On January 5, 2025 at the American Economic Association meetings in San Francisco, Jason Furman of Harvard’s Kennedy School, former Federal Reserve Chair Ben Bernanke (now of the Brookings Institution), former Council of Economic Advisers Chair Christina Romer of the University of California, Berkeley, and John Cochrane of Stanford’s Hoover Institition participated in a panel on “Inflation and the Macroeconomy.”

The discussion provides an interesting overview of a number of macroeconomic topics including:

The roles of aggregate demand shocks and aggregate supply shocks in explaining the sharp increase of inflation beginning in the spring of 2021.

The reasons for the Fed’s delay in responding to the increase in inflation.

Why macroeconomic forecasting models and most economists failed to anticipate the rise in inflation.

The role of the Fed’s 2020 monetary policy framework, how the Fed should revise the framework as a result of the review currently underway, and whether the Fed should change its inflation target. (We discuss the Fed’s monetary policy framework in several blog posts, including this one.)

The likely future course of inflation and the potential effects of the Trump Administration’s policies.

The likely consequences of large federal budget deficits.

Threats to Fed independence.

The discussion is fairly long at two hours, but most of it is nontechnical and should be understandable by students who have reached the monetary and fiscal policy chapters of a macroeconomic principles course (Chapters 15 and 16 of Macroeconomics; Chapters 25 and 26 of Economics).

As we discussed in this blog post on Wednesday, the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) voted to reduce its target for the federal funds rate by 0.25 percentage point. After the meeting, the committee released its “Summary of Economic Projections” (SEP). The SEP showed that the committee’s forecasts of the inflation rate as measured by the personal consumption expenditures (PCE) price index for this year and next year are both higher than the committee had forecast in September, when the last SEP was released. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target.

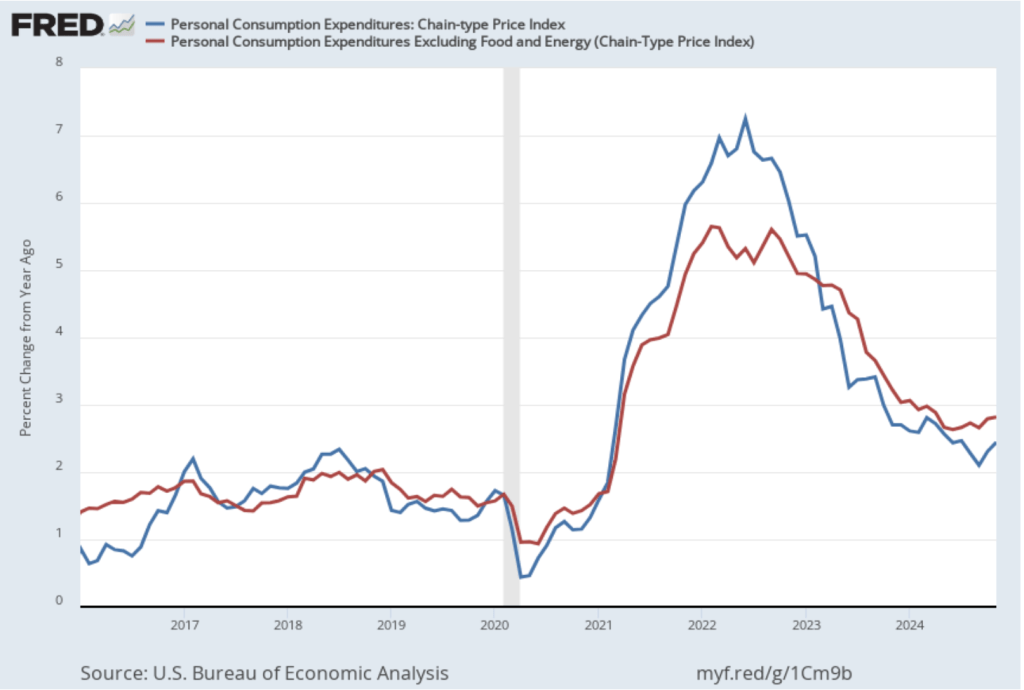

This morning (December 20), the BEA released monthly data on the PCE price index as part of its “Personal Income and Outlays” report for November.

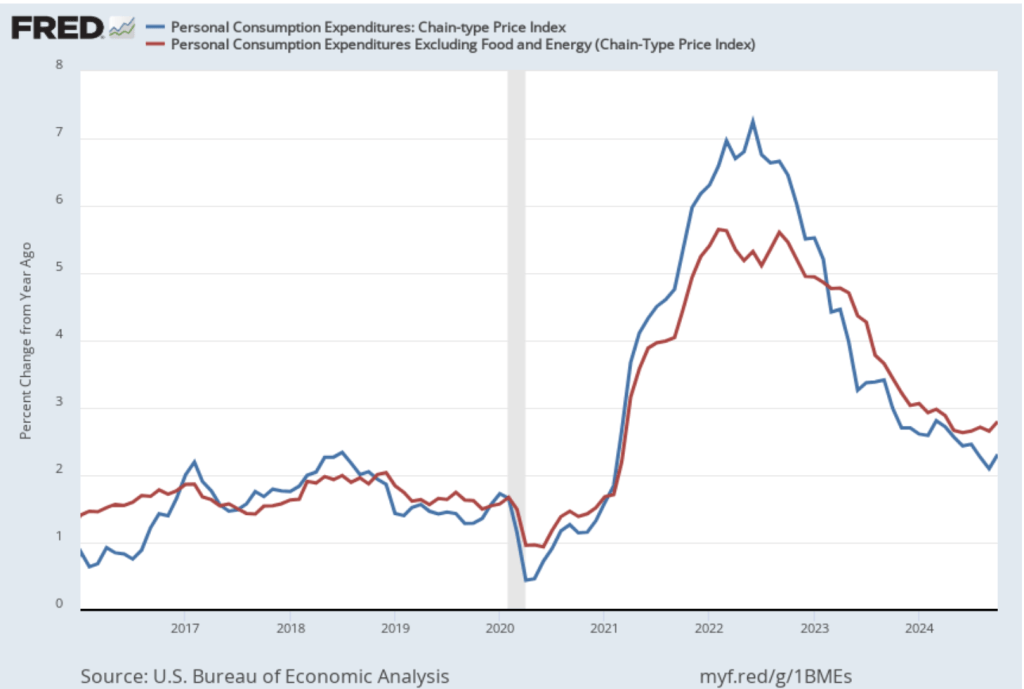

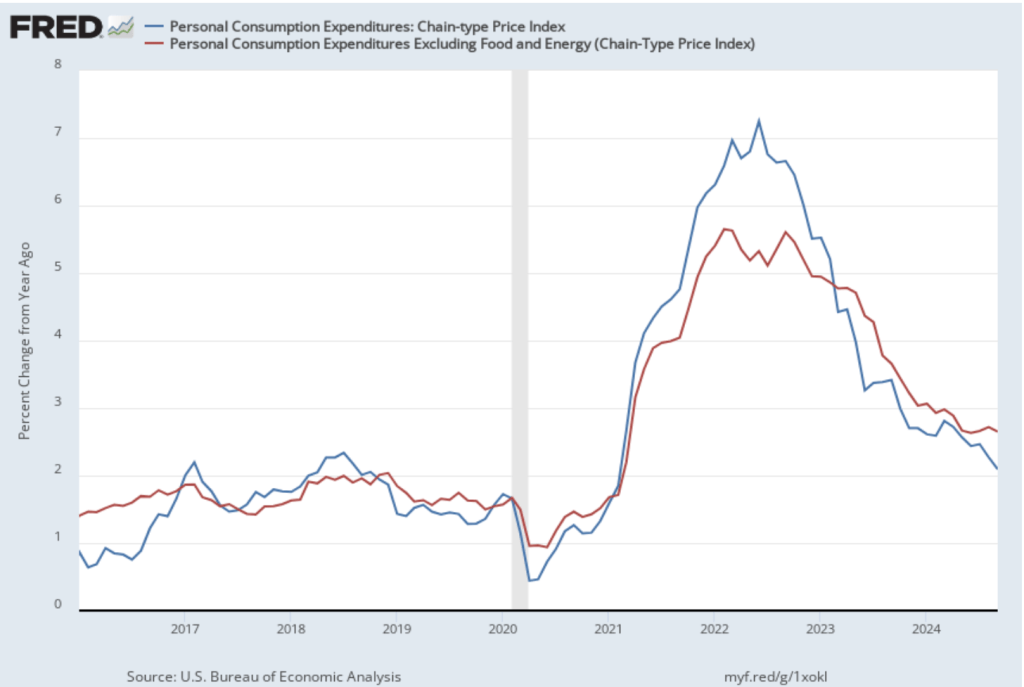

The following figure shows PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2016 with inflation measured as the percentage change in the PCE from the same month in the previous year. Measured this way, in November PCE inflation was 2.4 percent, up from 2.3 percent in October. Core PCE inflation in November was 2.8 percent, unchanged from October. Both PCE inflation and core PCE inflation were slightly lower than the expectations of economists surveyed before the data were released.

