In response to the 2007-2009 financial crisis, in December 2008, the Federal Open Market Committee effectively cut its target for the federal funds to zero where it remained during the first six years of the recovery. In December 2015, Fed Chair Janet Yellen and the FOMC began the process of normalizing monetary policy by raising the target for the federal funds rate to 0.25 to 0.50 percent.

The FOMC raised the target several more times during the following years (Jerome Powell succeeded Janet Yellen as Fed Chair in February 2018) until it reached 2.25 to 2.50 percent in December 2018. In Chapter 27 of the textbook we discuss the fact that the experience of the Great Inlfation that had lasted from the late 1960s to the early 1980s had convinced many economists inside and outside of the Fed that if the unemployment rate declined below the natural rate of unemployment (also referred to as the nonaccelerating inflation rate of unemployment, or NAIRU), the inflation rate was likely to accelerate unless the FOMC increased its target for the federal funds rate. The actions the FOMC took starting in December 2015 were consistent with this view.

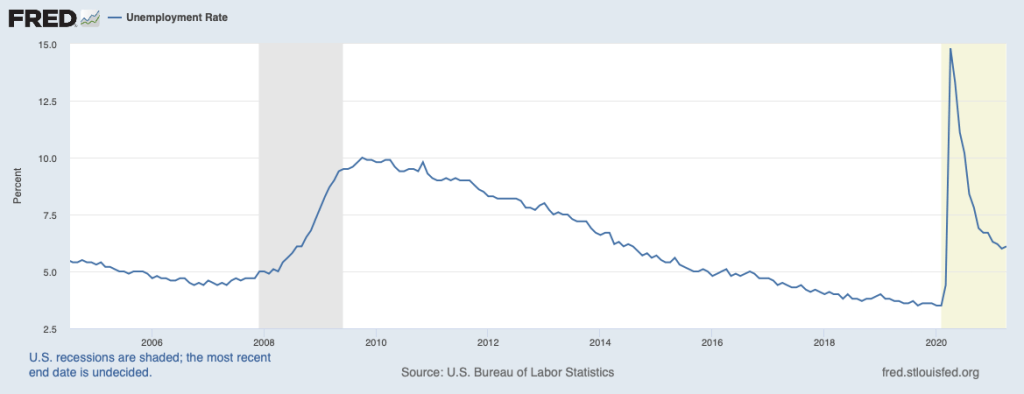

At the December 2015 meeting, the FOMC members gave their estimates of several key economic variables, including the natural rate of unemployment. At the time of the meeting, the unemployment rate was 5.0 percent. The average of the FOMC members’ estimates of the natural rate of unemployment was 4.9 percent. The inflation rate in December 2015 was 1.2 percent—well below the Fed’s target inflation rate of 2 percent. Although it might seem that with such a low inflation rate, the FOMC should not have been increasing the federal funds rate target, doing so was consistent with one of the lessons from the Great Inflation: Because monetary policy affects the economy with a lag, it’s important for the Fed to react before inflation begins to increase and a higher inflation rate becomes embedded in the economy. With many FOMC members believing that the NAIRU had been reached in December 2015, raising the federal funds rate from effectively zero seemed like an appropriate policy.

At least until the end of 2018, some members of the FOMC indicated publicly that they still believed that the Fed should pay close attention to the relationship between the natural rate of unemployment and the actual rate of unemployment. For example, in a speech delivered in December 2018, Raphael Bostic, president of the Federal Reserve Bank of Atlanta, who was serving that year on the FOMC, made the following points:

“[P]eriods of time when the actual unemployment rate fell below what the U.S. Congressional Budget Office now estimates as the so-called natural rate of unemployment … I refer to … as “high-pressure” periods. … Dating back to 1960, every high-pressure period ended in a recession. And all but one recession was preceded by a high-pressure period….

One potential consequence of overheating is that inflationary pressures inevitably build up, leading the central bank to take a much more “muscular” stance of policy at the end of these high-pressure periods to combat rising nominal pressures. Economic weakness follows. You might argue that the simple answer is to not respond so aggressively to building signs of inflation, but that would entail risks that few responsible central bankers would accept. It is true that the Fed and most other advanced-economy central banks have the luxury of solid credibility for achieving and maintaining their price stability goals. But we shouldn’t forget that such credibility was hard won. Inflation expectations are reasonably stable for now, but we know little about how far the scales can tip before it is no longer so.”

