Federal Reserve Governor Christopher J. Waller (photo from the Associated Press via the Wall Street Journal)

Fed Governor Christopher Waller has a reputation for being a policy hawk, which means that since the spring of 2022 he has been a forceful advocate of multiple increases in the target for the federal funds rate as the Fed attempts to slow the economy and bring inflation back to the Fed’s 2 percent target. (Waller’s biography on the Fed’s web site can be found here.)

So, it was notable that in a speech at the American Enterprise Institute (AEI) on November 28, he said that “I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2 percent.” Although he also stressed that “there is still significant uncertainty about the pace of future activity, and so I cannot say for sure whether the [Federal Open Market Committee] FOMC has done enough to achieve price stability” his remarks were interpreted as reinforcing the growing view among non-Fed economists and investors that the FOMC is unlikely to increase its target for the federal funds rate further and is likely to reduce the target at some point during 2024. The text of Waller’s speech can be found here.

AEI economist Michael Strain interviewed Waller following his speech. In the interview (which can be found here), Strain made the case for believing that the Fed’s ability to achieve a soft landing—returning inflation to the 2 percent target without pushing the economy into a recession—would be more difficult than Waller seems to believe. Included in the interview are discussions of whether expecting a soft landing is consistent with the historical record, what guidance the Taylor rule can give to monetary policymakers (we discuss the Taylor rule in Macroeconomics, Chapter 15, Section 15.5, Economics, Chapter 25, Section 15.5, and Essentials of Economics, Chapter 17, Section 17.5), the significance of rising labor force participation rates among prime-age workers, and the implications large federal budget deficits have for monetary policy.

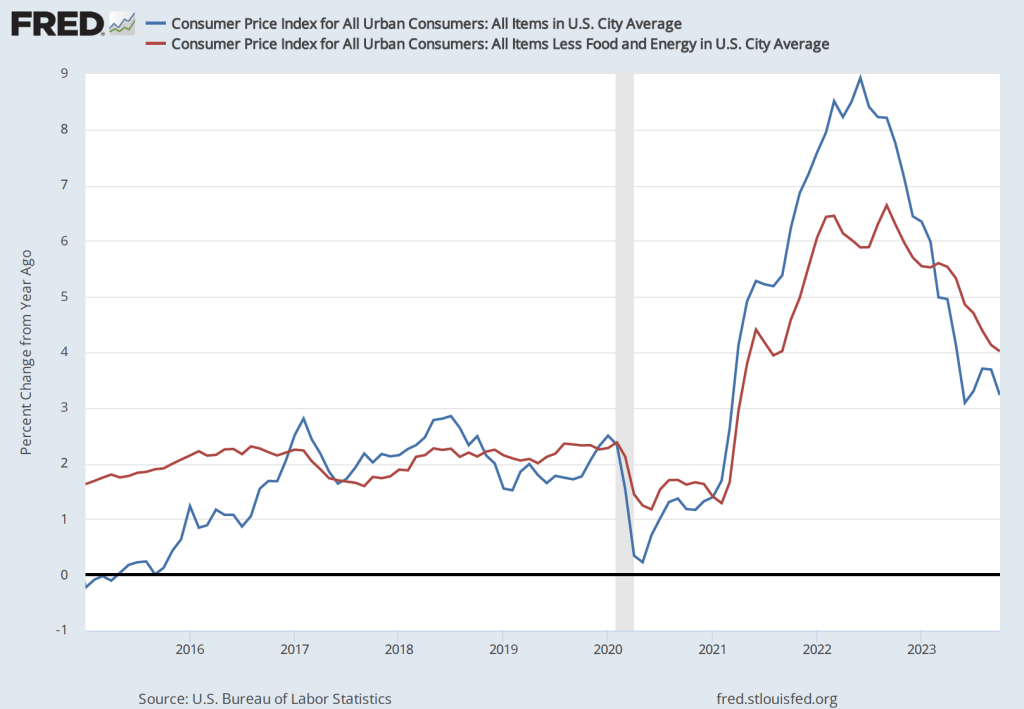

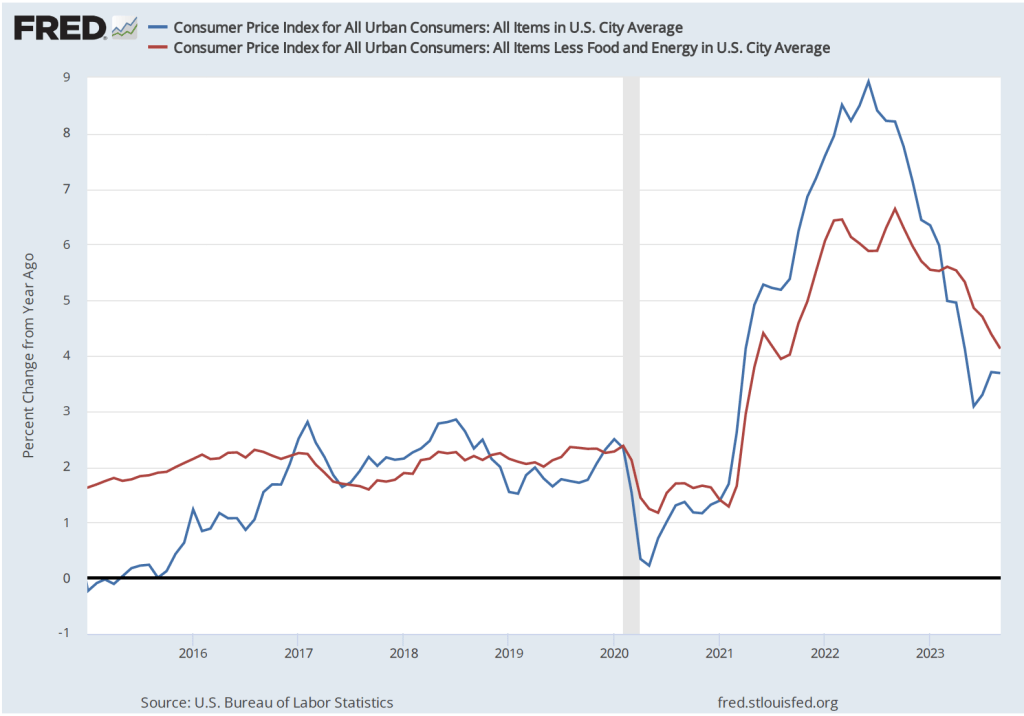

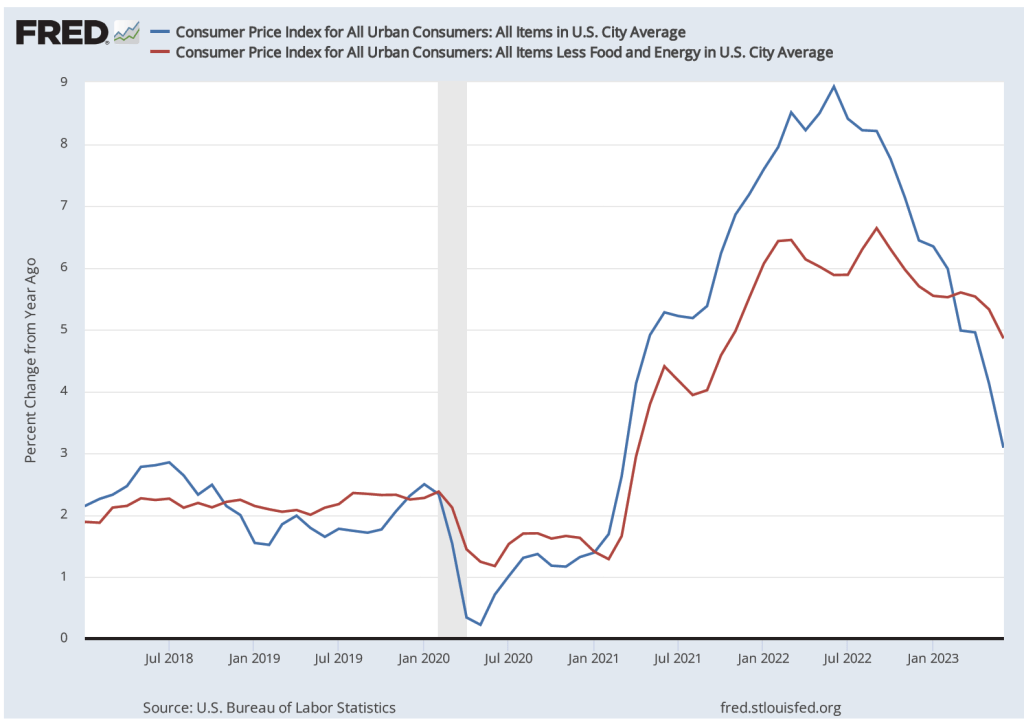

The Bureau of Labor Statistics released its latest report on consumer prices the morning of November 14. The Wall Street Journal’sheadline reflects the general reaction to the report: The inflation rate continued to decline, which made it less likely that the Fed’s Federal Open Market Committee will raise its target range for the federal funds rate again at its December meeting. The following figure shows inflation measured as the percentage change in the Consumer Price Index (CPI) from the same month in the previous year. It also shows the inflation rate measure using “core” CPI, which excludes prices for food and energy.

The inflation rate for the CPI declined from 3.7 percent in September to 3.2 percent in October. Core CPI declined from 4.1 percent in September to 4.0 percent in October. So, measured this way, inflation declined substantially when measured by the CPI including prices of all goods and services but only slightly when measured using core CPI.