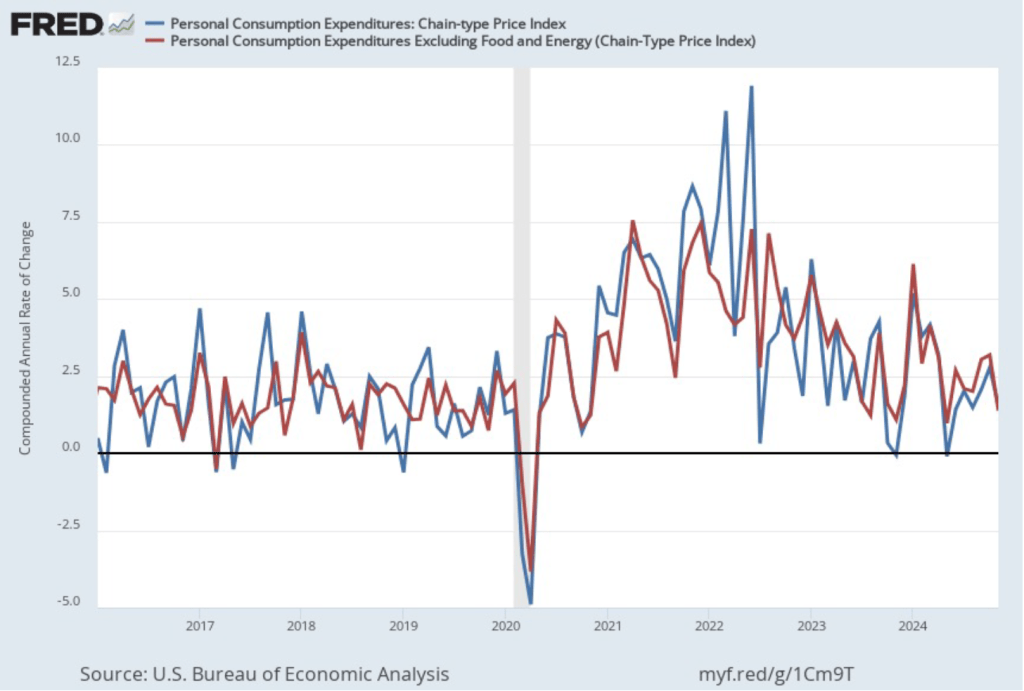

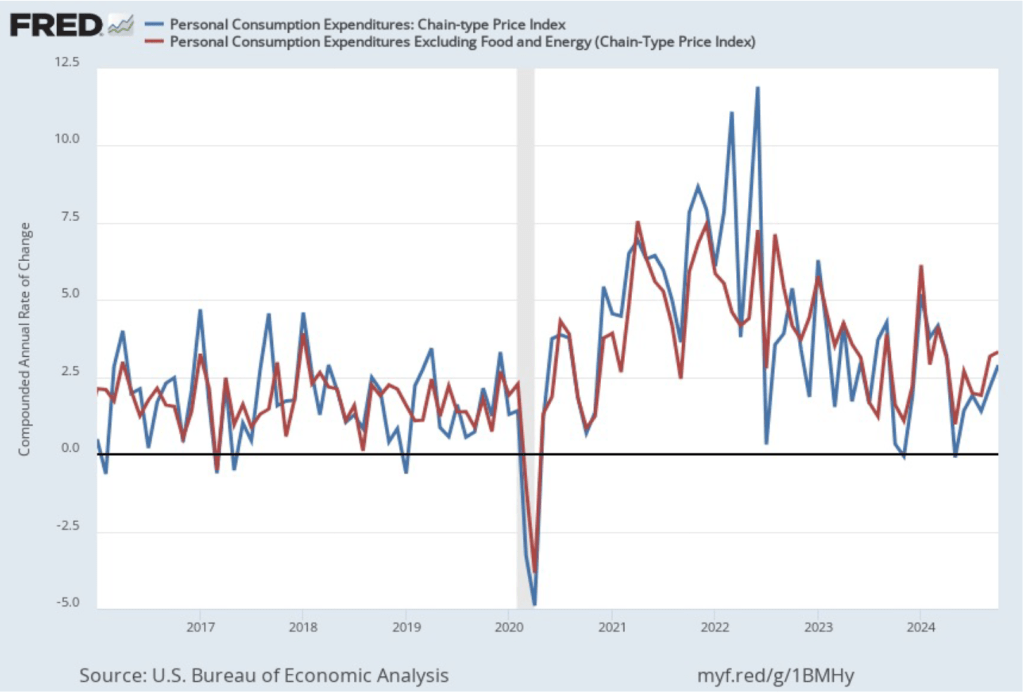

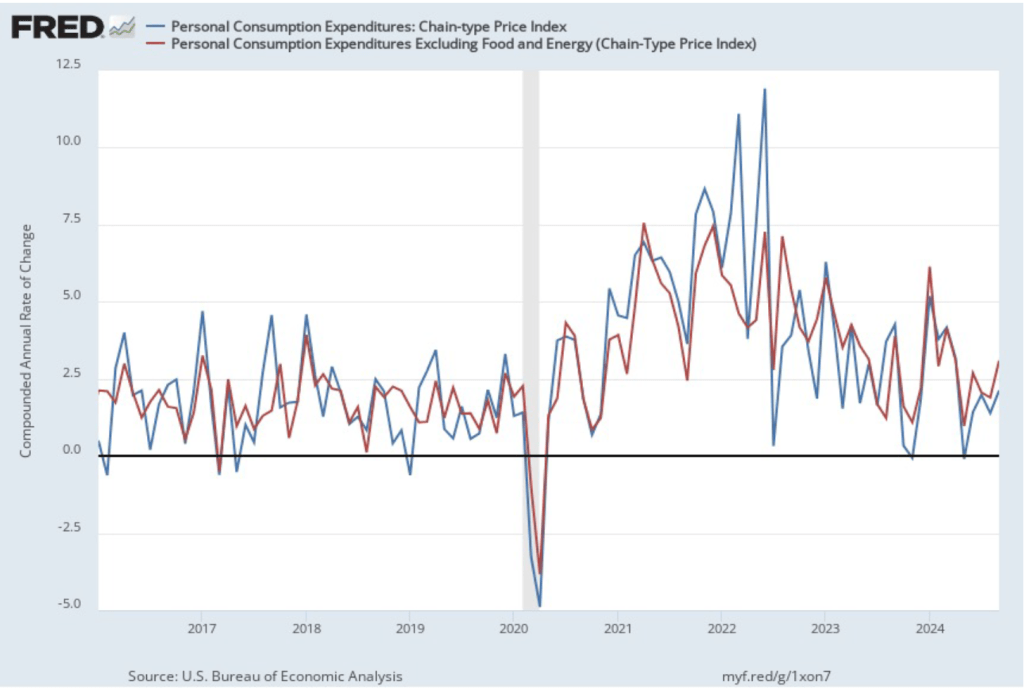

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation fell sharply in November to 1.5 percent from 2.8 percent in October. Core PCE inflation also fell from 3.2 percent in October to 1.4 percent in November. Although both 12-month PCE inflation and 12-month core PCE inflation remained above the Fed’s 2 percent annual inflation target, 1-month PCE inflation and 1-month core PCE inflation dropped to well below the inflation target. But the usual caution applies that data from one month shouldn’t be overly relied on; it’s far too soon to draw the conclusion that inflation is likely to remain below the 2 percent target in future months.

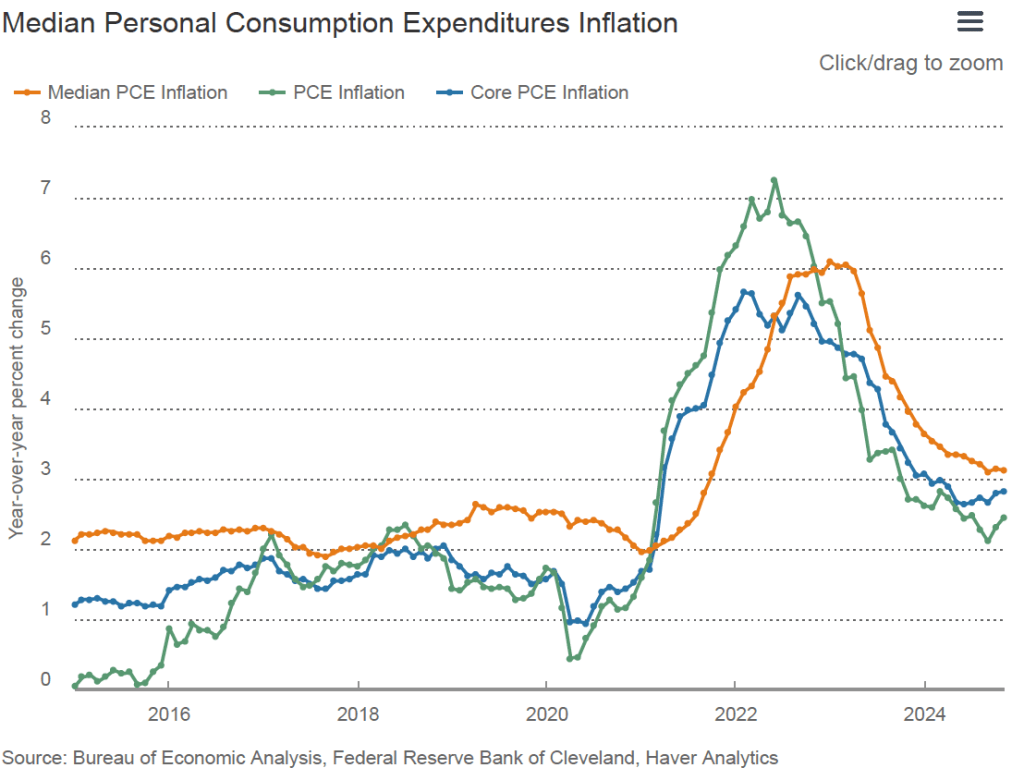

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University as another way of measuring the underlying trend in inflation. If we listed the inflation rate for each individual good or service included in the PCE, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates. The following figure from the Federal Reserve Bank of Cleveland includes, along with PCE inflation (the green line) and core PCE inflation (the blue line), median PCE inflation (the orange line). All three inflation rates are measured over 12 months. Median PCE inflation in November was 3.1 percent, unchanged from October.

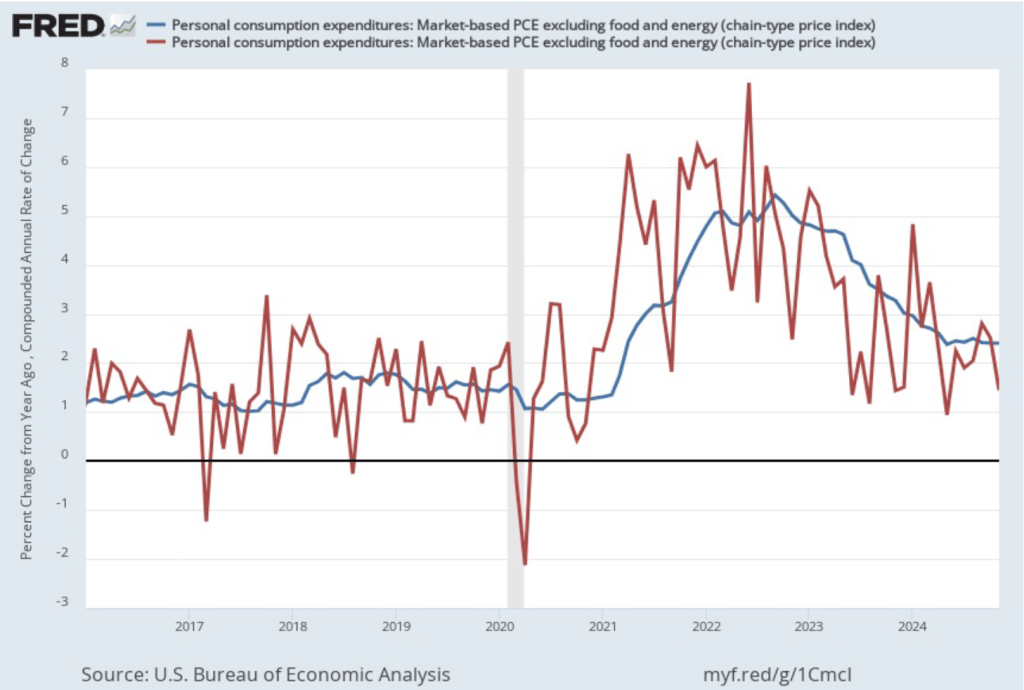

In his press conference earlier this week, Fed Chair Jerome Powell noted that: “we’ve had recent high readings from non-market services.” Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices rise, the prices of financial services included in the PCE price index also rise. Powell argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month inflation (the blue line) and 1-month inflation (the red line) for market-based PCE, excluding the prices of food and energy. (The BEA explains the market-based PCE measure here.)

These measures of inflation tell a similar story to the measures considered earlier: 12-month inflation continues to run above the Fed’s 2 percent inflation target, while 1-month inflation slowed significantly in November and is below the 2 percent target. By this measure 12-month inflation was unchanged in November at 2.4 percent, while 1-month inflation declined from 2.5 percent in October to 1.4 percent in November.

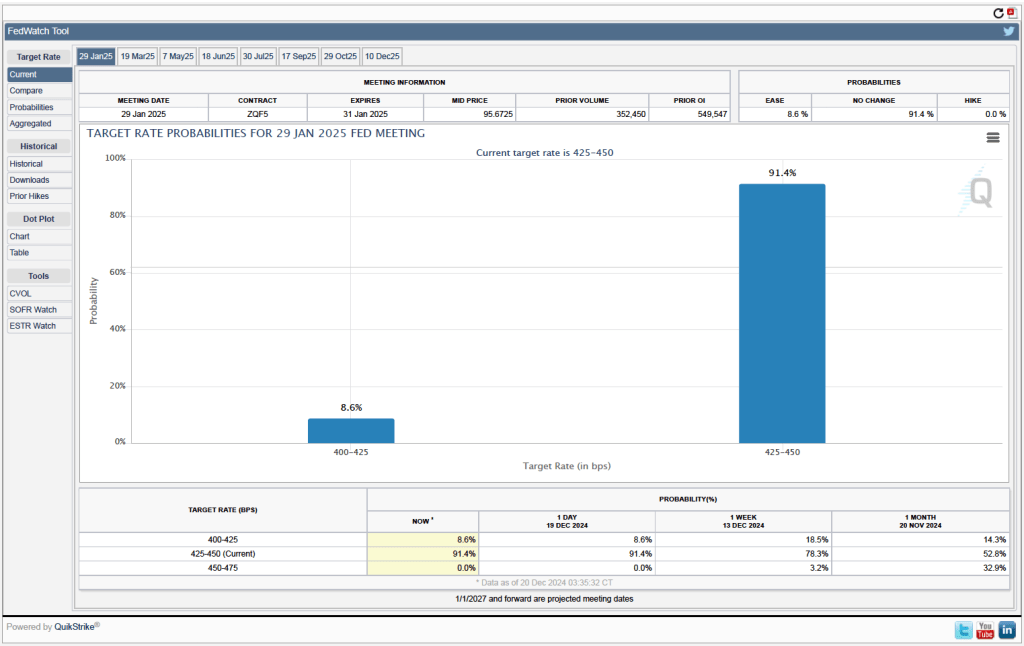

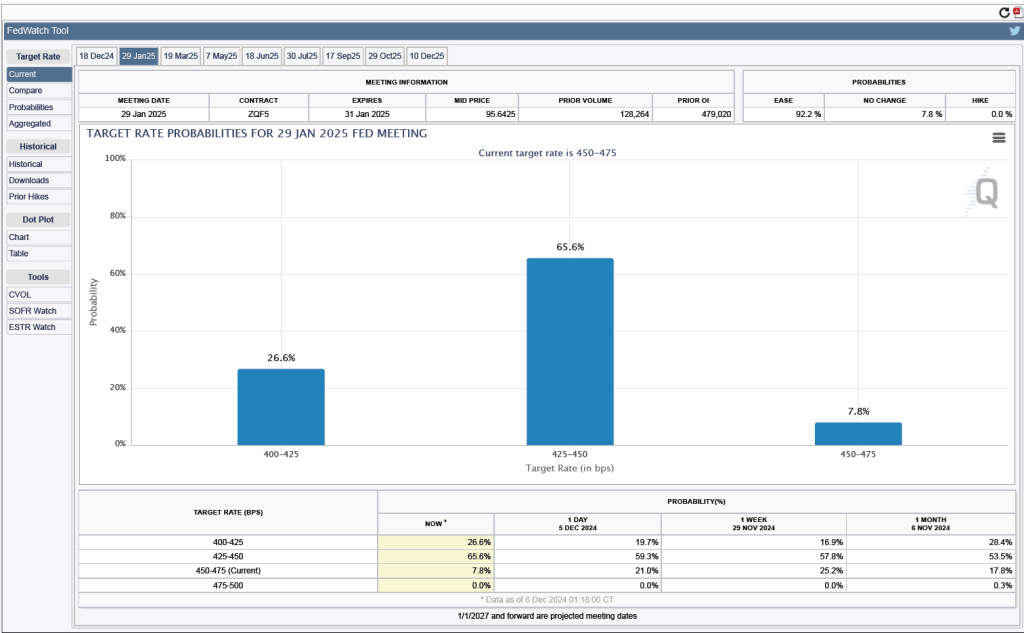

To summarize, the less volatile 12-month measures of inflation show it to be persistently above the Fed’s target, while the more volatile 1-month measures show inflation to have fallen below target. If the FOMC were to emphasize the 1-month measures, we might expect them to continue cutting the target for the federal funds rate at the committee’s next meeting on January 28-29. The more likely outcome is that, unless other macroeconomic data that are released between now and that meeting indicate a significant strengthening or weakening of the economy, the committee will leave its target for the federal funds rate unchanged. (The BEA’s next release of monthly PCE data won’t occur until January 31, which is after the FOMC meeting.)

