Image generated by ChatGPT

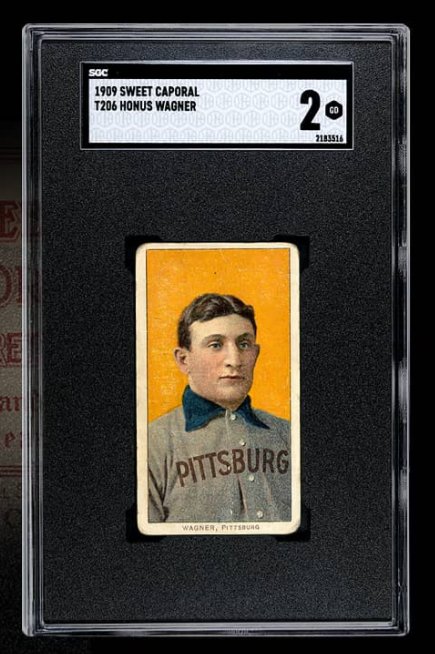

People have collected sports cards for decades. For many years, the most sought-after and highest-priced example was a baseball card featuring Pittsburgh Pirates shortstop Honus Wagner. In the early twentieth century, baseball cards were often included in packs of cigarettes. In 1909, each pack of Sweet Caporal Cigarettes included a baseball card from what collectors call the T206 set. Although Wagner was a major star, relatively few of his cards were issued. That may have been because he was opposed to tobacco use and didn’t want his card to help sell cigarettes or because the tobacco company declined to pay him the fee he required.

There are probably only 50 to 60 Wagner cards in existence. In August 2022, the Wagner card shown below sold at auction for $7.25 million, which was at the time a record.

Image from goldin.co

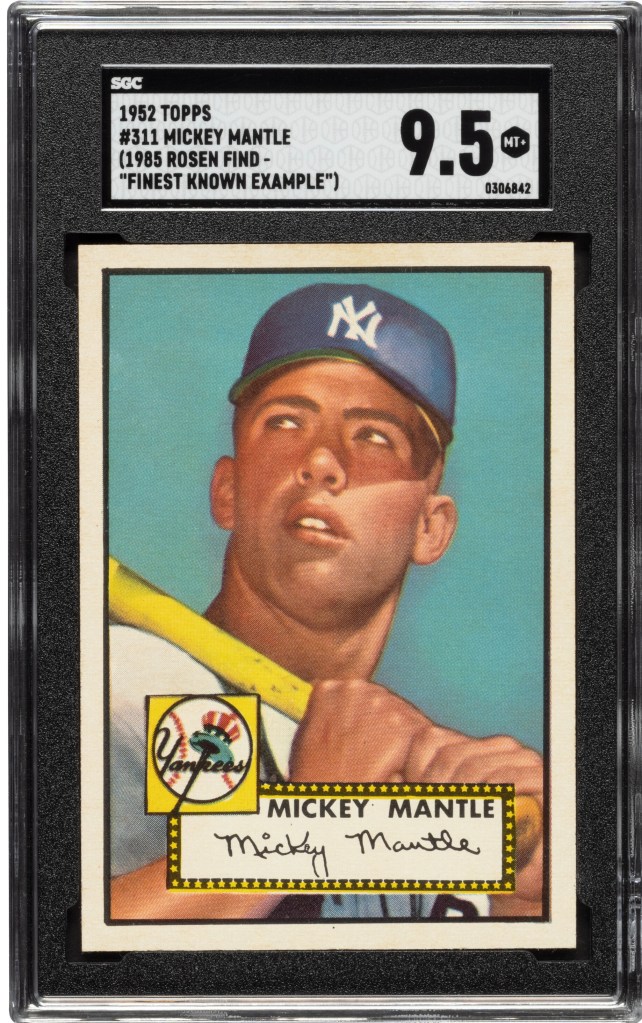

This record was broken a few days later when the Topps rookie card for New York Yankees outfielder Mickey Mantle sold for $12.6 million.

Image from ha.com

A new record as the highest-priced sports card was set in August 2025, when a card featuring basketball stars Michael Jordan and Kobe Bryant sold for $12.932 million.

Image from ha.com

In recent years, collecting cards from trading card games (TCG) such as Magic: The Gathering, Yu-Gi-Oh!, and, especially, Pokémon has become increasingly popular. Collectors pay higher prices for cards that are in nicer condition. Accordingly, many collectors and dealers submit cards to grading companies that assign the cards a numerical grade, with 10 being the highest grade. The leading card grading company is Professional Sports Authenticator (PSA). Despite its name, PSA now grades more TCG cards than sports card. In 2025, PSA graded 11.5 million TCG cards and 7.7 million sports cards.

In February of this year, a rare PSA-graded 1998 Japanese Pikachu Illustrator Pokémon card with a perfect grade of 10 sold for $16.492 million.

Image from goldin.co

The increasing popularity of collecting TCG cards and the publicity from media reports of the high sales prices of some cards has led to a surge in submissions to card grading companies. PSA is the largest card grading company, grading nearly four times as many cards as its closest competitor. Card grading fees increase with the market value of the card being graded. PSA charges significantly higher prices than its competitors. Collectors are apparently willing to pay the higher prices because PSA-graded cards often sell for higher prices than do cards graded by competitors.

