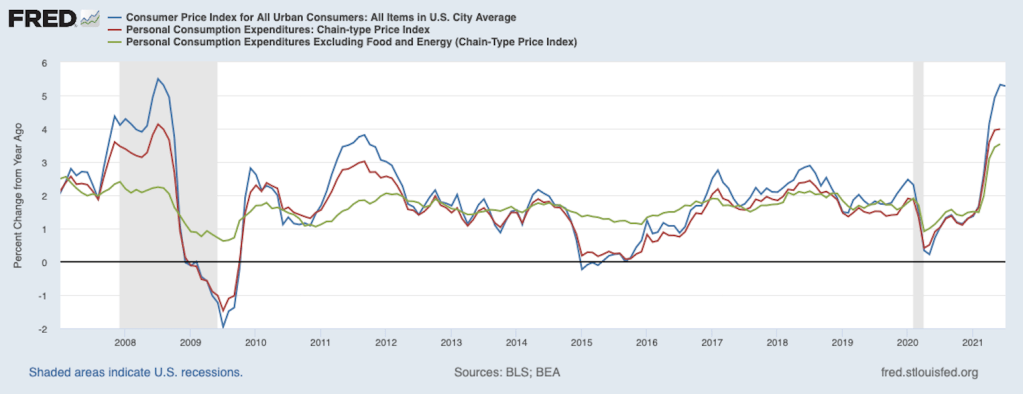

The U.S. inflation rate has accelerated. As the following figure shows, in mid-2021, inflation, measured as the percentage change in the CPI from the same month in the previous year (the blue line), rose above 5 percent for the first time since the summer of 2008.

As we discuss in an Apply the Concept in Chapter 25, Section 25.5 (Chapter 15, Section 15.5 of Macroeconomics), the Fed prefers to measure inflation using the personal consumption expenditures (PCE) price index. The PCE price index is a measure of the price level similar to the GDP deflator, except it includes only the prices of goods and services from the consumption category of GDP. Because the PCE price index includes more goods and services than the CPI, it is a broader measure of inflation. As the red line in the figure shows, inflation as measured by the PCE price index is generally lower than inflation measured by the CPI. The difference is particularly large during periods in which CPI inflation is especially high, as it was during 2008, 2011, and 2021.

Prices of food and energy are particularly volatile, so the measure of inflation the Fed focuses on most closely is the PCE price index, excluding food and energy prices (the green line in figure). The figure shows that this measure of inflation is more stable than either of the other two measures. For instance, during June 2021, measured by the CPI, inflation was 5.3 percent, but was 3.5 percent when measured by the PCE, excluding food and energy.

In the summer of 2021, even inflation measured by the PCE, excluding food and energy, is running well above the Fed’s long-run target rate of 2 percent. Why is inflation increasing? Most economists and policymakers believe that two sets of factors are responsible:

