Yesterday, in this blog post, we discussed the quarterly data on inflation as measured by changes in the personal consumption expenditures (PCE) price index. Today (July 31), the Bureau of Economic Analysis (BEA) released monthly data on the PCE price index as part of its “Personal Income and Outlays” report. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target.

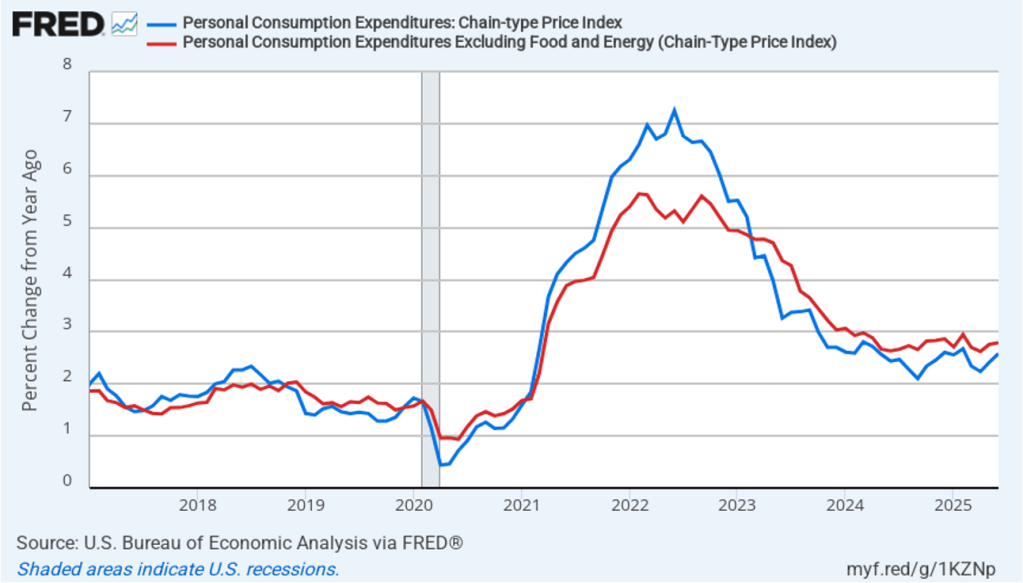

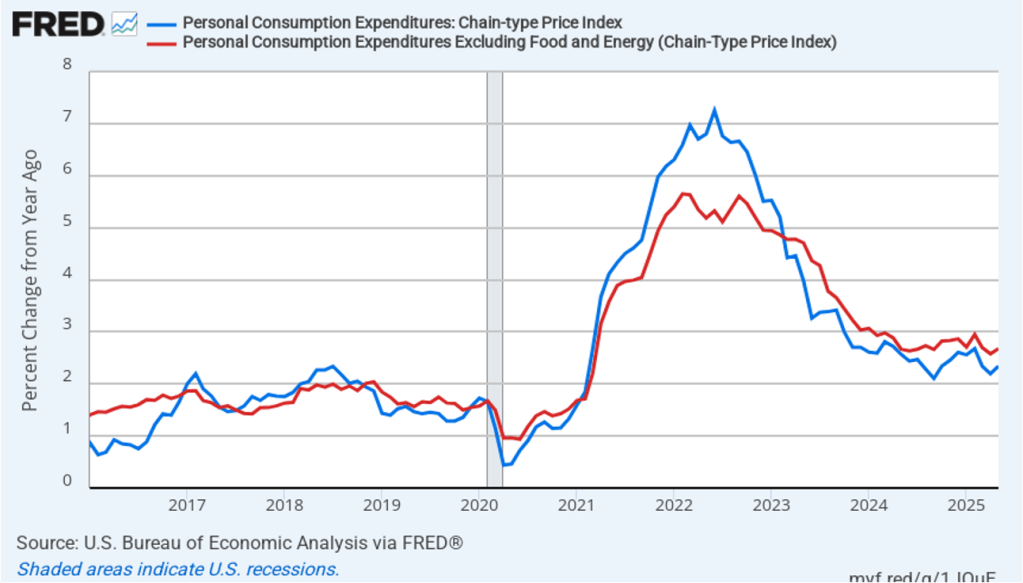

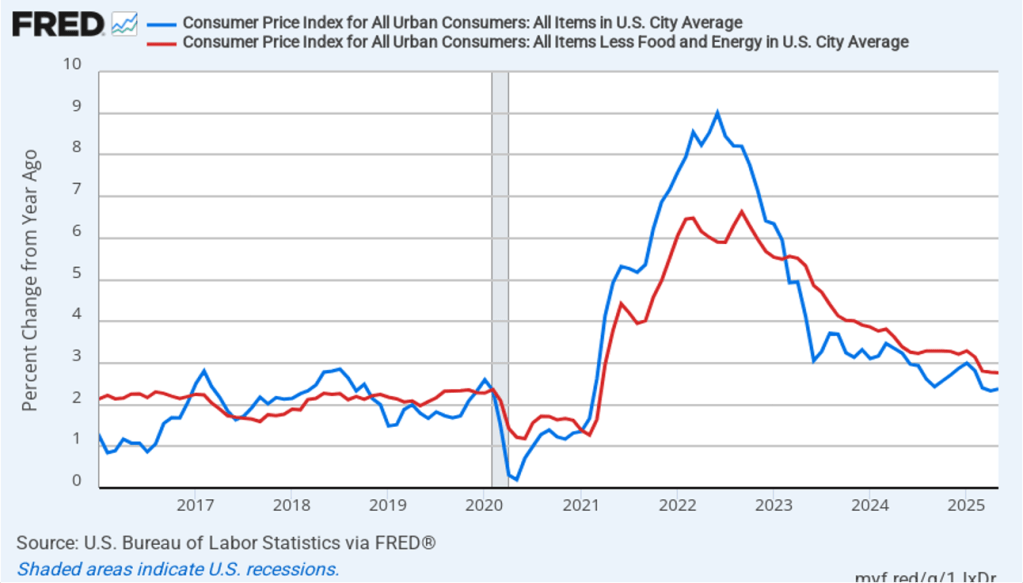

The following figure shows headline PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2017, with inflation measured as the percentage change in the PCE from the same month in the previous year. In June, headline PCE inflation was 2.6 percent, up from 2.4 percent in May. Core PCE inflation in June was 2.8 percent, unchanged from May. Headline PCE inflation was higher than the forecast of economists surveyed, while core PCE inflation was the same as forecast.

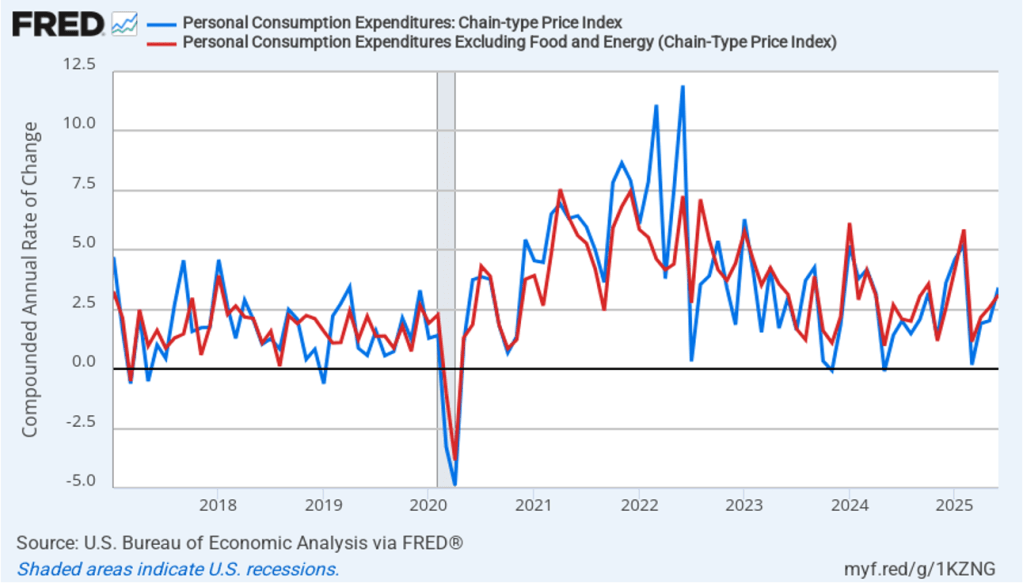

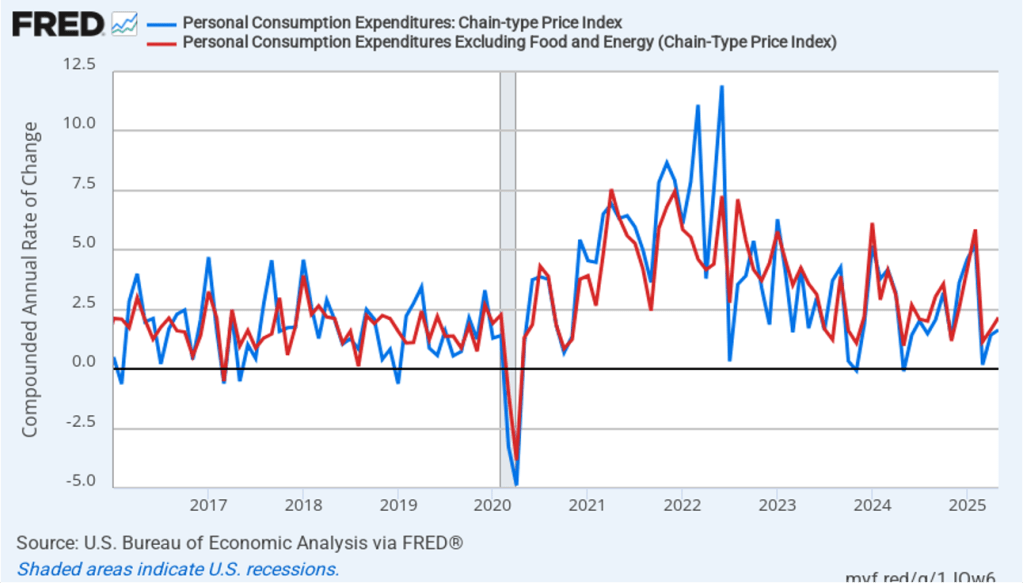

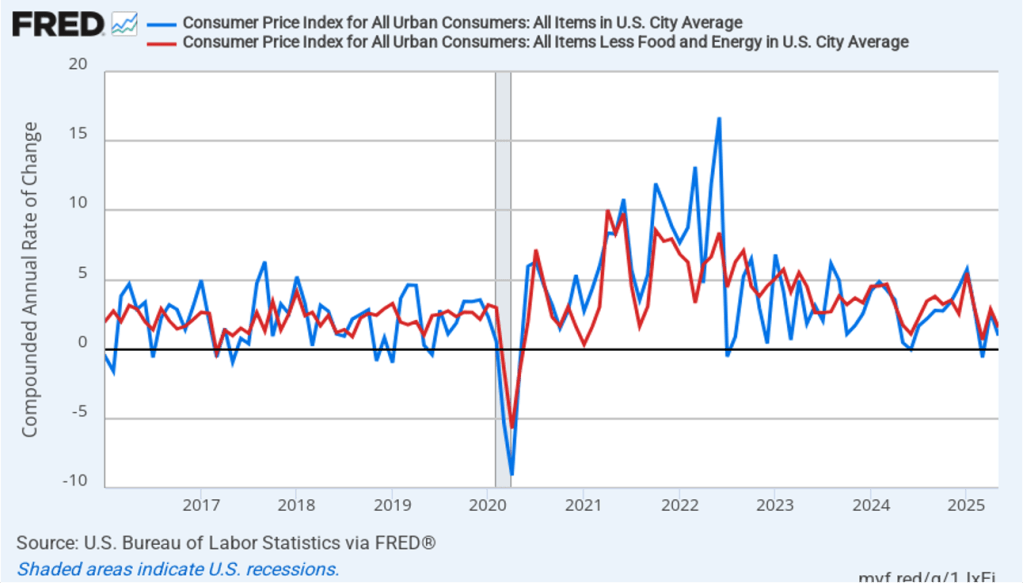

The following figure shows headline PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, headline PCE inflation jumped from 2.0 percent in May to 3.4 percent in June. Core PCE inflation increased from 2.6 percent in May to 3.1 percent in June. So, both 1-month PCE inflation estimates are well above the Fed’s 2 percent target. The usual caution applies that 1-month inflation figures are volatile (as can be seen in the figure), so we shouldn’t attempt to draw wider conclusions from one month’s data. In addition, these data likely don’t capture fully the higher prices likely to result from the tariff increases the Trump administration has implemented, including those in trade agreements that have only been announced in the past few days.

