Glenn Hubbard and Tony O’Brien continue their podcast series hosting guest – Professor Mike Ryan of Western Michigan University. During the conversation, we learn about Mike’s experiences working with faculty from Western Michigan School of Business taking their courses online. He also offers his thoughts on the current trade situation as well as personal insights from a January visit to Japan.

Glenn Hubbard and Tony O’Brien continue their podcast series hosting guest – Jonathan Meer, Professor of Economics from Texas A&M University as well as the Director of the Private Enterprise Research Center at Texas A&M. During the conversation, we learn about Jonathan’s teaching over 3,500 students annually in a large online Principles of Microeconomics lecture course. He discusses how his usual online teaching absolutely helped his transition when Texas A&M closed for the semester. He also talks about the state of Higher Education, non-profit giving, as well as some challenges nonprofits face in these uncertain times.

Some notes from this Podcast if you’d like more information:

1. Link to Jonathan Meer’s Youtube video on setting up an online course:

Jonathan Meer of Texas A&M University shares his best practices for teaching economics online.

4. Please refer to the Apply the Concept feature from Chapter 2 of Hubbard and O’Brien Economics, 7/E, on the use of market mechanisms to allocate food at the Feeding America charity (for your convenience, we hope to post this shortly so check back).

Glenn Hubbard and Tony O’Brien continue their podcast series with a first – hosing a guest – Penn State Economics Professor, James Tierney. We learn about the transition James had from an early return from spring break to now teaching hundreds of students exclusively online in response to the pandemic. Glenn and Tony also discuss with James the struggles of the housing market in a small college town like State College, PA. We also learn the reasons behind James becoming the founder of an adult Improv company in the State College-area and the impact it had on his teaching. Please listen and share!

Glenn Hubbard and Tony O’Brien continue their podcast series by spending just under 15 minutes discussing why it was so difficult for economists to see this pandemic and the associated economic downturn coming. Just as scientists lacked the indicators to see the pandemic coming, economists also didn’t have the tools available to see where the economy was headed even though some early signs were present. Please listen and SHARE with your students.

Glenn Hubbard and Tony O’Brien continued their podcast series by spending about 15 minutes discussing the impact of the Pandemic on the Mom and Pop Businesses across the country. Much of the stimulus package has been developed to save small business but might it be too late or just not enough? Please listen and SHARE with your students.

On April 24th, Glenn Hubbard and Tony O’Brien continued their podcast series by spending about 18 minutes discussing the role of uncertainty in how quickly the economy can rebound once things open back up. A very good discussion about business cycles occurs. Instructors – Please consider sharing these podcasts with your students. A lot of URL dropping in today’s conversation so we’re providing some show notes from today’s episodes if you’d like to explore them further:

Can Mom and Pop Businesses Survive the Coronavirus Pandemic?

By early April 2020, because of the coronavirus pandemic, all 50 state governments had issued declarations of emergency and had closed schools and some or all businesses considered to be non-essential. A survey by Alexander Bartik of the University of Illinois and colleagues indicated that about 43 percent of small businesses in the Unites States had closed, causing most of their revenue to disappear. As a result, those businesses had laid off about 40 percent of their employees.

In March 2020, Congress and President Donald Trump enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The act included the Paycheck Protection Program (PPP), which provided loans to businesses with 500 or fewer employees to pay for up to eight weeks of payroll expenses and certain other costs. The government would forgive the loans if business owners used 75 percent of the funds for payroll expenses.

The PPP was administered by the federal Small Business Administration with the loans being made primarily by local banks. Many small businesses have trouble borrowing from banks, particularly if they lack collateral, such as owning the building they operate in, or if they don’t have a long-term relationship with a bank by having borrowed from them in the past or having maintained a business checking account with them. In a survey by the Federal Reserve conducted in 2019, before the coronavirus pandemic, 64 percent of small businesses had faced financial challenges, such as paying operating expenses or purchasing inventories, during the previous year. Of those firms, 69 percent had relied on the owner’s personal funds to meet the financial challenge.

