Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

Members of the Fed’s policymaking Federal Open Market Committee (FOMC) had signaled clearly before today’s (June 18) meeting that the committee would leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. In the statement released after its meeting, the committee noted that a key reason for keeping its target range unchanged was that: “Uncertainty about the economic outlook has diminished but remains elevated.” Committee members were unanimous in voting to keep its target range unchanged.

In his press conference following the meeting, Fed Chair Jerome Powell indicated that a key source of economic uncertainty was the effect of tariffs on the inflation rate. Powell indicated that the likeliest outcome was that tariffs would lead to the inflation rate temporarily increasing. He noted that: “Beyond the next year or so, however, most measures of longer-term expectations [of inflation] remain consistent with our 2 percent inflation goal.”

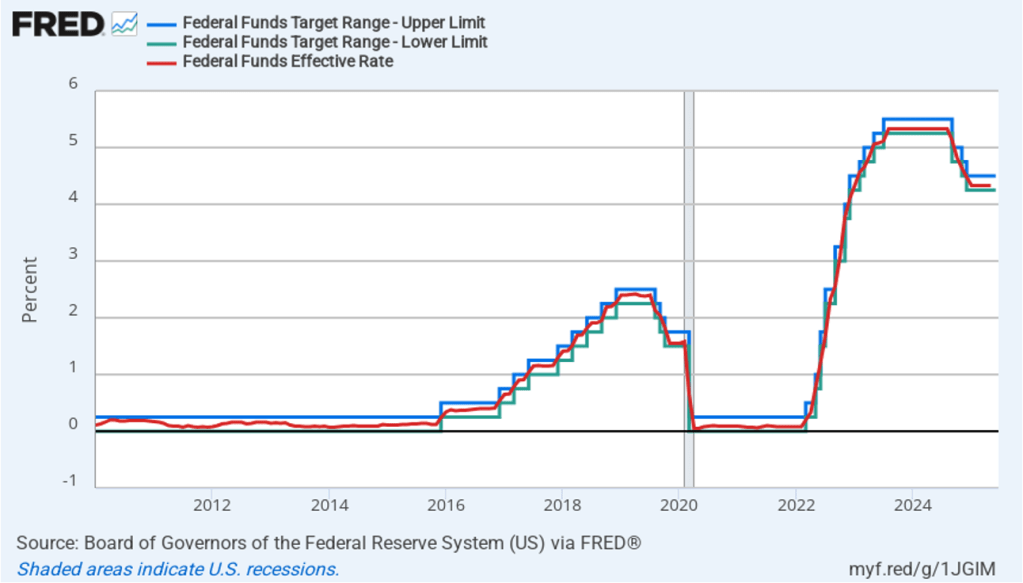

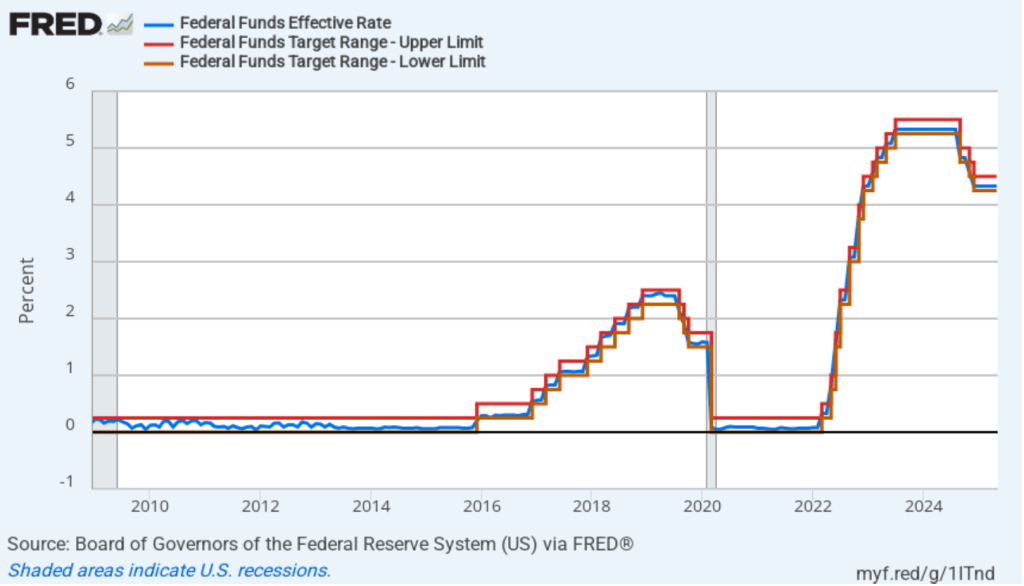

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

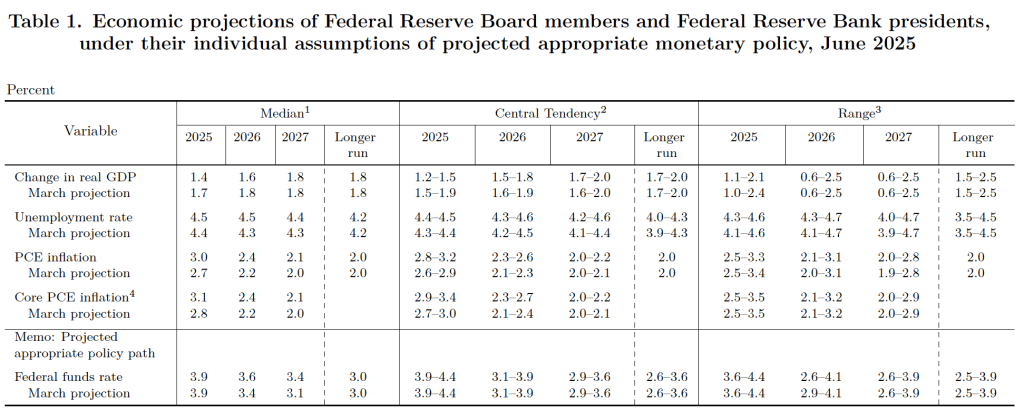

After the meeting, the committee also released a “Summary of Economic Projections” (SEP)—as it typically does after its March, June, September, and December meetings. The SEP presents median values of the 18 committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release.

There are several aspects of these forecasts worth noting:

Committee members reduced their forecast of real GDP growth for 2025 from 1.7 percent in March to 1.4 percent today. (It had been 2.1 percent in their December forecast.) Committee members also slightly increased their forecast of the unemployment rate at the end of 2025 from 4.4 percent to 4.5 percent. (The unemployment rate in May was 4.2 percent.)

Committee members now forecast that personal consumption expenditures (PCE) price inflation will be 3.0 percent at the end of 2025. In March they had forecast that it would be 2.7 percent at the end of 2025, and in December, they had forecast that it would 2.5 percent. Similarly, their forecast of core PCE inflation increased from 2.8 percent to 3.1 percent. It had been 2.5 percent in December. The committee does not expect that PCE inflation will decline to the Fed’s 2 percent annual target until sometime after 2027.

The committee’s forecast of the federal funds rate at the end of 2025 was unchanged at 3.9 percent. The federal funds rate today is 4.33 percent, which indicates that the median forecast of committee members is for two 0.25 percentage point (25 basis points) cuts in their target for the federal funds rate this year. Investors are similarly forecasting two 25 basis point cuts.

During his press conference, Powell indicated that because the tariff increases the Trump administration implemented beginning in April were larger than any in recent times, their effects on the economy are difficult to gauge. He noted that: “There’s the manufacturer, the exporter, the importer and the retailer and the consumer. And each one of those is going to be trying not to be the one to pay for the tariff, but together they will all pay together, or maybe one party will pay it all.” The more of the tariff that is passed on to consumers, the higher the inflation rate will be.

Earlier today, President Trump reiterated his view that the FOMC should be cutting its target for the federal funds rate, labeling Powell as “stupid” for not doing so. Trump has indicated that the Fed should cut its target rate by 1 percentage point to 2.5 percentage points in order to reduce the U.S. Treasury’s borrowing costs. During World War II and the beginning of the Korean War, the Fed pegged the interest rates on Treasury securities at low levels: 0.375 percent on Treasury bills and 2.5 percent on Treasury bonds. Following the Treasury-Federal Reserve Accord, reached in March 1951, the Federal Reserve was freed from the obligation to fix the interest rates on Treasury securities. (We discuss the Accord in Chapter 13 of Money, Banking, and the Financial System.) Since that time, the Fed has focused on its dual mandate of maximum employment and price stability and it has not been directly concerned with affecting the Treasury’s borrowing cost.

Barring a sharp slowdown in the growth of real GDP, a significant rise in the unemployment rate, or a significant rise in the inflation rate, the FOMC seems unlikely to change its target for the federal funds rate before its meeting on September 16–17 at the earliest.

Image generated by ChatGTP-4o of someone shopping for clothes.

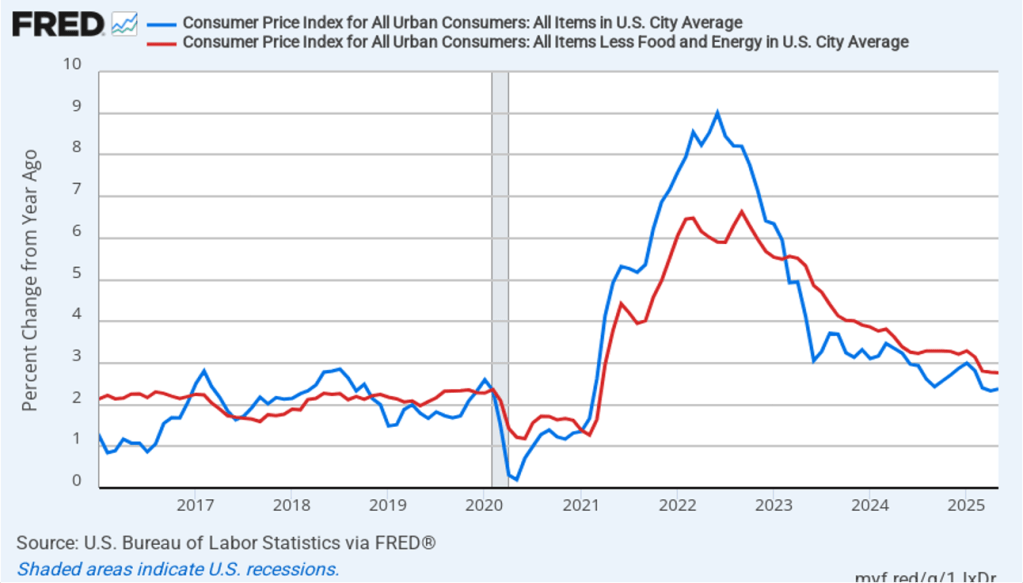

Today (June 11), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for May. The following figure compares headline CPI inflation (the blue line) and core CPI inflation (the green line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.4 percent in May—up slightly from 2.3 percent in April.

The core inflation rate,which excludes the prices of food and energy, was 2.9 percent in May—up slightly from 2.8 percent in April.

Headline inflation was slightly lower and core inflation was the same as what economists surveyed had expected.

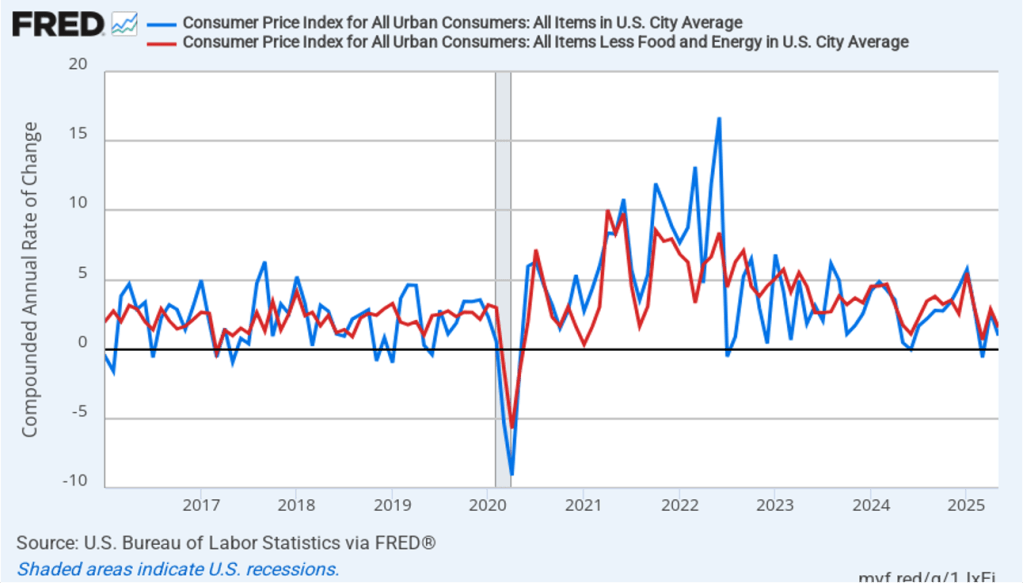

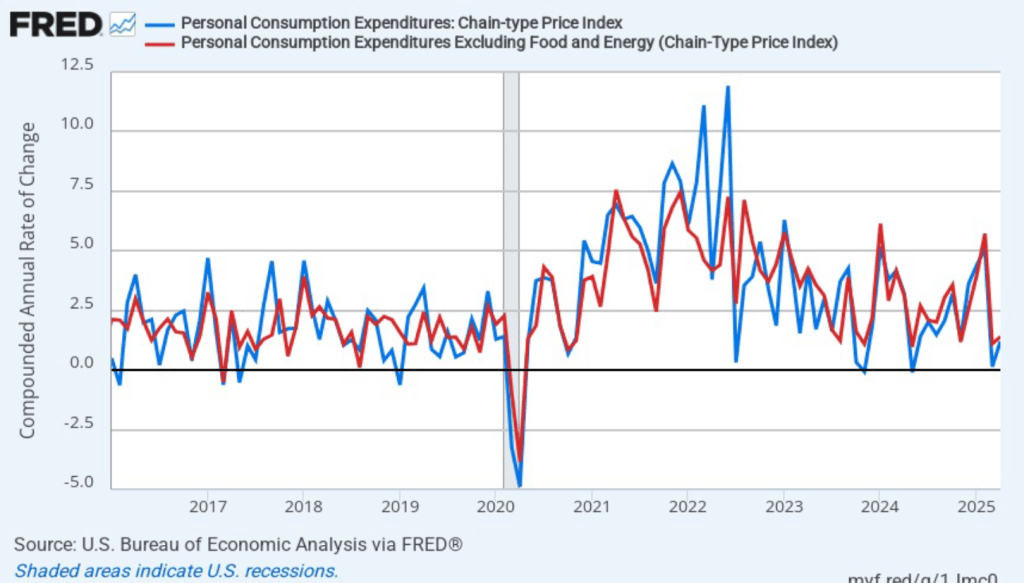

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) decreased from 2.7 percent in April to 1.0 percent in May. Core inflation (the red line) decreased from 2.9 percent in April to 1.6 percent in May.

