Photo of Federal Reserve Bank of New York President John Williams from newyorkfed.org

Many economists consider the three most influential people at the Federal Reserve to be the chair of the Board of Governors, the vice-chair of the Board of Governors, and the president of the Federal Reserve Bank of New York. The influence of the New York Fed president is attributable in part to being the only president of a District Bank to be a voting member of the Federal Open Market Committee (FOMC) every year and to the New York Fed being the location of the Open Market Desk, which is charged with implementing monetary policy. The Open Market Desk undertakes open market operations—buying and selling Treasury securities—and conducts repurchase agreements (repos) and reverse repurchase agreements (reverse repos) with the aim of keeping the federal funds rate within the target range specified by the FOMC. (We discuss the mechanics of how monetary policy is conducted in Macroeconomics, Chapter 15, Economics, Chapter 25, and Money, Banking, and the Financial System, Chapter 15.)

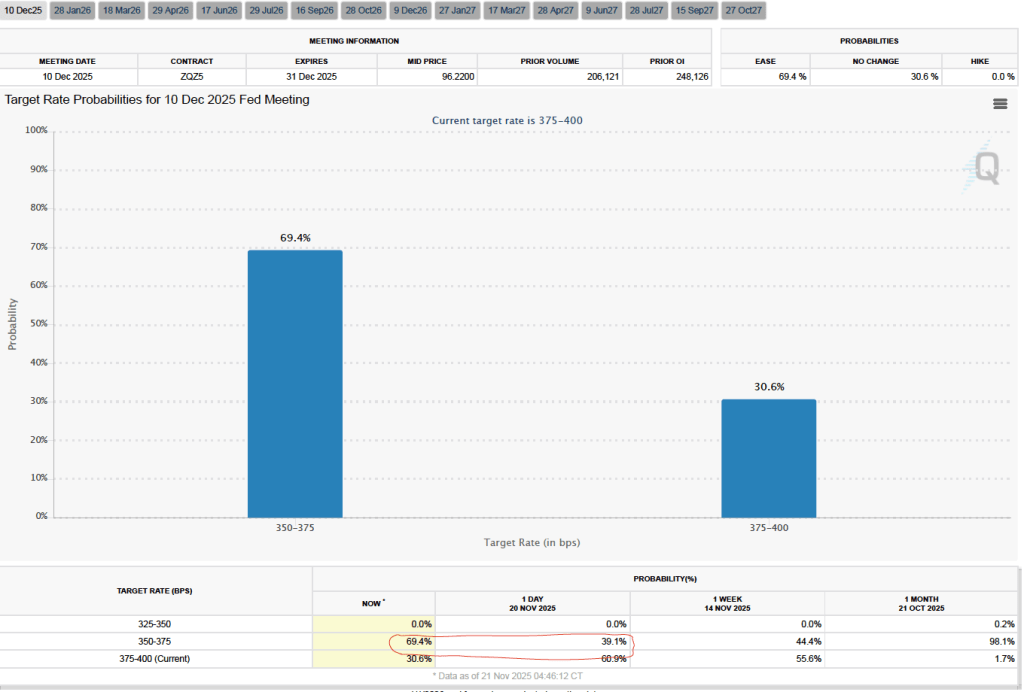

John Williams has served as president of the New York Fed since 2018. Given his important role in the formulation and execution of monetary policy, investors pay close attention to his speeches and other public remarks looking for clues about the likely future path of monetary policy. As we noted yesterday in a post discussing the latest jobs report, Fed watchers were uncertain as to whether the FOMC would cut its target for the federal funds rate at its next meeting on December 9–10.

Yesterday morning, investors who buy and sell federal funds futures contracts assigned a probability of 39.6 percent to the FOMC cutting its target range for the federal funds rate by 0.25 percentage point (25 basis points) from 3.75 percent to 4.00 to 3.50 percent to 3.75 percent. Today in a speech delivered at the Central Bank of Chile, John Williams stated that:”I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals” of maximum employment and price stability.

Investors interpreted this statement as indicating that Williams would support cutting the target range for the federal funds rate at the December FOMC meeting. Given his position on the committee, it seemed unlikely that Williams would have publicly supported a rate cut unless he believed that a majority of the committee would also support it. As the following figure shows, after the text of Williams’s speech was released this morning, investors in the federal funds futures market increased the probability they assigned to a rate cut to 69.4 percent. That movement in the federal funds futures market was a recognition of the important role the president of the New York Fed plays in formulating monetary policy.

Supports:Macroeconomics, Chapter 13, Section 13.3; Economics, Chapter 23, Section 23.3; and Essentials of Economics, Chapter 15, Section 15.3

Image generated by ChatGPT

A recent article on axios.com made the following observation: “The mainstream view on the Federal Open Market Committee is based on risk management—that the possibility of a further downshift in the job market appears to be the more pressing concern than the chance that inflation will spiral higher.” The article also notes that: “Tariffs’ effects on inflation are probably a one-time bump.”

a. What is the dual mandate that Congress has given the Federal Reserve?

b. In what circumstances might the Federal Open Market Committee (FOMC) be faced with a conflict between the goals in the dual mandate?

c. What does the author mean by tariffs’ effects on inflation being a “one-time bump”?

d. What does the author mean by the FOMC engaging in “risk management”? What is a “downshift” in the labor market? If the FOMC is more concerned about a downshift in the labor market than about inflation, will the committee raise or lower its target for the federal funds rate? Briefly explain.

Solving the Problem Step 1: Review the chapter material. This problem is about the policy dilemma the Fed can face when the unemployment rate and the inflation rate are both rising, so you may want to review Macroeconomics, Chapter 13, Section 13.3, “Macroeconomic Equilibrium in the Long Run and the Short Run.”

Step 2: Answer part a. by explaining what the Fed’s dual mandate is. Congress has given the Fed a dual mandate of achieving price stability and maximum employment.

Step 3: Answer part b. by explaining when the FOMC may face a conflict with respect to its dual mandate. When the FOMC is faced with rising unemployment and falling inflation, its preferred policy response is clear: The committee will lower its target for the federal funds rate in order to increase the growth of aggregate demand, which will increase real GDP and reduce unemployment. When the FOMC is faced with falling unemployment and rising inflation, its preferred policy response is also clear: The committee will raise its target for the federal funds rate in order to slow the growth of aggregate demand, which will reduce the inflation rate.

