Supports: Econ and Micro: Chapter 8, “Firms, the Stock Market, and Corporate Governance” Macro Chapter 6; Essentials Chapter 6

The Futures market and the strange case of negative price of oil

There’s a point that seems so obvious that we haven’t explicitly mentioned it until now: The price of a good or service is always positive. After all, a price being negative means that a seller is paying a buyer to accept a good or service, which seems very unlikely. But this strange outcome did occur in the U.S. oil market during the economic upheaval caused by the coronavirus pandemic of 2020.

In the spring of 2020, there were two important developments in the world oil market:

- A sharp decline in demand Many countries imposed social-distancing protocols and required non-essential business to shut down in response to the pandemic. These policies caused the demand for oil products to decline dramatically. For instance, in the United States, the demand for gasoline fell by about 50 percent between the middle of March and the middle of April. The decline was the largest in history over such a short period.

- A decline in world supply Twenty-three countries, including the United States, Russia, and Saudi Arabia—the world’s three largest oil producer—agreed to reduce oil production by 9.7 million barrels per day, or about 13 percent of daily world production. These countries hoped that the decline in supply would keep the world price of oil from falling to very low levels. In fact, though, through mid-April the decline in demand was larger than the decline in supply leading to a dramatic decline in oil prices.

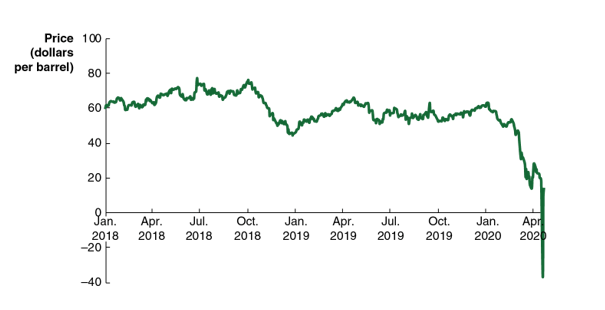

Crude oil from different rock formations can vary in its characteristics, such as its sulfur content. Crude oil that requires more processing as it is being refined into gasoline, aviation fuel, or other products, sells for a lower price. The benchmark oil price in the United States is for a grade of crude oil called West Texas Intermediate. The following figure shows the fluctuations in the price per barrel of this type of oil from January 2018 through late April 2020.

After reaching a high of $63 per barrel in January 2020, the price of oil declined to negative $37 per barrel on April 20. In other words, sellers were willing to pay buyers $37 per barrel to accept delivery of oil. Why would a seller ever pay someone to accept a product? There are two related reasons. We can discuss the first reason using demand and supply analysis. The second reason requires a brief discussion of how the oil market is different from most other markets for goods.

Demand and Supply in the Spot Market for Oil

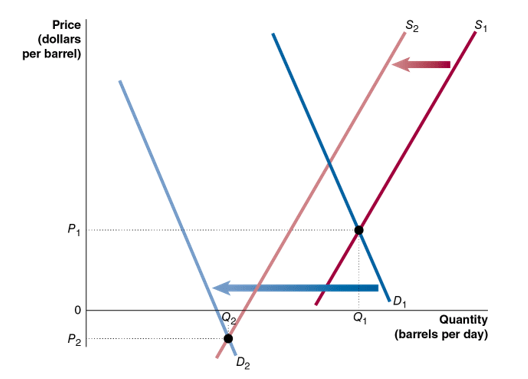

To understand how movements in demand and supply in the oil market resulted in a negative price, consider the following figure illustrating this situation. Before the coronavirus pandemic, the demand for oil is shown by demand curve D1 and the supply of oil by supply curve S1. The equilibrium price is P1. During the pandemic, the amount of oil demanded declined sharply from D1 to D2, and the supply of oil declined from S1 to S2. As a result, the new equilibrium price became negative at P2. We can see that for the equilibrium price to be negative, the demand curve and supply curve must intersect below the horizontal axis.

But why would a firm be willing to supply any oil at a negative price? The answer requires understanding how oil markets work. The spot price of oil is the price for oil that is available for immediate delivery. A seller at the spot price is typically a firm pumping oil, and a buyer is a firm that uses oil as an input, such as a firm that refines oil into gasoline. When you buy bread in the supermarket or a Big Mac at McDonald’s you are paying the spot price, which is the only price in the markets for most goods and services. In the figure we are showing the spot market for oil and the price is the spot price.

The Futures Market for Oil

But in addition to a spot market for oil, there is a futures market for oil, which allows individuals and firms to buy and sell futures contracts. A futures contract specifies the quantity of an asset—such as a barrel of oil—that will be delivered by the seller on a future date, the settlement date. Futures contracts exist for commodities such as oil, as well as for financial assets, such as Treasury bonds and stock indexes like the S&P 500. Futures contracts don’t set the price—the futures price—that the buyer will pay and the seller will receive on the settlement date. Instead, the price fluctuates as the contract is bought and sold on a futures exchange, such as the Chicago Board of Trade or the New York Mercantile Exchange, just as the price of a share of stock fluctuates as the stock is bought and sold in the stock market. Each oil futures contract represents 1,000 barrels (or 42,000 gallons) of oil.

