In June, the U.S. Census Bureau released its population estimates for 2024. Included was the following graphic showing the change in the U.S. population pyramid from 2004 to 2024. As the graphic shows, people 65 years and older have increased as a fraction of the total population, while children have decreased as a fraction of the total population. (The Census considers everyone 17 and younger to be a child.) Between 2004 and 2024, people 65 and older increased from 12.4 percent of the population to 18.0 percent. People younger than 18 fell from 25.0 percent of the population in 2004 to 21.5 percent in 2024.

The aging of the U.S. population reflects falling birth rates. Demographers and economists typically measure birth rates as the total fertility rate (TFR), which is defined by the World Bank as: “The number of children that would be born to a woman if she were to live to the end of her childbearing years and bear children in accordance with age-specific fertility rates currently observed.” The TFR has the advantage over the simple birth rate—which is the number of live births per thousand people—because the TFR corrects for the age structure of a country’s female population. Leaving aside the effects of immigration and emigration, a TFR of 2.1 is necessary to keep a country’s population stable. Stated another way, a country needs a TFR of 2.1 to achieve replacement level fertility. A country with a TFR above 2.1 experiences long-run population growth, while a country with a TFR of less than 2.1 experiences long-run population decline.

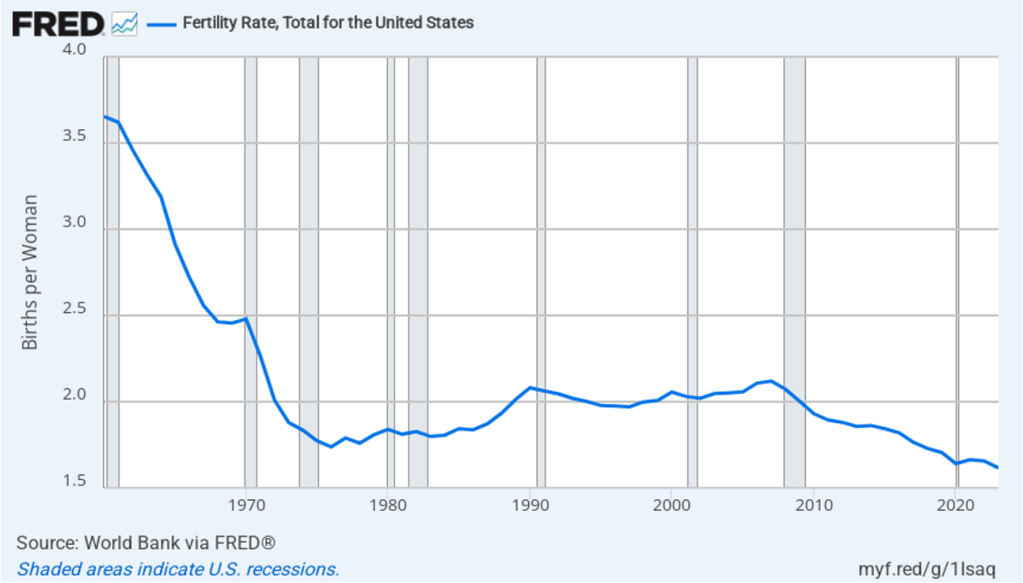

The following figure shows the TFR for the United States for each year between 1960 and 2023. Since 1971, the TFR has been below 2.1 in every year except for 2006 and 2007. Immigration has helped to offset the effects on population growth of a TFR below 2.1.

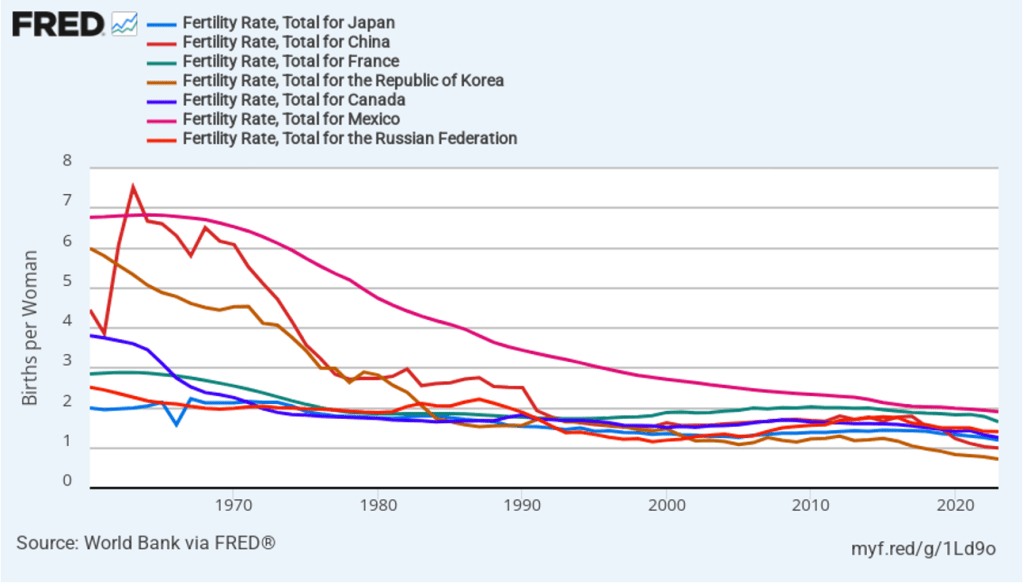

The United States is not alone in experiencing a sharp decline in its TFR since the 1960s. The following figure shows some other countries that currently have below replacement level fertility, including some countries—such as China, Japan, Korea, and Mexico—in which TFRs were well above 5 in the 1960s. In fact, only a relatively few countries, such as Israel and some countries in sub-Saharan Africa are still experiencing above replacement level fertility.

An aging population raises the number of retired people relative to the number of workers, making it difficult for governments to finance pensions and health care for older people. We discuss this problem with respect to the U.S. Social Security and Medicare programs in an Apply the Concept in Macroeconomics, Chapter 16 (Economics, Chapter 26 and Essentials of Economics, Chapter 18). Countries experiencing a declining population typically also experience lower rates of economic growth than do countries with growing populations. Finally, as we discuss in an Apply the Concept in Microeconomics, Chapter 3, different generations often differ in the mix of products they buy. For instance, a declining number of children results in declining demand for diapers, strollers, and toys.

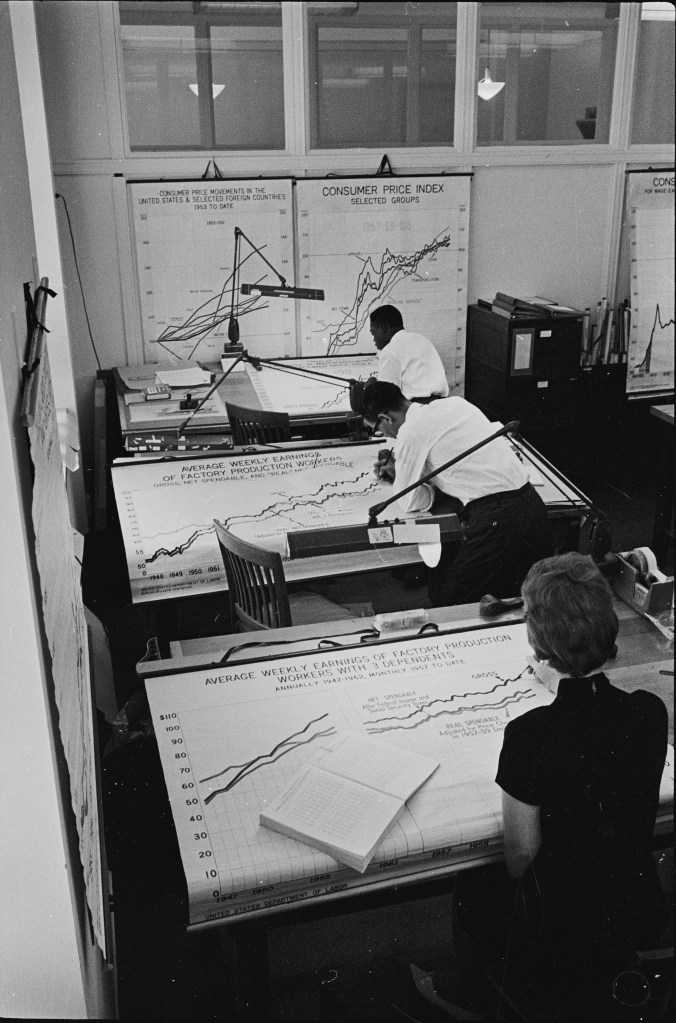

… there were artists in government agencies drawing time series graphs. As we discuss in this recent blog post, the Bureau of Labor Statistics (BLS) has been in the news lately—undoubtedly much more than the people who work there would like.