In mid-April 2020, it was unclear whether Congress might change the PPP to make it easier for small businesses to borrow through credit unions and other lenders that are not commercial banks. News reports indicated that a significant number of small businesses had exhausted the funds their owners had available and intended to permanently close. It’s not unusual for a small firm to fail. In a typical year, even when the economy is expanding, hundreds of thousands of businesses fail (and a similar number open). But some economists and policymakers were concerned that the effects of the pandemic might lead to a permanent reduction in the number of small firms, particularly so-called “Mom and Pop businesses”—sole proprietorships that employ fewer than 20 workers. (We discuss the differences between sole proprietorships and other ways of organizing a business in Chapter 8, Section 8.1)

The pandemic posed particular challenges for these businesses. Many small retailers, such as clothing stores, shoe stores, card shops, and toy stores, had already been hurt before the pandemic as consumers shopped at online sites such as Amazon. This trend increased during the pandemic. In addition, as many consumers shifted from eating in restaurants to buying groceries from supermarkets or online, the future of some small restaurants seemed in doubt.

Even as states and cities began to allow nonessential businesses to reopen, many consumers were reluctant to return to eating in restaurants, staying in hotels, and shopping in brick-and-mortar stores in the absence of a vaccine against the coronavirus. The shift to online buying was evident during March and April 2020 when, as many small businesses were laying off workers, Amazon was hiring an additional 175,000 workers and Walmart was hiring an additional 150,000. Some public health authorities and epidemiologists were suggesting that businesses take certain steps to reassure consumers, although doing so would raise the businesses’ costs of operating. For instance, Scott Gottlieb, former Food and Drug Administration commissioner, suggested that “businesses … should look at trying to bring testing on-site at the place of employment” to reassure customers that the businesses’ workers did not have the virus. He also suggested that restaurants print their menus on paper that could be thrown away after each use and commit to more frequent disinfecting. Clearly, the revenue earned by larger businesses would be better able to cover these costs while still at least breaking even.

If the world is entering a new period with more frequent epidemics of viruses to which most people lack immunity, small businesses will be at a further disadvantage. Although Congress and the president responded to the coronavirus with the PPP program, whether they would have funds to do so during future epidemics remained unclear. As a result, it may be of increased importance that firms have the resources to finance periods of closure without having to rely on government payments, loans from banks for which they may lack the necessary collateral, or running balances on high-interest rate credit cards. The survey by Alexander Bartik and colleagues referred to earlier indicated that the average small business has $10,000 in monthly costs and less than that amount readily available to use to pay those costs. In other words, many small businesses are dependent on paying their current costs from their current revenues.

Most small business owners are resourceful enough to respond to changing conditions, but the challenges posed by the coronavirus seemed likely to reshape the structure of some industries, including restaurants, small retail stores, gyms, non-chain hotels, and small medical and dental practices. When discussing the role that barriers to entry play in determining the level of competition and the size of firms in an industry, we emphasized the role played by physical economies of scale. For instance, we noted that:

A music streaming firm has the following high fixed costs: very large server capacity, large research and development costs for its app, and the cost of the complex accounting necessary to keep track of the payments to the musicians and other copyright holders whose songs are being streamed. A large streaming firm such as Spotify has much lower average costs than would a small music streaming firm, partly because a large firm can spread its fixed costs over a much larger quantity of subscriptions sold.

We also noted that economies of scale of this type did not exist in the restaurant industry. Prior to the pandemic, it was reasonable to argue that large restaurants were typically unable to serve meals at a lower average cost than smaller restaurants and that even if smaller restaurants faced higher average costs, by differentiating the meals they served, smaller restaurants could still attract customers despite charging a higher price than larger restaurants. But if small restaurants lack the ability to finance periods of closure during epidemics and have trouble breaking even due to the higher costs of printing paper menus, testing their employees onsite, and more frequent cleaning, they may struggle to survive. Larger restaurants can spread these costs over a larger number of meals, reducing the average cost of one meal compared with smaller restaurants. As more consumers avoid restaurants and eat more frequently at home, smaller restaurants may be pushed further up their average cost curves by being able to sell only a smaller quantity of meals.