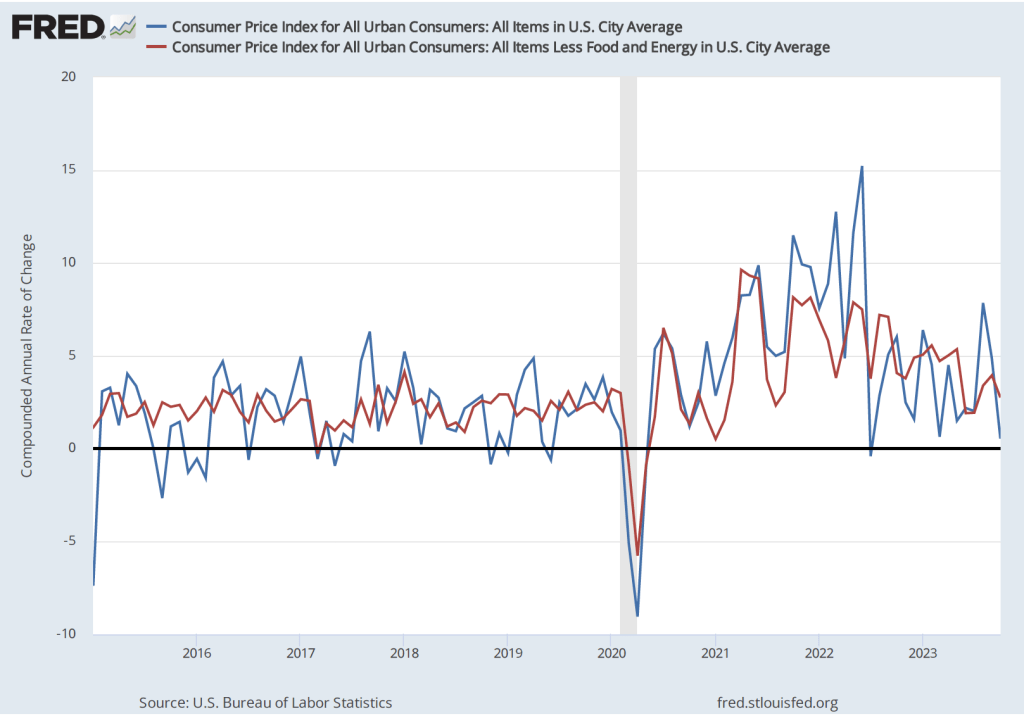

The 12-month inflation rate is the one typically reported in the Wall Street Journal and elsewhere, but it has the drawback that it doesn’t always reflect accurately the current trend in prices. The following figure shows the 1-month inflation rate—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year— for CPI and core CPI. The 1-month inflation rate is naturally more volatile than the 12-month inflation rate. In this case, 1-month rate shows a sharp decline in the inflation rate for the CPI from 4.9 percent in September to 0.5 percent in October. Core inflation declined less sharply from 3.9 percent in September to 2.8 percent in October.

The release of the CPI report was treated as good news on Wall Street, with the Dow Jones Industrial Average increasing by 500 points and the interest rate on the 10-year U.S. Treasury Note declining from 4.6 percent just before the report was released to 4.4 percent immediately after. The increases in stock and bond prices (recall that the prices of bonds and the yields on the bonds move in opposite directions, so bond prices rose following release of the report) reflect the view of financial investors that if the FOMC stops increasing its target for the federal funds rate, the chance that the U.S. economy will fall into a recession is reduced.

A word of caution, however. In a speech on November 9, Fed Chair Jerome Powell noted that the FOMC may need still need to implement additional increases to its federal funds rate target:

“My colleagues and I are gratified by this progress [against inflation] but expect that the process of getting inflation sustainably down to 2 percent has a long way to go…. The Federal Open Market Committee (FOMC) is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance. We know that ongoing progress toward our 2 percent goal is not assured: Inflation has given us a few head fakes. If it becomes appropriate to tighten policy further, we will not hesitate to do so.”

So, while the latest inflation report is good news, it’s still too early to know whether inflation is on a stable path to return to the Fed’s 2 percent target. (It’s worth noting that the Fed uses inflation as measured by the personal consumption expenditure (PCE) price index rather than as measured by the CPI when evaluating whether it has achieved its 2 percent target.)

Some interesting macro data were released during the past two weeks. On the key issues, the data indicate that inflation continues to run in the range of 3.0 percent to 3.5 percent, although depending on which series you focus on, you could conclude that inflation has dropped to a bit below 3 percent or that it is still in vicinity of 4 percent. On balance, output and employment data seem to be indicating that the economy may be cooling in response to the contractionary monetary policy that the Federal Open Market Committee began implementing in March 2022.

We can summarize the key data releases.

Employment, Unemployment, and Wages

On Friday morning, the Bureau of Labor Statistics (BLS) released its Employment Situation report. (The full report can be found here.) Economists and policymakers—notably including the members of the Federal Reserve’s Federal Open Market Committee (FOMC)—typically focus on the change in total nonfarm payroll employment as recorded in the establishment, or payroll, survey. That number gives what is generally considered to be the best indicator of the current state of the labor market.

The previous month’s report included a surprisingly strong net increase of 336,000 jobs during September. Economists surveyed by the Wall Street Journal last week forecast that the net increase in jobs in October would decline to 170,000. The number came in at 150,000, slightly below that estimate. In addition, the BLS revised down the initial estimates of employment growth in August and September by a 101,000 jobs. The figure below shows the net gain in jobs for each month of 2023.

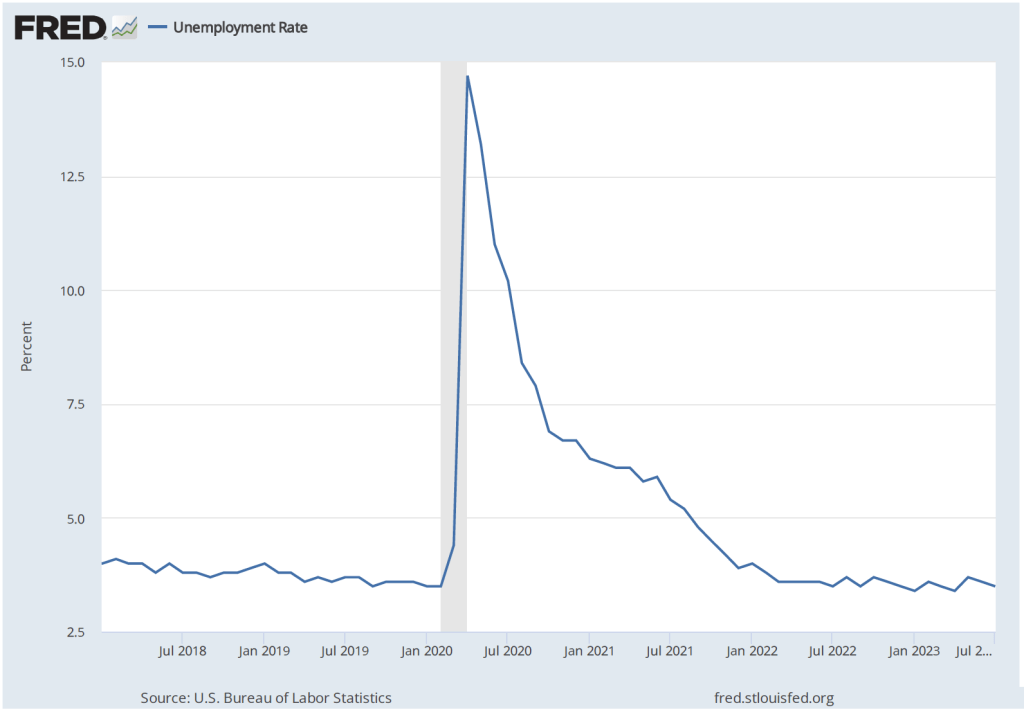

Although there are substantial fluctuations, employment increases have slowed in the second half of the year. The average increase in employment from January to June was 256,667. From July to October the average increase declined to 212,000. In the household survey, the unemployment rate ticked up from 3.8 percent in September to 3.9 percent in October. The unemployment rate has now increased by 0.5 percentage points from its low of 3.4 percent in April of this year.

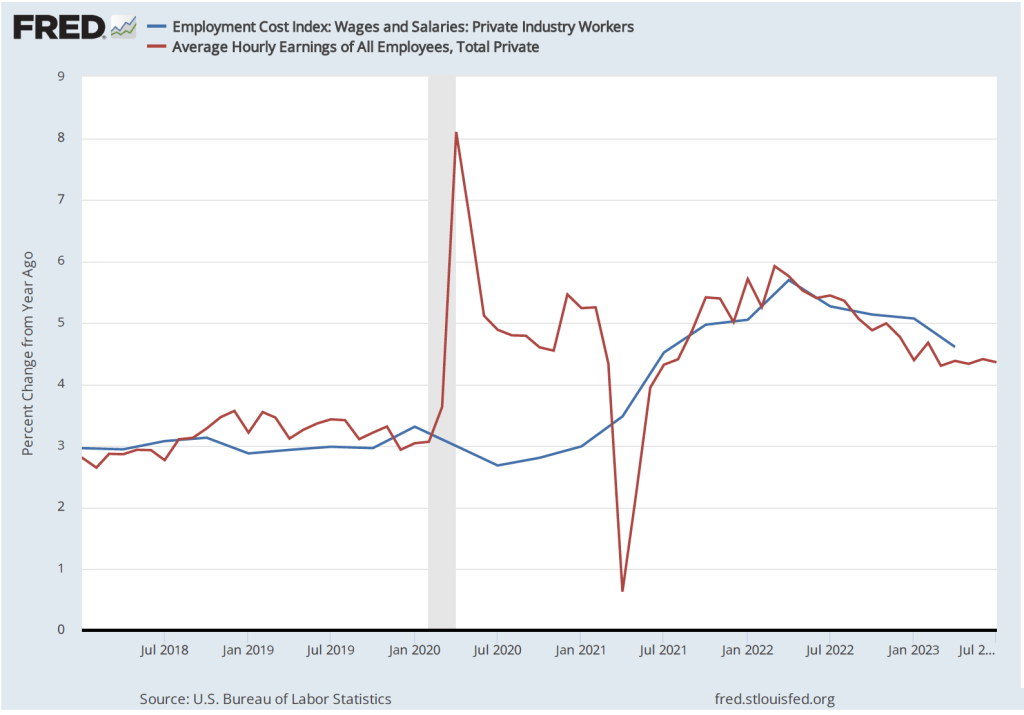

Finally, data in the employment report provides some evidence of a slowing in wage growth. The following figure shows wage inflation as measured by the percentage increase in average hourly earnings (AHE) from the same month in the previous year. The increase in October was 4.1 percent, continuing a generally downward trend since March 2022, although still somewhat above wage inflation during the pre-2020 period.

As the following figure shows, September growth in average hourly earnings measured as a compound annual growth rate was 2.5 percent, which—if sustained—would be consistent with a rate of price inflation in the range of the Fed’s 2 percent target. (The figure shows only the months since January 2021 to avoid obscuring the values for recent months by including the very large monthly increases and decreases during 2020.)