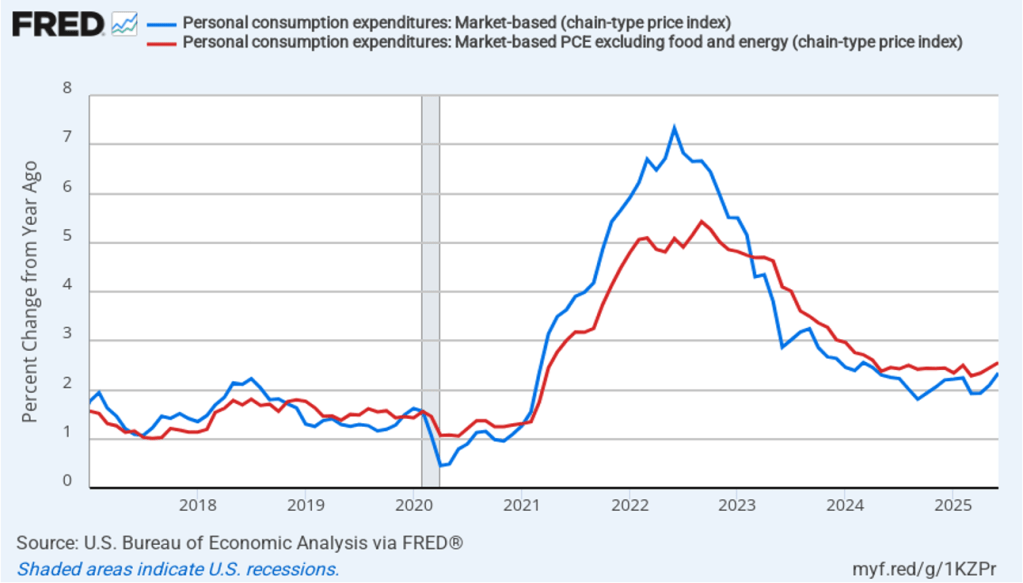

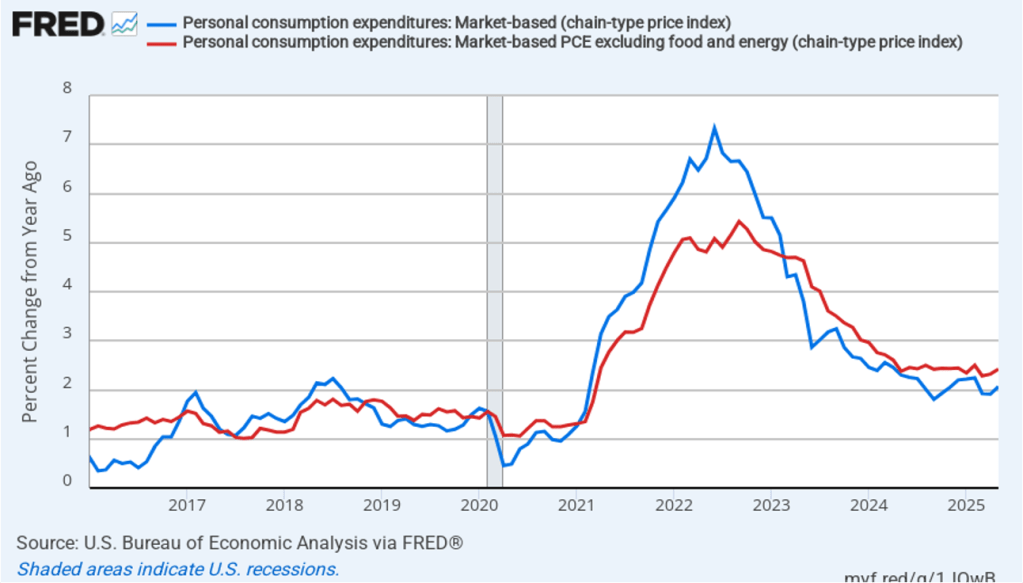

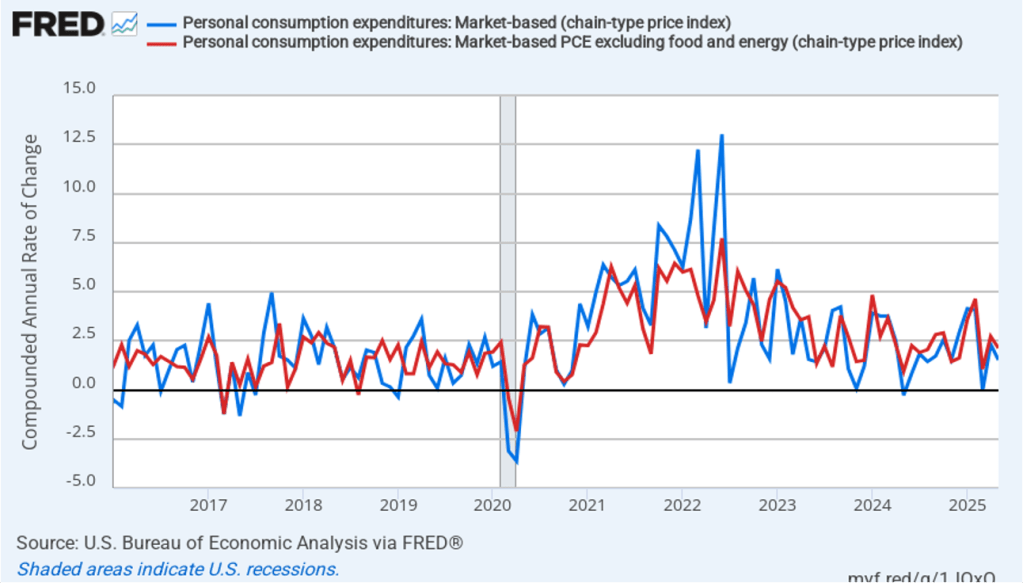

Fed Chair Jerome Powell has frequently noted that inflation in non-market services can skew PCE inflation. Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices fall, the prices of financial services included in the PCE price index also fall. Powell has argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month headline inflation (the blue line) and 12-month core inflation (the red line) for market-based PCE. (The BEA explains the market-based PCE measure here.)

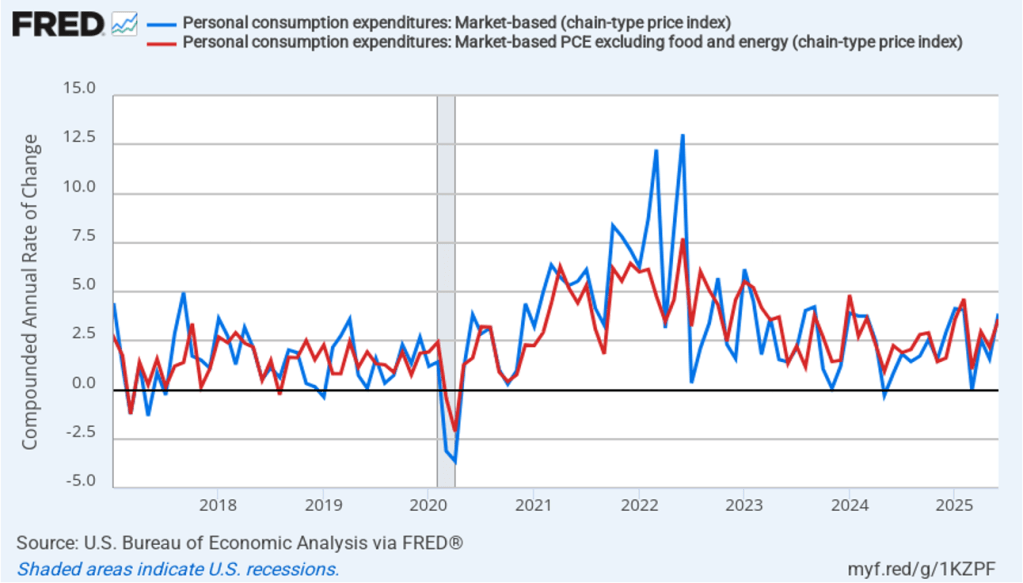

Headline market-based PCE inflation was 2.3 percent in June, up from 2.1 percent in May. Core market-based PCE inflation was 2.6 percent in June, up from 2.4 percent in May. So, both market-based measures show similar rates of inflation in June as the total measures do. In the following figure, we look at 1-month inflation using these measures. The 1-month inflation rates are both higher than the 12-month rates. One-month headline market-based inflation soared to 3.9 percent in June from 1.6 percent in May. One-month core market-based inflation also increased sharply to 3.6 percent in June from 2.2 percent in May. As the figure shows, the 1-month inflation rates are more volatile than the 12-month rates, which is why the Fed relies on the 12-month rates when gauging how close it is coming to hitting its target inflation rate. Still, looking at 1-month inflation gives us a better look at current trends in inflation, which these data indicate is rising significantly.

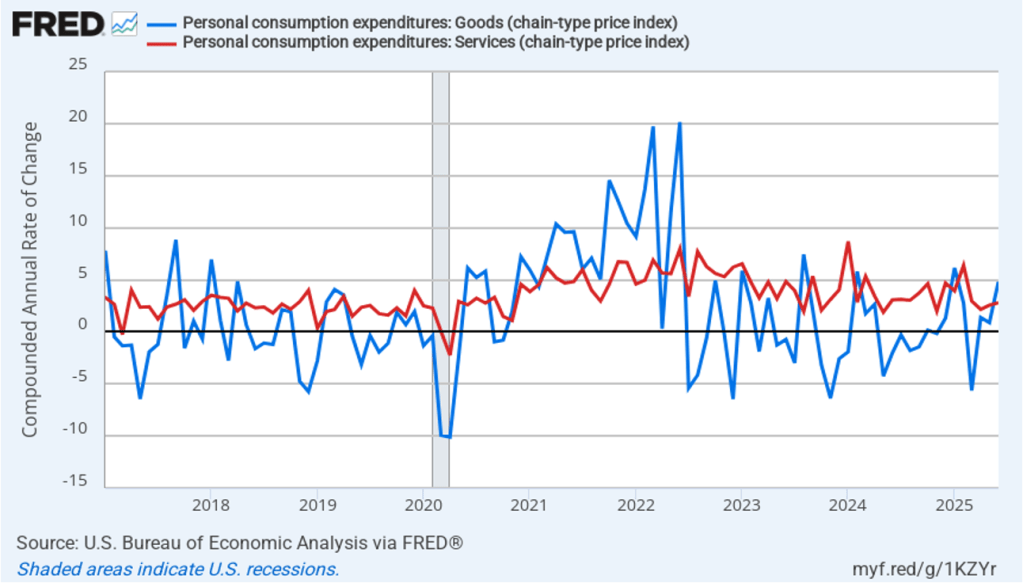

Is the increase in inflation attributable to the effects of tariffs? At this point, it’s too early to tell, particularly since, as noted earlier, all tariff increases have not yet been implemented. We can note, though, that the effect of tariffs are typically seen in goods prices, rather than in service prices because tariffs are levied primarily on imports of goods. As the following figure shows, one-month inflation in goods prices jumped from 0.9 percent in May to 4.8 percent in June, while one-month inflation in services prices increased only from 2.5 percent in May to 2.8 percent in June.