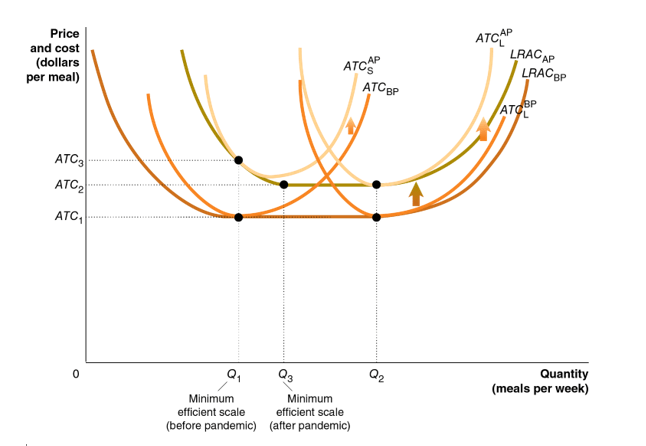

The following figure illustrates how the pandemic may affect the costs of a typical restaurant. The long-run average cost curve LRACBP shows the situation before the pandemic. The higher costs necessary to operate after the pandemic, including printing paper menus and more frequent cleaning, shifts up the long-run average cost curve to LRACAP. Before the pandemic, the average total cost curve for the small restaurant is and for the large restaurant is . Notice that even though the large restaurant serves Q2 meals per week and the small restaurant serves Q1 meals per week, they both have the same average total cost per meal, ATC1.

Also notice that before the pandemic, serving Q1 meals per week was the minimum efficient scale for a restaurant. Minimum efficient scale is the level of output at which all economies of scale are exhausted. The pandemic increases the costs of the small restaurant from to is , and the costs of the large restaurant from to . Minimum efficient scale increases to Q3, which is more meals per week than a small restaurant can sell. As a result, the average total cost of small restaurant increases to ATC3. A larger restaurant is still selling a quantity of meals that is beyond minimum efficient scale, so its average cost only rises to ATC2. With higher average costs, smaller restaurants are less able to successfully compete with larger restaurants.

Small firms in other industries are likely to face similar challenges. The result could be a contraction in the number of firms in some industries. For instance, we may see franchised firms replacing Mom and Pop businesses—more Domino’s and Pizza Hut outlets and fewer independent pizza restaurants. Although it’s too early to tell the full effects of the coronavirus pandemic on U.S. businesses, the effects are likely to be far-reaching.

Sources: Ruth Simon, “For These Companies, Stimulus Was No Solution; ‘We Decided to Cut Our Losses,’” Wall Street Journal, April 15, 2020; Amara Omeokwe, “Small-Business Funding Dispute Challenges Community Lenders,” Wall Street Journal, April 14, 2020; Alexander W. Bartik, Marianne Bertrand, Zoë B. Cullen, Edward L. Glaeser, Michael Luca, and Christopher T. Stanton, “How Are Small Businesses Adjusting to Covid-19? Early Evidence from a Survey,” National Bureua of Economic Research, Working Paper 26989, April 2020 (https://www.nber.org/papers/w26989.pdf); Board of Governors of the Federal Reserve System, 2019 Report on Employer Firms: Small Business Credit Survey, https://www.fedsmallbusiness.org/medialibrary/fedsmallbusiness/files/2019/sbcs-employer-firms-report.pdf, 2019; Norah O’Donnell And Margaret Hynds, “5 Things to Know about Reopening the Country from Dr. Scott Gottlieb,” cbsnews.com, April 14, 2020.