Bostic also noted in the speech that “it is very difficult to determine when the economy is actually overheating.” One indication of that difficulty is given by the following table, which shows how the average estimate by FOMC members of the natural rate of unemployment declined each year during the period in which they were raising the target for the federal funds rate.

| December 2015 | 4.9% |

| December 2016 | 4.8% |

| December 2017 | 4.7% |

| December 2018 | 4.4% |

| December 2019 | 4.1% |

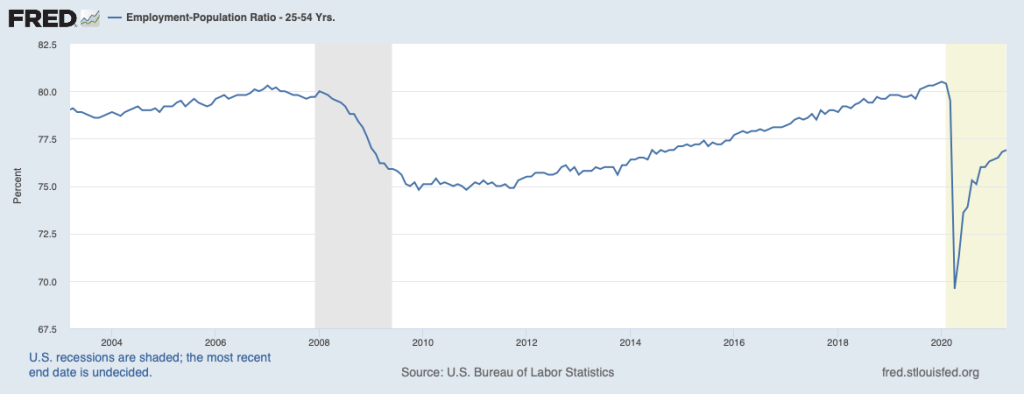

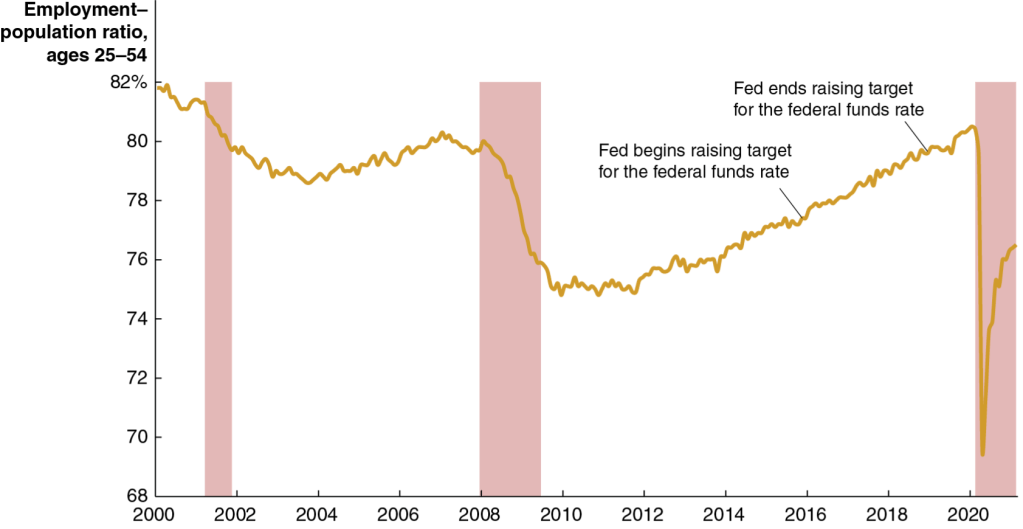

As we discuss in Chapter 19, Section 19.1 of the textbook, because of problems in measuring the actual unemployment rate and in estimating the natural rate of unemployment, some economists inside and outside of the Fed have argued that the employment-population ratio for prime age workers is a better measure of the state of the labor market. The following shows movements in the employment-population ratio for workers aged 25 to 54 between January 2000, when the ratio was near its post-World War II high, and February 2021.

The figure shows that in December 2015, when the Fed began to raise its target for the federal funds rate and when the average estimate of the FOMC members indicated that unemployment was at its natural rate, the employment-population rate was still 4.5 percentage points below its level of early 2000. The FOMC members do not report individual forecasts of the employment-population ratio. If they had focused on that measure rather than on the unemployment rate, they may have concluded that there was more slack in the labor market and, therefore, have been less concerned that inflation might be about to significantly increase.