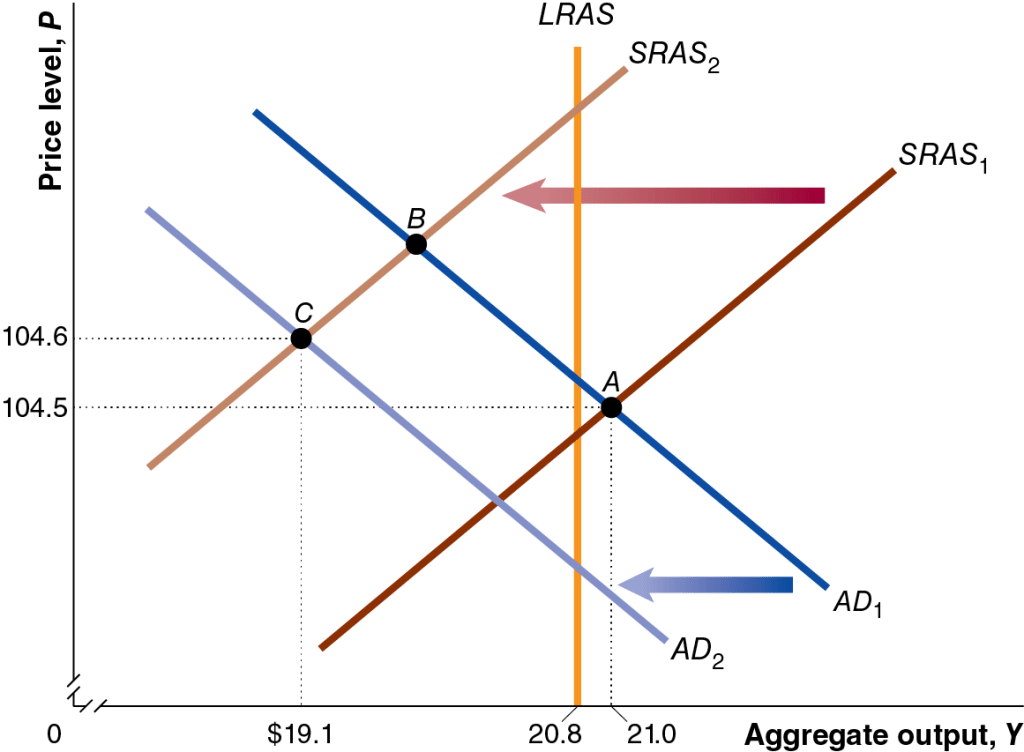

But when the Fed faces an aggregate supply shock, its preferred policy response is unclear. An aggregate supply shock, such as the U.S. economy experienced during the Covid pandemic and again with the tariff increases that the Trump administration began implementing in April, will shift the short-run aggregate supply curve (SRAS) will shift to the left, causing an increase in the price level, along with a decline in real GDP and employment. This combination of rising unemployment and inflation is called stagflation. In this situation, the FOMC faces a policy dilemma: Raising the target for the federal funds rate will help reduce inflation, but will likely increase unemployment, while lowering the target for the federal funds rate will lead to lower unemployment, but will likely increase inflation. The following figure shows the situation during the Covid pandemic when the economy experienced both an aggregate demand and aggregate supply shock. The aggregate demand curve and the aggregate supply curve both shifted to the left, resulting in falling real GDP (and employment) and a rising price level.

Step 4: Answer part c. by explaining what it means to refer to the effect of tariffs on inflation being a “one-time bump.” Tariffs cause the aggregate supply curve to shift to the left because by increasing the prices of raw materials and other inputs, they increase the production costs of some businesses. Assuming that tariffs are not continually increasing, their effect on the price level will end once the production costs of firms stop rising.

Step 5: Answer part d. by explaining what the author means by the FOMC engaing in “risk management,” explaining what a “downshift” in the labor is, and whether if the FOMC is more concerned about a downshift in the labor market than in inflation, it will raise or lower its target for the federal funds rate. The article refers to the “possibility” of a further downshift in the labor market. A downshift in the labor market means that the demand for labor may decline, raising the unemployment rate. Managing the risk of this possibility would involve concentrating on the maximum employment part of the Fed’s dual mandate by lowering its target for the federal funds rate. Note that the expectation that the effect of tariffs on the price level is a one-time bump makes it easier for the committee to focus on the maximum employment part of its mandate because the increase in inflation due to the tariff increases won’t persist.

Federal Reserve chairs often take the opportunity of the Kansas City Fed’s annual monetary policy symposium held in Jackson Hole, Wyoming to provide a summary of their views on monetary policy and on the state of the economy. In these speeches, Fed chairs are careful not to preempt decisions of the Federal Open Market Committee (FOMC) by stating that policy changes will occur that the committee hasn’t yet agreed to. In his speech at Jackson Hole today (August 22), Powell came about as close as Fed chairs ever do to announcing a policy change in a speech. In addition, Powell announced changes to the Fed’s monetary policy framework that had been in place since 2020.

Congress has given the Federal Reserve a dual mandate to achieve price stability and maximum employment. To reach its goal of price stability, the Fed has set an inflation target of 2 percent, with inflation being measured by the percentage change in the personal consumption expenditures (PCE) price index. In the statement that the FOMC releases after each meeting, it generally indicates the current “balance of risks” to meeting its two goals. In a press conference on July 30 following the last meeting of the FOMC, Powell stated that while the labor market appeared to be in balance at close to maximum employment, inflation was still running above the Fed’s 2 percent annual target.

In today’s speech, Powell stated that “the balance of risks appears to be shifting” and “that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.” These statements seem to signal that he expects that at its next meeting on September 16–17 the FOMC will cut its target for the federal funds rate from its current range of 4.25 percent to 4.50 percent.

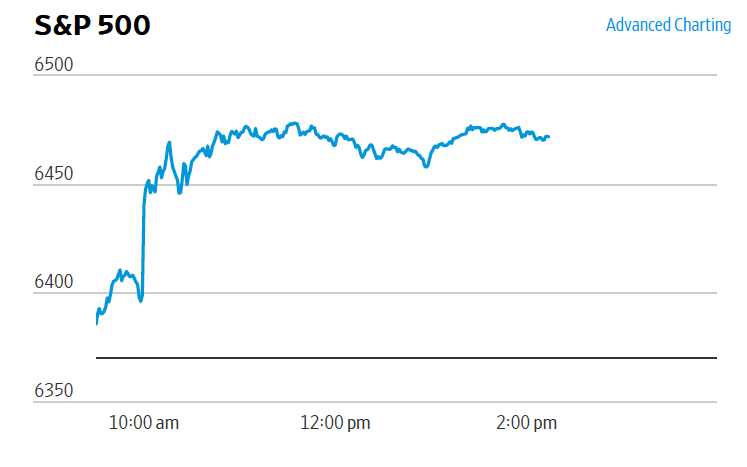

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) Yesterday, investors assigned a 75.0 percent probability to the committee cutting its target by 0.25 percentage point (25 basis points) to a range of 4.00 percent to 4.25 percent at its September meeting. After Powell’s speech at 10 a.m. eastern time, the probability of a 25 basis point cut increased to 85.3 percent. As the following figure from the Wall Street Journa shows, the stock market also jumped, with the S&P 500 stock index having increased about 1.5 percent at 2:00 p.m. Investors were presumably expecting that by cutting its federal funds rate target, the FOMC would help to offset some of the current weakness in the labor market. (We discussed the weakness in the latest jobs report in this blog post.)

Powell also announced that the Fed had revised its monetary policy framework, which had been in place since 2020. The previous framework was called flexible average-inflation targeting (FAIT). The policy was intended to automatically make monetary policy expansionary during recessions and contractionary during periods of unexpectedly high inflation. If households and firms accept that the Fed is following this policy, then during a recession when the inflation rate falls below the target, they would expect that the Fed would take action to increase the inflation rate. If a higher inflation rate results in a lower real interest rate, there will be an expansionary effect on the economy. Similarly, if the inflation rate were above the target, households and firms would expect future inflation rates to be lower, raising the real interest rate, which would have a contractionary effect on the economy.

An important point to note is that with a FAIT policy, after a period in which inflation is below 2%, the Fed would aim to keep inflation above 2% for a time to “make up” for the period of low inflation. But the converse would not be true—if inflation runs above 2%, the Fed would attempt to bring the inflation back to 2%, but would not push inflation below 2% for a time to make up for the period of low inflation. The result is that, on average, the economy would run “hotter,” lowering the average unemployment rate over time. Many policymakers at the Fed believed that, in the years before 2019, the unemployment could have been lower without causing the inflation rate to be persistently above the Fed’s target.

