionally more affected by the virus. The chart shows that people over age 65 experienced particularly high mortality rates. Strikingly, people over age 85 accounted for nearly 30 percent of all deaths in the United States, while making up only 2 percent of the U.S. population.

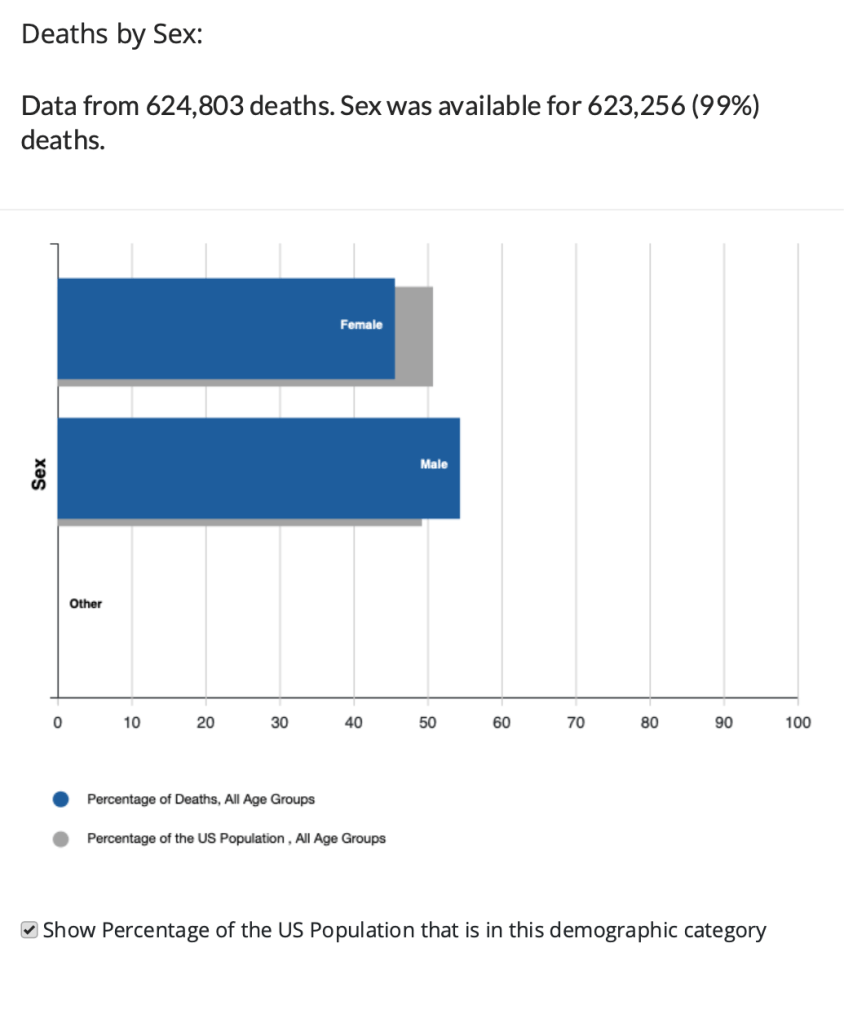

The following chart displays data on Covid deaths by gender. Men account for about 49 percent of the U.S. population but have accounted for about 54 percent of Covid deaths.

