Chair Jerome Powell at a meeting of the Federal Open Market Committee (photo from federalreserve.gov)

At the beginning of the year, there was an expectation among some economists and policymakers that the Fed’s policy-making Federal Open Market Committee (FOMC) would begin cutting its target range for the federal funds rate at the meeting that ended today (May 1). The Fed appeared to be bringing the U.S. economy in for a soft landing—inflation returning to the Fed’s 2 percent target without a recession occurring.

During the first quarter of 2024, production and employment have been expanding more rapidly than had been expected and inflation has been higher than expected. As a result, the nearly universal expectation prior to this meeting was that the FOMC would leave its target for the federal funds rate unchanged. Some economists and investment analysts have begun discussing the possiblity that the committee might not cut its target at all during 2024. The view that interest rates will be higher for longer than had been expected at the beginning of the year has contributed to increases in long-term interest rates, including the interest rates on the 10-year Treasury Note and on residential mortgage loans.

The statement that the FOMC issued after the meeting confirmed the consensus view:

“Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.”

In his press conference after the meeting, Fed Chair Jerome Powell emphasized that the FOMC was unlikely to cut its target for the federal funds rate until data indicated that the inflation rate had resumed falling towards the Fed’s 2 percent target. At one point in the press conference Powell noted that although it was taking longer than expected for the inflation rate to decline he still expected that the pace of economic actitivity was likely to slow sufficiently to allow the decline to take place. He indicated that—contrary to what some economists and investment analysts had suggested—it was unlikely that the FOMC would raise its target for the federal funds rate at a future meeting. He noted that the possibility of raising the target was not discussed at this meeting.

Was there any news in the FOMC statement or in Powell’s remarks at the press conference? One way to judge whether the outcome of an FOMC meeting is consistent with the expectations of investors in financial markets prior to the meeting is to look at movements in stock prices during the time between the release of the FOMC statement at 2 pm and the conclusion of Powell’s press conference at about 3:15 pm. The following figure from the Wall Street Journal, shows movements in the three most widely followed stock indexes—the Dow Jones Industrial Average, the S&P 500, and the Nasdaq composite. (We discuss movements in stock market indexes in Macroeconomics and Essentials of Economics, Chapter 6, Section 6.2 and in Economics, Chapter 8, Section 8.2.)

If either the FOMC statement or the Powell’s remarks during his press conference had raised the possibility that the committee was considering raising its target for the federal funds rate, stock prices would likely have declined. The decline would reflect investors’ concern that higher interest rates would slow the economy, reducing future corporate profits. If, on the other hand, the statement and Powell’s remarks indicated that the committee would likely cut its target for the federal funds rate relatively soon, stock prices would likely have risen. The figure shows that stock prices began to rise after the 2 pm release of the FOMC statement. Prices rose further as Powell seemed to rule out an increase in the target at a future meeting and expressed confidence that inflation would resume declining toward the 2 percent target. But, as often happens in the market, this sentiment reversed towards the end of Powell’s press conference and two of the three stock indexes ended up lower at the close of trading at 4 pm. Presumably, investors decided that on reflection there was no news in the statement or press conference that would change the consensus on when the FOMC might begin lowering its target for the federal funds rate.

The next signficant release of macroeconomic data will come on Friday when the Bureau of Labor Statistics issues its employment report for April.

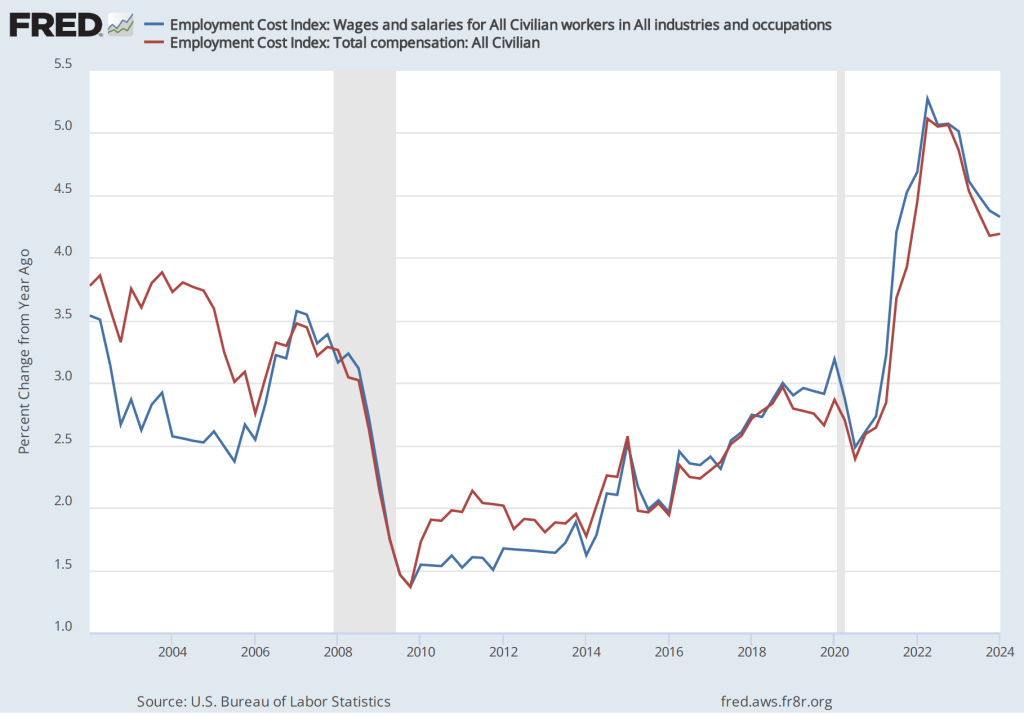

The latest significant piece of macroeconomic data that will be available to the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) before it concludes its meeting tomorrow is the report on the Employment Cost Index (ECI), released this morning by the Bureau of Labor Statistics (BLS). As we’ve noted in earlier posts, as a measure of the rate of increase in labor costs, the FOMC prefers the ECI to average hourly earnings (AHE) .

The AHE is calculated by adding all of the wages and salaries workers are paid—including overtime and bonus pay—and dividing by the total number of hours worked. As a measure of how wages are increasing or decreasing during a particular period, AHE can suffer from composition effects because AHE data aren’t adjusted for changes in the mix of occupations workers are employed in. For example, during a period in which there is a decline in the number of people working in occupations with higher-than-average wages, perhaps because of a downturn in some technology industries, AHE may show wages falling even though the wages of workers who are still employed have risen. In contrast, the ECI holds constant the mix of occupations in which people are employed. The ECI does have the drawback, that it is only available quarterly whereas the AHE is available monthly.

The data released this morning indicate that labor costs continue to increase at a rate that is higher than the rate that is likely needed for the Fed to hit its 2 percent price inflation target. The following figure shows the percentage change in the employment cost index for all civilian workers from the same quarter in 2023. The blue line looks only at wages and salaries while the red line is for total compensation, including non-wage benefits like employer contributions to health insurance. The rate of increase in the wage and salary measure decreased slightly from 4.4 percent in the fourth quarter of 2023 to 4.3 percent in the first quarter of 2024. The rate of increase in compensation was unchanged at 4.2 percent in both quarters.

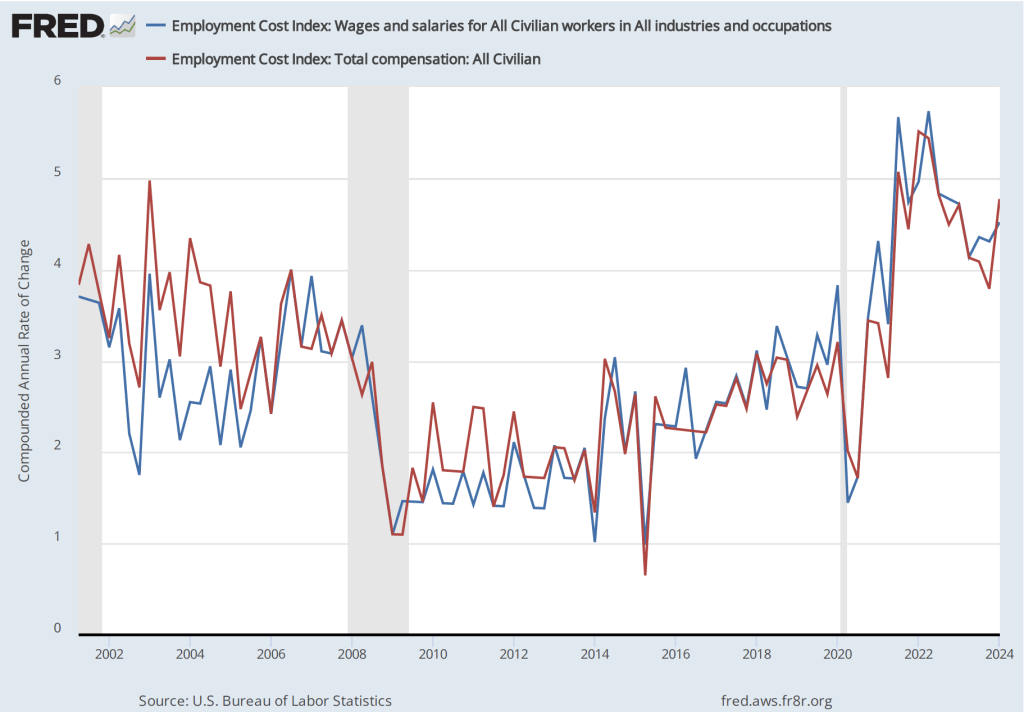

If we look at the compound annual growth rate of the ECI—the annual rate of increase assuming that the rate of growth in the quarter continued for an entire year—we find that the rate of increase in wages and salaries increased from 4.3 percent in the fourth quarter of 2023 to 4.5 percent in the first quarter of 2024. Similarly, the rate of increase in compensation increased from 3.8 percent in the third quarter of 2023 to 4.5 percent in the first quarter of 2024.