This post is not about the current controversy but steps back to make a bigger point: The availability of data has increased tremendously from the time when Glenn and Tony began their academic careers. In the 1980s, personal computers were becoming widespread, but the internet had not yet developed to the point where government statistics were available to download. To gather data usually required a trip to the university library to make photocopies of tables in the print publications of the BLS and other government agencies. You then had to enter the data by hand into very crude—by current standards—spreadsheet and statistical software. The software generally had limited graphing capabilities.

How were the time series figures in print government publications generated? The two photos shown above (both from the website of the Library of Congress) show that the figures were hand drawn by artists. The upper photo is from 1962 and the lower photo is from 1971.

Today, most government data is readily available online. The FRED (Federal Reserve Economic Data) site, hosted by economists at the Federal Reserve Bank of St. Louis makes available thousands of data series. We make use of these series in the Data Exercises included in the end-of-chapter problems in our textbooks. The FRED site makes it easy (we hope!) to do these exercises, including by combining or otherwise transforming data series and by graphing them—no artistic ability required!

Supports:Microeconomics and Economics, Chapter 15, Section 15.5, and Essentials of Economics, Chapter 10, Section 10.5

Image generated by ChatGTP 03

According to a recent article in the Economist, some U.S. airlines have “started charging higher per-person fares for single-passenger bookings than for identical itineraries with two people.” However, the difference in fares held only for round-trip tickets that included a weekday return flight. For round-trip tickets with a return flight on Saturday, the per-ticket price was the same whether booking for two people or for one person. Briefly explain why an airline might expect to increase its profit using this pricing strategy.

Step 1: Review the chapter material. This problem is about firms using price discrimination, so you may want to review Chapter 15, Sections 15.5

Step 2: Answer the question by explaining why an airline might expect to increase its profit by charging people traveling alone a higher ticket price than the price it charges per ticket to two people traveling together. The airline is attempting to increase its profit by using price discrimination. Price discrimination involves charging different prices to different customers for the same good or service when the price difference isn’t due to differences in cost. Firms who able to price discriminate increase their profits by doing so.

In Chapter 15, Section 15.5, we call the airlines the “kings of price discrimination” because they often charge many different prices for tickets on the same flight. One key way that airlines practice price discrimination is by charging higher prices to business travelers—who are likely to have a lower price elasticity of demand—than to leisure travelers—who are likely to have a higher price elasticity of demand. To employ this strategy, airlines have to successfully identify which flyers are business travelers. Someone flying alone is more likely than someone flying in a group of two or more people to be a business traveler. In addition, business travelers often attempt to complete their trips before the weekend. Therefore, people returning from a trip on a Saturday or Sunday are more likely to be leisure travelers.

We can conclude that an airline can expect to increase its profit using the pricing strategy discussed in the Economist article because the strategy helps the airline to better identify business travelers.

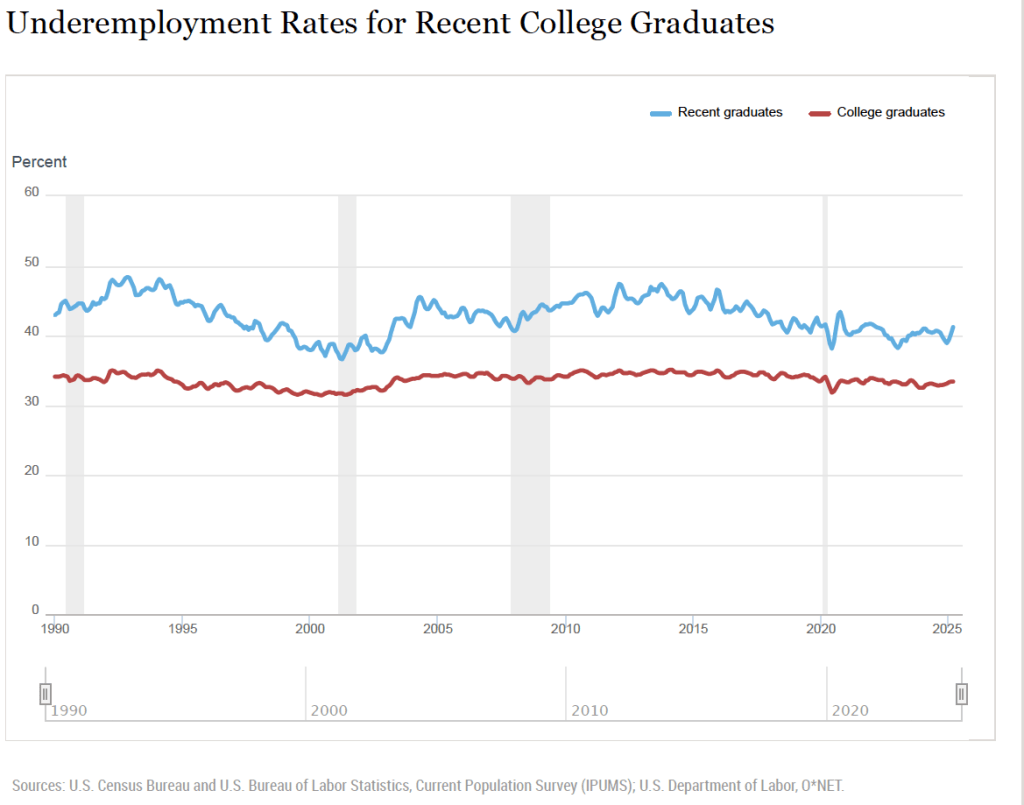

A number of news stories have highlighted the struggles some recent college graduates have had in finding a job. A report earlier this year by economists Jaison Abel and Richard Deitz at the Federal Reserve Bank of New York noted that: “The labor market for recent college graduates deteriorated noticeably in the first quarter of 2025. The unemployment rate jumped to 5.8 percent—the highest reading since 2021—and the underemployment rate rose sharply to 41.2 percent.” The authors define “underemployment” as “A college graduate working in a job that typically does not require a college degree is considered underemployed.”

The following figure shows data on the unemployment rate for people ages 20 to 24 years (red line) with a bachelor’s degree, the unemployment rate for people ages 25 to 34 years (blue line) with a bachelor’s degree, and the unemployment rate for the whole population (green line) whatever their age and level of education. (Note that the values for college graduates are for those people who have a bachelor’s degree but no advanced degree, such as a Ph.D. or an M.D.)

The figure shows that unemployment rates are more volatile for both categories of college graduates than the unemployment rate for the population as a whole. The same is true for the unemployment rates for nearly any sub-category of the unemployed lagely because the number of people included the sub-categories in the Bureau of Labor Statistics (BLS) household survey is much smaller than for the population as a whole. The figure shows that, over time, the unemployment rates for the youngest college graduates is nearly always above the unemployment rate for the population as a whole, while the unemployment rate for college graduates 25 to 34 years old is nearly always below the unemployment rate for the population as a whole. In June of this year, the unemployment rate for the population as a whole was 4.1 percent, while the unemployment for the youngest college graduates was 7.3 percent.

Why is the unemployment rate for the youngest college graduates so high? An article in the Wall Street Journal offers one explanation: “The culprit, economists say, is a general slowdown in hiring. That hasn’t really hurt people who already have jobs, because layoffs, too, have remained low, but it has made it much harder for people who don’t have work to find employment.” The following figure shows that the hiring rate—defined as the number of hires during a month divided by total employment in that month—has been falling. The hiring rate in June was 3.4 per cent, which—apart from two months at the beginning of the Covid pandemic—is the lowest rate since February 2014.

Abel and Deitz, of the New York Fed, have calculated the underemployment for new college graduates and for all college graduates. These data are shown in the following figure from the New York Fed site. The definitions used are somewhat different from the ones in the earlier figures. The definition of college graduates includes people who have advanced degrees and the definition of young college graduates includes people aged 22 years to 27 years. The data are three-month moving averages.

The data show that the underemployment rate for both recent graduates and all graduates are relatively high for the whole period shown. Typically, more than 30 percent of all college graduates and more than 40 percent of recent college graduates work in jobs in which more than 50 percent of employees don’t have college degrees. The latest underemployment rate for recent graduates is the highest since March 2022. It’s lower, though, than the rate for most of the period between the Great Recession of 2007–2009 and the Covid recession of 2020.