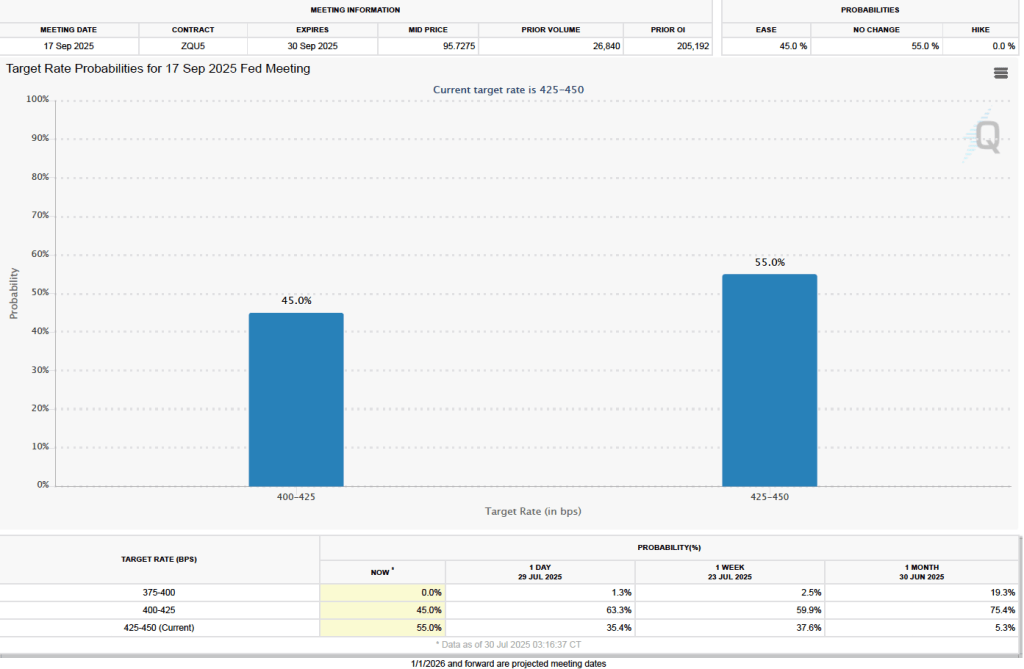

Finally, we noted in a blog post yesterday that investors trading federal funds rate futures assigned a 55.0 percent probability to the Federal Open Market Committee leaving its target for the federal funds rate unchanged at its meeting on September 16–17. With today’s PCE report showing higher than expected inflation, that probability has increased to 60.8 percent.

Photo of President Trump and Fed Chair Powell from Reuters via the Wall Street Journal

Today’s meeting of the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) occurred against a backdrop of President Trump pressuring the committee to reduce its target for the federal funds rate and two members of the Board of Governors signalling that they were likely to dissent if the committee voted to hold its target constant.

Last week President Trump made an unusual visit to the Fed’s headquarters in Washington, DC to discuss what he had said was the Fed’s excessive spending on renovating three buildings. As we discuss in this blog post, the Supreme Court is unlikely to allow a president to remove a Fed chair because of disagreements over monetary policy. A president would likely be allowed to remove a Fed chair “for cause.” Some members of the Trump administration have argued that excessive spending on renovating buildings might be sufficient cause for the president to remove Fed Chair Jerome Powell. President Trump has indicated that, in fact, he doesn’t intend to replace Powell before his term as chair ends in May 2026, but President Trump still urged Powell to make substantial cuts in the federal funds rate target.

As most observers had expected, the committee decided today to keep its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. Board of Governors members Michelle Bowman and Christopher Waller dissented, preferring “to lower the target range for the federal funds rate by 1/4 percentage point at this meeting.” It was the first time since 1993 that two members of the Board of Governors have voted against an FOMC decision.

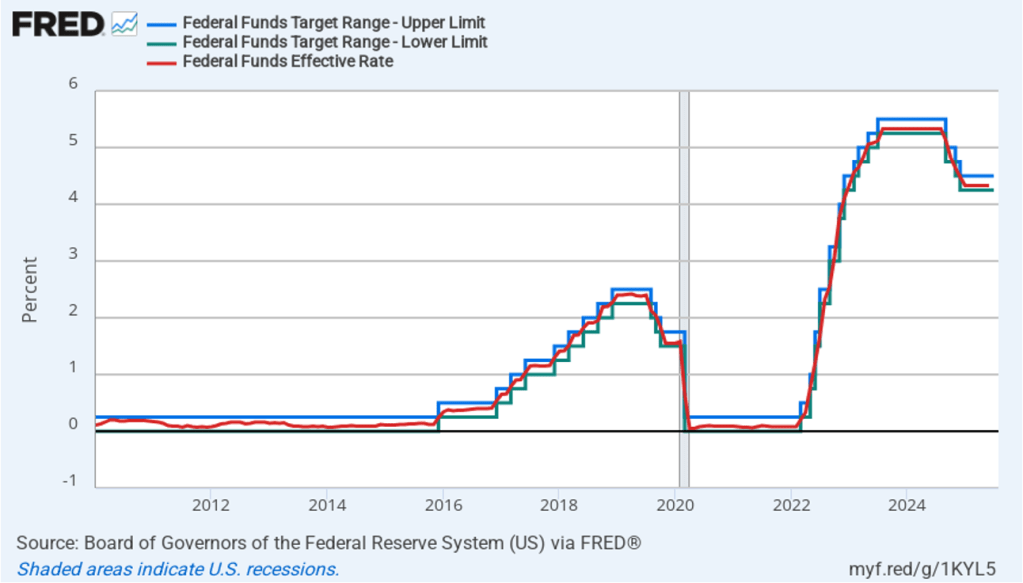

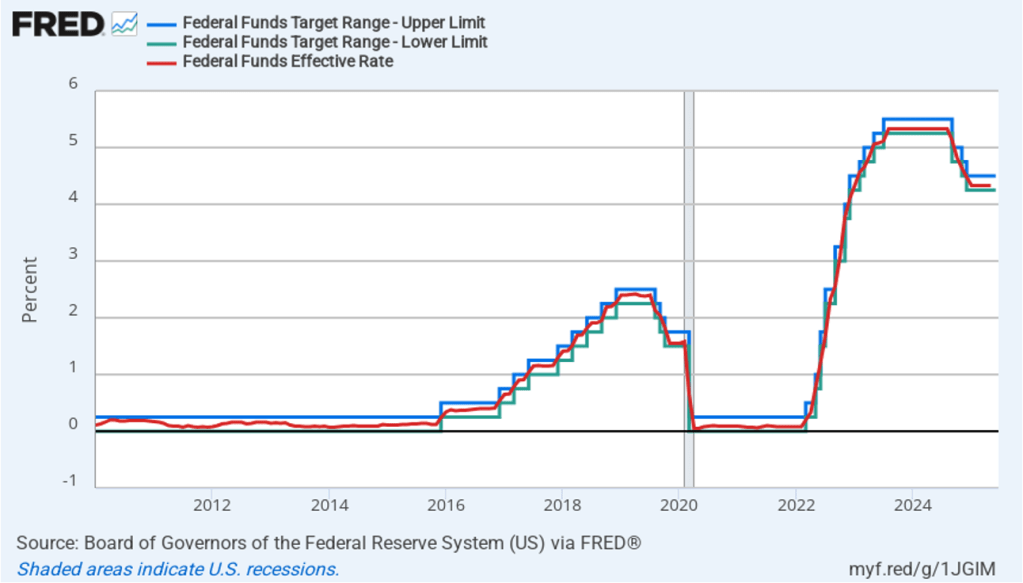

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

In his press conference following the meeting, Chair Powell indicated that a majority of the committee believed that: “Inflation is above target, maximum employment is at target, so policy should be slightly restrictive.” Policy is restrictive in the sense that the current range for the federal funds rate is higher than the long-run equilibrium rate. Powell noted that: “There are many uncertainties left to resolve. There is much more to come looking ahead.” Jn particular, with respect to the effect of tariffs, he stated that it’s “still quite early days …. [We’ve] seen substantial increases in tariff revenue collections … [but we] have to see how much of tariffs are passed through to consumers. A long way to go to know what has happened.”

One reason that President Trump has urged the FOMC to lower its target for the federal funds rate is that lower interest rates will reduce the amount the federal government has to pay on the $25 trillion in U.S. Treasury debt owned by private investors. At his press conference, Chair Powell was asked whether the committee discussed interest payments on the national debt during its deliberations. He responded that the committee considers only the dual mandate of price stability and maximum employment given to the Fed by Congress. Therefore, “We don’t consider the fiscal needs of the federal government.”

The FOMC’s next meeting is on September 16–17. Powell noted that before that meeting, the committee will have seen two more employment reports and two more inflation reports. The data in those reports may clarify the state of the economy. There has been a general expectation that the committee would cut its target for the federal funds rate at that meting

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that one month ago investors assigned a 75.4 percent probability to the committee cutting its target range by 0.25 percentage point (25 basis points) to 4.00 percent to 4.25 percent at the September meeting. Today, however, sentiment has changed, perhaps because investors now believe that inflation in coming months will be higher than they had previously expected. As the following figure shows, investors now assign a 55.0 percent probability to the committee leaving its target for the federal funds rate unchanged at that meeting and only a 45 percent probability of the committee cutting its target range by 25 basis points.

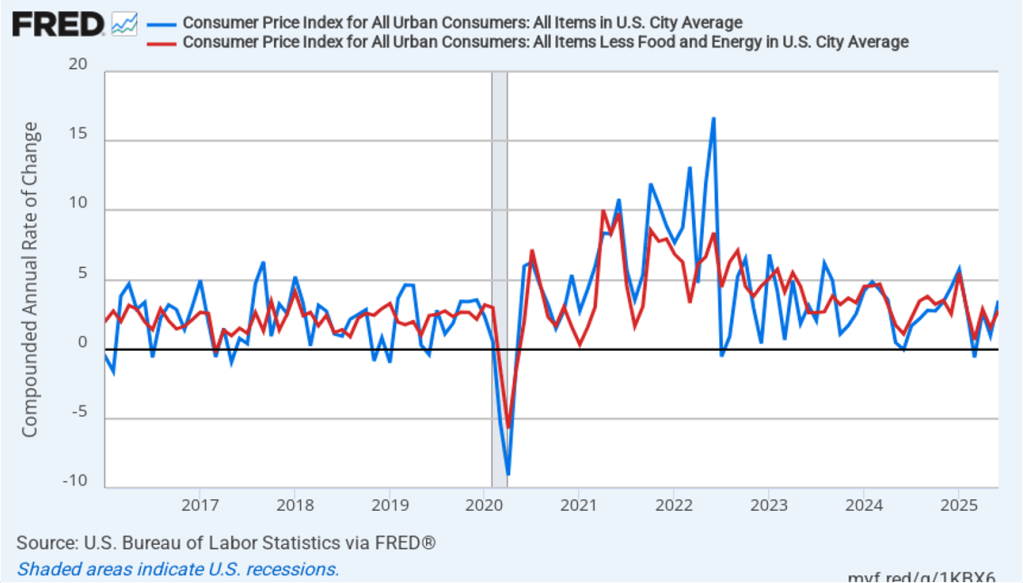

Today (July 15), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for June. The following figure compares headline CPI inflation (the blue line) and core CPI inflation (the red line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.7 percent in June—up from 2.4 percent in May.