Question:

Sendhil Mullainathann of the University of Chicago wrote an opinion column in the New York Times describing the situation facing the owner of a small restaurant:

She has little money in cash reserve; operating margins are thin … and her savings had already been spent on expanding the cramped kitchen. What was a thriving enterprise before the pandemic will emerge—if it emerges at all—as a hobbled business, which may well fail shortly thereafter.

A) What does Mullainathan mean by the restaurant’s “operating margins are thin”? Why would we expect the operating margins of a small restaurant to be thin?

B) If this restaurant was a “thriving enterprise” before the pandemic, why might it be likely to fail after the pandemic?

For Economics Instructors that would like the approved answers to the above questions, please email Christopher DeJohn from Pearson at christopher.dejohn@pearson.com and list your Institution and Course Number.

Supports: Econ and Micro: Chapter 8, “Firms, the Stock Market, and Corporate Governance” Macro Chapter 6; Essentials Chapter 6

The Futures market and the strange case of negative price of oil

There’s a point that seems so obvious that we haven’t explicitly mentioned it until now: The price of a good or service is always positive. After all, a price being negative means that a seller is paying a buyer to accept a good or service, which seems very unlikely. But this strange outcome did occur in the U.S. oil market during the economic upheaval caused by the coronavirus pandemic of 2020.

In the spring of 2020, there were two important developments in the world oil market:

A sharp decline in demand Many countries imposed social-distancing protocols and required non-essential business to shut down in response to the pandemic. These policies caused the demand for oil products to decline dramatically. For instance, in the United States, the demand for gasoline fell by about 50 percent between the middle of March and the middle of April. The decline was the largest in history over such a short period.

A decline in world supply Twenty-three countries, including the United States, Russia, and Saudi Arabia—the world’s three largest oil producer—agreed to reduce oil production by 9.7 million barrels per day, or about 13 percent of daily world production. These countries hoped that the decline in supply would keep the world price of oil from falling to very low levels. In fact, though, through mid-April the decline in demand was larger than the decline in supply leading to a dramatic decline in oil prices.

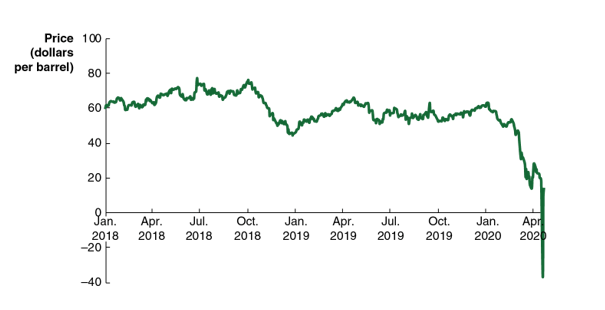

Crude oil from different rock formations can vary in its characteristics, such as its sulfur content. Crude oil that requires more processing as it is being refined into gasoline, aviation fuel, or other products, sells for a lower price. The benchmark oil price in the United States is for a grade of crude oil called West Texas Intermediate. The following figure shows the fluctuations in the price per barrel of this type of oil from January 2018 through late April 2020.

After reaching a high of $63 per barrel in January 2020, the price of oil declined to negative $37 per barrel on April 20. In other words, sellers were willing to pay buyers $37 per barrel to accept delivery of oil. Why would a seller ever pay someone to accept a product? There are two related reasons. We can discuss the first reason using demand and supply analysis. The second reason requires a brief discussion of how the oil market is different from most other markets for goods.