Job Openings and Labor Turnover Survey (JOLTS)

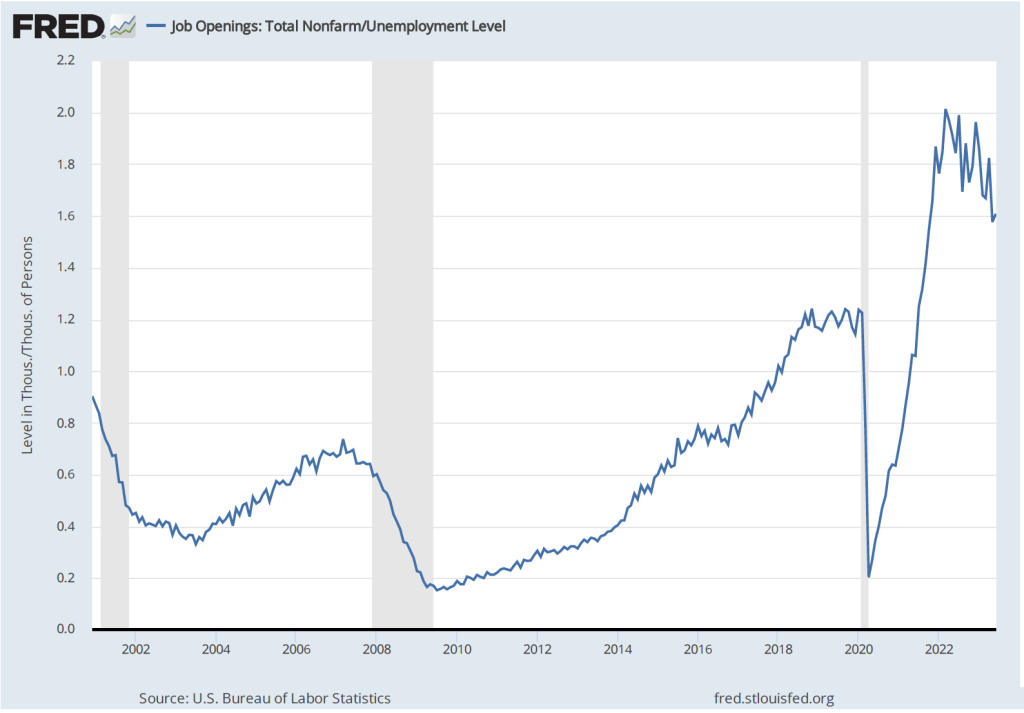

On November 1, the BLS released its Job Openings and Labor Turnover Survey (JOLTS) report for September 2023. (The full report can be found here.) The report indicated that the number of unfilled job openings was 9.5 million, well below the peak of 11.8 million job openings in December 2021 but—as shown in the following figure—well above prepandemic levels.

The following figure shows the ratio of the number of job opening to the number of unemployed people. The figure shows that, after peaking at 2.0 job openings per unemployed person in in March 2022, the ratio has decline to 1.5 job opening per unemployed person in September 2022. While high, that ratio was much closer to the ratio of 1.2 that prevailed during the year before the pandemic. In other words, while the labor market still appears to be strong, it has weakened somewhat in recent months.

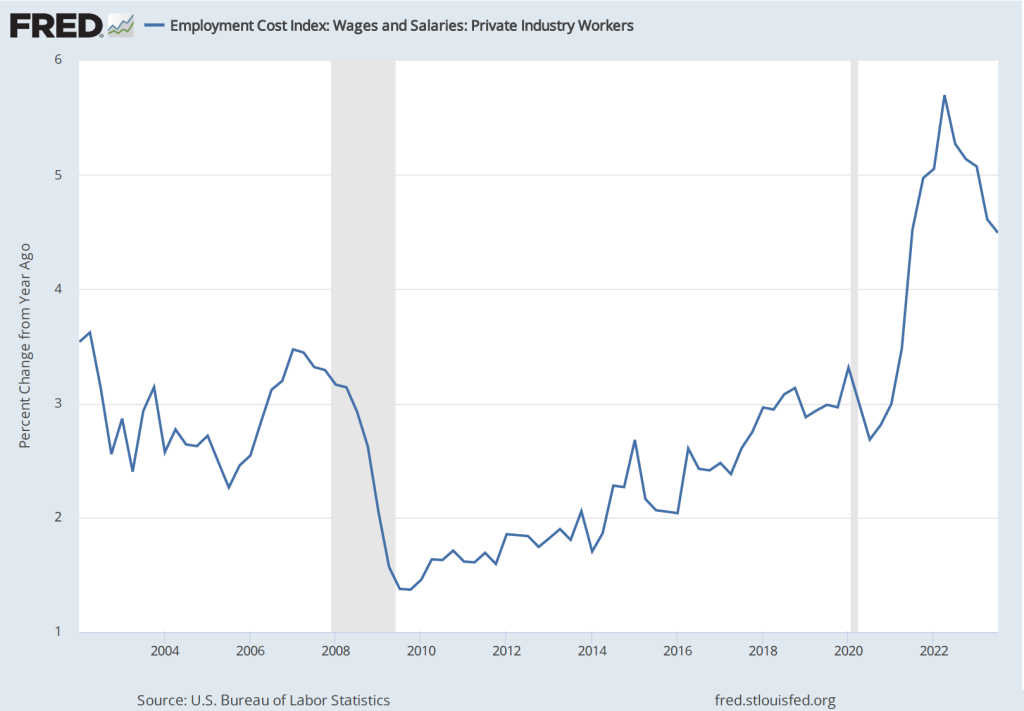

Employment Cost Index

As we note in this blog post, the employment cost index (ECI), published quarterly by the BLS, measures the cost to employers per employee hour worked and can be a better measure than AHE of the labor costs employers face. The BLS released its most recent report on October 31. (The report can be found here.) The first figure shows the percentage change in ECI from the same quarter in the previous year. The second figure shows the compound annual growth rate of the ECI. Both measures show a general downward trend in the growth of labor costs, although compound annual rate of change shows an uptick in the third quarter of 2023. (We look at wages and salaries rather than total compensation because non-wage and salary compensation can be subject to fluctuations unrelated to underlying trends in labor costs.)

The Federal Open Market Committee’s October 31-November 1 Meeting

As was widely expected from indications in recent statements by committee members, the Federal Open Market Committee voted at its most recent meeting to hold constant its targe range for the federal funds rate at 5.25 percent to 5.50 percent. (The FOMC’s statement can be found here.)

At a press conference following the meeting, Fed Chair Jerome Powell remarks made it seem unlikely that the FOMC would raise its target for the federal funds rate at its December 14-15 meeting—the last meeting of 2023. But Powell also noted that the committee was unlikely to reduce its target for the federal funds rate in the near future (as some economists and financial jounalists had speculated): “The fact is the Committee is not thinking about rate cuts right now at all. We’re not talking about rate cuts, we’re still very focused on the first question, which is: have we achieved a stance of monetary policy that’s sufficiently restrictive to bring inflation down to 2 percent over time, sustainably?” (The transcript of Powell’s press conference can be found here.)