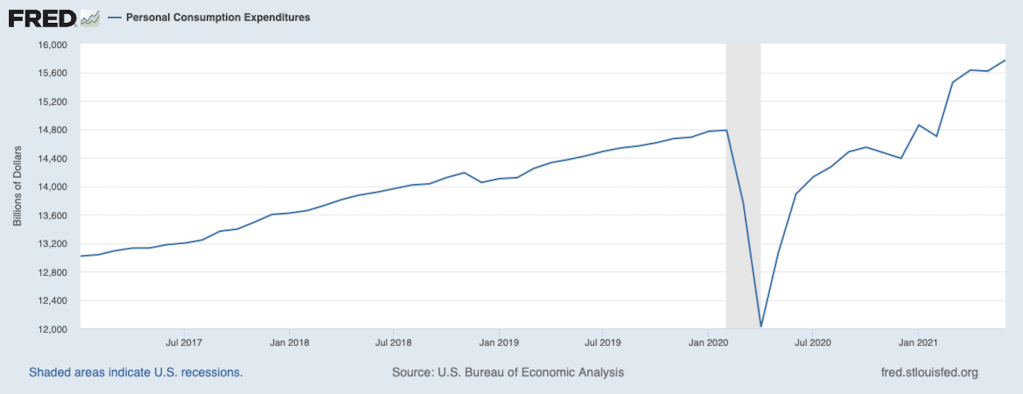

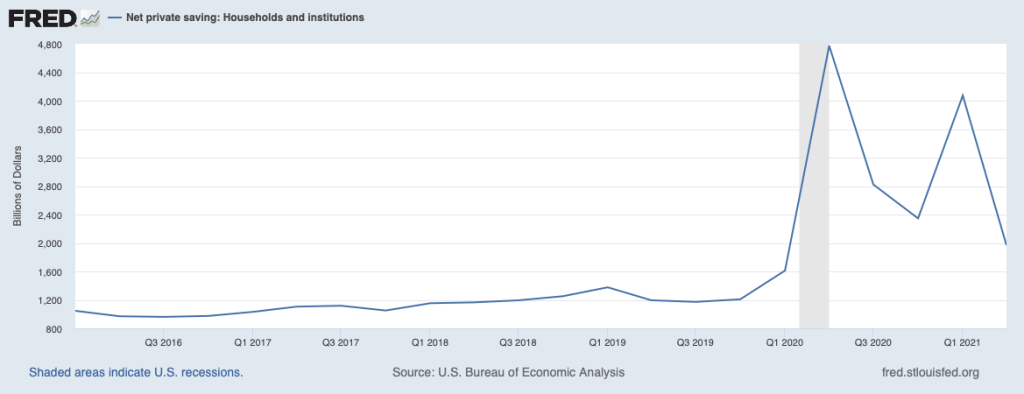

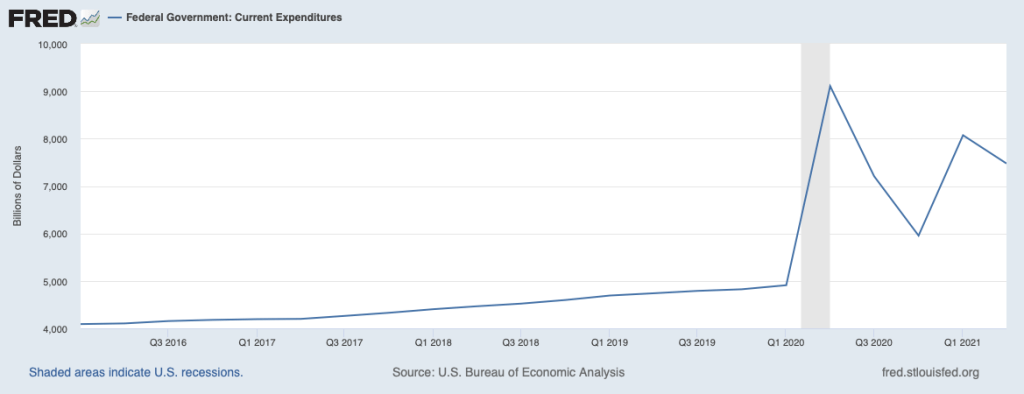

- Increases in aggregate demand. Consumption spending (see the first figure below) has increased as the economy has reopened and people have returned to eating in restaurants, going to the movies, working out in gyms, and spending at other businesses that were closed or operating at reduced capacity. Households have been able to sharply increase their spending because household saving (see the second figure below) soared during the pandemic in response to payments from the federal government, including supplemental unemployment insurance payments and checks sent directly to most households. The increase in federal government expenditures that helped fuel the increase in aggregate demand is shown in the third figure below.

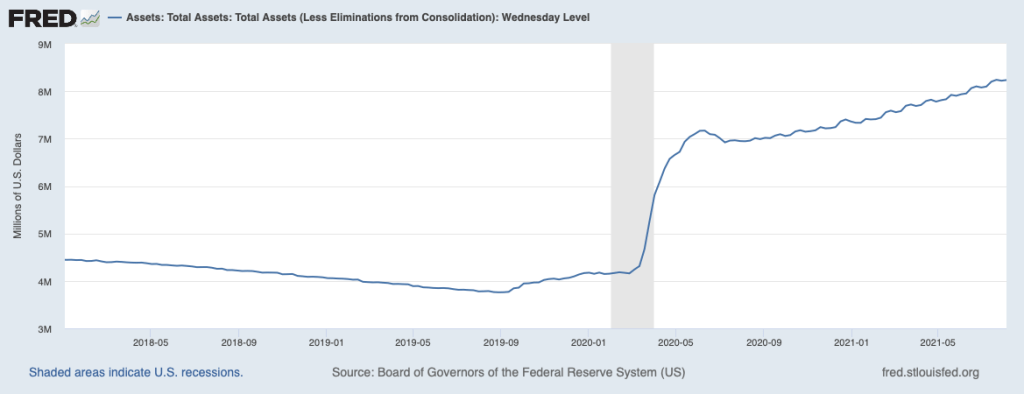

Fed policy has also been strongly expansionary, with the target for the federal funds kept near zero and the Fed continuing its substantial purchases of Treasury notes and mortgage-backed securities. The continuing expansion of the Fed’s balance sheet through the summer of 2021 is shown in the last of the figures below. The Fed’s asset purchases have help keep interest rates low and provided banks with ample funds to loan to households and firms.

2. Reductions in aggregate supply. The pandemic disrupted global supply chains, reducing the goods available to consumers. In the summer of 2021, not all of these supply chain issues had been resolved. In particular, a shortage of computer chips had reduced output of motor vehicles. New cars, trucks, SUVs, and minivans were often selling above their sticker prices. High prices for new vehicles led many consumers to increase their demand for used vehicles, driving up their prices. Between July 2020 and July 2021, prices of new vehicles rose 6.4 percent and prices for used vehicles rose an extraordinary 41.7 percent.

Supply issues also exist in some service industries, such as restaurants and hotels, that have had difficulty hiring enough workers to fully reopen.