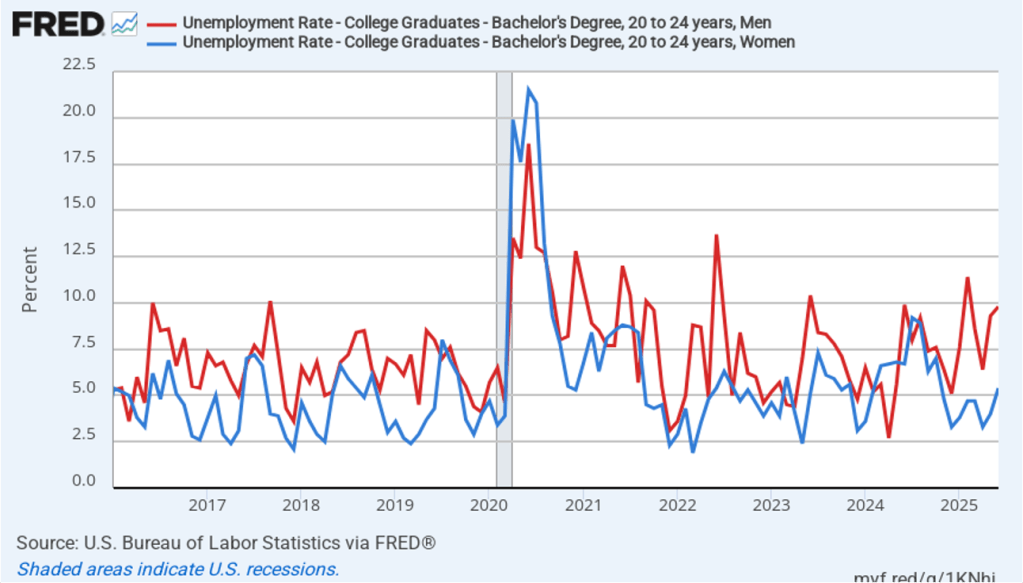

In a recent article, John Burn-Murdoch, a data journalist for the Financial Times, has made the point that the high unemployment rates of recent college graduates are concentrated among males. As the following figure shows, in recent months, unemployment rates among male college graduates 20 to 24 years old have been significantly higher than the unemployment rates among female college graduates. In June 2025, the unemployment rate for male recent college graduates was 9.8 percent, well above the 5.4 percent unemployment for female recent college graduates.

What explains the rise in male unemployment relative to female unemployment? Burn-Murdoch notes that, contrary to some media reports, the answer doesn’t seem to be that AI has resulted in a contraction in entry-level software coding jobs that have traditionally been held disproportionately by males. He presents data showing that “early-career coding employment is now tracking ahead of the [U.S.] economy.”

Instead he believes that the key is the continuing strong growth in healthcare jobs, which have traditionally been held disproportionately by females. The availability of these jobs has allowed women to fare better than men in an economy in which hiring rates have been relatively low.

Like most short-run trends, it’s possible that the relatively high unemployment rates experienced by recent college graduates may not continue in the long run.

Supports:Microeconomics, Macroeconomics, Economics, and Essentials of Economics, Chapter 4, Section 4.3

Image generated by ChatGTP-40 of a street in a Dutch city.

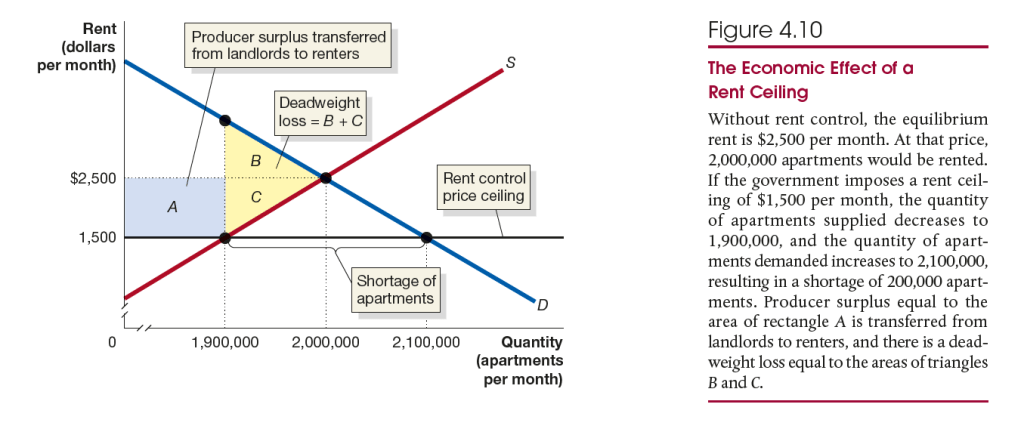

An article on bloomberg.com has the headline “How Rent Controls Are Deepening the Dutch Housing Crisis.” The article’s subheadline states that: “A law designed to make homes more affordable ended up aggravating an apartment shortage.” According to the article, the Dutch government passed a law that increased the number of apartments subject to rent control from 80% of all apartments to 96%.

Why might the Dutch government have seen expanding rent control as a way to make apartments more affordable?

Why might the law have aggravated the shortage of apartments in Holland?

Solving the Problem Step 1: Review the chapter material. This problem is about the effects of rent control, so you may want to review Chapter 4, Section 4.3, “Government Intervention in the Market: Price Floors and Price Ceilings.”

Step 2: Answer part a. by explaining why the Dutch government may have seen expanding rent control as a way to make apartments more affordable. Figure 4.10 from the textbook shows the effects of rent control. In the example illustrated in the figure, after the government imposes rent control, the 1,900,000 people who are still able to rent an apartment pay $1,500 per month rather than $2,500 per month. For these people, rent control has made apartments more affordable.

Step 3: Answer part b. by explaining why rent control laws can make an apartment shortage worse. As Figure 4.10 shows, rent control laws impose a price ceiling below the equilibrium market rent. The result is that the quantity of apartments supplied is less than the quantity of apartments demanded, causing a shortage of apartments. In the case of the Dutch law discussed in the article, existing rent controls were expanded to cover more apartments, forcing the rents charged by landlords for these apartments to fall below what had been the equilibrium market rent, thereby adding to the shortage of apartments in Holland.

Extra credit: The article notes that as a result of the law, some owners of apartments that had previously not been subject to rent control had decided to sell their apartments, taking them off the rental market. That result is common when governments impose rent control or expand the scope of an existing rent control law. One important aspect of rent control is that a shortage of apartments gives landlords a greater opportunity to pick and choose the tenants they prefer. The article notes that a provision of the new law requires that rental contracts be open-ended, rather than for only one or two years, as is more common. As a result, landlords have more difficulty evicting tenants who might be noisy or causing other problems. The law thereby gives landlords an incentive to rent to foreign tenants who would be more likely to give up their apartments voluntarily after a year or two. The result is even fewer apartments available for Dutch residents to rent.

A recent article on bloomberg.com notes that the negative consequences of the law expanding rent control has led the Dutch government to propose modifying the law to allow landlords to charge higher rents on at least some apartments. If passed by the Dutch parliment, the changes would go into effect January 1, 2026.

Supports:Microeconomics and Economics, Chapter 15, Section 15.5, and Essentials of Economics, Chapter 10, Section 10.5

Image generated by ChatGTP-4o

A national provider of cable television and internet service has been frequently criticized by customers on social media for using the following business strategy: The company raises its prices every six to nine months. Any subscriber who calls to complain is offered a discount off of the price increase. Analyze how this strategy can be profit mazimizing for the company.

Step 1: Review the chapter material. This problem is about firms using price discrimination, so you may want to review Chapter 15, Sections 15.5

Step 2: Answer the question by explaining how the cable company is using price discrimination to increase its profit. Price discrimination involves charging different prices to different customers for the same good or service when the price difference isn’t due to differences in cost. Firms who able to price discriminate increase their profits by doing so.

We’ve seen that there are three requirements for a firm to practice price discrimination: 1) The firm must possess market power, 2) some of the firm’s customers much have a greater willingness to pay for the product than do other customers, and 3) the firm must be able to segment the market to keep customers who buy the product at the low price from reselling it. Cable companies can meet all three requirements. Cable firms possess market power—they aren’t perfect competitors. Some customers have a higher willingness than other customers to pay for cable service. In fact, many people have become cable cutters and prefer to stream content rather than watch programs on cable. Finally, someone who receives a lower-priced cable subscription can’t resell it.

To increase profit by price discrimination, a firm needs to charger a higher price to customers with a lower price elasticity of demand, and a lower price to customers with a higher price elasticity of demand. People who call up to complain about an increase in the price of a cable subscription are likely to be more price sensitive—and, therefore, more likely to switch to a competing cable company or to cut the cable and switch to streaming—than are people who don’t complain about the increase in the price of a subscription. In other words, the complainers have a higher price elasticity of demand than do the non-complainers and receive a lower price. We can conclude that this business strategy is an example of price discrimination and will increase the profit of the cable company that uses it.

How does the number of people who majored in economics in college compare with the number of people who pursued other majors? How do the earnings of economics majors compare with the earnings of other majors? Recent data released by the Census Bureau provides some interesting answers to these and other questions about the economics major.

Each year the Census Bureau conducts the American Community Survey (ACS) by mailing a questionnaire to about 3.5 million households. The questionnaire contains 100 questions that ask about, among other things, the race, sex, age, educational attainment, employment, earnings, and health status of each person in the household. Responses are collected online, by mail, by telephone, or by a personal visit from a census employee.

Although the Census Bureau releases some data about 1 year after the data is collected, it typically takes longer to publish detailed studies of specific topics. The ACS report on Field of Bachelor’s Degree in the United States: 2022 was released this month, although it’s based on data collected during 2022. Anyone interested in the subject will find the whole report to be worthwhile reading, but we can summarize a few of the results.