The core inflation rate,which excludes the prices of food and energy, was 2.9 percent in June—up slightly from 2.8 percent in May.

Headline inflation was slightly higher and core inflation was slightly lower than what economists surveyed had expected.

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) surged from 1.0 percent in May to 3.5 percent in June. Core inflation (the red line) also increased sharply from 1.6 percent in May to 2.8 percent in June.

The 1-month and 12-month inflation rates are telling different stories, with 12-month inflation indicating that the rate of price increase is running moderately above the Fed’s 2 percent inflation target. The 1-month inflation rate indicates more clearly that inflation increased significantly during June.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that the 1-month inflation rate is particularly volatile. Also note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

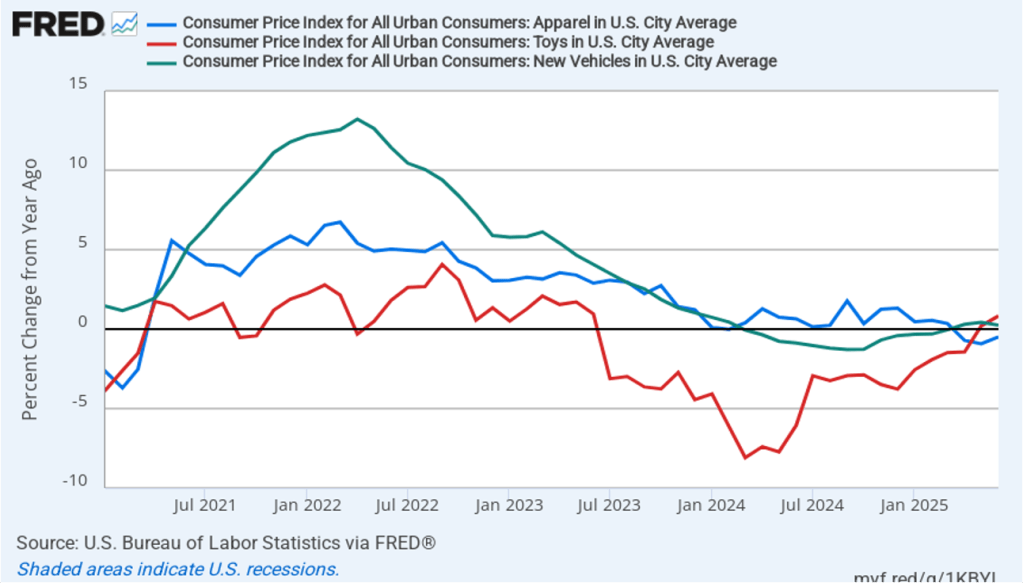

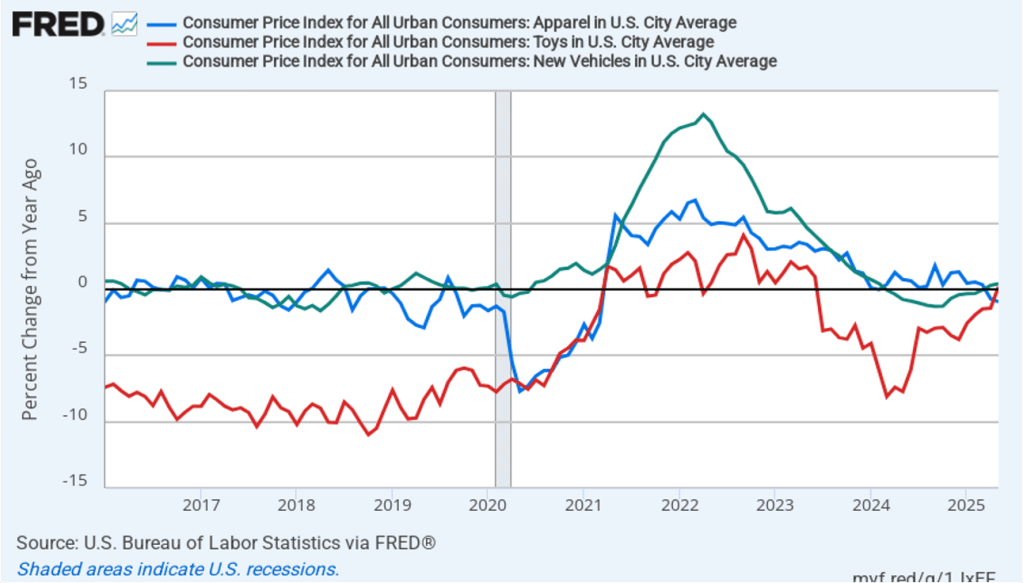

Does the increase in inflation represent the effects of the increases in tariffs that the Trump administration announced on April 2? (Note that some of the tariff increases announced on April 2 have since been reduced) The following figure shows 12-month inflation in three categories of products whose prices are thought to be particularly vulnerable to the effects of tariffs: apparel (the blue line), toys (the red line), and motor vehicles (the green line). To make recent changes clearer, we look only at the months since January 2021. In June, prices of apparel fell, while the prices of toys and motor vehicles rose by less than 1.0 percent.

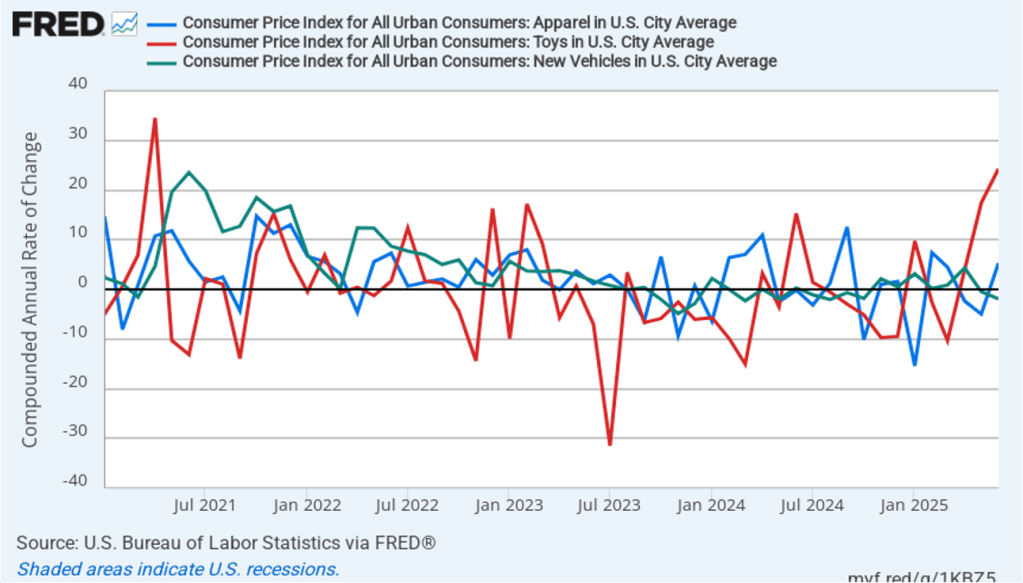

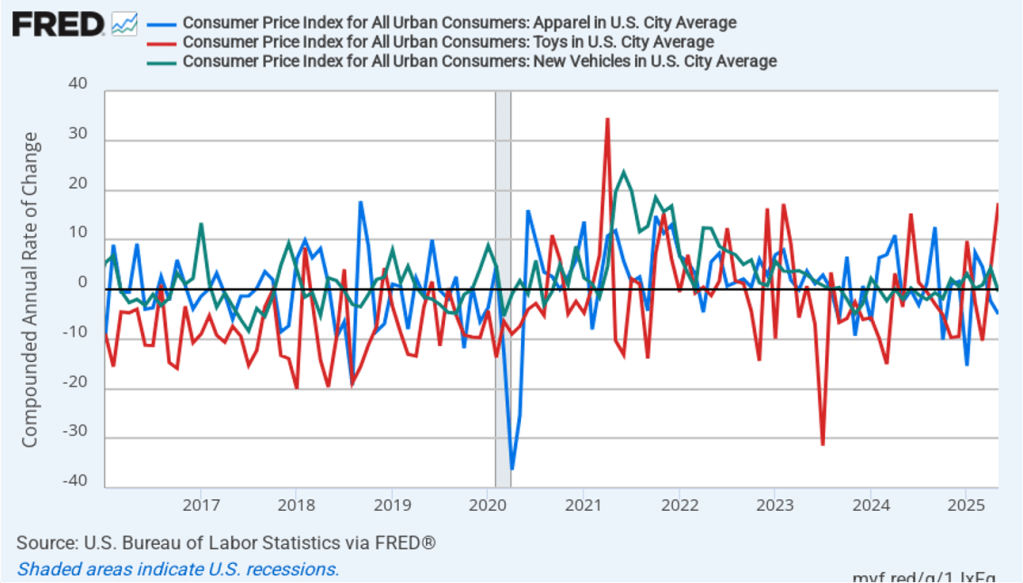

The following figure shows 1-month inflation in these prices of these products. In June, the motor vehicles prices fell, while apparel prices increased 5.3 percent and the prices of toys soared by 24.3 percent, which was the second month in a row of very large increases in toy prices.

The 1-month inflation data for these three products are a mixed bag with two of the products showing significant increases and one showing a decline. It’s likely that some of the effects of the tariffs are still being cushioned by firms increasing their inventories earlier in the year in anticipation of price increases resulting from the tariffs. As firms draw down their inventories, we may see tariff-related increases in the prices of more goods later in the year.

