Image generated by ChatGPT

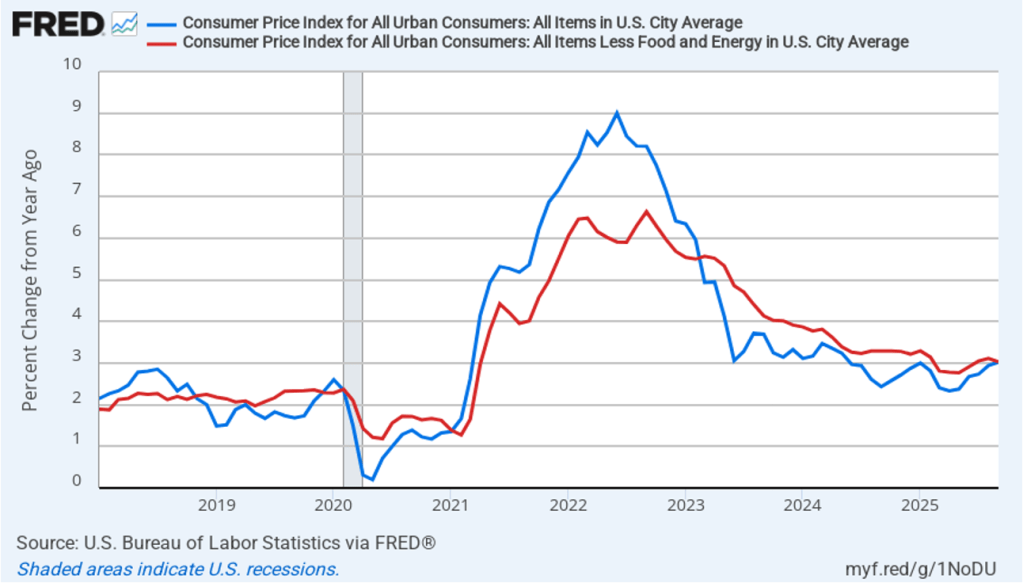

The Burea of Economic Analysis (BEA) released two reports this morning. One report included a revision of estimated growth in real GDP during the fourth quarter of 2025 from an advance estimate of 1.4 percent—which was already lower than had been expected—to 0.7 percent. Economists surveyed by the Wall Street Journal had expected that fourth quarter growth would be revised upward to 1.5 percent. The BEA’s “Personal Income and Outlays, January 2026” report indicated that the personal consumption expenditures (PCE) price index had increased 2.8 percent over the past year, slightly below the 2.9 percent that economists had expected.