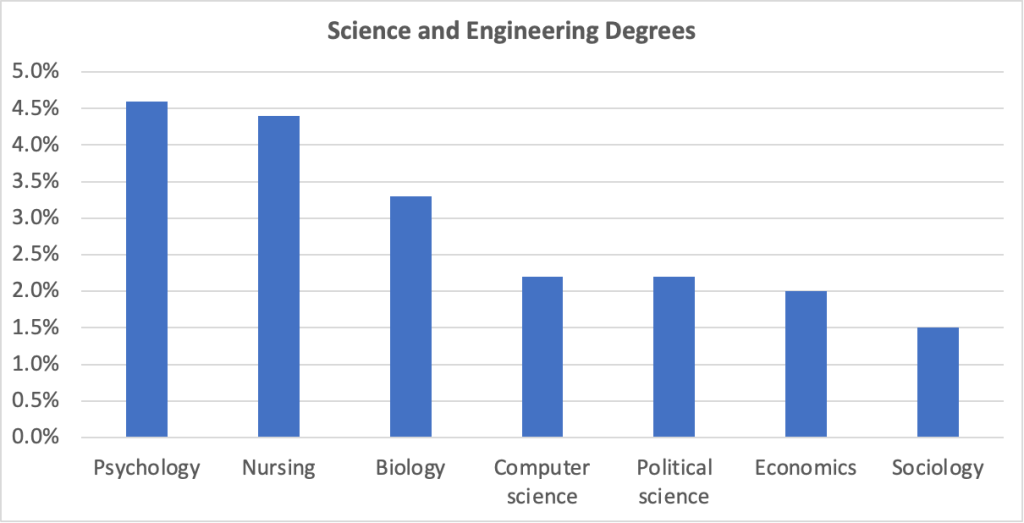

According to the census, in 2022, there were 81.9 million people in the United States aged 25 and older who had graduated from college with a bachelor’s degree. The report includes economics, along with several other social sciences—psychology, political science, and sociology—in the category of “Engineering and Science Degrees.” The following figure shows the leading majors in this category ranked by the percentage of all holders of a bachelor’s degree. (Sociology is included for comparison with the other three social sciences listed.) Psychology has the largest share of majors at 4.6 percent. Economics accounts for 2.0 percent of majors.

We can conclude that among social science majors, economics is less than half as popular as psychology, slightly less popular than political science, and significantly more popular than sociology.

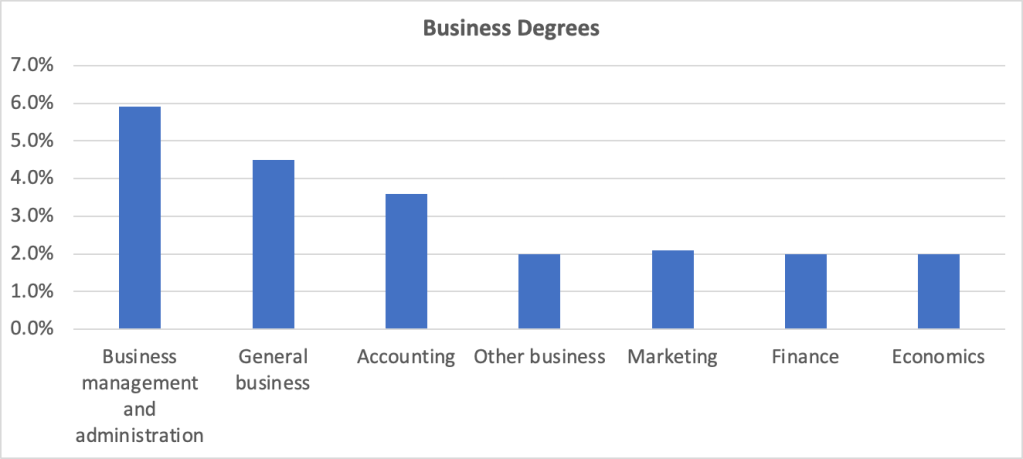

Economics departments are sometimes located in undergraduate business colleges. The following figure compares economics to other majors listed in the “Business Degrees” category of the report. At nearly 6 percent of all majors, “business management and administration” is the most popular of business majors, followed by general business and accounting. “Other business,” marketing, finance, and economics are all about equally popular with around 2 percent of all majors.

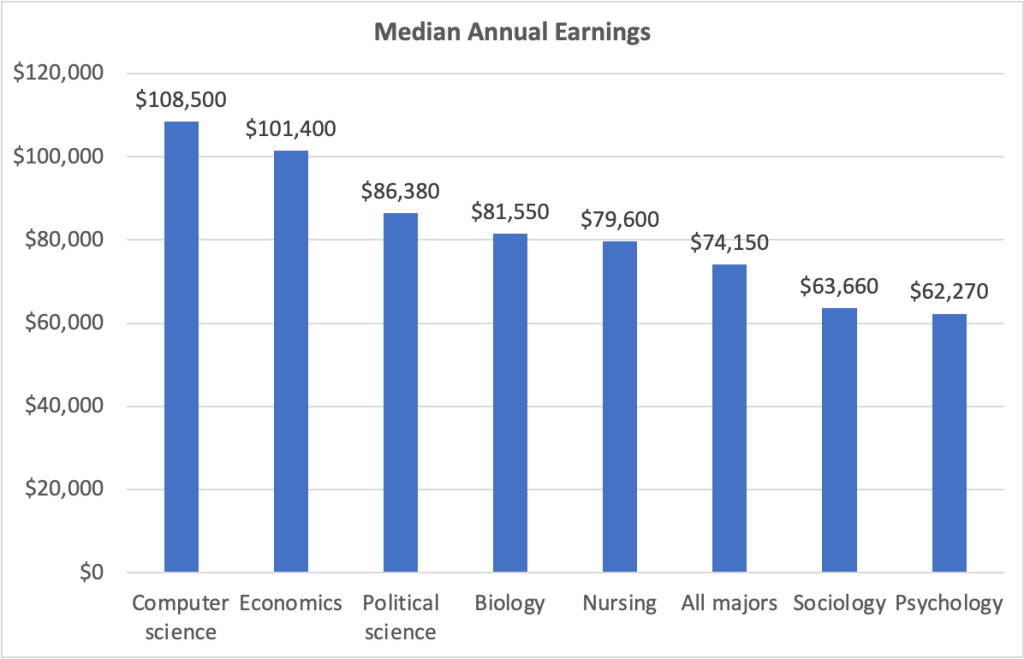

The figure below shows the median annual earnings for people aged 25 years to 64 years—prime-age workers—who majored in each of fields used in the first figure above, as well as for all holders of a bachelor’s degree. People who majored in economics earn significantly more than people who majored in the other social sciences listed and 35 percent more than people in all majors.

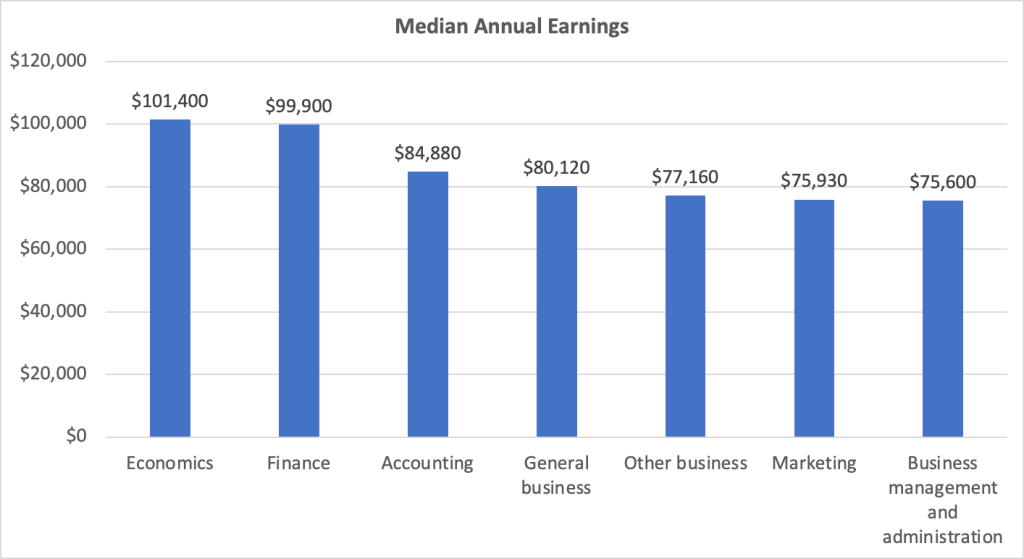

The next figure shows median annual earnings for economics majors compared with majors in other business fields. Perhaps surprisingly—although not to people who know the many benefits from majoring in economics!—economics majors earn more on average than do majors in other business fields.

