The Federal Reserve’s independence and the public’s perception of that independence are critical for economic performance, including achieving the goals Congress has set for the Federal Reserve of stable prices, maximum employment, and moderate long-term interest rates. The reported criminal inquiry into Federal Reserve Chair Jay Powell is an unprecedented attempt to use prosecutorial attacks to undermine that independence. This is how monetary policy is made in emerging markets with weak institutions, with highly negative consequences for inflation and the functioning of their economies more broadly. It has no place in the United States whose greatest strength is the rule of law, which is at the foundation of our economic success.

SIGNATORIES

Ben S. Bernanke served two terms as Chair of the Board of Governors of the Fed, as well as Chair of the Council of Economic Advisers under President George W. Bush.

Jared Bernstein served as Chair of the Council of Economic Advisers under President Joe Biden.

Jason Furman served as Chair of the Council of Economic Advisers under President Barack Obama.

Timothy F. Geithner served as the 75th Secretary of the Treasury under President Barack Obama, as well as President and Chief Executive Officer of the Federal Reserve Bank of New York.

Alan Greenspan served five terms as Chair of the Board of Governors of the Fed, first appointed by President Ronald Reagan and then reappointed by Presidents George H.W. Bush, Bill Clinton, and George W. Bush. He also was Chair of the Council of Economic Advisers under President Gerald Ford.

Glenn Hubbard served as Chair of the Council of Economic Advisers under President George W. Bush.

Jacob J. Lew served as the 76th Secretary of the Treasury under President Barack Obama.

N. Gregory Mankiw served as Chair of the Council of Economic Advisers under President George W. Bush.

Henry M. Paulson served as the 74th Secretary of the Treasury under President George W. Bush.

Kenneth Rogoff is the Maurits C. Boas Professor of International Economics at Harvard University and former chief economist of the International Monetary Fund.

Christina Romer served as Chair of the Council of Economic Advisers under President Barack Obama.

Robert E. Rubin served as the 70th Secretary of the Treasury under President Bill Clinton, after serving as the first director of the White House National Economic Council.

Janet Yellen served as the 78th Secretary of the Treasury under President Joe Biden, Chair and Vice Chair of the Board of Governors of the Fed, Chair of the Council of Economic Advisers under President Bill Clinton, and President and CEO of the Federal Reserve Bank of San Francisco.

*********************

Separately, Federal Reserve Chair Jerome Powell issued the following statement last night. (Here is a link to Powell’s statement and to a video of Powell reading the statement.)

Good evening.

On Friday, the Department of Justice served the Federal Reserve with grand jury subpoenas, threatening a criminal indictment related to my testimony before the Senate Banking Committee last June. That testimony concerned in part a multi-year project to renovate historic Federal Reserve office buildings.

I have deep respect for the rule of law and for accountability in our democracy. No one—certainly not the chair of the Federal Reserve—is above the law. But this unprecedented action should be seen in the broader context of the administration’s threats and ongoing pressure.

This new threat is not about my testimony last June or about the renovation of the Federal Reserve buildings. It is not about Congress’s oversight role; the Fed through testimony and other public disclosures made every effort to keep Congress informed about the renovation project. Those are pretexts. The threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President.

This is about whether the Fed will be able to continue to set interest rates based on evidence and economic conditions—or whether instead monetary policy will be directed by political pressure or intimidation.

I have served at the Federal Reserve under four administrations, Republicans and Democrats alike. In every case, I have carried out my duties without political fear or favor, focused solely on our mandate of price stability and maximum employment. Public service sometimes requires standing firm in the face of threats. I will continue to do the job the Senate confirmed me to do, with integrity and a commitment to serving the American people.

Photo of Federal Reserve Chair Jerome Powell from federalreserve.gov.

As we discussed in a recent blog post, through the years a number of presidents have attempted to pressure Fed chairs to implement the monetary policy the president preferred. Although President Donald Trump nominated Jerome Powell to his first term as Fed chair—which began in February 2018—Trump has had many critical things to say about Powell’s conduct of monetary policy. Early in Trump’s current term, it seemed possible that he would attempt to replace Powell as Fed chair before the end of Powell’s second term in May 2026. Trump has stated, though, that he doesn’t intend to remove Powell. (As we discussed in this recent blog post, it seems unlikely that the Supreme Court would allow a president to remove a Fed chair because of disagreements over monetary policy.)