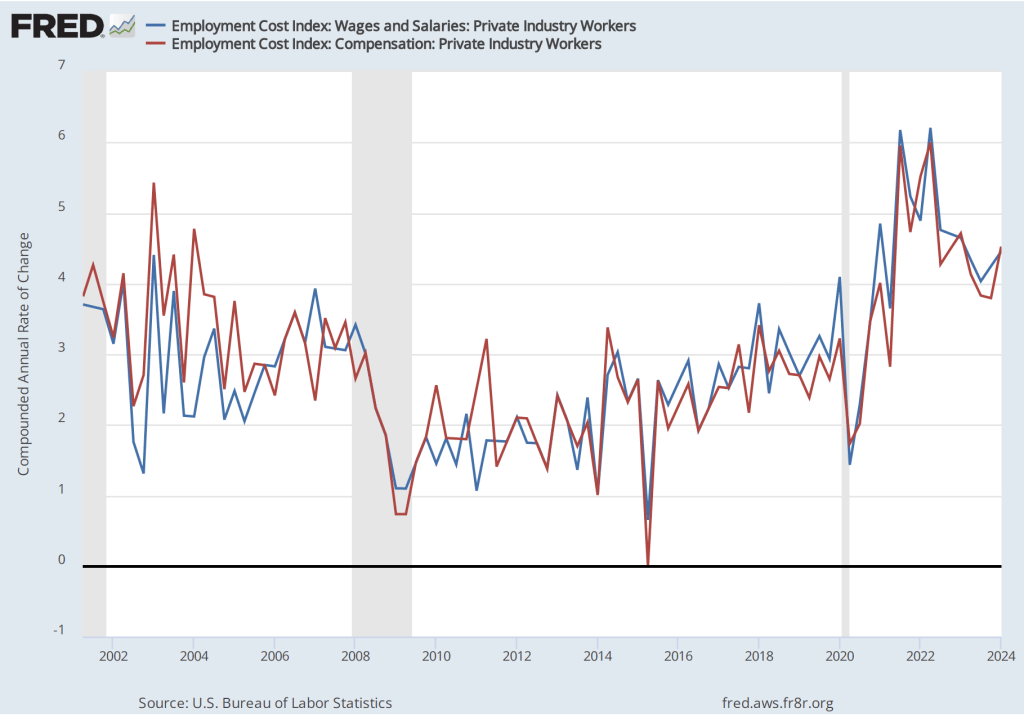

Some economists and policymakers prefer to look at the rate of increase in ECI for private industry workers rather than for all civilian workers because the wages of government workers are less likely to respond to inflationary pressure in the labor market. The first of the following figures shows the rate of increase of wages and salaries and in total compensation for private industry workers measured as the percentage increase from the same quarter in the previous year. The second figure shows the rate of increase calculated as a compound growth rate.

The first figure shows a slight decrease in the rate of growth of labor costs from the fourth quarter of 2023 to the first quarter of 2024, while the second figure shows a fairly sharp increase in the rate of growth.

Taken together, these four figures indicate that there is little sign that the rate of increase in employment costs is falling to a level consistent with a 2 percent inflation rate. At his press conference tomorrow afternoon, following the conclusion of the FOMC’s meeting, Fed Chair Jerome Powell will give his thoughts on the implications for future monetary policy 0f recent macroeconomic data.

Federal Reserve Chair Jerome Powell (Photo from federalreserve.gov)

In a post yesterday, we noted that the quarterly data on the personal consumption expenditures (PCE) price index in the latest GDP report released by the Bureau of Economic Analysis (BEA) indicated that inflation was running higher than expected. Today (April 26), the BEA released its “Personal Income and Outlays” report for March, which includes monthly data on the PCE. The monthly data are consistent with the quarterly data in showing that PCE inflation remains higher than the Federal Reserve’s 2 percent annual inflation target. (A reminder that PCE inflation is particularly important because it’s the inflation measure the Fed uses to gauge whether it’s hitting its inflation target.)

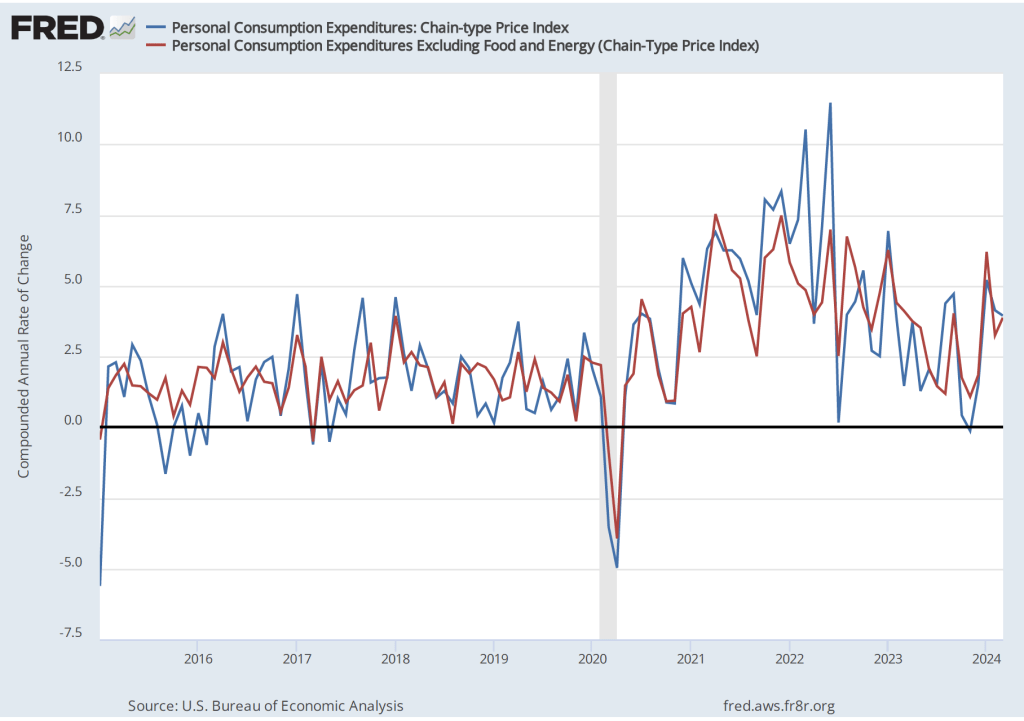

The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—with inflation measured as the percentage change in the PCE from the same month in the previous year. Many economists believe that core inflation gives a better gauge of the underlying inflation rate. Measured this way, PCE inflation increased from 2.5 percent in February to 2.7 percent in March. Core PCE inflation remained unchanged at 2.8 percent.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation declined from 4.1 percent in February to 3.9 percent in March. Core PCE inflation increased from 3.2 percent in February to 3.9 in March. So, March was another month in which both PCE inflation and core PCE inflation remained well above the Fed’s 2 percent inflation target.

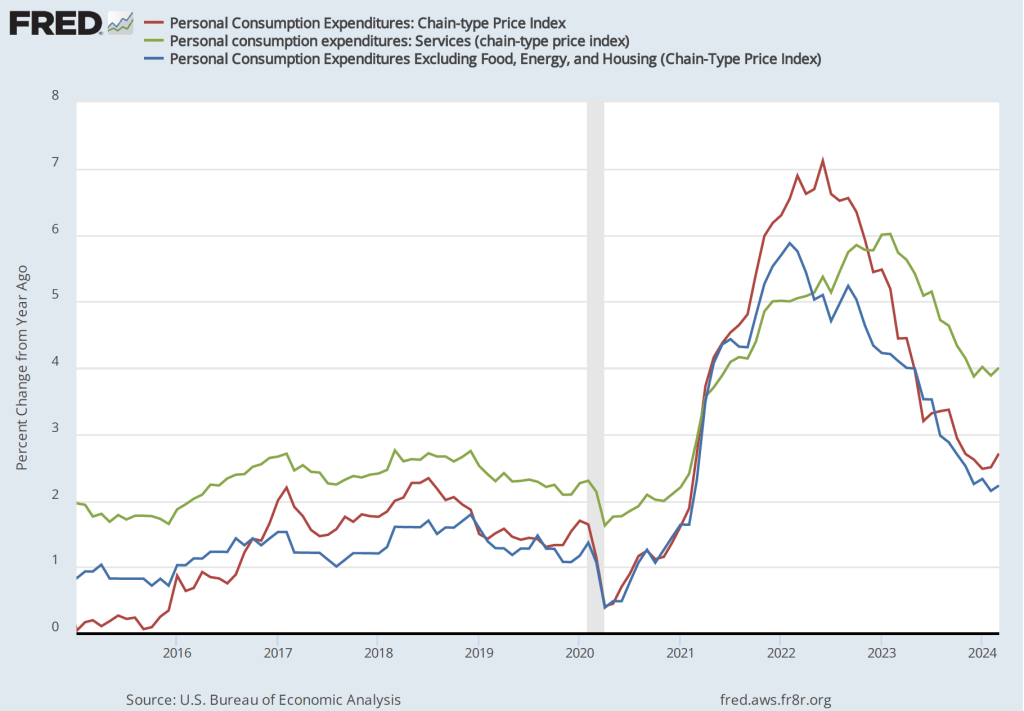

The following figure shows other ways of gauging inflation by including the 12-month inflation rate in the PCE (the same as shown in the figure above—although note that PCE inflation is now the red line rather than the blue line), inflation as measured using only the prices of the services included in the PCE (the green line), and the rate of inflation (the blue line) excluding the prices of housing, food, and energy. Fed Chair Jerome Powell has said that he is particularly concerned by elevated rates of inflation in services. Some economists believe that the price of housing isn’t accurately measured in the PCE, which makes it interesting to see if excluding the price of housing makes much difference in calculating the inflation rate. All three measures of inflation increased from February to March, with inflation in services remaining well above overall inflation and inflation excluding the prices of housing, food, and energy being somewhat lower than overall inflation.