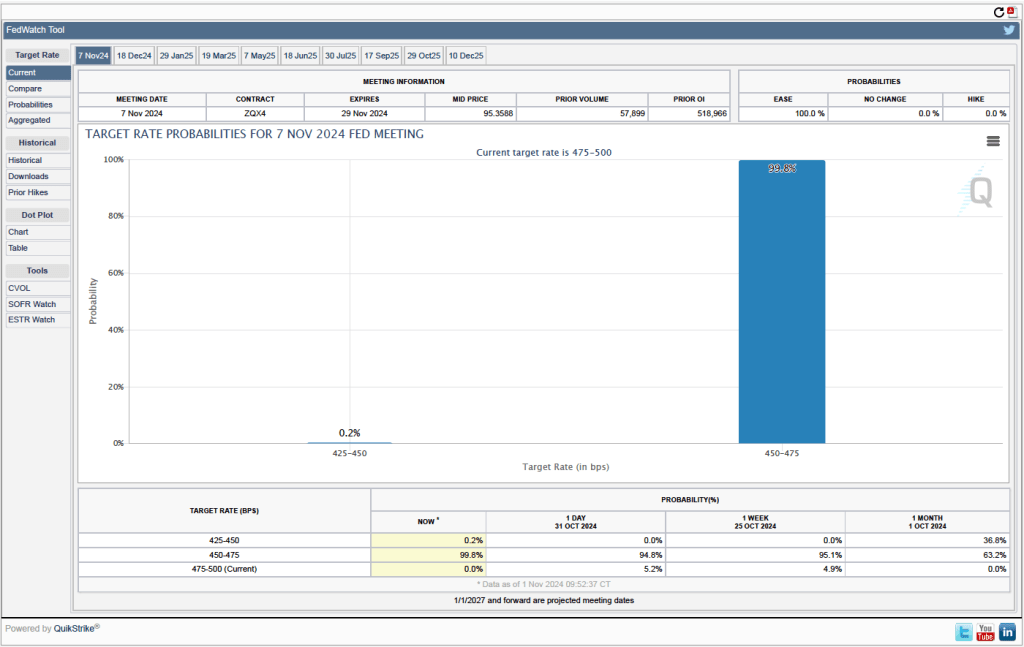

Investors who buy and sell federal funds futures contracts expect that the FOMC will leave its federal funds rate target unchanged at its next meeting. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, investors assign a probability of 91.4 percent to the FOMC leaving its target for the federal funds rate at the current range of 4.25 percent to 4.50. Investors assign a probability of only 8.6 percent to the FOMC cutting its target by 0.25 percentage point.

Federal Reserve Chair Jerome Powell speaks at a press conference following a meeting of the Federal Open Market Committee. (Photo from federalreserve.gov)

Members of the Fed’s Federal Open Market Committee (FOMC) had signaled that the committee was likely to cut its target range for the federal funds rate by 0.25 percentage point (25 basis points) at its meeting today (December 18). As we noted in this recent post, investors had overwhelming expected a cut of this size. Although the committee followed through with a 25 basis point cut, Fed Chair Jerome Powell noted in a press conference following the meeting that it was a “closer call” than were the two earlier cuts this year. The statement the committee released after the meeting showed that only one member—Beth M. Hammack, president of the Federal Reserve Bank of Cleveland—ended up voting against the decision to cut the target rate.

In his press conference, Powell noted that although there were some indications that the labor market has weakened, the committee believed that unemployment was likely to remain near the natural rate. The committee also saw real GDP increasing at a steady rate. Powell stated that he was optimistic about the economy and that “I expect another good year next year.” The main obstacle to the committee fulfilling its dual mandate for full employment and price stability is that inflation remains persistently above the Fed’s target of a 2 percent annual inflation rate.

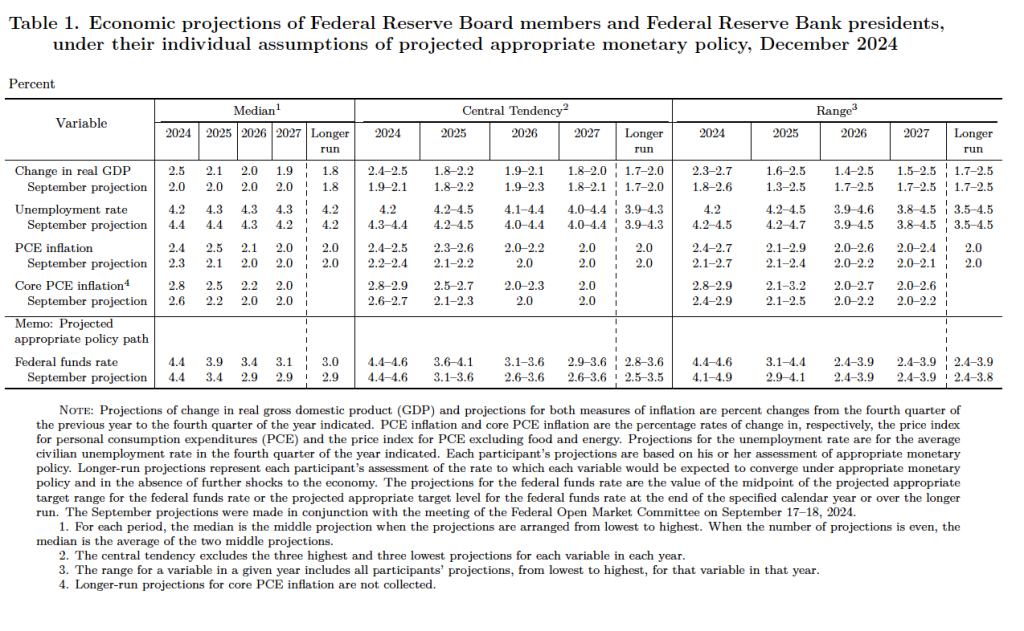

After the meeting, the committee also released a “Summary of Economic Projections” (SEP)—as it typically does at its March, June, September, and December meetings. The SEP presents median values of the committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release.

The forecasts mirror the points that Powell made in his news conference:

Committee members now forecast that GDP will be higher in 2024, and that the unemployment rate will be lower, than they had forecast in September.

Committee members now forecast that both personal consumption expenditures (PCE) price inflation and core PCE inflation will be slightly higher in 2024 than they had forecast in September.

Most notably, whereas in September committee members had forecast that PCE inflation would be 2.1 percent in 2025, they now forecast it will be 2.5 percent—notably higher. And committee members now forecast that inflation will not fall to the Fed’s 2 percent target until 2027, rather than 2026.

Finally, committee members now project that the federal funds rate will end 2025 50 basis points lower than it is now, rather than 100 basis points lower. In other words, committee members ares now forecasting only two 25 basis point cuts in the target next year rather than the four cuts they had forecast in September.

In his press conference, Powell noted that the main reason that PCE inflation remains high is that inflation in the prices of housing services has been running high, as have the prices of some other services. Noting that monetary policy affects the economy “with long and variable lags,” Powell stated that he believes that inflation is still on track to fall to the 2 percent target.

Given that inflation has been running closer to 2.5 percent and that the committee expects the inflation rate will still be 2.5 percent next year, a reporter asked Powell if the committee had considered the possibility of accepting a 2.5 percent inflation rate in the long run. Powell replied that: “No. We’re not going to settle for [2.5 percent inflation].” He stated that a 2 percent inflation rate is what the Fed “owes the public.”

Finally, Powell indicated that the committee would have to take into account the effects of the incoming Trump Administration’s fiscal policy actions—particularly tariff increases—when they occur. President Trump has stated that he would like to see interest rates decline more quickly, so the committee may face criticism for keeping the target for the federal funds rate higher next year than they had originally intended.

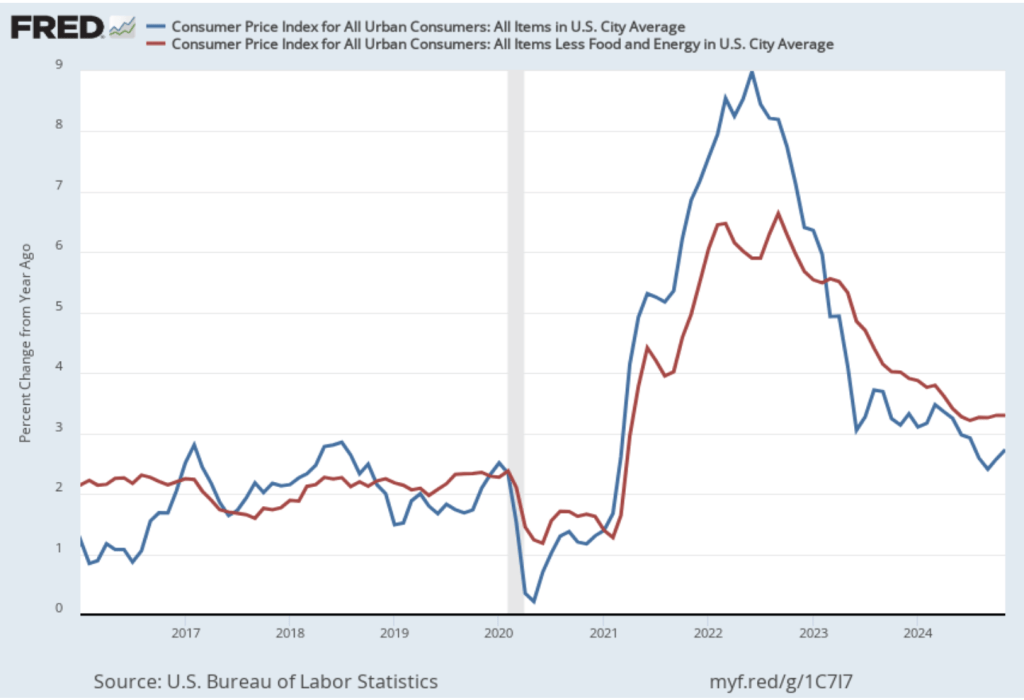

On December 11, the Bureau of Labor Statistics (BLS) released its monthly report on the consumer price index (CPI). The following figure compares headline inflation (the blue line) and core inflation (the red line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous month, was 2.7 percent—up from 2.6 percent in October.

The core inflation rate,which excludes the prices of food and energy, was unchanged at 3.3 percent for the fourth month in a row.

Both headline inflation and core inflation were the same as economists surveyed by the Wall Street Journal had expected.

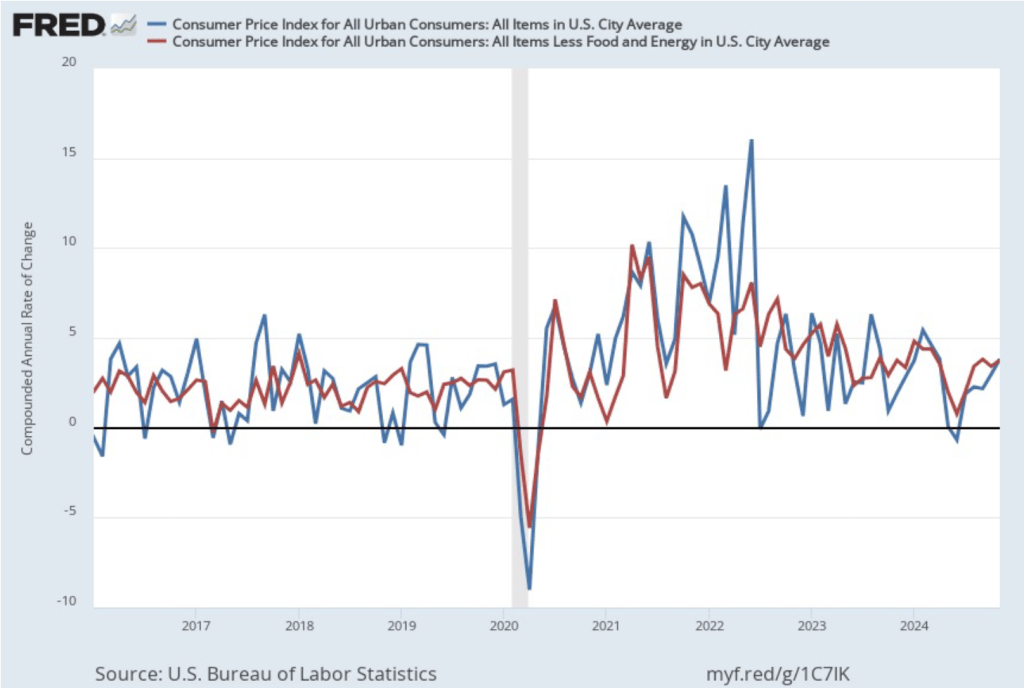

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) increased sharply from 3.0 percent in October to 3.8 percent in November. Core inflation (the red line) increased from 3.4 percent in October to 3.8 percent in November.

Overall, considering 1-month and 12-month inflation together, the U.S. economy may still be on course for a soft landing—with the annual inflation rate returning to the Fed’s 2 percent target without the economy being pushed into a recession. However, progress on lowering inflation has slowed or, possibly, stalled. So, the probability of a “no landing” outcome, with inflation remaining above the Fed’s target for an indefinite period, seems to have increased.

The relatively high rates of core inflation in both the 12-month and 1-month measures are concerning because most economists believe that core inflation is a better indicator of the underlying inflation rate than is headline inflation. It’s important not to overinterpret the data from a single month, although this is the fourth month in a row that core inflation has been above 3 percent. (Note, that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI in evaluating whether it is hitting its 2 percent inflation target.)