It’s not unusual for Fed chairs to meet with presidents, but until today (May 29) Powell had not met with Trump. When asked in a press conference on May 7 about a meeting with Trump, Powell responded that: “I don’t think it’s up to a Fed Chair to seek a meeting with the President, although maybe some have done so. I’ve never done so, and I can’t imagine myself doing that. It’s—I think it’s always—comes the other way: A President wants to meet with you. But that hasn’t happened.”

Today, Powell met with Trump after Trump requested a meeting. After the meeting, the Fed released this brief statement:

“At the President’s invitation, Chair Powell met with the President today at the White House to discuss economic developments including for growth, employment, and inflation.

Chair Powell did not discuss his expectations for monetary policy, except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook.

Finally, Chair Powell said that he and his colleagues on the FOMC will set monetary policy, as required by law, to support maximum employment and stable prices and will make those decisions based solely on careful, objective, and non-political analysis.”

According to an article in the Wall Street Journal, following the meeting, White House Press Secretary Karoline Leavitt stated that:

“The president did say that he believes the Fed chair is making a mistake by not lowering interest rates, which is putting us at an economic disadvantage to China and other countries. The president has been very vocal about that both publicly—and now I can reveal—privately, as well.”

In this photo of a Federal Open Market Committee meeting, Fed Chair Jerome Powell is on the far left and Fed Governor Christopher Waller is the third person to Powell’s left. (Photo from federalreserve.gov)

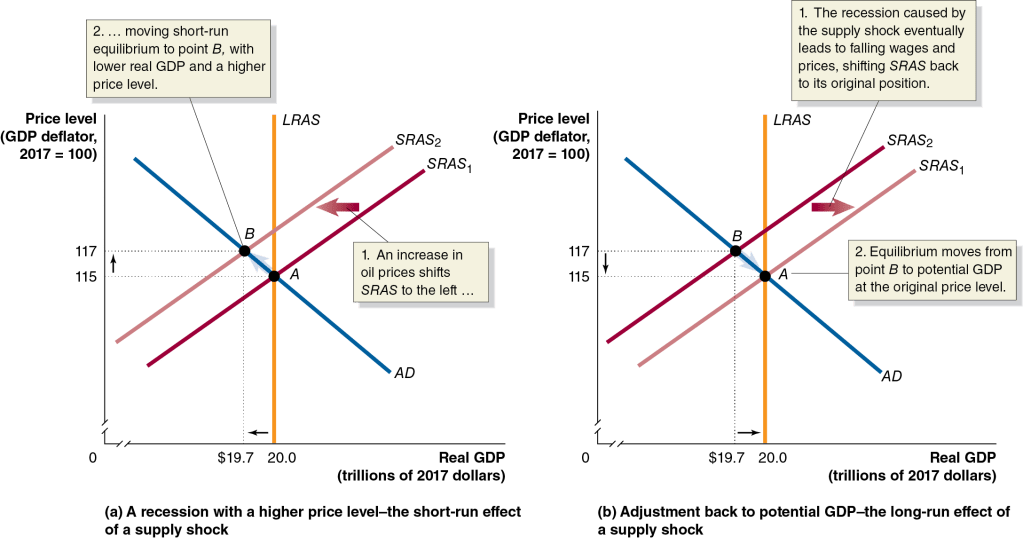

This post discusses two developments this week that involve the Federal Reserve. First, we discuss the apparent disagreement between Fed Chair Jerome Powell and Fed Governor Christopher Waller over the best way to respond to the Trump Administration’s tariff increases. As we discuss in this blog post and in this podcast, in terms of the aggregate demand and aggregate supply model, a large unexpected increase in tariffs results in an aggregate supply shock to the economy, shifting the short-run aggregate supply curve (SRAS) to the left. The following is Figure 13.7 from Macroeconomics (Figure 23.7 from Economics) and illustrates the effects of an aggregate supply shock on short-run macroeconomic equilibrium.

Although the figure shows the effects of an aggregate supply shock that results from an unexpected increase in oil prices, using this model, the result is the same for an aggregate supply shock caused by an unexpected increase in tariffs. Two-thirds of U.S. imports are raw materials, intermediate goods, or capital goods, all of which are used as inputs by U.S. firms. So, in both the case of an increase in oil prices and in the case of an increase in tariffs, the result of the supply shock is an increase in U.S. firms’ production costs. This increase in costs reduces the quantity of goods firms will supply at every price level, shifting the SRAS curve to the left, as shown in panel (a) of the figure. In the new macroeconomic equilibrium, point B in panel (a), the price level increases and the level of real GDP declines. The decline in real GDP will likely result in an increase in the unemployment rate.