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

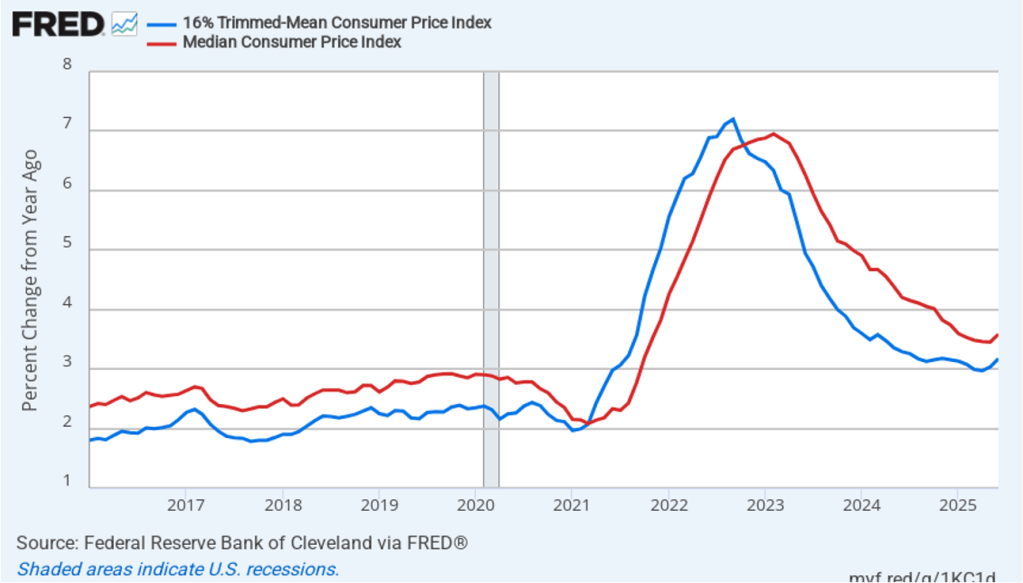

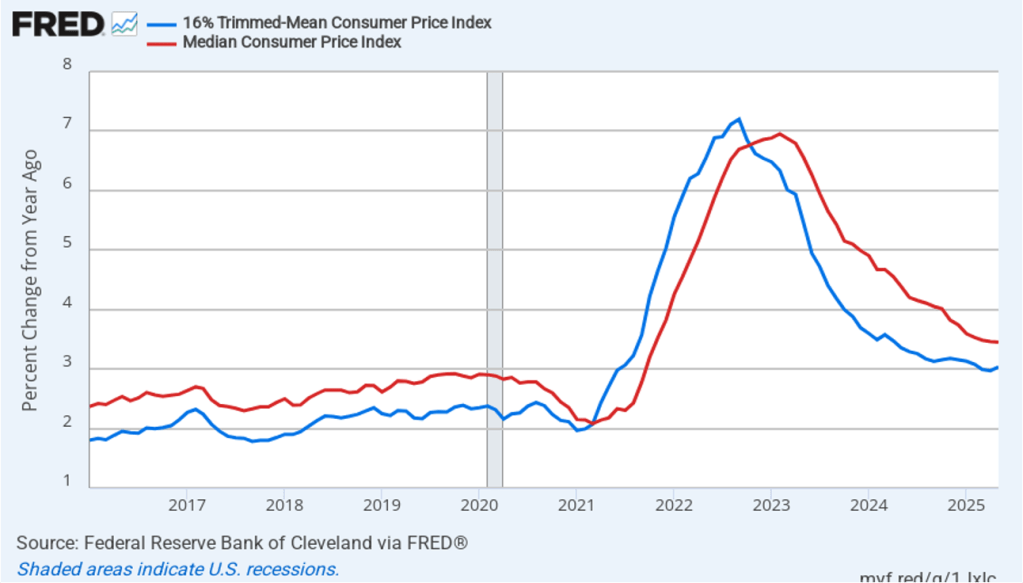

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.2 percent in June, up from 3.0 percent in May. Twelve-month median inflation (the red line) 3.6 percent in June, up from 3.5 percent in May.

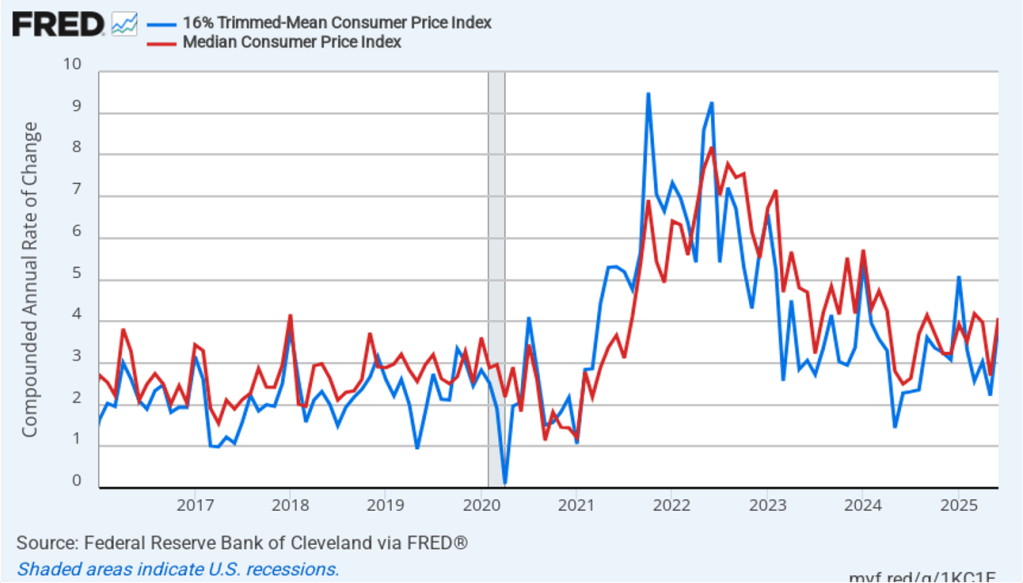

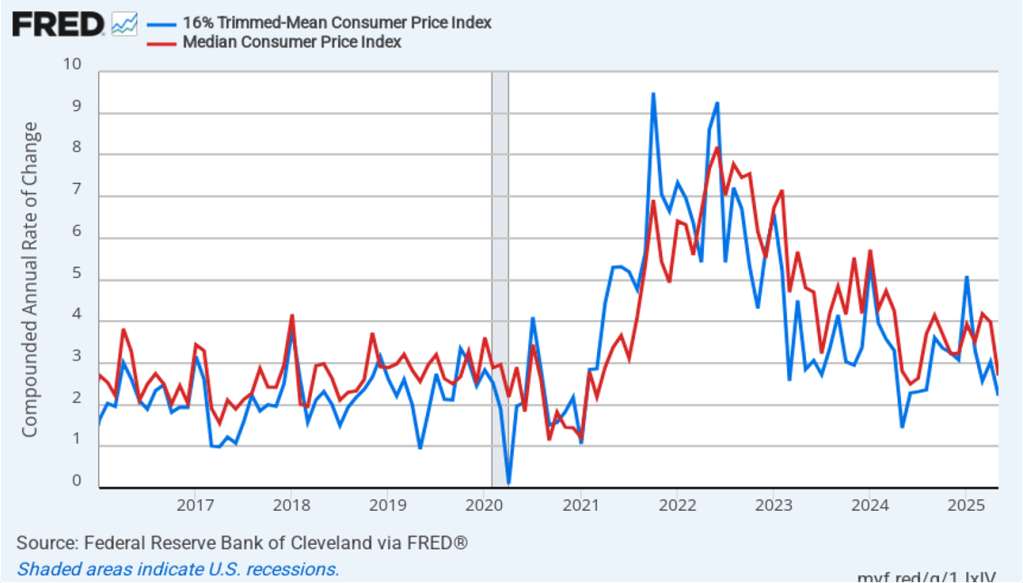

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation rose sharply from 2.2 percent in May to 3.9 percent in June. One-month median inflation also rose sharply from 2.7 percent in May to 4.1 percent in June. These data provide some confirmation that inflation likely rose from May to June.

What are the implications of this CPI report for the actions the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) may take at its next meetings? Investors who buy and sell federal funds futures contracts still expect that the FOMC will leave its target for the federal funds rate unchanged at its July 29–30 meeting before cutting its target by 0.25 (25 basis points) from its current target range of 4.25 percent to 4.50 percent at its September 16–17 meeting. (We discuss the futures market for federal funds in this blog post.) The FOMC’s actions will likely depend in part on the effect of the tariff increases on the inflation rate during the coming months. If inflation were to increase significantly, it’s possible that the committee would decide to raise, rather than lower, its target range.

This morning (July 3), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for June. The data in the report show that the labor market was stronger than expected in June. There have been many stories in the media about businesspeople becoming pessimistic as a result of the large tariff increases the Trump Administration announced on April 2—some of which have since been reduced—and some large firms—including Microsoft and Walt Disney—have announced layoffs. In addition, yesterday payroll processing firm ADP estimated that private sector employment had declined by 33,000 in June. But despite these signs of weakness in the labor market, as the headline in the Wall Street Journal put it “Hiring Defied Expectations in June.”

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

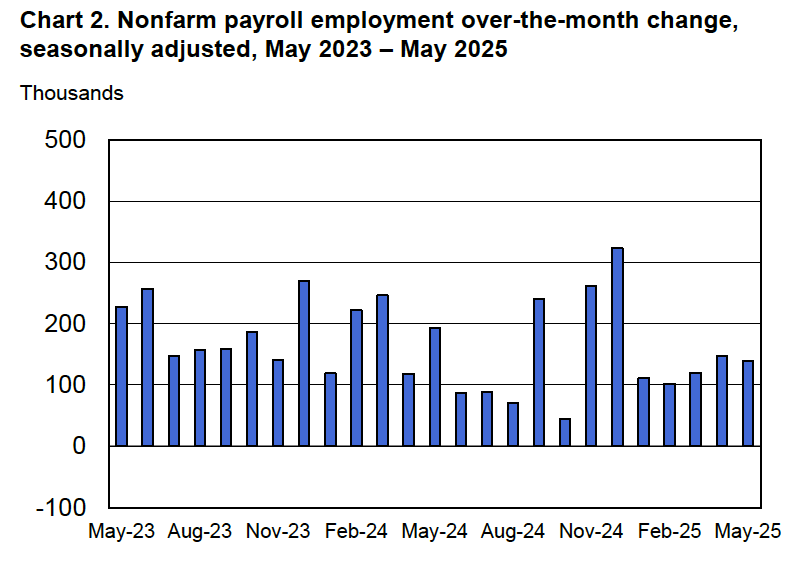

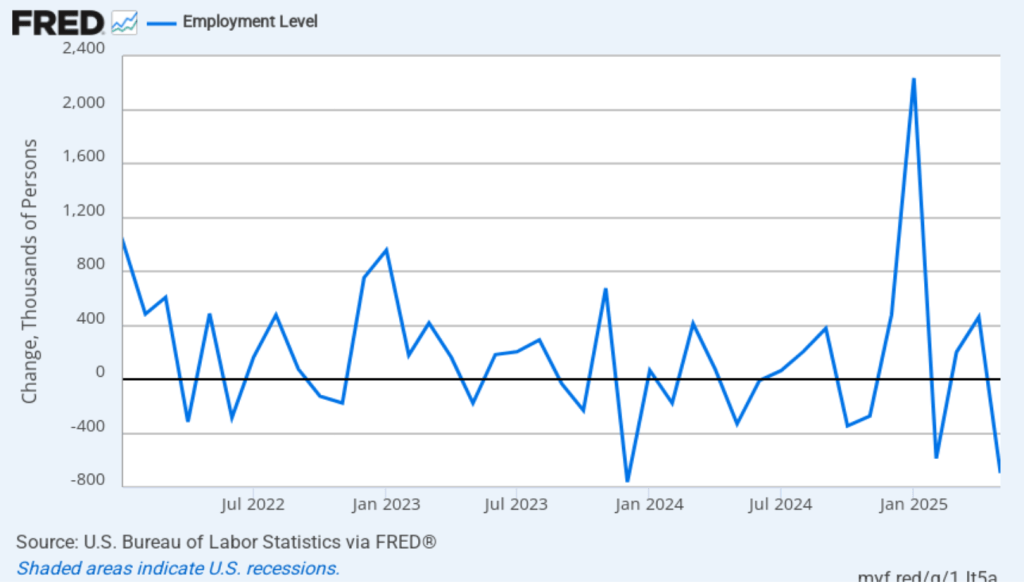

According to the establishment survey, there was a net increase of 147,000 nonfarm jobs during June. This increase was above the increase of 1115,000 that economists surveyed had forecast. In addition, the BLS revised upward its previous estimates of employment in April and May by a combined 16,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years.