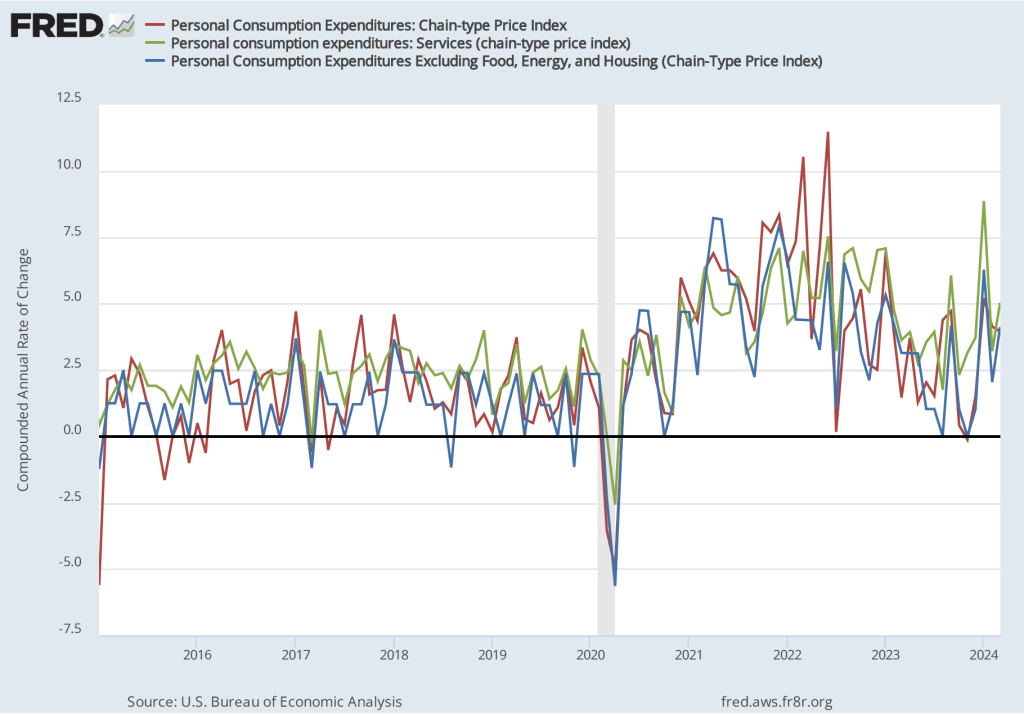

The following figure uses the same three inflation measures as the figure above, but shows the 1-month inflation rate rather than the 12-month inflation rate. Measured this way, inflation in services increased sharply from 3.2 percent in February to 5.0 percent in March. Inflation excluding the prices of housing, food, and energy doubled from 2.0 percent in February to 4.1 percent in March.

Overall, the data in this report indicate that the decline in inflation during the second half of 2023 hasn’t continued in the first three months of 2024. In fact, the inflation rate may be slightly increasing. As a result, it no longer seems clear that the Fed’s policy-making Federal Open Market Committee (FOMC) will cut its target for the federal funds rate this year. (We discuss the possibility that the FOMC will keep its target unchanged through the end of the year in this blog post.) At the press conference following the FOMC’s next meeting on April 30-May 1, Fed Chair Jerome Powell may explain what effect the most recent data have had on the FOMC’s planned actions during the remainder of the year.

Federal Reserve Vice Chair Philip Jefferson (photo from the Federal Reserve)

Federal Reserve Chair Jerome Powell (photo from the Federal Reserve)

At the beginning of 2024, investors were expecting that during the year the Fed’s policy-making Federal Open Market Committee (FOMC) would cut its target range for the federal funds rate six or seven times. At its meeting on March 19-20 the economic projections of the members of the FOMC indicated that they were expecting to cut the target range three times from its current 5.25 percent to 5.50 percent. But, as we noted in this recent post and in this podcast, macroeconomic data during the first three months of this year indicated that the U.S. economy was growing more rapidly than the Fed had expected and the reductions in inflation that occurred during the second half of 2023 had not persisted into the beginning of 2024.

The unexpected strength of the economy and the persistence of inflation above the Fed’s 2 percent target have raised the issue of whether the FOMC will cut its target range for the federal funds rate at all this year. Earlier this month, Neel Kashkari, president of the Federal Reserve Bank of Minneapolis raised the possibility that the FOMC would not cut its target range this year.

Today (April 16) both Fed Vice Chair Philip Jefferson and Fed Chair Jerome Powell addressed the issue of monetary policy. They gave what appeared to be somewhat different signals about the likely path of the federal funds target during the remainder of this year—bearing in mind that Fed officials never commit to any specific policy when making a speech. Adressing the International Research Forum on Monetary Policy, Vice Chair Jefferson stated that:

“My baseline outlook continues to be that inflation will decline further, with the policy rate held steady at its current level, and that the labor market will remain strong, with labor demand and supply continuing to rebalance. Of course, the outlook is still quite uncertain, and if incoming data suggest that inflation is more persistent than I currently expect it to be, it will be appropriate to hold in place the current restrictive stance of policy for longer.”

One interpretation of his point here is that he is still expecting that the FOMC will cut its target for the federal funds rate sometime this year unless inflation remains persistently higher than the Fed’s target—which he doesn’t expect.

Chair Powell, speaking at a panel discussion at the Wilson Center in Washington, D.C., seemed to indicate that he believed it was less likely that the FOMC would reduce its federal funds rate target in the near future. The Wall Street Journal summarized his remarks this way:

“Federal Reserve Chair Jerome Powell said firm inflation during the first quarter had introduced new uncertainty over whether the central bank would be able to lower interest rates this year without signs of an economic slowdown. His remarks indicated a clear shift in the Fed’s outlook following a third consecutive month of stronger-than-anticipated inflation readings ….”

An article on bloomberg.com had a similar interpretation of Powell’s remarks: “Federal Reserve Chair Jerome Powell signaled policymakers will wait longer than previously anticipated to cut interest rates following a series of surprisingly high inflation readings.”

Politics may also play a role in the FOMC’s decisions. As we discuss in Macroeconomics, Chapter 17, Section 17.4 (Economics, Chapter 27, Section 27.4), the Federal Reserve Act, which Congress passed in 1913 and has amended several times since, puts the Federal Reserve in an unusal position in the federal government. Although the members of the Board of Governors are appointed by the president and confirmed by the Senate, the Fed was intended to act independently of Congress and the president. Over the years, Fed Chairs have protected that independence by, for the most part, avoiding taking actions beyond the narrow responsibilites Congress has given to the Fed by Congress and by avoiding actions that could be interpreted as political.

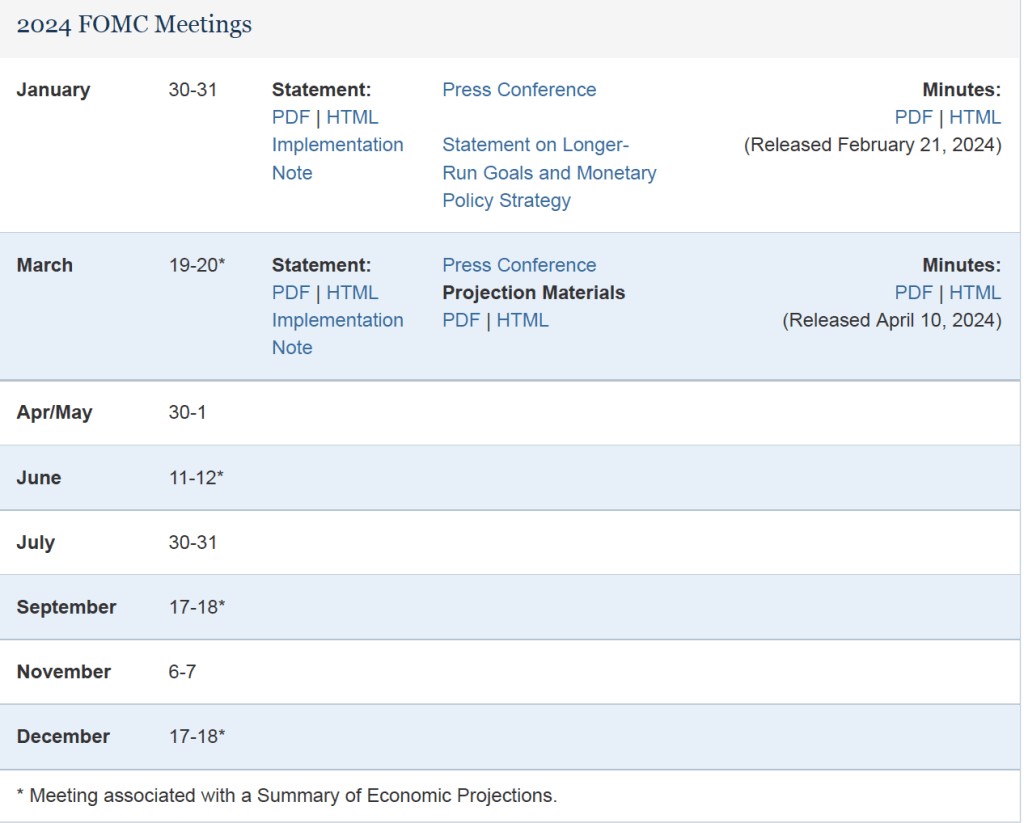

This year is, of course, a presidential election year. The following table from the Fed’s web site lists the FOMC meetings this year. The presidential election will occur on November 5. There are four scheduled FOMC meetings before then. Given that inflation has been running well above the Fed’s target during the first three months of the year, it would likely take at least two months of lower inflation data—or a weakening of the economy as indicated by a rising unemployment rate—before the FOMC would consider lowering its federal funds rate target. If so, the meeting on July 30-31 might be the first meeting at which a rate reduction would occur. If the FOMC doesn’t act at its July meeting, it might be reluctant to cut its target at the September 17-18 meeting because acting close to the election might be interpreted as an attempt to aid President Joe Biden’s reelection.

Although we don’t know whether avoiding the appearance of intervening in politics is an important consideration for the members of the FOMC, some discussion in the business press raises the possibility. For instance, a recent article in the Wall Street Journal noted that:

“The longer that officials wait, the less likely there will be cuts this year, some analysts said. That is because officials will likely resist starting to lower rates in the midst of this year’s presidential election campaign to avoid political entanglements.”

These are clearly not the easiest times to be a Fed policymaker!

In a recent podcast we discussed what actions the Fed may take if inflation continues to run well above the Fed’s 2 percent target. We are likely a step closer to finding out with the release this morning (April 10) by the Bureau of Labor Statistics (BLS) of data on the consumer price index (CPI) for March. The inflation rate measured by the percentage change in the CPI from the same month in the previous month—headline inflation—was 3.5 percent, slightly higher than expected (as indicated here and here). As the following figure shows, core inflation—which excludes the prices of food and energy—was 3.8 percent, the same as in January.