An aggregate supply shock poses a policy dilemma for the Fed’s policymaking Federal Open Market Committee (FOMC). If the FOMC responds to the decline n real GDP and the increase in the unemployment rate with an expansionary monetary policy of lowering the target for the federal funds rate, the result is likely to be a further increase in the price level. Using a contractionary monetary policy of increasing the target for the federla funds rate to deal with the rising price level can cause real GDP to fall further, possibly pushing the economy into a recession. One way to avoid the policy dilemma from an aggregate supply shock caused by an increase in tariffs is for the FOMC to “look through”—that is, not respond—to the increase in tariffs. As panel (b) in the figure shows, if the FOMC looks through the tariff increase, the effect of the aggregate supply shock can be transitory as the economy absorbs the one-time increase in the price level. In time, real GDP will return to equilibrium at potential real GDP and the unemployment rate will fall back to the natural rate of unemployment.

On Monday (April 14), Fed Governor Christopher Waller in a speech to the Certified Financial Analysts Society of St. Louis made the argument for either looking through the macroeconomic effects of the tariff increase—even if the tariff increase turns out to be large, which at this time is unclear—or responding to the negative effects of the tariffs increases on real GDP and unemployment:

“I am saying that I expect that elevated inflation would be temporary, and ‘temporary’ is another word for ‘transitory.’ Despite the fact that the last surge of inflation beginning in 2021 lasted longer than I and other policymakers initially expected, my best judgment is that higher inflation from tariffs will be temporary…. While I expect the inflationary effects of higher tariffs to be temporary, their effects on output and employment could be longer-lasting and an important factor in determining the appropriate stance of monetary policy. If the slowdown is significant and even threatens a recession, then I would expect to favor cutting the FOMC’s policy rate sooner, and to a greater extent than I had previously thought.”

In a press conference after the last FOMC meeting on March 19, Fed Chair Jerome Powell took a similar position, arguing that: “If there’s an inflation that’s going to go away on its own, it’s not the correct response to tighten policy.” But in a speech yesterday (April 16) at the Economic Club of Chicago, Powell indicated that looking through the increase in the price level resulting from a tariff increase might be a mistake:

“The level of the tariff increases announced so far is significantly larger than anticipated. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. Both survey- and market-based measures of near-term inflation expectations have moved up significantly, with survey participants pointing to tariffs…. Tariffs are highly likely to generate at least a temporary rise in inflation. The inflationary effects could also be more persistent…. Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.”

In a discussion following his speech, Powell argued that tariff increases may disrupt global supply chains for some U.S. industries, such as automobiles, in way that could be similar to the disruptions caused by the Covid pandemic of 2020. As a result: “When you think about supply disruptions, that is the kind of thing that can take time to resolve and it can lead what would’ve been a one-time inflation shock to be extended, perhaps more persistent.” Whereas Waller seemed to indicate that as a result of the tariff increases the FOMC might be led to cut its target for the federal funds sooner or to larger extent in order to meet the maximum employment part of its dual mandate, Powell seemed to indicate that the FOMC might keep its target unchanged longer in order to meet the price stability part of the dual mandate.

Powell’s speech caught the notice of President Donald Trump who has been pushing the FOMC to cut its target for the federal funds rate sooner. An article in the Wall Street Journal, quoted Trump as posting to social media that: “Powell’s termination cannot come fast enough!” Powell’s term as Fed chair is scheduled to end in May 2026. Does Trump have the legal authority to replace Powell earlier than that? As we discuss in Macroeconomics, Chapter 27 (Economics Chapter 17), according to the Federal Reserve Act, once a Fed chair is notimated to a four-year term by the president (President Trump first nominated Powell to be chair in 2017 and Powell took office in 2018) and confirmed by the Senate, the president cannot remove the Fed chair except “for cause.” Most legal scholars argue that a president cannot remove a Fed chair due to a disagreement over monetary policy.

Article I, Section II of the Constitution of the United States states that: “The executive Power shall be vested in a President of the United States of America.” The ability of Congress to limit the president’s power to appoint and remove heads of commissions, agencies, and other bodies in the executive branch of government—such as the Federal Reserve—is not clearly specified in the Constitution. In 1935, a unanimous Supreme Court ruled in the case of Humphrey’s Executor v. United States that President Franklin Roosevelt couldn’t remove a member of the Federal Trade Commission (FTC) because in creating the FTC, Congress specified that members could only be removed for cause. Legal scholars have presumed that the ruling in this case would also bar attempts by a president to remove members of the Fed’s Board of Governors because of a disagreement over monetary policy.