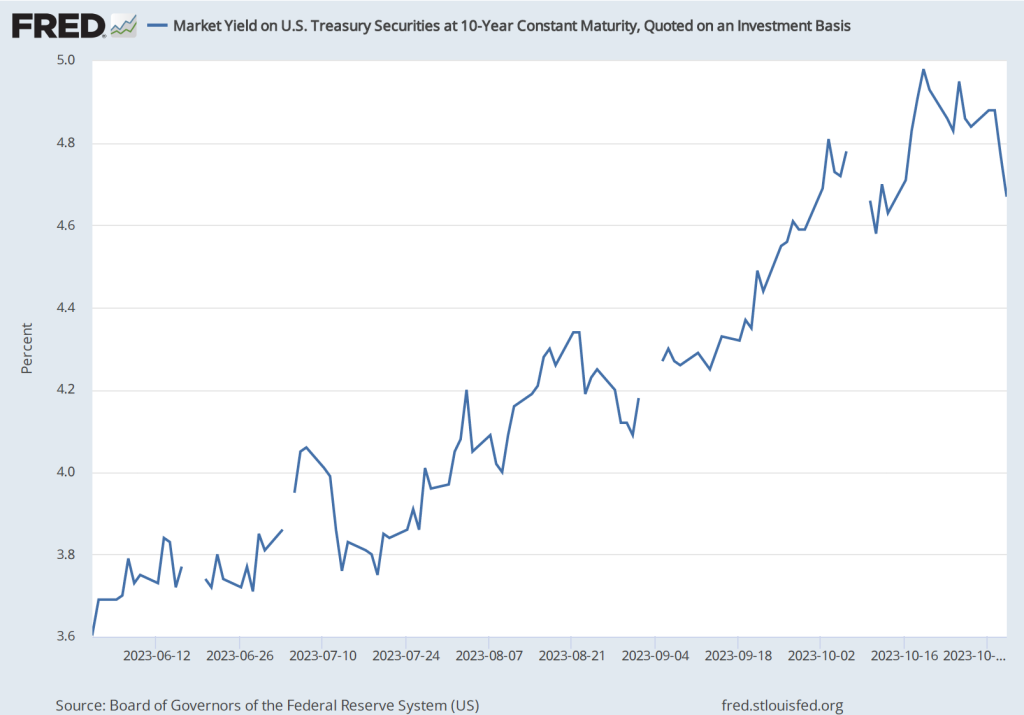

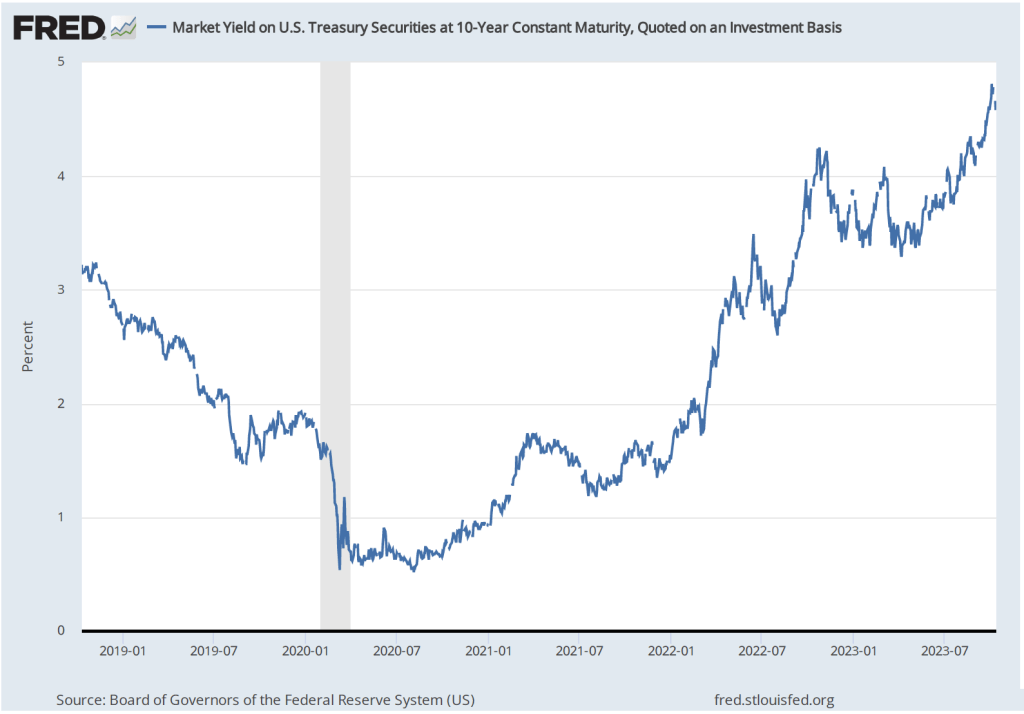

Investors in the bond market reacted to Powell’s press conference by pushing down the interest rate on the 10-year Treasury note, as shown in the following figure. (Note that the figure gives daily values with the gaps representing days on which the bond market was closed) The interest rate on the Treasury note reflects investors expectations of future short-term interest rates (as well as other factors). Investors interpreted Powell’s remarks as indicating that short-term rates may be somewhat lower than they had previously expected.

Real GDPand the Atlanta Fed’s Real GDPNow Estimate for the Fourth Quarter

On October 26, the Bureau of Economic Analysis (BEA) released its advance estimate of real GDP for the third quarter of 2023. (The full report can be found here.) We discussed the report in this recent blog post. Although, as we note in that post, the estimated increase in real GDP of 4.9 percent is quite strong, there are indications that real GDP may be growing significantly more slowly during the current (fourth) quarter.

The Federal Reserve Bank of Atlanta compiles a forecast of real GDP called GDPNow. The GDPNow forecast uses data that are released monthly on 13 components of GDP. This method allows economists at the Atlanta Fed to issue forecasts of real GDP well in advance of the BEA’s estimates. On November 1, the GDPNow forecast was that real GDP in the fourth quarter of 2023 would increase at a slow rate of 1.2 percent. If this preliminary estimate proves to be accurate, the growth rate of the U.S. economy will have sharply declined from the third to the fourth quarter.

Fed Chair Powell has indicated that economic growth will likely need to slow if the inflation rate is to fall back to the target rate of 2 percent. The hope, of course, is that contractionary monetary policy doesn’t cause aggregate demand growth to slow to the point that the economy slips into a recession.

Fed Chair Jerome Powell and Fed Vice-Chair Philip Jefferson this summer at the Fed conference in Jackson Hole, Wyoming. (Photo from the AP via the Washington Post.)

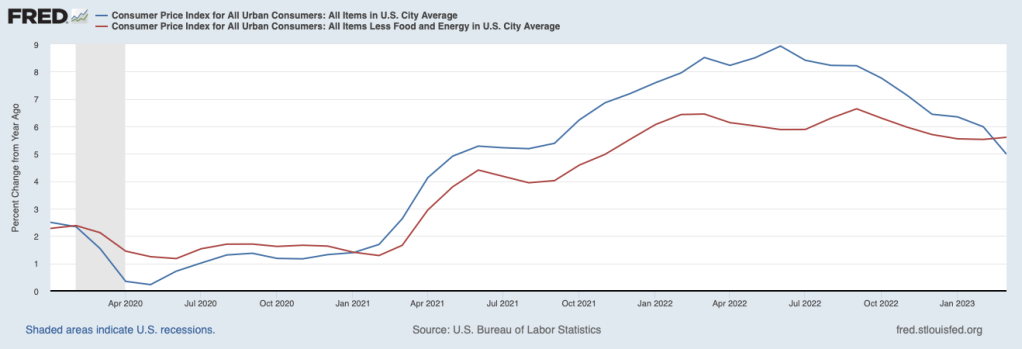

This morning, the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for September. (The full report can be found here.) The report was consistent with other recent data showing that inflation has declined markedly from its summer 2022 highs, but appears, at least for now, to be stuck in the 3 percent to 4 percent range—well above the Fed’s 2 percent inflation target.

The report indicated that the CPI rose by 0.4 percent in September, which was down from 0.6 percent in August. Measured by the percentage change from the same month in the previous year, the inflation rate was 3.7 percent, the same as in August. Core CPI, which excludes the prices of food and energy, increased by 4.1 percent in September, down from 4.4 percent in August. The following figure shows inflation since 2015 measured by CPI and core CPI.

Reporters Gabriel Rubin and Nick Timiraos, writing in the Wall Street Journalsummarized the prevailing interpretation of this report:

“The latest inflation data highlight the risk that without a further slowdown in the economy, inflation might settle around 3%—well below the alarming rates that prompted a series of rapid Federal Reserve rate increases last year but still above the 2% inflation rate that the central bank has set as its target.”

As we discuss in this blog post, some economists and policymakers have argued that the Fed should now declare victory over the high inflation rates of 2022 and accept a 3 percent inflation rate as consistent with Congress’s mandate that the Fed achieve price stability. It seems unlikely that the Fed will follow that course, however. Fed Chair Jerome Powell ruled it out in a speech in August: “It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so.”

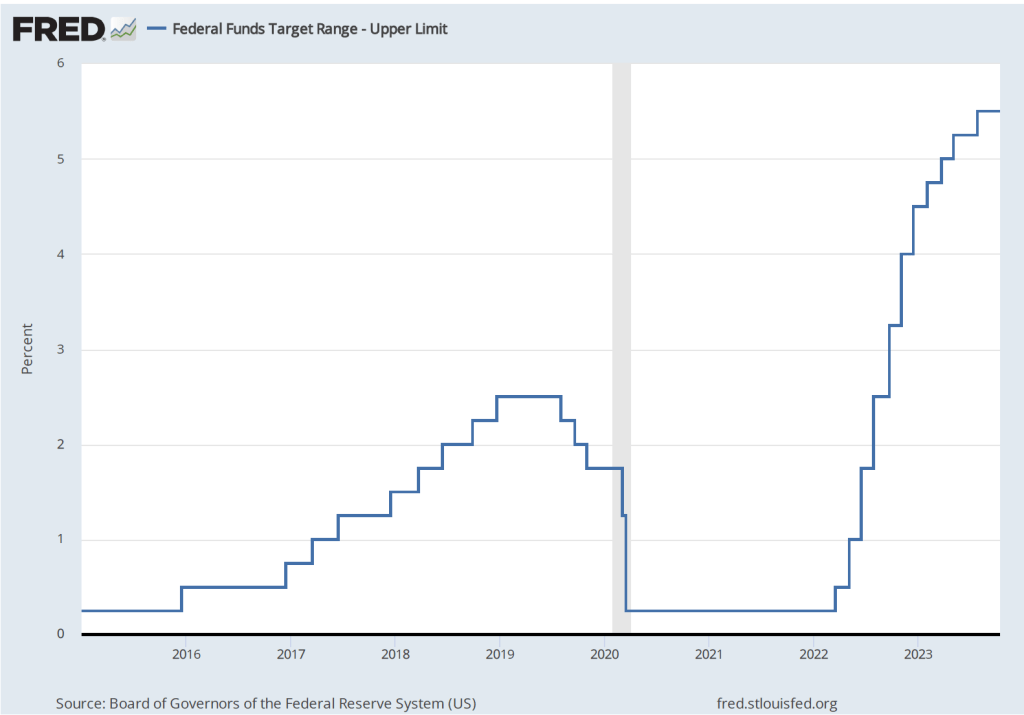

To achieve its goal of bringing inflation back to its 2 percent targer, it seems likely that economic growth in the United States will have to slow, thereby reducing upward pressure on wages and prices. Will this slowing require another increase in the Federal Open Market Committe’s target range for the federal funds rate, which is currently 5.25 to 5.50 percent? The following figure shows changes in the upper bound for the FOMC’s target range since 2015.

Several members of the FOMC have raised the possibility that financial markets may have already effectively achieved the same degree of policy tightening that would result from raising the target for the federal funds rate. The interest rate on the 10-year Treasury note has been steadily increasing as shown in the following figure. The 10-year Treasury note plays an important role in the financial system, influencing interest rates on mortgages and corporate bonds. In fact, the main way in which monetary policy works is for the FOMC’s increases or decreases in its target for the federal funds rate to result in increases or decreases in long-run interest rates. Higher long-run interest rates typically result in a decline in spending by consumrs on new housing and by businesses on new equipment, factories computers, and software.