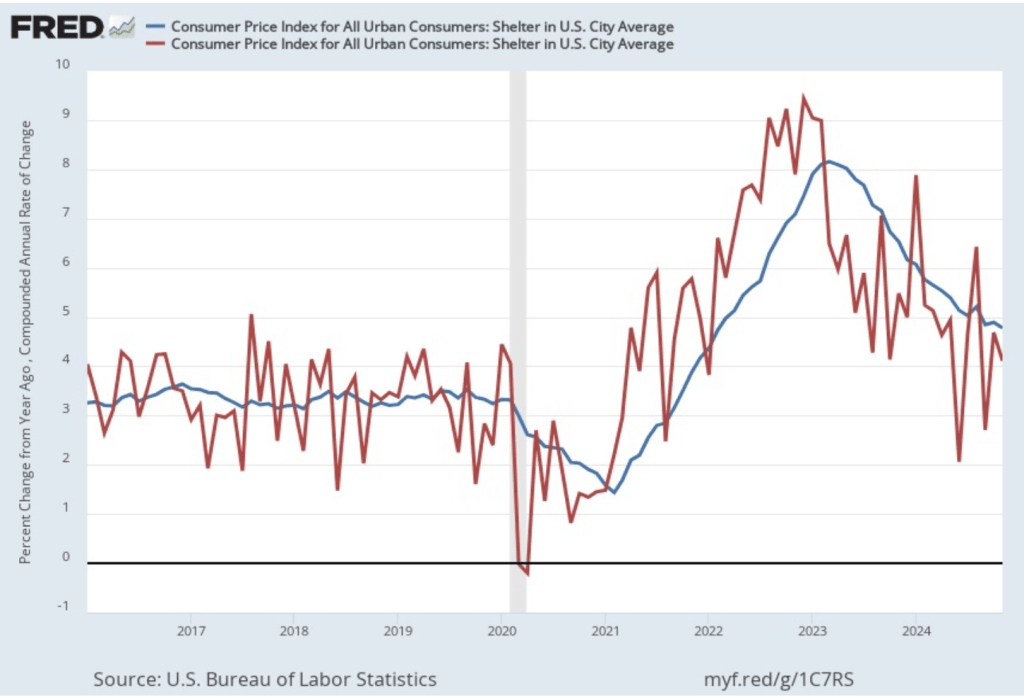

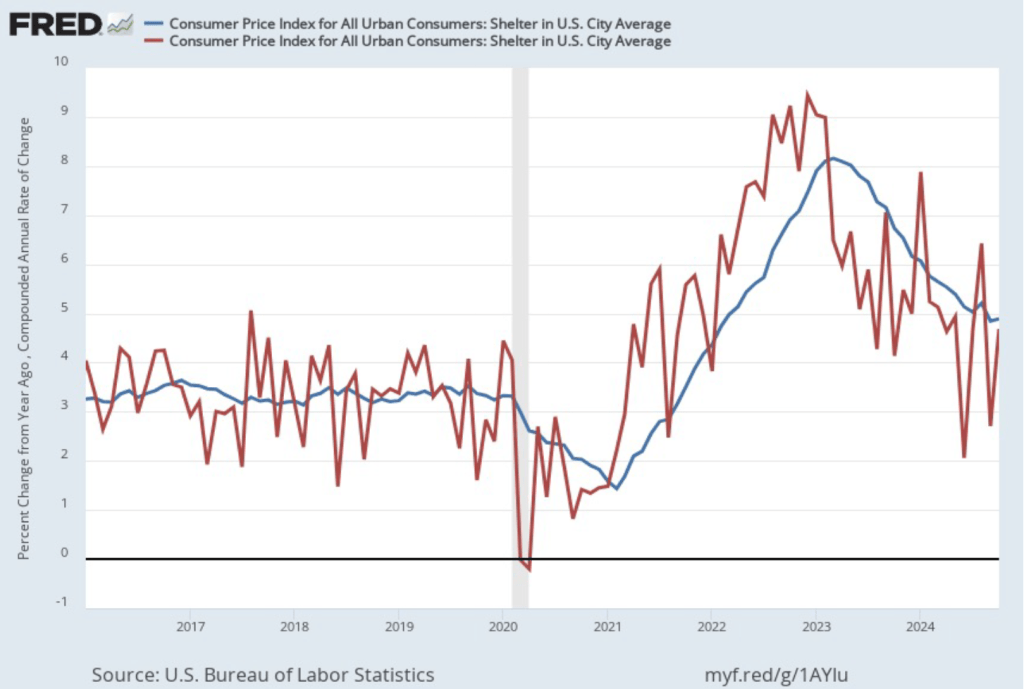

As we’ve discussed in previous blog posts, Federal Reserve Chair Jerome Powell and his colleagues on the Fed’s policymaking Federal Open Market Committee (FOMC) have been closely following inflation in the price of shelter. The price of “shelter” in the CPI, as explained here, includes both rent paid for an apartment or house and “owners’ equivalent rent of residences (OER),” which is an estimate of what a house (or apartment) would rent for if the owner were renting it out. OER is included in the CPI to account for the value of the services an owner receives from living in an apartment or house.

As the following figure shows, inflation in the price of shelter has been a significant contributor to headline inflation. The blue line shows 12-month inflation in shelter, and the red line shows 1-month inflation in shelter. Twelve-month inflation in shelter has been declining since the spring of 2023, but in November it was at a still high 4.8 percent. One-month inflation in shelter—which is much more volatile than 12-month inflation in shelter—fell from 4.7 percent in October to 4.1 percent in November.

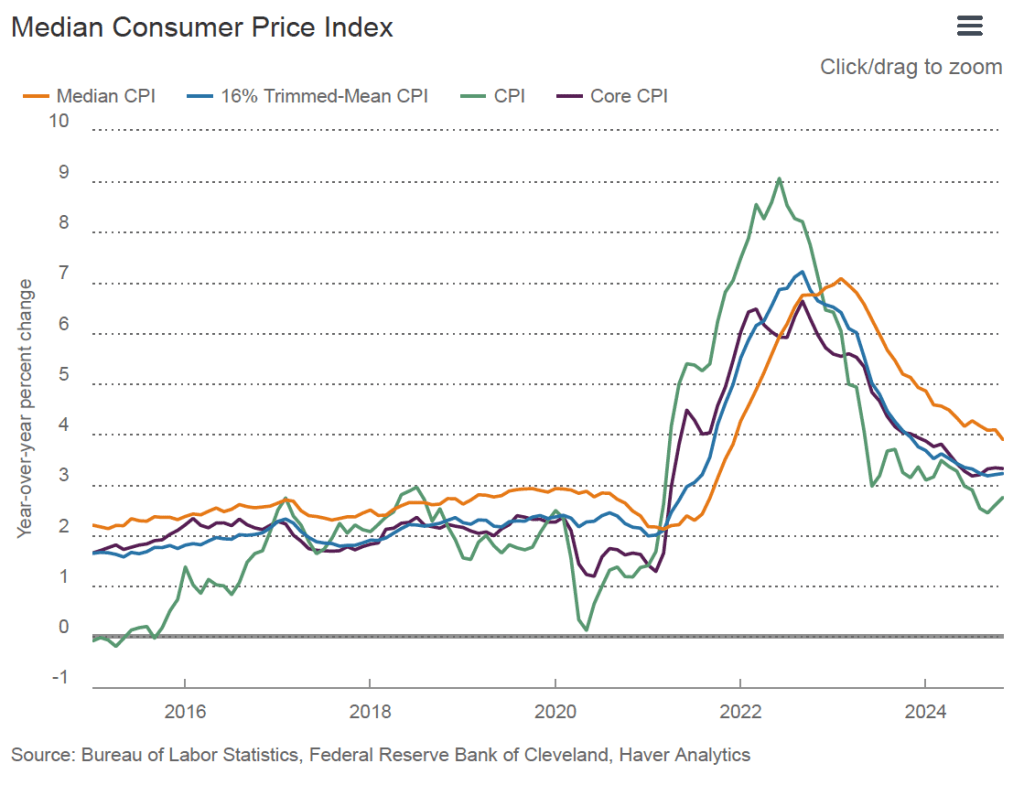

To better estimate of the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed mean inflation drops the 8 percent of good and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure is from the Federal Reserve Bank of Cleveland. It shows that median inflation (the orange line) fell from 4.1 percent in October to 3.9 percent in November. Trimmed mean inflation (the blue line) was unchanged at 3.2 percent for the fourth month in a row. These data provide confirmation that (1) core CPI inflation at this point is likely running higher than a rate that would be consistent with the Fed achieving its inflation target, and (2) that progress toward the target has slowed.

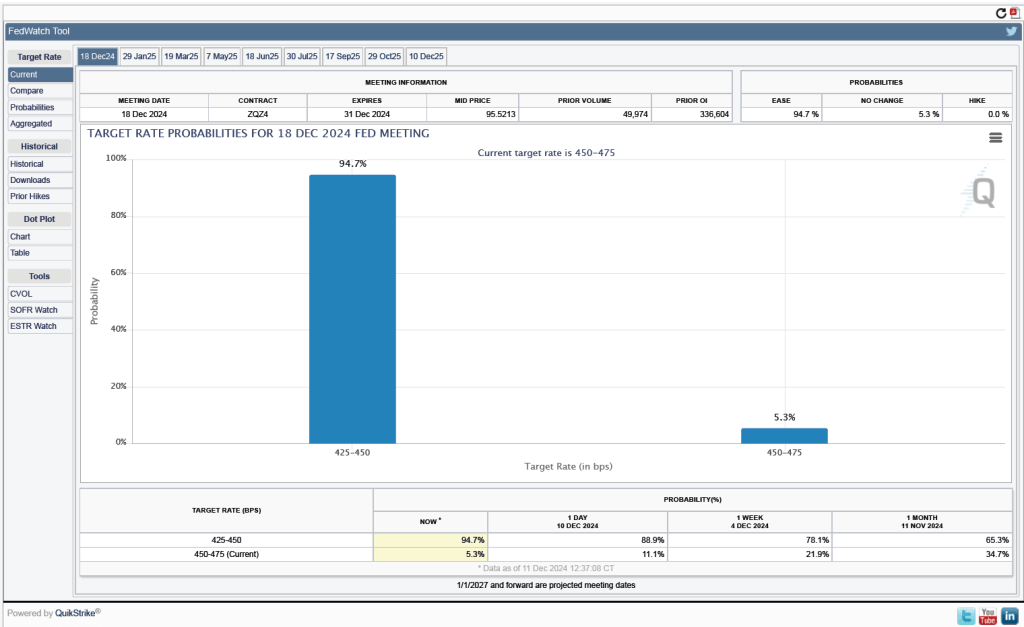

Will this persistence in inflation above the Fed’s 2 percent target cause the FOMC to hold constant its target range for the federal funds rate? Investors who buy and sell federal funds futures contracts still expect that the FOMC will cut its target for the federal funds rate by 0.25 percentage point at its next meeting on December 17-18. (We discuss the futures market for federal funds in this blog post.) The following figure shows that today these investors assign a probability of 94.7 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point and a probability of only 5.3 percent to the committee leaving its target unchanged at its current range of 4.50 percent to 4.75 percent.

An image generated by GTP-4o of people going to work.

The Federal Reserve’s policymaking Federal Open Market Committee (FOMC) has its next meeting on December 17-18. Although the committee is expected to lower its target range for the federal funds rate at that meeting, some members of the committee have been concerned that inflation has remained above the committee’s 2 percent annual target. For instance, in an interview on December 4, Fed Chair Jerome Powell said: “Growth is definitely stronger than we thought, and inflation is coming a little higher. The good news is that we can afford to be a little more cautious as we try to find [the] neutral [federal funds rate].”

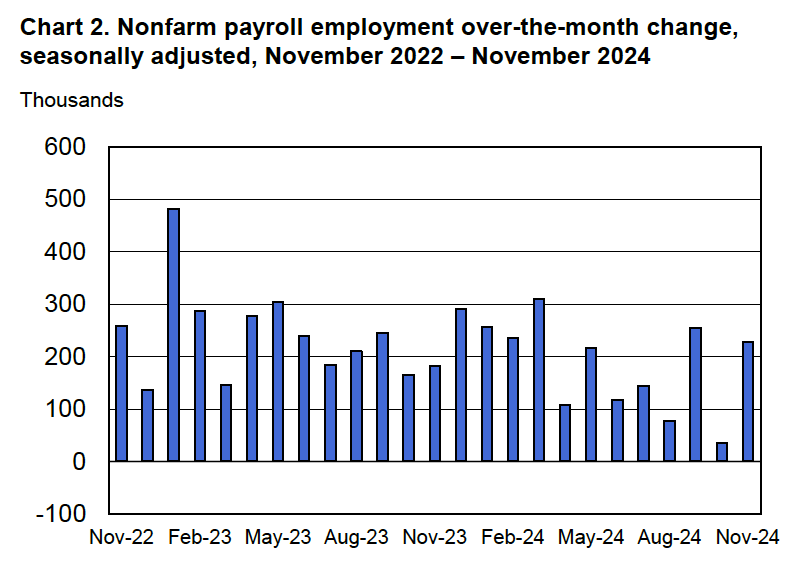

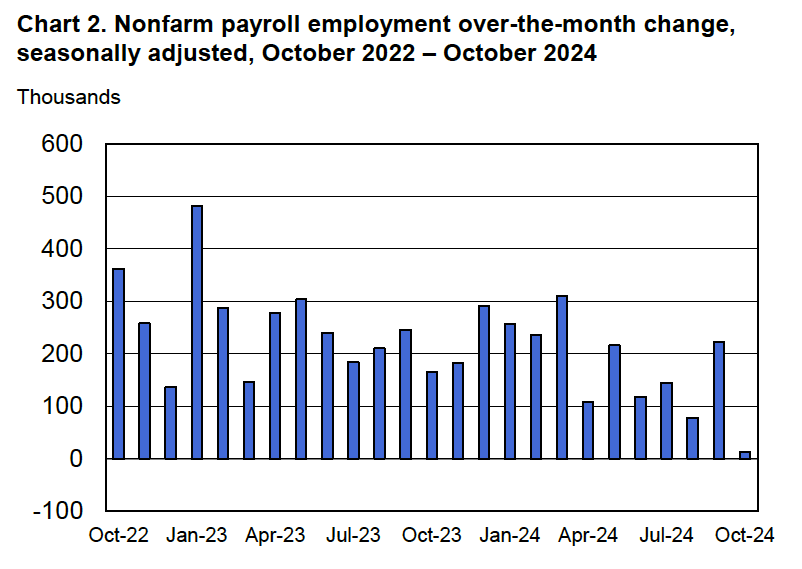

This morning (December 6), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for November. The report provided data indicating that the labor market remained strong—perhaps stronger than is consistent with the FOMC being willing to rapidly cut its federal funds rate target. The data in the October report (which we discussed in this blog post) were distorted by the effects of hurricanes and strikes. Today’s report indicated a bounce back in the labor market as many workers in areas affected by hurricanes returned to work and key strikes ended.