The Trump Administration recently fired a member of the National Labor Relations Board and a member of the Merit Systems Protection Board. The members sued and the Supreme Court is considering the case. The Trump Adminstration is asking the Court to overturn the Humphrey’s Executor decision as having been wrongly decided because the decision infringed on the executive power given to the president by the Constitution. If the Court agrees with the administration and overturns the precdent established by Humphrey’s Executor, would President Trump be free to fire Chair Powell before Powell’s term ends? (An overview of the issues involved in this Court case can be found in this article from the Associated Press.)

The answer isn’t clear because, as we’ve noted in Macroeconomics, Chapter 14, Section 14.4, Congress gave the Fed an unusual hybrid public-private structure and the ability to fund its own operations without needing appropriations from Congress. It’s possible that the Court would rule that in overturning Humphrey’s Executor—if the Court should decide to do that—it wasn’t authorizing the president to replace the Fed chair at will. In response to a question following his speech yesterday, Powell seemed to indicate that the Fed’s unique structure might shield it from the effects of the Court’s decision.

If the Court were to overturn its ruling in Humphrey’s Executor and indicate that the ruling did authorize the president to remove the Fed chair, the Fed’s ability to conduce monetary policy independently of the president would be seriously undermined. In Macroeconomics, Chapter 17, Section 17.4 we review the arguments for and against Fed independence. It’s unclear at this point when the Court might rule on the case.

President-elect Donald Trump has stated that he believes that presidents should have more say in monetary policy. There had been some speculation that once in office Trump would try to replace Federal Reserve Chair Jerome Powell, although Trump later indicated that he would not attempt to replace Powell until Powell’s term as chair ends in May 2026. Can the president remove the Fed Chair or another member of the Board of Governors? The relevant section of the Federal Reserve Act States that: “each member [of the Board of Governors] shall hold office for a term of fourteen years from the expiration of the term of his predecessor, unless sooner removed for cause by the President.”

“Removed for cause” has generally been interpreted by lawyers inside and outside of the Fed as not authorizing the president to remove a member of the Board of Governors because of a disagreement over monetary policy. The following flat statement appears on a page of the web site of the Federal Reserve Bank of St. Louis: “Federal Reserve officials cannot be fired simply because the president or a member of Congress disagrees with Federal Reserve decisions about interest rates.”

At his press conference following the November 7 meeting of the Federal Open Market Committee (FOMC), Powell was asked by a reporter: “do you believe the President has the power to fire or demote you, and has the Fed determined the legality of a President demoting at will any of the other Governors with leadership positions?” Powell replied: “Not permitted under the law.” Despite Powell’s definitive statement, because no president has attempted to remove a member of the Board of Governors, the federal courts have never been asked to decide what the “removed for cause” language in the Federal Reserve Act means.

The president is free to remove the members of most agencies of the federal government, so why shouldn’t he or she be able to remove the Fed Chair? When Congress passed the Federal Reserve Act in 1913, it intended the central bank to be able set policy independently of the president and Congress. The president and members of Congress may take a short-term view of policy, focusing on conditions at the time that they run for reelection. Expansionary monetary policies can temporarily boost employment and output in the short run, but cause inflation to increase in the long run.

