In respect to its mandate to achieve price stability, the Federal Open Market Committee focuses on data for the personal consumption expenditure (PCE) price index and the core PCE price index. (The core PCE price index omits food and energy prices, as does the core consumer price index.) After the March, June, September, and December FOMC meetings, each committee member projects future values of these price indexes. The projections, which are made public, provide a means for investors, businesses, and households to understand what the Fed expects to happen with future inflation.

In his press conference following the December 2021 FOMC meeting, Chair Jerome Powell surprised some economists by discussing the importance of the employment cost index (ECI) in the committee’s evaluation of the current state of inflation. Powell was asked this question by a journalist: “I wonder if you could talk a little bit about what prompted your recent pivot toward greater wariness around inflation.” He responded, in part:

“We got the ECI reading on the eve of the November meeting—it was the Friday before the November meeting—and it was very high, 5.7 percent reading for the employment compensation index for the third quarter … That’s really what happened [that resulted in FOMC deciding to focus more on inflation]. It was essentially higher inflation and faster—turns out much faster progress in the labor market.”

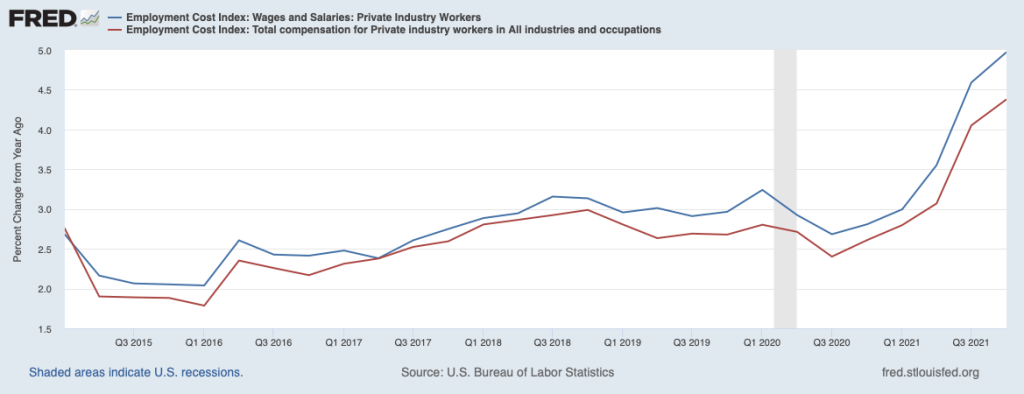

The ECI is compiled by the Bureau of Labor Statistics and is published quarterly. It measures the cost to employers per employee hour worked. The BLS publishes data that includes only wages and salaries and data that includes, in addition to wages and salaries, non-wage benefits—such as contributions to retirement accounts or health insurance—that firms pay workers. The figure below shows the ECI including just wages and salaries (red line) and including all compensation (blue line). The difference between the two lines shows that wages and salaries have been increasing more rapidly than has total compensation.

A focus on the labor market when analyzing inflation is unsurprising. In Macroeconomics, Chapter 17, Section 17.1 (Economics, Chapter 27, Section 27.1) we discuss how the Phillips curve links the state of the labor market—as measured by the unemployment rate—to the inflation rate. The link between the unemployment rate and the inflation rate operates through the labor market: When the unemployment rate is low, firms raise wages as they attempt to attract the relatively small number of available workers and to keep their own workers from leaving. (As first drawn by economist A.W. Phillips, the Phillips curve showed the relationship between the unemployment rate and the rate of wage inflation, rather than the relationship between the unemployment rate and the rate of price inflation.) As firms’ wage costs rise, they increase prices. So, as Powell noted, we would expect that if wages are rising rapidly, the rate of price inflation will also increase.

Powell noted that the FOMC is concerned that rising wages might eventually lead to a wage-price spiral in which higher wages lead to higher prices, which, in turn, cause workers to press for higher nominal wages to keep their real wages from falling, which then leads firms to increases their prices even more, and so on. Some economists interpret the inflation rates during the Great Inflation for 1968–1982 as resulting from a wage-price spiral. One condition for a wage-price spiral to begin is that workers and firms cease to believe that the Fed will be able to return to its target inflation rate—which is currently 2 percent.

In terms of the Phillips curve analysis of Chapter 17, a wage-price spiral can be interpreted as a shifting up of the short-run Phillips curve. The Phillips curve shifts up when households, firms, and investors increase their expectations of future inflation. We discuss this process in Chapter 17, Section 17.2. As the short-run Phillips curve shifts up the tradeoff between inflation and unemployment becomes worse. That is, the inflation rate is higher at every unemployment rate. For the Fed to reduce the inflation rate—bring it back down to the Fed’s target—becomes more difficult without causing a recession. The Great Inflation was only ended after the Fed raised its target for the federal funds rate to levels that helped cause the severe recession of 1981–1982.

The FOMC has been closely monitoring movements in the ECI to make sure that it heads off a wage-price spiral before it begins.

Sources: The transcript of Chair Powell’s press conference can be found here; the most recent economic projections of FOMC members can be found here; and a news article discussing Powell’s fears of a wage-price spiral can be found here (subscription may be required).