Economists and policymakers differ as to whether high inflation rates are transitory or whether the U.S. economy might be entering a prolonged period of higher inflation. Most Federal Reserve policymakers argue that the higher inflation rates in mid-2021 are transitory. For instance, in a statement following its July 28, 2021 meeting, the Federal Open Market Committee noted that: “Inflation has risen, largely reflecting transitory factors.” Although the statement also noted that inflation is “on track to moderately exceed 2 percent for some time.”

In a speech at the end of July, Fed Governor Lael Brainard expanded on the Fed’s reasoning:

“Recent high inflation readings reflect supply–demand mismatches in a handful of sectors that are likely to prove transitory…. I am attentive to the risk that inflation pressures could broaden or prove persistent, perhaps as a result of wage pressures, persistent increases in rent, or businesses passing on a larger fraction of cost increases rather than reducing markups, as in recent recoveries. I am particularly attentive to any signs that currently high inflation readings are pushing longer-term inflation expectations above our 2 percent objective.”

“Currently, I do not see such signs. Most measures of survey- and market-based expectations suggest that the current high inflation pressures are transitory, and underlying trend inflation remains near its pre-COVID trend…. Many of the forces currently leading to outsized gains in prices are likely to dissipate by this time next year. Current tailwinds from fiscal support and pent-up consumption are likely to shift to headwinds, and some of the outsized price increases associated with acute supply bottlenecks may ease or partially reverse as those bottlenecks are resolved.”

Brainard’s remarks highlight a point that we make in Chapter 27, Section 27.1 (Chapter 17, Section 17.1 of Macroeconomics): The expectations of households and firms of future inflation play an important part in determining current inflation. Inflation can rise above and fall below the expected inflation rate in response to changes in the labor market—which affect the wages firms pay and, therefore, the firms’ costs—as well as in response to fluctuations in aggregate supply resulting from positive or negative supply shocks—such as the pandemic’s negative effects on aggregate supply. Fed Chair Jerome Powell has argued that with households and firms’ expectations still well-anchored at around 2 percent, inflation was unlikely to remain above that level in the long run.

Some economists are less convinced that households and firms will continue to expect 2 percent inflation if they experience higher inflation rates through the end of 2021. The Wall Street Journal’s editorial board summed up this view: “One risk for the Fed is that more months of these price increases will become what consumers and businesses come to expect. To use the Fed jargon, prices would no longer be ‘well-anchored.’ That may be happening.”

As we discuss in Chapter 27, Sections 27.2 and 27.3 (Macroeconomics, Chapter 17, Sections 17.2 and 17.3), during the late 1960s and early 1970s, higher rates of inflation eventually increased households and firms’ expectations of the inflation rate, leading to an acceleration of inflation that was difficult for the Fed to reverse.

Earlier this year, Olivier Blanchard of the Peterson Institute for International Economics, formerly a professor of economics at MIT and director of research at the International Monetary Fund, raised the possibility that overly expansionary monetary and fiscal policies might result in the Fed facing conditions similar to those in the 1970s. The Fed would then be forced to choose between two undesirable policies:

“If inflation were to take off, there would be two scenarios: one in which the Fed would let inflation increase, perhaps substantially, and another—more likely—in which the Fed would tighten monetary policy, perhaps again substantially. Neither of these two scenarios is ideal. In the first, inflation expectations would likely become deanchored, cancelling one of the major accomplishments of monetary policy in the last 20 years and making monetary policy more difficult to use in the future. In the second, the increase in interest rates might have to be very large, leading to problems in financial markets. I would rather not go there.”

In a recent interview, Lawrence Summers of Harvard University, who served as secretary of the Treasury in the Clinton administration, made similar points:

“We have inflation that since the beginning of the year has been running at a 5 percent annual rate. …. Starting at high inflation, we’ve got an economy that’s going to grow at extremely high rates for the next quarter or two. … I think we’re going to find ourselves with a new normal of inflation above 3 percent. Then the Fed is either going to have to be inconsistent with all the promises and commitments it’s made [to maintain a target inflation rate of 2 percent] or it’s going to have to attempt the task of slowing down the economy, which is rarely a controlled process.”

Clearly the pandemic and the resulting policy responses have left the Fed in a challenging situation.

Sources: Federal Reserve Open Market Committee, “Federal Reserve Press Release,” federalreserve.gov, July 28, 2021; Lael Brainard, “Assessing Progress as the Economy Moves from Reopening to Recovery,” speech at “Rebuilding the Post-Pandemic Economy” 2021 Annual Meeting of the Aspen Economic Strategy Group, Aspen, Colorado, federalreserve.gov, July 30, 2021; Wall Street Journal editorial board, “Powell Gets His Inflation,” Wall Street Journal, July 13, 2021; Olivier Blanchard, “In Defense of Concerns over the $1.9 Trillion Relief Plan,” piie.com, February 21, 2012; “Former Treasury Secretary on Consumer Prices, U.S. Role in Global Pandemic, Efforts,” wbur.org, August 22, 2021; and Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org.