If we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—the values seem to confirm that inflation, while still far below its peak in mid-2022, has been running somewhat higher than it did during the last months of 2023. Headline CPI inflation in March was 4.6 percent (down from 5.4 percent in February) and core CPI inflation was 4.4 percent (unchanged from February). It’s worth bearing in mind that the Fed’s inflation target is measured using the personal consumption expenditures (PCE) price index, not the CPI. But CPI inflation at these levels is not consistent with PCE inflation of only 2 percent.

As has been true in recent months, the path of inflation in the prices of services has been concerning. As we’ve noted in earlier posts, Federal Reserve Chair Jerome Powell has emphasized that as supply chain problems have gradually been resolved, inflation in the prices of goods has been rapidly declining. But inflaion in services hasn’t declined nearly as much. Last summer he stated the point this way:

“Part of the reason for the modest decline of nonhousing services inflation so far is that many of these services were less affected by global supply chain bottlenecks and are generally thought to be less interest sensitive than other sectors such as housing or durable goods. Production of these services is also relatively labor intensive, and the labor market remains tight. Given the size of this sector, some further progress here will be essential to restoring price stability.”

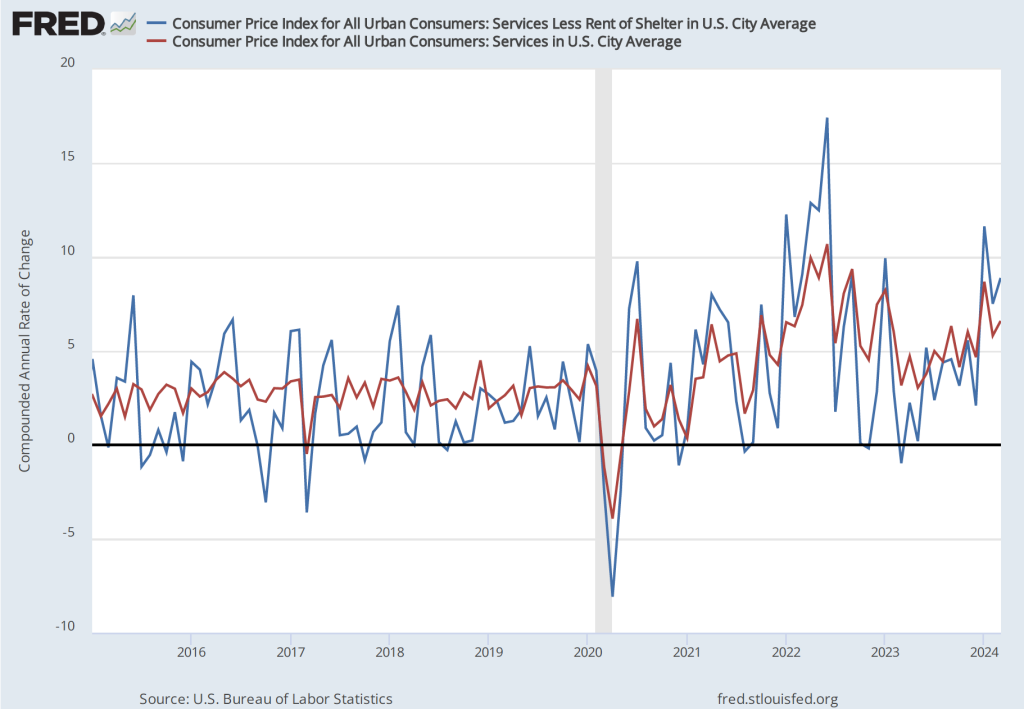

The following figure shows the 1-month inflation rate in services prices and in services prices not included including housing rent. Some economists believe that the rent component of the CPI isn’t well measured and can be volatile, so it’s worthwhile to look at inflation in service prices not including rent. The figure shows that inflation in all service prices has been above 4 percent in every month since July 2023. Inflation in service prices increased from 5.8 percent in February to 6.6 percent in March . Inflation in service prices not including housing rent was even higher, increasing from 7.5 percent in February to 8.9 percent in March. Such large increases in the prices of services, if they were to continue, wouldn’t be consistent with the Fed meeting its 2 percent inflation target.

Finally, some economists and policymakers look at median inflation to gain insight into the underlying trend in the inflation rate. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates. As the following figure shows, although median inflation declined in March, it was still high at 4.3 percent. Median inflation is volatile, but the trend has been generally upward since July 2023.

Financial investors, who had been expecting that this CPI report would show inflation slowing, reacted strongly to the news that, in fact, inflation had ticked up. As of late morning, the Dow Jones Industrial Average had decline by nearly 500 points and the S&P 5o0 had declined by 59 points. (We discuss the stock market indexes in Macroeconomics, Chapter 6, Section 6.2 and in Microeconomics and Economics, Chapter 8, Section 8.2.) The following figure from the Wall Street Journal shows the sharp reaction in the bond market as the interest rate on the 10-year Treasury note rose sharply following the release of the CPI report.

Lower stock prices and higher long-term interest rates reflect the fact that investors have changed their views concerning when the Fed’s Federal Open Market Committee (FOMC) will cut its target for the federal funds and how many rate cuts there may be this year. At the start of 2024, the consensus among investors was for six or seven rate cuts, starting as early as the FOMC’s meeting on March 19-20. But with inflation remaining persistently high, investors had recently been expecting only two or three rate cuts, with the first cut occurring at the FOMC’s meeting on June 11-12. Two days ago, Neel Kashkari, president of the Federal Reserve Bank of Minneapolis raised the possibility that the FOMC might not cut its target for the federal funds rate during 2024. Some economists have even begun to speculate that the FOMC might feel obliged to increase its target in the coming months.

After the FOMC’s next meeting on April 30-May 1 first, Chair Powell may provide some additional information on the committee’s current thinking.

McDonald’s raising the price of its burgers by 10 percent in 2023 led to a decline in sales. (Photo from mcdonalds.com)

Inflation as measured by changes in the consumer price index (CPI) receives the most attention in the media, but the Federal Reserve looks instead to inflation as measured by changes in personal consumption expenditures (PCE) price index when evaluating whether it is meeting its 2 percent inflation target. The Bureau of Economic Analysis (BEA) released PCE data for February as part of its “Personal Income and Outlays” report on March 29.

The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—for the period since January 2015 with inflation measured as the change in PCE from the same month in the previous year. Measured this way, PCE inflation increased slightly from 2.4 percent in January to 2.5 percent in February. Core PCE inflation decreased slightly from 2.9 percent to 2.8 percent.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, both PCE inflation and core PCE inflation declined in February, but the decline only partly offset the sharp increases in December and January. Both PCE inflation—at 4.1 percent—and core PCE inflation—at 3.2 percent—remained well above the Fed’s 2 percent target.

The following figure shows another way of gauging inflation by including the 12-month inflation rate in the PCE (the same as shown in the figure above—although note that PCE inflation is now the red line rather than the blue line), inflation as measured using only the prices of the services included in the PCE (the green line), and the trimmed mean rate of PCE inflation (the blue line). Fed Chair Jerome Powell has said that he is particularly concerned by elevated rates of inflation in services. The trimmed mean measure is compiled by economists at the Federal Reserve Bank of Dallas by dropping from the PCE the goods and services that have the highest and lowest rates of inflation. It can be thought of as another way of looking at core inflation.

In February, 12-month trimmed mean PCE inflation was 3.1 percent, a little below core inflation of 3.3 percent. Twelve-month inflation in services was 3.8 percent, a slight decrease from 3.9 percent in January. Trimmed mean and services inflation tell the same story as PCE and PCE core inflation: Inflation has decline significantly from its highs of mid-2022, but remains stubbornly above the Fed’s 2 percent target.

It seems unlikely that this month’s PCE data will have much effect on when the members of the Federal Open Market Committee will decide to lower the target for the federal funds rate.

The Bureau of Economic Analysis (BEA) has issued its third estimate of real GDP for the fourth quarter of 2023. The BEA now estimates that real GDP increased in the fourth quarter of 2023 at an annual rate of 3.4 percent, an increase from the BEA’s second estimate of 3.2 percent. The BEA noted that: “The update primarily reflected upward revisions to consumer spending and nonresidential fixed investment that were partly offset by a downward revision to private inventory investment.”

As the blue line in the following figure shows, despite the upward revision, fourth quarter growth in real GDP decline significantly from the very high growth rate of 4.9 percent in the third quarter. In addition, two widely followed “nowcast” estimates of real GDP growth in the first quarter of 2024 show a futher slowdown. The nowcast from the Federal Reserve Bank of Atlanta estimates that real GDP will have grown at an annualized rate of 2.1 percent in the first quarter and the nowcast from the Federal Reserve Bank of New York estimates a growth rate of 1.9 percent. (The Atlanta Fed describes its nowcast as “a running estimate of real GDP growth based on available economic data for the current measured quarter.” The New York Fed explains: “Our model reads the flow of information from a wide range of macroeconomic data as they become available, evaluating their implications for current economic conditions; the result is a ‘nowcast’ of GDP growth ….”)

Data on growth in real gross domestic income (GDI), on the other hand, show an upward trend, as indicated by the red line in the figure. As we discuss in Macroeconomics, Chapter 8, Section 8.4 (Economics, Chapter 18, Section 18.4), gross domestic product measures the economy’s output from the production side, while gross domestic income does so from the income side. The two measures are designed to be equal, but they can differ because each measure uses different data series and the errors in data on production can differ from the errors in data on income. Economists differ on whether data on growth in real GDP or data on growth in real GDI do a better job of forecasting future changes in the economy. Accordingly, economists and policymakers will differ on how much weight to put on the fact that while the growth in real GDI had been well below growth in real GDP from the fourth quarter of 2022 to the fourth quarter of 2023, during the fourth quarter of 2023, growth in real GDI was 1.5 percentage points higher than growth in real GDP.