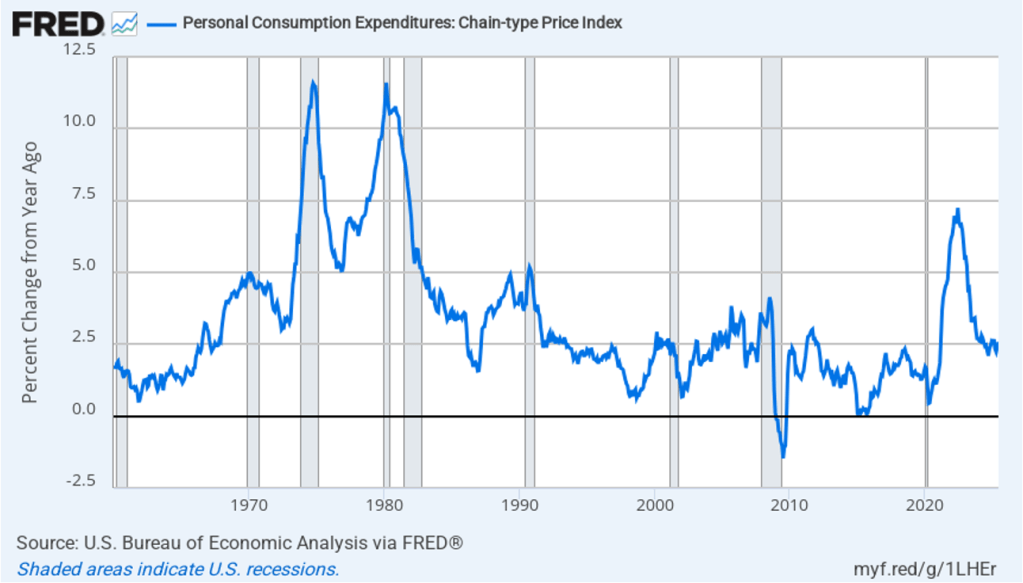

With hindsight, some economists and policymakers argue that FAIT was implemented at just the wrong time. The policy was designed to address the problem of inflation running below the 2% target for most of the period between 2012 and 2019, resulting in unemployment being higher than was consistent with the Fed’s mandate for maximum employment. But, in fact, as the following figure shows, in 2020 the U.S. economy was about to enter a period with the highest inflation rates since the early 1980s.

In his speech today, Powell noted that:

“The economic conditions that brought the policy rate to the ELB [effective lower bound to the federal funds rate, 0 percent to 0.25 percent] and drove the 2020 framework changes were thought to be rooted in slow-moving global factors that would persist for an extended period—and might well have done so, if not for the pandemic. … In the event, rather than low inflation and the ELB, the post-pandemic reopening brought the highest inflation in 40 years to economies around the world.”

Powell outlined the key changes in the policy framework:

“First, we removed language indicating that the ELB was a defining feature of the economic landscape. Instead, we noted that our ‘monetary policy strategy is designed to promote maximum employment and stable prices across a broad range of economic conditions.'”

“Second, we returned to a framework of flexible inflation targeting and eliminated the ‘makeup’ strategy. As it turned out, the idea of an intentional, moderate inflation overshoot [after a period when inflation had been below the 2 percent annual target] had proved irrelevant. … Our revised statement emphasizes our commitment to act forcefully to ensure that longer-term inflation expectations remain well anchored, to the benefit of both sides of our dual mandate. It also notes that ‘price stability is essential for a sound and stable economy and supports the well-being of all Americans.’ “

“Third, our 2020 statement said that we would mitigate ‘shortfalls,’ rather than ‘deviations,’ from maximum employment. … [T]he use of ‘shortfalls’ was not intended as a commitment to permanently forswear preemption or to ignore labor market tightness. Accordingly, we removed ‘shortfalls’ from our statement. Instead, the revised document now states more precisely that ‘the Committee recognizes that employment may at times run above real-time assessments of maximum employment without necessarily creating risks to price stability.’ … [But] preemptive action would likely be warranted if tightness in the labor market or other factors pose risks to price stability.”

“Fourth, consistent with the removal of ‘shortfalls,’ we made changes to clarify our approach in periods when our employment and inflation objectives are not complementary. In those circumstances, we will follow a balanced approach in promoting them.”

“Finally, the revised consensus statement retained our commitment to conduct a public review roughly every five years.”

To summarize, the two key changes in the framework are: 1) The FOMC will no longer attempt to push inflation beyond its 2 percent goal if inflation has been below that goal for a period, and 2) The FOMC may still attempt to preempt an increase in inflation if labor market conditions or other data make it appear likely that inflation will accelerate, but it won’t necessarily do so just because the unemployment rate is currently lower than what had been considered consistent with maximum employment.

Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

Members of the Fed’s policymaking Federal Open Market Committee (FOMC) had signaled clearly before today’s (May 7) meeting that the committee would leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. In the statement released after its meeting, the committee made one significant change to the wording in its statement following its last meeting on March 19. The committee added the words in bold to the following sentence:

“The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.”

The key event since the last FOMC meeting was President Trump’s announcement on April 2 that he would implement tariff increases that were much higher than had previously been expected.

As we noted in an earlier blog post, an unexpected increase in tariff rates will result in an aggregate supply shock to the economy. As we discuss in Macroeconomics, Chapter 13,Section 13.3 (Economics, Chapter 23, Section 23.3), an aggregate supply shock puts upward pressure on the price level at the same time as it causes a decline in real GDP and employment. The result, as the FOMC statement indicates, can be both rising inflation and rising unemployment. If higher inflation and higher unemployment persist, the U.S. economy would be experiencing stagflation. The United States last experienced stagflation during the 1970s when large increases in oil prices caused an aggregate supply shock.

During his press conference following the meeting, Fed Chair Jerome Powell indicated that the increase in tariffs might the Fed’s dual mandate goals of price stability and maximum employment “in tension” if both inflation and unemployment increase. If the FOMC were to increase its target for the federal funds rate in order to slow the growth of demand and bring down the inflation rate, the result might be to further increase unemployment. But if the FOMC were to cut its target for the federal funds rate to increase the growth of demand and reduce the unemployment rate, the result might be to further increase the inflation rate.

Powell emphasized during his press conference that tariffs had not yet had an effect on either inflation or unemployment that was large enough to be reflected in macroeconomic data—as we’ve noted in blog posts discussing recent macroeconomic data releases. As a result, the consensus among committee members is that it would be better to wait to future meetings before deciding what changes in the federal funds rate might be needed: “We’re in a good position to wait and see. We don’t have to be in a hurry.”

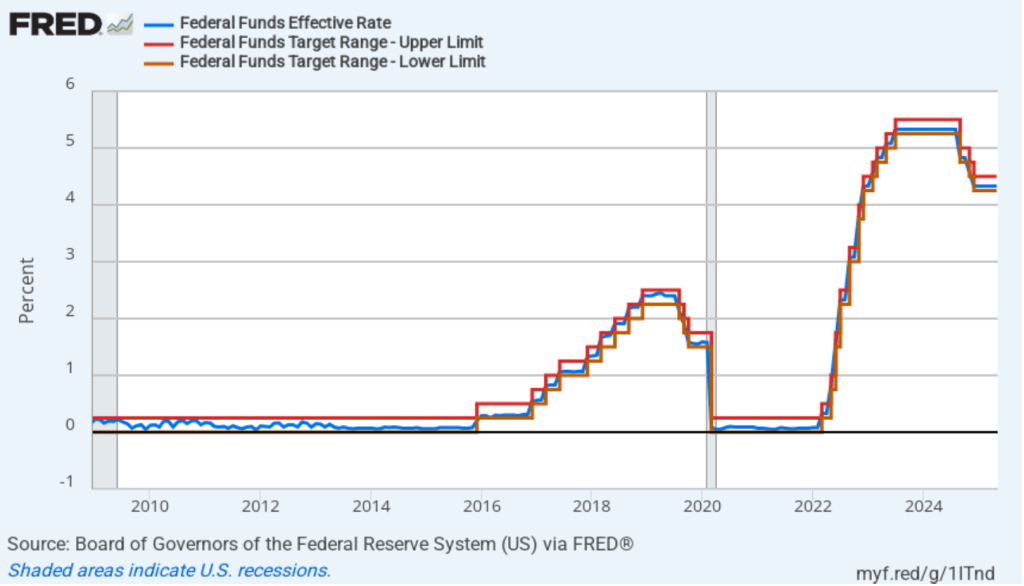

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed is successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

In his press conference, Powell indicated that when the committee would change its target for the federal funds rate was dependent on the trends in macroeconomic data on inflation, unemployment, and output during the coming months. He noted that if both unemployment and inflation significantly increased, the committee would focus on which variable had moved furthest from the Fed’s target. He also noted that it was possible that neither inflation nor unemployment might end up significantly increasing either because tariff negotiations lead to lower tariff rates or because the economy proves to be better able to deal with the effects of tariff increases than many economist now expect.