Demand and Supply in the Spot Market for Oil

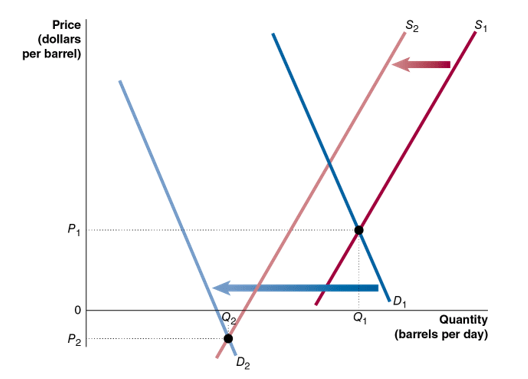

To understand how movements in demand and supply in the oil market resulted in a negative price, consider the following figure illustrating this situation. Before the coronavirus pandemic, the demand for oil is shown by demand curve D1 and the supply of oil by supply curve S1. The equilibrium price is P1. During the pandemic, the amount of oil demanded declined sharply from D1 to D2, and the supply of oil declined from S1 to S2. As a result, the new equilibrium price became negative at P2. We can see that for the equilibrium price to be negative, the demand curve and supply curve must intersect below the horizontal axis.

But why would a firm be willing to supply any oil at a negative price? The answer requires understanding how oil markets work. The spot price of oil is the price for oil that is available for immediate delivery. A seller at the spot price is typically a firm pumping oil, and a buyer is a firm that uses oil as an input, such as a firm that refines oil into gasoline. When you buy bread in the supermarket or a Big Mac at McDonald’s you are paying the spot price, which is the only price in the markets for most goods and services. In the figure we are showing the spot market for oil and the price is the spot price.

The Futures Market for Oil

But in addition to a spot market for oil, there is a futures market for oil, which allows individuals and firms to buy and sell futures contracts. A futures contract specifies the quantity of an asset—such as a barrel of oil—that will be delivered by the seller on a future date, the settlement date. Futures contracts exist for commodities such as oil, as well as for financial assets, such as Treasury bonds and stock indexes like the S&P 500. Futures contracts don’t set the price—the futures price—that the buyer will pay and the seller will receive on the settlement date. Instead, the price fluctuates as the contract is bought and sold on a futures exchange, such as the Chicago Board of Trade or the New York Mercantile Exchange, just as the price of a share of stock fluctuates as the stock is bought and sold in the stock market. Each oil futures contract represents 1,000 barrels (or 42,000 gallons) of oil.

The futures price of oil can differ from the spot price if people trading futures contracts expect that conditions in the oil market will differ on the settlement date from conditions today. For instance, on April 20, 2020, the date on which the spot price of oil was negative, the oil futures price on a contract with a settlement date in June was $22 per barrel and the price on a contract with a settlement date in November was $33 per barrel. The higher oil prices for June and November reflected the view among buyers and sellers and futures contracts that (1) the economy was likely to begin recovering from the worst of the pandemic by then, increasing the demand for oil and (2) the supply of oil was likely to decline further.

The spot price and the futures price are linked because it’s possible to store oil. So, the futures price should roughly equal the spot price plus the cost of storing oil between today and the settlement date of the futures contract. As the settlement date approaches, the futures price comes closer to the spot price, eventually equaling the spot price on the settlement date. Why must the spot price equal the futures price on the settlement date? Because if there were a difference between the two prices, it would be possible for an investor to make a profit. For instance, if the spot price of oil was $35 on the settlement date of the futures contract but the futures price was $40, an investor could buy oil on the spot market and simultaneously sell futures contracts. The buyers of the futures contract would have to accept delivery of oil at $40, which would allow the investor to make a risk-free profit of $5 per barrel. In practice, investors selling additional futures contracts would drive down the futures price until it equaled the spot price. Only then would the ability to make a profit disappear.

Unlike with the spot market, buyers and sellers in the futures market may not be involved with either pumping or using oil. Instead, they may be investors who hope to profit by placing a bet on which way the price of oil will change in the future. These market participants are called speculators. Speculators serve the useful purpose of adding to the number of buyers and sellers in the futures market, thereby increasing market liquidity, which is the ease with which a buyer or seller can sell an asset, such as a futures contract.