In 2019, the Fed began to cut its target for the federal funds rate as the growth of real GDP slowed. In March 2020, following the start of the Covid-19 pandemic, the Fed cut the target back to 0 to 0.25 percent. During that time, some members of the FOMC and some economists outside of the Fed concluded that the Fed may have made a mistake by raising the target for the federal funds rate multiple times between 2015 and 2018. For example, Bostic in a speech in November 2020, noted that “the actual unemployment rate exceeded estimates of the NAIRU by an average of 0.8 percentage points each year” between 1979 and 2019. He concluded that “If estimates of the NAIRU are actually too conservative, as many would argue they have been …unemployment could have averaged one to two percentage points lower” between 1979 and 2019, which he argues would have been a particular benefit to black workers. In a speech in September 2020, Lael Brainard, a member of the Fed’s Board of Governors, noted that the Fed’s previous approach of making policy less expansionary “when the unemployment rate nears the [natural] rate in anticipation of high inflation that is unlikely to materialize risks an unwanted loss of opportunity for many Americans.”

in August 2020, the Fed announced the results of a review of its monetary policy. In a speech that accompanied the statement Fed Chair Jerome Powell noted that in attempting to achieve its mandate of high employment, the Fed faces the difficulty that “the maximum level of employment is not directly measurable and changes over time for reasons unrelated to monetary policy. The significant shifts in estimates of the natural rate of unemployment over the past decade reinforce this point.” Powell noted that the in the Fed’s new monetary policy statement, policy will depend on the FOMC’s: “’assessments of the shortfalls of employment from its maximum level’ rather than by ‘deviations from its maximum level’ as in our previous statement. This change may appear subtle, but it reflects our view that a robust job market can be sustained without causing an outbreak of inflation.”

At this point, the details of how the Fed’s new monetary policy strategy will be implemented are still uncertain. But it seems clear that the Fed has ended its approach dating back to the early 1980s of raising its target for the federal funds rate when the unemployment rate declined to or below the FOMC’s estimate of the natural rate of unemployment. Particularly after Congress and the Biden administration passed the $1.9 trillion American Rescue Plan in March 2021, some economists wondered whether the Fed’s new strategy might make it harder to counter an increase in inflation without pushing the U.S. economy into a recession. For instance, Olivier Blanchard of the Peterson Institute for International Economics argued that the combination of very expansionary fiscal and monetary policies might lead to a situation similar to the late 1960s:

“From 1961 to 1967, the Kennedy and Johnson administrations ran the economy above potential [GDP], leading to a steady decrease in the unemployment rate down to less than 4 percent. Inflation increased but not very much, from 1 percent to just below 3 percent, suggesting to many a permanent trade-off between inflation and unemployment. In 1967, however, inflation expectations started adjusting, and by 1969, inflation had increased to close to 6 percent and was then seen as a major issue. Fiscal and monetary policies tightened, leading to a recession from the end of 1969 to the end of 1970.”

Fed Chair Jerome Powell seems confident, however, that any increase in inflation will only be temporary. In testifying before Congress, he stated that: “We might see some upward pressure on prices [as a result of expansionary monetary and fiscal policy]. Our best view is that the effect on inflation will be neither particularly large nor persistent.”

Time will tell which side in what one economic columnist called the Great Overheating Debate of 2021 will turn out to be correct.

Sources: Neil Irwin, “If the Economy Overheats, How Will We Know?” New York Times, March 24, 2012; Olivier Blanchard, “In Defense of Concerns over the $1.9 Trillion Relief Plan,” piie.com, February 18, 2021; Paul Kiernan and Kate Davidson, “Powell Says Stimulus Package Isn’t Likely to Fuel Unwelcome Inflation,” Wall Street Journal, March 23, 2021; Federal Open Market Committee, “Minutes,” various dates; Lael Brainard, “Bringing the Statement on Longer-Run Goals and Monetary Policy Strategy into Alignment with Longer-Run Changes in the Economy,” September 1, 2020; Raphael Bostic, “Views on the Economic and Policy Outlook,” December 6, 2018; Raphael Bostic, “Racism and the Economy: Focus on Employment,” November 17, 2020; Jerome Powell, “New Economic Challenges and the Fed’s Monetary Policy Review,” August 27, 2020; and Federal Reserve Bank of St. Louis.