Federal Reserve Bank of Dallas President Lorie Logan, who serves on the FOMC, noted in a speech that “If long-term interest rates remain elevated … there may be less need to raise the fed funds rate.” Similarly, Fed Vice-Chair Philip Jefferson stated in a speech that: “I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

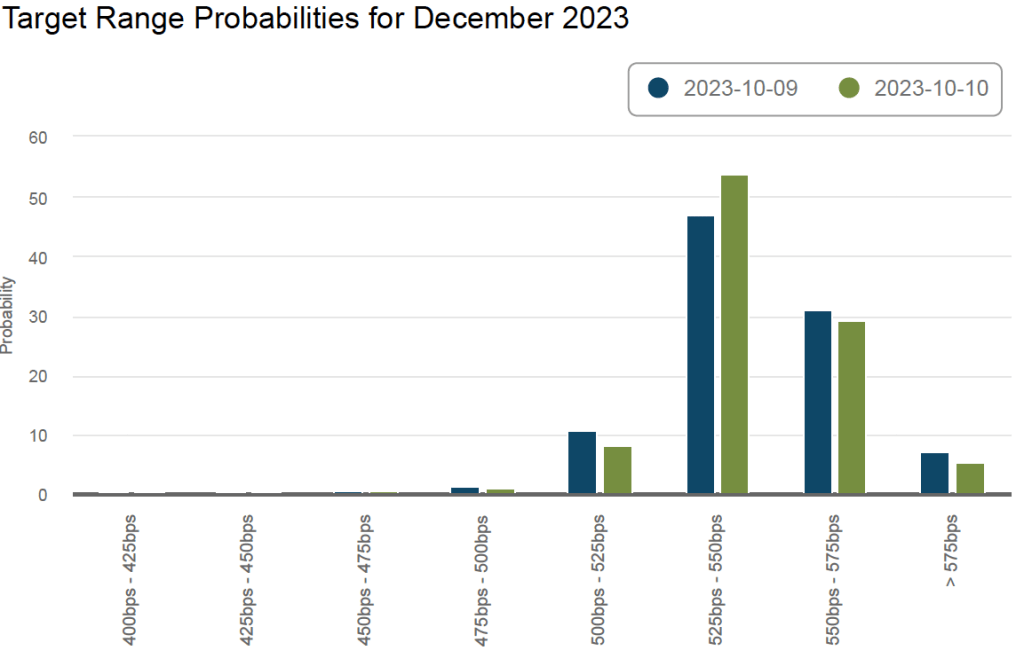

The FOMC has two more meetings scheduled for 2023: One on October 31-November 1 and one on December 12-13. The following figure from the web site of the Federal Reserve Bank of Atlanta shows financial market expectations of the FOMC’s target range for the federal funds rate in December. According to this estimate, financial markets assign a 35 percent probability to the FOMC raising its target for the federal funds rate by 0.25 or more. Following the release of the CPI report, that probability declined from about 38 percent. That change reflects the general expectation that the report didn’t substantially affect the likelihood of the FOMC raising its target for the federal funds rate again by the end of the year.

A trader on the New York Stock Exchange listtening to Fed Chair Jerome Powell (from Reuters via the New York Times)

Accounting for movements in the market prices of stocks and bonds is not an exact exercise. Accounts in the Wall Street Journal and on other business web sites often attribute movements in stock and bond prices to the Fed having acted in a way that investors didn’t expect.

The decision by the Fed’s Federal Open Market Committee (FOMC) at its meeting on September 20-21, 2023 to hold its target for the federal funds rate constant at a range of 5.25 percent to 5.50 percent wasn’t a surprise. Fed Chair Jerome Powell had signaled during his press conference on July 26 following the FOMC’s previous meeting that the FOMC was likely to pause further increases in the federal funds rate target. (A transcript of Powell’s July 26 press conference can be found here.)

In advance of the September meeting, some other members of the FOMC had also signaled that the committee was unlikely to increase its target. For instance, an article in the Wall Street Journal quoted Susan Collins, president of the Federal Reserve Bank of Boston, as stating that: “The risk of inflation staying higher for longer must now be weighed against the risk that an overly restrictive stance of monetary policy will lead to a greater slowdown than is needed to restore price stability.” And in a speech in August, Raphael Bostic, president of the Federal Reserve Bank of Atlanta, explained his position on future rate increases: “Based on current dynamics in the macroeconomy, I feel policy is appropriately restrictive. I think we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain.”

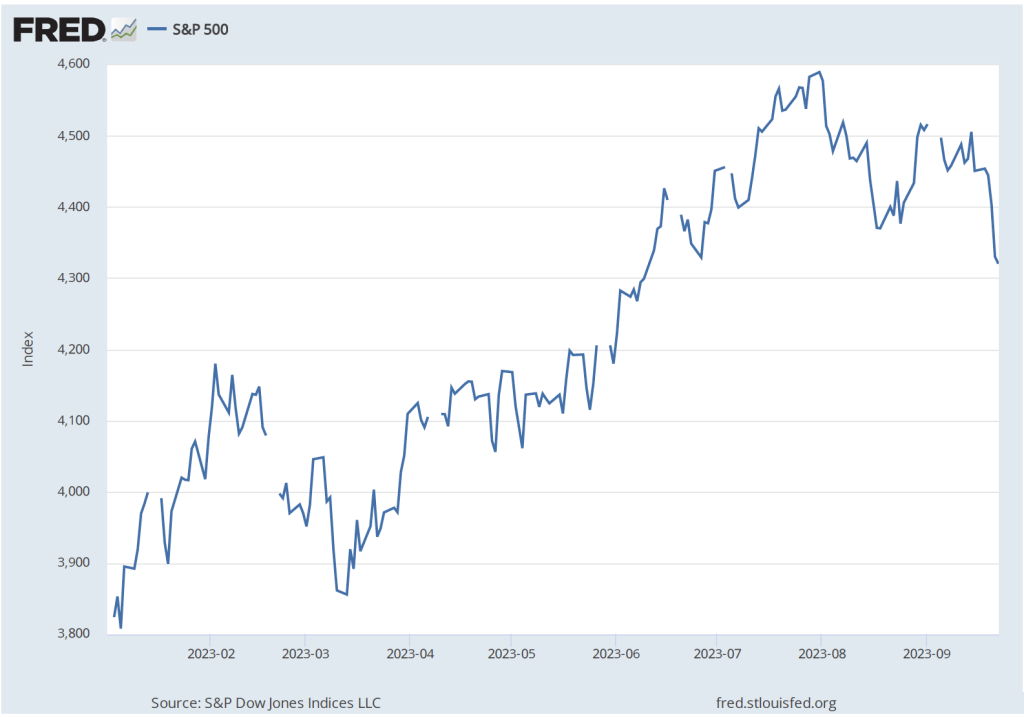

Although it wasn’t a surprise that the FOMCdecided to hold its target for the federal funds rate constant, after the decision was announced, stock and bond prices declined. The following figure shows the S&P 500 index of stock prices. The index declined 2.8 percent from September 19—the day before the FOMC meeting—to September 22—two days after the meeting. (We discuss indexes of stock prices in Macroeconomics, Chapter 6, Section 6.2; Economics, Chapter 8, Section 8.2; and Essentials of Economics, Chapter 8, Section 8.2.)

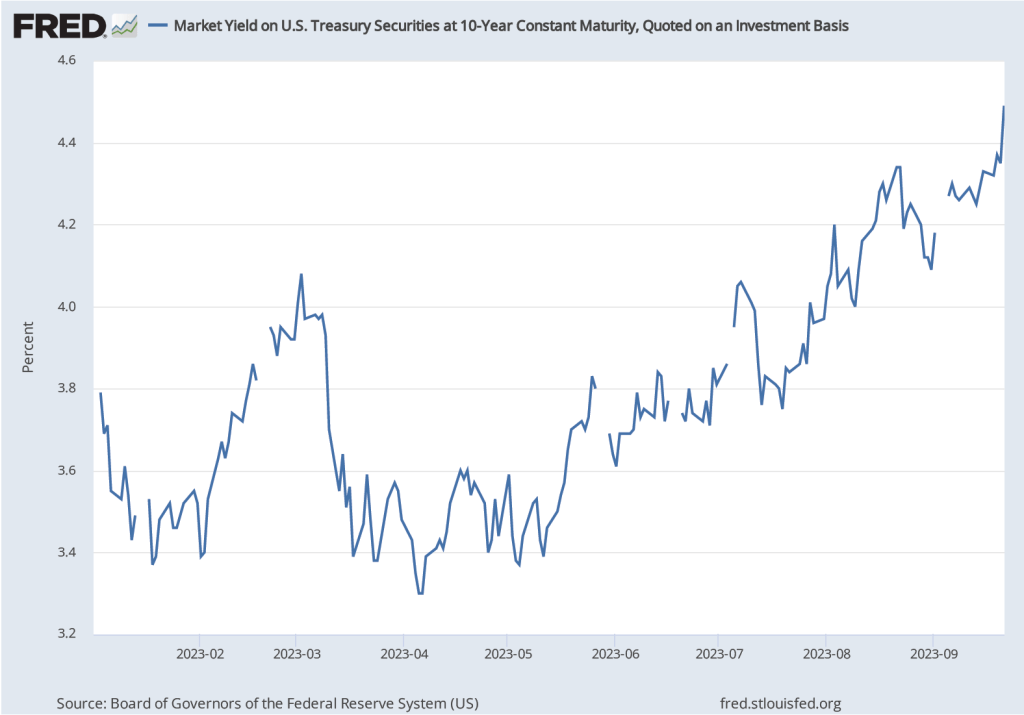

We see a similar pattern in the bond market. Recall that when the price of bonds declines in the bond market, the interest rates—or yields—on the bonds increase. As the following figure shows, the interest rate on the 10-year Treasury note rose from 4.37 percent on September 19 to 4.49 percent on September 21. The 10-year Treasury note plays an important role in the financial system, influencing interest rates on mortgages and corporate bonds. So, the yield on the 10-year Treasury note increasing from 3.3 percent in the spring of 2023 to 4.5 percent following the FOMC meeting has the effect of increasing long-term interest rates throughout the U.S. economy.

What explains the movements in the prices of stocks and bonds following the September FOMC meeting? Investors seem to have been surprised by: 1) what Chair Powell had to say in his news conference following the meeting; and 2) the committee members’ Summary of Economic Projections (SEP), which was released after the meeting.

Powell’s remarks were interpreted as indicating that the FOMC was likely to increase its target for the federal funds rate at least once more in 2023 and was unlikely to cut its target before late 2024. For instance, in response to a question Powell said: “We need policy to be restrictive so that we can get inflation down to target. Okay. And we’re going to need that to remain to be the case for some time.” Investors often disagree in their interpretations of what a Fed chair says. Fed chairs don’t act unilaterally because the 12 voting members of the FOMC decide on the target for the federal funds rate. So chairs tend to speak cautiously about future policy. Still, their seemed to be a consensus among investors that Powell was indicating that Fed policy would be more restrictive (or contractionary) than had been anticipated prior to the meeting.