Economists who had been surveyed by the Wall Street Journal had forecast that payroll employment, as reported in the establishment survey, would increase by 214,000. The BLS reported that payroll employment in November had increased by 227,000, slightly above expectations. The unemployment rate—which is calculated from data in the household survey—was 4.2 percent, up slightly from 4.1 percent in October. In addition, the BLS revised upward its estimates of the employment increases in September and October by a total of 56,000. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure, taken from the BLS report, shows the net changes in employment for each month during the past two years.

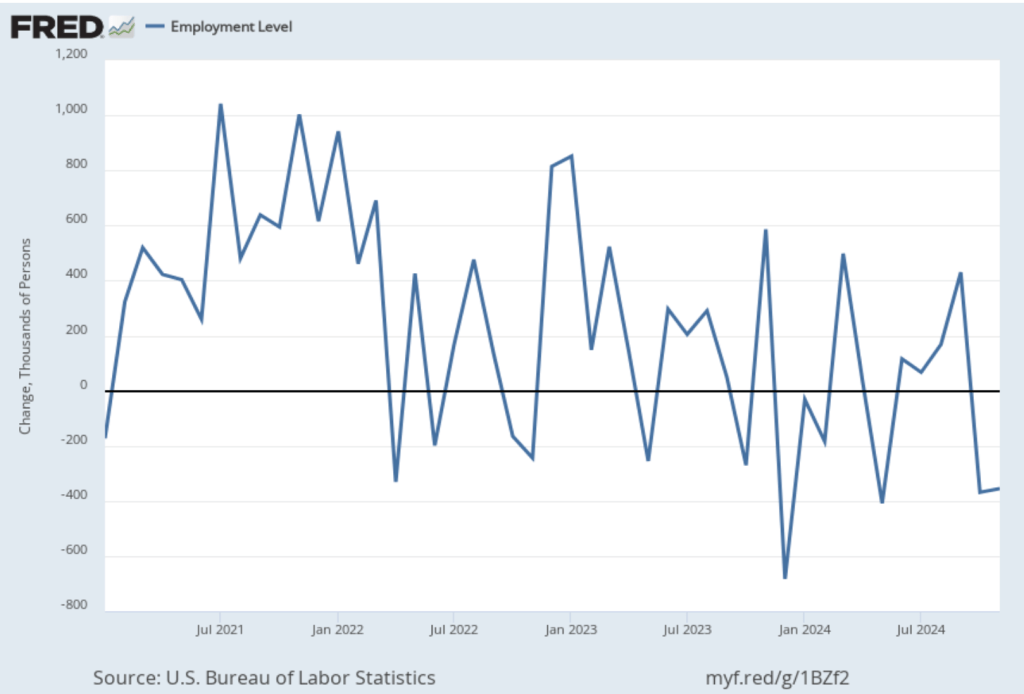

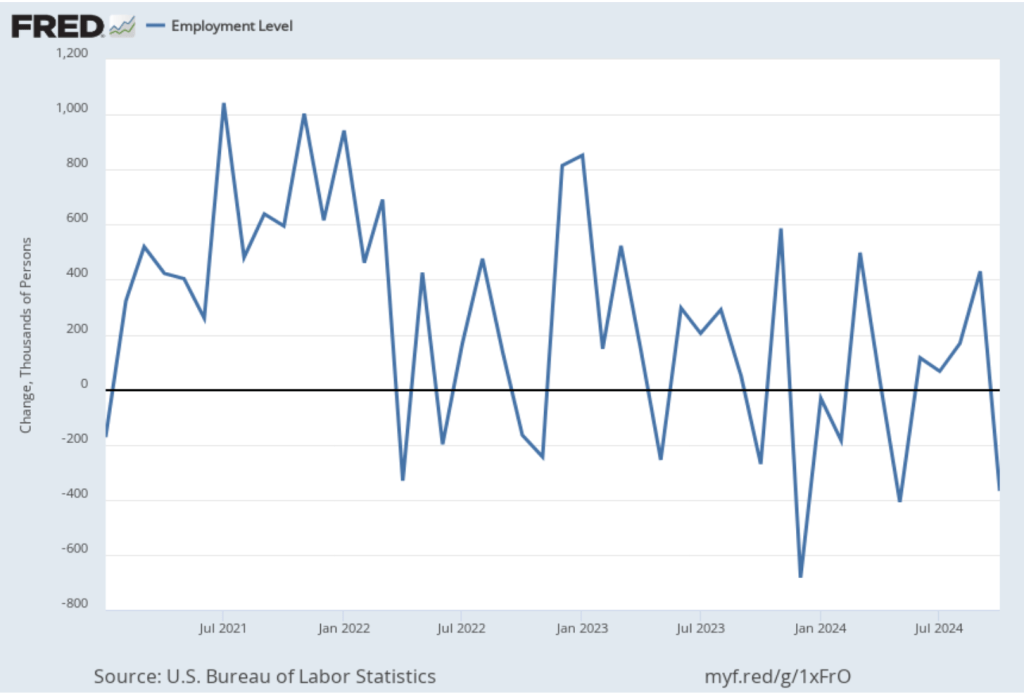

As the following figure shows, the net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. The net change in jobs as measured by the household survey for November was a decline of 355,000 jobs following a decline of 368,000 jobs in October. So, the story told by the two surveys is somewhat at odds, with a solid employment gain in the establishment survey contrasted with a significant employment decline in the household survey. (In this blog post, we discuss the differences between the employment estimates in the household survey and the employment estimates in the establishment survey.)

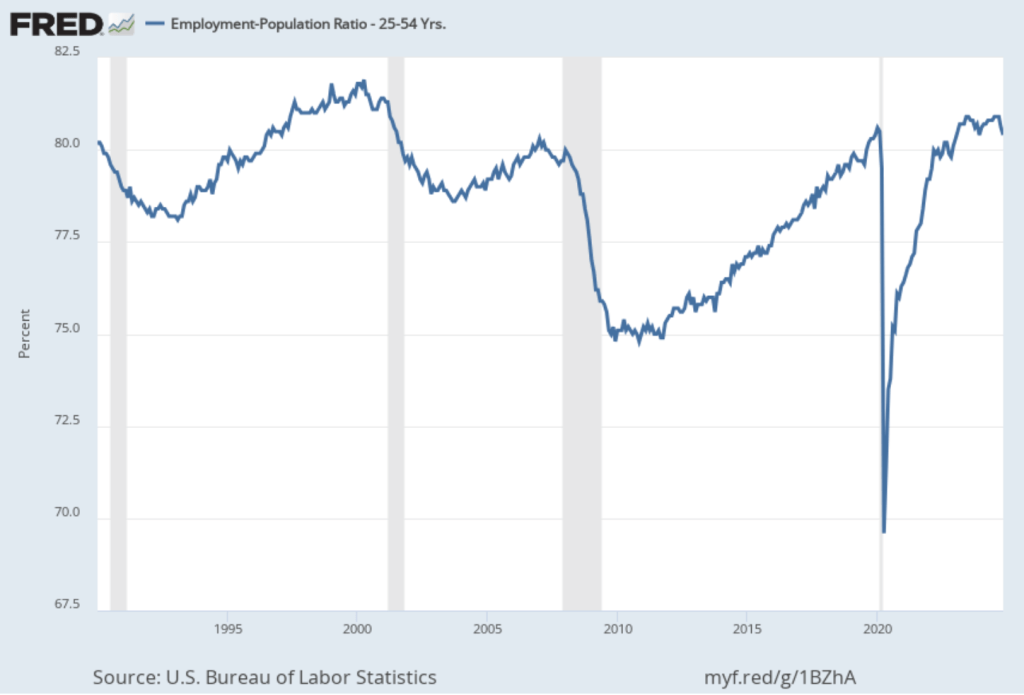

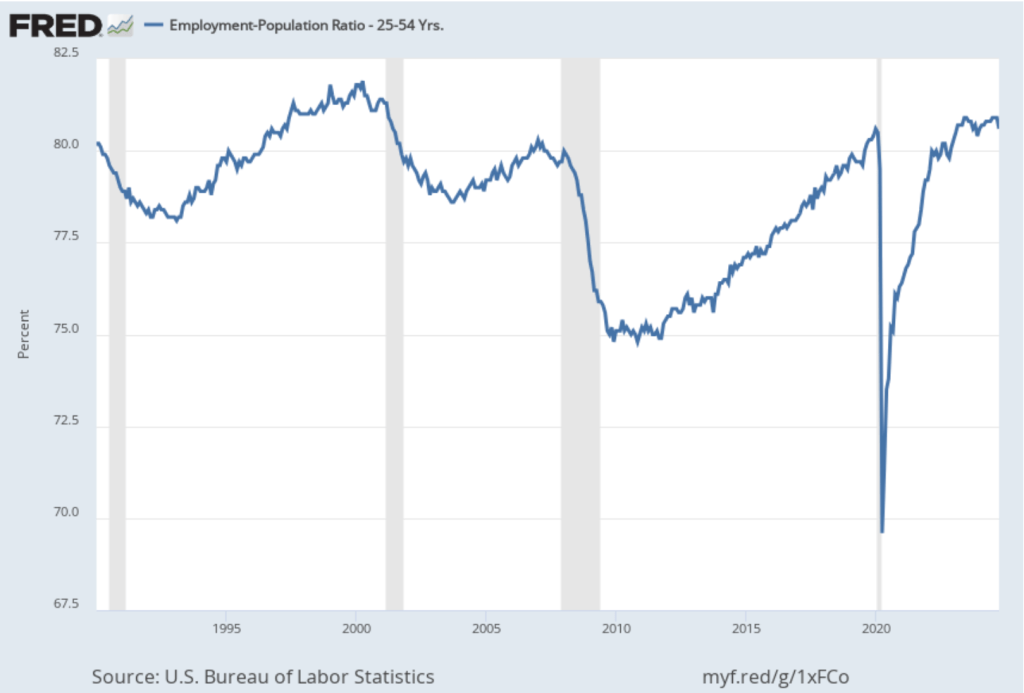

The employment-population ratio for prime age workers—those aged 25 to 54—also declined, as shown in the following figure, to 80.4 percent in November from 80.6 percent in October. Although this was the second consecutive month of decline, the employment-population ratio remained high relative to levels seen since 2001.

As the following figure shows, the unemployment rate, which is also reported in the household survey, increased slightly to 4.2 percent in November from 4.1 percent in October. The unemployment is still below its recent high of 4.3 percent in July.

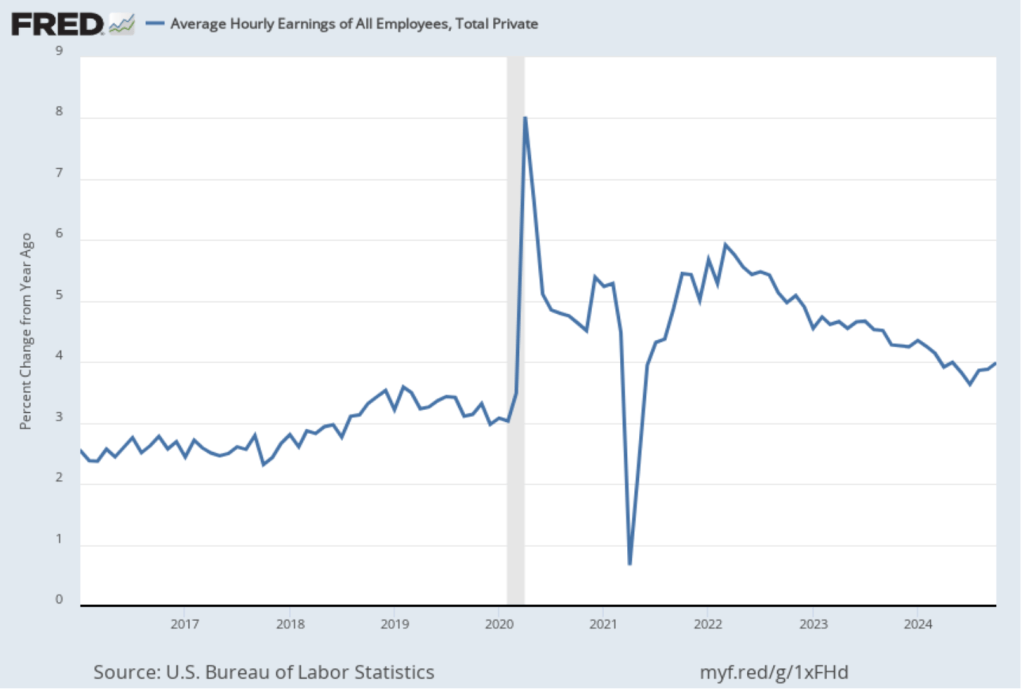

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage that it is available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 4.0 percent in November, the same as in October.