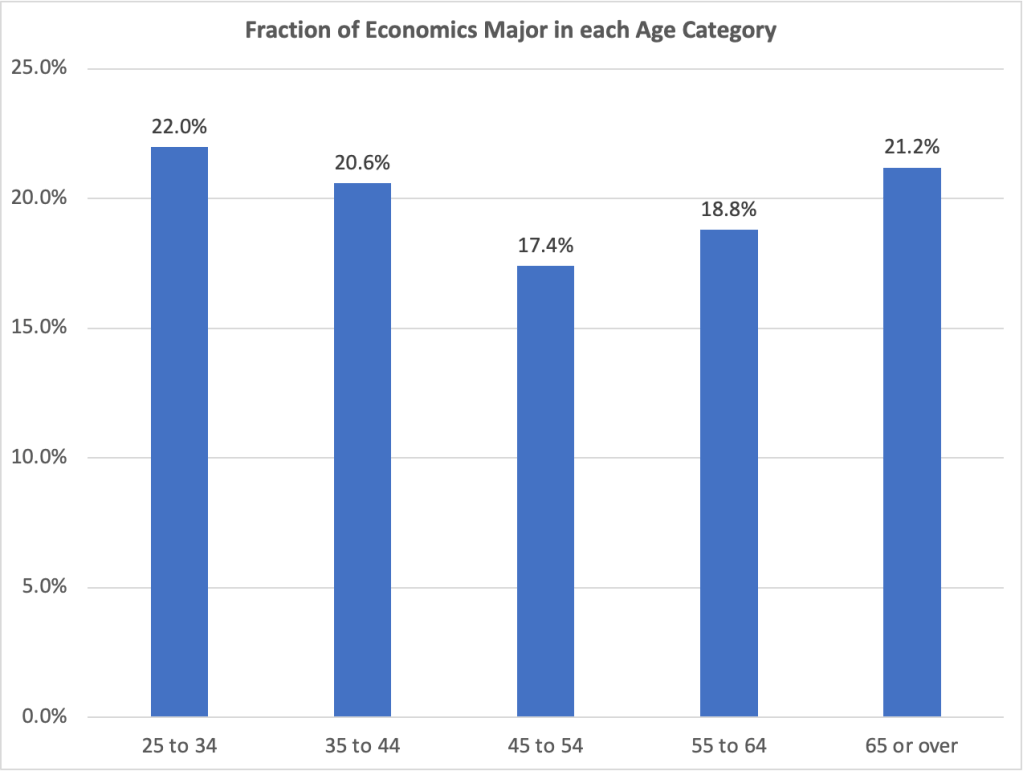

The following figure shows how many people with bacherlor’s degrees in economics majors fall into each age group. People aged 25 years to 34 years make up 22 percent of all economics majors, the most of any of the age groups. This result indicates that the economics major has gained in popularity (although note that the age groups don’t have equal numbers of people in them).

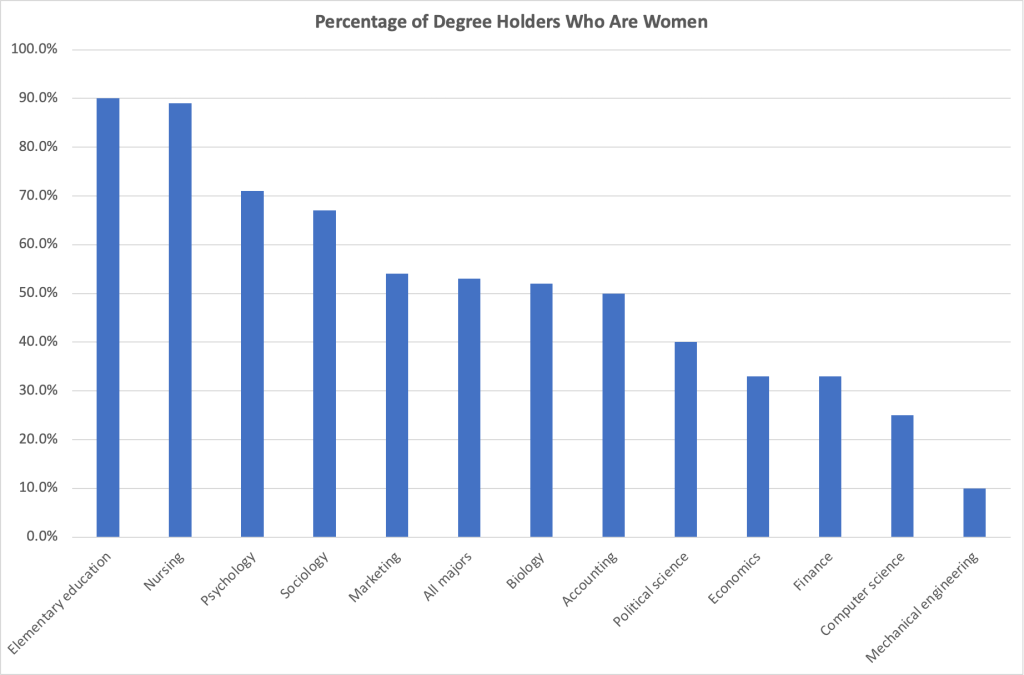

Finally, we can look at the demographic characteristics of economics majors. The next figure shows the percentage of degree holders in some popular majors who are women. Although women hold 53 percent of all bachelor’s degrees, they hold only 33 percent of bachelor’s degrees in economics. The share for economics is lower than for the other social sciences shown, the same as for finance majors, and more than for computer science and mechanical engineering majors.

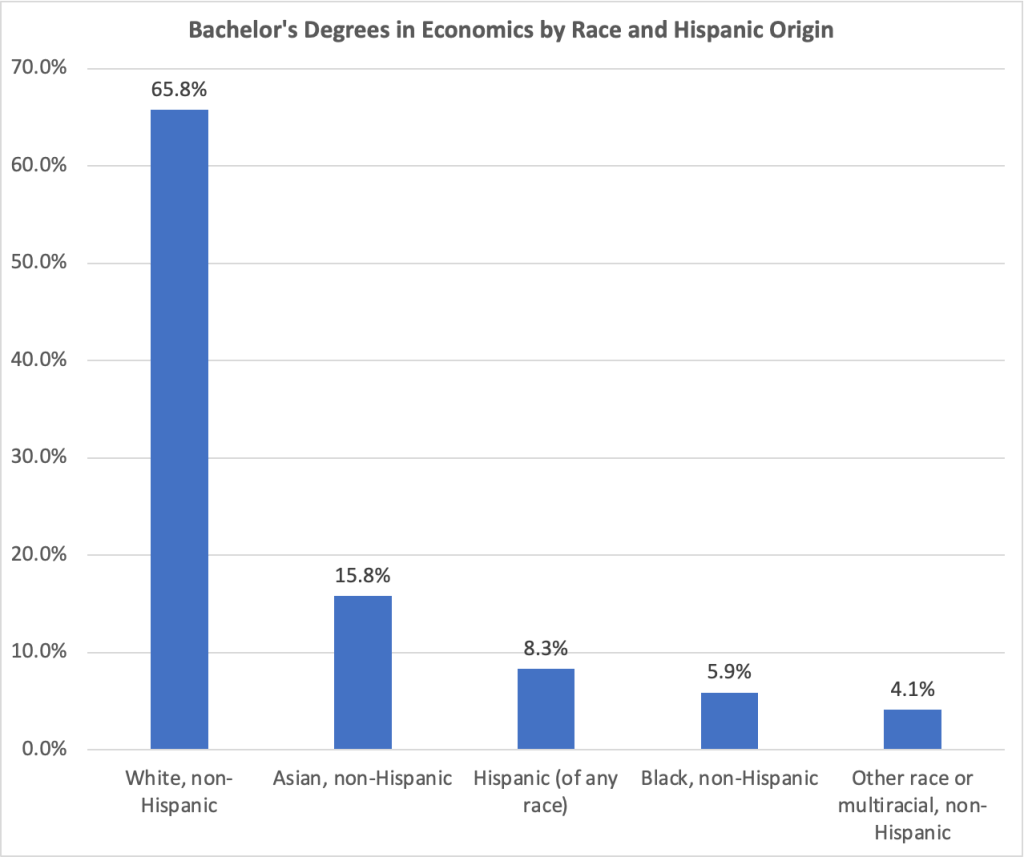

The next figure shows bachelor’s degrees in economics by race and Hispanic origin. Non-Hispanic whites and non-Hispanic Asians are overrepresented among economics majors compared with the percentages they make up of all bachelor’s degree holders. Non-Hispanic Blacks and Hispanics are underrepresented among economics majors compared with the percentages they make up of all bachelor’s degree holders. People who are multiracial or of another race hold the same percentage of economics degrees as of degrees in other subjects.

Photo of Caitlin Clark when she played for the University of Iowa from Reuters via the Wall Street Journal.