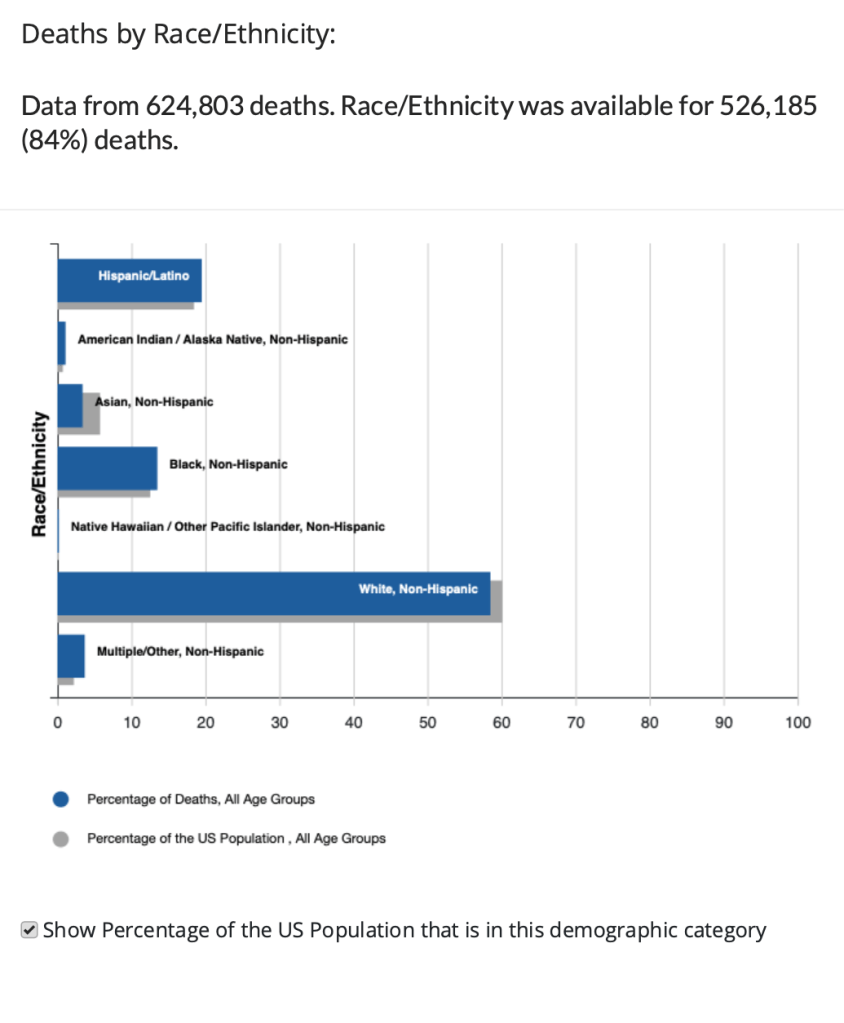

Finally, the following chart displays data on Covid deaths by race or ethnicity. Hispanic, Black, and American Indian or Alaskan Native people have experienced proportionally higher Covid mortality rates than have Asian or white people.

What explains the disparity in mortality rates across demographic groups? With respect to age, we would expect older people to have weaker immune systems and therefore be more likely to die from any illness. In addition, early in the pandemic many older people in nursing homes died of Covid before it was widely understood that the disease spread through aerosols and that keeping people close together inside unmasked made it easy for the virus to spread. The very young have immature immune systems, which might have made them particularly susceptible to Covid, but for reasons not well understood, they turned not to be.

There continues to be debate over why men have experienced a higher mortality rate from Covid than have women. Vaccination rates among men are somewhat lower than among women, which may account for part of the difference. In an opinion column in the New York Times, Dr. Ezekiel Emanuel of the University of Pennsylvania noted that researchers at Yale University have observed “that there are well-established differences in immune responses to infections between men and women.” But why this pattern should be reflected in Covid deaths is unclear at this point.

Medical researchers and epidemiologists have also not arrived at a consensus in explaining differences in mortality rates across racial or ethnic groups. Groups with higher mortality rates have had lower vaccination, which explains some of the difference. Groups with higher mortality rates are also more likely to suffer from other conditions, such as hypertension, that have been identified as contributing factors in some Covid deaths. These groups are also less likely to have access to health care than are the groups with lower mortality rates. The CDC notes that: “Race and ethnicity are risk markers for other underlying conditions that affect health, including socioeconomic status, access to health care, and exposure to the virus related to occupation, e.g., frontline, essential, and critical infrastructure workers.”

Sources: Ezekiel J. Emanuel, “An Unsolved Mystery: Why Do More Men Die of Covid-19?” nytimes.com, November 2, 2021; Daniela Hernandez, “Covid-19 Vaccinations Proceed Slowly Among Older Latino, Black People,” wsj.com, March 2, 2021; Anushree Dave, “Half-Million Excess U.S. Deaths in 2020 Hit Minorities Worse,” bloomberg.com, October 4, 2021; Centers for Disease Control and Prevention, “Hospitalization and Death by Race/Ethnicity,” cdc.gov, September 9, 2021; Centers for Disease Control and Prevention, “Demographic Trends of COVID-19 cases and deaths in the US reported to CDC,” cdc.gov, November 5, 2021 Centers for Disease Control and Prevention, “2018–2019 Flu Season Burden Estimates,” cdc.gov; and Jeffery K. Taubenberger and David M. Morens, “1918 Influenza: the Mother of All Pandemics,” Emerging Infectious Diseases, Vol. 12, No. 1, January 2006, pp. 15-22.