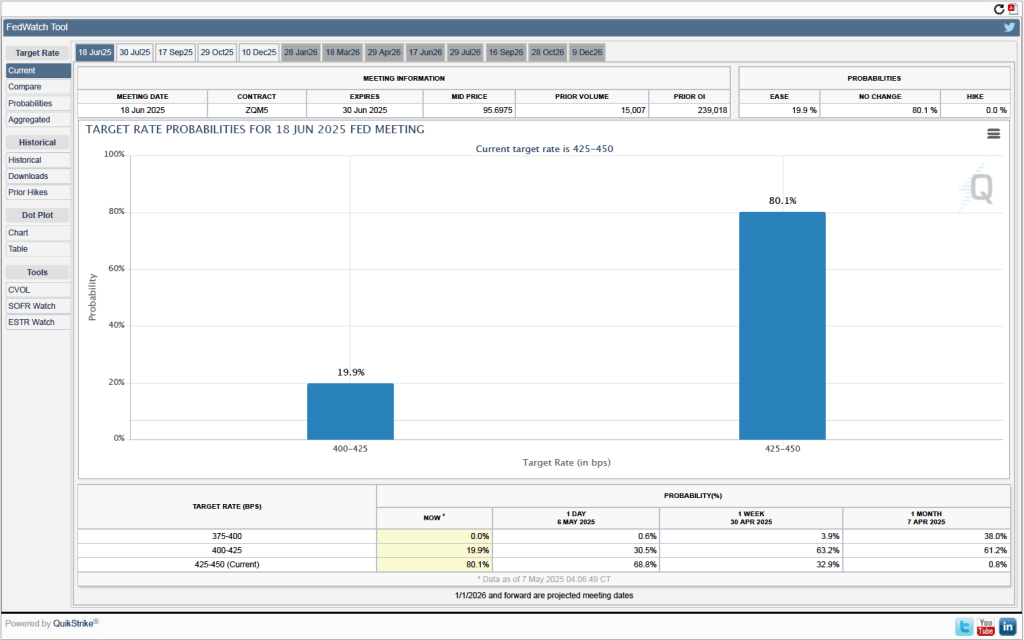

One indication of expectations of future changes in the target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that investors don’t expect that the FOMC will cut its target for the federal funds rate at its May 17–18 meeting. As shown in the following figure, investors assign a 80.1 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

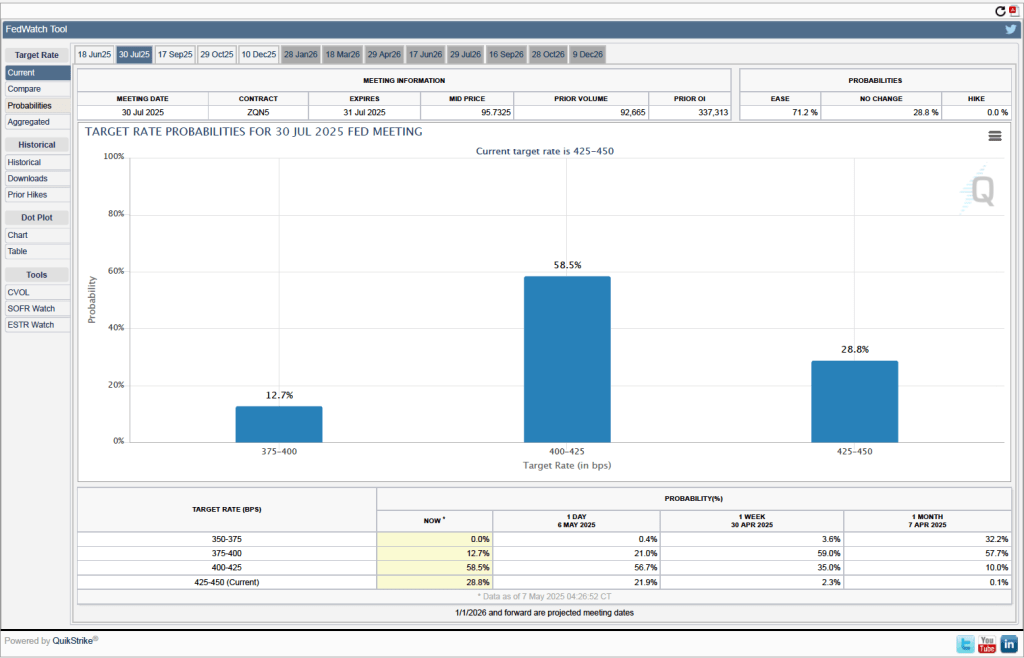

When will the Fed likely cut its target for the federal funds rate? As the following figure shows, investors expect it to happen at the FOMC’s July 29–30 meeting. Investors assign a probably of 58.5 percent to the committee cutting its target by 0.25 percentage point (25 basis points) at that meeting and a probability of 12.7 percent to the committee cutting its target by 50 basis points. Investors assign a probability of only 28.8 percent to the committee leaving its target unchanged.

In this photo of a Federal Open Market Committee meeting, Fed Chair Jerome Powell is on the far left and Fed Governor Christopher Waller is the third person to Powell’s left. (Photo from federalreserve.gov)

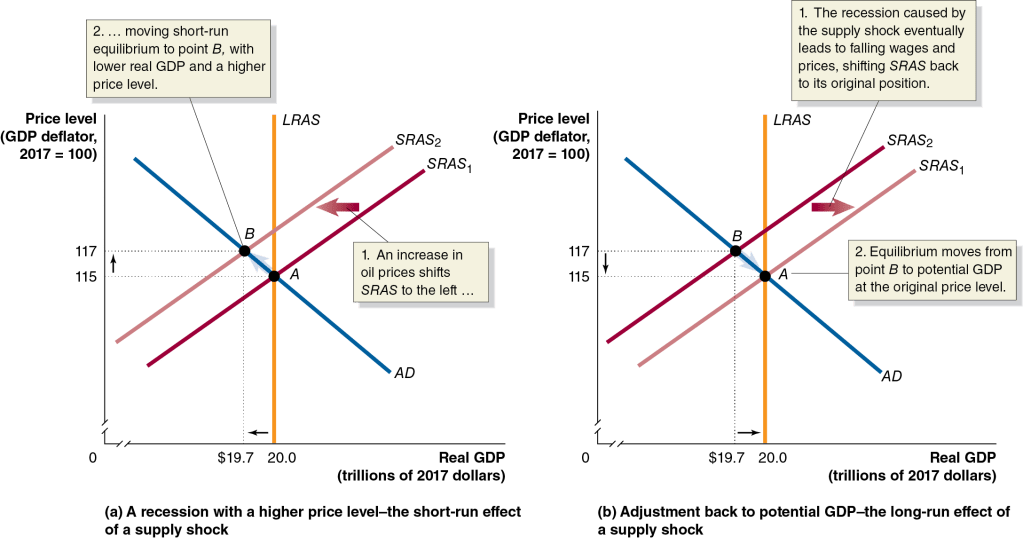

This post discusses two developments this week that involve the Federal Reserve. First, we discuss the apparent disagreement between Fed Chair Jerome Powell and Fed Governor Christopher Waller over the best way to respond to the Trump Administration’s tariff increases. As we discuss in this blog post and in this podcast, in terms of the aggregate demand and aggregate supply model, a large unexpected increase in tariffs results in an aggregate supply shock to the economy, shifting the short-run aggregate supply curve (SRAS) to the left. The following is Figure 13.7 from Macroeconomics (Figure 23.7 from Economics) and illustrates the effects of an aggregate supply shock on short-run macroeconomic equilibrium.