On balance, it seems likely that these data will reinforce the views of those members of the Fed’s policy-making Federal Open Market Committee (FOMC) who were cautious about reducing the target for the federal funds rate until the macroeconomic data indicate more clearly that the economy is slowing sufficiently to ensure that inflation is returning to the Fed’s 2 percent target. In a speech on March 27 (before the latest GDP revisions became available), Fed Governor Christopher Waller reviewed the most recent macro data and concluded that:

“Adding this new data to what we saw earlier in the year reinforces my view that there is no rush to cut the [federal funds] rate. Indeed, it tells me that it is prudent to hold this rate at its current restrictive stance perhaps for longer than previously thought to help keep inflation on a sustainable trajectory toward 2 percent.”

Most other members of the FOMC appear to share Waller’s view.

Federal Reserve Chair Jerome Powell (Photo from the New York Times)

As always, economists and investors had been awaiting the outcome of today’s meeting of the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) to get further insight into future monetary policy. The expectation has been that the FOMC would begin reducing its target for the federal funds rate, mostly likely beginning with its meeting on June 11-12. Financial markets were expecting that the FOMC would make three 0.25 percentage point cuts by the end of the year, reducing its target range from the current 5.25 to 5.50 percent to 4.50 to 4.75 percent.

There appears to be nothing in the committees statement (found here) or in Powell’s press conference following the meeting to warrant a change in expectations of future Fed policy. The committee’s statement noted that: “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” As Powell stated in his press conference, although the committee found the general trend in inflation data to be encouraging, they would have to see additional months of data that were consistent with their 2 percent inflation target before reducing their target for the federal funds rate.

As we’ve noted in earlier blog posts (here, here, and here), inflation during January and February has been somewhat higher than expected. Some economists and investors had wondered if, as a result, the committee might delay its first cut in the federal funds target range or implement only two cuts rather than three. In his press conference, Powell seemed unconcerned about the January and February data and expected that falling inflation rates of the second half of 2023 to resume.

Typically, at the FOMC’s December, March, June, and September meetings, the committee releases a “Summary of Economic Projections” (SEP), which presents median values of the committee members’ forecasts of key economic variables.

The table shows that the committee members made relatively small changes to their projections since their December meeting. Most notable was an increase in the median projection of growth in real GDP for 2024 from 1.4 percent at the December meeting to 2.1 percent at this meeting. Correspondingly, the median projection of unemployment during 2024 dropped from 4.1 percent to 4.0 percent. The key projection of the value of the federal funds rate at the end of 2024 was left unchanged at 4.6 percent. As noted earlier, that rate is consistent with three 0.25 percent cuts in the target range during the remainder of the year.

The SEP also includes a “dot plot.” Each dot in the plot represents the projection of an individual committee member. (The committee doesn’t disclose which member is associated with which dot.) Note that there are 19 dots, representing the 7 members of the Fed’s Board of Governors and the 12 presidents of the Fed’s district banks. Although only the president of the New York Fed and the presidents of 4 of the 11 district banks are voting members of the committee, all the district bank presidents attend the committee meetings and provide economic projections.

The plots on the far left of the figure represent the projections of each of the 19 members of the value of the federal funds rate at the end of 2024. These dots are bunched fairly closely around the median projection of 4.6 percent. The dots representing the projections for 2025 and 2026 are more dispersed, representing greater uncertainty among committee members about conditions in the future. The dots on the far right represent the members’ projections of the value of the federal funds rate in the long run. As Table 1 shows, the median projected value is 2.6 percent (up slightly from 2.5 percent in December), although the plot indicates that all but one member expects that the long-run rate will be 2.5 percent or higher. In other words, few members expect a return to the very low federal funds rates of the period from 2008 to 2016.

A bookstore in New York City closed during Covid. (Photo from the New York Times)

Four years ago, in mid-March 2020, Covid–19 began to significantly affect the U.S. economy, with hospitalizations rising and many state and local governments closing schools and some businesses. In this blog post we review what’s happened to key macro variables during the past four years. Each monthly series starts in February 2020 and the quarterly series start in the fourth quarter of 2019.

Production

Real GDP declined by 5.8 percent from the fourth quarter of 2019 to the first quarter of 2020 and by an additional 28.0 percent from the first quarter of 2020 to the second quarter. This decline was by far the largest in such a short period in the history of the United States. From the second quarter to the third quarter of 2020, as businesses began to reopen, real GDP increased by 34.8 percent, which was by far the largest increase in a single quarter in U.S. history.

Industrial production followed a similar—although less dramatic—path to real GDP, declining by 16.8 percent from February 2020 to April 2020 before increasing by 12.3 percent from April 2020 to June 2020. Industrial production did not regain its February 2020 level until March 2022. The swings in industrial production were smaller than the swings in GDP because industrial production doesn’t include the output of the service sector, which includes firms like restaurants, movie theaters, and gyms that were largely shutdown in some areas. (Industrial production measures the real output of the U.S. manufacturing, mining, and electric and gas utilities industries. The data are issued by the Federal Reserve and discussed here.)

Employment

Nonfarm payroll employment, collected by the Bureau of Labor Statistics (BLS) in its establishment survey, followed a path very similar to the path of production. Between February and April 2020, employment declined by an astouding 22 million workers, or by 14.4 percent. This decline was by far the largest in U.S. history over such a short period. Employment increased rapidly beginning in April but didn’t regain its February 2020 level until June 2022.

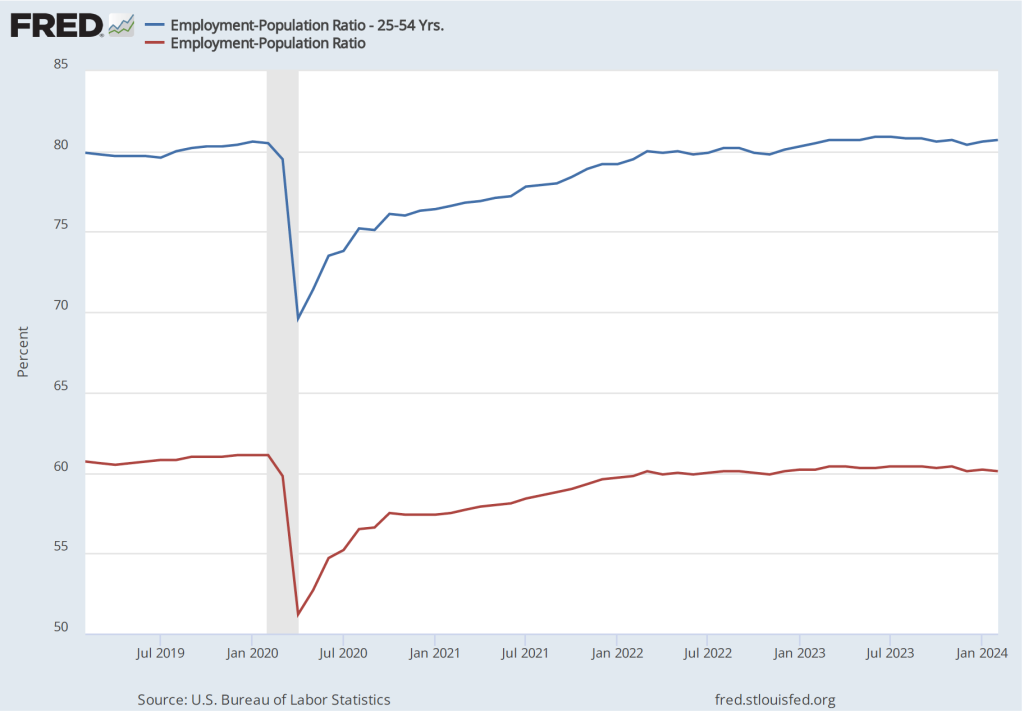

The employment-population ratio measures the percentage of the working-age population that is employed. It provides a more comprehensive measure of an economy’s utilization of available labor than does the total number of people employed. In the following figure, the blue line shows the employment-population ratio for the whole working-age population and the red line shows the employment-population ratio for “prime age workers,” those aged 25 to 54.

For both groups, the employment-population ratio plunged as a result of Covid and then slowly recovered as the production began increasing after April 2020. The employment-population ratio for prime age workers didn’t regain its February 2020 value until February 2023, an indication of how long it took the labor market to fully overcome the effects of the pandemic. As of February 2024, the employment-population ratio for all people of working age hasn’t returned to its February 2020 value, largely because of the aging of the U.S. population.

Average weekly hours worked followed an unusual pattern, declining during March 2020 but then increasing to beyond its February 2020 level to a peak in April 2021. This increase reflects firms attempting to deal with a shortage of workers by increasing the hours of those people they were able to hire. By April 2023, average weekly hours worked had returned to its February 2020 level.

Income

Real average hourly earnings surged by more than six percent between February and April 2020—a very large increase over a two-month period. But some of the increase represented a composition effect—as workers with lower incomes in services industries such as restaurants were more likely to be out of work during this period—rather than an actual increase in the real wages received by people employed during both months. (Real average hourly earnings are calculated by dividing nominal average hourly earnings by the consumer price index (CPI) and multiplying by 100.)