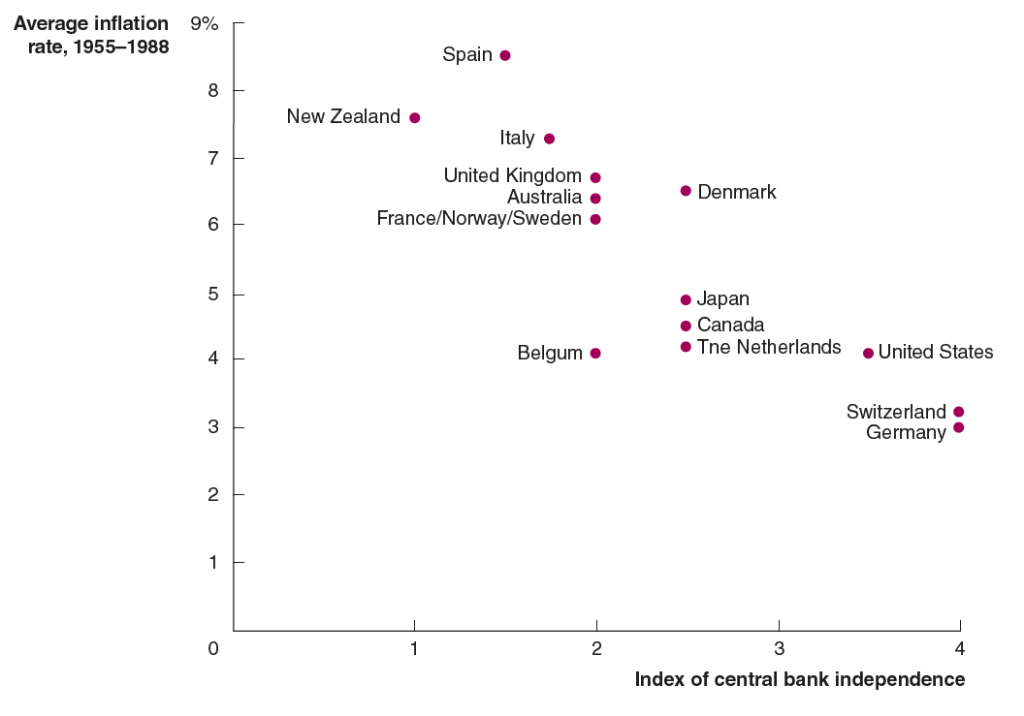

As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), in a classic study, Alberto Alesina and Lawrence Summers compared the degree of central bank independence and the inflation rate for 16 high-income countries during the years from 1955 to 1988. As the following figure shows, countries with highly independent central banks, such as the United States, Switzerland, and Germany, had lower inflation rates than countries whose central banks had little independence, such as New Zealand, Italy, and Spain.

Yesterday, something unusual happened that might seem to undermine Fed independence. Michael Barr, a member of the Board of Governors and the Board’s Vice Chair for Supervision, said that on February 28 he will step down from his position as Vice Chair, but will remain on the Board. His term as Vice Chair was scheduled to end in July 2026. His term on the Board is scheduled to end in January 2032.

Barr has been an advocate for stricter regulation of banks, including higher capital requirements for large banks. These positions have come in for criticism from banks, from some policymakers, and from advisers to Trump. Barr stated that he was stepping down because: “The risk of a dispute over the position could be a distraction from our mission. In the current environment, I’ve determined that I would be more effective in serving the American people from my role as governor.” Trump will nominate someone to assume the position of vice chair, but because there are no openings on the Board of Governors he will have to choose from among the current members.

Does this episode indicate that Fed independence is eroding? Not necessarily because the Fed’s regulatory role is distinct from its monetary policy role. As financial journalist Neil Irwin points out, “top [Fed] bank supervision officials view their role as more explicitly carrying out the regulatory agenda of the president who appointed them—and that a new president is entitled, in reasonable time, to their own choices.” In the past, other members of the Board who have held positions similar to the one Barr holds have resigned following the election of a new president.

So, it’s unclear at this point whether Barr’s resignation as vice chair indicates that the incoming Trump Administration will be taking steps to influence the Fed’s monetary policy actions or how the Fed’s leadership will react if it does.

A meeting of the Federal Open Market Committee (Photo from federalreserve.gov)

The Federal Reserve’s policymaking Federal Open Market Committee (FOMC) concluded its meeting today (November 7) after considering a mixed batch of macroeconomic data. As we noted in this blog post, the most recent jobs report showed a much smaller increase in payroll employment than had been expected. However, the effects of hurricanes and strikes on the labor market made the data in the report difficult to interpret. Real GDP growth during the third quarter of 2024, while relatively strong, was slower than expected. Finally, as we discuss in this post, inflation has been running above the Fed’s 2 percent annual target with wages also growing faster than is consistent with 2 percent price inflation.

Congress has given the Fed a dual mandate of achieving maximum employment and price stability. If FOMC members had been most concerned about lower-than-expected real GDP growth and some weakening in the labor market, the likely course would have been to cut the target range for the federal funds rate by 0.50 percentage point (50 basis points) from its current range of 4.75 percent to 5.00 percent to a range of 4.25 percent to 4.50 percent.