The 1-month and 12-month inflation rates are telling different stories, with 12-month inflation indicating that the rate of price increase is running slightly above the Fed’s 2 percent inflation target. The 1-month inflation rate indicates a significant slowing of inflation during May.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that the 1-month inflation rate is particularly volatile. Also note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

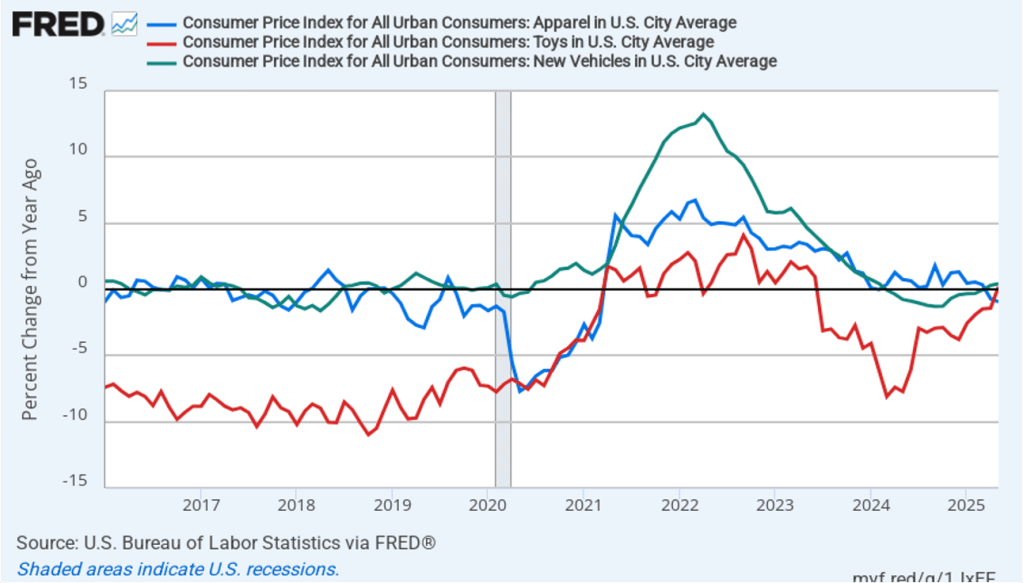

One of the key questions facing Federal Reserve policymakers is to what extent inflation will be affected by the increase in tariffs that the Trump administration announced on April 2. The following figure shows 12-month inflation in three categories of products whose prices are thought to be particularly vulnerable to the effects of tariffs: apparel (the blue line), toys (the red line), and motor vehicles (the green line). In May, prices of apparel fell, while the prices of toys and motor vehicles rose by less than 0.5 percent.

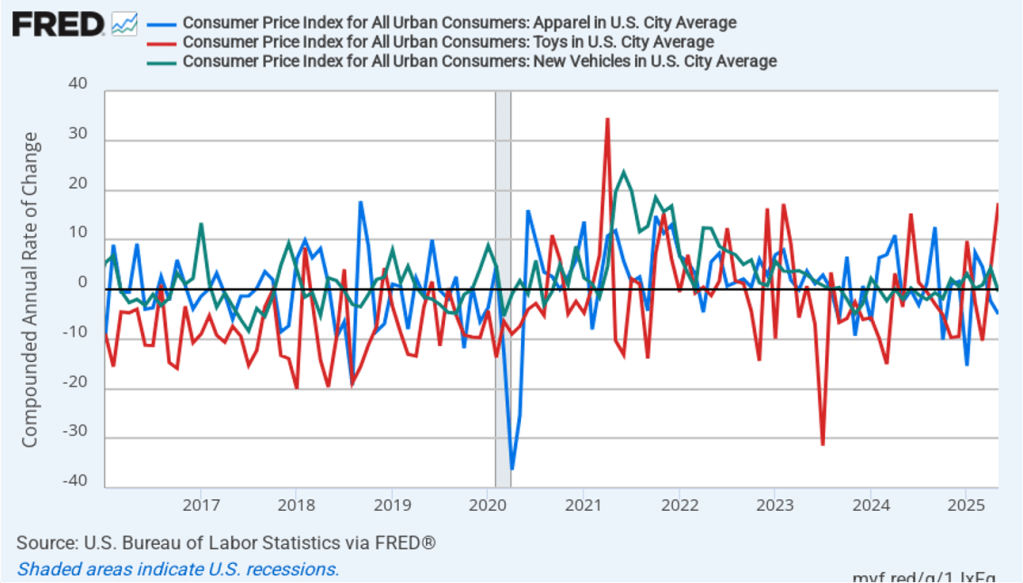

The following figure shows 1-month inflation in these categories. In May, the prices of apparel and motor vehicles fell, while the price of toys soared by 17.4 percent, but that followed a decline of 10.3 percent in April.

Taken together this month’s CPI data don’t show much effect of tariffs on inflation. It’s possible that some of the effects of the tariffs have been cushioned by firms increasing their inventories earlier in the year in anticipation of price increases resulting from the tariffs. If so, as firms draw down their inventories, we may see tariff-related increases in the prices of some goods later in the year.

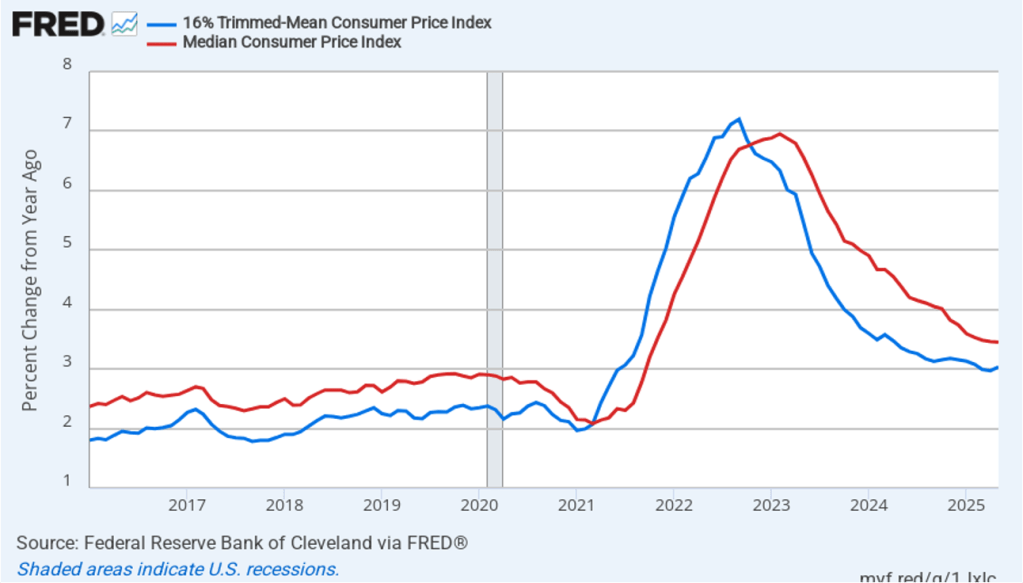

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.0 percent in May, unchanged from April. Twelve-month median inflation (the red line) 3.5 percent in May, also unchanged from April.

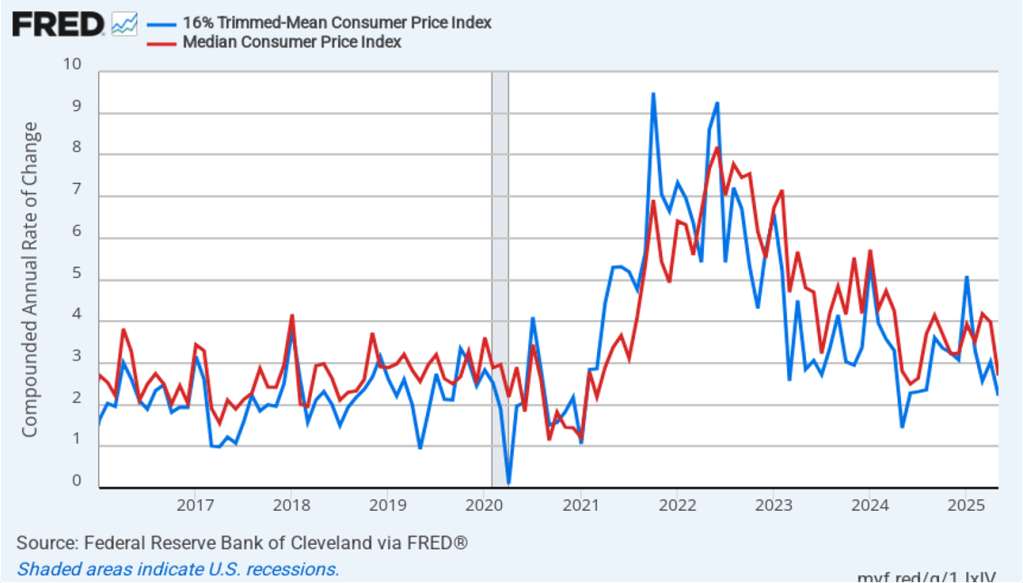

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation decreased from 3.0 percent in April to 2.2. percent in May. One-month median inflation declined from 4.0 percent in April to 2.7 percent in May. These data provide some confirmation that inflation likely fell somewhat from April to May.

What are the implications of this CPI report for the actions the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) may take at its next several meetings? Investors who buy and sell federal funds futures contracts still do not expect that the FOMC will cut its target for the federal funds rate at its next two meetings. (We discuss the futures market for federal funds in this blog post.) Investors assign the highest probability to the FOMC making two 0.25 percentage point (25 basis points) cuts in its target rate by the end of the year. Those cuts would reduce the target range from the current 4.25 percent to 4.50 percent range to a range of 3.75 to 4.00 percent. The FOMC’s actions will likely depend in part on what the tariff increases will end up being following the conclusion of the current trade negotiations and what the effect on inflation from the tariff increases will be.

This morning (June 6), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for May. The data in the report show that the labor market continues to be strong. There have been many stories in the media about businesspeople becoming pessimistic as a result of the large tariff increases the Trump Administration announced on April 2—some of which have since been reduced—but we don’t see the effects in the employment data. Some firms may be maintaining employment until they receive greater clarity about where tariff rates will end up. Similarly, although there are some indications that consumer spending may be slowing, to this point, the effects are not evident in the labor market.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