The futures price of oil can differ from the spot price if people trading futures contracts expect that conditions in the oil market will differ on the settlement date from conditions today. For instance, on April 20, 2020, the date on which the spot price of oil was negative, the oil futures price on a contract with a settlement date in June was $22 per barrel and the price on a contract with a settlement date in November was $33 per barrel. The higher oil prices for June and November reflected the view among buyers and sellers and futures contracts that (1) the economy was likely to begin recovering from the worst of the pandemic by then, increasing the demand for oil and (2) the supply of oil was likely to decline further.

The spot price and the futures price are linked because it’s possible to store oil. So, the futures price should roughly equal the spot price plus the cost of storing oil between today and the settlement date of the futures contract. As the settlement date approaches, the futures price comes closer to the spot price, eventually equaling the spot price on the settlement date. Why must the spot price equal the futures price on the settlement date? Because if there were a difference between the two prices, it would be possible for an investor to make a profit. For instance, if the spot price of oil was $35 on the settlement date of the futures contract but the futures price was $40, an investor could buy oil on the spot market and simultaneously sell futures contracts. The buyers of the futures contract would have to accept delivery of oil at $40, which would allow the investor to make a risk-free profit of $5 per barrel. In practice, investors selling additional futures contracts would drive down the futures price until it equaled the spot price. Only then would the ability to make a profit disappear.

Unlike with the spot market, buyers and sellers in the futures market may not be involved with either pumping or using oil. Instead, they may be investors who hope to profit by placing a bet on which way the price of oil will change in the future. These market participants are called speculators. Speculators serve the useful purpose of adding to the number of buyers and sellers in the futures market, thereby increasing market liquidity, which is the ease with which a buyer or seller can sell an asset, such as a futures contract.

You can speculate on the price of oil using the futures market in oil. If you believe that the futures price is lower than the spot price of oil will be on the settlement date, you can hope to make a profit by buying futures contracts today and selling them after the price rises. Similarly, if you believe that the futures prices is higher than the price of oil will be in the spot market on the settlement date, you can sell futures contracts at the current high price and buy them back after the price has fallen. It’s important to understand that investors doing this type of buying and selling of futures contracts don’t expect to actually deliver or receive barrels of oil.

What Happened in the Oil Market in April 2020?

Ordinarily, when firms pumping oil expect prices to be significantly higher in the future, they can respond by withholding oil from the market in several ways: (1) They can reduce the quantity of oil they pump, in effect storing it in the ground until prices increase; (2) they can pump oil and store it until prices rise; and (3) they can store oil products like gasoline that are refined from oil on supertankers, which are capable of holding millions of barrels of oil, waiting for prices to rise.

But in the spring of 2020, the decline in demand was so large and so sudden that firms were uncertain how much to reduce the quantity of oil they were pumping. If the decline in demand was temporary, lasting only during the worst of the pandemic, firms that cut back too much would face both the cost of both closing and then reopening oil wells. In some cases, even temporarily stopping production from a well can permanently reduce how much oil can be recovered from the well. In addition, the usual places to store oil were rapidly reaching capacity. As an article in the Wall Street Journal put it: “The buildup of crude is overwhelming storage space and clogging pipelines. And in areas where tanker-ship storage isn’t readily available, producers could need to go to extremes to get rid of the excess.” The “extremes” included accepting negative prices.

On April 20, there was a second factor pushing oil prices into negative values. The May futures contract was expiring the next day, meaning that any buyer who had not sold the contract would legally have to pay for and accept delivery of 1,000 barrels of oil. As we’ve seen, some buyers and sellers of oil futures contracts are speculators who don’t intend to deliver or receive barrels of oil. Given the shortage of storage facilities, rather than accept delivery for oil with nowhere to put it, speculators were willing to take steep losses by selling their contracts at a negative price. In effect, a buyer of a contract received $37,000 ($37 per barrel × 1,000 barrels per contract) in addition to 1,000 barrels of oil—a great deal, but only if you had somewhere to store the oil.

If oil producers become convinced that the decline in demand is likely to be long-lived, they will reduce the supply of oil substantially and the spot price will rise enough to ensure that the producers are able to cover all of their costs. But the fact that the spot price of oil was briefly negative indicates the level of economic disruption the coronavirus caused.

Sources: Ryan Dezember, “U.S. Oil Costs Less Than Zero After a Sharp Monday Selloff,” Wall Street Journal, April 21, 2020; Neil Irwin, “What the Negative Price of Oil Is Telling Us,” New York Times, April 21, 2020; Myra P. Saefong, “Oil Market in ‘Super Contango’ Underlines Storage Fears as Coronavirus Destroys Crude Demand,” marketwatch.com, April 18, 2020; Benoit Faucon, Summer Said, and Timothy Puko, “U.S., Saudi Arabia, Russia Lead Pact for Record Cuts in Oil Output,” Wall Street Journal, April 12, 2020; Federal Reserve Bank of St. Louis; and U.S. Energy Information Administration.

Question:

- If a futures market for oil didn’t exist, would the spot price of oil ever be negative?

- If you were a manager of a firm that owns oil wells, how would you benefit from the existence of a futures market for oil? If you were a manager of a firm that buys oil to refine into gasoline, how would you benefit from the existence of a futures market for oil?

For Economics Instructors that would like the approved answers to the above questions, please email Christopher DeJohn from Pearson at christopher.dejohn@pearson.com and list your Institution and Course Number.