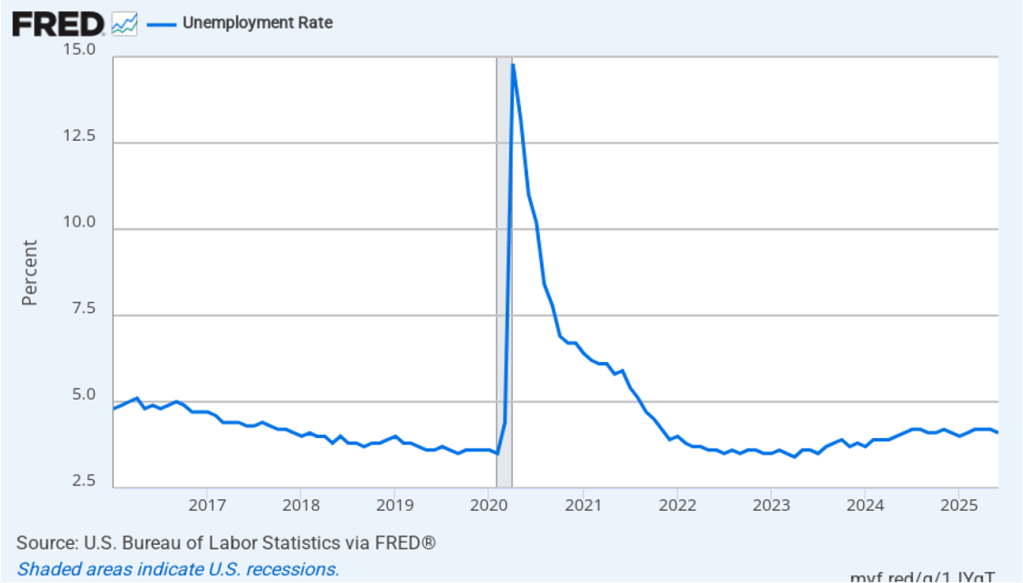

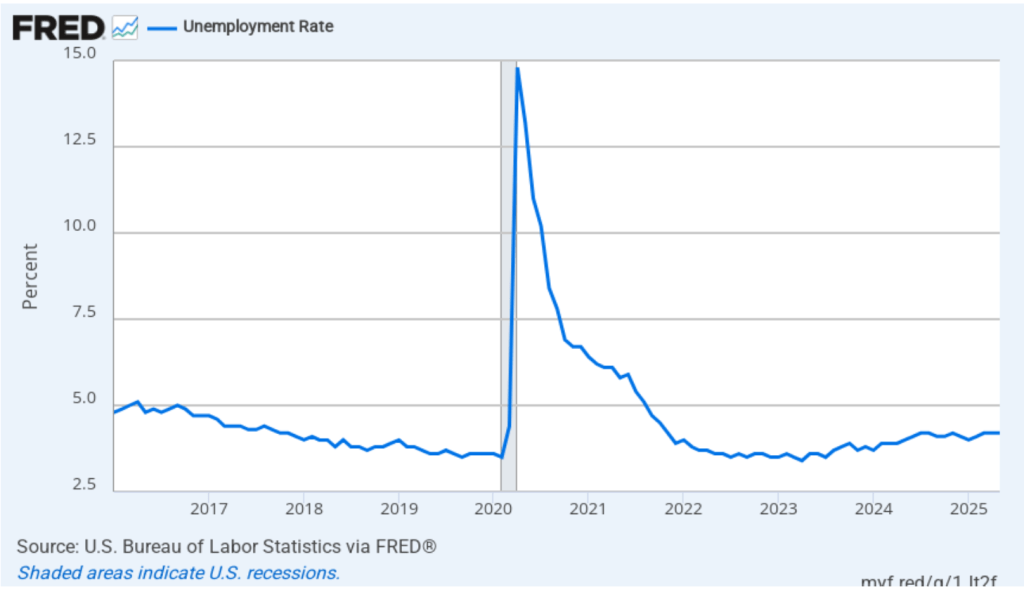

The unemployment rate declined from 4.2 in May to 4.1 percent in June. Economists surveyed had forecast an increase in the unemployment rate to 4.3 percent. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In June, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.5 percent. The unemployment rate would have to rise significantly in the second half of the year for that forecast to be accurate.

Each month, the Federal Reserve Bank of Atlanta estimates how many net new jobs are required to keep the unemployment rate stable. Given a slowing in the growth of the working-age population due the aging of the U.S. population and a sharp decline in immigration, the Atlanta Fed currently estimates that the economy would have to create 113,500 net new jobs each month to keep the unemployment rate stable at 4.1 percent.

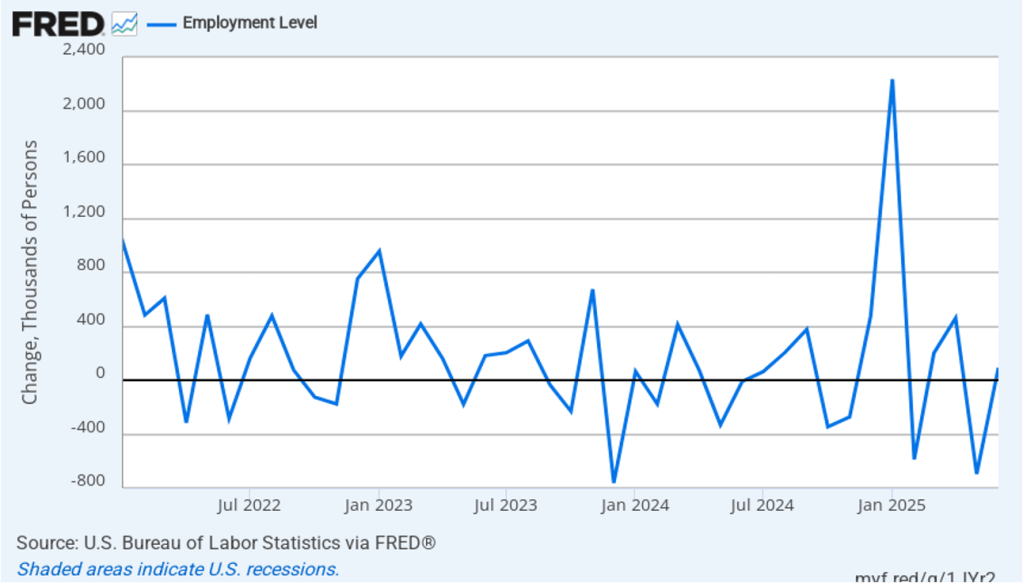

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 93,000 jobs in June, following a decrease of 696,000 jobs in May. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, the two surveys were consistent in both showing a net increase in employment. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

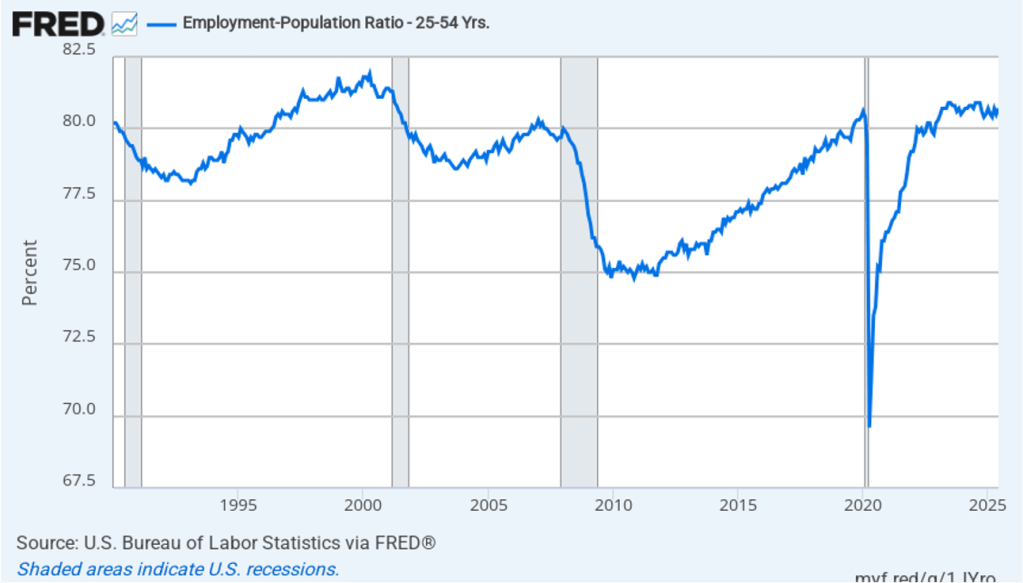

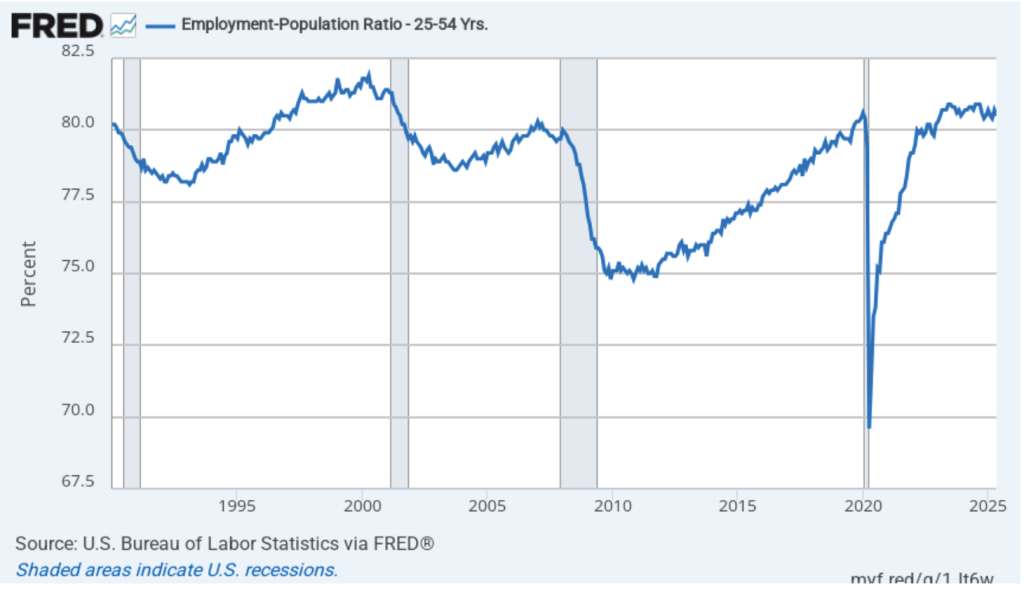

The household survey has another important labor market indicator. The employment-population ratio forprime age workers—those aged 25 to 54—rose from 80.5 percent in May to 80.7 percent in June. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to January 2020.