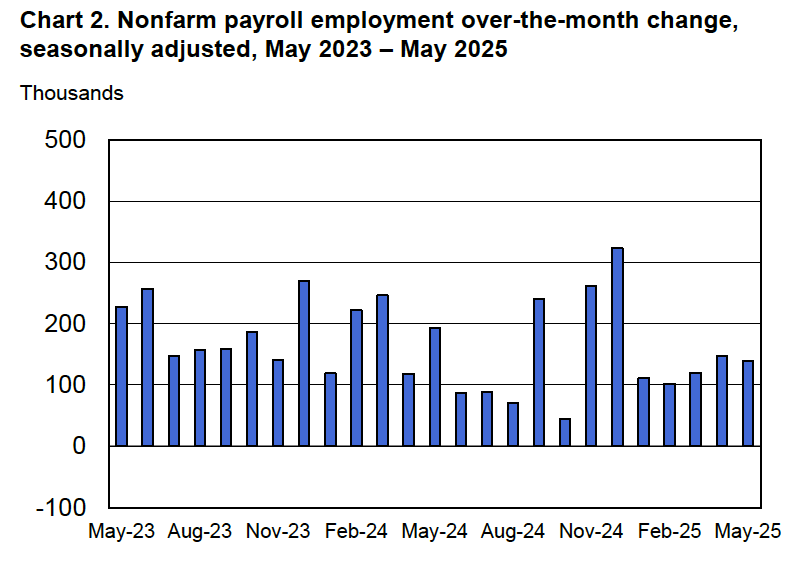

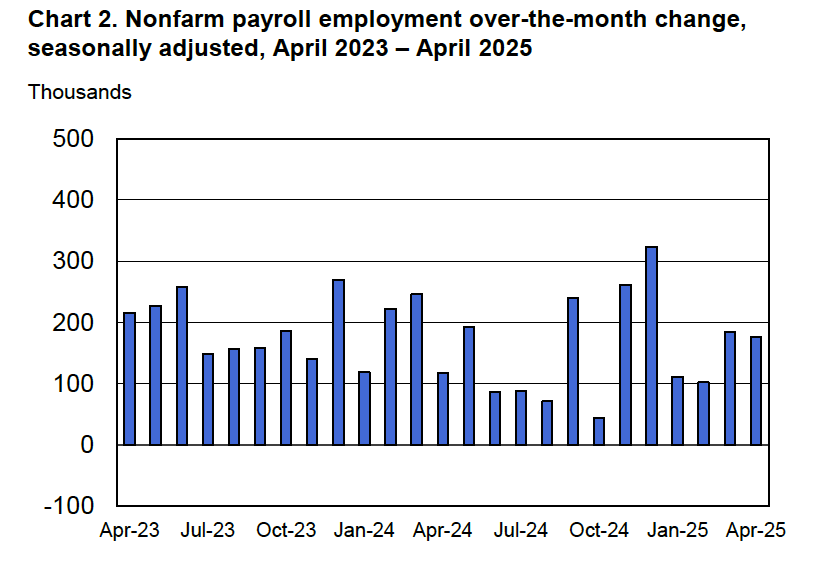

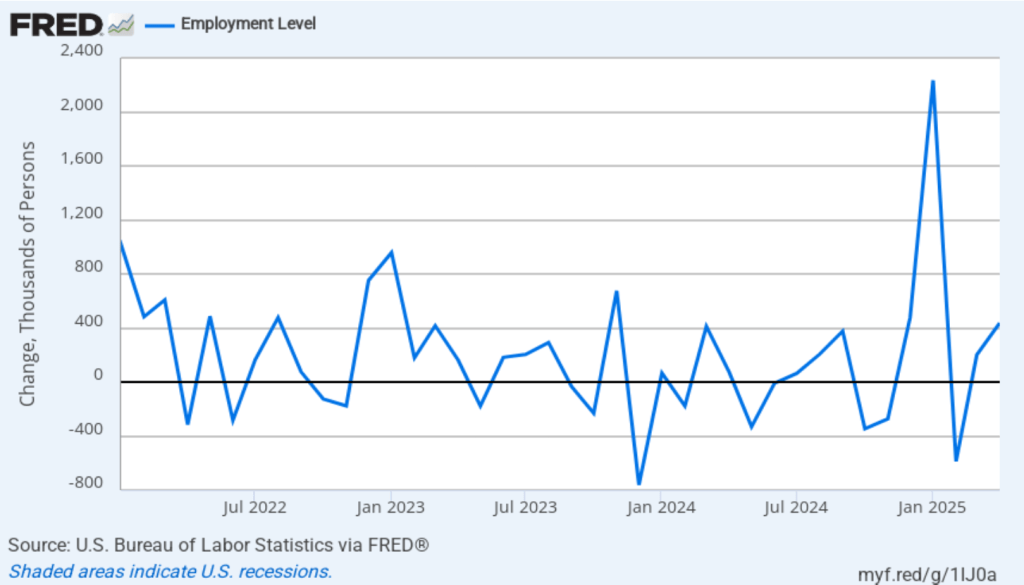

According to the establishment survey, there was a net increase of 139,000 nonfarm jobs during May. This increase was above the increase of 125,000 that economists surveyed had forecast. Somewhat offsetting this increase, the BLS revised downward its previous estimates of employment in March and April by a combined 95,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years.

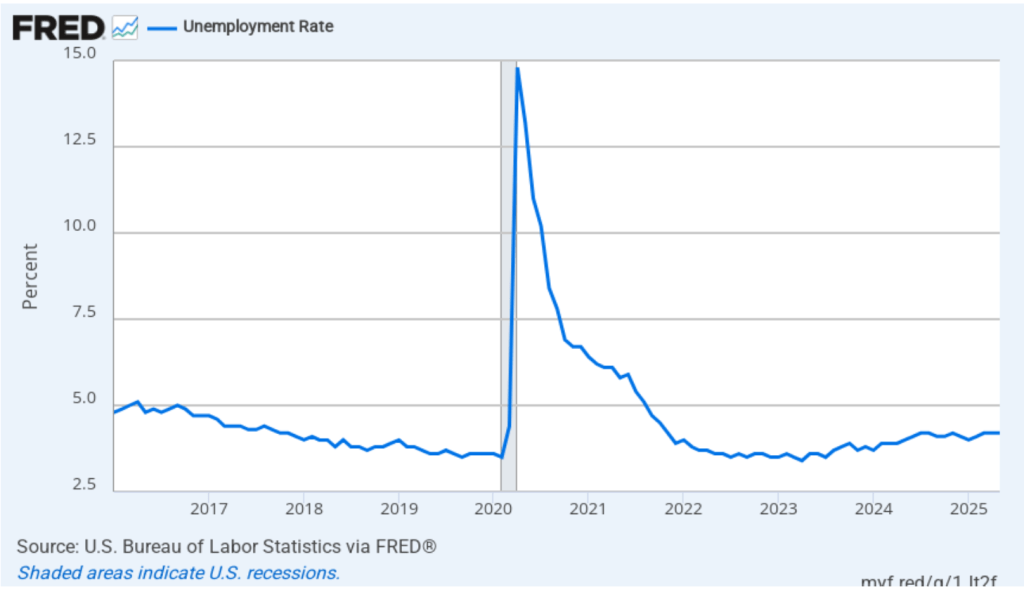

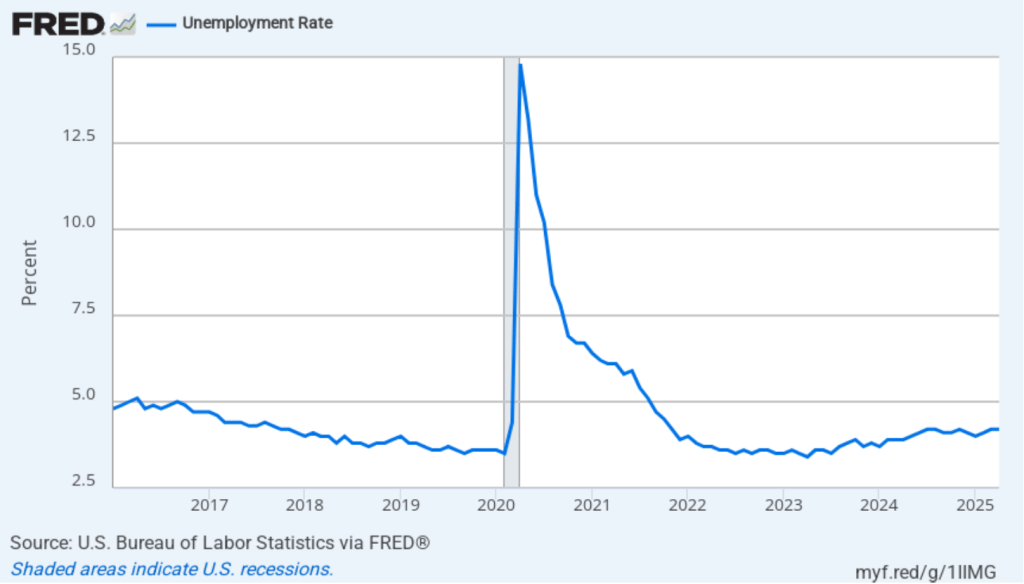

The unemployment rate was unchanged to 4.2 percent in May. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

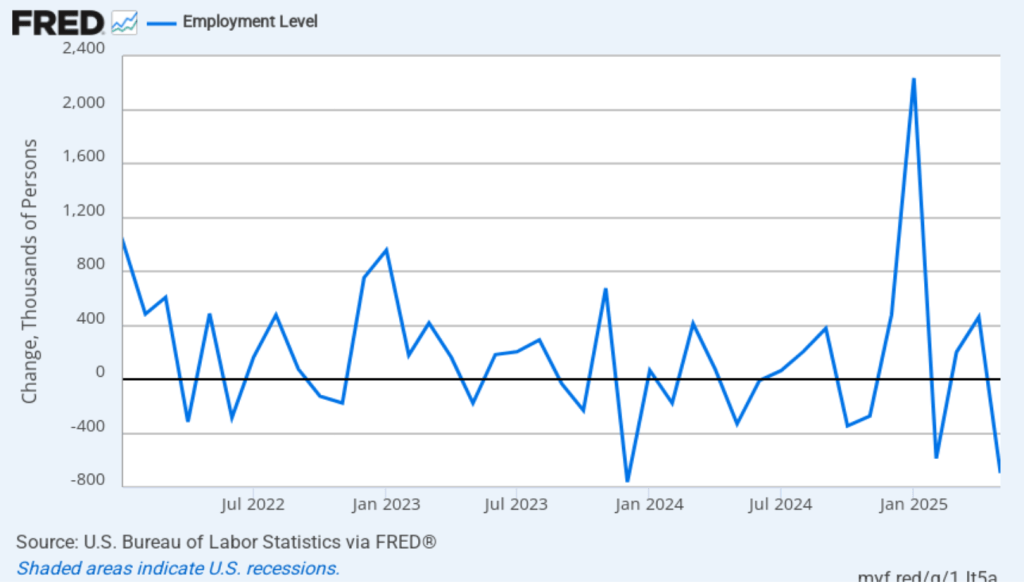

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net decrease of 696,000 jobs in May, following an increase of 461,000 jobs in April. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, the discrepancy between the two surveys in their estimates of the change in net jobs was particularly large. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

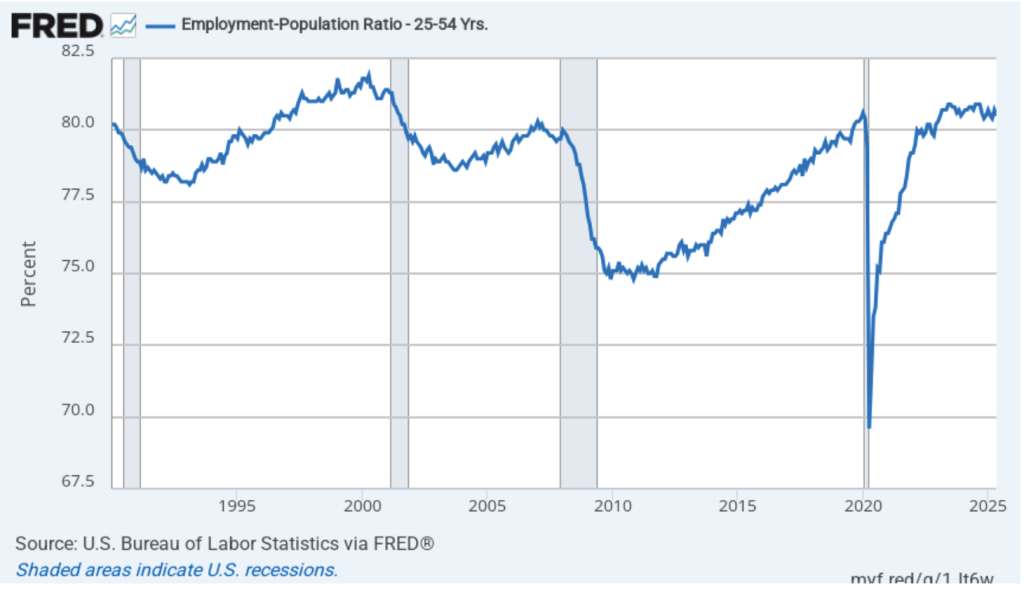

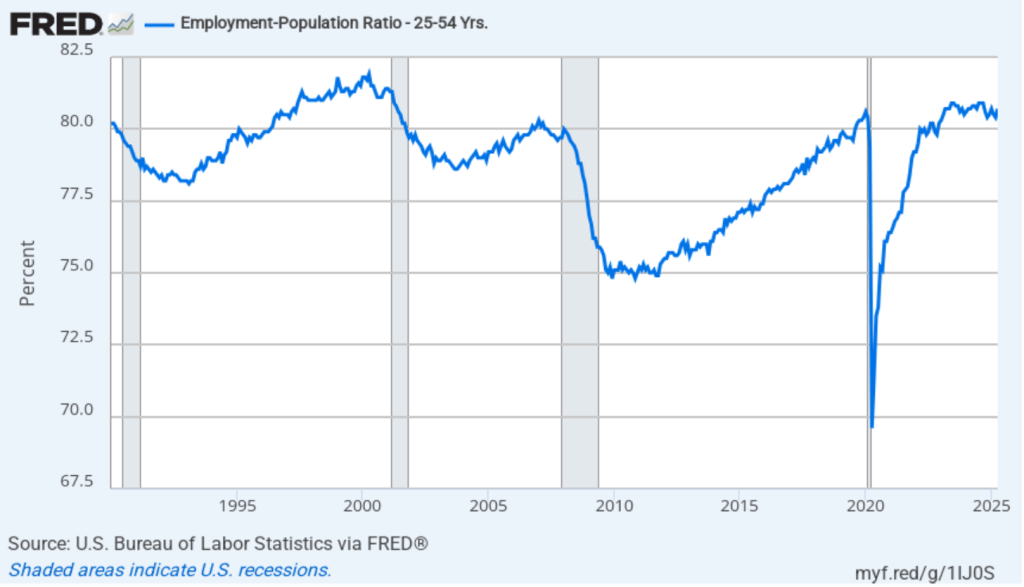

The household survey has another important labor market indicator. The employment-population ratio for prime age workers—those aged 25 to 54—declined from 80.7 percent in April to 80.5 percent in May. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to December 2019.