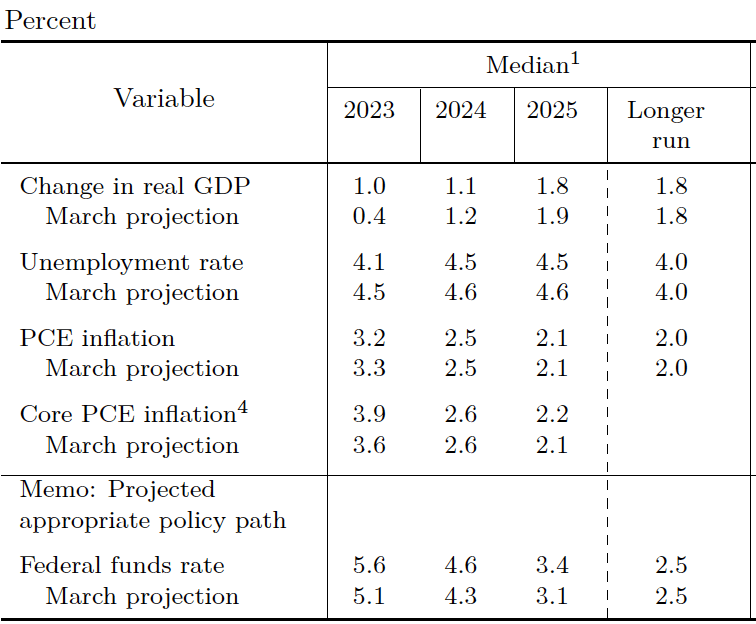

The FOMC releases the SEP four times per year. The most recent SEP before the September meeting was from the June meeting. The table below shows the median of the projections, or forecasts, of key economic variables made by the members of the FOMC at the June meeting. Note the second row from the bottom, which shows members’ median forecast of the federal funds rate.

The following table shows the median values of members’ forecast at the September meeting. Look again at the next to last row. The members’ forecast of the federal funds rate at the end of 2023 was unchanged. But their forecasts for the federal funds rate at the end of 2024 and 2025 were both 0.50 percent higher.

Why were members of the FOMC signaling that they expected to hold their target for the federal funds rate higher for a longer period? The other economic projections in the tables provide a clue. In September, the members expected that real GDP growth would be higher and the unemployment rate would be lower than they had expected in June. Stronger economic growth and a tighter labor market seemed likely to require them to maintain a contractionary monetary policy for a longer period if the inflation rate was to return to their 2.0 percent target. Note that the members didn’t expect that the inflation rate would return to their target until 2026.

A job fair in Albuquerque, New Mexico earlier this year. (Photo from Zuma Press via the Wall Street Journal.)

In his speech at the Kansas City Fed’s Jackson Hole, Wyoming symposium, Fed Chair Jerome Powell noted that: “Getting inflation back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.” To this point, there isn’t much indication that the U.S. economy is experiencing slower economic growth. The Atlanta Fed’s widely followed GDPNow forecast has real GDP increasing at a rapid 5.3 percent during the third quarter of 2023.

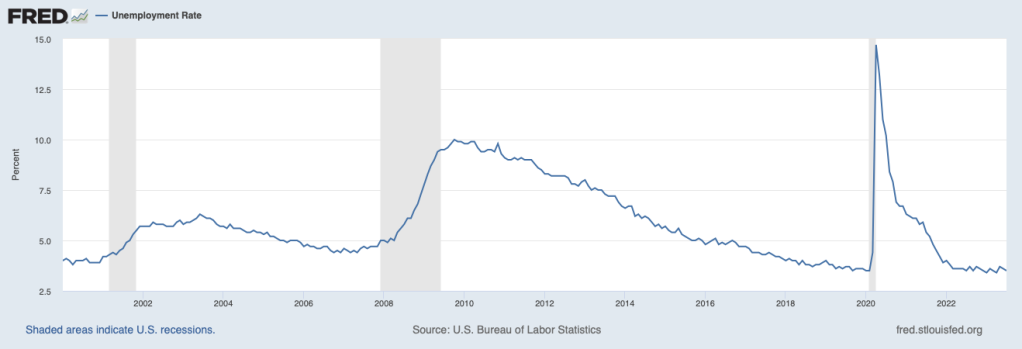

But the labor market does appear to be softening. The most familiar measure of the state of the labor market is the unemployment rate. As the following figure shows, the unemployment rate remains very low.

But, as we noted in this earlier post, an alternative way of gauging the strength of the labor market is to look at the ratio of the number of job openings to the number of unemployed workers. The Bureau of Labor Statistics (BLS) defines a job opening as a full-time or part-time job that a firm is advertising and that will start within 30 days. The higher the ratio of job openings to unemployed workers, the more difficulty firms have in filling jobs, and the tighter the labor market is. As indicated by the earlier quote from Powell, the Fed is concerned that in a very tight labor market, wages will increase more rapidly, which will likely lead firms to increase prices. The following figure shows that in July the ratio of job openings to unemployed workers has declined from the very high level of around 2.0 that was reached in several months between March 2022 and December 2022. The July 2023 value of 1.5, though, was still well above the level of 1.2 that prevailed from mid-2018 to February 2022, just before the beginning of the Covid–19 pandemic. These data indicate that labor market conditions continue to ease, although they remain tighter than they were just before the pandemic.

The following figure shows movements in the quit rate. The BLS calculates job quit rates by dividing the number of people quitting jobs by total employment. When the labor market is tight and competition among firms for workers is high, workers are more likely to quit to take another job that may be offering higher wages. The quit rate in July 2023 had fallen to 2.3 percent of total employment from a high of 3.0 percent, reached in both November 2021 and April 2022. The quit rate was back to its value just before the pandemic. The quit rate data are consistent with easing conditions in the labor market. (The data on job openings and quits are from the BLS report Job Openings and Labor Turnover—July 2023—the JOLTS report—released on August 29. The report can be found here.)

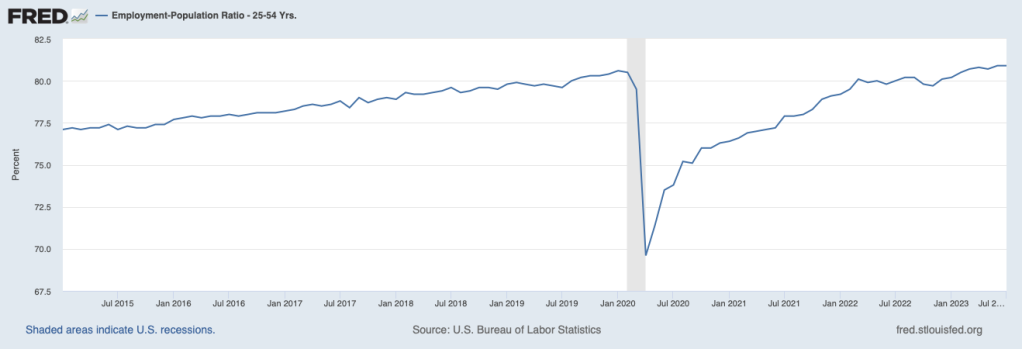

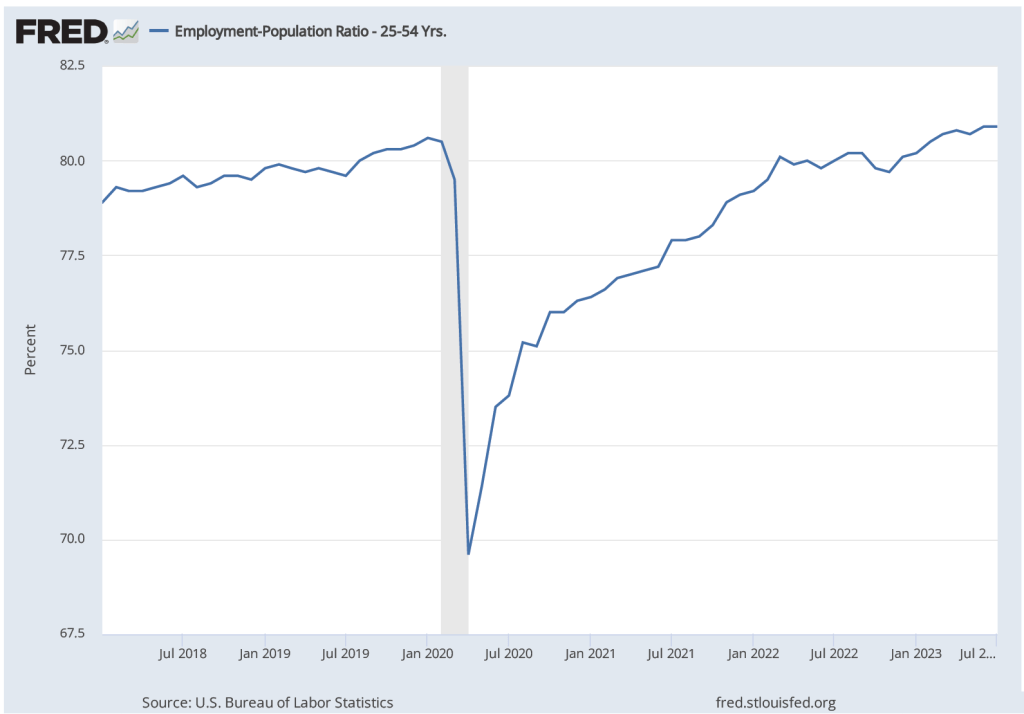

In his Jackson Hole speech, Powell noted that: “Labor supply has improved, driven by stronger participation among workers aged 25 to 54 and by an increase in immigration back toward pre-pandemic levels.” The following figure shows the employment-population ratio for people aged 25 to to 54—so-called prime-age workers. In July 2023, 80.9 percent of people in this age group were employed, actually above the ratio of 80.5 percent just before the pandemic. This increase in labor supply is another indication that the labor market disruptions caused by the pandemic has continued to ease, allowing for an increase in labor supply.

Taken together, these data indicate that labor market conditions are easing, likely reducing upward pressure on wages, and aiding the continuing decline in the inflation rate towards the Fed’s 2 percent target. Unless the data for August show an acceleration in inflation or a tightening of labor market conditions—which is certainly possible given what appears to be a strong expansion of real GDP during the third quarter—at its September meeting the Federal Open Market Committee is likely to keep its target for the federal funds rate unchanged.

The Federal Reserve building in Washington, DC. (Photo from Bloomberg News via the Wall Street Journal.)

The key macroeconomic question of the past two years is whether the Federal Reserve could bring down the high inflation rate without triggering a recession. In this blog post from back in February, we described the three likely macroeconomic outcomes as:

A soft landing—inflation returns to the Fed’s 2 percent target without a recession occurring.