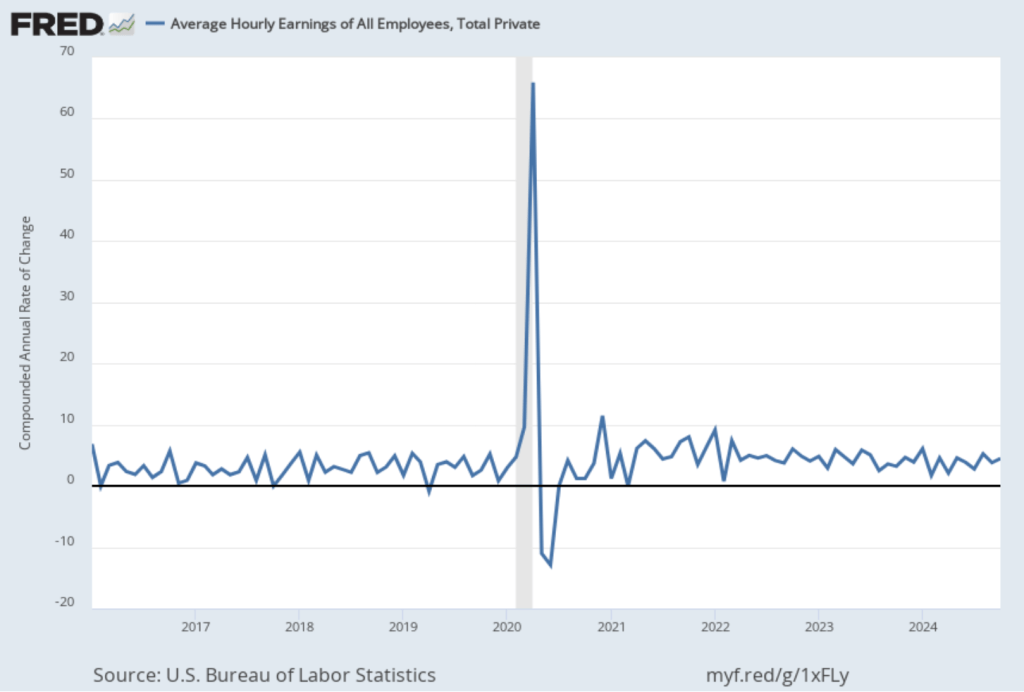

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. The November 1-month rate of wage inflation was 4.5 percent, a decline from the 5.2 percent rate in October. Whether measured as a 12-month increase or as a 1-month increase, AHE is still increasing more rapidly than is consistent with the Fed achieving its 2 percent target rate of price inflation.

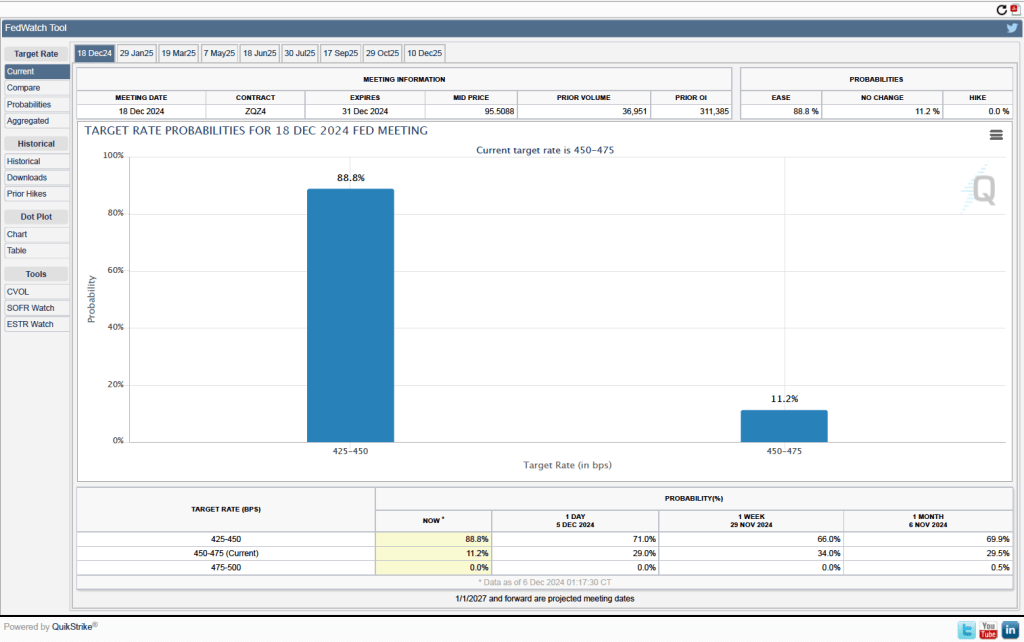

Given these data from the jobs report, is it likely that the FOMC will reduce its target range for the federal funds rate at its next meeting? One indication of expectations of future rate cuts comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 88.8 percent to the FOMC cutting its target range for the federal funds rate by 0.25 percentage point (25 basis points) from the current range of 4.50 percent to 4.75 percent, at its next meeting. Investors assign a probability of only 11.2 percent of the committee leaving its target range unchanged.

What do investors expect will happen at the next FOMC meeting after the December 17-18 meeting, which will occur on January 28-29, 2025? As of today, investors assing a probability of only 26.5 percent that the committee will set its target range at 4.00 percent to 4.25 percent, or 50 basis points, below the current target. In other words, only a minority of investors are expecting the committee to cut its target range at both its December and January meetings.

This morning (November 27), the BEA released monthly data on the personal consumption expenditures (PCE) price index as part of its “Personal Income and Outlays” report for October. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. This month’s data indicates that progress towards the Fed’s target may have stalled.

The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—for the period since January 2016 with inflation measured as the percentage change in the PCE from the same month in the previous year. Measured this way, in October, PCE inflation (the blue line) was 2.3 percent, up from 2.1 percent in September. Core PCE inflation (the red line) in October was 2.8 percent, up from 2.7 percent in September. Both PCE inflation and core PCE inflation were in accordance with the expectations of economists surveyed.

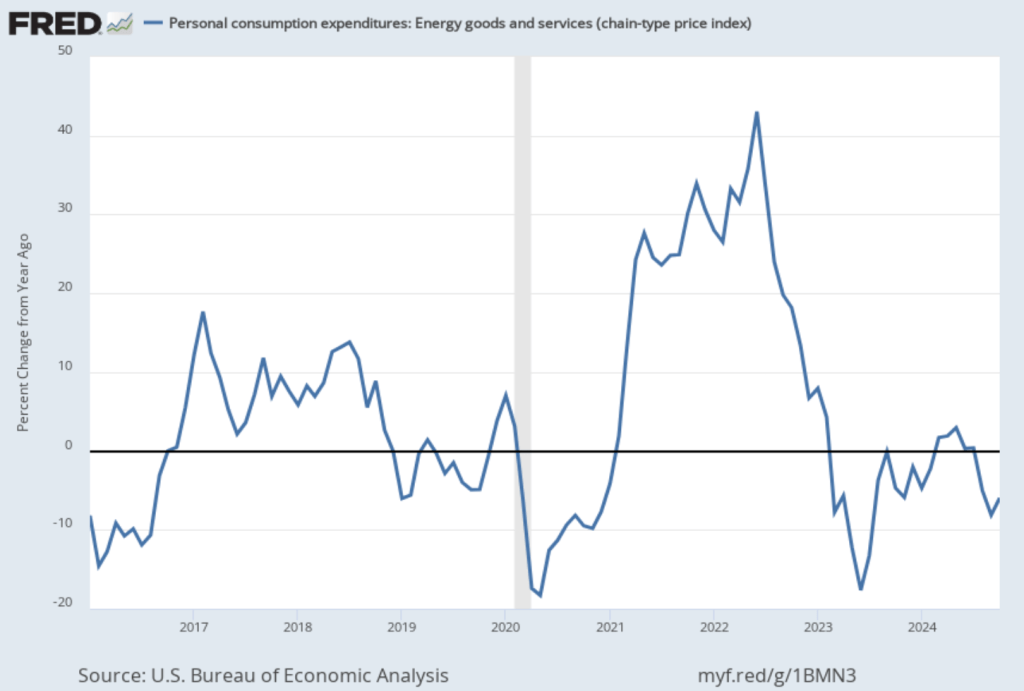

One reason that PCE inflation has been lower than core PCE inflation in recent months is that PCE inflation has been held down by falling energy prices, as shown in the following figure. Energy prices have been falling over the last three months and were down 5.9 percent in October. It seems unlikely that falling energy prices will persist.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation rose in October to 2.9 percent from 2.1 percent in September. Core PCE inflation rose from 3.2 percent in September to 3.3 percent in October. Because core inflation is generally a better measure of the underlying trend in inflation, both 12-month and 1-month core PCE inflation indicate that inflation may still run well above the Fed’s 2 percent target in coming months. But the usual caution applies that data from one month shouldn’t be overly relied on.

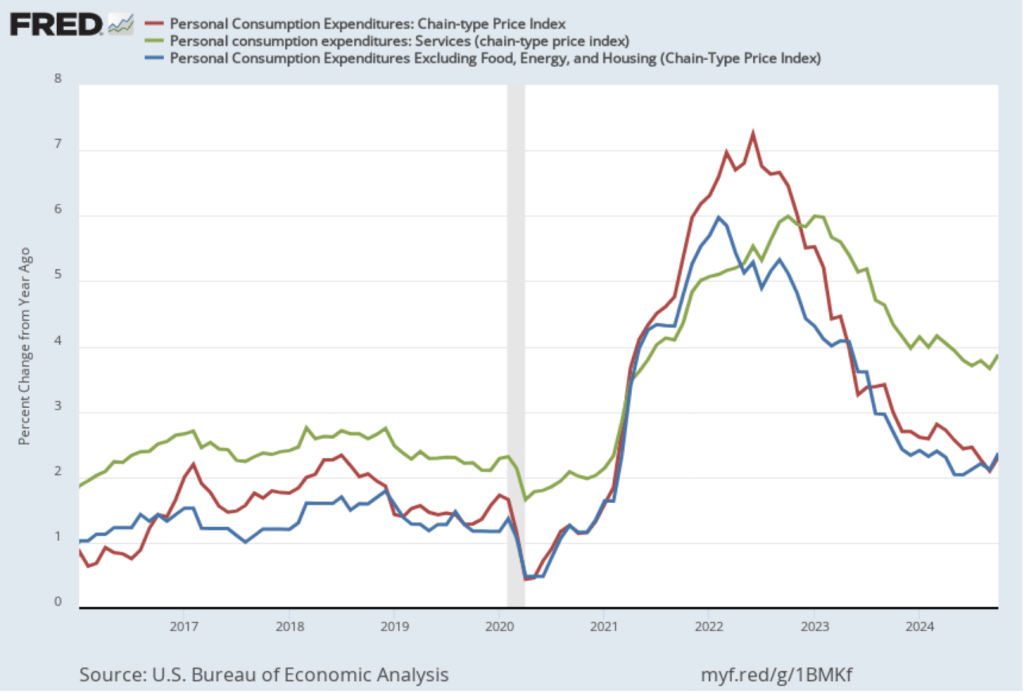

The following figure shows other ways of gauging inflation by including the 12-month inflation rate in the PCE (the same as shown in the figure above—although note that PCE inflation is now the red line rather than the blue line), inflation as measured using only the prices of the services included in the PCE (the green line), and core inflation, excluding the price of housing services as well as the prices of food and energy (the blue line). Fed Chair Jerome Powell and other members of the Federal Open Market Committee (FOMC) have said that they are concerned by the persistence of elevated rates of inflation in services and in housing.

Inflation in services remained high, increasing from 3.7 percent in September to 3.9 percent in October. Core inflation, measured by excluding housing as well as food and energy, increased from 2.1 percent in September to 2.4 percent in October.

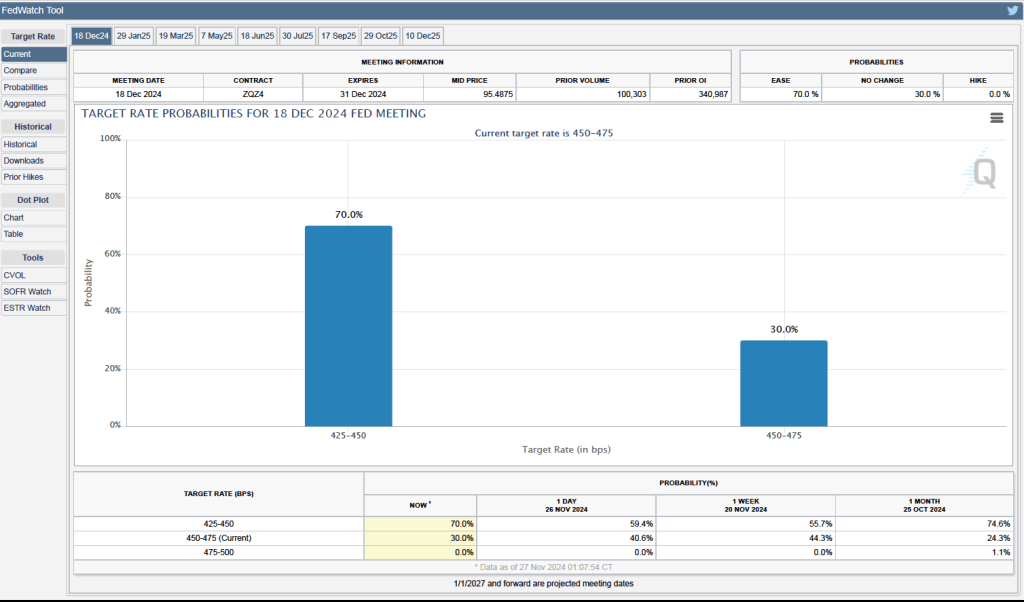

Some Fed watchers have suggested that higher inflation readings may lead he Fed’s policymaking Federal Open Market Committee (FOMC) to leave its target for the federal funds rate unchanged at its next meeting on December 17-18. As of today, however, investors who buy and sell federal funds futures contracts are still expecting that the FOMC will reduce its target by 0.25 percent (25 basis points) at its next meeting. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, investors assign a probability of 70 percent to the FOMC cutting its target for the federal funds rate from the current range of 4.50 percent to 4.75 percent to a range of 4.25 percent to 4.50 percent. Investors assign a probability of only 30 percent to the FOMC leaving its target unchanged.