Why do countries impose tariffs on imported goods? As we discuss in Economics Chapter 9 and MacroeconomicsChapter 7 (particularly in Section 5 of these chapters) countries primarily use tariffs to protect domestic industries from foreign competition. Protectionism appeared to be the main motivation when the Trump administration imposed tariffs on imports of steel, aluminum, and some other products from China, Canada, and countries in the European Union. It was also the main reason that the Biden administration decided in 2021 to retain many of those tariffs.

The other main justification for imposing tariffs is for reasons of national security. For instance, as we note in the textbook, the United States would not want to import its jet fighter engines from China. In fact, the Trump administration relied on Section 232 of the Trade Expansion Act of 1962 when it imposed tariffs, particularly tariffs on steel and aluminum. The Biden administration also cited this section of the law when continuing the tariffs. (In October 2021, the Biden administration negotiated with the European Union a partial reduction of these tariffs.) Under that section of the law, if the president decides that imports of a good threaten nationals security, “he shall take such action, and for such time, as he deems necessary to adjust the imports of such article and its derivatives so that such imports will not so threaten to impair the national security.” In other words, presidents have the power to impose tariffs on imports of a good if they assert that doing so protects the national security of the United States.

When they invoked this section of the law, both the Trump and Biden administrations were criticized for stretching its application beyond what Congress had intended. Critics argue that using this section of the law to impose tariffs on such close allies of the United States as the countries of the European Union was a violation of Congress’s intent because it was unlikely that imports of steel or aluminum from Europe threaten the national security of the United States.

If used as intended, Section 232 is a rare example of imposing tariffs for reasons other than protecting domestic industries. (It’s worth noting that during the 1800s and early 1900s, before there was a federal income tax, Congress relied on revenues from tariffs as the main source of funds to the federal government. In recent years tariff revenues have been very small compared with income taxes and the federal government’s other sources of revenue.) In 2021, some policymakers were proposing using tariffs for another purpose unrelated to protecting domestic industries: Slowing climate change.

In November 2021, the United States and the European Union announced that they would explore imposing tariffs on imports of steel from countries that impose few regulations on carbon emissions from steel mills. (These climate tariffs are sometimes referred to as border carbon adjustments (BCAs).) The tariffs might be extended to include imports of aluminum, chemicals, and cement. The rationale for these tariffs is that in the United States and Europe, steel producers must install expensive equipment to reduce carbon emissions or must pay a tax on those emissions.

These regulations raise the cost of producing steel and, therefore, the price of steel produced in Europe and the United States. As a result, U.S. and European firms that use steel, such as automobile companies, have an incentive to import lower-priced steel from countries that have few regulations on carbon emissions. According to one estimate, the production of steel being imported into the United States generates 50 percent to 100 percent more carbon dioxide emissions than does the production of domestic steel. An article in the Wall Street Journal noted that a report from a consulting firm argued that “the emissions that many developed countries claim to have eliminated were ‘outsourced to developing countries,’ which generally have fewer resources to invest in cleaner and more advanced technology.”

Critics of using tariffs as a means of slowing climate change note that there are other measures that countries can use to reduce their own CO2 emissions and that attempts to use economic coercion to prod countries into changing policies have not generally been successful. They also note that Section 232 of the Trade Expansion Act of 1962 was intended to be used only for reasons of national security but has been used by the Trump and Biden administration more broadly to protect domestic industries. They fear that the same thing may happen if climate tariffs are allowed under international agreements: The tariffs may be used to protect domestic industries for reasons that have nothing to do with reducing climate change. In fact, an article on barrons.com noted that the agreement between the United States and the European Union to impose climate tariffs on steel imports was “aimed, according to administration officials, at countering the flood of cheap steel from China, which accounts for roughly 60% of production worldwide.”

In addition, some economists and policymakers fear that imposing climate tariffs may undermine the rules of the World Trade Organization (WTO), which do not authorize countries to impose tariffs for this reason. This outcome is particularly likely if some countries see the tariffs as aimed more at protecting domestic industries than at slowing climate change. As we discuss in Section 5 of Chapter 9 in Economics (Macroeconomics Chapter 7), the WTO and its predecessor, the General Agreement on Tariffs and Trade (GATT) resulted in decades of multilateral negotiations that greatly reduced tariffs. The tariff reductions spurred a tremendous expansion in world trade, which significantly increased incomes in the United States and most other countries—although it also disrupted some domestic industries in those countries. If the WTO were to cease to be effective, the world might return to the situation of the 1930s and earlier when countries used tariffs for a variety of policy reasons. The trade war of the 1930s, during which most countries raised tariff rates, led to a collapse in world trade and helped to worsen the Great Depression.

If climate tariffs become common, the effect on both the climate and on the international trading system may be significant.