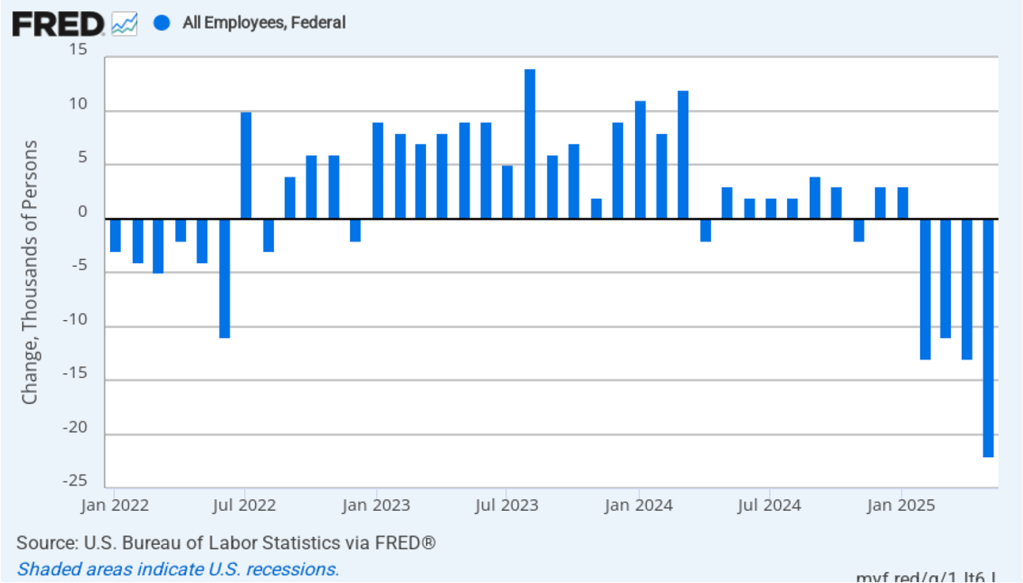

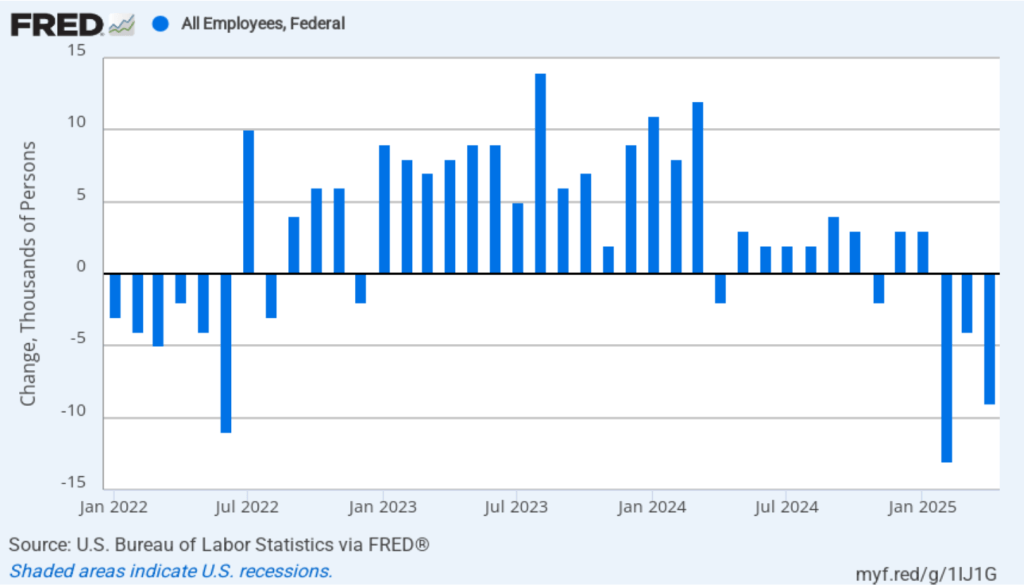

It remains unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 22,000 in May and a total decline of 59,000 beginning in February. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

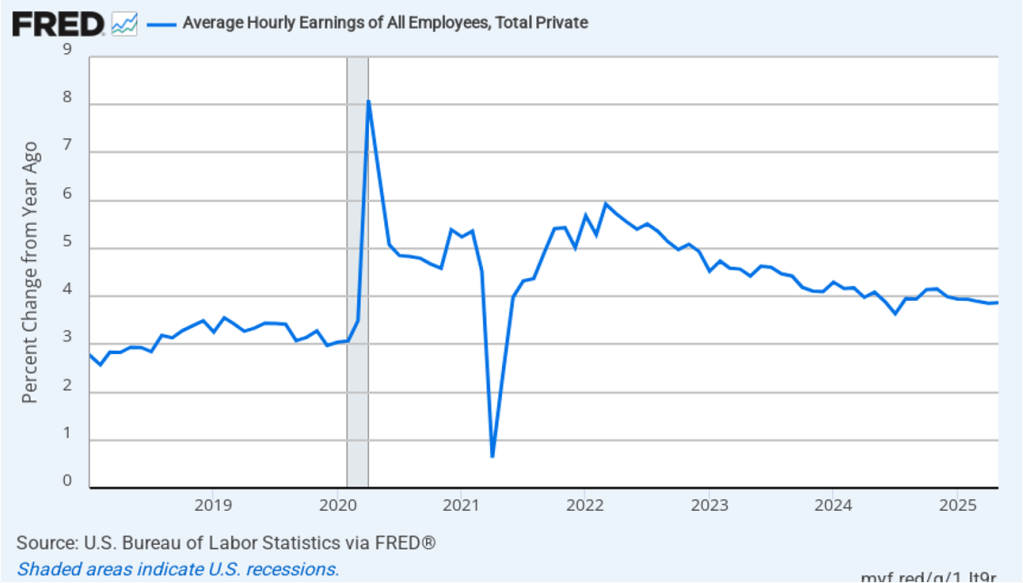

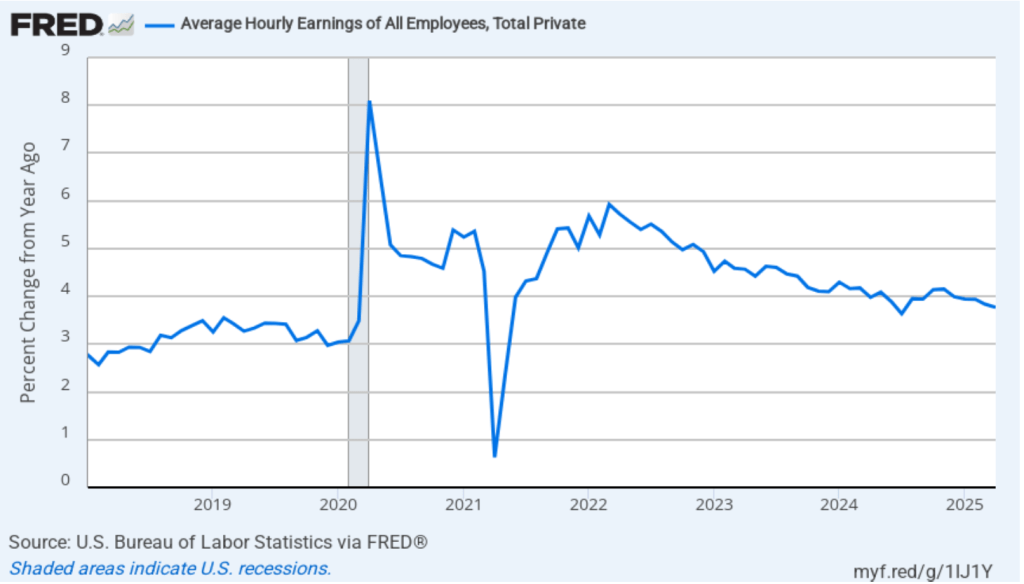

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.9 percent in May. Movements in AHE have been remarkably stable, showing increases of 3.9 percent each month since January.

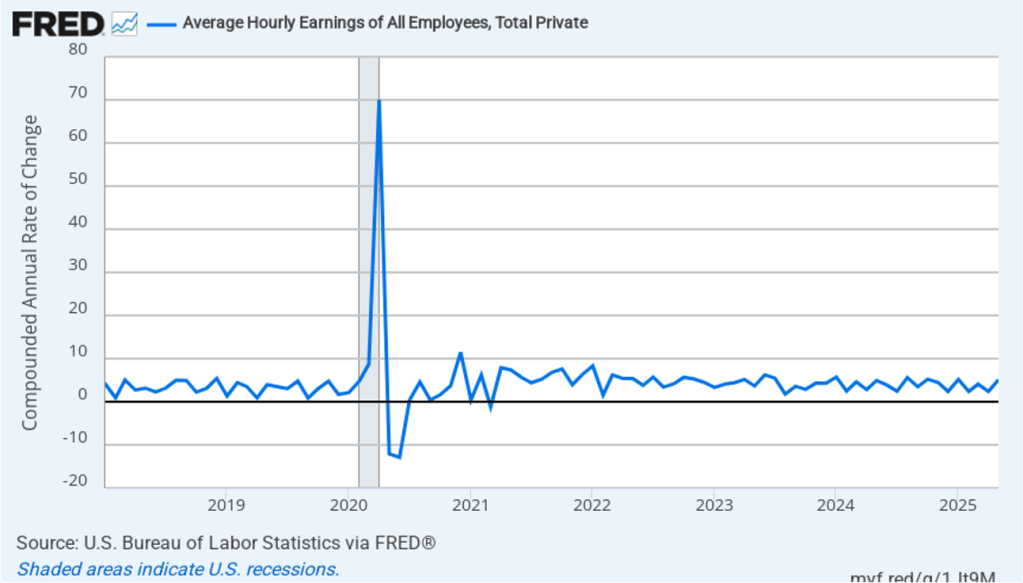

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In May, the 1-month rate of wage inflation was 5.1 percent, up sharply from 2.4 percent in April. If the 1-month increase in AHE is sustained, it would indicate that the Fed will struggle to achieve its 2 percent target rate of price inflation. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

Today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. Looming over monetary policy, however, is the expected effect of the Trump Administration’s tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

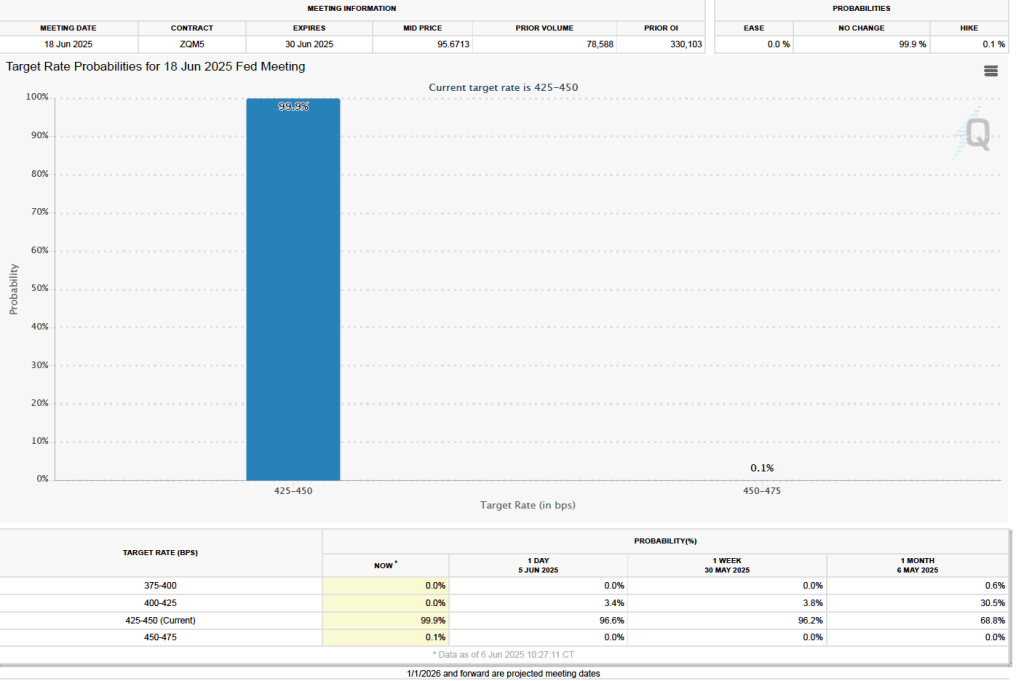

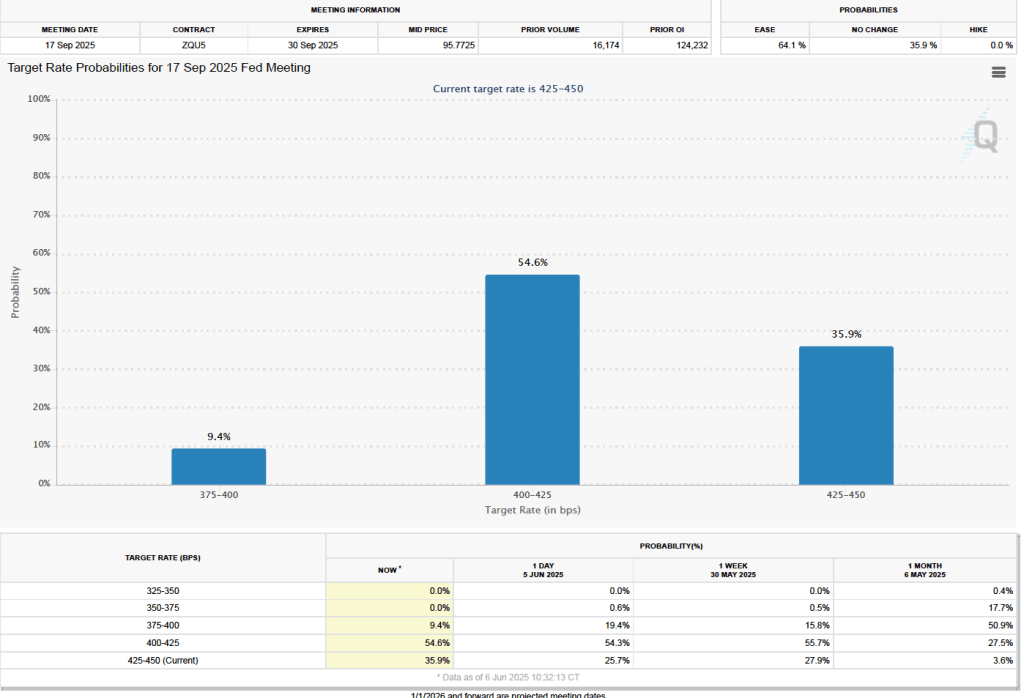

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its June 17–18 meeting. As shown in the following figure, investors assign a 99.9 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

As the following figure shows, investors don’t expect the FOMC to cut its federal funds rate target until the committee’s September 16-17 meeting. Investors assign a probability of 54.6 percent that at that meeting the committee will cut its target range by 0.25 percentage point (25 basis points) to 4.00 percent to 4.25 percent. And a probability of 9.4 percent that the committee will cut its target rate by 50 baisis points to 3.75 percent to 4.00 percent. At 35.9 percent, investors assign a fairly high probability to the committee keeping its target range constant at that meeting.

Photo of the Federal Reserve Bank of Dallas from federalreservehistory.org.

The unusual structure of the Federal Reserve System reflects the political situation at the time that Congress passed the Federal Reserve Act in 1913. As we discuss in Money, Banking, and the Financial System, Chapter 13, at that time, many members of Congress believed that a unified central bank based in Washington, DC would concentrate too much economic power in the hands of the officials running the bank. So, the act divided economic power within the Federal Reserve System in three ways: among bankers and business interests, among states and regions, and between the federal government and the private sector.