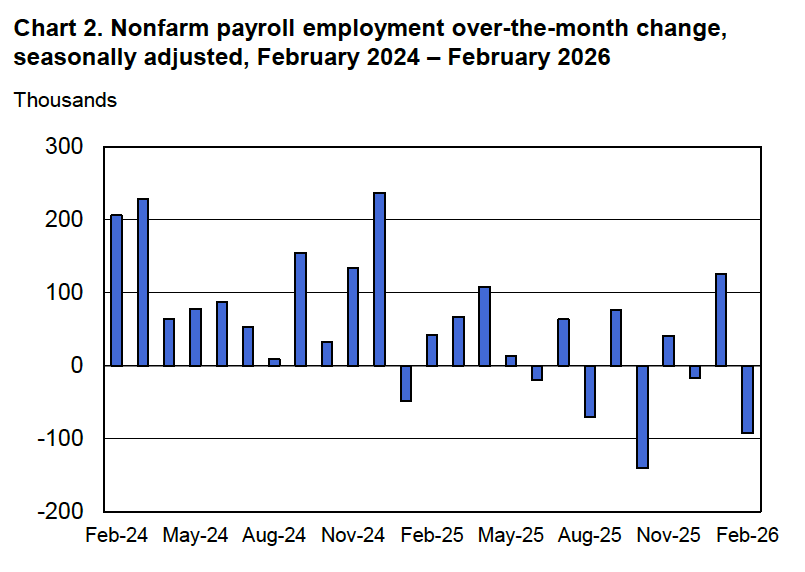

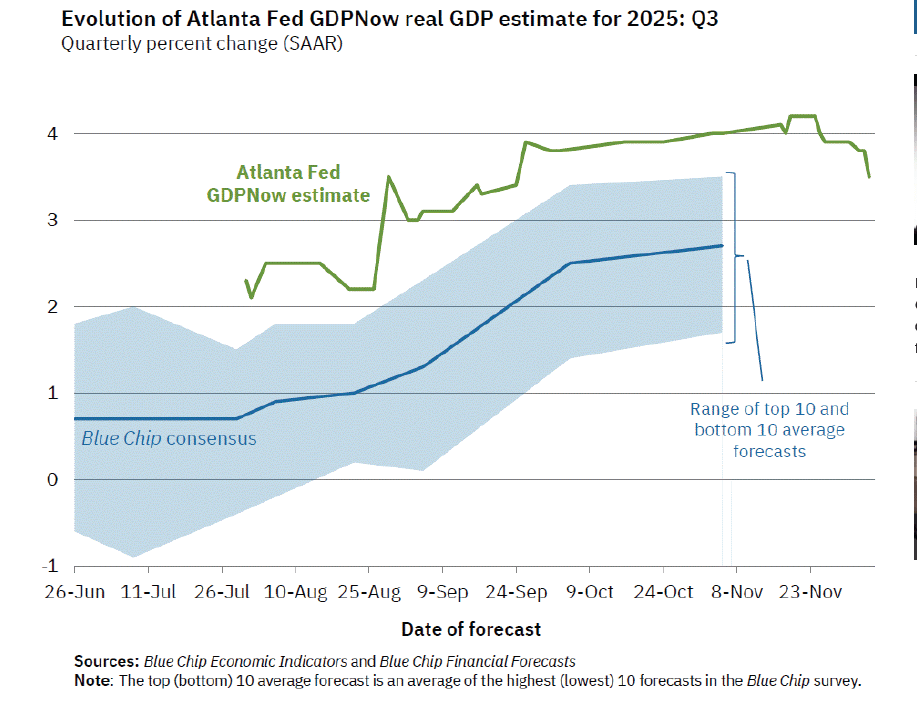

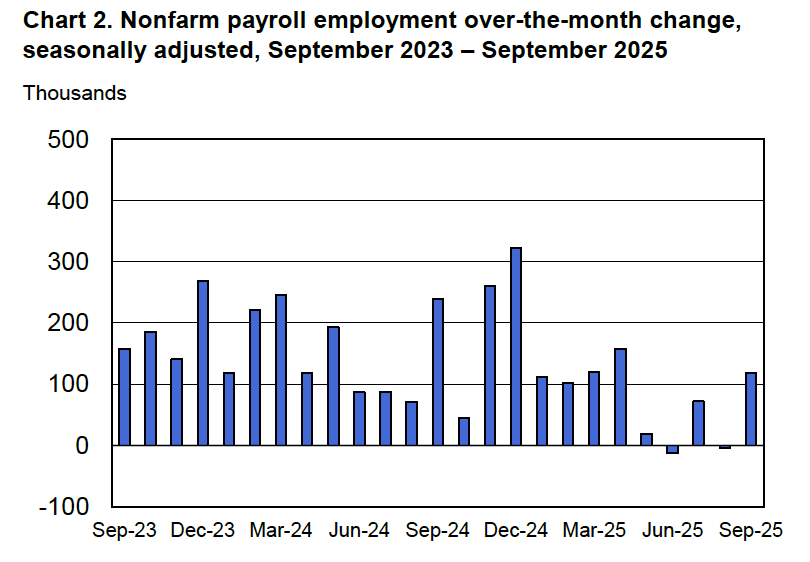

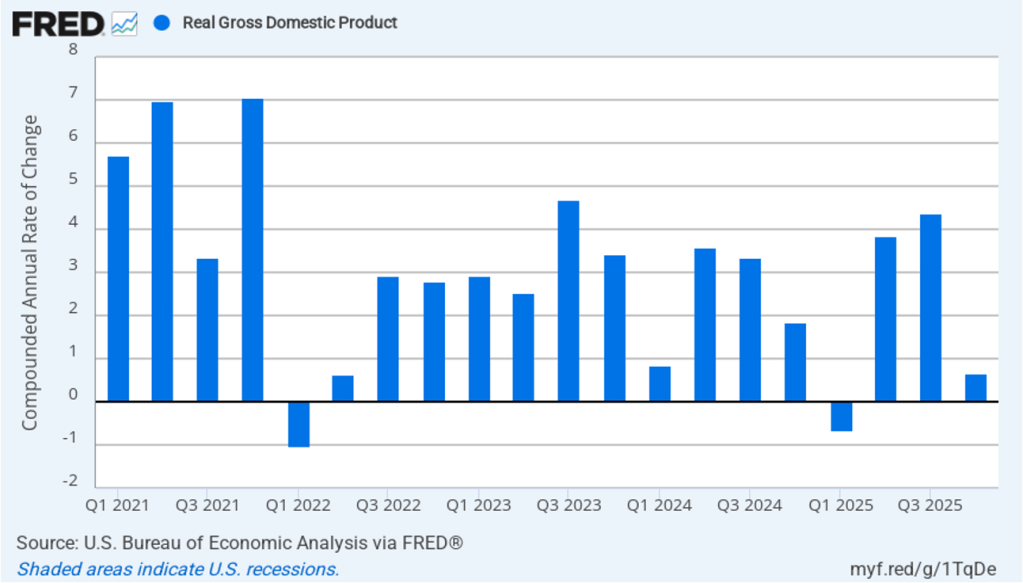

The following figure shows the estimated rates of GDP growth in each quarter beginning with the first quarter of 2021.

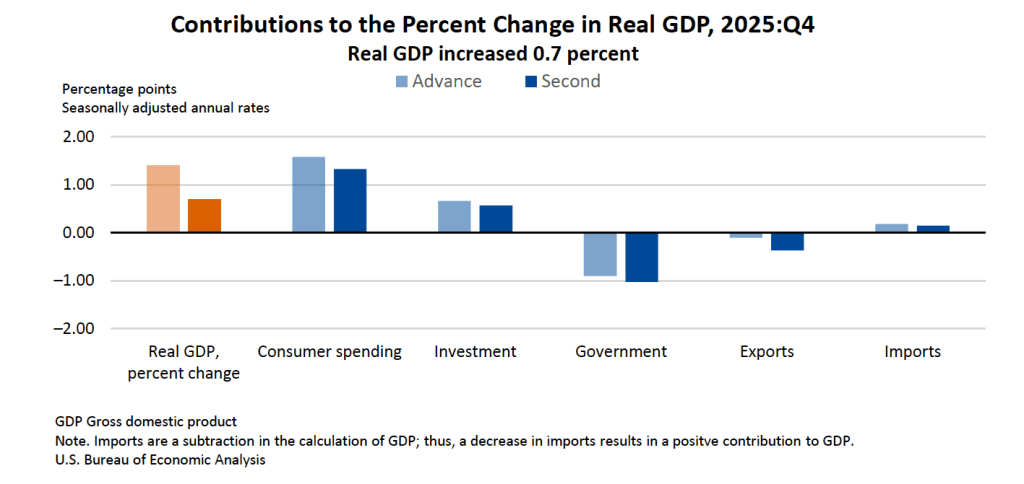

As the following figure—taken from the BEA report—shows, consumer spending, investment spending, government spending, and net exports were all revised downward from the original advance estimates. The decline in real government expenditures of –1.0 percent at an annual rate—revised downward from –0.9 percent—was the most important factor contributing to the slowing growth in real GDP during the fourth quarter. The decline in government expenditures is largely attributable to the federal government shutdown, which lasted from October 1, 2025 to November 12, 2025.

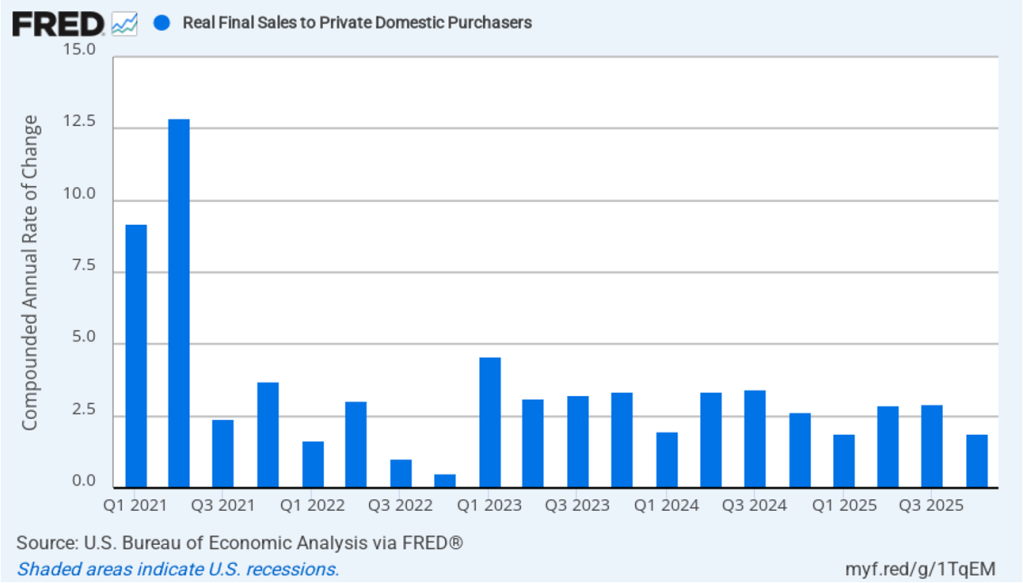

As we’ve discussed in previous blog posts, to better gauge the state of the economy, policymakers—including Fed Chair Jerome Powell—often prefer to strip out the effects of imports, inventory investment, and government expenditures—which can be volatile—by looking at real final sales to private domestic purchasers, which includes only spending by U.S. households and firms on domestic production. As the following figure shows, real final sales to domestic purchasers increased by 1.9 percent in the fourth quarter at an annual rate—revised downward from the advance estimate of 2.4 percent—which was well above the 0.9 percent increase in real GDP and slightly above the U.S. economy’s expected long-run annual real growth rate of 1.8 percent. Note also that real final sales to private domestic purchasers grew by 2.9 percent in the third quarter, during which real GDP grew by 4.4 percent, and by 1.9 percent in the first quarter of 2025, when real GDP declined by 0.6 percent. So this measure of output is more stable and likely is a better indicator of the underlying growth rate in the economy than is growth in real GDP.