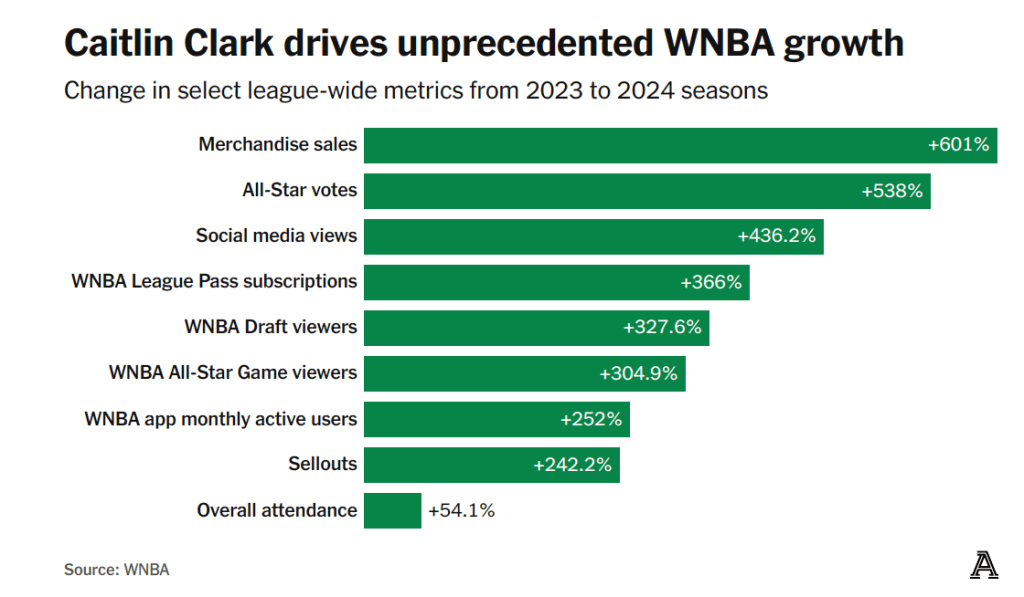

Caitlin Clark’s ability to hit three-point shots made her a star at the University of Iowa. Since she joined the Indiana Fever of the Women’s National Basketball Association (WNBA) in 2024, she’s been, arguably, the league’s biggest star. An article on theathletic.com discussing Clark’s effect on the league includes the following chart:

Clark’s popularity has resulted in substantially increased revenue for her team and for the WNBA. Should that fact affect the salary she receives from the Indiana Fever? The article states that: “Clark will almost assuredly never receive in salary what she is worth to the WNBA. In that regard, she’s a lot like [former men’s basketball star Michael] Jordan, and other all-time greats across sports.” Why won’t Clark be paid a salary equal to her worth to the WNBA?

In Microeconomics, Chapter 16, we show that in a competitive labor market, workers receive the value of their maginal products. The value of a basketball player’s marginal product is the additional revenue the player’s team earns from employing the player. We note that the marginal product of an athlete is the additional number of games the athlete’s team wins by employing the player. The value of a player’s marginal product is the additional revenue the team earns from those additional wins. Teams that win more games attract more fans to watch the teams play—both in person and on television or online. Teams earn revenue from selling tickets, as well as concessions and souvenirs sold in the area. Teams are paid for the rights to broadcast or stream their games. And, as the chart above shows, a player as popular as Clark will increase the game jerseys and other merchandise a team can sell.

We note in Chapter 16 that, once their inital contracts with their teams expire, the best professional athletes tend to sign contracts with teams in larger cities. Although an athlete’s marginal product may be no larger in a big city than in a smaller city, the revenue a team earns from the additional games the team wins from employing a star athlete depends in part on the population of the city the team plays in. Clark’s 2025 salary is only $78,066, far below the value of her marginal product, which is likely at least several million dollars. Her current contract with the Fever lasts through the 2027 season. But even after the contract expires, by league rules, she can’t be paid more than $294,244 by whichever team signs her. (It’s possible that amount may have increased by the time her current contract expires.)

The ceiling on WBNA salaries is far below the average salary in most U.S. men’s professional leagues. For instance, the average salary in the men’s National Basketball Association (NBA) during the 2024–2025 year was nearly $12 million. A low salary cap is common in leagues that are relatively new or that aren’t popular enough to receive large payments for the rights to broadcast or stream their games. For example, men’s Major League Soccer (MLS) has a salary limit of about $6 million per team. The WNBA was founded in 1996 (the NBA was founded in 1946) and, although the broadcast and online viewership for its games has increased, its viewership remains well below the NBA’s viewership.

Clark has been earning millions of dollars from endorisng Nike, Gatoade, and other products. But unless the factors just discussed change, it seems unlikely that she will receive a salary equal to the value of her marginal product to the Fever or any WNBA team she might play for in the future. The excerpt from theathletic.com article that we quoted above, though, compares her salary not to the value of her marginal product to the Fever but to the WNBA as a whole. Are there any circumstances under which we might expect a major sports star to be paid a salary equal to the additional revenue he or she is generating for a league as a whole?

The quotation from the article notes that no “all-time great” players, inclduing Michael Jordan of the NBA, have received salaries equal to the value of their marginal product to the leagues they played in. This outcome shouldn’t be surprising. Returns that entrepreneurs or workers earn in a market system are typically well below the total value they provide to society. For example, in a classic academic paper Nobel laureate William Nordhaus of Yale University estimated that entrepreneurs keep just 2.2 percent of the economic surplus they create by founding new firms. (We discuss the concept of economic surplus in Microeconomics, Chapter 4.) Leaving aside the monetary value of Clark to her team and her league, she has provided substantial consumer surplus to viewers of her games that is not captured by arena ticket prices or cable or streaming subscriptions. As we discuss in Chapter 4, the same is true of most goods and services in competitive markets.

Caitlin Clark, like Amazon founder Jeff Bezos, has only received a small fraction of the economic surplus she has created. (Photo from the Wall Street Journal)

So, although Caitlin Clark is a millionaire as a result of the money she has been paid to endorse products, the actual additional value she has created for her team, her league, and the economy is far greater than the income she earns.

“Clark will almost assuredly never receive in salary what she is worth to the WNBA. In that regard, she’s a lot like [Michael] Jordan, and other all-time greats across sports.”

This morning (June 6), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for May. The data in the report show that the labor market continues to be strong. There have been many stories in the media about businesspeople becoming pessimistic as a result of the large tariff increases the Trump Administration announced on April 2—some of which have since been reduced—but we don’t see the effects in the employment data. Some firms may be maintaining employment until they receive greater clarity about where tariff rates will end up. Similarly, although there are some indications that consumer spending may be slowing, to this point, the effects are not evident in the labor market.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

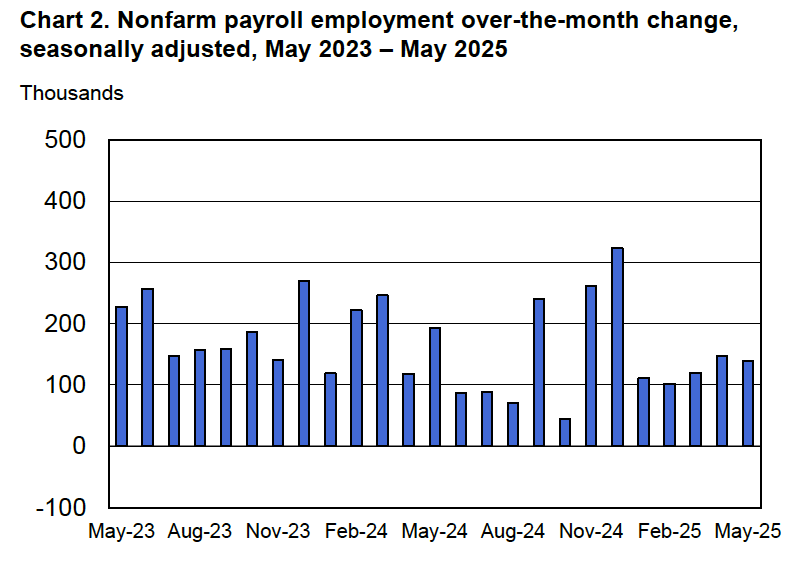

According to the establishment survey, there was a net increase of 139,000 nonfarm jobs during May. This increase was above the increase of 125,000 that economists surveyed had forecast. Somewhat offsetting this increase, the BLS revised downward its previous estimates of employment in March and April by a combined 95,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years.

