Authors Glenn Hubbard and Tony O’Brien follow up on last week’s fiscal policy podcast by discussing monetary policy in today’s world. The Fed’s role has changed significantly since it was first introduced. They keep an eye on inflation and employment but aren’t clear on which is their priority. The tools and models used by economists even a decade ago seem outdated in a world where these concepts of a previous generation may be outdated. But, are they? LIsten to Glenn & Tony discuss these issues in some depth as we navigate our way through a difficult financial time.

Just search Hubbard O’Brien Economics on Apple iTunes or any other Podcast provider and subscribe! Today’s episode is appropriate for Principles of Economics and/or Money & Banking!

Authors Glenn Hubbard and Tony O’Brien discuss the long-term impacts of recent fiscal policy decisions as well as the proposed infrastructure investment by the Biden administration. The most recent round of fiscal stimulus means that we’re spending almost 4.5 Trillion which is a high percentage of what we recently spent in an entire fiscal year. They deal with the question of if the infrastructure spending will increase future productivity or will just be spent on the social programs. Also, Glenn deals with the proposed corporate tax increase to 28% which has been designated to fund these programs but does have an impact on stock market values held by millions through 401K’s and IRA’s.

Just search Hubbard O’Brien Economics on Apple iTunes or any other Podcast provider and subscribe!

Authors Glenn Hubbard and Tony O’Brien discuss early thoughts on the Biden Administration’s economic plan. They consider criticisms of the most recent stimulus packages price tag of $1.9B that it may spur inflation in future quarters. They offer thoughts on how this may become the primary legislative initiative of Biden’s first term as it crowds out other potential policy initiatives. Questions are asked about what bounce we may see for the economy and comparisons are made to the Post World War II era. Please listen and share with students!

The following editorials are mentioned in the podcast:

Authors Glenn Hubbard and Tony O’Brien look at the economic outlook given the current status of the presidential election. Will a divided government lead to economic prosperity or result in more gridlock? They discuss how much the President actually controls economic policy by setting the tone but that other instruments of our government likely have more effect in creating long-term growth in the Economy.

Just search Hubbard O’Brien Economics on Apple iTunes or any other Podcast provider and subscribe!

Authors Glenn Hubbard and Tony O’Brien discuss the economic impacts of what was discussed in the final Presidental debate on 10/22/20. They discuss wide-ranging topics that were raised in the debate from reopening the economy & schools, decreasing participation of women in the workforce due to COVID, healthcare, environment, and general tax policy. Listen to gain economic context on these important items. Click HERE for the New York Times article discussed during the Podcast:

Just search Hubbard O’Brien Economics on Apple iTunes and subscribe!

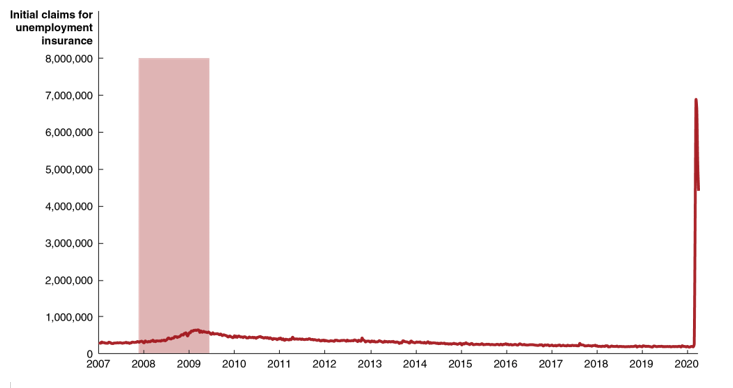

Apply the Concept: The Double-Edged Sword of Unemployment Insurance

Here’s the key point: Unemployment insurance payments during the pandemic cushioned worker income losses but made layoffs more likely and made some workers reluctant to return to work.

When workers lose their jobs, they are usually eligible for unemployment insurance payments. State governments are responsible for funding the payments, although the federal government provides guidelines states must meet and contributes funds to pay for administering the program. As the following figure shows, the U.S. experienced an extraordinary surge in weekly unemployment insurance claims during April 2020. The increase in claims was much greater than occurred at any point during the Great Recession of 2007-2009, which was the most severe recession the U.S. economy had experienced since the Great Depression of the 1930s.

The spike in people losing their jobs and applying for unemployment insurance was primarily due to many mayors and governors ordering the closure of nonessential businesses to fight the spread of the Covid-19 disease caused by the coronavirus. Unemployment insurance payments vary across states but typically last for 26 weeks and are intended to replace about 50 percent of a worker’s wage, subject to a cap. In 2020, Congress and President Donald Trump enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act to provide funds to support firms and businesses suffering from the effects of the coronavirus pandemic. Included in the act was a provision to increase the normal state unemployment insurance payment by $600 per week for up to four months.