Since the FOMC began increasing the target for the federal funds rate in the spring of 2022, economists have discussed three possible outcomes of the Fed’s monetary policy:

A hard landing, with the economy only returning to the Fed’s 2 percent inflation target if the U.S. economy experiences a recession

A soft landing, with the economy returning to 2 percent inflation without experiencing a recession.

No landing, with the economy not experiencing a recession but with inflation remaining persistently above the Fed’s 2 percent target.

With GDP and employment data showing no indication that a recession will begin soon and with today’s data showing inflation—while having declined substantially from its mid-2022 peak—remaining above the Fed’s 2 percent target, the chances of the no landing outcome seem to be increasing.

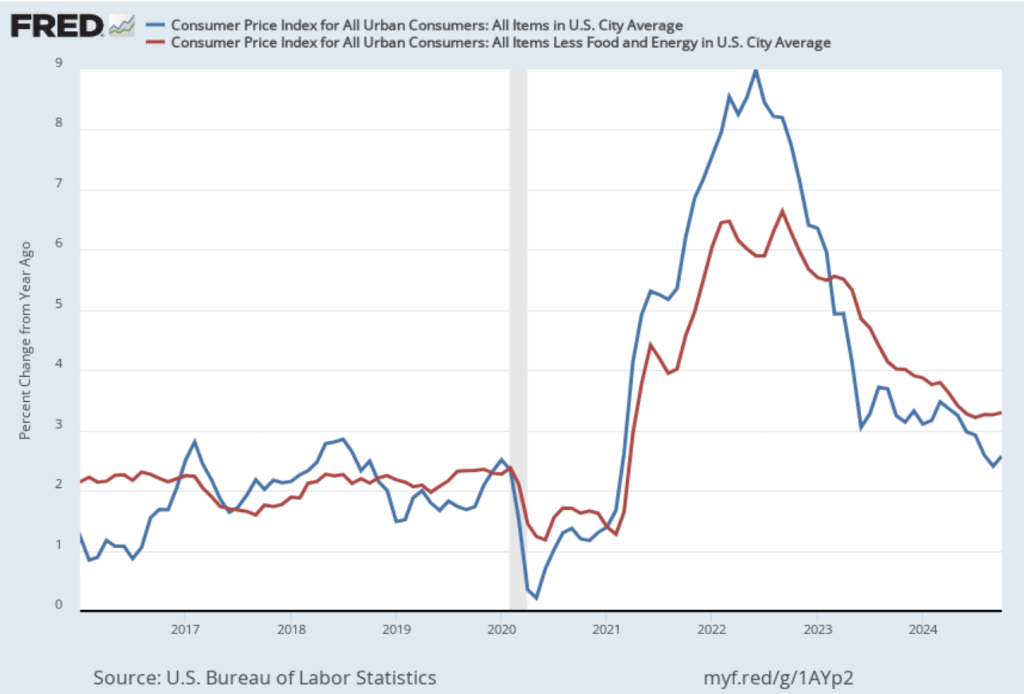

On November 13, the Bureau of Labor Statistics (BLS) released its monthly report on the consumer price index (CPI). The following figure compares headline inflation (the blue line) and core inflation (the red line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous month, was 2.6 percent—up from 2.4 percent in September.

The core inflation rate,which excludes the prices of food and energy, was unchanged at 3.3 percent for the third month in a row.

Both headline inflation and core inflation were the values that economists surveyed by the Wall Street Journal had expected.

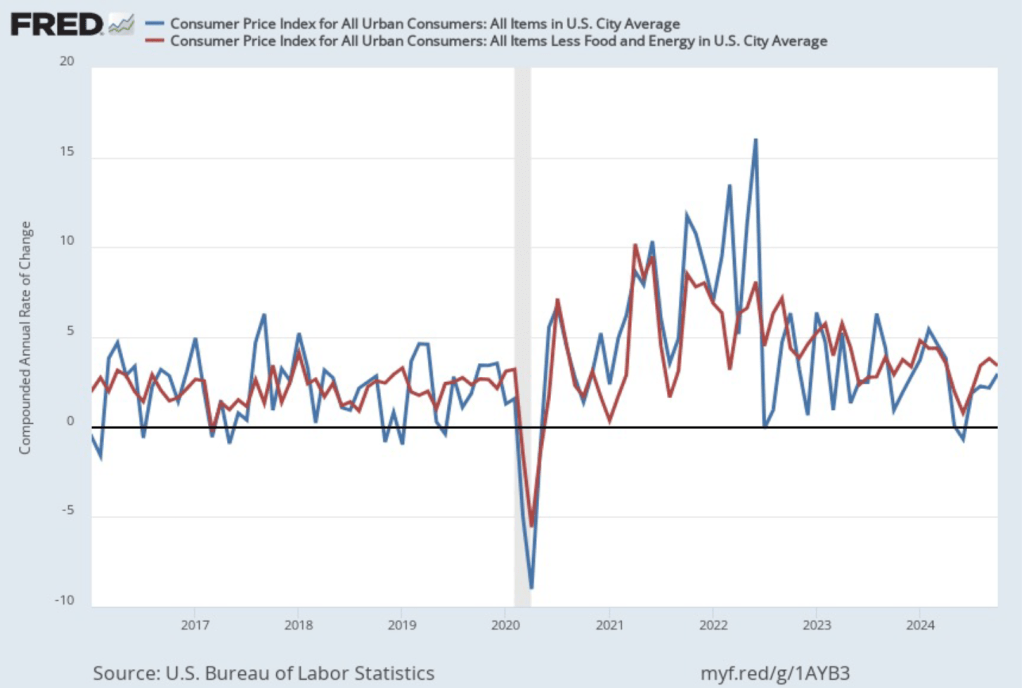

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) increased from 2.2 percent in September to 3.0 percent in October. Core inflation (the red line) fell from 3.8 percent in September to 3.4 percent in October.

Overall, considering 1-month and 12-month inflation together, the U.S. economy may still be on course for a soft landing—with the annual inflation rate returning to the Fed’s 2 percent target without the economy being pushed into a recession. However, progress on lowering inflation may have slowed or, possibly, stalled. The relatively high rates of core inflation in both the 12-month and 1-month measures are concerning because most economists believe that core inflation is a better indicator of the underlying inflation rate than is headline inflation. It’s important not to overinterpret the data from a single month, although this is the third month in a row that core inflation has been above 3 percent. (Note, that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI in evaluating whether it is hitting its 2 percent inflation target.)

As we’ve discussed in previous blog posts, Federal Reserve Chair Jerome Powell and his colleagues on the Fed’s policymaking Federal Open Market Committee (FOMC) have been closely following inflation in the price of shelter. The price of “shelter” in the CPI, as explained here, includes both rent paid for an apartment or house and “owners’ equivalent rent of residences (OER),” which is an estimate of what a house (or apartment) would rent for if the owner were renting it out. OER is included in the CPI to account for the value of the services an owner receives from living in an apartment or house.

As the following figure shows, inflation in the price of shelter has been a significant contributor to headline inflation. The blue line shows 12-month inflation in shelter, and the red line shows 1-month inflation in shelter. Twelve-month inflation in shelter has been declining since the spring of 2023, but increased in October to 4.9 percent from 4.8 percent in September. One-month inflation in shelter—which is much more volatile than 12-month inflation in shelter—increased sharply from 2.7 percent in September to 4.7 percent in October.

Chair Powell and the other members of the FOMC have been expecting that the inflation in shelter would continue to decline. For instance, in his press conference following the last FOMC meeting on November 7, Powell stated that:

“What’s going on there is, you know, market rents, newly signed leases, are experiencing very low inflation. And what’s happening is older—you know, leases that are turning over are taking several years to catch up to where market leases are; market rent leases are. So that’s just a catch-up problem. It’s not really reflecting current inflationary pressures, it’s reflecting past inflationary pressures.”

The recent uptick in shelter inflation may concern FOMC members as they consider whether, and by how much, to cut their target for the federal funds rate at their next meeting on December 17-18. Bear in mind, though, that shelter has a weight of only 15 percent in the PCE price index that the Fed uses to gauge whether it is hitting its 2 percent inflation target in contrast with the 33 percent weight that shelter has in the CPI.

To better estimate of the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed mean inflation drops the 8 percent of good and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure is from the Federal Reserve Bank of Cleveland. It shows that median inflation (the orange line) was unchanged in October at 4.1 percent. Trimmed mean inflation (the blue line) was also unchanged at 3.2 percent. These data provide confirmation that (1) core CPI inflation at this point is likely running at least slightly higher than a rate that would be consistent with the Fed achieving its inflation target and (2) that progress toward the target has slowed.

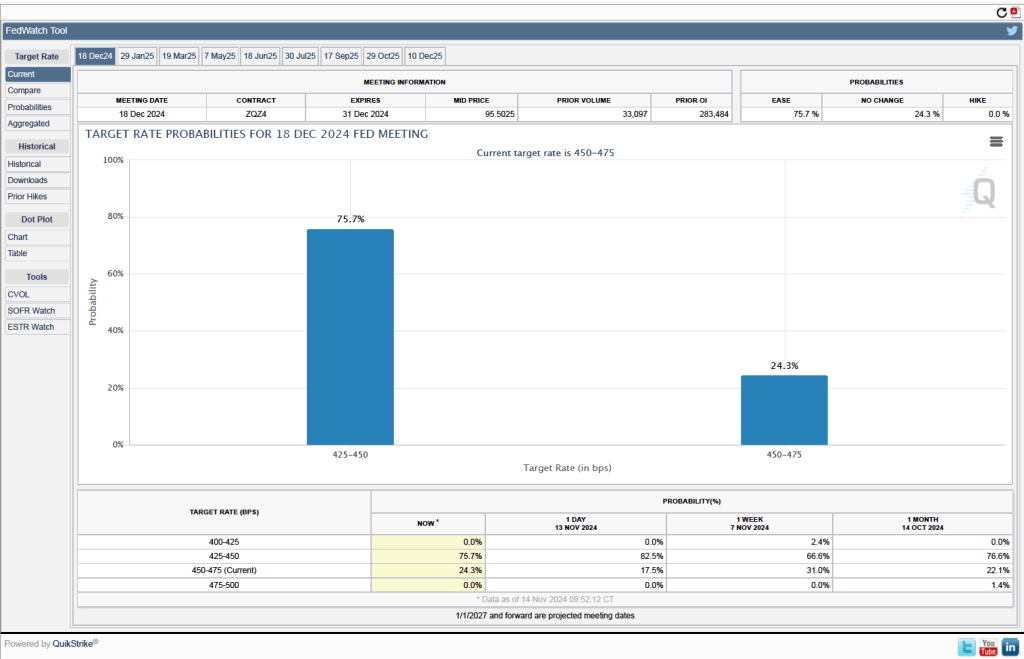

Will this persistence in inflation above the Fed’s 2 percent target cause the FOMC to hold constant its target range for the federal funds rate? Investors who buy and sell federal funds futures contracts expect that the FOMC will cut still cut its target for the federal funds rate by 0.25 percentage point at its December meeting. (We discuss the futures market for federal funds in this blog post.) The following figure that today these investors assign a probability of 75.7 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point and a probability of 24.3 percent to the committee leaving its target unchanged at a range of 4.50 percent to 4.75 percent.

A meeting of the Federal Open Market Committee (Photo from federalreserve.gov)

The Federal Reserve’s policymaking Federal Open Market Committee (FOMC) concluded its meeting today (November 7) after considering a mixed batch of macroeconomic data. As we noted in this blog post, the most recent jobs report showed a much smaller increase in payroll employment than had been expected. However, the effects of hurricanes and strikes on the labor market made the data in the report difficult to interpret. Real GDP growth during the third quarter of 2024, while relatively strong, was slower than expected. Finally, as we discuss in this post, inflation has been running above the Fed’s 2 percent annual target with wages also growing faster than is consistent with 2 percent price inflation.

Congress has given the Fed a dual mandate of achieving maximum employment and price stability. If FOMC members had been most concerned about lower-than-expected real GDP growth and some weakening in the labor market, the likely course would have been to cut the target range for the federal funds rate by 0.50 percentage point (50 basis points) from its current range of 4.75 percent to 5.00 percent to a range of 4.25 percent to 4.50 percent.

If the committee had been most concerned about inflation remaining above target, the likely course would have been to leave the target range for the federal funds rate unchanged. Instead, the committee split the difference by reducing the target range by 25 basis points. As we noted near the end of this blog post, financial markets had been expecting a 25 basis point cut. At the conclusion of each meeting, the committee holds a formal vote on its target for the federal funds rate. The vote today was unanimous.

In a press conference following the meeting, Fed Chair Jerome Powell noted that: “We see the risks to achieving our employment and inflation goals as being roughly in balance, and we are attentive to the risks to both sides of our mandate.” Powell also indicated his confidence that the committee would succeed in staying on what he labeled the “middle path” that monetary policy needs to follow: “We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing policy restraint too slowly could unduly weaken economic activity and employment …. Policy is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate.”

With respect to the effect of the macroeconomic policies of the incoming Trump Administration, Powell noted that the Fed doesn’t comment on fiscal policy nor did he consider it appropriate to comment in any way on the recent election. He stated that the committee would wait to see new policies enacted before considering their consequences for monetary policy. When asked by a reporter whether he would leave the position of Fed chair if asked to do so by someone in the Trump Administration, Powell answered “no.” When asked whether he believes the president has the power to remove a Fed chair before the end of the chair’s term, Powell again answered “no.” (Most legal scholars believe that, according to the Federal Reserve Act, a president can’t remove a Fed chair because of policy disagreements, but only “for cause.” See Macroeconomics, Chapter 17, Section 17.4/Economics, Chapter 27, Section 27.4 for more on this topic.)