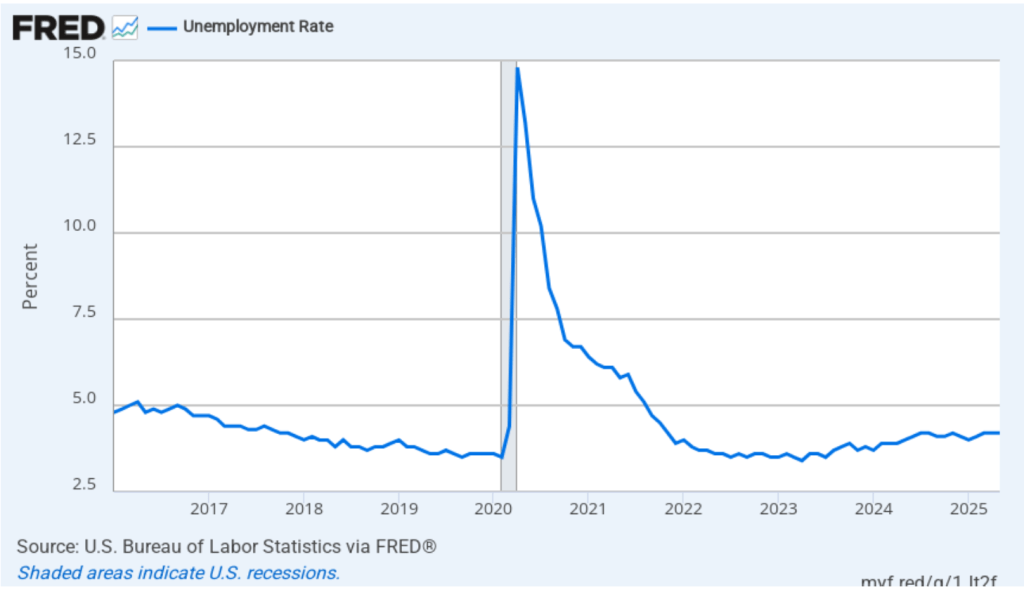

The unemployment rate was unchanged to 4.2 percent in May. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

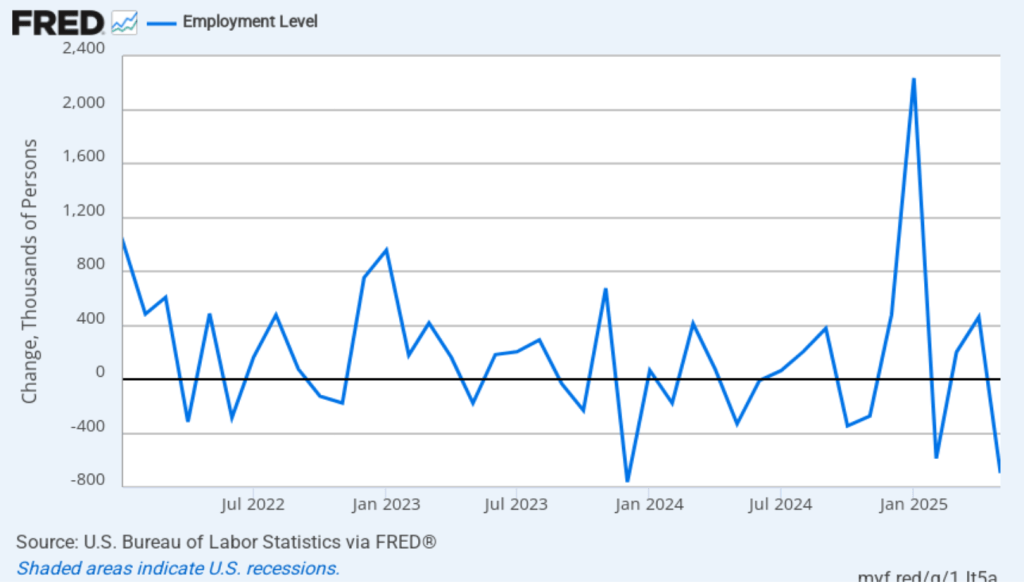

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net decrease of 696,000 jobs in May, following an increase of 461,000 jobs in April. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, the discrepancy between the two surveys in their estimates of the change in net jobs was particularly large. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

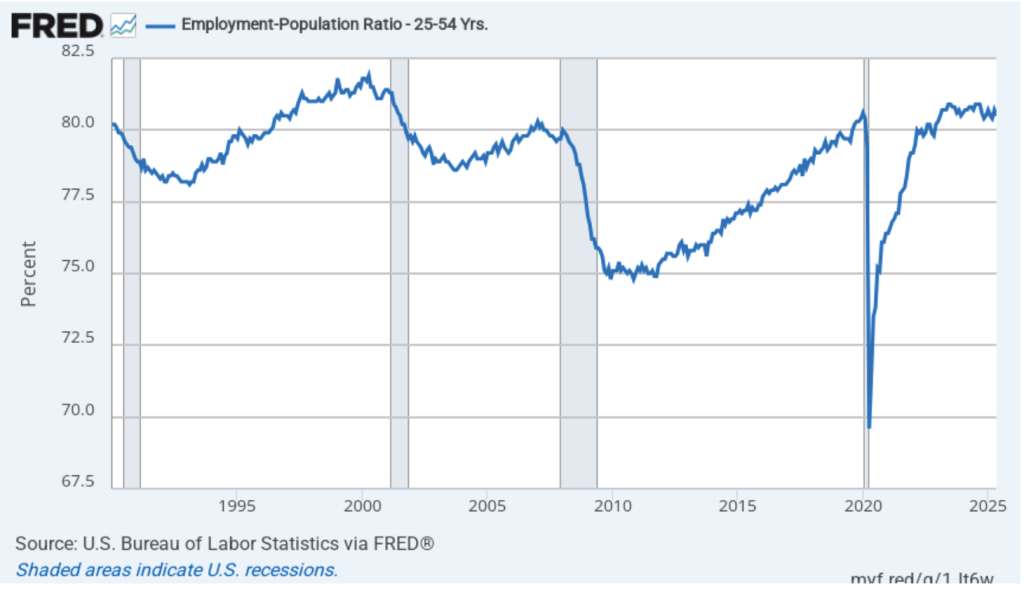

The household survey has another important labor market indicator. The employment-population ratio for prime age workers—those aged 25 to 54—declined from 80.7 percent in April to 80.5 percent in May. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to December 2019.

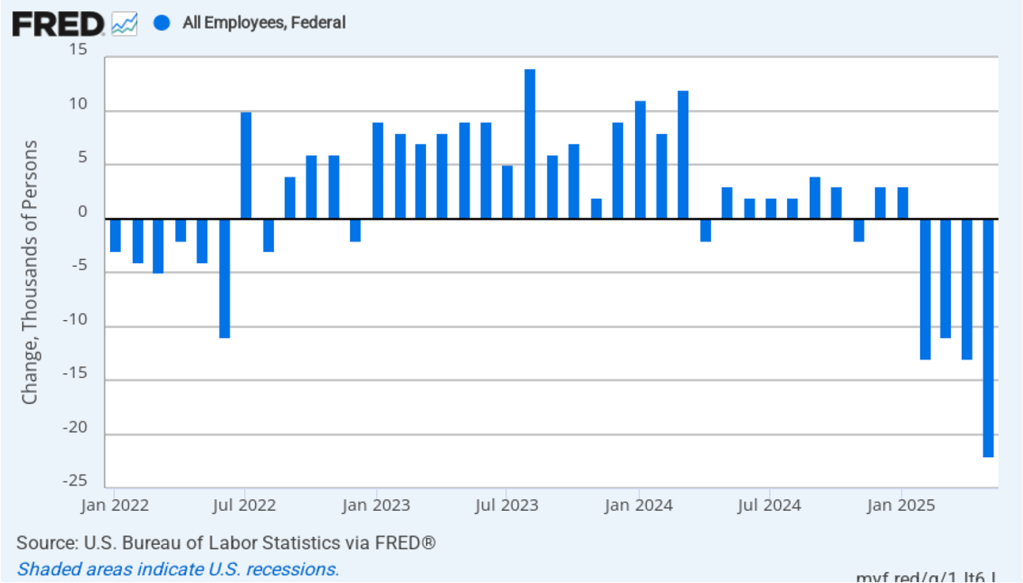

It remains unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 22,000 in May and a total decline of 59,000 beginning in February. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

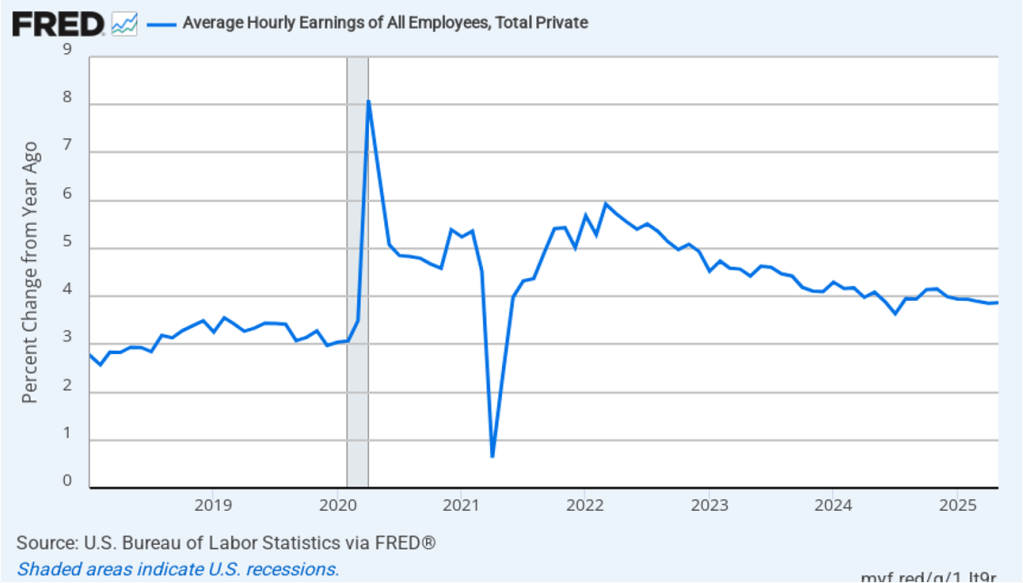

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.9 percent in May. Movements in AHE have been remarkably stable, showing increases of 3.9 percent each month since January.