Although the figure shows the effects of an aggregate supply shock that results from an unexpected increase in oil prices, using this model, the result is the same for an aggregate supply shock caused by an unexpected increase in tariffs. Two-thirds of U.S. imports are raw materials, intermediate goods, or capital goods, all of which are used as inputs by U.S. firms. So, in both the case of an increase in oil prices and in the case of an increase in tariffs, the result of the supply shock is an increase in U.S. firms’ production costs. This increase in costs reduces the quantity of goods firms will supply at every price level, shifting the SRAS curve to the left, as shown in panel (a) of the figure. In the new macroeconomic equilibrium, point B in panel (a), the price level increases and the level of real GDP declines. The decline in real GDP will likely result in an increase in the unemployment rate.

An aggregate supply shock poses a policy dilemma for the Fed’s policymaking Federal Open Market Committee (FOMC). If the FOMC responds to the decline n real GDP and the increase in the unemployment rate with an expansionary monetary policy of lowering the target for the federal funds rate, the result is likely to be a further increase in the price level. Using a contractionary monetary policy of increasing the target for the federla funds rate to deal with the rising price level can cause real GDP to fall further, possibly pushing the economy into a recession. One way to avoid the policy dilemma from an aggregate supply shock caused by an increase in tariffs is for the FOMC to “look through”—that is, not respond—to the increase in tariffs. As panel (b) in the figure shows, if the FOMC looks through the tariff increase, the effect of the aggregate supply shock can be transitory as the economy absorbs the one-time increase in the price level. In time, real GDP will return to equilibrium at potential real GDP and the unemployment rate will fall back to the natural rate of unemployment.

On Monday (April 14), Fed Governor Christopher Waller in a speech to the Certified Financial Analysts Society of St. Louis made the argument for either looking through the macroeconomic effects of the tariff increase—even if the tariff increase turns out to be large, which at this time is unclear—or responding to the negative effects of the tariffs increases on real GDP and unemployment:

“I am saying that I expect that elevated inflation would be temporary, and ‘temporary’ is another word for ‘transitory.’ Despite the fact that the last surge of inflation beginning in 2021 lasted longer than I and other policymakers initially expected, my best judgment is that higher inflation from tariffs will be temporary…. While I expect the inflationary effects of higher tariffs to be temporary, their effects on output and employment could be longer-lasting and an important factor in determining the appropriate stance of monetary policy. If the slowdown is significant and even threatens a recession, then I would expect to favor cutting the FOMC’s policy rate sooner, and to a greater extent than I had previously thought.”

In a press conference after the last FOMC meeting on March 19, Fed Chair Jerome Powell took a similar position, arguing that: “If there’s an inflation that’s going to go away on its own, it’s not the correct response to tighten policy.” But in a speech yesterday (April 16) at the Economic Club of Chicago, Powell indicated that looking through the increase in the price level resulting from a tariff increase might be a mistake:

“The level of the tariff increases announced so far is significantly larger than anticipated. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. Both survey- and market-based measures of near-term inflation expectations have moved up significantly, with survey participants pointing to tariffs…. Tariffs are highly likely to generate at least a temporary rise in inflation. The inflationary effects could also be more persistent…. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.”

In a discussion following his speech, Powell argued that tariff increases may disrupt global supply chains for some U.S. industries, such as automobiles, in way that could be similar to the disruptions caused by the Covid pandemic of 2020. As a result: “When you think about supply disruptions, that is the kind of thing that can take time to resolve and it can lead what would’ve been a one-time inflation shock to be extended, perhaps more persistent.” Whereas Waller seemed to indicate that as a result of the tariff increases the FOMC might be led to cut its target for the federal funds sooner or to larger extent in order to meet the maximum employment part of its dual mandate, Powell seemed to indicate that the FOMC might keep its target unchanged longer in order to meet the price stability part of the dual mandate.

Powell’s speech caught the notice of President Donald Trump who has been pushing the FOMC to cut its target for the federal funds rate sooner. An article in the Wall Street Journal, quoted Trump as posting to social media that: “Powell’s termination cannot come fast enough!” Powell’s term as Fed chair is scheduled to end in May 2026. Does Trump have the legal authority to replace Powell earlier than that? As we discuss in Macroeconomics, Chapter 27 (Economics Chapter 17), according to the Federal Reserve Act, once a Fed chair is notimated to a four-year term by the president (President Trump first nominated Powell to be chair in 2017 and Powell took office in 2018) and confirmed by the Senate, the president cannot remove the Fed chair except “for cause.” Most legal scholars argue that a president cannot remove a Fed chair due to a disagreement over monetary policy.

Article I, Section II of the Constitution of the United States states that: “The executive Power shall be vested in a President of the United States of America.” The ability of Congress to limit the president’s power to appoint and remove heads of commissions, agencies, and other bodies in the executive branch of government—such as the Federal Reserve—is not clearly specified in the Constitution. In 1935, a unanimous Supreme Court ruled in the case of Humphrey’s Executor v. United States that President Franklin Roosevelt couldn’t remove a member of the Federal Trade Commission (FTC) because in creating the FTC, Congress specified that members could only be removed for cause. Legal scholars have presumed that the ruling in this case would also bar attempts by a president to remove members of the Fed’s Board of Governors because of a disagreement over monetary policy.

The Trump Administration recently fired a member of the National Labor Relations Board and a member of the Merit Systems Protection Board. The members sued and the Supreme Court is considering the case. The Trump Adminstration is asking the Court to overturn the Humphrey’s Executor decision as having been wrongly decided because the decision infringed on the executive power given to the president by the Constitution. If the Court agrees with the administration and overturns the precdent established by Humphrey’s Executor, would President Trump be free to fire Chair Powell before Powell’s term ends? (An overview of the issues involved in this Court case can be found in this article from the Associated Press.)

The answer isn’t clear because, as we’ve noted in Macroeconomics, Chapter 14, Section 14.4, Congress gave the Fed an unusual hybrid public-private structure and the ability to fund its own operations without needing appropriations from Congress. It’s possible that the Court would rule that in overturning Humphrey’s Executor—if the Court should decide to do that—it wasn’t authorizing the president to replace the Fed chair at will. In response to a question following his speech yesterday, Powell seemed to indicate that the Fed’s unique structure might shield it from the effects of the Court’s decision.

If the Court were to overturn its ruling in Humphrey’s Executor and indicate that the ruling did authorize the president to remove the Fed chair, the Fed’s ability to conduce monetary policy independently of the president would be seriously undermined. In Macroeconomics, Chapter 17, Section 17.4 we review the arguments for and against Fed independence. It’s unclear at this point when the Court might rule on the case.

A meeting of the Federal Open Market Committee (Photo from federalreserve.gov)

The Federal Reserve’s policymaking Federal Open Market Committee (FOMC) concluded its meeting today (November 7) after considering a mixed batch of macroeconomic data. As we noted in this blog post, the most recent jobs report showed a much smaller increase in payroll employment than had been expected. However, the effects of hurricanes and strikes on the labor market made the data in the report difficult to interpret. Real GDP growth during the third quarter of 2024, while relatively strong, was slower than expected. Finally, as we discuss in this post, inflation has been running above the Fed’s 2 percent annual target with wages also growing faster than is consistent with 2 percent price inflation.