Sources: Josh Zumbrun, “U.S.-EU Steel Tariffs Deal Is Onerous for Smaller Importers,” wsj.com, November 5, 2021; Yuka Hayashi and Jacob M. Schlesinger, “Tariffs to Tackle Climate Change Gain Momentum. The Idea Could Reshape Industries,” wsj.com, November 2, 2021; By Reshma Kapadia, “The EU Tariff Deal Doesn’t Mean the Trade War With China Is Over,” barrons.com, November 2, 2021; Jennifer A. Dlouhy and Ari Natter, “Democrats Propose Tax on Carbon-Intensive Imports in Budget,” bloomberg.com, July 14, 2021; and Billy Pizer, “The Trade Tool that Could Unlock Climate Ambitions,” barrons.com, November 5, 2021.

In Chapter 12 of the textbook, we discuss developments over the years in the intensely competitive egg market. Many of the 65,000 egg farmers in the United States have continued to produce eggs using traditional methods. But some egg farmers have adopted cage-free methods that allow chickens to have sufficient room to move around. Using cage-free methods increases a farmer’s costs but some consumers are willing to pay more for these eggs. More recently, some egg farmers have turned to selling “pastured eggs” laid by chickens that are allowed to roam freely outside. Raising pastured eggs has even higher costs than raising eggs using cage-free methods, but pastured eggs also sell for higher prices.

As consumer willingness to spend on eggs produced in ways that involve more humane treatment of chickens increases, we’d expect that egg farmers will adapt by embracing these methods. But in 2021, a development occurred in the egg market that was much more difficult for egg farmers to respond to. Some consumers have been moving away from animal products to plant-based replacements. These consumers have a variety of concerns about animal products: Some consumers have ethical concerns about consuming any animal products, others believes consuming these products may have negative health effects, while others are concerned by what they believe to be the negative effects of farming on the environment.

Many people are familiar with the Impossible company’s “impossible burger,” a hamburger made from soy and potatoes rather than from beef. But it’s less well known that several companies have begun selling eggs made from plants. San Francisco-based Eat Just, Inc. has begun selling in the United States eggs made from mung beans and in October 2021 was authorized to begin selling these eggs in Europe. The Swiss firm Nestlé under its Garden Gourmet brand has also begun selling in Europe eggs made from soy. Nestlé’s eggs are sold in liquid form and are primarily intended as a substitute for natural eggs in cooking.

As of late 2021, plant-based eggs have captured only a tiny slice of the egg market. But if their popularity should increase significantly, it will be bad news for egg farmers. While many egg farmers have been able to adapt to changes in how they produce eggs, they lack the specialized equipment to produce plant-based eggs or access to the distribution and marketing resources necessary to sell them.

The market for eggs may be about to be disrupted in a way that will force many egg farmers out of the industry.

Sources: Corinne Gretler and Thomas Buckley, “Nestlé Tests Plant-Based Frontier With Vegan Eggs and Shrimp,” bloomberg.com, October 6, 2021; Aine Quinn, “Fake Eggs From Mung Beans Get Closer to Reality in Europe,” bloomberg.com, October 20, 2021; Jon Swartz, “Eat Just’s Plant-Based Egg Products to Come to Another 5,000 Retail Outlets,” marketwatch.com, September 2, 2020; Deena Shanker, “Faux-Egg Maker Eat Just Raises $200 Million More in Latest Round,” bloomberg.com, March 3, 2021; and Jon Emont, “Real Meat That Vegetarians Can Eat,” wsj.com, March 6 2021.