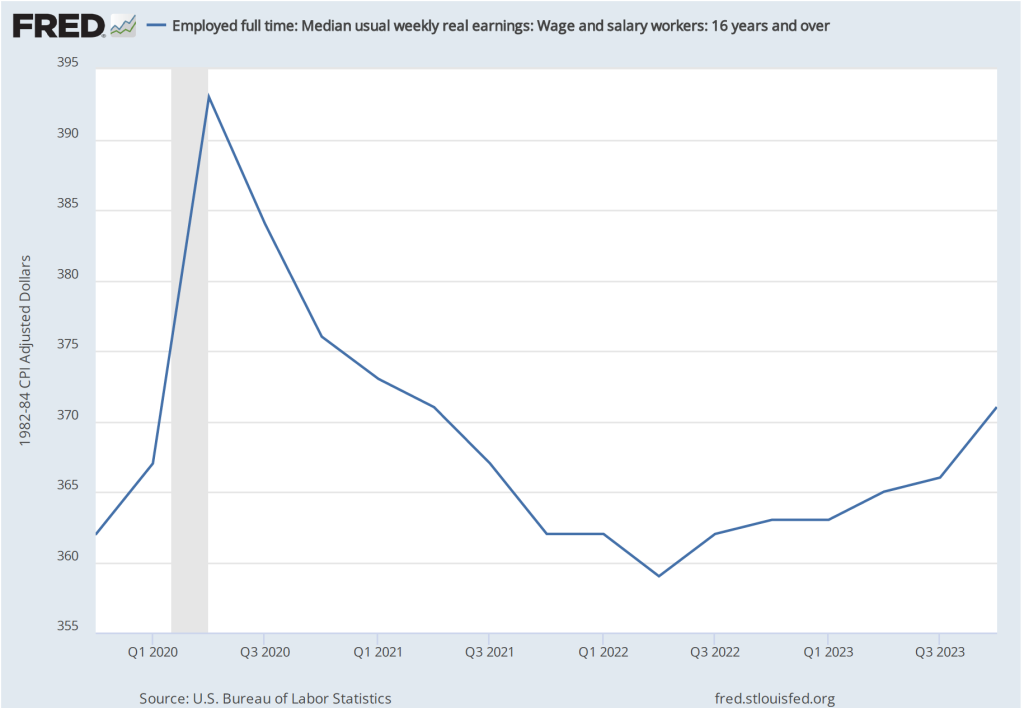

Median weekly real earnings, because it is calculated as a median rather than as an average (or mean), is less subject to composition effects than is real average hourly earnings. Median weekly real earnings increased sharply between February and April of 2020 before declining through June 2022. Earnings then gradually increased. In February 2024 they were 2.5 percent higher than in February 2020.

Inflation

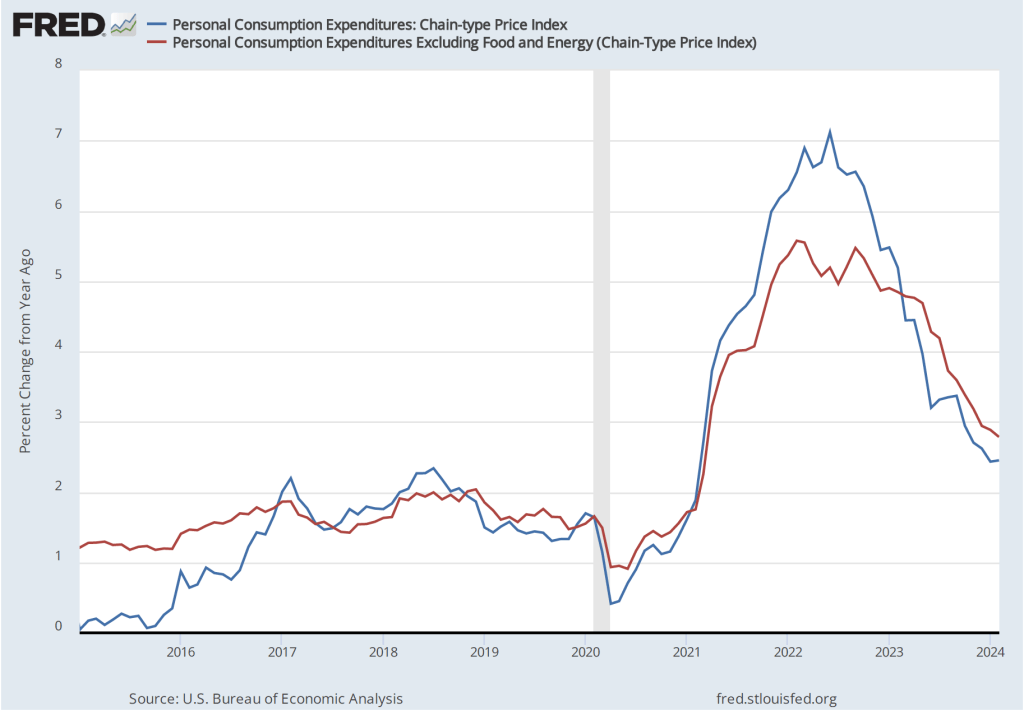

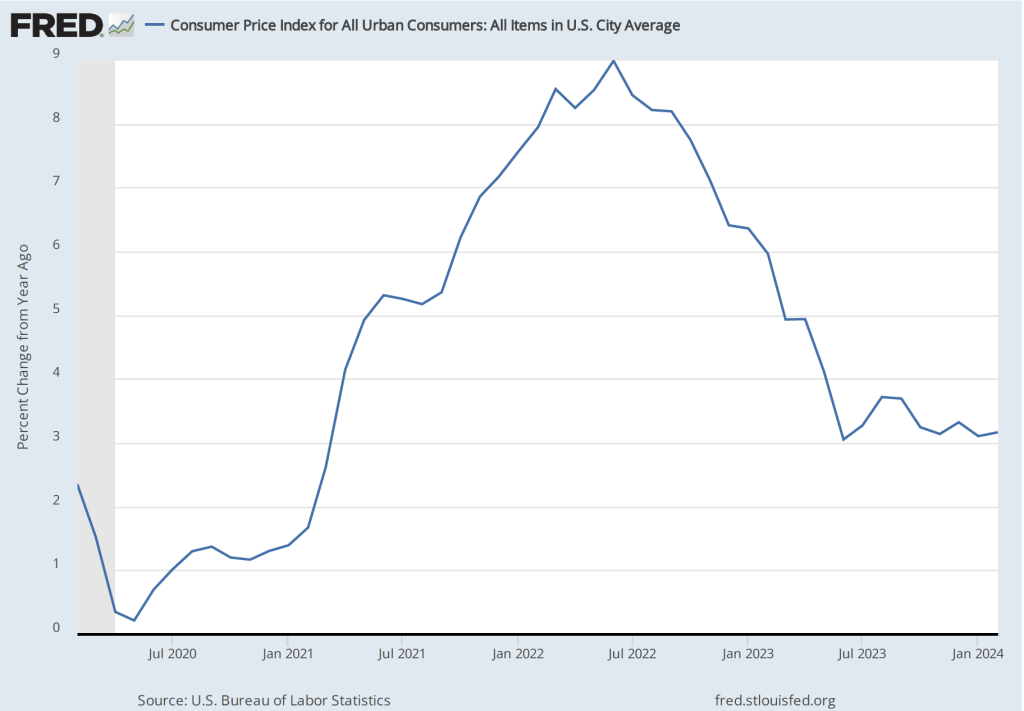

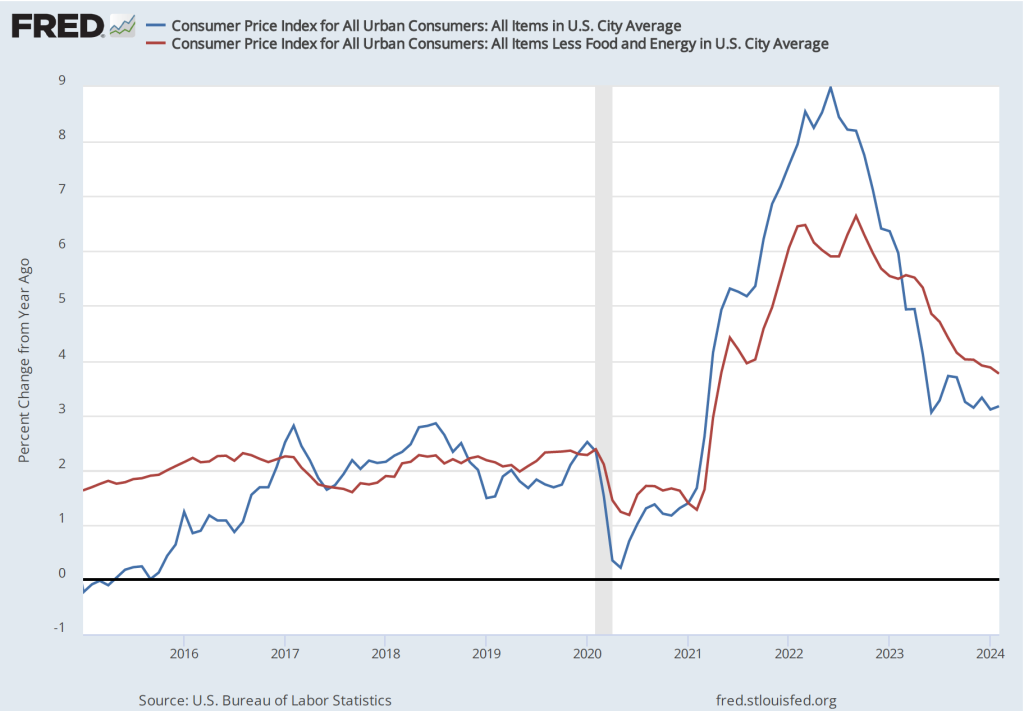

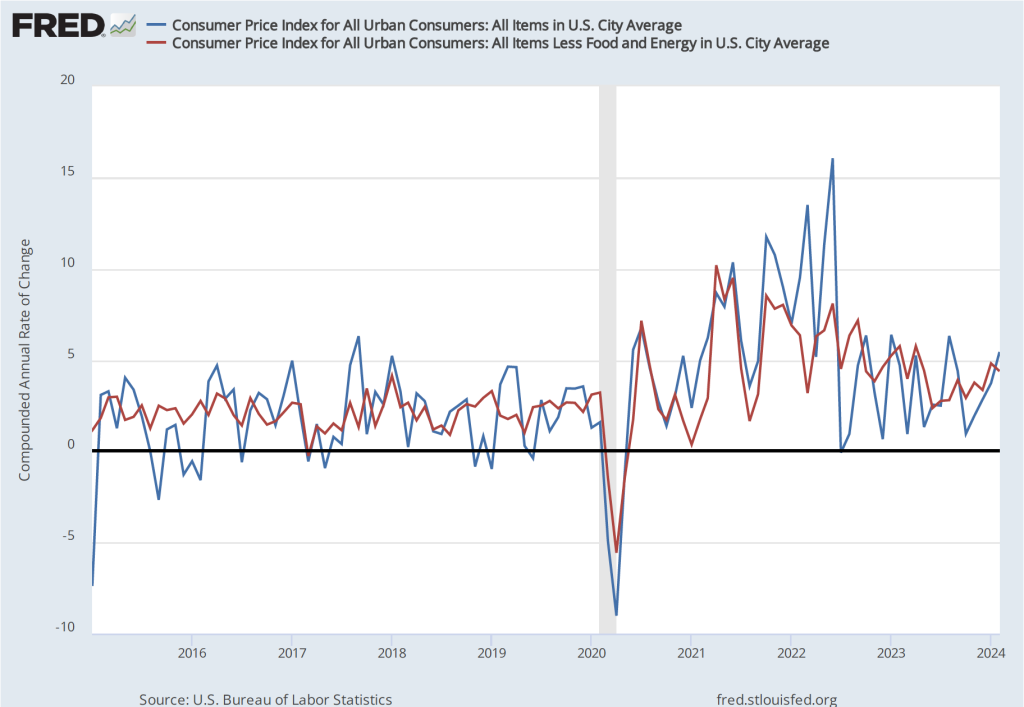

The inflation rate most commonly mentioned in media reports is the percentage change in the CPI from the same month in the previous year. The following figure shows that inflation declined from February to May 2020. Inflation then began to rise slowly before rising rapidly beginning in the spring of 2021, reaching a peak in June 2022 at 9.0 percent. That inflation rate was the highest since November 1981. Inflation then declined steadily through June 2023. Since that time it has fluctuated while remaining above 3 percent.