Congress and President Franklin Roosevelt created the U.S. unemployment insurance system during the Great Depression as part of the Social Security Act of 1935. The first payments were made in 1939. Congress has had two main goals in establishing and maintaining a system of unemployment insurance: (1) To provide the means for workers who have lost their jobs to continue to buy food, clothing, and other necessities; and (2) to help support the level of total spending in the economy to avoid making recessions worse. From the beginning, some members of Congress and some state legislators were concerned that payments to the unemployed would reduce the recipients’ incentive to quickly find a new job. In establishing the program in the 1930s, policymakers were influenced by the experience in England where high rates of unemployment throughout most of the 1920s had resulted in many people receiving government payments—being “on the dole”—for years. In reaction, most states established 26 weeks as the length of time the unemployed could receive payments and kept the amount of money at roughly half a worker’s previous wage.

Economists believe that any type of insurance results in moral hazard, which refers to the actions people take after they have entered into a transaction. In particular, insurance makes the event being insured against more likely. For instance, once a firm has purchased a fire insurance policy on a warehouse, it may choose not to install an expensive sprinkler system thereby increasing the chance that the warehouse will burn down. People with health insurance may visit a doctor for treatment of a cold or other minor illness, which they would not do if they lacked insurance. Similarly, moral hazard resulting from the unemployment insurance system may result in workers not accepting jobs that they would have taken in the absence of unemployment insurance.

Economists debate the extent to which the moral hazard involved in unemployment insurance has a significant effect on U.S. labor markets. Most studies indicate that unemployment does increase the length of time that workers are unemployed—the duration of spells of unemployment—thereby reducing the efficiency of the economy by decreasing the size of the labor force and the quantity of goods and services produced. But because unemployment insurance reduces the opportunity cost of searching for a job—since workers give up less income during the time they are searching—it may also result in a better fit between workers and jobs, thereby increasing worker productivity and economic efficiency. Most economists conclude that, on balance, unemployment insurance that lasts for only 26 weeks and replaces only 50 percent of previous income probably does not significantly reduce economic efficiency in the United States.

After passage of the CARES, some policymakers and economists again raised the issue of whether the unemployment insurance system provides disincentives for people to work. The additional $600 that an unemployed worker received under the CARES act increased the average unemployment insurance benefit from $378 per week to $978 per week. That income was equivalent to a wage of $24.45 per hour for a 40-hour week and was greater than the wage rate received by more than half of workers in the United States in early 2020, before the coronavirus pandemic began. As a result, some workers were reluctant to return to their previous jobs as some firms began to reopen during May.

A restaurant owner in Oregon noted that one of his cooks was receiving $376 more per week in unemployment insurance than he had earned working: “Why on earth would he want to come back to work?” The restaurant was having difficulty attracting enough workers to provide takeout and delivery services while the restaurant’s dining room was closed. As the head of the National Restaurant Association put it: “It’s not that these workers are lazy, they’re just making the best economic decision for their families.”

Some firms that were unsure whether to continue to employ workers during the period the firms were ordered closed. Retaining workers would make it easier to restart once mayors and governors had lifted restrictions on operating. But the availability of higher unemployment insurance payments made some of these firms decide to lay off workers instead. For example, according to an article in the Wall Street Journal, Macy’s chief executive stated that “the new benefits in the federal stimulus program played a role in the company’s decision to furlough 125,000 workers this past week.”

The supplementary unemployment insurance payments included in the CARES act succeeded in cushioning the income losses workers suffered from the layoffs during the pandemic, but they had also made it more likely that firms would lay off workers and made some workers more reluctant to return to work. Given that the additional $600 payments were scheduled to end after four months, it remained unclear whether the payments would have a lasting effect on the U.S. labor market.

Sources: Kurt Huffman, “Our Restaurants Can’t Reopen Until August,” Wall Street Journal, April 12, 20202; Eric Morath, “Coronavirus Relief Often Pays Workers More Than Work,” Wall Street Journal, April 28, 2020; Patrick Thomas and Chip Cutter, “Companies Cite New Government Benefits in Cutting Workers,” Wall Street Journal, April 7, 2020; Henry S. Farber and Robert G. Valletta, “Do Extended Unemployment Benefits Lengthen Unemployment Spells? Evidence from Recent Cycles in the U.S. Labor Market,” Journal of Human Resources, Vol. 50, No. 4, Fall 2015, pp. 873-909; Congressional Budget Office, “Understanding and Responding to Persistently High Unemployment,” February 2012; Daniel N. Price, “Unemployment Insurance, Then and Now, 1935-85,” Social Security Bulletin, Vol. 48, No. 10, October 1985, pp. 22-32; and Federal Reserve Bank of St. Louis.