If the committee had been most concerned about inflation remaining above target, the likely course would have been to leave the target range for the federal funds rate unchanged. Instead, the committee split the difference by reducing the target range by 25 basis points. As we noted near the end of this blog post, financial markets had been expecting a 25 basis point cut. At the conclusion of each meeting, the committee holds a formal vote on its target for the federal funds rate. The vote today was unanimous.

In a press conference following the meeting, Fed Chair Jerome Powell noted that: “We see the risks to achieving our employment and inflation goals as being roughly in balance, and we are attentive to the risks to both sides of our mandate.” Powell also indicated his confidence that the committee would succeed in staying on what he labeled the “middle path” that monetary policy needs to follow: “We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing policy restraint too slowly could unduly weaken economic activity and employment …. Policy is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate.”

With respect to the effect of the macroeconomic policies of the incoming Trump Administration, Powell noted that the Fed doesn’t comment on fiscal policy nor did he consider it appropriate to comment in any way on the recent election. He stated that the committee would wait to see new policies enacted before considering their consequences for monetary policy. When asked by a reporter whether he would leave the position of Fed chair if asked to do so by someone in the Trump Administration, Powell answered “no.” When asked whether he believes the president has the power to remove a Fed chair before the end of the chair’s term, Powell again answered “no.” (Most legal scholars believe that, according to the Federal Reserve Act, a president can’t remove a Fed chair because of policy disagreements, but only “for cause.” See Macroeconomics, Chapter 17, Section 17.4/Economics, Chapter 27, Section 27.4 for more on this topic.)

Federal Reserve Vice Chair Philip Jefferson (photo from the Federal Reserve)

Federal Reserve Chair Jerome Powell (photo from the Federal Reserve)

At the beginning of 2024, investors were expecting that during the year the Fed’s policy-making Federal Open Market Committee (FOMC) would cut its target range for the federal funds rate six or seven times. At its meeting on March 19-20 the economic projections of the members of the FOMC indicated that they were expecting to cut the target range three times from its current 5.25 percent to 5.50 percent. But, as we noted in this recent post and in this podcast, macroeconomic data during the first three months of this year indicated that the U.S. economy was growing more rapidly than the Fed had expected and the reductions in inflation that occurred during the second half of 2023 had not persisted into the beginning of 2024.

The unexpected strength of the economy and the persistence of inflation above the Fed’s 2 percent target have raised the issue of whether the FOMC will cut its target range for the federal funds rate at all this year. Earlier this month, Neel Kashkari, president of the Federal Reserve Bank of Minneapolis raised the possibility that the FOMC would not cut its target range this year.

Today (April 16) both Fed Vice Chair Philip Jefferson and Fed Chair Jerome Powell addressed the issue of monetary policy. They gave what appeared to be somewhat different signals about the likely path of the federal funds target during the remainder of this year—bearing in mind that Fed officials never commit to any specific policy when making a speech. Adressing the International Research Forum on Monetary Policy, Vice Chair Jefferson stated that:

“My baseline outlook continues to be that inflation will decline further, with the policy rate held steady at its current level, and that the labor market will remain strong, with labor demand and supply continuing to rebalance. Of course, the outlook is still quite uncertain, and if incoming data suggest that inflation is more persistent than I currently expect it to be, it will be appropriate to hold in place the current restrictive stance of policy for longer.”

One interpretation of his point here is that he is still expecting that the FOMC will cut its target for the federal funds rate sometime this year unless inflation remains persistently higher than the Fed’s target—which he doesn’t expect.

Chair Powell, speaking at a panel discussion at the Wilson Center in Washington, D.C., seemed to indicate that he believed it was less likely that the FOMC would reduce its federal funds rate target in the near future. The Wall Street Journal summarized his remarks this way:

“Federal Reserve Chair Jerome Powell said firm inflation during the first quarter had introduced new uncertainty over whether the central bank would be able to lower interest rates this year without signs of an economic slowdown. His remarks indicated a clear shift in the Fed’s outlook following a third consecutive month of stronger-than-anticipated inflation readings ….”

An article on bloomberg.com had a similar interpretation of Powell’s remarks: “Federal Reserve Chair Jerome Powell signaled policymakers will wait longer than previously anticipated to cut interest rates following a series of surprisingly high inflation readings.”