The Bureau of Labor Statistics (BLS) releases the “Employment Situation” report (often called the “jobs report”) monthly. Economists and policymakers follow this report closely because it provides important insight into the current state of the U.S. economy. The October jobs report was released this morning, November 1 As sometimes happens, the data in the report were distorted by unusual events last month, primarily the effects of hurricanes and strikes. The BLS reported the results of its surveys without attempting to correct for these events. With respect to hurricanes, the BLS noted:

“No changes were made to either the establishment or household survey estimation procedures for the October data. It is likely that payroll employment estimates in some industries were affected by the hurricanes; however, it is not possible to quantify the net effect on the over-the-month change in national employment, hours, or earnings estimates because the establishment survey is not designed to isolate effects from extreme weather events. There was no discernible effect on the national unemployment rate from the household survey.”

Economists who participated in various surveys had forecast that payroll employment would increase by 117,500, with the unemployment rate—which is calculated from data in the household survey—being unchanged at 4.1 percent. The forecast of the unemployment rate was accurate, as the BLS reported a 4.1 percent unemployment rate in October. But the BLS reported that payroll employment had increased by only 12,000. In addition, the BLS revised downward its estimates of the employment increases in August and September by a total of 112,000. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure, taken from the BLS report, shows the net changes in employment for each month during the past two years.

What had initially seemed to be particularly strong growth in employment in September, possibly indicating a significant increase in the demand for labor, has been partially reversed by the data revision.

As the following figure shows, the net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. The net change in jobs as measured by the household survey for October was a decline of 368,000 jobs after an increase of 430,000 jobs in September. So, the story told by the two surveys was similar: significant weakening in the job market. But we need to keep in mind the important qualification that the job market in some areas of the country had been disrupted by unusual events during the month.

Other data in the jobs report told a more optimistic story of conditions in job market. The following figure shows the employment-population ratio for prime age workers—those aged 25 to 54. Although it declined from 80.9 percent to 80.6 percent, it remained high relative to levels seen since 2001.

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post yesterday, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage that it is available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. AHE increased 4.0 percent in October, up from a 3.9 percent increase in September.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic.

The October 1-month rate of wage inflation was 4.5 percent, an increase from the 3.8 percent rate in September. Whether measured as a 12-month increase or as a 1-month increase, AHE is increasing more rapidly than is consistent with the Fed achieving its 2 percent target rate of price inflation.

The Federal Reserve’s policy-making Federal Open Market Committee (FOMC) has its next meeting on November 6-7. What effect will this jobs report likely have on the committee’s actions at that meeting? One indication of expectations of future rate cuts comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 99.8 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point (25 basis points) at its next meeting. Investors see effectively no chance of the committee leaving its target range unchanged at the current 4.75 percent to 5.00 percent or of the committee cutting its target rate by 50 basis point cut.

Investors don’t appear to believe that the acceleration in wage growth indicated by today’s jobs report will cause the FOMC to pause its rate cutting. Nor do they appear to believe that the unexpectedly small increase in payroll employment will cause the committee to cut its target for the federal funds rate by 50 basis points.

Yesterday, the Bureau of Economic Analysis (BEA) released quarterly data on the personal consumption expenditures (PCE) price index as part of its advance estimate of third quarter GDP. (We discuss that release in this blog post.) Today, the BEA released monthly data on the PCE as part of its Personal Income and Outlays report. In addition, the Bureau of Labor Statistics (BLS) released quarterly data on the Employment Cost Index (ECI).

The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—for the period since January 2016 with inflation measured as the percentage change in the PCE from the same month in the previous year. Measured this way, in September PCE inflation (the blue line) was 2.1 percent, down from 2.3 percent in August. Core PCE inflation (the red line) in September was 2.7 percent, which was unchanged from August. PCE inflation was in accordance with the expectations of economists surveyed by the Wall Street Journal, but core inflation was higher than expected.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation rose in September to 2.1 percent from 1.4 percent in August. Core PCE inflation rose from 1.9 percent in August to 3.1 percent in June. Because core inflation is generally a better measure of the underlying trend in inflation, both 12-month and 1-month core PCE inflation indicate that inflation may still run above the Fed’s 2 percent target in coming months. But the usual caution applies that data from one month shouldn’t be overly relied on.

Turning to wages, as we’ve noted in earlier posts, as a measure of the rate of increase in labor costs, the Fed’s policy-making Federal Open Market Committee (FOMC) prefers the ECI to average hourly earnings (AHE).

The AHE is calculated by adding all of the wages and salaries workers are paid—including overtime and bonus pay—and dividing by the total number of hours worked. As a measure of how wages are increasing or decreasing during a particular period, AHE can suffer from composition effects because AHE data aren’t adjusted for changes in the mix of occupations workers are employed in. For example, during a period in which there is a decline in the number of people working in occupations with higher-than-average wages, perhaps because of a downturn in some technology industries, AHE may show wages falling even though the wages of workers who are still employed have risen. In contrast, the ECI holds constant the mix of occupations in which people are employed. The ECI does have this drawback: It is only available quarterly whereas the AHE is available monthly.

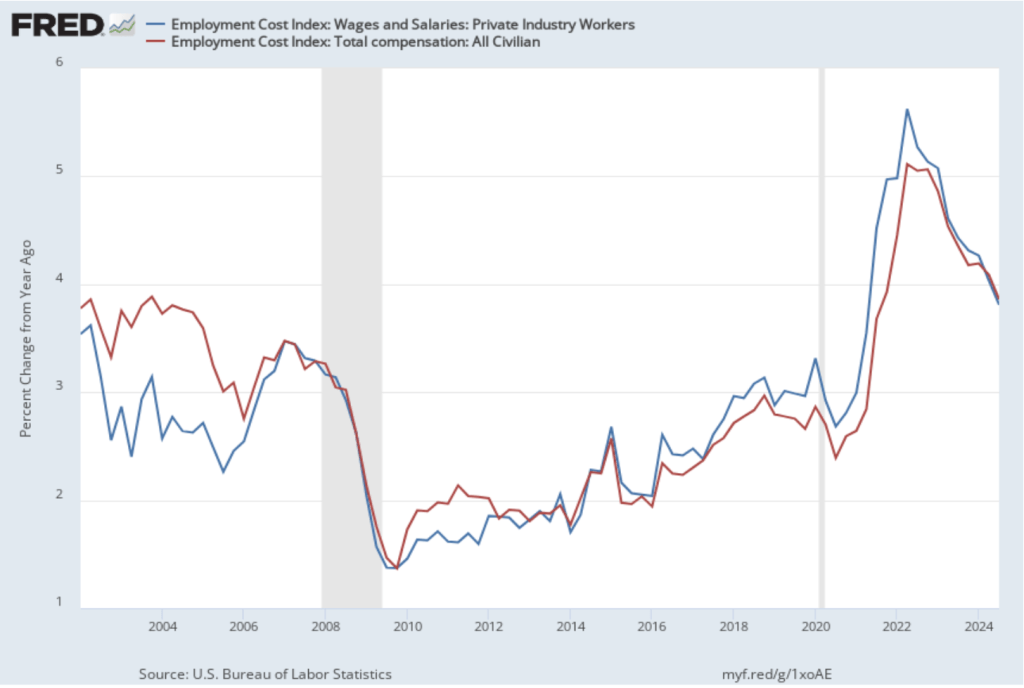

The data released this morning indicate that labor costs continue to increase at a rate that is higher than the rate that is likely needed for the Fed to hit its 2 percent price inflation target. The following figure shows the percentage change in the employment cost index for all civilian workers from the same quarter in 2023. The blue line shows only wages and salaries while the red line shows total compensation, including non-wage benefits like employer contributions to health insurance. The rate of increase in the wage and salary measure decreased from 4.0 percent in the second quarter of 2024 to 3.8 percent in the third quarter. The movement in the rate of increase in compensation was very similar, decreasing from 4.1 percent in the second quarter of 2024 to 3.9 percent in the third quarter.

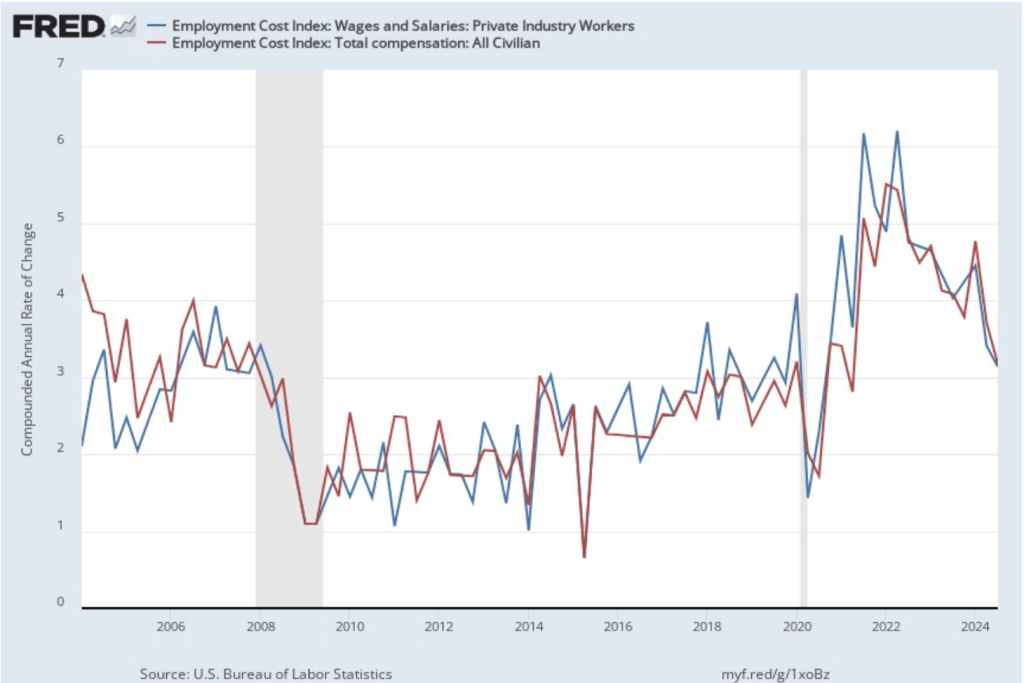

If we look at the compound annual growth rate of the ECI—the annual rate of increase assuming that the rate of growth in the quarter continued for an entire year—we find that the rate of increase in wages and salaries decreased from 3.4 percent in the second quarter of 2024 to 3.1 percent in the third quarter. Similarly, the rate of increase in compensation decreased from 3.7 percent in the second quarter of 2024 to 3.2 percent in the third quarter. So, this measure indicates that there has been some easing of wage inflation in the third quarter, although, again, we have to use caution in interpreting one quarter’s data.

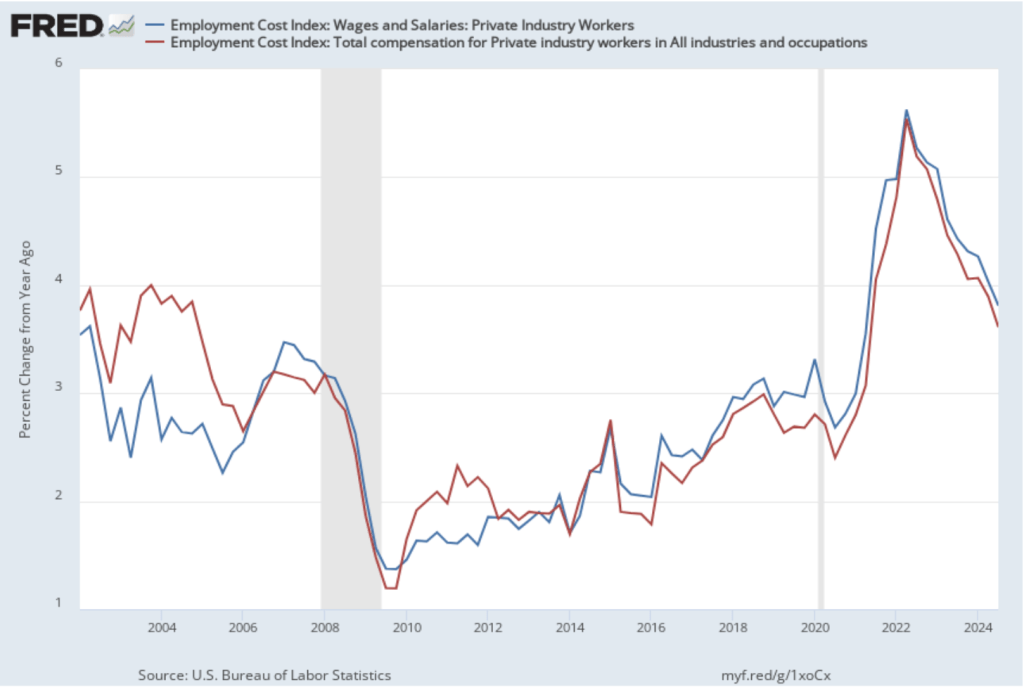

Some economists and policymakers prefer to look at the rate of increase in ECI for private industry workers rather than for all civilian workers because the wages of government workers are less likely to respond to inflationary pressure in the labor market. The first of the following figures shows the rate of increase of wages and salaries and in total compensation for private industry workers measured as the percentage increase from the same quarter in the previous year. The second figure shows the rate of increase calculated as a compound growth rate.

Both figures show results consistent with the 12-month PCE inflation figures: A decrease in wage inflation during the third quarter compared with the second quarter but with wage inflation still running somewhat above the level consistent with the Fed’s 2 percent price inflation target.

Taken together, the PCE and ECI data released today indicate that the Fed has not yet managed to bring about soft landing—returning inflation to its 2 percent target without pushing the economy into a recession. As we noted in yesterday’s post, although output growth remains strong, there are some indications that the labor market may be weakening. If so, future months may see a further decrease in wage growth that will make it more likely that the Fed will hit its inflation target. The BLS is scheduled to release its “Employment Situation” report for October on Friday, November 1. That report will provide additional data for assessing the current state of the labor market.