A hard landing—inflation returns to the Fed’s 2 percent target with a recession occurring.

No landing—inflation remains above the Fed’s 2 percent target but no recession occurs.

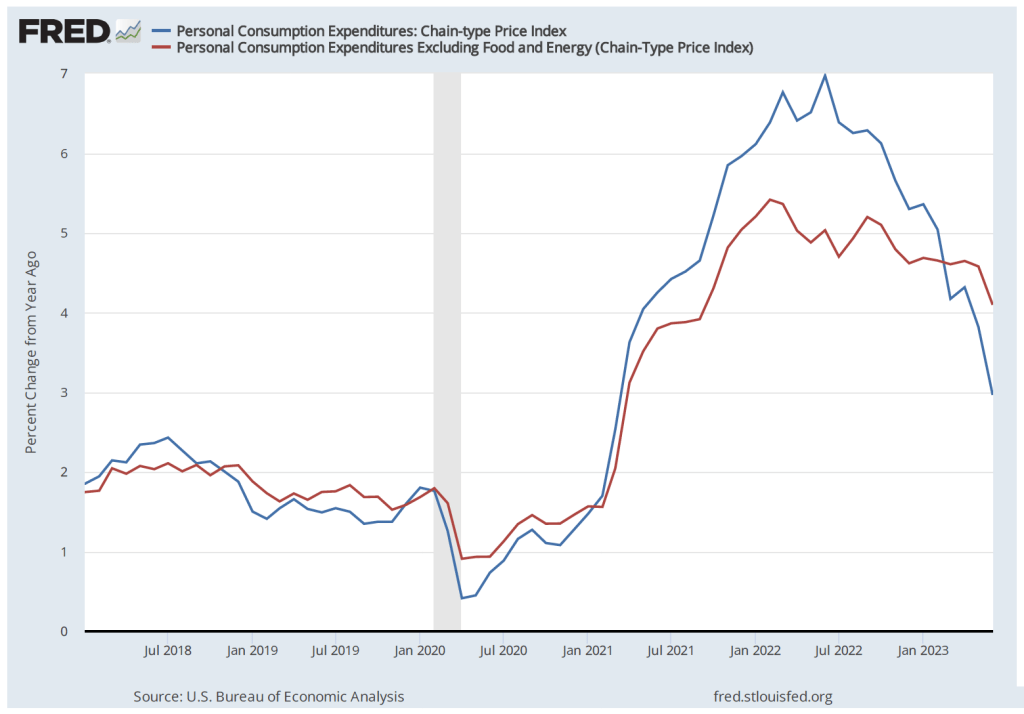

The following figure shows inflation measured as the percentage change in the personal consumption expenditures (PCE) price index and in the core PCE, which excludes food and energy prices. Recall that the Fed uses inflation as measured by the PCE to determine whether it is hitting its inflation target of 2 percent. Because food and energy prices tend to be volatile, many economists inside and outside of the Fed use the core PCE to better judge the underlying rate of inflation—in other words, the inflation rate likely to persist in at least the near future.

The figure shows that inflation first began to rise above the Fed’s target in March 2021. Most members of the Federal Open Market Committee (FOMC) believed that the inflation was caused by temporary disruptions to supply chains caused by the effects of the Covid–19 pandemic. Accordingly, the FOMC didn’t raise its target for the federal funds from 0 to 0.25 percent until March 2022. Since March 2022, the FOMC has raised its target for the federal funds rate in a series of steps until the target range reached 5.25 to 5.50 percent following the FOMC’s July 26, 2023 meeting.

PCE inflation peaked at 7.0 percent in June 2022 and had fallen to 2.9 percent in June 2023. Core PCE had a lower and earlier peak of 5.4 percent in February 2023, but had experienced a smaller decline—to 4.1 percent in June 2023. Inflation as measured by the consumer price index (CPI) followed a similar pattern, as shown in the following figure. Inflation measured by core CPI reached a lower peak than did inflation measured by the CPI and declined by less through June 2023.

As inflation has been falling since mid-2022, , the unemployment rate has remained low and the employment-population ratio for prime-age workers (workers aged 25 to 54) has risen above its 2019 pre-pandemic peak, as the following two figures show.

So, the Fed seems to be well on its way to achieving a soft landing. But in the press conference following the July 26 FOMC meeting Chair Jerome Powell was cautious in summarizing the inflation situation:

“Inflation has moderated somewhat since the middle of last year. Nonetheless, the process of getting inflation back down to 2 percent has a long way to go. Despite elevated inflation, longer-term inflation expectations appear to remain well anchored, as reflected in a broad range of surveys of households, businesses, and forecasters, as well as measures from financial markets.”

By “longer-term expectations appear to remain well anchored,” Powell was referring to the fact that households, firms, and investors appear to be expecting that the inflation rate will decline over the following year to the Fed’s 2 percent target.

Those economists who still believe that there is a good chance of a recession occuring during the next year have tended to focus on the following three points:

1. As shown in the following two figures, the labor market remains tight, with wage increases remaining high—although slowing in recent months—and the ratio of job openings to the number of unemployed workers remaining at historic levels—although that ratio has also been declining in recent months. If the labor market remains very tight, wages may continue to rise at a rate that isn’t consistent with 2 percent inflation. In that case, the FOMC may have to persist in raising its target for the federal funds rate, increasing the chances for a recession.

2. The lagged effect of the Fed’s contractionary monetary policy over the past year—increases in the target for the federal funds rate and quantitative tightening (allowing the Fed’s holdings of Treasury securites and mortgage-backed securities to decline; a process of quantitative tightening (QT))—may have a significant negative effect on the growth of aggegate demand in the coming months. Economists disagree on the extent to which monetary policy has lagged effects on the economy. Some economists believe that lags in policy have been significantly reduced in recent years, while other economists believe the lags are still substantial. The lagged effects of monetary policy, if sufficiently large, may be enough to push the economy into a recession.

3. The economies of key trading partners, including the European Union, the United Kingdom, China, and Japan are either growing more slowly than in the previous year or are in recession. The result could be a decline in net exports, which have been contributing to the growth of aggregate demand since early 2021.

In summary, we can say that in early August 2023, the probability of the Fed bringing off a soft landing has increased compared with the situation in mid-2022 or even at the beginning of 2023. But problems can still arise before the plane is safely on the ground.

(Photo from the Associated Press via the Wall Street Journal.)

During most periods, the “Employment Situation” report that the Bureau of Labor Statistics issues on the first Friday of each month includes the most closely watched macroeconomic data. Since the spring of 2021, high inflation rates have made the BLS’s “Consumer Price Index Summary” at least a close second in interest to the employment report. The data in the CPI report is usually more readily comprehensible than the data in the employment report. So, we think it’s worth class time to go into some of the details of the employment report, as we do in Macroeconomics, Chapter 9, Section 9.1, Economics, Chapter 19, Section 19.1, and Essentials of Economics, Chapter 13, Section 13.1.

When the BLS released the May employment report, the Wall Street Journal noted that: “Employers added 339,000 jobs last month; unemployment rate rose to 3.7%.” Employment increased … but the unemployment rate also rose? How is that possible? One key to understanding media accounts of the report is to note that the report contains data from two separate surveys: 1) the household survey and 2) the employment or establishment survey. As in the statement just quoted from the Wall Street Journal, media accounts often mix data from the two surveys.

The data showing an increase of 339,000 jobs in May are from the payroll survey, while the data showing that the unemployment rate rose are from the household survey. Below we reproduce part of the relevant table from the report showing some of the data from the household survey. Note that total employment in the household survey falls by 310,000, so there appears to be no contradiction to explain—the unemployment rate increased because the number of people employed fell and the number of people unemployed rose. But why, then, did employment rise in the payroll survey?

Employment can rise in one survey and fall in the other because: 1) the types of employment measured in the two series differ, 2) the periods during which the data are collected differ, and 3) because of measurement error. The household survey uses a broader measure of employment that includes several categories of workers who are not included in the payroll survey: agricultural workers, self-employed workers, unpaid workers in family businesses, workers employed in private households rather than in businsses, and workers on unpaid leave from their jobs. In addition, the payroll employment numbers are revised—sometimes substantially—as additional data are collected from firms, while the household employment numbers are subject to much smaller revisions because data in the household survey are collected during a single week. A detailed discussion of the differences between the employment measures in the two series can be found here.

Usefully, the BLS publishes a series labeled “Adjusted employment” that estimates what the value for household employment would be if the household survey was measuring the same categories of employment as the payroll survey. In this case, the adjusted employment series shows an increase in employment in May of 394,000—close to the payroll survey’s increase of 339,000.

To summarize, the May employment report indicates that payroll employment increased, while the non-payroll categories of household employment declined, and the unemployment rate rose. Note also in the table above that the number of people counted as not being in labor force rose slightly and the employment-population ratio fell slightly. Average weekly hours (not shown in the table above) decreased slightly from 34.4 hours per week to 34.3.

A reasonable conclusion from the report is that the labor market remains strong, although it may have weakened slightly. Prior to release of the report, there was much speculation in the business press about how the report might affect the deliberations of the Federal Reserve’s Federal Open Market Committe (FOMC) at its next meeting to be held on June 13th and 14th. The report showed stronger employment growth than economists surveyed by Dow Jones had expected, indicating that the FOMC was likely to remain concerned that a tight labor market might continue to put upward pressure on wages, which firms could pass through to higher prices. Members of the FOMC had been signalling that they were likely to keep their target for the federal funds rate unchanged in June. The reported employment increase was likely not large enough to cause the FOMC to change course.

Photo from the Associated Press of Fed Chair Jerome Powell at a news conference

At its Wednesday, May 3, 2023 meeting, the Federal Open Market Committee (FOMC) raised its target for the federal funds rate by 0.25 percentage point to a range of 5.00 to 5.25. The decision by the committee’s 11 voting members was unanimous. After each meeting, the FOMC releases a statement (the statement for this meeting can be found here) explaining its reasons for its actions at the meeting.

The statement for this meeting had a key change from the statement the committee issued after its last meeting on March 22. The previous statement (found here) included this sentence:

“The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

In the statement for this meeting, the committee rewrote that sentence to read:

“In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

This change indicates that the FOMC has stopped—or at least suspended—use of forward guidance. As we explain in Money, Banking, and the Financial System, Chapter 15, Section 5.2, forward guidance refers to statements by the FOMC about how it will conduct monetary policy in the future.