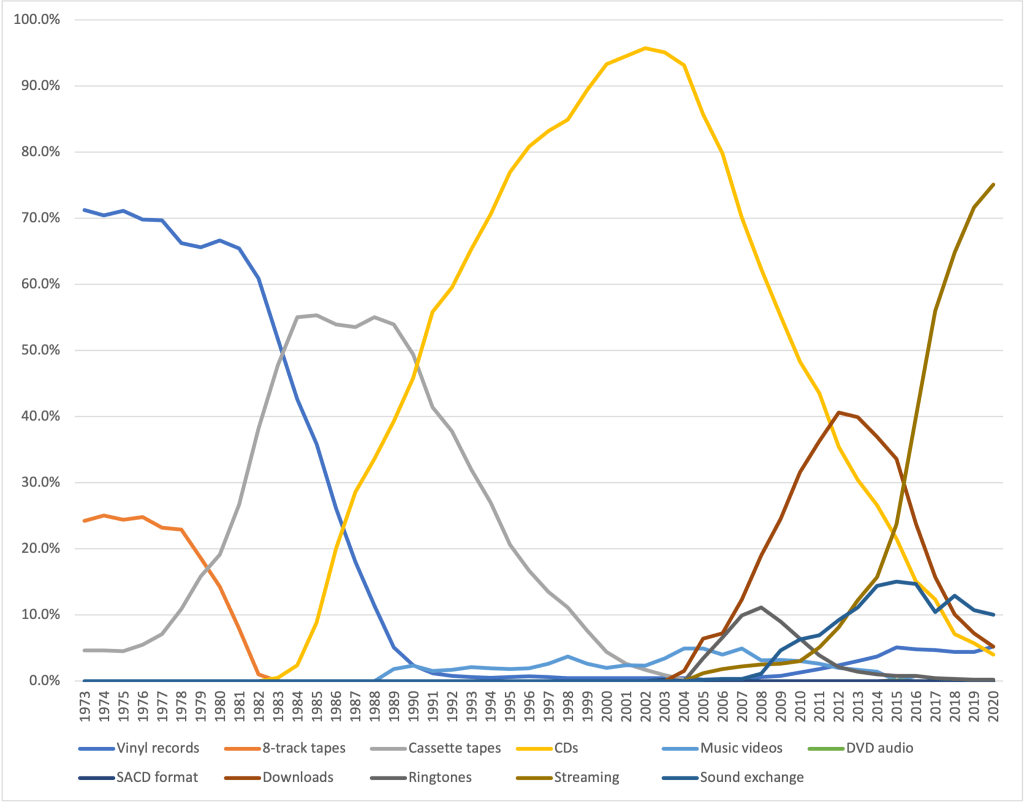

Listening to recorded music seems like a basic, uncomplicated activity, but as we discuss in the opening to Chapter 14, few markets have been as disrupted by technological change over the years as the market for recorded music. The following graph shows the distribution of revenue received by firms in the recording industry by type of music format. The data are first available for 1973.

From the 1930s to the mid-1960s, nearly all recorded music was sold on vinyl records. In the 1960s, 8-track tapes began to compete with vinyl records. In 1973, recording companies received about 71 percent of their revenue from selling vinyl records, 24 percent from selling 8-track tapes, and 5 percent from selling cassette tapes. Cassette tapes became increasingly popular after Sony introduced the Walkman, a portable cassette player, in 1979. The popularity of cassettes contributed to a sharp decline in sales of vinyl records. The share of vinyl records in revenue received from sales of recorded music dropped from 71 percent in 1975 to only 2 percent in 1990. The greater portability of cassette tapes was a significant advantage over 8-track tapes, which were most frequently used in players built into automobiles. By 1983, 8-track tapes had largely disappeared from the market.

The introduction of digital compact discs (CDs) in the early 1980s ended the rapid rise in sales of cassette tapes. By the end of the 1980s, sales of cassette tapes began to decline rapidly and their share of the market had fallen to less than 2 percent by the early 2000s.

As discussed in the opening to Chapter 14, the development by engineers in Germany of the MP3 file format made it possible to store the contents of a music CD on a file small enough to be downloaded from the internet. Apple’s opening its iTunes online music store in 2003 increased sales of music downloads, which peaked at 40 percent of the market in 2012. In that year, recording companies earned about 8 percent of their revenue from payments from streaming services like Spotify or Apple Music.

Steaming music has become increasingly popular and by 2020, 75 percent of industry revenue was earned from streaming. Ten percent was earned from “sound exchange,” which refers to revenue recording companies receive when music is used in a movie, television series, advertisement, or online video. (Some industry analysts consider sound exchange to be a form of streaming. Using that definition raises streaming’s share to 85 percent of the market.) Downloads had a market share of only 5 percent, about the same as the share of vinyl records, which had increased from a low point of less than 1 percent in 2007. CD sales continue to slowly decline and make up about 4 percent of the market.

In Chapter 14, we discuss the streaming market as an example of oligopolistic competition. When a market expands as rapidly as music streaming has, competition can be less intense because it’s possible for firms to increase their revenue as the market expands without having to attract customers from competitors. Typically when a market matures and the increase in total revenue levels off, competition can become more intense. We may see that development in the market for streaming music in coming years.

Source: Data from Recording Industry Association of America, “U.S. Sales Database.”

For the past few decades, across different presidential administrations, antitrust policy has typically involved the following key points, which we discuss in Chapter 15, Section 15.6:

Responsibility for antitrust policy is divided between the Federal Trade Commission (FTC) and the Antitrust Division of the Department of Justice (DOJ).