Politics may also play a role in the FOMC’s decisions. As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), the Federal Reserve Act, which Congress passed in 1913 and has amended several times since, puts the Federal Reserve in an unusal position in the federal government. Although the members of the Board of Governors are appointed by the president and confirmed by the Senate, the Fed was intended to act independently of Congress and the president. Over the years, Fed Chairs have protected that independence by, for the most part, avoiding taking actions beyond the narrow responsibilites Congress has given to the Fed by Congress and by avoiding actions that could be interpreted as political.

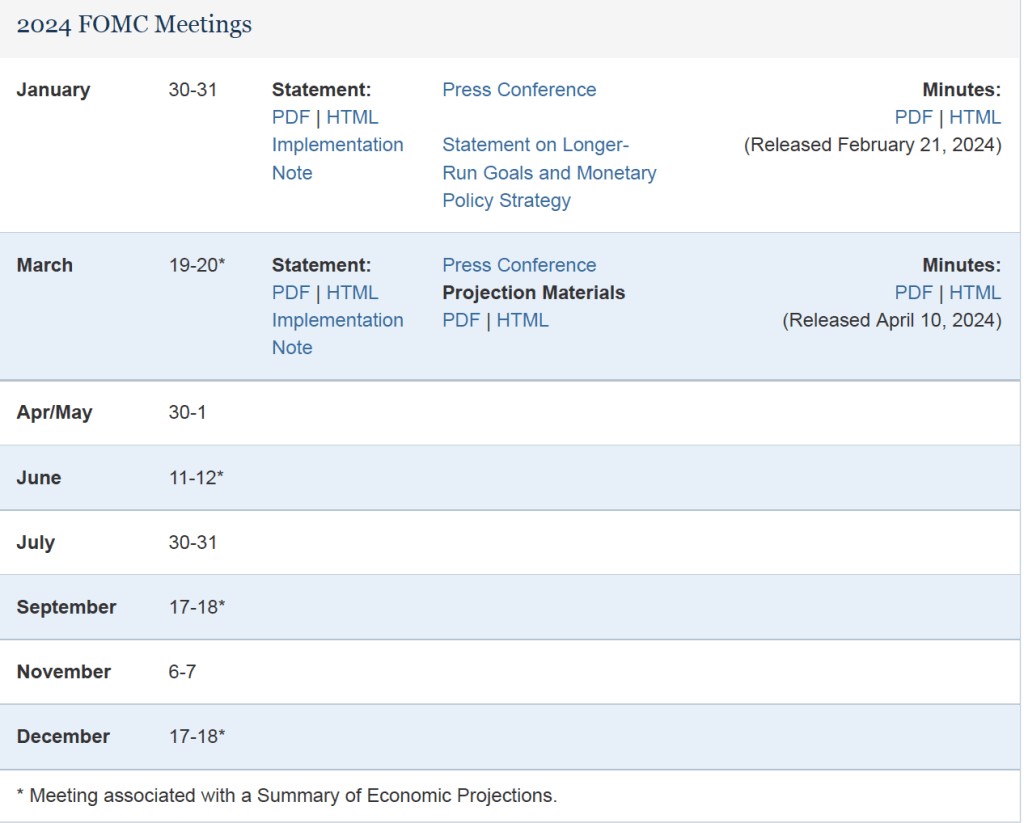

This year is, of course, a presidential election year. The following table from the Fed’s web site lists the FOMC meetings this year. The presidential election will occur on November 5. There are four scheduled FOMC meetings before then. Given that inflation has been running well above the Fed’s target during the first three months of the year, it would likely take at least two months of lower inflation data—or a weakening of the economy as indicated by a rising unemployment rate—before the FOMC would consider lowering its federal funds rate target. If so, the meeting on July 30-31 might be the first meeting at which a rate reduction would occur. If the FOMC doesn’t act at its July meeting, it might be reluctant to cut its target at the September 17-18 meeting because acting close to the election might be interpreted as an attempt to aid President Joe Biden’s reelection.

Although we don’t know whether avoiding the appearance of intervening in politics is an important consideration for the members of the FOMC, some discussion in the business press raises the possibility. For instance, a recent article in the Wall Street Journal noted that:

“The longer that officials wait, the less likely there will be cuts this year, some analysts said. That is because officials will likely resist starting to lower rates in the midst of this year’s presidential election campaign to avoid political entanglements.”

These are clearly not the easiest times to be a Fed policymaker!

Neel Kashkari, president of the Federal Reserve Bank of Minneapolis. Photo from the Wall Street Journal.Pat Toomey, U.S. Senator from Pennsylvania. Photo from http://www.toomey.senate.gov.