Congress has given the Fed a dual mandate of achieving maximum employment and price stability. If FOMC members had been most concerned about lower-than-expected real GDP growth and some weakening in the labor market, the likely course would have been to cut the target range for the federal funds rate by 0.50 percentage point (50 basis points) from its current range of 4.75 percent to 5.00 percent to a range of 4.25 percent to 4.50 percent.

If the committee had been most concerned about inflation remaining above target, the likely course would have been to leave the target range for the federal funds rate unchanged. Instead, the committee split the difference by reducing the target range by 25 basis points. As we noted near the end of this blog post, financial markets had been expecting a 25 basis point cut. At the conclusion of each meeting, the committee holds a formal vote on its target for the federal funds rate. The vote today was unanimous.

In a press conference following the meeting, Fed Chair Jerome Powell noted that: “We see the risks to achieving our employment and inflation goals as being roughly in balance, and we are attentive to the risks to both sides of our mandate.” Powell also indicated his confidence that the committee would succeed in staying on what he labeled the “middle path” that monetary policy needs to follow: “We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing policy restraint too slowly could unduly weaken economic activity and employment …. Policy is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate.”

With respect to the effect of the macroeconomic policies of the incoming Trump Administration, Powell noted that the Fed doesn’t comment on fiscal policy nor did he consider it appropriate to comment in any way on the recent election. He stated that the committee would wait to see new policies enacted before considering their consequences for monetary policy. When asked by a reporter whether he would leave the position of Fed chair if asked to do so by someone in the Trump Administration, Powell answered “no.” When asked whether he believes the president has the power to remove a Fed chair before the end of the chair’s term, Powell again answered “no.” (Most legal scholars believe that, according to the Federal Reserve Act, a president can’t remove a Fed chair because of policy disagreements, but only “for cause.” See Macroeconomics, Chapter 17, Section 17.4/Economics, Chapter 27, Section 27.4 for more on this topic.)

Federal Reserve Chair Jerome Powell (Photo from federalreserve.gov)

In a blog post yesterday (September 17), we noted that trading on the CME’s federal funds futures market indicated that investors assigned a probability of 63 percent to the Federal Open Market Committee (FOMC) announcing today a 0.50 percentage point (50 basis points) cut to its target range for the federal funds rate and a probability of 37 percent to a 0.25 percentage point (25 basis points) cut. (100 basis points equals 1 percentage point.) The forecast proved correct when the FOMC announced this afternoon that it was cutting its target range to 4.75 percent to 5.00 percent, from the range of 5.25 percent to 5.50 percent that had been in place since July 2023.

Congress has given the Fed a dual mandate to achieve maximum employment and price stability. In March 2022, the FOMC began responding to the surge in inflation that had begun in the spring of 2021 by raising its target for the federal funds rate. Up through its July 2024 meeting, the FOMC had been focused on the risk that the inflation rate would remain above the Fed’s target inflation rate of 2 percent. In the statement released after today’s meeting, the committee stated that it “has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance.”

In a press conference following the meeting, Fed Chair Jerome Powell indicated that with inflation close to the 2 percent target and the labor market continuing to cool “by any measure,” the committee judged that it was time to begin normalizing its target range for the federal funds rate. Powell said that: “The U.S. economy is in a good place and our action is intended to keep it there.” When asked by a reporter whether the committee cut its target by 50 basis points today to catch up for not having cut its target at its July meeting, Powell responded that: “We don’t think we’re behind [on cutting the target range]. We think this [50 basis point cut] will keep us from falling behind.”

At the conclusion of each meeting, the committee holds a formal vote on its target for the federal funds rate. The vote today was 15-1, with Governor Michelle Bowman casting the sole negative vote. She stated that she would have preferred a 25 basis point cut. Dissenting votes have been rare in recent years.

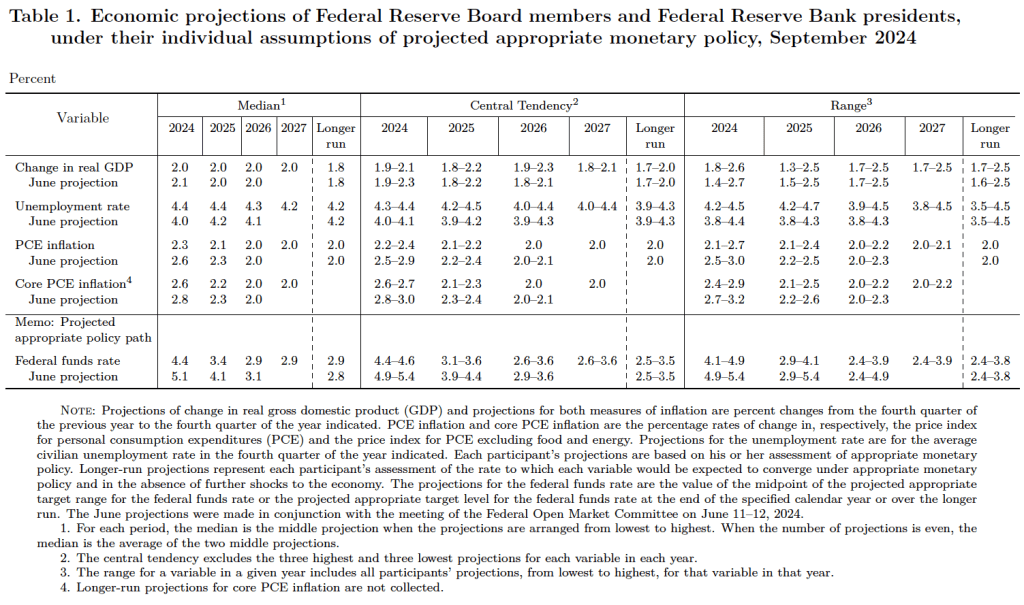

How much lower will the federal funds target range go? Typically at the FOMC’s December, March, June, and September meetings, the committee releases a “Summary of Economic Projections” (SEP), which presents median values of the committee members’ forecasts of key economic variables. The following table is from the SEP released after today’s meeting.

Looking at the values under the heading “Median” on the left side of the table, the median projection for the federal funds rate at the end of the 2024 is 4.4 percent. That projection signals that the committee will likely cut its target range by 25 basis points at each of its two remaining meetings on November 6-7 and December 17-18. The median projection for the federal funds rate at the end of 2025 is 3.4 percent, implying four additional 25 basis points cuts. In the long run, the median projection of the committee is that the federal funds rate will be 2.9 percent, which is somewhat higher than the 2.5 percent rate that the committee had projected at its December 2019 meeting before the start of the Covid pandemic.

Committee members project that the unemployment rate will end the year at 4.4 percent, up from the 4.2 percent rate in August. They expect that the unemployment rate will be 4.2 percent in the long run. The long run unemployment rate is ofter referred to as the natural rate of unemployment. (We discuss the natural rate of unemployment in Macroeconomics, Chapter 9, Section 9.2 and Economics, Chapter 19, Section 19.2.)

The median projection of the committe members is that at the end of 2024 the inflation rate, as measured by the percentage change in the personal consumption expenditures (PCE) price index, will be 2.3 percent, slightly above the Fed’s target rate. Inflation will also run slightly above the Fed’s target in 2025 at 2.1 percent before retuning to 2 percent by the end of 2026. The median projections of the inflation rate at the ends of 2024 and 2025 are lower than the median projections in the SEP that was released after the FOMC meeting on June 11-12.

Image generated by GTP-4o “illustrating interest rates.”