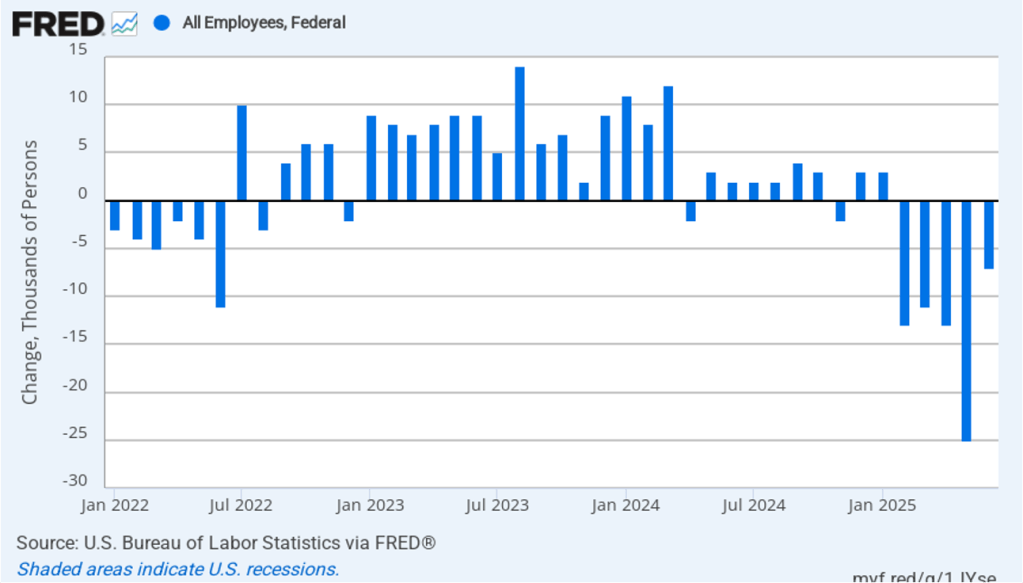

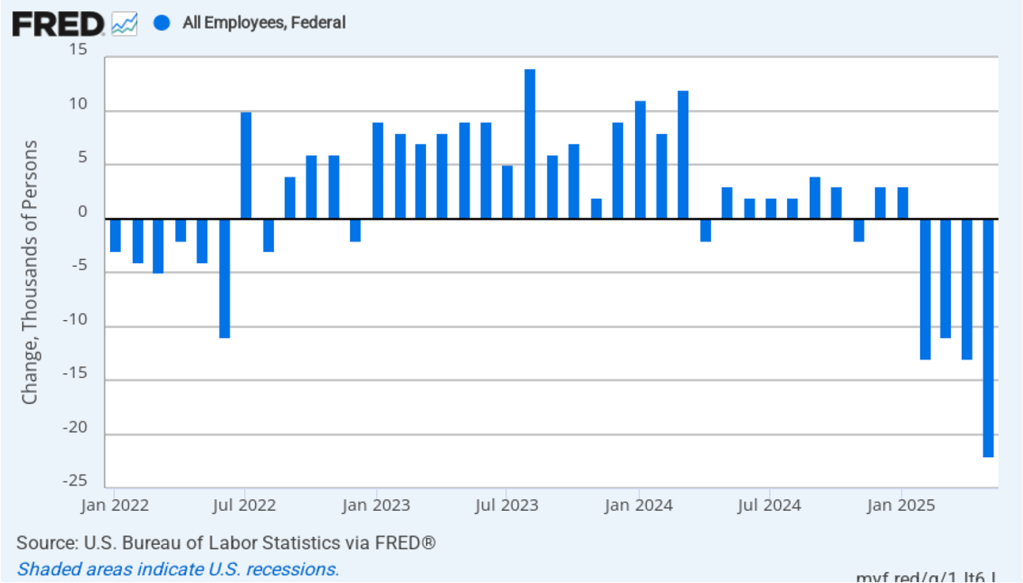

It is still unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 7,000 in June and a total decline of 69,000 since the beginning of February. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

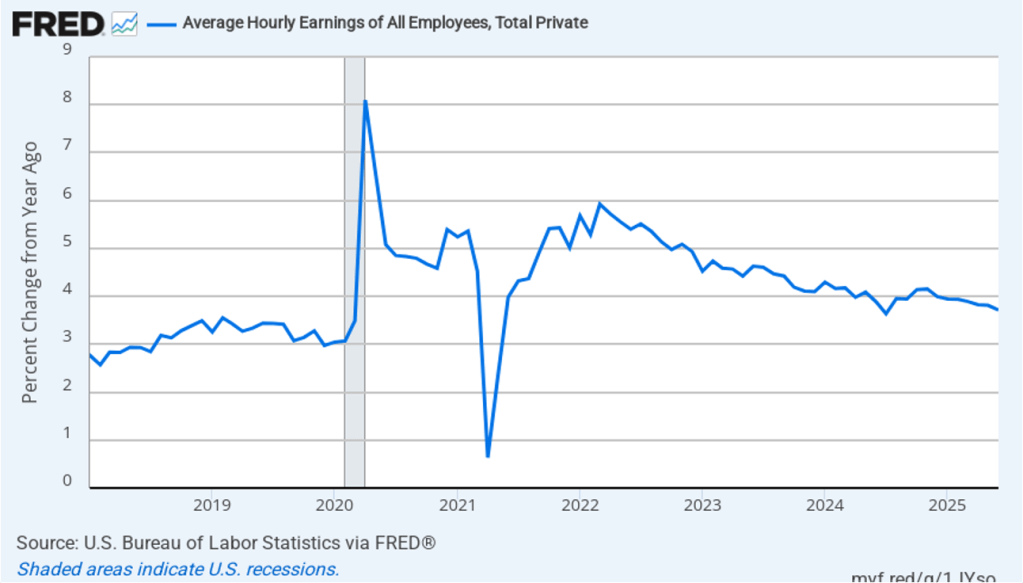

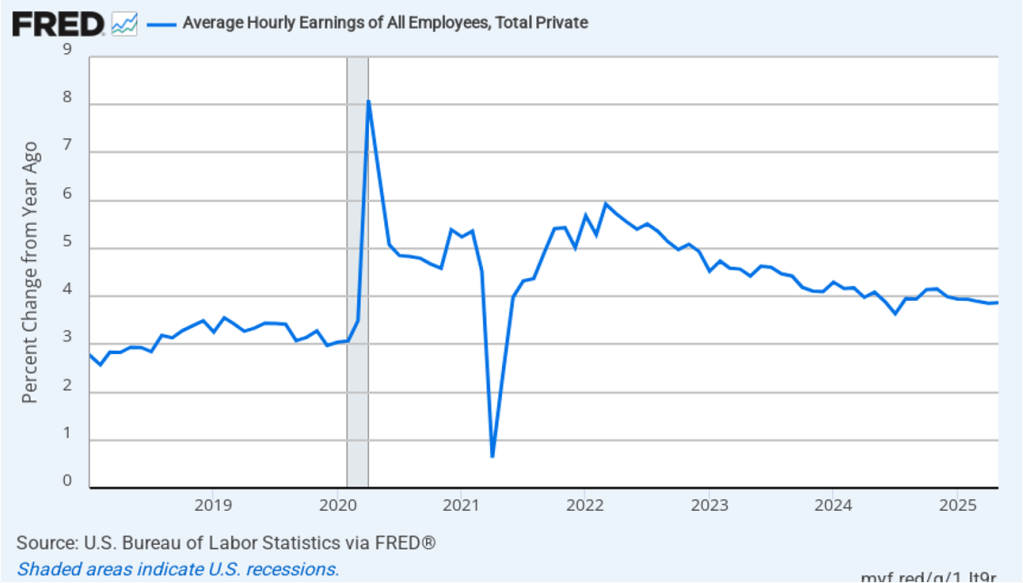

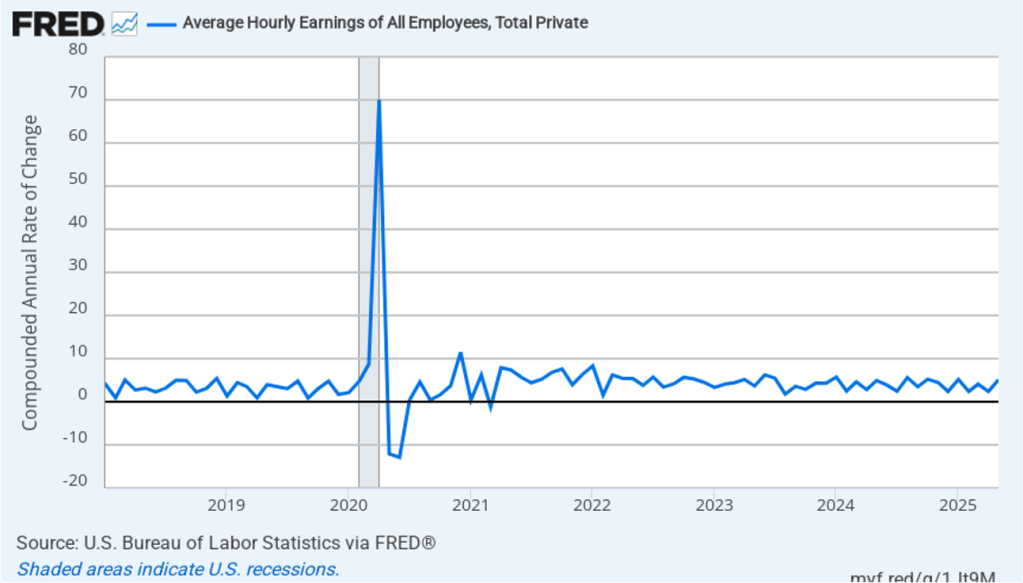

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.7 percent in June, down from an increase of 3.8 percent in May.

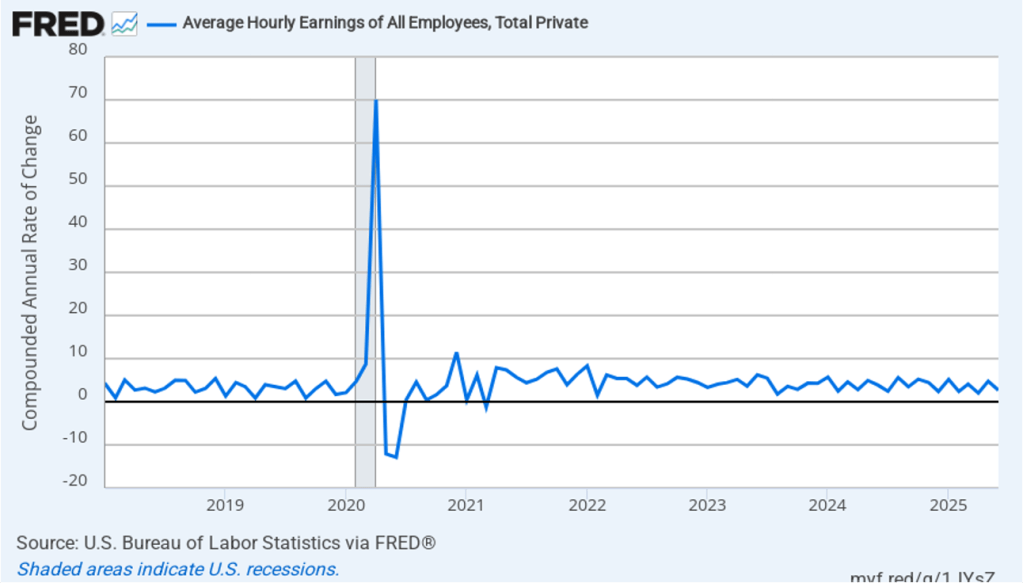

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In June, the 1-month rate of wage inflation was 2.7 percent, down significantly from 4.8 percent in May. If the 1-month increase in AHE is sustained, it would indicate that the Fed may have an easier time achieving its 2 percent target rate of price inflation. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

Before today’s jobs reports the signs that the labor market was weakening, which we discussed earlier, had led some economists and policymakers to speculate that a weak jobs report would lead the FOMC to cut its target range for the federal funds rate at its next meeting on July 29–30. That now seems very unlikely.