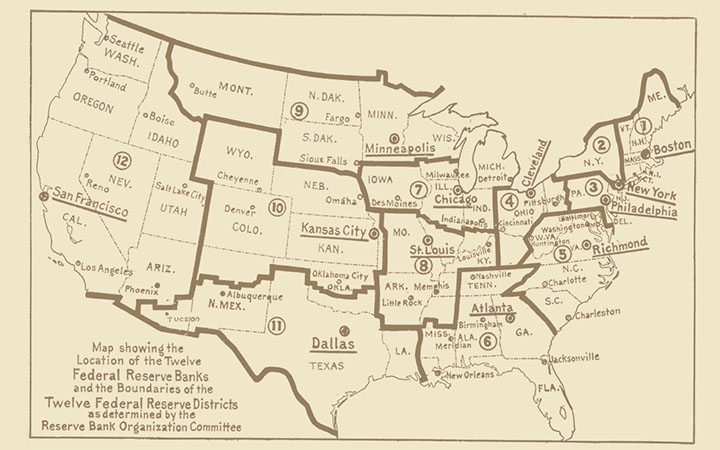

As part of its plan to divide authority within the Federal Reserve System, Congress decided not to establish a single central bank with branches, which had been the structure of both the First and Second Banks of the United States—which were the two attempts by Congress during the period from 1791 to 1836 to establish a central bank. Instead, the Federal Reserve Act divided the United States into 12 Federal Reserve districts, each of which has a Federal Reserve Bank in one city (and, in most cases, additional branches in other cities in the district). The following figure is the original map drawn by the Federal Reserve Organizing Committee in 1913 showing the 12 Federal Reserve Districts. Congress adopted the map with a few changes, following which the areas of the 12 districts have remained largely unchanged down to the present.

The map is from federalreservehistory.org.

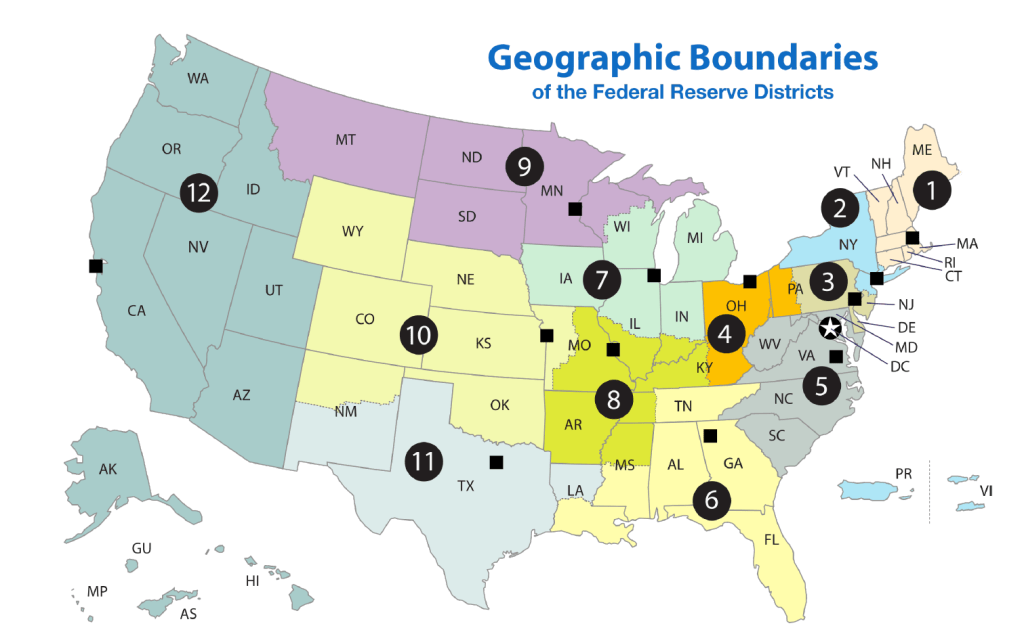

The following map shows the current boundaries of the Federal Reserve Districts.

The map is reproduced from the working paper discussed below.

All national banks—commercial banks with charters from the federal government—were required to join the Federal Reserve System. State banks—commercial banks with charters from state governments—were given the option to join. Congress intended that the primary function of each of the Federal Reserve Banks would be to make discount loans to member banks in its region. These loans were to provide liquidity to banks, thereby fulfilling in a decentralized way the system’s role as a lender of last resort.

When banks join the Federal Reserve System, they are required to buy stock in their Federal Reserve Bank, which pays member banks a dividend on this stock. So, in principle, the private commercial banks in each district that are members of the Federal Reserve System own the District Bank. In fact, each Federal Reserve Bank is a private–government joint venture because the member banks enjoy few of the rights and privileges that shareholders ordinarily exercise. For example, member banks do not have a legal claim on the profits of the District Banks, as shareholders of private corporations do.

On paper, the Federal Reserve System is a decentralized organization with a public-private structure. In practice, power within the system is concentrated in the seven member Board of Governors in Washington, DC. Control over the most important aspect of monetary policy—setting the target for the federal funds rate—is vested in the Federal Open Market Committee (FOMC). The voting membership of the FOMC consists of the seven member of the Board of Governors, the president of the Federal Reserve Bank of New York and four other district bank presidents on a rotating basis (although all 12 district presidents participate in committee discussions). The district bank presidents are elected by the boards of directors of the district banks, but the Board of Governors has final say on who is chosen as a district bank president.

Given these considerations, does the structure of the Fed matter or is it an unimportant historical curiosity? There are reasons to think the Fed’s structure does still matter. First, as we discuss in this blog post, in a recent decision, the U.S. Supreme Court implied—but didn’t state explicitly—that, because of the Fed’s structure, U.S. presidents will likely not be allowed to remove Fed chairs except for cause. That is, if presidents disagree with monetary policy actions, they will not be able to remove Fed chairs on that basis.

Second, as Michael Bordo of Rutgers University and the late Nobel Laureate Edward Prescott argue, the decentralized structure of the Fed has helped increase the variety of policy views that are discussed within the system:

“What is unique about the Federal Reserve, at least compared with other entities created by the federal government, is that the Reserve Banks’ semi-independent corporate structure allows for ideas to be communicated to the System . . . . Moreover, it also allows for new and sometimes dissenting views to develop and gestate within the System without being viewed as an expression of disloyalty that undermines the organization as a whole, as would be more likely within a government bureau.”

Finally, recent research by Anton Bobrov of the University of Michigan, Rupal Kamdar of Indiana University, and Mauricio Ulate of the Federal Reserve Bank of San Francisco indicates that the FOMC votes of the district bank presidents reflect economic conditions in those districts. This result indicates that the district bank presidents arrive at independent judgements about monetary policy rather than just reflecting the views of the Board of Governors, which has to approve the appointment of the presidents. The authors analyze the 896 dissenting votes district bank presidents (other than the president of the NY Fed) cast during the period from 1990 to 2017. A dissenting vote is one in which the district bank president voted to either increase or decrease the target for the federal funds relative to the target the majority of the committee favored.

The authors’ key finding is that the FOMC votes of district bank presidents are influenced by the level of unemployment in the district: “a 1 percentage point higher District unemployment rate increases the likelihood that the respective District president will dissent in favor of looser policy [that is, a lower federal funds rate target than the majority of the committee preferred] at the FOMC by around 9 percentage points.” The authors note that: “The influence of local economic conditions on dissents by District presidents reflects the regional structure of the Federal Reserve System, which was designed to accommodate diverse views across the nation.” (The full text of the paper can be found here. A summary of the paper’s findings by Ulate and Caroline Paulson and Aditi Poduri of the San Francisco Fed can be found here.)

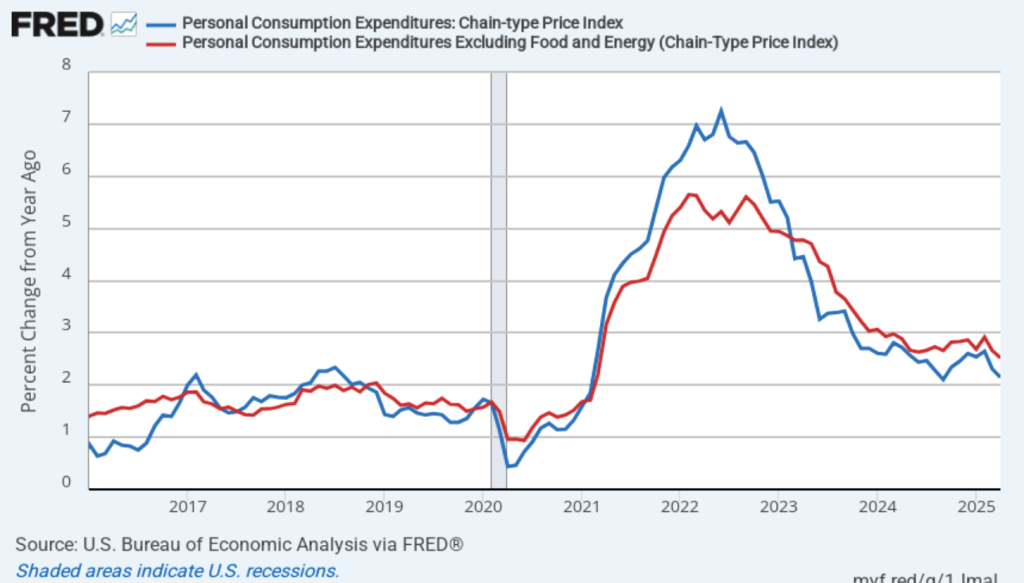

Today (May 30), the BEA released monthly data on the personal consumption expenditures (PCE) price index as part of its “Personal Income and Outlays” report. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2016, with inflation measured as the percentage change in the PCE from the same month in the previous year. In April, PCE inflation was 2.1 percent, down from 2.3 percent in March. Core PCE inflation in April was 2.5 percent, down from 2.7 percent in March. Headline PCE inflation was below the forecast of economists surveyed, while core PCE inflation was consistent with the forecast.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation increased in April to 1.2 percent from 0.1 percent in March. Core PCE inflation also increased from 1.1 percent in March to 1.4 percent in April. So, both 1-month PCE inflation estimates are well below the Fed’s 2 percent target. The usual caution applies that 1-month inflation figures are volatile (as can be seen in the figure), so we shouldn’t attempt to draw wider conclusions from one month’s data. In addition, because these data are for April, they don’t capture fully the price increases resulting from the tariff increases the Trump administration announced on April 2.

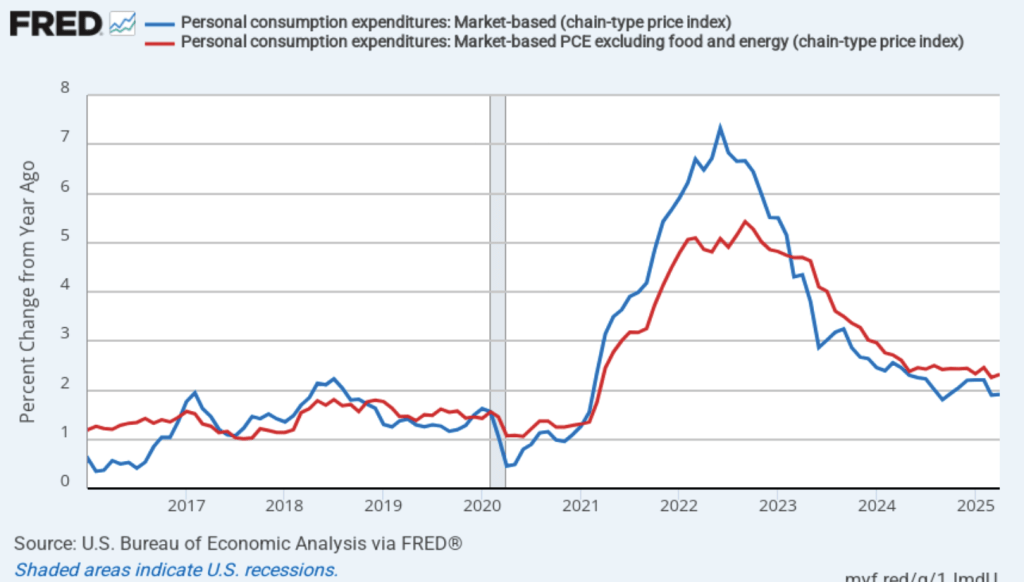

Fed Chair Jerome Powell has noted that inflation in non-market services has been high. Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices fall, the prices of financial services included in the PCE price index also fall. Powell has argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month headline inflation (the blue line) and 12-month core inflation (the red line) for market-based PCE. (The BEA explains the market-based PCE measure here.)

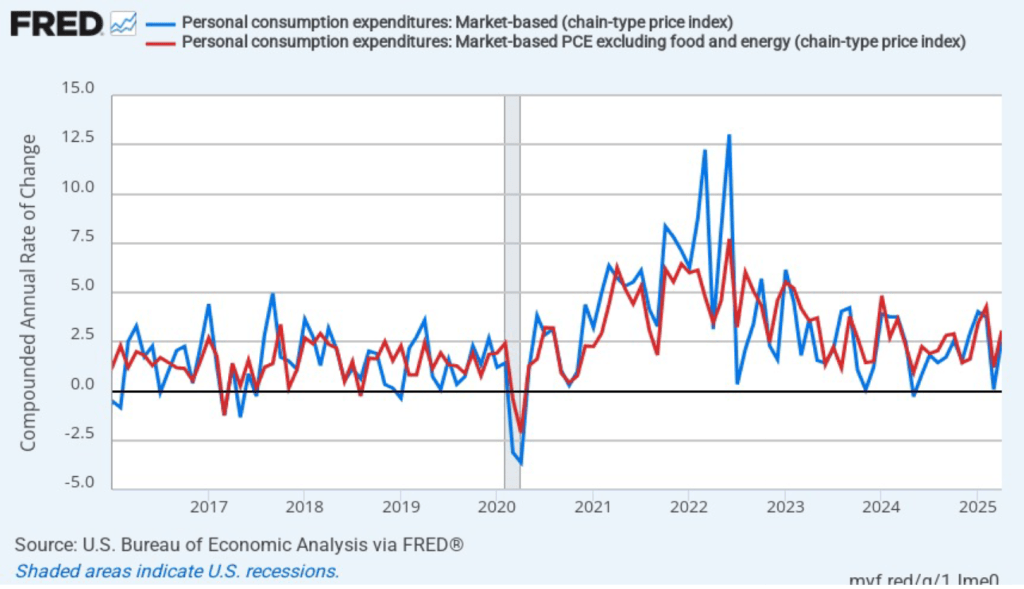

Headline market-based PCE inflation was 1.9 percent in April, unchanged from March. Core market-based PCE inflation was 2.3 percent in April, which was also unchanged from March. So, both market-based measures show about the same rate of inflation in April as the total measures do. In the following figure, we look at 1-month inflation using these measures. The 1-month inflation rates are both higher than the 12-month rates. Headline market-based inflation was 2.6 percent in April, up from 0.1 percent in March. Core market-based inflation was 3.1 percent in April, up from 1.2 percent in March. As the figure shows, the 1-month inflation rates are more volatile than the 12-month rates, which is why the Fed relies on the 12-month rates when gauging how close it is coming to hitting its target inflation rate.