Tomorrow (September 18) at 2 p.m. EDT, the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) will announce its target for the federal funds rate. It’s been clear since Fed Chair Jerome Powell’s speech on August 23 at the Kansas City Fed’s annual monetary policy symposium held in Jackson Hole, Wyoming that the FOMC would cut its target for the federal funds rate at its meeting on September 17-18. (We discuss Powell’s speech in this blog post.)

The only suspense has been over the size of the cut. Traditionally, the FOMC has raised or lowered its target for the federal funds rate in 0.25% (or 25 basis points) increments. Occasionally, however, either because economic conditions are changing rapidly or because the committee concludes that it has been adjusting its target too slowly (“fallen behind the curve” is the usual way of putting it) the committee makes 0.50% (50 basis points) changes to its target.

Futures markets allow investors to buy and sell futures contracts on commodities–such as wheat and oil–and on financial assets. Investors can use futures contracts both to hedge against risk—such as a sudden increase in oil prices or in interest rates—and to speculate by, in effect, betting on whether the price of a commodity or financial asset is likely to rise or fall. (We discuss the mechanics of futures markets in Chapter 7, Section 7.3 of Money, Banking, and the Financial System.) The CME Group was formed from several futures markets, including the Chicago Mercantile Exchange, and allows investors to trade federal funds futures contracts. The data that result from trading on the CME indicate what investors in financial markets expect future values of the federal funds rate to be.

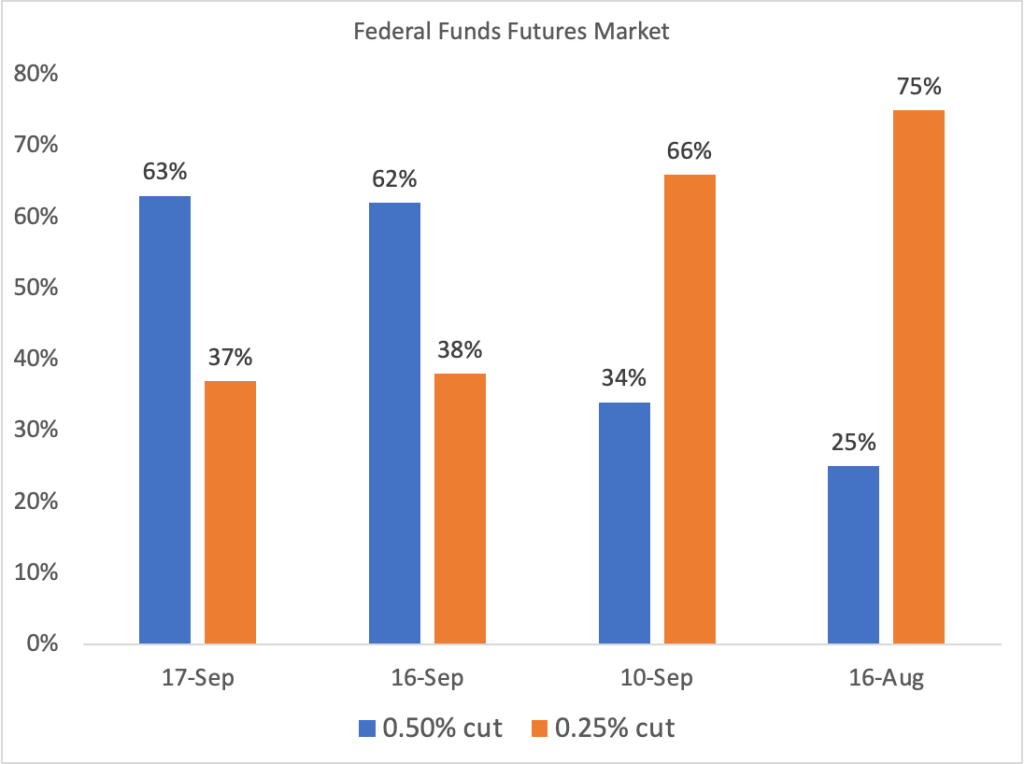

The following figure summarizes the implied probabilities from federal funds rate futures trading of the FOMC cutting its target by 25 basis points (the orange bars) or 50 basis points (the blue bars) at tomorrow’s meeting. The probabilities on four days are shown—today, yesterday, one week ago, and one month ago.

The figure shows how sentiment among investors has changed over the past month. On August 16, investors assigned a 75 percent probability of a 25 basis point cut in the target range and only a 25 percent probability of a 50 basis point cut. Yesterday and today, investor sentiment has swung sharply toward expecting a 50 basis point cut. Why the shift? As the Fed attempts to fulfill its dual mandate of maximum employment and price stability, it’s focus since the spring of 2022 had been on bringing inflation back down to its 2 perecent target. But as the unemployment rate has slowly risen, output growth has cooled, and more consumers are delinquent on their auto loan and credit card payments, some members of the committee now believe that the committee made a mistake in not cutting the target range by 25 basis points at its last meeting at the end of July. For these members, a 50 basis point cut tomorrow would bring the changes in the target range back on track.

How well did investors in the federal funds futures market forecast the FOMC’s decision? If you are reading this after 2 p.m. EDT on September 18, you’ll know the answer.

Supports: Macroeconomics, Chapter 15,Economics, Chapter 25, Essentials of Economics, Chapter 17, and Money, Banking, and the Financial System, Chapter 15.

Image generated by ChatGTP-4o.

In a book review in the Wall Street Journal, the financial writer James Grant referred to “the Federal Reserve’s goal to cheapen the dollar by 2% a year.”

Briefly explain what “cheapen the dollar” means.

Briefly explain what Grant means by writing that the Fed has a “goal to cheapen the dollar by 2% a year.”

Do you agree with Grant that the Fed has this goal? Briefly explain.

Solving the Problem Step 1: Review the chapter material. This problem is about the economic effects of the Federal Reserve’s policy goal of a 2 percent annual inflation rate, so you may want to review Chapter 15, Section 15.5, “A Closer Look at the Fed’s Setting Monetary Policy Targets.”

Step 2: Answer part a. by explaining what “cheapen the dollar” means. Judging from the context, “cheapen the dollar” means to reduce the purchasing power of a dollar. Whenever inflation occurs, the amount of goods and services a dollar can purchase declines. If the inflation rate in a year is 10 percent, than at the end of the year $1,000 can buy 10 percent fewer goods and services than it could at the beginning of the year.

Step 3: Answer part b. by expalining what Grant means by the Fed having a goal of cheapening the dollar by 2 percent a year. Congress has given a dual mandate of high employment and price stability. Since 2012, the Fed has interpreted a 2 percent annual inflation rate as meeting its mandate for price stability. So, Grant means that the Fed’s 2 percent annual inflation goal in effect is also a goal to cheapen—or reduce the purchasing power of the dollar—by 2 percent a year.

Step 4: Answer part c. by explaining whether you agree with Grant that the Fed has a goal of cheapening the dollar by 2 percent a year. As explained in the answer to part b., there is a sense in which Grant is correct; the Fed’s goal of a 2 percent inflation rate is a goal of allowing the purchasing power of the dollar to decline by 2 percent a year. One complication, however, is that most economists believe that changes in price indexes such as the consumer price index (CPI) and the personal consumption expenditures (PCE) price index overstate the actual amount of inflation occurring in the economy. As we discuss in Macroeconomics, Chapter 9, Section 9.4 (Economics, Chapter 19, Section 19.4, and Essentials of Economics, Chapter 13, Section 13.4), there are several biases that cause price indexes to overstate the true inflation rate; the most important of the biases is the failure of price indexes to take fully into account improvements over time in the quality of many goods and services. If increases in price indexes are overstating the inflation rate by one percentage point, then the Fed’s goal of a 2 percent inflation rate results in the dollar losing 1 percent—rather than 2 percent—of its purchasing power over time, corrected for changes in quality.