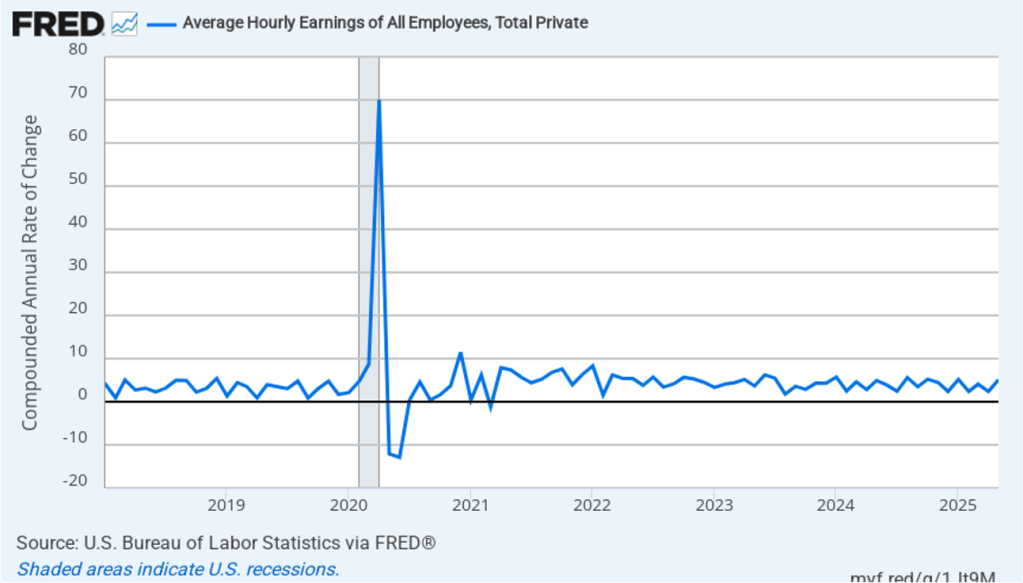

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In May, the 1-month rate of wage inflation was 5.1 percent, up sharply from 2.4 percent in April. If the 1-month increase in AHE is sustained, it would indicate that the Fed will struggle to achieve its 2 percent target rate of price inflation. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

Today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. Looming over monetary policy, however, is the expected effect of the Trump Administration’s tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

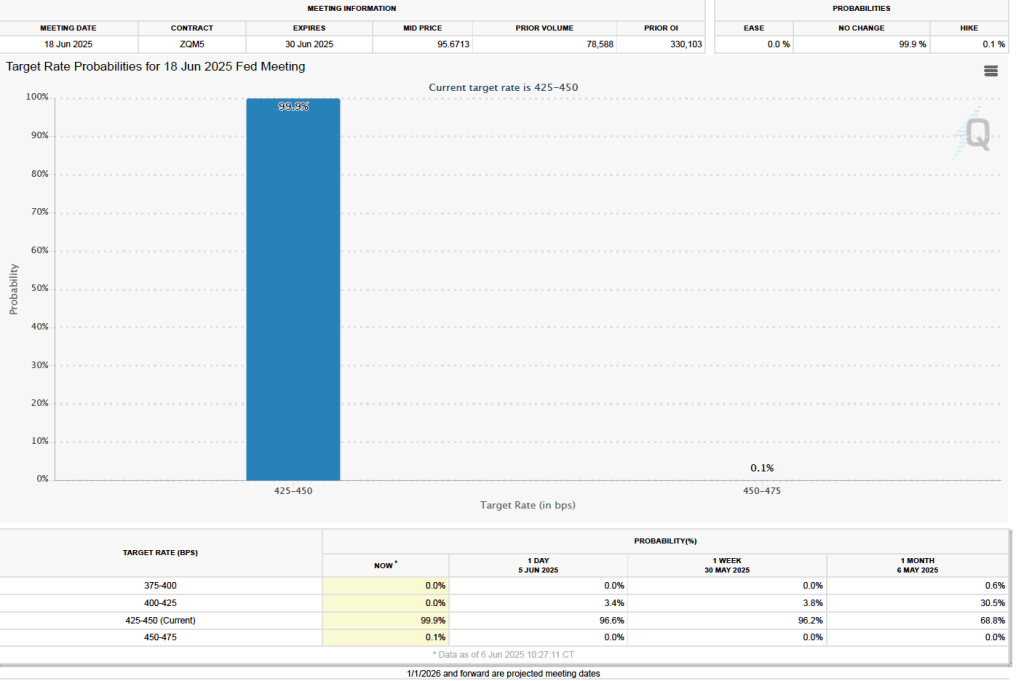

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its June 17–18 meeting. As shown in the following figure, investors assign a 99.9 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

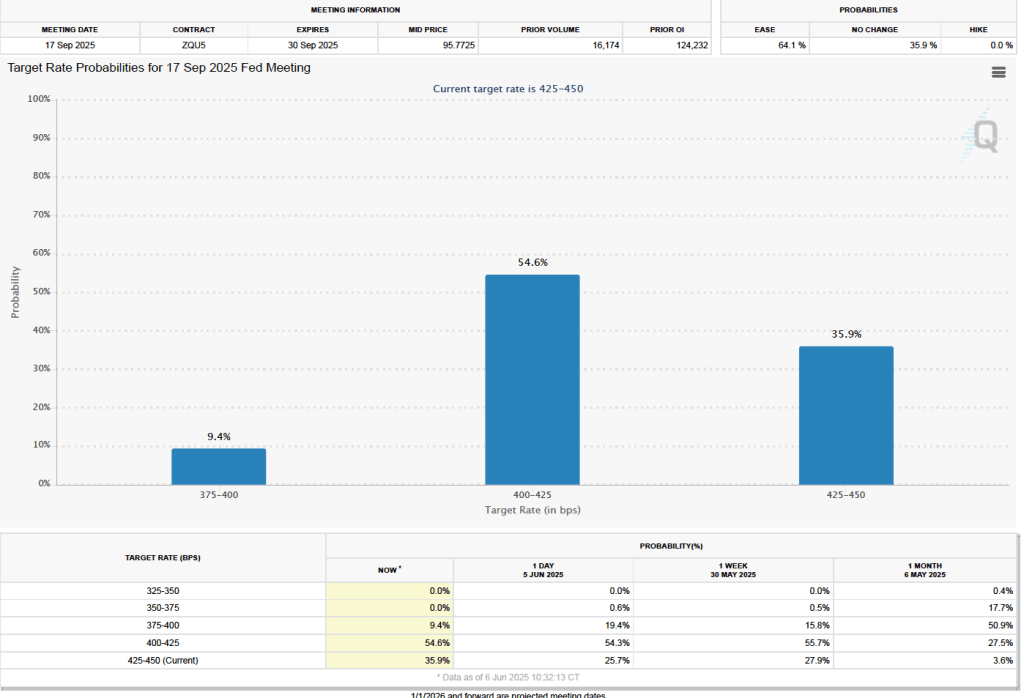

As the following figure shows, investors don’t expect the FOMC to cut its federal funds rate target until the committee’s September 16-17 meeting. Investors assign a probability of 54.6 percent that at that meeting the committee will cut its target range by 0.25 percentage point (25 basis points) to 4.00 percent to 4.25 percent. And a probability of 9.4 percent that the committee will cut its target rate by 50 baisis points to 3.75 percent to 4.00 percent. At 35.9 percent, investors assign a fairly high probability to the committee keeping its target range constant at that meeting.

Glenn, along with co-authors Douglas Elmendorf of Harvard’s Kennedy School and Zachary Liscow of the Yale Law School, has written a new National Bureau of Economic Research working paper: “Policies to Reduce Federal Budget Deficits by Increasing Economic Growth”

Here’s the abstract:

Could policy changes boost economic growth enough and at a low enough cost to meaningfully reduce federal budget deficits? We assess seven areas of economic policy: immigration of high-skilled workers, housing regulation, safety net programs, regulation of electricity transmission, government support for research and development, tax policy related to business investment, and permitting of infrastructure construction. We find that growth-enhancing policies almost certainly cannot stabilize federal debt on their own, but that such policies can reduce the explicit tax hikes, spending cuts, or both that are needed to stabilize debt. We also find a dearth of research on the likely impacts of potential growth-enhancing policies and on ways to design such policies to restrain federal debt, and we offer suggestions for ways to build a larger base of evidence.