In summary, today’s data provide some evidence that the inflation rate is getting closer to the Fed’s 2 percent annual target. Improving inflation combined with some indications that output growth is slowing—the BEA release indicated that growth in real consumption expenditures slowed in April—might make it more likely that the Fed’s policymaking Federal Open Market Committee (FOMC) will cut its target for the federal funds rate relatively soon.

However, investors who buy and sell federal funds futures contracts expect that the FOMC will leave its federal funds rate target unchanged at its next meetings on June 17–18 and July 29–30. (We discuss the futures market for federal funds in this blog post.) Investors assign a probability 0f 72.6 percent to the FOMC cutting its target at its September 29–30 meeting. Investor expectations reflect the recent statements from Fed Chair Jerome Powell and other members of the FOMC that they intend to wait until the effects of the tariff increases on the economy are clearer before changing the target for the federal funds rate.

Image generated by ChatGTP-4o of a family shopping in a supermarket.

Today (May 13), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for April. The following figure compares headline inflation (the blue line) and core inflation (the green line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.3 percent in April—down from 2.4 percent in March.

The core inflation rate,which excludes the prices of food and energy, was 2.8 percent in April—unchanged from March.

Headline inflation was the lowest since February in 2021—before the acceleration in inflation that began in the spring of 2021. Core inflation was the lowest since March 2021. Both headline inflation and core inflation were what economists surveyed had expected.

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) rose from –0.6 percent in March to 2.7 percent in April. Core inflation (the red line) rose from 0.9 percent in March to 2.9 percent in April.

The 1-month and 12-month inflation rates are telling different stories, with 12-month inflation indicating that the rate of price increase is back to what it was in early 2021. The 1-month inflation rate indicates a significant increase in April from the very low rate of price increase in March. The 1-month inflation rate indicates that inflation is still running ahead of the Fed’s 2 percent annual inflation target.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that 1-month inflation is particularly volatile. It is possible, though, that the increase in 1-month inflation in April reflects the effect on the price level of the large tariff increases the Trump Administration announced on April 2. Whether those effects will persist is unclear because the administration has been engaged in negotiations that may significantly reduce the tariff increases announced in April. Finally, note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

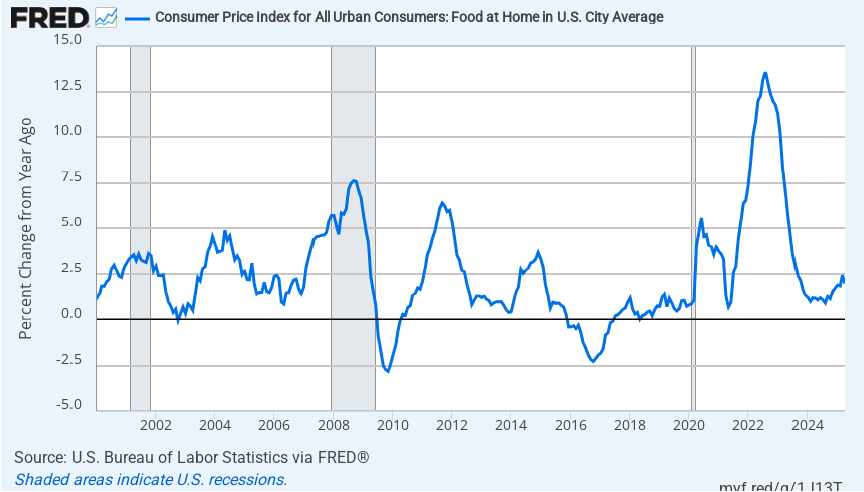

There’s been considerable discussion in the media about continuing inflation in grocery prices. The following figure shows inflation in the CPI category “food at home,” which is primarily grocery prices. Inflation in grocery prices was 2.0 percent in April and has been below 2.5 percent every month since September 2023. Over the past year, there has been a slight upward trend in inflation in grocery prices but to this point it remains relatively low, although well above the very low rates of inflation in grocery prices that prevailed from 2015 to 2019.

It’s the nature of the CPI that in any given month some prices will increase rapidly while other prices will increase slowly or even decline. Although, on average, grocery price inflation has been relatively low, there have been substantial increases in the prices of some food items. For instance, a recent article in the Wall Street Journal noted that rising cattle prices will likely be reflected in coming months rising prices for beef purchased in supermarkets. The following figure shows inflation in the prices of ground beef and steaks over the period starting in January 2015. As we should expect, the prices of these two goods are more volatile mont to month than are grocery prices as a whole. Ground beef prices increased 10.8 percent in April, an increase that will likely be noticeable to someone planning for a Memorial Day cookout.

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.0 percent in April, unchanged from March. Twelve-month median inflation (the red line) 3.5 percent in April, also unchanged from March.

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation increased from 2.6 percent in March to 3.0. percent in April. One-month median inflation declined from 4.2 percent in March to 4.0 percent in April. These data, although mixed, provide some confirmation that inflation likely increased somewhat from March to April.

What are the implications of this CPI report for the actions the FOMC may take at its next several meetings? Investors who buy and sell federal funds futures contracts still do not expect that the FOMC will cut its target for the federal funds rate at its next two meetings. (We discuss the futures market for federal funds in this blog post.) Today, investors assigned only an 8.4 percent probability to the Fed’s policymaking Federal Open Market Committee (FOMC) cutting its target from the current 4.25 percent to 4.50 percent range at its meeting on June 17–18. Investors assigned a probability of 34.9 percent that the FOMC will cut its target after its meeting on July 29–30. Investors assigned a probability of 73.1 percent that the committee will cut its target after its meeting on September 16–17. The FOMC’s actions will likely depend in part on the success of the current trade negotiations.

Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

Members of the Fed’s policymaking Federal Open Market Committee (FOMC) had signaled clearly before today’s (May 7) meeting that the committee would leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. In the statement released after its meeting, the committee made one significant change to the wording in its statement following its last meeting on March 19. The committee added the words in bold to the following sentence:

“The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.”

The key event since the last FOMC meeting was President Trump’s announcement on April 2 that he would implement tariff increases that were much higher than had previously been expected.

As we noted in an earlier blog post, an unexpected increase in tariff rates will result in an aggregate supply shock to the economy. As we discuss in Macroeconomics, Chapter 13,Section 13.3 (Economics, Chapter 23, Section 23.3), an aggregate supply shock puts upward pressure on the price level at the same time as it causes a decline in real GDP and employment. The result, as the FOMC statement indicates, can be both rising inflation and rising unemployment. If higher inflation and higher unemployment persist, the U.S. economy would be experiencing stagflation. The United States last experienced stagflation during the 1970s when large increases in oil prices caused an aggregate supply shock.

During his press conference following the meeting, Fed Chair Jerome Powell indicated that the increase in tariffs might the Fed’s dual mandate goals of price stability and maximum employment “in tension” if both inflation and unemployment increase. If the FOMC were to increase its target for the federal funds rate in order to slow the growth of demand and bring down the inflation rate, the result might be to further increase unemployment. But if the FOMC were to cut its target for the federal funds rate to increase the growth of demand and reduce the unemployment rate, the result might be to further increase the inflation rate.

Powell emphasized during his press conference that tariffs had not yet had an effect on either inflation or unemployment that was large enough to be reflected in macroeconomic data—as we’ve noted in blog posts discussing recent macroeconomic data releases. As a result, the consensus among committee members is that it would be better to wait to future meetings before deciding what changes in the federal funds rate might be needed: “We’re in a good position to wait and see. We don’t have to be in a hurry.”

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed is successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

In his press conference, Powell indicated that when the committee would change its target for the federal funds rate was dependent on the trends in macroeconomic data on inflation, unemployment, and output during the coming months. He noted that if both unemployment and inflation significantly increased, the committee would focus on which variable had moved furthest from the Fed’s target. He also noted that it was possible that neither inflation nor unemployment might end up significantly increasing either because tariff negotiations lead to lower tariff rates or because the economy proves to be better able to deal with the effects of tariff increases than many economist now expect.

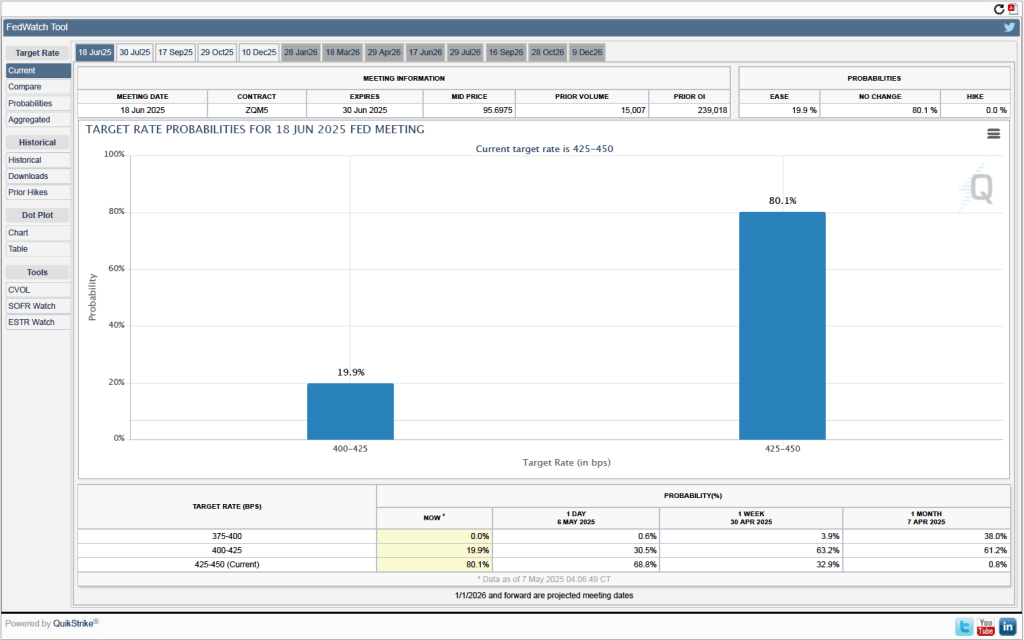

One indication of expectations of future changes in the target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that investors don’t expect that the FOMC will cut its target for the federal funds rate at its May 17–18 meeting. As shown in the following figure, investors assign a 80.1 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

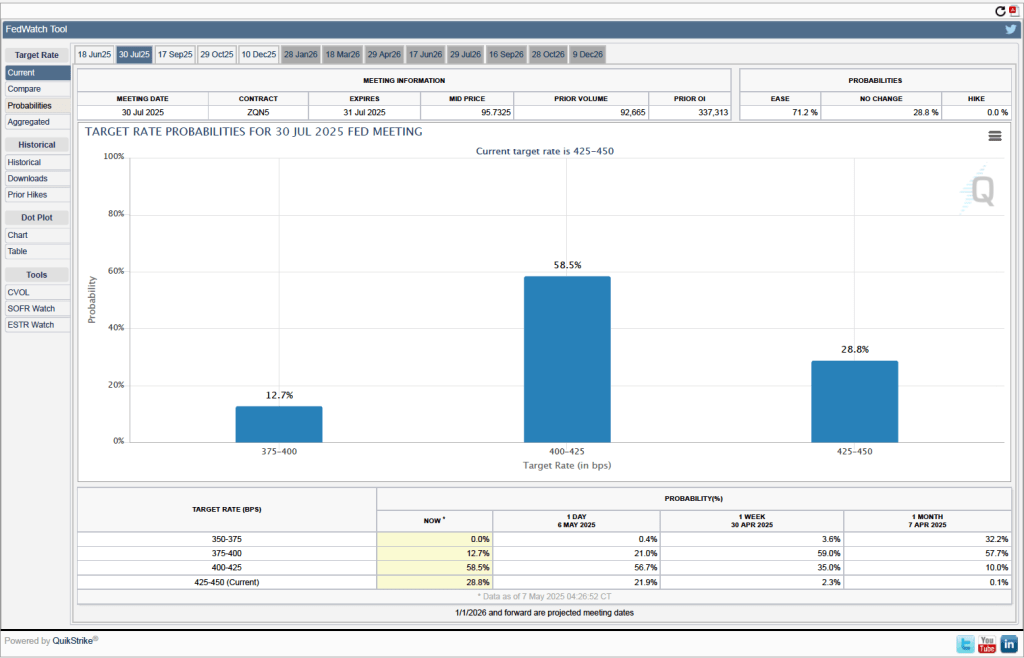

When will the Fed likely cut its target for the federal funds rate? As the following figure shows, investors expect it to happen at the FOMC’s July 29–30 meeting. Investors assign a probably of 58.5 percent to the committee cutting its target by 0.25 percentage point (25 basis points) at that meeting and a probability of 12.7 percent to the committee cutting its target by 50 basis points. Investors assign a probability of only 28.8 percent to the committee leaving its target unchanged.

Image created by ChatGTP=4o of workers on an automobile assembly line.