Federal Reserve Chair Jerome Powell at Jackson Hole, Wyoming, August 2023 (Photo from the Associated Press.)

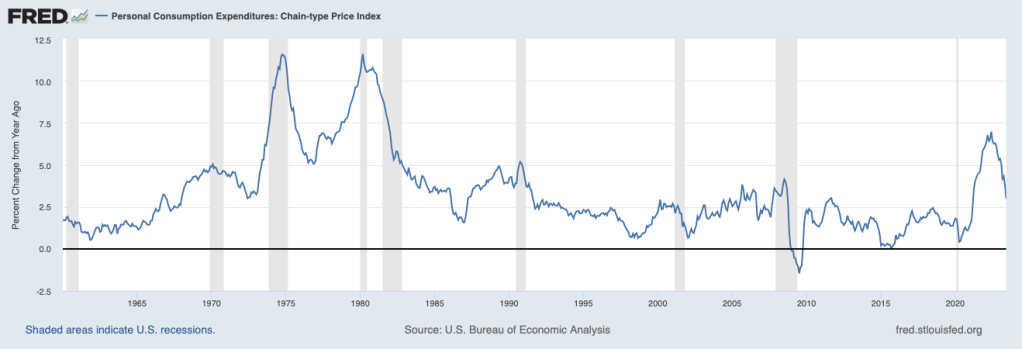

Congress has given the Federal Reserve a dual mandate to achieve price stability and high employment. To reach its goal of price stability, the Fed has set an inflation target of 2 percent, with inflation being measured by the percentage change in the personal consumption expenditures (PCE) price index.

It’s reasonable to ask whether “price stability” is achieved only when the price level is constant—that is, at a zero inflation rate. In practice, Congress has given the Fed wide latitude in deciding when price stability and high employment has been achieved. The Fed didn’t announce a formal inflation target of 2 percent until 2012. But the members of the Federal Open Market Committee (FOMC) had agreed to set a 2 percent inflation target much earlier—in 1996—although they didn’t publicly announce it at the time. (The transcript of the FOMC’s July 2-3, 1996 meeting includes a discussion of the FOMC’s decision to adopt an inflation target.) Implicitly, the FOMC had been acting as if it had a 2 percent target since at least the mid–1980s.

But why did the Fed decide on an inflation target of 2 percent rather than 0 percent, 1 percent, 3 percent, or some other rate? There are three key reasons:

As we discuss in Macroeconomics, Chapter 9, Section 9.4 (Economics, Chapter 19, Section 29.4 and Essentials of Economics, Chapter 13, Section 13.4), price indexes overstate the actual inflation rate by 0.5 percentage point to 1 percentage point. So, a measured inflation of 2 percent corresponds to an actual inflation rate of 1 to 1.5 percent.

As we discuss in Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5), the FOMC has a target for the long-run real federal funds rate. Although the target has been as high as 2 percent, in recent years it has been 0.5 percent. With an inflation target of 2 percent, the long-run nominal federal funds rate target is 2.5 percent. (The FOMC’s long-run target federall funds target can be found in the Summary of Economic Projections here.) As the Fed notes, with an inflation target of less than 2 percent “there would be less room to cut interest rates to boost employment during an economic downturn.”

An inflation target of less than 2 percent would make it more likely that during recessions, the U.S. economy might experience deflation, or a period during which the price level is falling. Deflation can be damaging if falling prices cause consumers to postpone purchases in the hope of being able to buy goods and services at lower prices in the future. The resulting decline in aggregate demand can make a recession worse. In addition, deflation increases the real interest rate associated with a given nominal interest rate, imposing costs on borrowers, particularly if the deflation is unexpected.

The following figure shows that for most of the period from late 2008 until the spring of 2021, the inflation rate as measured by the PCE was below the Fed’s 2 percent target. Beginning in the spring of 2021, inflation soared, reaching a peak of 7.0 percent in June 2022. Inflation declined over the following year, falling to 3.0 in June 2023.

On August 25, at the Fed’s annual monetary policy symposium in Jackson Hole, Wyoming, Fed Chair Jerome Powell made clear that the Fed intended to continue a restrictive monetary policy until the inflation rate had returned to 2 percent: “It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so.” (The text of Powell’s speech can be found here.) Some economists have been arguing that once the Fed had succeeded in pushing the inflation rate back to 2 percent it should, in the future, consider raising its inflation target to 3 percent. At Jackson Hole, Powell appeared to rule out this possibility: “Two percent is and will remain our inflation target.”

Why might a 3 percent inflation target be preferrable to a 2 percent inflation target? Proponents of the change point to two key advantages:

Reducing the likelihood of monetary policy being constrained by the zero lower bound. Because the federal funds rate can’t be negative, zero provides a lower bound on how much the FOMC can cut its federal funds rate target in a recession. Monetary policy was constrained by the zero lower bound during both the Great Recession of 2007–2009 and the Covid recession of 2020. Because an inflation target of 3 percent could likely be achieved with a federal funds rate that is higher than the FOMC’s current long-run target of 2.5 percent, the FOMC should have more room to cut its target during a recession.

During a recession, firms attempting to reduce costs can do so by cutting workers’ nominal wages. But, as we discuss in Macroeconomics, Chapter 13, Section 13.2 (Economics, Chapter 23, Section 23.2 and Essentials of Economics, Chapter 15, Section 15.2), most workers dislike wage cuts. Some workers will quit rather than accept a wage cut and the productivity of workers who remain may decline. As a result, firms often use a policy of freezing wages rather than cutting them. Freezing nominal wages when inflation is occurring results in cuts to real wages. The higher the inflation rate, the greater the decline in real wages and the more firms can reduce their labor costs without laying off workers.

Why would Powell rule out increasing the Fed’s target for the inflation rate? Although he didn’t spell out the reasons in his Jackson Hole speech, these are two main points usually raised by those who favor keeping the target at 2 percent:

A target rate above 2 percent would be inconsistent with the price stability component of the Fed’s dual mandate. During the years between 2008 and 2021 when the inflation rate was usually at or below 2 percent, most consumers, workers, and firms found the inflation rate to be low enough that it could be safely ignored. A rate of 3 percent, though, causes money to lose its purchasing power more quickly and makes it less likely that people will ignore it. To reduce the effects of inflation people are likely to spend resources in ways such as firms reprinting menus or price lists more frequently or labor unions negotiating for higher wages in multiyear wage contracts. The resources devoted to avoiding the negative effects of inflation represent an efficiency loss to the economy.

Raising the target for the inflation rate might undermine the Fed’s credibility in fighting inflation. One of the reasons that the Fed was able to bring down the inflation rate without causing a recession—at least through August 2023—was that the expectations of workers, firms, and investors remained firmly anchored. That is, there was a general expectation that the Fed would ultimately succeed in bringing the inflation back down to 2 percent. If expectations of inflation become unanchored, fighting inflation becomes harder because workers, firms, and investors are more likely to take actions that contribute to inflation. For instance, lenders won’t assume that inflation will be 2 percent in the future and so will require higher nominal interest rates on loans. Workers will press for higher nominal wages to protect themselves from the effects of higher inflation, thereby raising firms’ costs. Raising its inflation target to 3 percent may also cause workers, firms, and investors to question whether during a future period of high inflation the Fed will raise its target to an even higher rate. If that happens, inflation may be more persistent than it was during 2022 and 2023.

It seems unlikely that the Fed will raise its target for the inflation rate in the near future. But the Fed is scheduled to review its current monetary policy strategy in 2025. It’s possible that as part of that review, the Fed may revisit the issue of its inflation target.