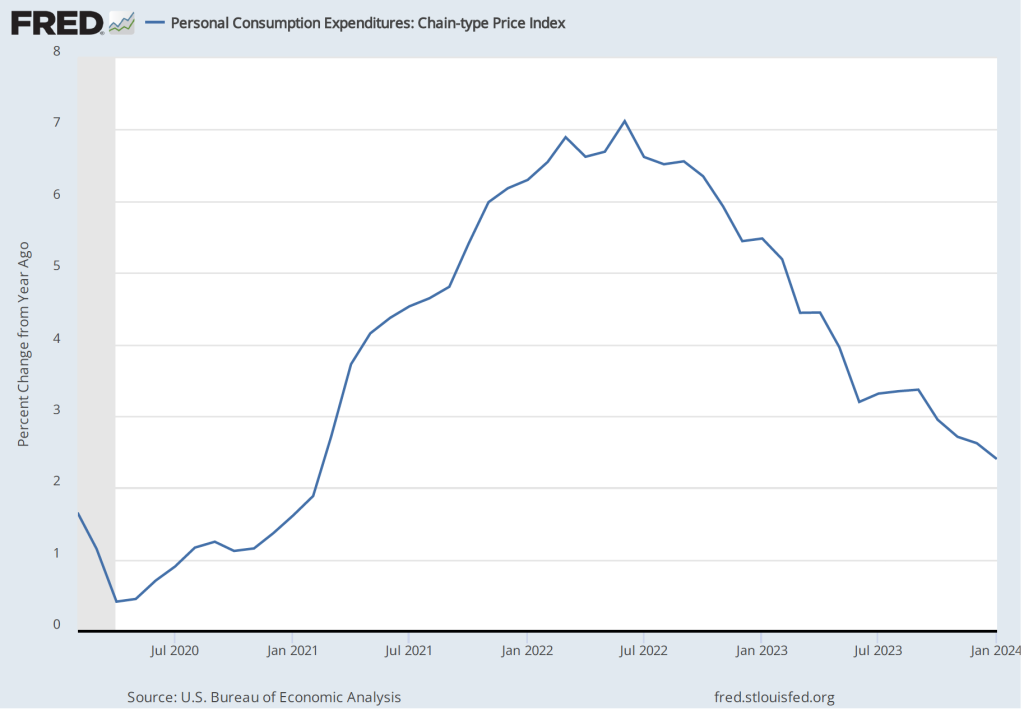

As we discuss in Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5), the Federal Reserve gauges its success in meeting its goal of an inflation rate of 2 percent using the personal consumption expenditures (PCE) price index. The following figure shows that PCE inflation followed roughly the same path as CPI inflation, although it reached a lower peak and had declined below 3 percent by November 2023. (A more detailed discussion of recent inflation data can be found in this post and in this post.)

Monetary Policy

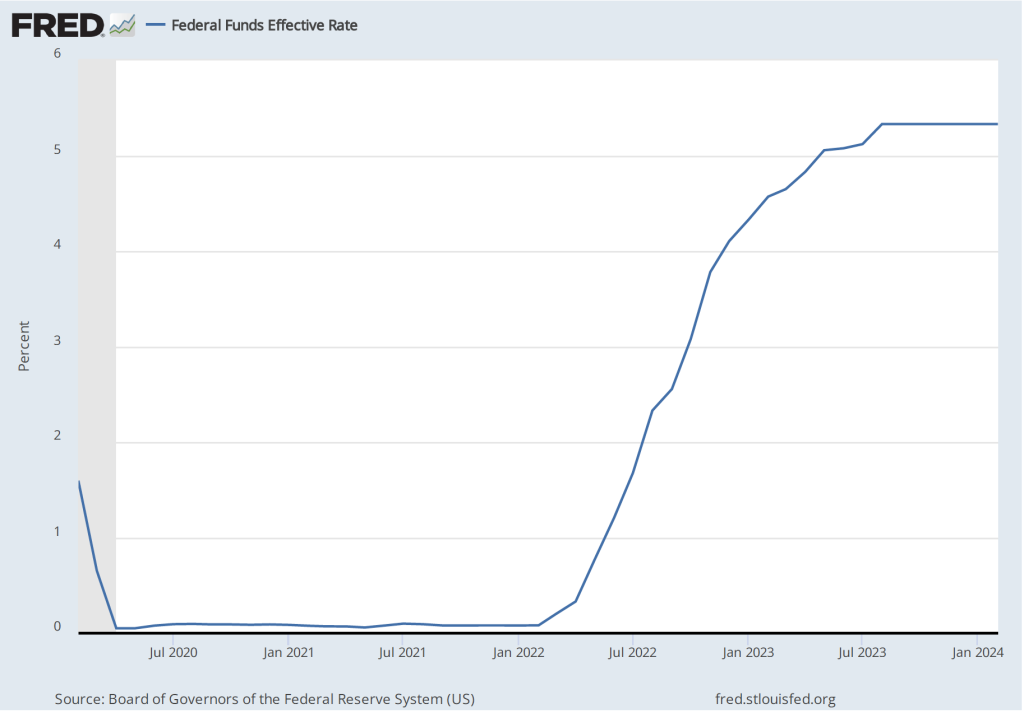

The following figure shows the effective federal funds rate, which is the rate—nearly always within the upper and lower bounds of the Fed’s target range—that prevails during a particular period in the federal funds market. In March 2020, the Fed cut its target range to 0 to 0.25 percent in response to the economic disruptions caused by the pandemic. It kept the target unchanged until March 2022 despite the sharp increase in inflation that had begun a year earlier. The members of the Federal Reserve’s Federal Open Market Committee (FOMC) had initially hoped that the surge in inflation was largely caused by disuptions to supply chains and would be transitory, falling as supply chains returned to normal. Beginning in March 2022, the FOMC rapidly increased its target range in response to continuing high rates of inflation. The targer range reached 5.25 to 5.50 percent in July 2023 where it has remained through March 2024.

Although the money supply is no longer the focus of monetary policy, some economists have noted that the rate of growth in the M2 measure of the money supply increased very rapidly just before the inflation rate began to accelerate in the spring of 2021 and then declined—eventually becoming negative—during the period in which the inflation rate declined.