For horizontal mergers, the DOJ and the FTC have published numerical guidelines that provide a benchmark for their decisions on whether to oppose a merger and give firms a good idea of whether a proposed merger will be allowed.

Antitrust enforcement is focused on consumer well-being, so a merger that increases monopoly power while at the same time improving economic efficiency will be allowed if the net effect of the merger is to increase consumer surplus.

If firms disagree with a merger decision from the FTC or the DOJ, those agencies typically file a law suit in a federal court to enforce their decision. Therefore, antitrust policy ultimately depends on how the federal courts interpret the antitrust laws. (We list the most important antitrust laws in Chapter 15, Table 15.2.)

During the 2020 presidential campaign President Joe Biden did not announce a detailed policy towards antitrust and the issue played only a small role in the campaign. Late in the campaign, a Biden spokesman did state that, “growing economic concentration and monopoly power in our nation today threatens our American values of competition, choice, and shared prosperity.” Once in office, Biden’s appointments to key antitrust positions favored a more aggressive approach to antitrust policy.

The views of most Biden appointees were similar to those of Louis Brandeis who served on the U.S. Supreme Court from 1916 to 1939. Brandeis was not familiar with economics and his views on antitrust as stated in his articles and court decisions can be contradictory.

But Robert Bork of the University of Chicago in his book the Antitrust Paradox provided an influential interpretation of Brandeis’s views. According to Bork, in the early twentieth century, “the dominant goal [of antitrust policy] was the protection of consumer welfare, though Justice Louis Brandeis … was the first to give operative weight to the conflicting goal of small-business welfare.” Bork argued that an implication of Brandeis’s views was that antitrust enforcement might end up “protecting the inefficient [firms] from competition.” Similarly, Daniel Crane of the University of Michigan refers to the “’Brandeisian’ tradition, associated with US Supreme Court Justice Louis Brandeis, [which] is often described as … supporting atomistic competition because of its beneficial effects on personal liberty and autonomy.”

President Biden has appointed several people who support the Brandeis approach to antitrust including Lina Khan of Columbia University as chair of the FTC; Tim Wu of Columbia University as an adviser to the president; and Bharat Ramamurti, a former aide to Massachusetts Senator Elizabeth Warren, as deputy director of the National Economic Council. John Cassidy, an economics writer for the New Yorker, summarized their position:

“Proponents of the New Brandeis-ism contend that these agencies should act proactively—carrying out broad investigations, publishing reports, and establishing rules of conduct for companies with a great deal of market power, including tech platforms and broadband providers.”

In July 2021, President Biden issued an executive order creating a White House Competition Council. According to a statement from the White House, the purpose of the council is to: “to coordinate the federal government’s response to the rising power of large corporations in the economy.” Also in July 2021, the FTC under Chair Khan’s leadership voted to move away from the consumer welfare standard for judging anticompetitive business strategies, including merging or acquiring other firms and certain pricing decisions, such as cutting prices to below those charged by smaller rivals. The result of the FTC’s new approach is that the agency will take action against business strategies that are not directly in violation of the federal antitrust laws. The FTC is particularly concerned by strategies used over the years by large technology firms such as Facebook, Google, Amazon, and Apple.

The Biden administration’s redirection of antitrust policy has run into criticism. An article in the Wall Street Journalquoted the president of the Consumer Technology Association as stating that: “The consumer-welfare standard grounds competition policy in objective facts and evidence. By protecting consumers rather than competitors, we ensure antitrust decisions are not subjective or political.” The “consumer-welfare standard” is the standard that had been used under previous presidential administrations as we outlined in points 2. and 3. above. A possible barrier to the Biden administration’s change in policy is that ultimately it is up to the federal courts to decide the legality of a business strategy. In recent decades, the federal courts have consistently required that for a strategy to be declared illegal it must be a violation of the antitrust laws.

Until the FTC or the DOJ use the new standard to bring actions against firms and until the courts either uphold or dismiss those actions, it won’t be possible to know whether the Biden administration’s antitrust policy will end up being much different from the policies of previous administrations. It could be a number of years before actions brought under the new standard make their way through the court system.