You can speculate on the price of oil using the futures market in oil. If you believe that the futures price is lower than the spot price of oil will be on the settlement date, you can hope to make a profit by buying futures contracts today and selling them after the price rises. Similarly, if you believe that the futures prices is higher than the price of oil will be in the spot market on the settlement date, you can sell futures contracts at the current high price and buy them back after the price has fallen. It’s important to understand that investors doing this type of buying and selling of futures contracts don’t expect to actually deliver or receive barrels of oil.

What Happened in the Oil Market in April 2020?

Ordinarily, when firms pumping oil expect prices to be significantly higher in the future, they can respond by withholding oil from the market in several ways: (1) They can reduce the quantity of oil they pump, in effect storing it in the ground until prices increase; (2) they can pump oil and store it until prices rise; and (3) they can store oil products like gasoline that are refined from oil on supertankers, which are capable of holding millions of barrels of oil, waiting for prices to rise.

But in the spring of 2020, the decline in demand was so large and so sudden that firms were uncertain how much to reduce the quantity of oil they were pumping. If the decline in demand was temporary, lasting only during the worst of the pandemic, firms that cut back too much would face both the cost of both closing and then reopening oil wells. In some cases, even temporarily stopping production from a well can permanently reduce how much oil can be recovered from the well. In addition, the usual places to store oil were rapidly reaching capacity. As an article in the Wall Street Journal put it: “The buildup of crude is overwhelming storage space and clogging pipelines. And in areas where tanker-ship storage isn’t readily available, producers could need to go to extremes to get rid of the excess.” The “extremes” included accepting negative prices.

On April 20, there was a second factor pushing oil prices into negative values. The May futures contract was expiring the next day, meaning that any buyer who had not sold the contract would legally have to pay for and accept delivery of 1,000 barrels of oil. As we’ve seen, some buyers and sellers of oil futures contracts are speculators who don’t intend to deliver or receive barrels of oil. Given the shortage of storage facilities, rather than accept delivery for oil with nowhere to put it, speculators were willing to take steep losses by selling their contracts at a negative price. In effect, a buyer of a contract received $37,000 ($37 per barrel × 1,000 barrels per contract) in addition to 1,000 barrels of oil—a great deal, but only if you had somewhere to store the oil.

If oil producers become convinced that the decline in demand is likely to be long-lived, they will reduce the supply of oil substantially and the spot price will rise enough to ensure that the producers are able to cover all of their costs. But the fact that the spot price of oil was briefly negative indicates the level of economic disruption the coronavirus caused.

Sources: Ryan Dezember, “U.S. Oil Costs Less Than Zero After a Sharp Monday Selloff,” Wall Street Journal, April 21, 2020; Neil Irwin, “What the Negative Price of Oil Is Telling Us,” New York Times, April 21, 2020; Myra P. Saefong, “Oil Market in ‘Super Contango’ Underlines Storage Fears as Coronavirus Destroys Crude Demand,” marketwatch.com, April 18, 2020; Benoit Faucon, Summer Said, and Timothy Puko, “U.S., Saudi Arabia, Russia Lead Pact for Record Cuts in Oil Output,” Wall Street Journal, April 12, 2020; Federal Reserve Bank of St. Louis; and U.S. Energy Information Administration.

Question:

If a futures market for oil didn’t exist, would the spot price of oil ever be negative?

If you were a manager of a firm that owns oil wells, how would you benefit from the existence of a futures market for oil? If you were a manager of a firm that buys oil to refine into gasoline, how would you benefit from the existence of a futures market for oil?

For Economics Instructors that would like the approved answers to the above questions, please email Christopher DeJohn from Pearson at christopher.dejohn@pearson.com and list your Institution and Course Number.

On April 17th, Glenn Hubbard and Tony O’Brien continued their podcast series by spending just under 30 minutes discuss varied topics such as the Federal Reserve’s monetary response, record unemployment numbers, panic buying of toilet paper as compared to bank runs, as well as recent books they’ve been reading with increased downtime from the pandemic.

Supports: Chapter 12 in Economics and Microeconomics – Firms in Perfectly Competitive Markets; Essentials Chapter 9.