As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), the Federal Reserve is unusual among federal government agencies in being able to operate largely independently of Congress and the president. Congress passed the Federal Reserve Act, which established the Federal Reserve System, in 1913, and has amended it several times in the years since. (Note that, as we discuss in the Apply the Concept, “End the Fed?” in this chapter, the U.S. Constitution does not explicitly authorized the federal government to establish a central bank.) Section 2A of the act gives the Federal Reserve System the following charge:

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

Elsewhere in the act, the Fed was given other specified responsibilities, such as supervising commercial banks that are members of the Federal Reserve System and serving on the Financial Stability Oversight Council (FSOC), which is charged with assessing risks to the financial system.

Because Congress can change the structure and operations of the Fed at any time and because Congress has given the Fed only certain specific responsibilities, traditionally the Fed has avoided becoming involved in policy debates that are not directly concerned with its responsibilities. Over the years, most members of the Board of Governors have believed that if the Fed were to become involved in issues beyond monetary policy and the working of the financial system, Congress might decide to revise the Federal Reserve Act to reduce, or even eliminate, Fed independence.

In the spring of 2022, though, there were two instances where some members of Congress argued that the Fed had become involved in policy issues that went beyond the Fed’s responsibilities under the Federal Reserve Act. The first instance involved President Joe Biden’s nomination in January 2022 of Sarah Bloom Raskin to serve on the Fed’s Board of Governors. In 2010, Raskin was nominated to the Board of Governors by President Barack Obama and confirmed by the Senate in a voice vote without significant opposition. (In 2014, she resigned from the Board to accept a position in the Treasury Department.)

Her nomination by President Biden encountered significant opposition, however, largely because in July 2020 she had suggested that when the Fed expanded its lending programs during the Covid-19 pandemic it should have excluded firms in the oil, natural gas, and coal industries: “The Fed is ignoring clear warning signs about the economic repercussions of the impending climate crisis by taking action that will lead to increases in greenhouse gas emissions at a time when even in the short term, fossil fuels are a terrible investment.” Although her supporters argued that in formulating policy the Fed should take into account the threats to financial stability caused by climate change, when it became clear that a majority of the Senate disagreed, Raskin withdrew her nomination.

In April 2022, some members of Congress, including Senator Pat Toomey of Pennsylvania, questioned whether it was appropriate for President Neel Kashkari of the Federal Reserve Bank of Minneapolis to formally support the campaign to amend the Minnesota state constitution to include a provision stating that, “All children have a fundamental right to a quality public education …. It is a paramount duty of the state to ensure quality public schools that fulfill this fundamental right.”

The Bank defended its support for the amendment in a statement on its website: “The Federal Reserve Bank of Minneapolis’ support of the Page amendment is closely linked to the mission of the Federal Reserve. Congress assigned the Federal Reserve the dual goals of achieving (1) stable prices and (2) maximum employment, and one of the greatest determinants of success in the job market is education.”

Senator Toomey strongly disagreed, arguing in a letter of Bank President Kashkari that: “This amendment is highly political, as it wades into an ongoing debate about whether government-run school systems are preferable to parental choice in education.” Toomey asserted that: “These political lobbying efforts by you and other Minneapolis Fed officials … are well beyond the Federal Reserve’s mandate, violate Federal Reserve Bank policies, constitute a misuse of Minneapolis Fed resources, and ultimately undermine the Federal Reserve’s independence and credibility.”

It remains to be seen whether Congress will ultimately accept the arguments of Federal Reserve policymakers such as Kashkari and Raskin that the Fed needs to interpret its mandate from Congress more broadly, or whether Congress will decide to amend the Federal Reserve Act to more explicitly limit the boundaries of Fed action—or to reduce Fed independence in some other ways.

Sources: Sarah Bloom Raskin, “Why Is the Fed Spending So Much Money on a Dying Industry?” New York Times, May 28, 2020; Andrew Ackerman and Ken Thomas, “Sarah Bloom Raskin Withdraws as Biden’s Pick for Top Fed Banking Regulator,” Wall Street Journal, March 15, 2022; Michael S. Derby, “GOP Senator Criticizes Minneapolis Fed Over Education Issue,” Wall Street Journal, April 12, 2022; Federal Reserve Bank of Minneapolis, “Page Amendment: Every Child Deserves a Quality Public Education,” minneapolisfed.org; and Pat Toomey, “Letter to Neel Kashkari,” banking.senate. gov, April 11, 2022.