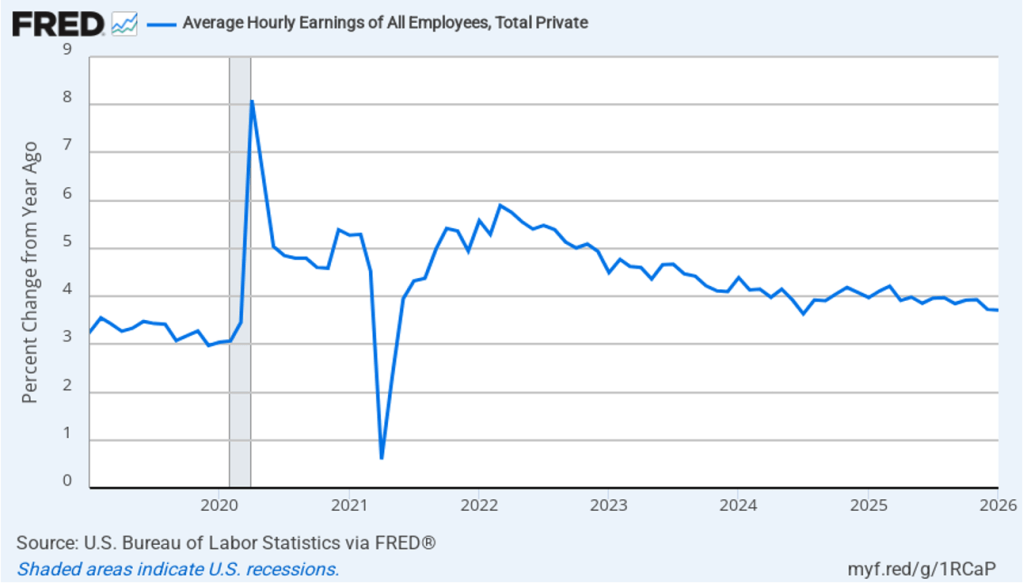

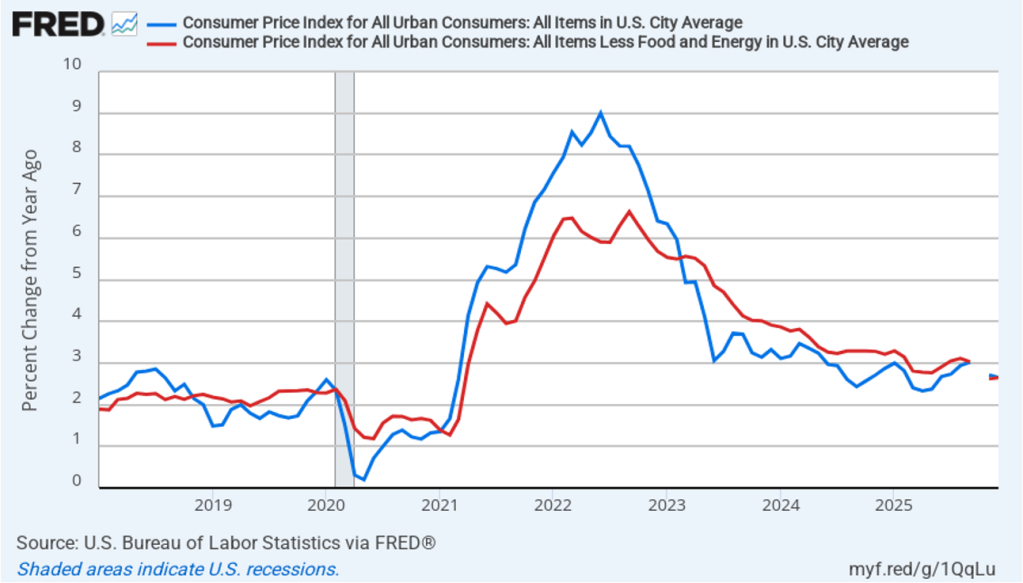

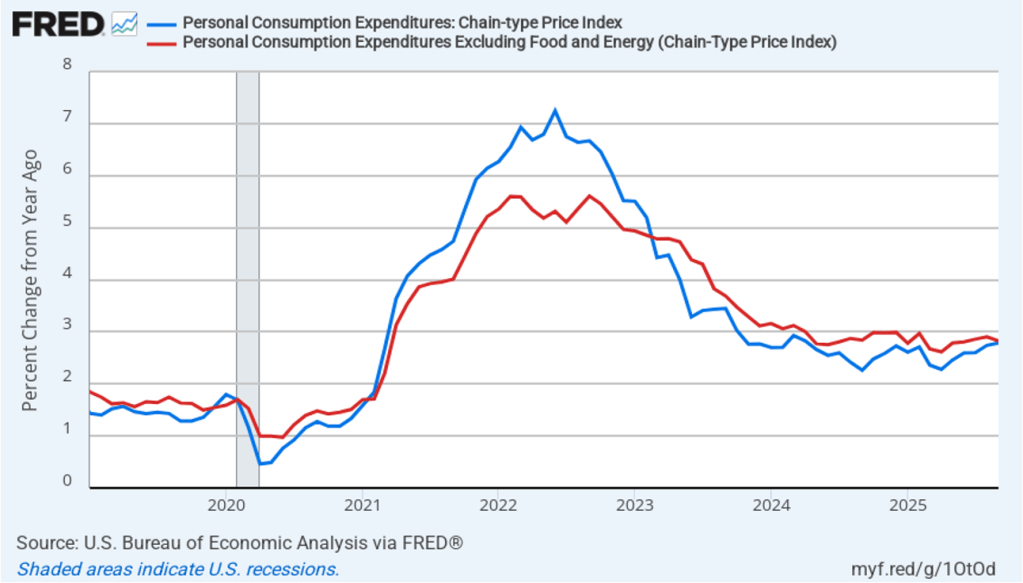

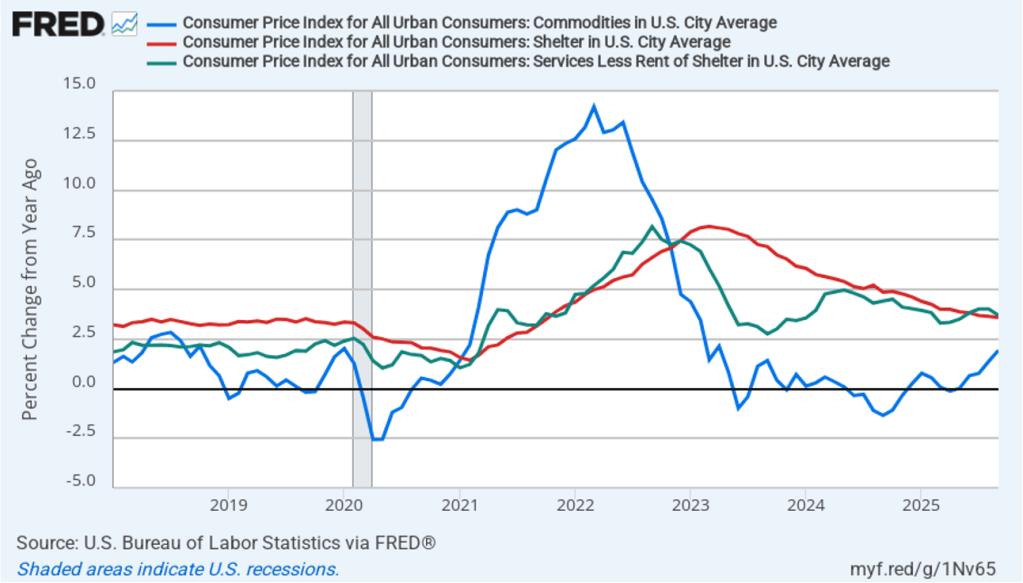

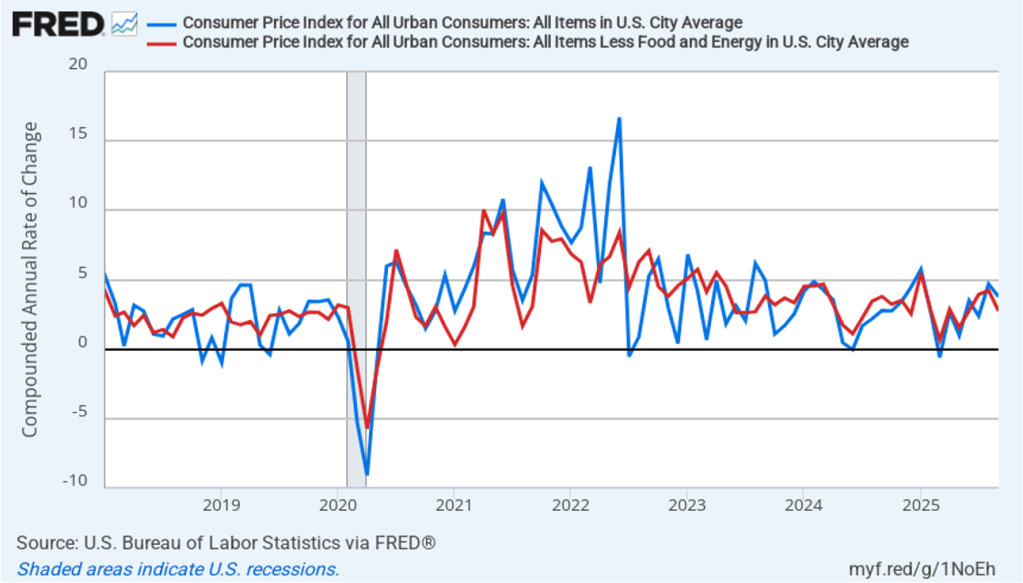

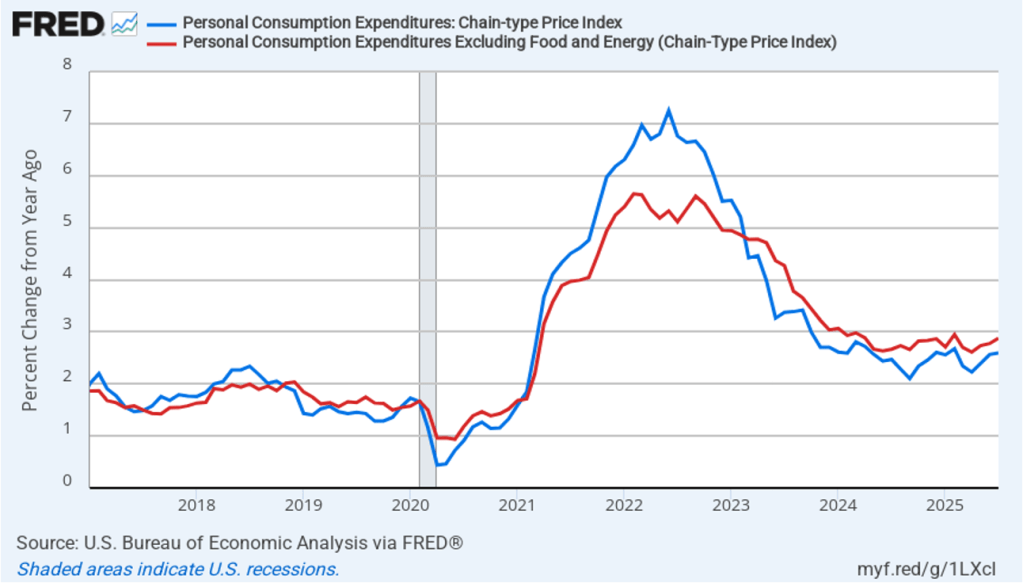

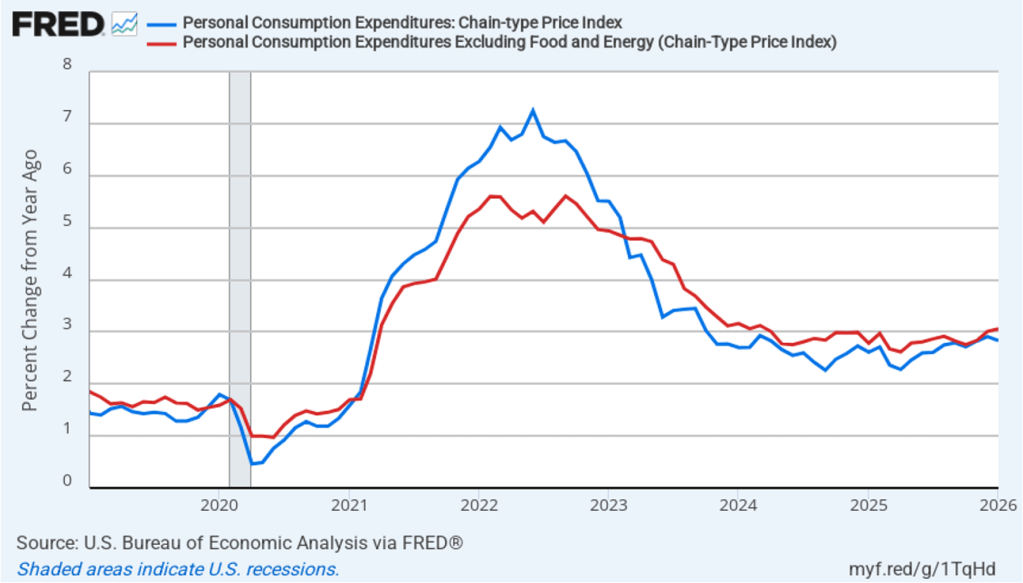

The second BEA report this morning included monthly data on the personal consumption expenditures (PCE) price index for January 2026. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2.0 percent annual inflation target. The following figure shows headline PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices— with inflation measured as the percentage change in the PCE from the same month in the previous year. In January 2026, headline PCE inflation was 2.8 percent, down slightly from 2.9 percent in December 2025 (which was also the inflation rate economists had expected for January 2026). Core PCE inflation in January was 3.1 percent, up slightly from 3.0 in December. Both headline PCE inflation and core PCE inflation remained above the Fed’s 2.0 percent annual inflation target.