Question: An article published in the New York Times during April 2020, quoted a policy analyst as stating that: “I would never two months ago have ever thought of advocating for 100 percent income replacement.”

What does the analyst mean by “100 percent income replacement”?

Why during an economic expansion or mild economic recession would most policymakers be reluctant to adopt a policy of 100 percent income replacement?

Are there benefits to such a policy during an economic expansion or mild economic recessions? How is the desirability of such a policy affected if the economy is in a severe recession?

Source: Ella Koeze, “The $600 Unemployment Booster Shot, State by State,” New York Times, April 23, 2020.

For Economics Instructors that would like the approved answers to the above questions, please email Christopher DeJohn from Pearson at christopher.dejohn@pearson.com and list your Institution and Course Number.

On April 17th, Glenn Hubbard and Tony O’Brien continued their podcast series by spending just under 30 minutes discuss varied topics such as the Federal Reserve’s monetary response, record unemployment numbers, panic buying of toilet paper as compared to bank runs, as well as recent books they’ve been reading with increased downtime from the pandemic.

During the initial UNWRITTEN webinar from Pearson, Glenn Hubbard had a conversation with Jaylen Brown, a Pearson Campus Ambassador as well as a student at University of Central Florida -also Glenn’s undergrad alma mater!

Over the 30-minute broadcast, they discussed topics of relevance to all students – real world outlook on jobs, supply and demand, and the policies aimed at relief. Glenn talks of recovery shaped like a Nike swoosh with a sharp decline and a slightly longer climb back to normalcy. Check out the full episode now posted on YouTube!

On April 10th Glenn Hubbard and Tony O’Brien sat down together to discuss some of the larger impacts of the pandemic.

In these 18 minutes, Glenn and Tony discuss the fiscal & monetary response, the future relationship of the US Treasury and the Federal Reserve System, as well as several other topics.

Supports: Hubbard/O’Brien, Chapter 24, Money, Banks, and the Federal Reserve System; Macroeconomics Chapter 14; Essentials of Economics Chapter 16.

Apply the Concept: WHAT DO BANK RUNS TELL US ABOUT PANIC TOILET PAPER BUYING DURING THE CORONAVIRUS PANDEMIC?

Here’s the key point: Lack of confidence leads to panic buying, but a return of confidence leads to a return to normal buying.

In Chapter 24, Section 24.4 of the Hubbard and O’Brien Economics 8e text (Chapter 14, Section 14.4 of Macroeconomics 8e) we discuss the problem of bank runs that plagued the U.S. financial system during the years before the Federal Reserve began operations 1914. During the 2020 coronavirus epidemic in the United States consumers bought most of the toilet paper available in supermarkets leaving the shelves bare. Toilet paper runs turn out to be surprisingly similar to bank runs.

First, consider bank runs. The United States, like other countries, has a fractional reserve banking system, which means that banks keep less than 100 percent of their deposits as reserves. During most days, banks will experience roughly the same amount of funds being withdrawn as being deposited. But if, unexpectedly, a large number of depositors simultaneously attempt to withdraw their deposits from a bank, the bank experiences a run that it may not be able to meet with its cash on hand. If large numbers of banks experience runs, the result is a bank panic that can shut down the banking system.

Runs on commercial banks in the United States have effectively ended due to the combination of the Federal Reserve acting as a lender of last resort to banks experiencing runs and the Federal Deposit Insurance Corporation (FDIC) insuring bank deposits (currently up to $250,000 per person, per bank). But consider the situation prior to 1914. As a depositor in a bank during that period, if you had any reason to suspect that your bank was having problems, you had an incentive to be at the front of the line to withdraw your money. Even if you were convinced that your bank was well managed and its loans and investments were sound, if you believed the bank’s other depositors thought the bank had a problem, you still had an incentive to withdraw your money before the other depositors arrived and forced the bank to close. In other words, in the absence of a lender of last resort or deposit insurance, the stability of a bank depends on the confidence of its depositors. In such a situation, if bad news—or even false rumors—shakes that confidence, a bank will experience a run.

Moreover, without a system of government deposit insurance, bad news about one bank can snowball and affect other banks, in a process called contagion. Once one bank has experienced a run, depositors of other banks may become concerned that their banks might also have problems. These depositors have an incentive to withdraw their money from their banks to avoid losing it should their banks be forced to close.