Sources: Brent Kendall, “New Policy Gives FTC Greater Control Over How Companies Do M&A,” wsj.com, October 29, 2021; Executive Office of the President, “Fact Sheet: Executive Order on Promoting Competition in the American Economy,” whitehouse.gov, July 9, 2021; John D. McKinnon, “FTC Vote to Broaden Agency’s Mandate Seen as Targeting Tech Industry,” wsj.com, July 1, 2021; John Cassidy, “The Biden Antitrust Revolution,” newyorker.com, July 12, 2021; David McCabe and Jim Tankersley, “Biden Urges More Scrutiny of Big Businesses, Such as Tech Giants,” nytimes.com, September 16, 2021; Daniel A. Crane, “Rationales for Antitrust: Economics and Other Bases,” in Roger D. Blair and D. Daniel Sokol, The Oxford Handbook of International Antitrust Economics, Vol. 1, New York: Oxford University Press, 2015; Robert H. Bork, The Antitrust Paradox: A Policy at War with Itself, New York: Basic Books, 1978; and Kenneth G. Elzinga and Micah Webber, “Louis Brandeis and Contemporary Antitrust Enforcement,” Touro Law Review, 2015, Vol. 33, No. 1 , Article 15.

The restaurant industry was hit hard by the Covid-19 pandemic. Fast food restaurants like McDonalds and Taco Bell had their revenues hold up the best because many of their customers were experienced in using their drive-through windows, which typically remained open except during the worst of the pandemic in the Spring of 2020. Restaurants that rely on table service suffered steeper declines in revenue because even when local governments allowed them to be open, they were typically required to operate at reduced capacity. In addition, through most of 2021, some consumers were reluctant to spend an hour or more eating indoors for fear of contracting the virus.

In the years leading up to the pandemic, fast-casual restaurants like Chipotle, Panera Bread, and Cheesecake Factory had been increasing in popularity, drawing customers from both more formal table service restaurants and from fast food-food restaurants. But because of their reliance on indoor dining, many fast-casual restaurants suffered sharp declines in revenue. For instance, in the spring of 2020, Cheesecake Factory was losing $6 million per week and at one point had less than $100 million remaining on hand to meet its costs.

As we discuss in Chapter 13, Section 13.3, firms in a monopolistically competitive like restaurants have difficulty earning an economic profit in the long run. Normally, economic profit is eliminated by entry of new firms. But during the pandemic, the process was speeded up as what had been profitable business strategies suddenly no longer were.

Cheesecake Factory had been earning an economic profit by following a strategy that differentiated it from similar restaurant chains. At 10,000 square feet, the dining rooms in its restaurants are much larger than in other fast-casual restaurants and Cheesecake Factory has many more items on its menus. Both these features turned into liabilities during the pandemic because before the pandemic Cheesecake Factory’s revenue would exceed its costs only if its restaurants were operated close to their capacity. In many cities, well into 2021, government restrictions required restaurants to operate at reduced capacity. In addition, like most other restaurants, as it reopened Cheesecake Factory had trouble attracting enough servers and cooks—a particular problem given the large number of items on its menus.

Cheesecake Factory returned to profitability in 2021 by adopting a new strategy of emphasizing delivering orders and having orders available for pickup at its restaurants (“to-go” orders). This strategy was successful in part because Cheesecake Factory executives made the decision during 2020 to continue to pay its 3,000 managers during the period when most of its restaurants were closed. Doing so meant having to raise $200 million from investors to pay the managers’ salaries. Keeping managers on payroll meant that the firm had the staff on hand to successfully manage the increase in to-go and delivery orders.

The success of the strategy was helped by the fact that cheesecake turned out to be a more popular delivery item than the firm had expected. An article in the Wall Street Journal quoted the firm’s president as saying that people were ordering it for a delivery throughout the day, including people “who are just getting slices at nine o’clock at night delivered to their house.” The firm has doubled its to-go orders compared with before the pandemic and its overall sales per restaurant have increased from an average of $11 million before the pandemic to $12 million in 2021.

Is Cheesecake Factory’s recent success sustainable? In emphasizing to-go and delivery orders, Cheesecake Factory initially had an advantage over its competitors because it had retained thousands of managers who could implement this new strategy. But this advantage may not last long for two reasons: 1) as the effects of the pandemic lessen, consumers may want to return to indoor dining, so the volume of to-go and delivery orders may decline; and 2) to the extent that consumers have permanently reduced their demand for indoor dining, competitors can copy Cheesecake Factory’s approach. Many competitors in fact have devoted more resources to to-go and delivery orders and the market for this type of dining is becoming as competitive as the market for in-door dining.

Cheesecake Factory has one other advantage: Cheesecake turned out to be a particularly popular food for delivery and cheesecake sales have become a larger percentage of the firm’s revenues since the beginning of the pandemic. Although, because the word “cheesecake” is in the firm’s name, it may retain some advantage among consumers who want to order a delivery of cheesecake, competitors can easily also add cheesecake to their delivery menus.