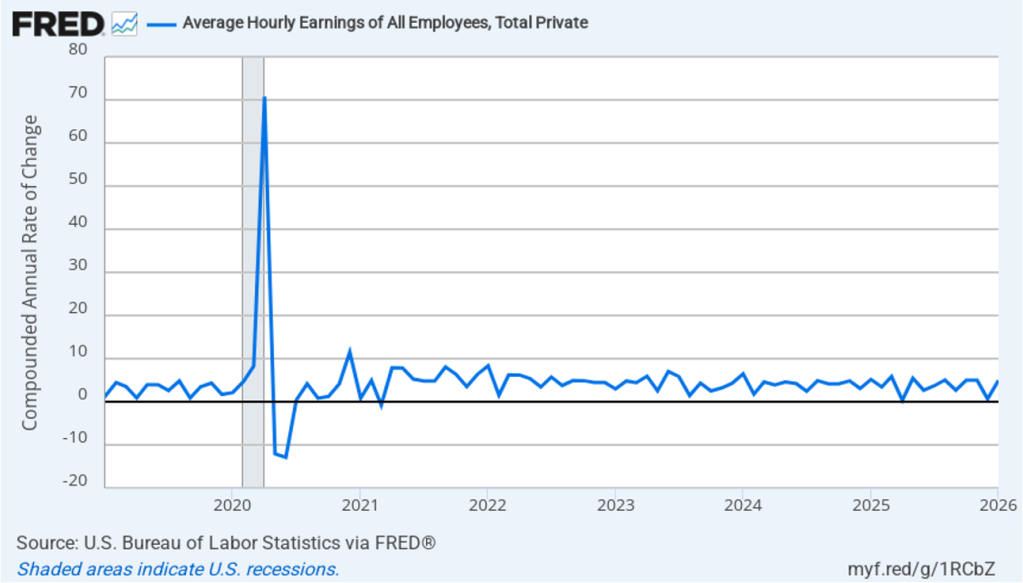

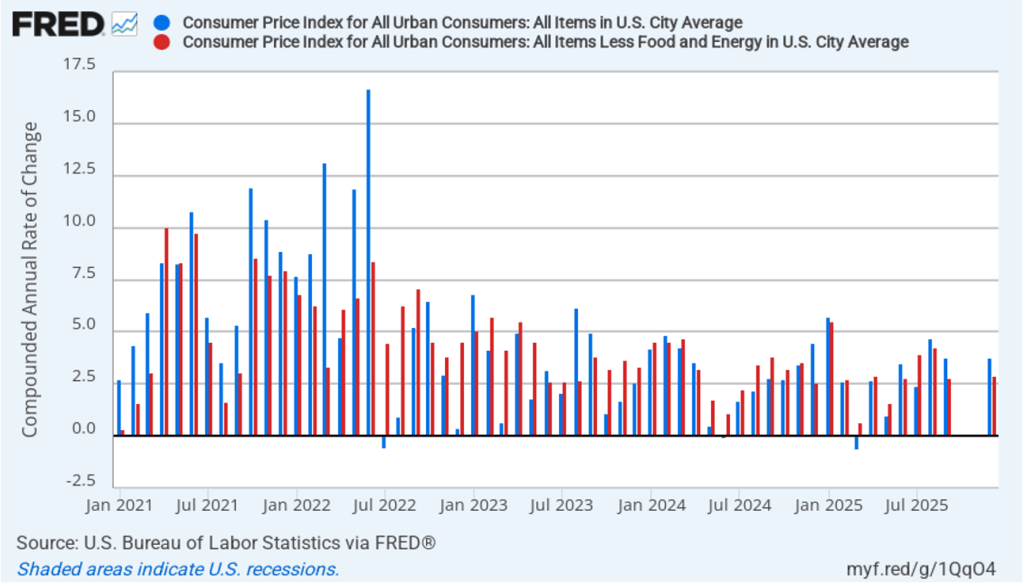

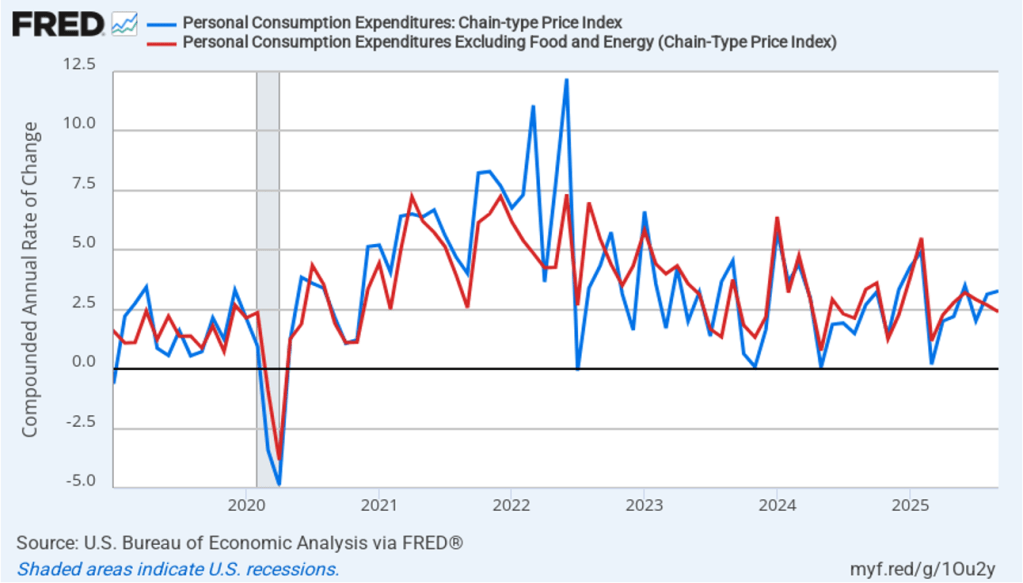

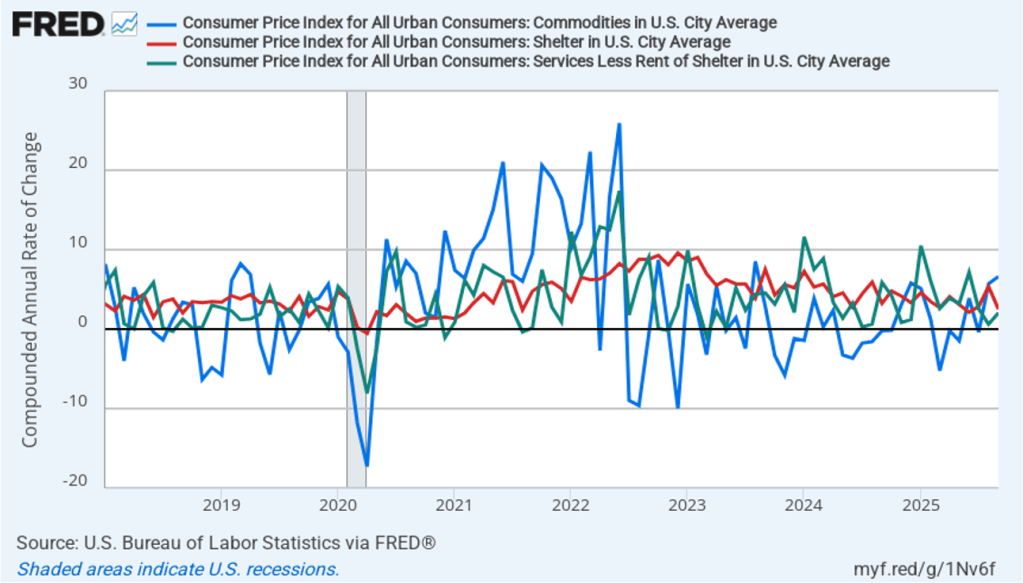

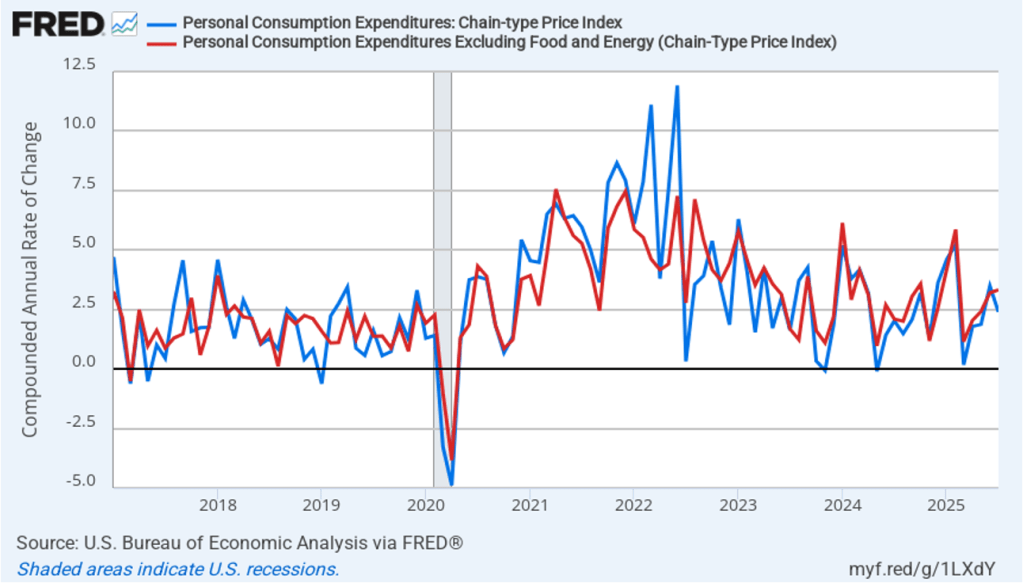

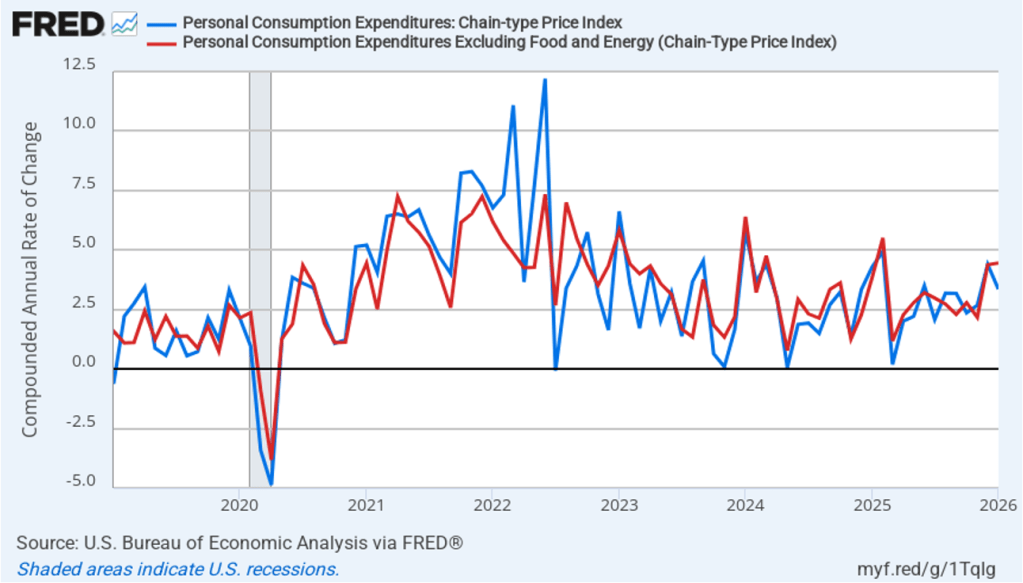

The following figure shows headline PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while the figure below shows 1-month inflation.) Measured this way, headline PCE inflation declined to 3.4 percent in January, from to 4.4 percent in December. Core PCE inflation fell to 4.4 percent in January from 4.5 percent in December. Measured this way, both core and headline PCE inflation were well above the Fed’s target.