Now think about toilet paper in supermarkets. From long experience, supermarkets, such as Kroger, Walmart, and Giant Eagle, know their usual daily sales and can place orders that will keep their shelves stocked. The same is true of online sites like Amazon. By the same token, manufacturers like Kimberly-Clark and Procter and Gamble, set their production schedules to meet their usual monthly sales. Consumers buy toilet paper as needed, confident that supermarkets will always have some available.

Photo of empty supermarket shelves taken in Boston, MA in March 2020. Credit: Lena Buananno

But then the coronavirus hit and in some states non-essential businesses, colleges, and schools were closed and people were advised to stay home as much as possible. Supermarkets remained open everywhere as did, of course, online sites such as Amazon. But as people began to consider what products they would need if they were to remain at home for several weeks, toilet paper came to mind.

At first only a few people decided to buy several weeks worth of toilet paper at one time, but that was enough to make the shelves holding toilet paper begin to look bare in some supermarkets. As they saw the bare shelves, some people who would otherwise have just bought their usual number of rolls decided that they, too, needed to buy several weeks worth, which made the shelves look even more bare, which inspired more to people to buy several weeks worth, and so on until most supermarkets had sold out of toilet paper, as did Amazon and other online sites.

Before 1914 if you were a bank depositor, you knew that if other depositors were withdrawing their money, you had to withdraw yours before the bank had given out all its cash and closed. In the coronavirus epidemic, you knew that if you failed to rush to the supermarket to buy toilet paper, the supermarket was likely to be sold out when you needed some. Just as banks relied on the confidence of depositors that their money would be available when they wanted to withdraw it, supermarkets rely on the confidence of shoppers that toilet paper and other products will be available to buy when they need them. A loss of that confidence can cause a run on toilet paper just as before 1914 a similar loss of confidence caused runs on banks.

In bank runs, depositors are, in effect, transferring a large part of the country’s inventory of currency out of banks, where it’s usually kept, and into the depositors’ homes. Similarly, during the epidemic, consumers were transferring a large part of the country’s inventory of toilet paper out of supermarkets and into the consumers’ homes. Just as currency is more efficiently stored in banks to be withdrawn only as depositors need it, toilet paper is more efficiently stored in supermarkets (or in Amazon’s warehouses) to be purchased only when consumers need it.

Notice that contagion is even more of a problem in a toilet paper run than in a bank run. People can ordinarily only withdraw funds from banks where they have a deposit, but consumers can buy toilet paper wherever they can find it. And during the epidemic there were news stories of people traveling from store to store—often starting early in the morning—buying up toilet paper.

Finally, should the government’s response to the toilet paper run of 2020 be similar to its response to the bank runs of the 1800s and early 1900s? To end bank runs, Congress established (1) the Fed—to lend banks currency during a run—and (2) the FDIC—to insure deposits, thereby removing a depositor’s fear that the depositor needed to be near the head of the line to withdraw money before the bank’s cash holdings were exhausted.

The situation is different with toilet paper. Supermarkets are eventually able to obtain as much toilet paper as they need from manufacturers. Once production increases enough to restock supermarket shelves, consumers—many of whom already have enough toilet paper to last them several weeks—stop panic buying and ample quantities of toilet paper will be available. Once consumers regain confidence that toilet paper will be available when they need it, they have less incentive to hoard it. Just as a lack of confidence leads to panic buying, a return of confidence leads to a return to normal buying.

Although socialist countries such as Venezuela, Cuba, and North Korea suffer from chronic shortages of many goods, market economies like the United States experience shortages only under unusual circumstances like an epidemic or natural disaster.

Note: For more on bank panics, see Hubbard and O’Brien, Money, Banking, and Financial Markets, 3rd edition, Chapter 12 on which some of this discussion is based.

Sources: Sharon Terlep, “Relax, America: The U.S. Has Plenty of Toilet Paper,” Wall Street Journal, March 16, 2020; Matthew Boyle, “You’ll Get Your Toilet Paper, But Tough Choices Have to Be Made: Grocery CEO,” bloomberg.com, March 18, 2020; and Michael Corkery and Sapna Maheshwari, “Is There Really a Toilet Paper Shortage?” New York Times, March 13, 2020.

Question

Suppose that as a result of their experience during the coronavirus pandemic, the typical household begins to store two weeks worth of toilet paper instead of just a few days worth as they had previously been doing. Will the result be that toilet paper manufacturers permanently increase the quantity of toilet paper that they produce each week?

Instructors can access the answers to these questions by emailing Pearson at christopher.dejohn@pearson.com and stating your name, affiliation, school email address, course number.