So, our general conclusion holds that it is very difficult for firms in a monopolistically competitive industry to earn an economic profit in the long run.

Sources: Heather Haddon, “How Cheesecake to Go Saved the Cheesecake Factory,” wsj.com, October 29, 2021; Teresa Rivas, “Cheesecake Factory Stock Is Falling Because Sales Took a Nose Dive,” barrons.com, July 29, 2020; Rick Clough, “Cheesecake Factory Settles SEC Charges over Covid Statements,” bloomberg.com, December 4, 2020; Tomi Kilgore, “Cheesecake Factory Stock Jumps after Upbeat Sales Update,” marketwatch.com, June 2, 2021.

Some governments have been subsidizing purchases of electric vehicles, or more broadly, fuel-efficient vehicles to slow climate change. How well do such policies work? Are they more or less efficient than other policies intended to reduce carbon dioxide emissions?

A subsidy is a payment by the government that provides an incentive for people to take an action they otherwise wouldn’t, such as buying an electric car. Subsidies have the potential downside that they may involve payments to people to do something they would have done anyway. For instance, in the United States in 2021, buyers of electric cars were eligible for a credit of up to $7,500 against their federal income taxes. Suppose that you become aware of this subsidy only after you have already purchased an electric car. In that case, the federal government has wasted $7,500 because you would have bought the electric car even without the subsidy. The same would be true if you knew about the subsidy before you bought but because of the subsidy you bought a higher-priced electric car rather than a lower-priced one.

These complications make it difficult for policymakers to assess the efficiency of subsidizing fuel-efficient cars as a means of slowing climate change. Two recent academic papers address this difficulty.

Chia-Wen Chen of Academia Sinica in Taiwan, We-Min Hu of National Chengchi University in Taiwan, and Christopher Knittel of the Massachusetts Institute of Technology have analyzed a Chinese government program that subsidizes the purchase of fuel-efficient cars. Because the study used data from 2010 and 2011, these vehicles were fuel-efficient gasoline powered cars rather than electric cars. They find that only about 44 percent of the subsidies went to car buyers who would otherwise not have bought a fuel-efficient car. “Thus, about 56 percent of the program’s payments were ineffective ….”

The authors calculate that the subsidy cost about $89 per metric ton of carbon dioxide reduced, which is high relative to other policies, such as a carbon tax. With a carbon tax, the government taxes energy consumption on the basis of the carbon content of the energy. (We discuss a carbon tax in the opener to Chapter 5.) The authors conclude: “Paying more than $89 for a metric ton of carbon dioxide is not a cost effective way to reduce carbon dioxide; if the main policy objective of China’s subsidy program on fuel-efficient vehicles was to reduce carbon dioxide emissions, then our results suggest that it was an ineffective way to achieve this goal.”

Jianwei Xing of Peking University, Benjamin Leard of Resources for the Future, and Shanjun Li of Cornell University analyze the efficiency of the U.S. federal income tax credit for purchasing an electric vehicle. As with the study just discussed, they find that consumers who use the credit to buy an electric vehicle were likely to have otherwise bought a hybrid vehicle (a vehicle that combines an electric motor with a gasoline engine) or a relatively fuel-efficient gasoline powered car. They also find, as with the other study, that the federal subsidy is inefficient because while it increased electric vehicle sales by 29 percent, “70 percent of the [tax] credits were obtained by households that would have bought an EV without the credits.”

Because the design of a particular subsidy for buying an electric car will affect the subsidy’s efficiency, these studies are not conclusive evidence that all programs of subsidizing electric cars will be inefficient. But their results show that two existing programs in large markets—China and the United States—are, in fact, inefficient.

As we note in Chapter 5, many economists favor a carbon tax as a way to reduce carbon emissions rather than policies, such as the federal electric vehicle tax credit, that target a particular source of carbon emissions. Economists can contribute to debates over public policy by using economic principles to identify programs that are more or less likely to efficiently achieve policy goals. They can also, as the authors of these two papers do, use statistical methods to analyze the effects of particular policies.

Sources: Chia-Wen Chen, We-Min Hu, and Christopher R. Knittel, “Subsidizing Fuel-Efficient Cars: Evidence from China’s Automobile Industry,” American Economic Journal: Economic Policy, Vo. 13, No. 4, November 2021, pp. 152-184; Jianwei Xing, Benjamin Leard, and Shanjun Li, “What Does an Electric Vehicle Replace,” National Bureau of Economic Research, Working Paper 25771, February 2021.