We noted in a blog post earlier this week that although the preliminary estimate from the Bureau of Economic Analysis (BEA) indicated that real GDP had declined during the first quarter of 2025, the report didn’t provide a clear indication that the U.S. economy was in recession. This morning (May 2), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for April. The data in the report also show no sign that the U.S. economy is in a recession. Although there have been many stories in the media about businesspeople becoming increasingly pessimistic, we don’t yet see it in the employment data. We should add two caveats, however: 1. The effects of the large tariff increases the Trump Administration announced on April 2 are likely not reflected in the data from this report, and 2. at the beginning of a recession the data in the jobs report can be subject to large revisions.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

According to the establishment survey, there was a net increase of 177,000 jobs during April. This increase was well above the increase of 135,000 that economists surveyed had forecast. Somewhat offsetting this unexpectedly large increase was the BLS revising downward its previous estimates of employment in February and March by a combined 58,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in payroll employment for each month in the last two years.

The unemployment rate was unchanged to 4.2 percent in April. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 436,000 jobs in April, following an increase of 201,000 jobs in March. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, however, both surveys showed net jobs increasing. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

The household survey has another indication of continuing strength in the labor market. The employment-population ratio for prime age workers—those aged 25 to 54—increased from 80.4 percent in March to 80.7 percent in April. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to January 2020.

It remains unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 9,000 in April. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may find a more significant decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.8 percent in April, which is unchanged from the March increase.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. The April, the 1-month rate of wage inflation was 2.0 percent, down from 3.4 percent in March. If the 1-month increase in AHE is sustained, it would contribute to the Fed’s achieving its 2 percent target rate of price inflation.

Today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. Looming over monetary policy, however, is the expected effect of the Trump Administration’s unexpectedly large tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

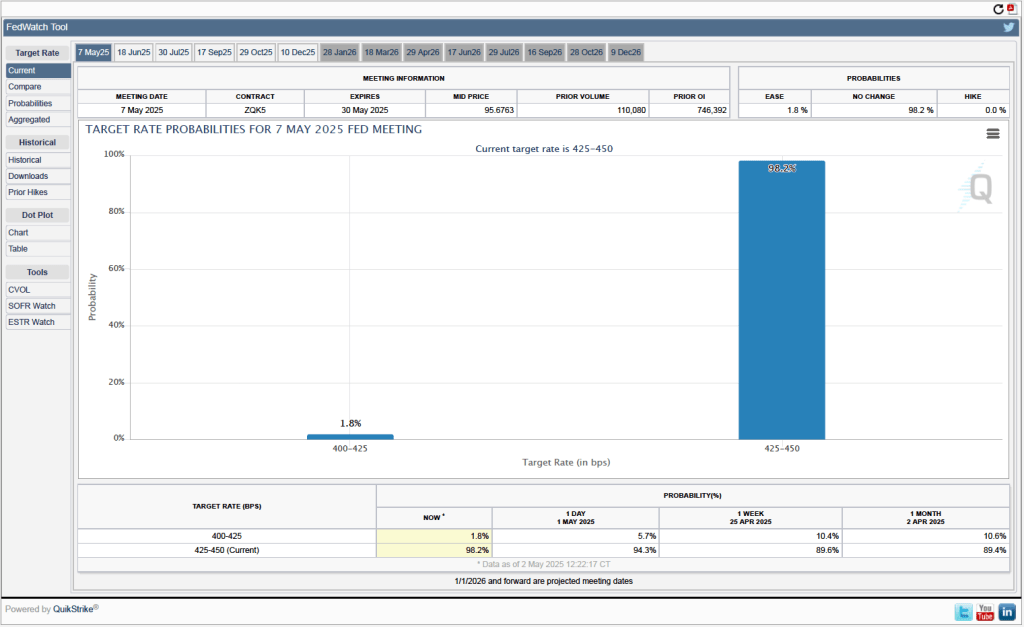

One indication of expectations of future changes in the target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the surprisingly large tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its May 6–7 meeting. As shown in the following figure, investors assign a 98.2 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

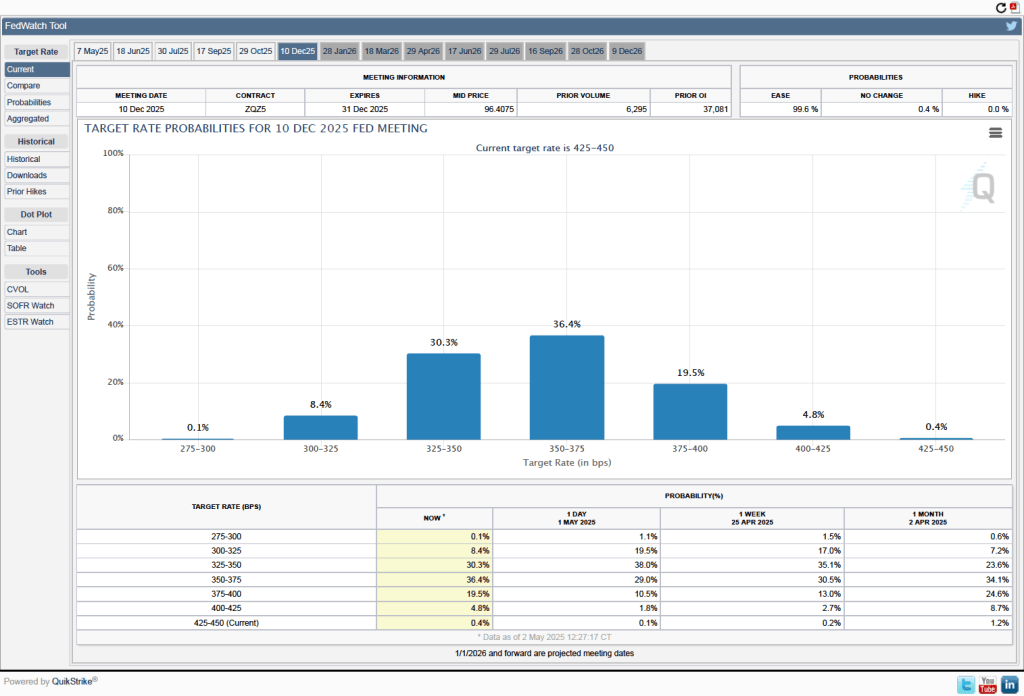

It’s a different story if we look at the end of the year. As the following figure shows, investors now expect that by the end of the FOMC’s meeting on December 9-10, the committee will have implemented at least three 0.25 percentage point (25 basis points) cuts in its target range for the federal funds rate. Investors assign a probability of 75.9 percent that the target range will end the year at 3.50 percent to 3.75 percent or lower. At their March meeting, FOMC members projected only two 25 basis point cuts this year—but that was before the announcement of the unexpectedly large tariff increases.

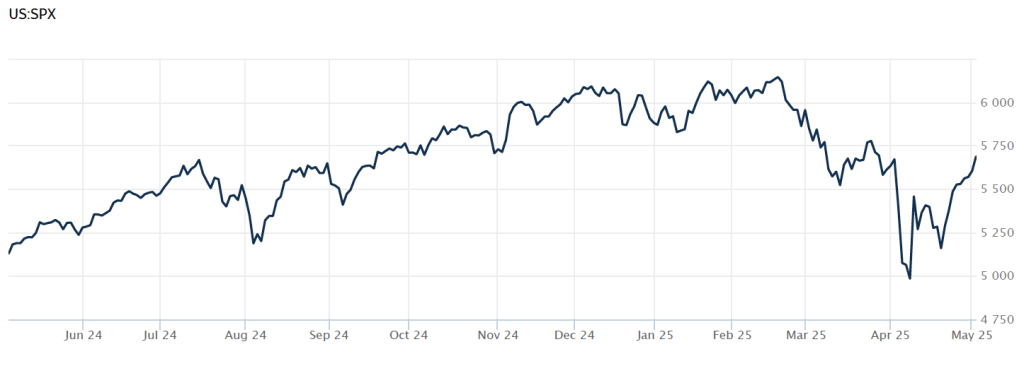

How the economy will fare for the remainder of the year depends heavily on what happens with respect to tariffs. News today that China and the United States may be negotiating lower tariff rates has contributed to rising stock prices. The following figure from the Wall Street Journal shows movements in the S&P stock index over the past year. The index declined sharply on April 2, following President Trump’s announcement of the tariff increases. As of 2 pm today, the S&P index has risen above its value on April 1, meaning that it has recovered all of the losses since the announcement of the tariff increases. The increase in stock prices likely indicates that investors expect that the tariff increases will end up being much smaller than those originally announced and that the chances of a recession happening soon are lower than they appeared to be on April 2.

An image generated by ChatGTP-4o of a hypothetical meeting between President Richard Nixon and Fed Chair Arthur Burns in the White House.

In a speech on April 15 at the Economic Club of Chicago, Federal Reserve Chair Jerome Powell discussed how the Fed might react to President Donald Trump’s tariff increases: “Tariffs are highly likely to generate at least a temporary rise in inflation. The inflationary effects could also be more persistent…. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.”

Powell’s remarks were interpreted as indicating that the Fed’s policymaking Federal Open Market Committee (FOMC) was unlikely to cut its target for the federal funds rate anytime soon. President Trump, who has stated several times that the FOMC should cut its target, was displeased with Powell’s position and posted on social media that “Powell’s termination cannot come fast enough!” Stock prices declined sharply on the possibility that Trump might try to fire Powell because many economists and market participants believed that move would increase uncertainty and possibly undermine the FOMC’s continuing attempts to bring inflation down to the Fed’s 2 percent target. Trump, possibly responding to the fall in stock prices, stated to reporters that he had “no intention” of firing Powell. In this recent blog post we discuss the debate over whether presidents can legally fire Fed chairs.

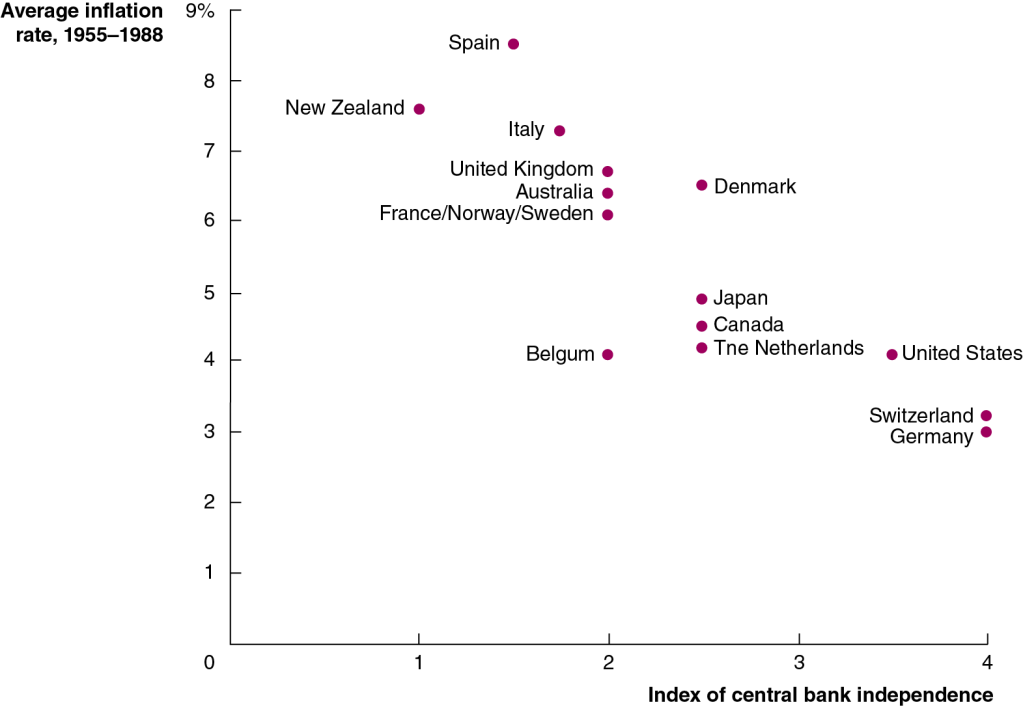

Leaving aside the legal issue of whether a president can fire a Fed chair, would it be better or worse for the conduct of monetary if the presdient did have that power? We review the arguments for and against the Fed conducting monetary policy independently of the president and Congress in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4). One key point that’s often made in favor of Fed independence is illustrated in Figure 17.12, which is reproduced below.

The figure is from a classic study by Alberto Alesina and Lawrence Summers, who were both economists at Harvard University at the time. Alesina and Summers tested the assertion that the less independent a country’s central bank, the higher the country’s inflation rate will be by comparing the degree of central bank independence and the inflation rate for 16 high-income countries during the years from 1955 to 1988. As the figure shows, countries with highly independent central banks, such as the United States, Switzerland, and Germany, had lower inflation rates than countries whose central banks had little independence, such as New Zealand, Italy, and Spain. In the following years, New Zealand and Canada granted their banks more independence, at least partly to better fight inflation.

Debates over Fed independence didn’t start with President Trump and Fed Chair Powell; they date all the way back to the passage of the Federal Reserve Act in 1913. The background to the passage of the Act is the political struggle over establishing a central bank during the early years of the country. In 1791, Congress established the Bank of the United States, at the urging of the country’s first Treasury secretary, Alexander Hamilton. When the bank’s initial 20-year charter expired in 1811, political opposition kept the charter from being renewed, and the bank went out of existence. The bank’s opponents believed that the bank’s actions had the effect of reducing loans to farmers and owners of small businesses and that Congress had exceeded its constitutional authority in establishing the bank. Financial problems during the War of 1812 led Congress to charter the Second Bank of the United States in 1816. But, again, political opposition, this time led by President Andrew Jackson, resulted in the bank’s charter not being renewed in 1836.

As we discuss in Chapter 14, Section 14.4, Congress established the Federal Reserve as a lender of last resort to bring an end to bank panics. In 1913, Congress was less concerned aboout making the Fed independent from Congress and the president than it was in overcoming political opposition to establishing a central bank located in Washington, DC. Accordingly, Congress established a decentralized system by having 12 District Banks that would be owned by the member banks in the district. Congress gave the responsibility for overseeing the system to the Federal Reserve Board, which was the forerunner of the current Board of Governors. The president had a greater influence on the Federal Reserve Board than presidents today have on the Board of Governors because the Federal Reserve Board included the secretary of the Treasury and the comptroller of the currency as members. Then as now, the president is free to replace the secretary of the Treasury and the comptroller of the currency at any time.