SOLVED PROBLEM: HOW WILL THE CORONAVIRUS PANDEMIC AFFECT THE AIRLINE INDUSTRY?

During the coronavirus pandemic, many airlines experienced a sharp decline in ticket sales. Some airlines responded by cutting ticket prices to very low levels. For example, in early March, Frontier Airlines was offering round-trip tickets from New York City to Miami for $51 (compared to over $200 three months earlier). As one columnist in the Wall Street Journal put it, the price of many airline tickets was “cheaper than dinner or what you’ll spend on Ubers or taxis.”

Briefly explain whether it was likely that the price Frontier was charging was high enough to cover the average total cost of a flying an airplane from New York City to Miami. Why was Frontier willing to accept such a low price? Would the airline be willing to accept such a low price in the long run?

Some airlines believed that even after the pandemic was over, consumers might not be willing to fly on planes as crowded as they were prior to the pandemic. Accordingly, airlines were considering either flying planes with some rows kept empty or reconfiguring planes to have more space between rows—and therefore fewer seats per plane. Briefly explain what effect having fewer seats per airplane might have on the price of an airline ticket.

Sources: Jonathan Roeder, “NYC to Miami for $51: Coronavirus Slump Leads to Steep Airfare Discounts,” bloomberg.com, March 5, 2020; and Scott McCartney, “There Are Plenty of Coronavirus Flight Deals Out There, But Think Before You Buy,” Wall Street Journal, March 25, 2020.

Solving the Problem

Step 1: Review the chapter material. This problem is about the break-even price for a firm in the short run and in the long run, so you may want to review Chapter 12, Section 12.4 “Deciding Whether to Produce or to Shut Down in the Short Run” and Section 12.5 “‘If Everyone Can Do It, You Can’t Make Money at It’: The Entry and Exit of Firms in the Long Run.”. In Hubbard/O’Brien, Essentials of Economics, it is Chapter 9.

Step 2: Answer part a. by explaining why even though a ticket price of $51 was unlikely to cover the average total cost of the flight, Frontier Airlines was still willing to accept such a low ticket price—but only in the short run. As we’ve seen in Section 12.5, competition among firms drives the price of a good to equal the average total cost of the typical firm. Assuming that ticket prices prior to the pandemic equaled average total cost, then the low ticket prices in the spring of 2020 must have been below average total cost. We have also seen, though, that firms will continue to produce in the short run provided they receive a price equal to or greater than average variable cost. For a particular flight, the fixed cost—primarily the cost of aviation fuel and the salaries of the flight crew—is much greater than the variable cost—additional meals served, somewhat more fuel used because more passengers make the plane heavier, and possibly an additional flight attendant needed to assist additional passengers. So, the $51 ticket price may have been enough for Frontier to cover its average variable cost. The airline would not accept such a low price in the long run, though, because in the long run it would need to cover all of its costs or it would no longer fly the route. (Note: In the short run, an airline might have another reason to continue to fly planes on a route even if it is unable to cover the average total cost of a flight. The contracts that airlines have with airports sometimes require a specified number of flights each day in order for the airline to retain the right to use certain airport gates.)

Step 3: Answer part b. by explaining the effect that having fewer seats per airplane would have on airline ticket prices. For an airline to break even on a flight, its total revenue from the flight must equal its total cost. Flying fewer seats per plane will not greatly reduce the airline’s cost of the flight because, as noted in the answer to part b., most of the cost of a flight is fixed and so the total cost of a flight doesn’t vary much with the number of passengers on the flight. But flying half as many passengers—if every other row is left empty—will significantly decrease the revenue the airline earns from the flight. To increase revenue on the flight, the airline would have to increase the price of a ticket. We can conclude that if airlines decide to fly planes equipped with fewer seats, ticket prices are likely to rise. Note that if on some routes the demand for tickets is price elastic, raising the price will reduce revenue and the airline will be unable to cover its cost of flying the route.