After the March meeting, the committee was providing investors, firms, and households with the forward guidance that it intended to continue raising its target for the federal funds rate—which is what the reference to “additional policy firming” means. The statement after the May meeting indicated that the committee was no longer giving guidance about future changes in its target for the federal funds rate other than to state that it would depend on the future state of the economy. In other words, the committee was indicating that it might not raise its target for the federal funds rate after its next meeting on June 14. The committee didn’t indicate directly that it was pausing further increases in the federal funds rate but indicated that pausing further increases was a possible outcome.

Following the end of the meeting, Fed Chair Jerome Powell conducted a press conference. Although not yet available when this post was written, a transcript will be posted to the Fed’s website here. Powell made the following points in response to questions:

He was not willing to move beyond the formal statement to indicate that the committee would pause further rate increases.

He believed that the bank runs that had led to the closure and sale of Silicon Valley Bank, Signature Bank, and First Republic Bank were likely to be over. He didn’t believe that other regional banks were likely to experience runs. He indicated that the Fed needed to adjust its regulatory and supervisory actions to help ensure that similar runs didn’t happen in the future.

He repeated that he believed that the Fed could achieve its target inflation rate of 2 percent without the U.S. economy experiencing a recession. In other words, he believed that a soft landing was still possible. He acknowledged that some other members of the committee and the committee’s staff economist disagreed with him and expected a mild recession to occur later this year.

He stated that as banks have attempted to become more liquid following the failure of the three regional banks, they have reduced the volume of loans they are making. This credit contraction has an effect on the economy similar to that of an increase in the federal funds rate in that increases in the target for the federal funds rate are also intended to reduce demand for goods, such as housing and business fixed investment, that depend on borrowing. He noted that both those sectors had been contracting in recent months, slowing the economy and potentially reducing the inflation rate.

He indicated that although inflation had declined somewhat during the past year, it was still well above the Fed’s target. He mentioned that wage increases were still higher than is consistent with an inflation rate of 2 percent. In response to a question, he indicated that if the inflation rate were to fall from current rates above 4 percent to 3 percent, the FOMC would not be satisfied to accept that rate. In other words, the FOMC still had a firm target rate of 2 percent.

In summary, the FOMC finds itself in the same situation it has been in since it began raising its target for the federal funds rate in March 2022: Trying to bring high inflation rates back down to its 2 percent target without causing the U.S. economy to experience a significant recession.

The Federal Reserve’s goal has been to end the current period of high inflation by bringing the economy in for a soft landing—reducing the inflation rate to closer to the Fed’s 2 percent target while avoiding a recession. Although Fed Chair Jerome Powell has said repeatedly during the last year that he expected the Fed would achieve a soft landing, many economists have been much more doubtful.

It’s possible to read recent economic data as indicating that it’s more likely that the economy is approaching a soft landing, but there is clearly still a great deal of uncertainty. On April 12, the Bureau of Labor Statistics released the latest CPI data. The figure below shows the inflation rate as measured by the CPI (blue line) and by core CPI—which excludes the prices of food and fuel (red line). In both cases the inflation rate is the percentage change from the same month in the previous year.

The inflation rate as measured by the CPI has been trending down since it hit a peak of 8.9 percent in June 2022. The inflation rate as measured by core CPI has been trending down more gradually since it reached a peak of 6.6 percent in September 2022. In March, it was up slightly to 5.6 percent from 5.5 percent in February.

As the following figure shows, payroll employment while still increasing, has been increasing more slowly during the past three months—bearing in mind that the payroll employment data are often subject to substantial revisions. The slowing growth in payroll employment is what we would expect with a slowing economy. The goal of the Fed in slowing the economy is, of course, to bring down the inflation rate. That payroll employment is still growing indicates that the economy is likely not yet in a recession.

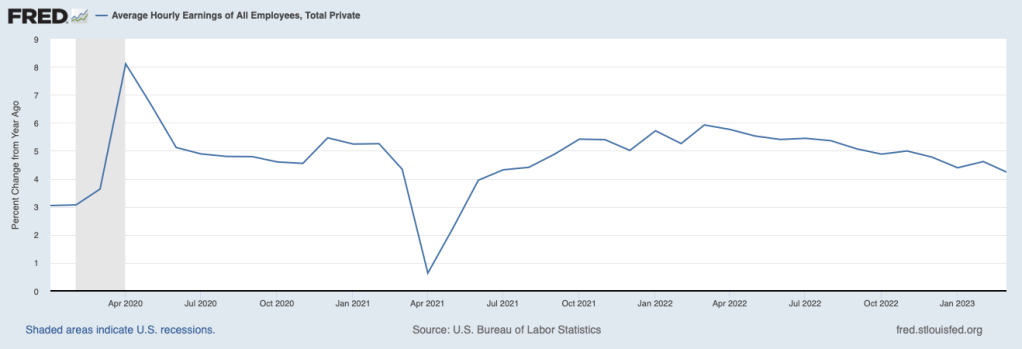

The slowing in employment growth has been matched by slowing wage growth, as measured by the percentage change in average hourly earnings. As the following figure shows, the rate of increase in average hourly earnings has declined from 5.9 percent in March 2022 to 4.2 percent in March 2023. This decline indicates that businesses are experiencing somewhat lower increases in their labor costs, which may pass through to lower increases in prices.

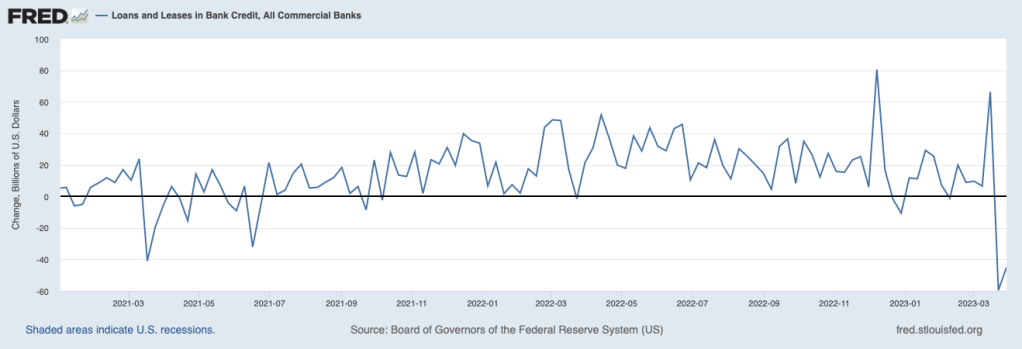

Credit conditions also indicate a slowing economy As the following figure shows, bank lending to businesses and consumers has declined sharply, partly because banks have experienced an outflow of deposits following the failure of Silicon Valley and Signature Banks and partly because some banks have raised their requirements for households and firms to qualify for loans in anticipation of the economy slowing. In a slowing economy, households and firms are more likely to default on loans. To the extent that consumers and businesses also anticipate the possibility of a recession, they may have reduced their demand for loans.

But such a sharp decline in bank lending may also be an indication that the economy is not just slowing, on its way to a making a soft landing, but is on the verge of a recession. The minutes of the March meeting of the Federal Open Market Committee (FOMC) included the information that the FOMC’s staff economists forceast “at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.” (The minutes can be found here.) The increased chance of a recession was attributed largely to “banking and financial conditions.”

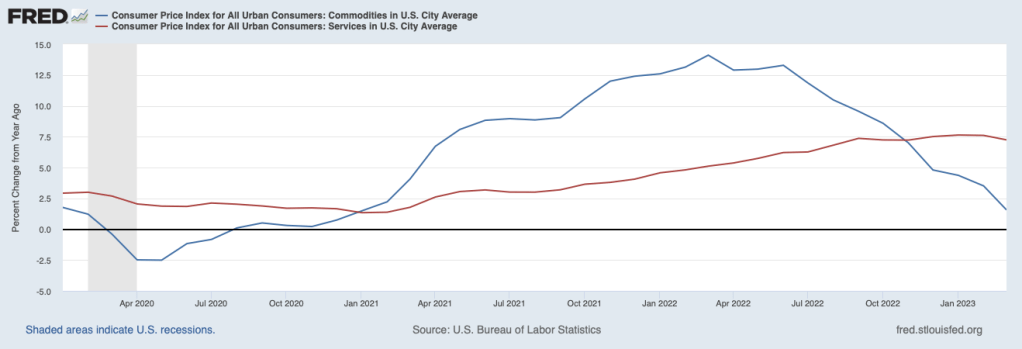

At its next meeting in May, the FOMC will have to decide whether to once more increase its target range for the federal funds rate. The target range is currently 4.75 percent to 5.00 percent. The FOMC will have to decide whether inflation is on a course to fall back to the Fed’s 2 percent target or whether the FOMC needs to further slow the economy by increasing its target range for the federal funds rate. One factor likely to be considered by the FOMC is, as the following figure shows, the sharp difference between the inflation rate in prices of goods (blue line) and the inflation rate in prices of services (red line).

During the period from January 2021 to November 2022, inflation in goods was higher—often much higher—than inflation in services. The high rates of inflation in goods were partly the result of disruptions to supply chains resulting from the Covid-19 pandemic and partly due to a surge in demand for goods as a result of very expansionary fiscal and monetary policies. Since November 2022, inflation in the prices of services has remained high, while inflation in the prices of goods has continued to decline. In March, goods inflation was only 1.6 percent, while services inflation was 7.2 percent. In his press conference following the last FOMC meeting, Fed Chair Jerome Powell stated that as long as services inflation remains high “it would be very premature to declare victory [over inflation] or to think that we’ve really got this.” (The transcript of Powell’s news conference can be found here.) This statement coupled with the latest data on service inflation would seem to indicate that Powell will be in favor of another 0.25 percentage point increase in the federal funds rate target range.

The Fed’s inflation target is stated in terms of the personal consumption expenditure (PCE) price index, not the CPI. The Bureau of Economic Analysis will release the March PCE on April 28, before the next FOMC meeting. If the Fed is as closely divided as it appears to be over whether additional increases in the federal funds rate target range are necessary, the latest PCE data may prove to have a significan effect on their decision.

So—as usual!—the macroeconomic picture is murky. The economy appears to be slowing and inflation seems to be declining but it’s still difficult to determine whether the Fed will be able to bring inflation back to its 2 percent target without causing a recession.