When the United States entered World War I in April 1917, the Fed came under pressure to help the Treasury finance the war by making loans to banks to help the banks purchase Treasury securities—Liberty Bonds—and by lending funds to banks that banks could loan to households to purchase bonds. In 1919, a ruling by the attorney general clarified that Congress had intended in the Federal Reserve Act to give the Federal Reserve Board the power to set the discounts rate the 12 District Banks charged member banks on loans.

Despite this ruling, authority within the Fed remained much more divided than is true today. Divided authority proved to be a serious problem when the Fed had to deal with the Great Depression, which began in August 1929 and worsened as the result of a series of bank panics. As we’ve seen, the secretary of the Treasury and the comptroller of the currency, both of whom report directly to the president of the United States, served on the Federal Reserve Board. So, the Fed had less independence from the executive branch of the government than it does today.

In addition, the heads of the 12 District Banks operated much more independently than they do today, with the head of the Federal Reserve Bank of New York having nearly as much influence within the system as the head of the Federal Reserve Board. At the time of the bank panics, George Harrison, the head of the Federal Reserve Bank of New York, served as chair of the Open Market Policy Conference, the predecessor of the current Federal Open Market Committee. Harrison frequently acted independently of Roy Young and Eugene Meyer, who served as heads of the Federal Reserve Board during those years. Important decisions could be made only with the consensus of these different groups. During the early 1930s, consensus proved hard to come by, and taking decisive policy actions was difficult.

The difficulties the Fed had in responding to the Great Depression led Congress to reorganize the system with the passage of the Banking Act of 1935. Most of the current structure of the Fed was put in place by that law. Power was concentrated in the hands of the Board of Governors. The removal of the secretary of the Treasury and the comptroller of the currency from the Board reduced the ability of the president to influence the Fed’s decisions.

During World War II, the Fed again came under pressure to help the federal government finance the war. The Fed agreed to hold interest rates on Treasury securities at low levels: 0.375% on Treasury bills and 2.5% on Treasury bonds. The Fed could keep interest rates at these low levels only by buying any bonds that were not purchased by private investors, thereby fixing, or pegging, the rates.

When the war ended in 1945, the Treasury and President Harry Truman wanted to continue this policy, but the Fed didn’t agree. The Fed’s concern was inflation: Larger purchases of Treasury securities by the Fed could increase the growth rate of the money supply and the rate of inflation. Fed Chair Marriner Eccles strongly objected to the policy of fixing interest rates. His opposition led President Truman to not reappoint him as chair in 1948,although Eccles continued to fight for Fed independence during the remainder of his time as a governor. On March 4, 1951, the federal government formally abandoned the wartime policy of fixing the interest rates on Treasury securities with the Treasury–Federal Reserve Accord. This agreement was important in eestablishing the Fed’s ability to operate independently of the Treasury.

Conflicts between the Treasury and the Fed didn’t end with that agreement, however. Thomas Drechsel of the University of Maryland has analyzed the daily schedules of presidents during the period from 1933 to 2016 and finds that during these years presidents met with Fed officials on more than 800 occasions. Of course, not all of these interactions involved attempts by a president to influence the actions of a Fed Chair, but some seem to have. For example, research by Helen Fessenden of the Federal Reserve Bank of Richmond has shown that in 1967, President Lyndon Johnson, who was facing reelection in 1968, was anxious that Fed Chair William McChesney Martin adopt a more expansionary monetary policy. There is some evidence that Johnson and Martin came to an agreement that if Johnson agreed to push Congress to increase taxes, Martin would pursue an expansionary monetary policy.

An image generated by ChatGTP-4o of a hypothetical meeting between President Lyndon Johnson and Fed Chair William McChesney Martin in the White House.

Similarly, in late 1971, President Richard Nixon was concerned that the unemployment rate was at 6%, which he believed would, if it persisted, endanger his chance of reelection in 1972. Dreschel finds that Nixon met with Fed Chair Arthur Burns 34 times during the second half of 1971. Evidence from tape recordings of Nixon’s conversations with Burns at the White House and from Burns’s diary entries indicate that Nixon pressured Burns to increase the rate of growth of the money supply and that Burns agreed to do so.

President Ronald Reagan and Federal Reserve Chair Paul Volcker argued over who was at fault for the severe economic recession of the early 1980s. Reagan blamed the Fed for soaring interest rates. Volcker held that the Fed could not take action to bring down interest rates until the budget deficit—which results from policy actions of the president and Congress—was reduced. Similar conflicts occurred during the administrations of George H.W. Bush and Bill Clinton, with the Treasury frequently pushing for lower short-term interest rates than the Fed considered advisable.

During the financial crisis of 2007–2009 and during the 2020 Covid pandemic, the Fed worked closely with the Treasury. The relationship was so close, in fact, that some economists and policymakers worried that the Fed might be sacrificing some of its independence. The frequent consultations between Fed Chair Ben Bernanke and Treasury Secretary Henry Paulson in the fall of 2008, during the height of the crisis, were a break with the tradition of Fed chairs formulating policy independently of a presidential administration. During the 2020 pandemic, Fed Chair Jerome Powell and Treasury Secretary Steven Mnuchin also frequently consulted on policy.

These examples from the Fed’s history indicate that presidents have persistently attempted to influence Fed policy. Most economists believe that central bank independence is an important check on inflation. But, given the importance of monetary policy, it’s probably inevitable that presidents and members of Congress will continue to attempt to sway Fed policy.

Image generated by ChatGTP-4o One of the key issues in monetary policy—dating back decades—is whether policy should be governed by a rule or whether the members of the Federal Open Market Committee (FOMC) should make “data-driven” decisions. Currently, the FOMC believes that the best approach is to let macroeconomic data drive decisions about the appropriate target … Continue reading “Should We Turn Monetary Policy over to Generative Artificial Intelligence?”

Image generated by ChatGTP-4o

One of the key issues in monetary policy—dating back decades—is whether policy should be governed by a rule or whether the members of the Federal Open Market Committee (FOMC) should make “data-driven” decisions. Currently, the FOMC believes that the best approach is to let macroeconomic data drive decisions about the appropriate target for the federal funds rate rather than to allow a policy rule to determine the target.

In its most recent Monetary Policy Report to Congress, the Fed’s Board of Governors noted that policy rules “can provide useful benchmarks for the consideration of monetary policy. However, simple rules cannot capture all of the complex considerations that go into the formation of appropriate monetary policy, and many practical considerations make it undesirable for the FOMC to adhere strictly to the prescriptions of any specific rule.” We discuss the debate over monetary policy rules—sometimes described as the debate over “rules versus discretion” in conducting policy—in Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5.)

Probably the best known advocate of the Fed relying on policy rules is John Taylor of Stanford University. The Taylor rule for monetary policy begins with an estimate of the value of the real federal funds rate, which is the federal funds rate—adjusted for inflation—that would be consistent with real GDP being equal to potential real GDP in the long run. With real GDP equal to potential real GDP, cyclical unemployment should be zero, and the Fed will have attained its policy goal of maximum employment, as the Fed defines it.

According to the Taylor rule, the Fed should set its current federal funds rate target equal to the sum of the current inflation rate, the equilibrium real federal funds rate, and two additional terms. The first of these terms is the inflation gap—the difference between current inflation and the target rate (currently 2 percent, as measured by the percentage change in the personal consumption expenditures (PCE) price index; the second term is the output gap—the percentage difference of real GDP from potential real GDP. The inflation gap and the output gap are each given “weights” that reflect their influence on the federal funds rate target. With weights of one-half for both gaps, we have the following Taylor rule:

Federal funds rate target = Current inflation rate + Equilibrium real federal funds rate + (1/2 × Inflation gap) + (1/2 × Output gap).

So when the inflation rate is above the Fed’s target rate, the FOMC will raise the target for the federal funds rate. Similarly, when the output gap is negative—that is, when real GDP is less than potential GDP—the FOMC will lower the target for the federal funds rate. In calibrating this rule, Taylor assumed that the equilibrium real federal funds rate is 2 percent and the target rate of inflation is 2 percent. (Note that the Taylor rule we are using here was the one Taylor first proposed in 1993. Since that time, Taylor and other economists have also analyzed other similar rules with, for instance, an assumption of a lower equilibrium real federal funds rate.)

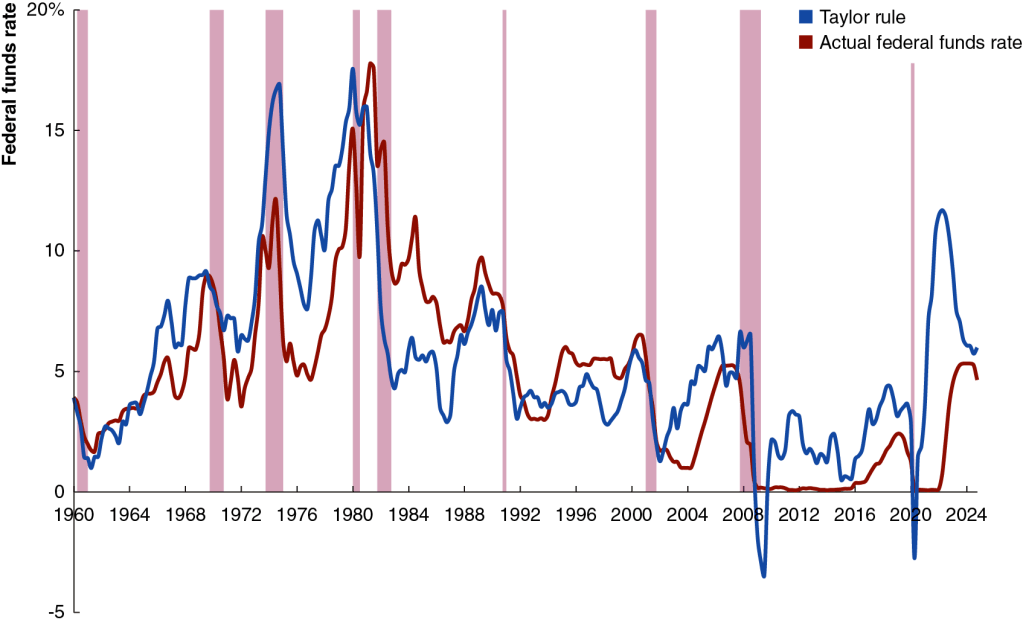

The following figure shows the level of the federal funds rate that would have occurred if the Fed had strictly followed the original Taylor rule (the blue line) and the actual federal funds rate (the red line). The figure indicates that because during many years the two lines are close together, the Taylor rule does a reasonable job of explaining Federal Reserve policy. There are noticeable exceptions, however, such as the period of high inflation that began in the spring of 2021. During that period, the Taylor rule indicates that the FOMC should have begun raising its target for the federal funds rate earlier and raised it much higher than it did.

Taylor has presented a number of arguments in favor of the Fed relying on a rule in conducting monetary policy, including the following:

A simple policy rule (such as the Taylor rule) makes it easier for households, firms, and investors to understand Fed policy.

Conducting policy according to a rule makes it less likely that households, firms, and investors will be surprised by Fed policy.

Fed policy is less likely to be subject to political pressure if it follows a rule: “If monetary policy appears to be run in an ad hoc and complicated way rather than a systematic way, then politicians may argue that they can be just as ad hoc and interfere with monetary policy decisions.”

Following a rule makes it easier to hold the Fed accountable for policy errors.

The Fed hasn’t been persuaded by Taylor’s arguments, preferring its current data-driven approach. In setting monetary policy, the members of the FOMC believe in the importance of being forward looking, attempting to take into account the future paths of inflation and unemployment. But committee members can struggle to accurately forecast inflation and unemployment. For instance, at the time of the June 2021 meeting of the FOMC, inflation had already risen above 4%. Nevertheless, committee members forecast that inflation in 2022 would be 2.1%. Inflation in 2022 turned out to be much higher—6.6%.

To succeed with a data-driven approach to policy, members of the FOMC must be able to correctly interpret the importance of new data on economic variables as it becomes available and also accurately forecast the effects of policy changes on key variables, particularly unemployment and inflation. How do the committee members approach these tasks? To some extent they rely on formal economic models, such as those developed by the economists on the committee’s staff. But, judging by their speeches and media interviews, committee members also rely on qualitative analysis in interpreting new data and in forming their expectations of how monetary policy will affect the economy.

In recent years, generative artificial intelligence (AI) and machine learning (ML) programs have made great strides in analyzing large data sets. Should the Fed rely more heavily on these programs in conducting monetary policy? The Fed is currently only in the beginning stages of incorporating AI into its operations. In 2024, the Fed appointed a Chief Artificial Intelligence Officer (CAIO) to coordinate its AI initiatives. Initially, the Fed has used AI primarily in the areas of supervising the payment system and promoting financial stability. AI has the ability to quickly analyze millions of financial transactions to identify those that may be fraudulent or may not be in compliance with financial and banking regulations. How households, firms, and investors respond to Fed policies is an important part of how effective the policies will be. The Fed staff has used AI to analyze how financial markets are likely to react to FOMC policy announcements.

The Central Bank of Canada has gone further than the Fed in using AI. According to Tiff Macklem, the Governor of the Bank of Canada, AI is used to:

• forecast inflation, economic activity and demand for bank notes • track sentiment in key sectors of the economy • clean and verify regulatory data • improve efficiency and de-risk operations

Will central banks begin to use AI to carry out the key activity of setting policy interest rates, such as the federal funds rate in the United States? AI has the potential to adjust the federal funds rate more promptly than the members of the FOMC are able to do in their eight yearly meetings. Will it happen? At this point, generative AI and ML models are not capable of taking on that responsibility. In addition, as noted earlier, Taylor and other supporters of rules-based policies have argued that simple rules are necessary for the public to understand Fed policy. AI generated rules are likely to be too complex to be readily understood by non-specialists.

It’s too early in the process of central banks adopting AI in their operations to know the eventual outcome. But AI is likely to have a significant effect on central banks, just as it is already affecting many businesses.