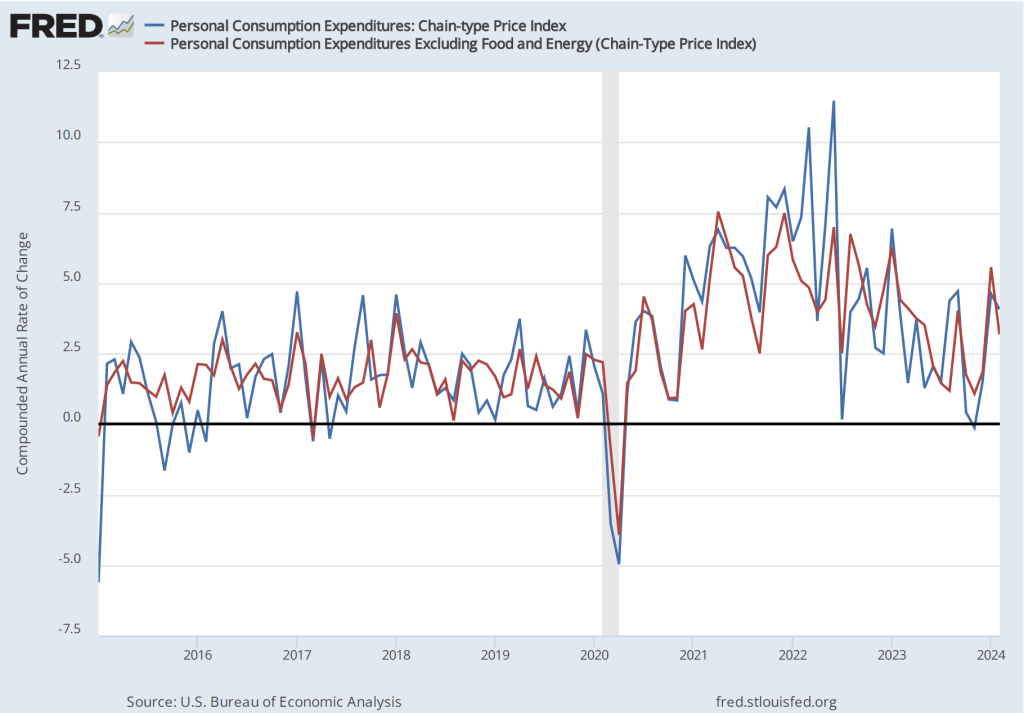

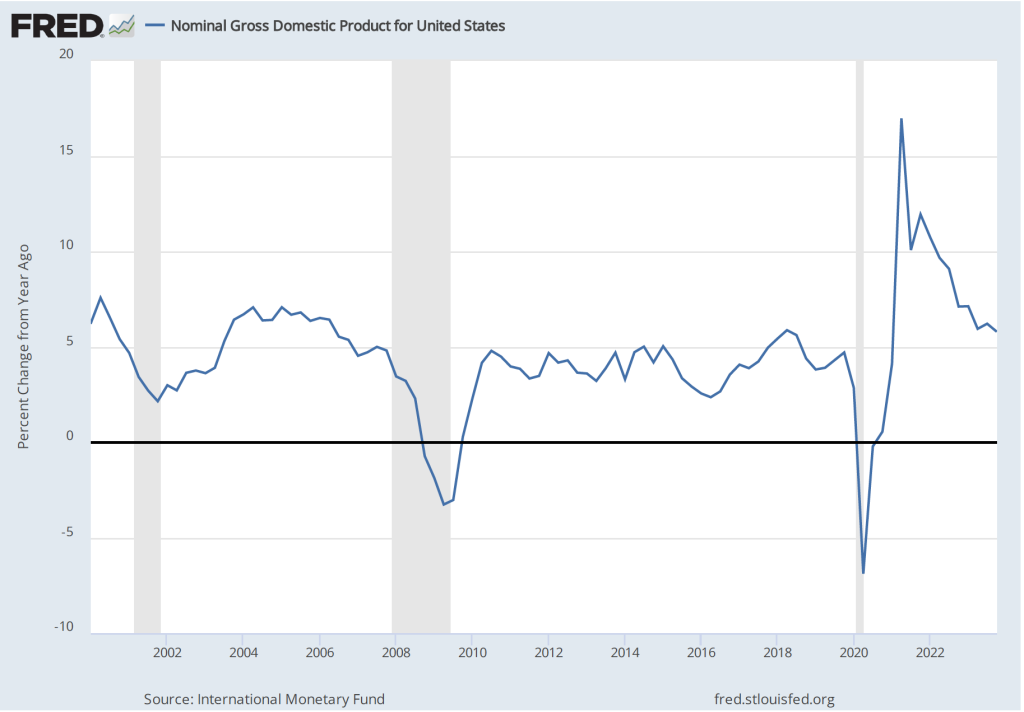

As we discuss in the new 9th edition of Macroeconomics, Chapter 15, Section 15.5 (Economics, Chapter 25, Section 25.5), some economists believe that the FOMC should engage in nominal GDP targeting. They argue that this approach has the best chance of stabilizing the growth rate of real GDP while keeping the inflation rate close to the Fed’s 2 percent target. The following figure shows the economy experienced very high rates of inflation during the period when nominal GDP was increasing at an annual rate of greater than 10 percent and that inflation declined as the rate of nominal GDP growth declined toward 5 percent, which is closer to the growth rates seen during the 2000s. (This figure begins in the first quarter of 2000 to put the high growth rates in nominal GDP of 2021 and 2022 in context.)

Fiscal Policy

As we discuss in the new 9th edition of Macroeconomics, Chapter 15 (Economics, Chapter 25), in response to the Covid pandemic Congress and Presidents Trump and Biden implemented the largest discretionary fiscal policy actions in U.S. history. The resulting increases in spending are reflected in the two spikes in federal government expenditures shown in the following figure.

The initial fiscal policy actions resulted in an extraordinary increase in federal expenditures of $3.69 trillion, or 81.3 percent, from the first quarter to the second quarter of 2020. This was followed by an increase in federal expenditures of $2.31 trillion, or 39.4 percent, from the fourth quarter of 2020 to the first quarter of 2021. As we recount in the text, there was a lively debate among economists about whether these increases in spending were necessary to offest the negative economic effects of the pandemic or whether they were greater than what was needed and contributed substantially to the sharp increase in inflation that began in the spring of 2021.

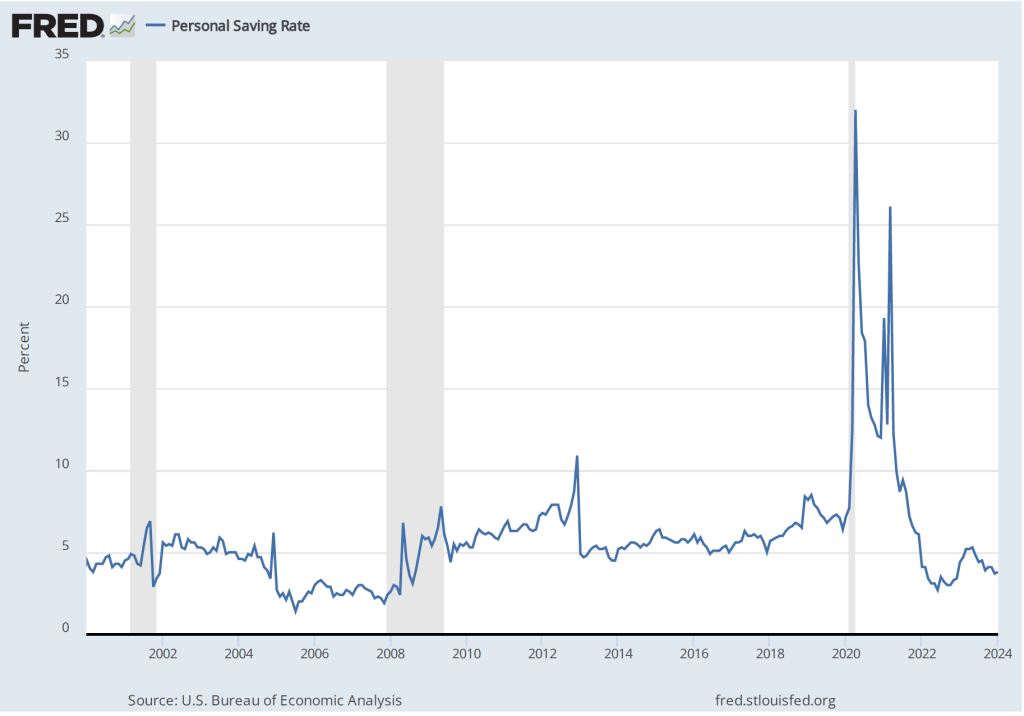

Saving

As a result of the fiscal policy actions of 2020 and 2021, many households received checks from the federal government. In total, the federal government distributed about $80o billion directly to households. As the figure shows, one result was to markedly increase the personal saving rate—measured as personal saving as a percentage of disposable personal income—from 6.4 percent in December 2019 to 22.0 in April 2020. (The figure begins in January 2020 to put the size of the spike in the saving rate in perspective.)

The rise in the saving rate helped households maintain high levels of consumption spending, particularly on consumer durables such as automobiles. The first of the following figure shows real personal consumption expenditures and the second figure shows real personal consumption expenditures on durable goods.

Taken together, these data provide an overview of the momentous macroeconomic events of the past four years.

Federal Reserve Chair Jerome Powell (Photo from Bloomberg News via the Wall Street Journal.)

Economists, policymakers, and Wall Street analysts have been waiting for macroeconomic data to confirm that the Federal Reserve has brought the U.S. economy in for a soft landing, with inflation arrving back at the Fed’s target of 2 percent without the economy slipping into a recession. Fed officials have been cautious about declaring that they have yet seen sufficient data to be sure that a soft landing has actually been achieved. Accordingly, they are not yet willing to begin cutting their target for the federal funds rate.

For instance, on March 6, in testifying before the Commitee on Financial Services of the U.S. House of Representatives, Fed Chair Jerome Powell stated that the Fed’s Federal Open Market Committee (FOMC) “does not expect that it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” (Powell’s statement before his testimony can be found here.)

The BLS’s release today (March 12) of its report on the consumer price index (CPI) (found here) for February indicated that inflation was still running higher than the Fed’s target, reinforcing the cautious approach that Powell and other members of the FOMC have been taking. The increase in the CPI that includes the prices of all goods and services in the market basket—often called headline inflation—was 3.2 percent from the same month in 2023, up slightly from 3.1 In January. (We discuss how the BLS constructs the CPI in Macroeconomics, Chapter 9, Section 19.4, Economics, Chapter 19, Section 19.4, and Essentials of Economics, Chapter 3, Section 13.4.) As the following figure shows, core inflation—which excludes the prices of food and energy—was 3.8 percent, down slightly from 3.9 percent in January.

If we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—the values are more concerning, as indicated in the following figure. Headline CPI inflation is 5.4 percent (up from 3.7 percent in January) and core CPI inflation is 4.4 percent (although that is down from 4.8 percent in January). The Fed’s inflation target is measured using the personal consumption expenditures (PCE) price index, not the CPI. But CPI inflation at these levels is not consistent with PCE inflation of only 2 percent.

Even more concerning is the path of inflation in the prices of services. As we’ve noted in earlier posts, Chair Powell has emphasized that as supply chain problems have gradually been resolved, inflation in the prices of goods has been rapidly declining. But inflaion in services hasn’t declined nearly as much. Last summer he stated the point this way:

“Part of the reason for the modest decline of nonhousing services inflation so far is that many of these services were less affected by global supply chain bottlenecks and are generally thought to be less interest sensitive than other sectors such as housing or durable goods. Production of these services is also relatively labor intensive, and the labor market remains tight. Given the size of this sector, some further progress here will be essential to restoring price stability.”

The following figure shows the 1-month inflation rate in services prices and in services prices not included including housing rent. Some economists believe that the rent component of the CPI isn’t well measured and can be volatile, so it’s worthwhile to look at inflation in service prices not including rent. The figure shows that inflation in all service prices has been above 4 percent in every month since July 2023. Although inflation in service prices declined from January, it was still a very high 5.8 percent in February. Inflation in service prices not including housing rent was even higher at 7.5 percent. Such large increases in the prices of services, if they were to continue, wouldn’t be consistent with the Fed meeting its 2 percent inflation target.

Finally, some economists and policymakers look at median inflation to gain insight into the underlying trend in the inflation rate. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates. As the following figure shows, although median inflation declined in February, it was still high at 4.6 percent and, although median inflation is volatile, the trend has been generally upward since July 2023.

The data in this month’s BLS report on the CPI reinforces the view that the FOMC will not move to cut its target for the federal funds rate in the meeting next week and makes it somewhat less likely that the committee will cut its target at the following meeting on April 30-May 1.