On May 28, PSA surprised many card collectors by announcing that its backlog of cards collectors had submitted but that the company had not yet graded had reached 10 million. As a result, the company stated it was no longer accepting new submissions of lower priced cards. (Cards submitted to its Value Bulk, Value, Value Plus, and Value Max tiers.) The company described the policy as a “temporary pause” that would remain in place until its backlog of ungraded cards had declined to 5 million. PSA estimated that it would take four months to reach that target.

Why did PSA allow its backlog of ungraded cards to grow to 10 million? The backlog is an indication that at the prices it was charging, the quantity of its grading services demanded was much greater than the quantity of grading services it could supply with its existing workforce and grading equipment. Why, then, didn’t it raise its prices to reduce the quantity of its grading services demanded?

In Microeconomics, Chapter 10, Section 10.3, we describe several examples of firms being a situation similar to the one PSA finds itself in. In these situations, firms choose not to raise their prices even though doing so would seem to increase their profits. As we discuss in that chapter, the key reason firms don’t raise prices is they believe their customers might see the price increases as being unfair.

We thought it would be interesting to ask ChatGPT to analyze why PSA didn’t raise its prices when faced with a rapidly expanding backlog of ungraded cards. Here’s ChatGPT’s—lengthy!—answer to this economic puzzle:

Image generated by ChatGPT

They probably could have raised price enough to slow submissions, but that would not have solved the whole problem PSA was trying to solve.

In the current 2026 pause, PSA said Value Bulk, Value, Value Plus, and Value Max submissions were being paused because a surge added 1.6 million cards and pushed the active backlog toward 10 million; PSA’s stated goal is to reduce that backlog to 5 million before reopening those tiers. In other words, the target was not “new submissions = grading capacity.” The target was new submissions well below capacity so the existing queue could shrink.

The clean economic answer is:

1. A market-clearing price would only stop the backlog from getting worse.

Suppose PSA can grade 90,000 cards per day, a capacity figure PSA itself recently gave for global output. If they priced submissions so exactly 90,000 new cards arrived per day, the backlog would not fall; it would stay stuck. To reduce a 10-million-card backlog to 5 million, they need throughput to exceed incoming volume by millions of cards over the pause period. That means they needed rationing that was stronger than ordinary price clearing.

2. They actually did use price rationing, just in a blunt tiered way.

PSA did not close everything. It paused the lower-priced value tiers and left Regular, Express, Super Express, Walk-Through, and premium services open. PSA’s own pricing page shows Regular at $79.99/card, Express at $149/card, Super Express at $349/card, Walk-Through at $599/card, and premium tiers much higher. Baseball America summarized the effect as PSA temporarily pausing all card grading tiers under $80. So one way to read the move is: PSA effectively raised the minimum direct price for new card grading to the Regular tier, while refusing to call the paused Value tiers “available at a surge price.”

3. The demand curve was probably unstable and hard to estimate.

A normal market-clearing price assumes the firm can predict how many units will arrive at each price. PSA’s demand was not behaving smoothly. In 2021, after a price increase, PSA still reported receiving more cards in three days than it had received in the prior three months. In 2026, PSA said updated turnaround/service announcements were followed by another rapid demand spike. In that environment, “raise the price until volume equals capacity” is not simple, because each price change can trigger a rush, panic submissions, dealer behavior, and speculation.

4. A huge price increase would damage the brand more than a pause.

If PSA had said, “Value Bulk is still open, but now it costs $80, $120, or $200 per card,” many collectors would view that as gouging, especially because value-tier grading is used for lower-value cards. A pause lets PSA say, “we are protecting turnaround times and existing customers,” rather than “we are monetizing a bottleneck.” PSA explicitly framed the 2026 pause as a way to avoid compromising existing orders and to focus on cards already in its care.

5. Grading quality is part of the product.

PSA is not just selling a slot in a queue; it is selling trust in the grade. If a backlog forces rushed hiring, rushed training, overloaded receiving, or inconsistent review, the long-term asset — confidence in PSA 10, PSA 9, etc. — can be worth more than the short-term revenue from accepting every card at a higher price. PSA’s own statement tied the pause to protecting the “integrity of the PSA standard.”

6. A pause is easier to reverse than a surge-price regime.

A temporary stop says: “These tiers are closed until backlog conditions improve.” A giant price hike creates other problems: customers anchor to the new price, dealers renegotiate, memberships lose value, submitters complain when prices later fall, and competitors can market PSA as exploitative. PSA instead extended Collectors Club memberships during the pause, which suggests they were trying to preserve customer goodwill while reducing intake.

So the best answer is: because the bottleneck was a stock problem, not just a flow problem. Raising prices enough to make new submissions equal daily capacity would still leave the backlog in place. To drain the backlog, PSA needed submissions below capacity; pausing the cheapest/highest-volume tiers achieved that more predictably, while keeping high-value urgent tiers open and avoiding the optics of extreme surge pricing.