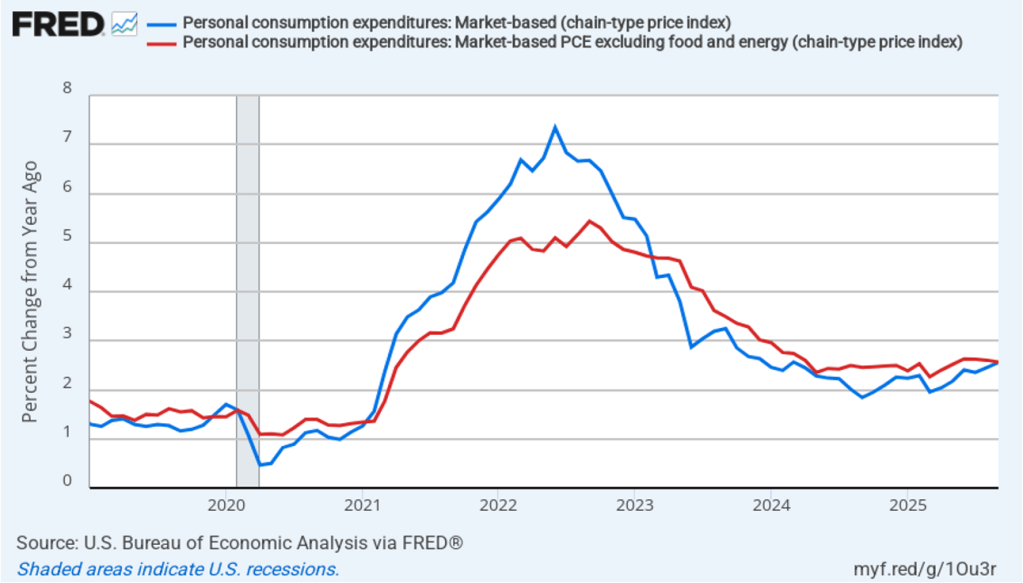

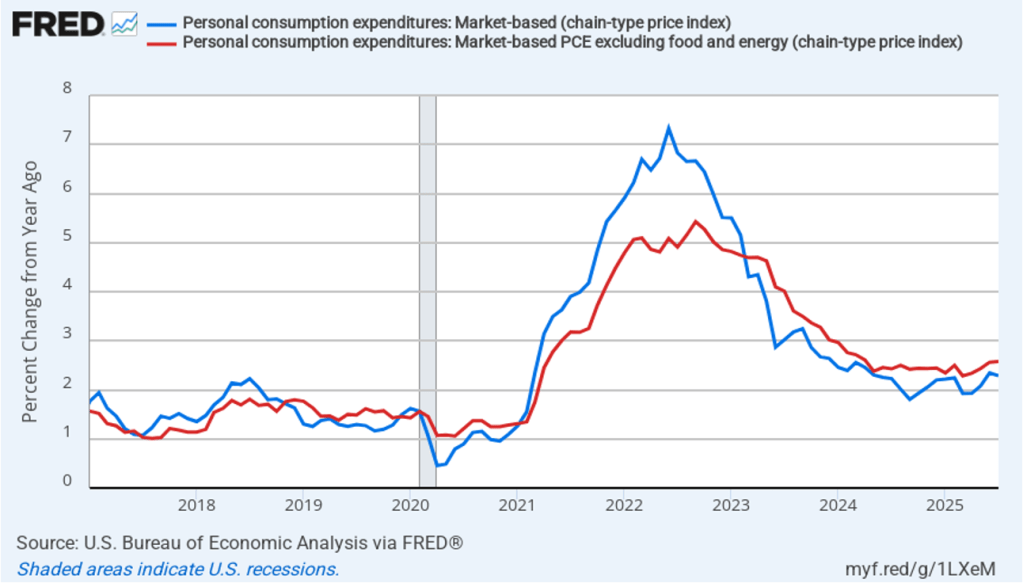

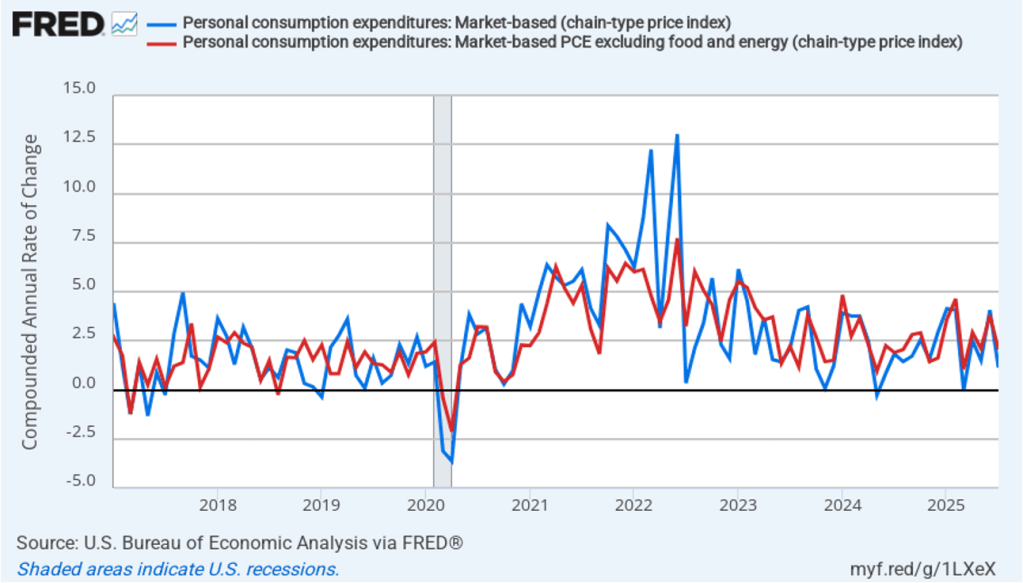

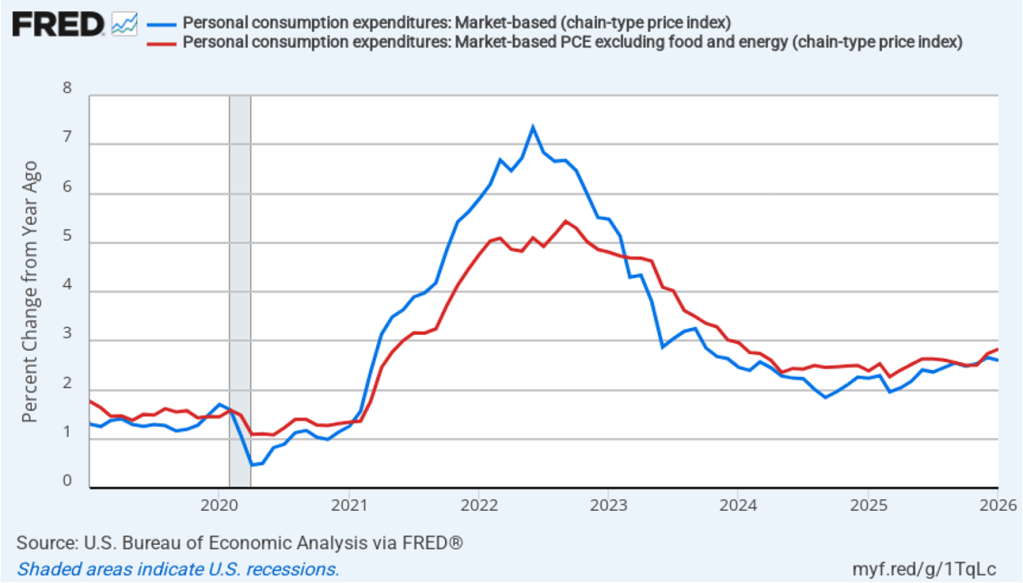

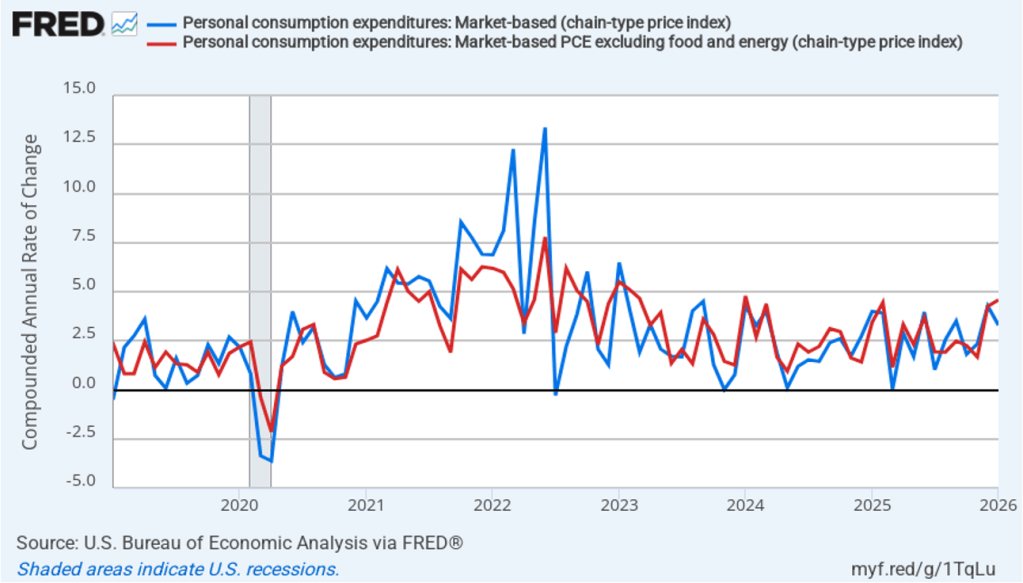

Fed Chair Jerome Powell has frequently mentioned that inflation in non-market services can skew PCE inflation. Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices fall, the prices of financial services included in the PCE price index also fall. Powell has argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month headline inflation (the blue line) and 12-month core inflation (the red line) for market-based PCE. (The BEA explains the market-based PCE measure here.)

Headline market-based PCE inflation was 2.6 percent in January, down from 2.7 percent in December. Core market-based PCE inflation was 2.8 percent in January, up from 2.7 in December. So, both market-based measures show inflation as stable but above the Fed’s 2 percent target.

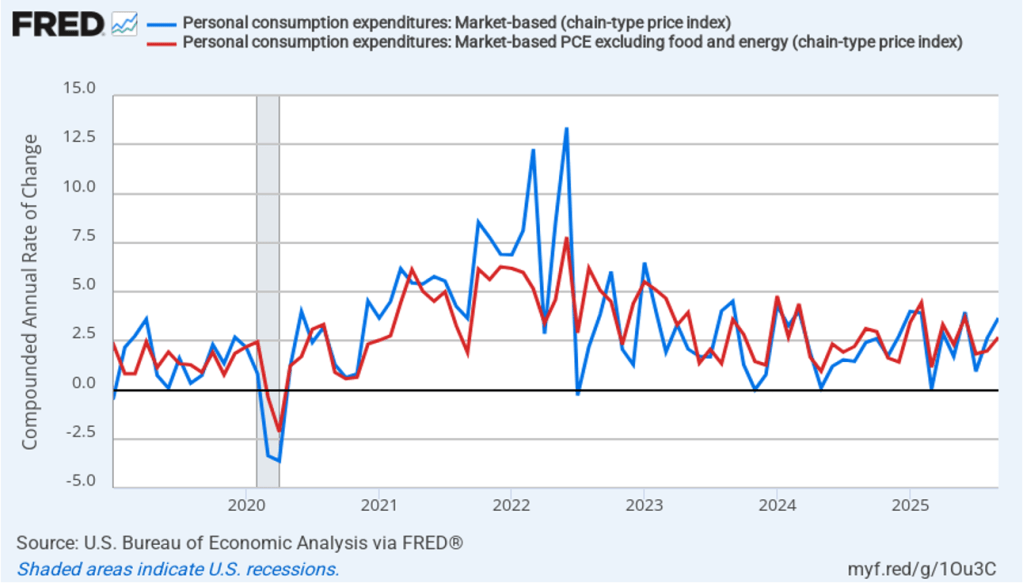

In the following figure, we look at 1-month inflation using these measures. One-month headline market-based inflation was 3.3 percent in January, down from 4.3 percent in December. One-month core market-based inflation increased to 4.6 percent in January from 4.4 percent in December. As the figure shows, the 1-month inflation rates are more volatile than the 12-month rates, which is why the Fed relies on the 12-month rates when gauging how close it is coming to hitting its target inflation rate.

Today’s data arrive against the backdrop of the conflict in Iran. According to the AAA, gasoline prices have risen to an average of $3.63 per gallon from $2.94 a month ago. Assuming that the conflict is resolved relatively soon, that increase should have only a transitory effect on inflation. Chair Powell as indicated that he believes that the upward pressure of tariffs on the price level is also still working its way through the economy.

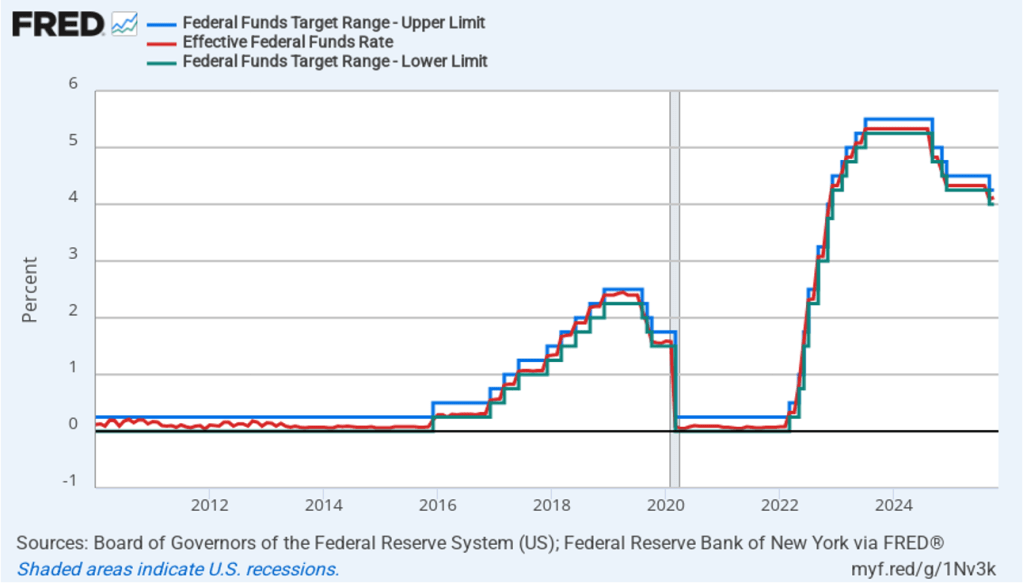

Recent macroeconomic data, along with the effects of tariffs and the conflict in Iran, make it unlikely that members of the Fed’s policymaking Federal Open Market Committee (FOMC) will reduce their target range for the federal funds rate any time soon. The probability that investors in the federal funds futures market assign to the FOMC keeping its target rate unchanged at its March 17–18 meeting decreased only slightly this afternoon to 99.1 percent from rom 99.9 percent yesterday. Investors don’t assign a greater than 50 percent probability to the FOMC cutting its federal funds rate target at any meeting before the meeting on October 27–28.