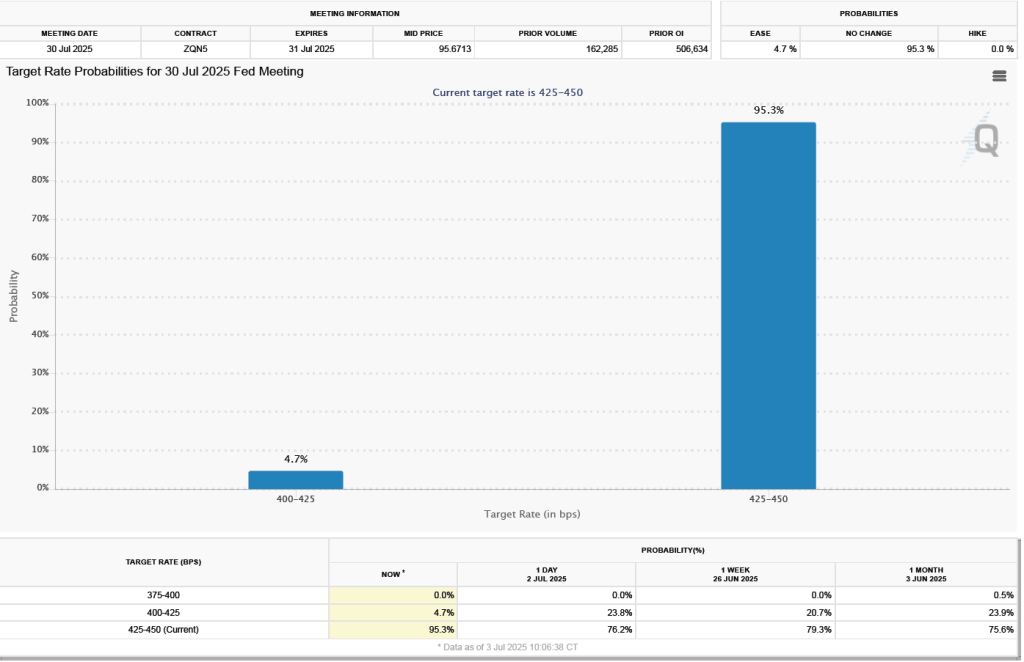

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today investors assign a 95.3 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at the July meeting.

Image illustrating stablecoins generated by ChatGTP4-o

Recently, U.S. Treasury Secretary Scott Bessent testified before Congress that the value of stablecoins could reach $2 trillion. In a post on X (formerly Twitter) he stated that “that stablecoins could grow into a $3.7 trillion market by the end of the decade.” Those amounts are far above the $250 billion estimated value of stablecoins in June 2025, yet still small relative to the value of M2—currently $21.9 trillion. But if the value of stablecoins were to rise to $2 trillion, that would be large enough to have a noticeable effect on the U.S. financial system.

As we discuss in Macroeconomics, Chapter 24 and in Money, Banking, and the Financial System, Chapter 2, stablecoins are a type of cryptocurrency—bitcoin is the best-known cryptocurrency—that can be bought and sold for a constant number of units of a currency, usually U.S. dollars. Typically, one stablecoin can be exchanged for one dollar.

Tether CEO Paolo Ardoino (photo from Bloomberg news via the Wall Street Journal)

Firms that issue stablecoins will redeem them in the underlying currency, which—as already noted—is nearly always the U.S. dollar. To make the promise to redeem stablecoins in dollars credible, firms that issue stablecoins hold reserve assets that are safe and highly liquid, such as U.S. Treasury bills or U.S. dollar bank deposits. Tether, which is headquartered in El Salvador, is the largest issuer of stablecoins, with about two-thirds of the market. As with bitcoins and other cryptocurrencies, stablecoins are stored and traded on public blockchains, which are decentralized networks of ledgers that record transactions. This system avoids the use of financial intermediaries—such as banks—which advocates for cryptocurrencies see as a key advantage because it eliminates the possibility that the intermediary might reject the transaction. But it also increases the appeal of stablecoins to people engaged in illegal activities.

Advocates for stablecoins believe that they can become a digital medium of exchange, which is a role that initially bitcoin was intended to play. The swings in the value of bitcoin turned out to be much larger than most people expected and made that crypto currency unsuitable for use as a medium of exchange. Stablecoins avoid this problem by keeping the value of the stablecoins fixed at one dollar. To this point, though, stablecoins have been primarily used to buy and sell bitcoin and other crypto currencies. As Federal Reserve Governor Christopher Waller put it in a speech earlier this year: “By their tie to the dollar, stablecoins are the medium of exchange and unit of account in the crypto ecosystem.” According to Waller, more than 80 percent of trading in cryptocurrencies is conducted using stablecoins.

One drawback to stablecoins is that firms that issue them charge a fee to redeem them. For instance, Tether requires that a minimum of $100,000 of stablecoins be redeemed and charges a fee of 0.1 percent of the amount redeemed with a minimum charge of $1,000. The redemption fee would be less important if stablecoins are used in large dollar transactions, such as occur in international trade. Advocates for stablecoins believe that they are particularly well suited for use in cross-border transactions because they don’t involve banks, as typically is necessary when firms buy or sell goods or services in foreign countries. The fees stablecoin issuers charge are generally lower than the fees banks charge for foreign exchange transactions.

The main source of profit for firms issuing stablecoins is the interest they earn on the assets they use to back the stablecoins they issue. Note, though, that firms issuing stablecoins have an incentive to buy riskier assets in order to increase the return on the stablecoins they issue. The incentives are similar to those banks face in investing depositors’ funds in assets that are riskier than the depositors would prefer. However, the risk that commercial banks take on is limited by bank regulations, which don’t yet apply to firms issuing stablecoins, although they may soon.

On June 17, the U.S. Senate moved to provide a regulatory framework for stablecoins by passing the Guiding and Establishing National Innovation for U.S. Stablecoins Act (Genius Act). The act requires that firms issuing stablecoins in the United States back them 100 percent with a limited number of reserve assets: dollar deposits in banks, Treasury securities that mature in 93 days or less, repurchase agreements backed by Treasuries (we discuss repurchase agreements in Macroeconomics, Chapter 15; Economics, Chapter 25; and Money, Banking, and the Financial System, Chapter 10), and money market funds that invest in eligible Treasury securities and repurchase agreements. Issuers of stablecoins will be subject to audits by U.S. federal regulators. To become law, the Genius Act must also be passed by the U.S. House and signed by President Trump.

Passage of the Genius Act would potentially provide a regulatory framework that would reassure users that the stablecoins they hold can be readily redeemed for dollars. Passage is also expected to lead some large retail firms, such as Walmart and Amazon, to issue stablecoins that could be used to make purchases on their sites. If enough consumers are willing to use stablecoins, these large retailers could save the fees they currently pay to credit card companies. In addition, stablecoin transactions can be cleared instantly, as opposed to the several days it can take for credit card payments to clear. Why would a consumer want to use stablecoin rather than a credit card to pay for something? Apart from the familiarity of using credit cards, the cards often provide rewards, such as points that can be redeemed for airline tickets or hotel stays. To attract consumers, stablecoin issuers would likely have to offer similar rewards to consumers who use stablecoins to make purchases.

As Waller notes, it will likely take years before consumers and firms routinely use stablecoins for day-to-day transactions. Today, very few retail firms are equipped to accept stablecoins and very few consumers own stablecoins.

Passage of the Genius Act would pose potential problems for Tether. Tether has held a wide range of reserve assets to back its stablecoins, including bitcoin and precious metals. It has also not been willing to be fully audited. Either Tether would have to change its business model to fit the requirements of the Genius Act or it would have to issue a separate stablecoin that would be used only in the United States and would meet the Genius Act requirements.

We noted earlier that Treasury Secretary Bessent believes that over the next few years, the value of stablecoins could increase to several trillions dollars. If that happens, the demand for Treasury securities would increase substantially as firms issuing stablecoins accumulated reserve assets. The result could be higher prices on Treasury securities and lower interest rates, which would eventually reduce the interest payments the Treasury makes on the federal government’s debt.

Finally, as we note in the text, Barry Eichengreen of the University of California, Berkeley as been a notable skeptic of stablecoins. As he wrote back in 2018, when the idea of stablecoins was just beginning to be widely discussed, when someone exchanges a dollar for a stablecoin, “one of us then will have traded a perfectly liquid dollar, supported by the full faith and credit of the U.S. government, for a cryptocurrency with questionable backing that is awkward to use. This exchange may be attractive to money launderers and tax evaders, but not to others.”

Could issuers of stablecoins be subject to runs like the one that led to the failure of Silicon Valley Bank in the spring of 2023?

In a recent opinion column in the New York Times, Eichengreen wrote that he is concerned about the possibility of runs on stablecoins. As we discuss in Macroeconomics, Chapter 14, and in Money, Banking, and the Financial Systems, Chapter 10, a commercial bank can be subject to a run if the bank’s depositors believe that the value of the bank’s assets are no longer sufficient to pay off the bank’s depositors. As we discuss in this blog post, Silocon Valley Bank experienced a run in the spring of 2023 that affected several other banks. Runs on commercial banks are unusual in the United States because of deposit insurance and the willingness of the Federal Reserve to act as lender of last resort to banks suffering liquidity problems. Eichengreen raises the question of whether stablecoins could experience runs if holders of the stablecoins come to doubt that the value of issuers’ reserve assets is sufficient to redeem all the coins.

Although the Genius Act provides for regulation of stablecoin issuers, Eichengreen believes that if enough firms begin issuing stablecoins, it’s likely that at some point one of them will experience a decline in the value of its reserve assets, which will cause a run. If the run spreads from one issuer to many in a process called contagion, stablecoin issuers will have to sell reserve assets, including Treasury securities. The result could be a sharp fall in the prices of those asset and an increase in interest rates. It’s possible that the outcome could be a wider financial panic and a deep recession. To head off that possibility, the Federal Reserve might feel obliged to intervene to save some, possibly many, stablecoin issuers from failing. The result could be that taxpayer dollars would flow to firms issuing stablecoins, which would likely cause a significant political backlash.

Many people see stablecoins as an exciting development in the financial system. But, as we’ve noted, there still remain some substantial roadblocks in the way of stablecoins becoming an important means of transacting business in the U.S. economy.

Today (June 27), the BEA released monthly data on the personal consumption expenditures (PCE) price index as part of its “Personal Income and Outlays” report. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows headline PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2016, with inflation measured as the percentage change in the PCE from the same month in the previous year. In May, headline PCE inflation was 2.3 percent, up from 2.2 percent in April. Core PCE inflation in May was 2.7 percent, up from 2.6 percent in April. Headline PCE inflation was equal to the forecast of economists surveyed, while core PCE inflation was slightly higher than forecast.

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation increased in from 1.4 percent in April to 1.6 percent in May. Core PCE inflation also increased from 1.6 percent in April to 2.2 percent in May. So, both 1-month PCE inflation estimates are close to the Fed’s 2 percent target. The usual caution applies that 1-month inflation figures are volatile (as can be seen in the figure), so we shouldn’t attempt to draw wider conclusions from one month’s data. In addition, these data likely don’t capture fully the higher prices likely to result from the tariff increases the Trump administration announced on April 2.

Fed Chair Jerome Powell has frequently noted that inflation in non-market services can skew PCE inflation. Non-market services are services whose prices the BEA imputes rather than measures directly. For instance, the BEA assumes that prices of financial services—such as brokerage fees—vary with the prices of financial assets. So that if stock prices fall, the prices of financial services included in the PCE price index also fall. Powell has argued that these imputed prices “don’t really tell us much about … tightness in the economy. They don’t really reflect that.” The following figure shows 12-month headline inflation (the blue line) and 12-month core inflation (the red line) for market-based PCE. (The BEA explains the market-based PCE measure here.)

Headline market-based PCE inflation was 2.1 percent in May, up from 1.9 percent in April. Core market-based PCE inflation was 2.4 percent in May, up from 2.3 percent in April. So, both market-based measures show similar rates of inflation in May as the total measures do. In the following figure, we look at 1-month inflation using these measures. The 1-month inflation rates are both lower than the 12-month rates. One-month headline market-based inflation was 1.5 percent in May, down from 2.3 percent in April. One-month core market-based inflation was 2.1 percent in May, down from 2.7 percent in April. As the figure shows, the 1-month inflation rates are more volatile than the 12-month rates, which is why the Fed relies on the 12-month rates when gauging how close it is coming to hitting its target inflation rate.

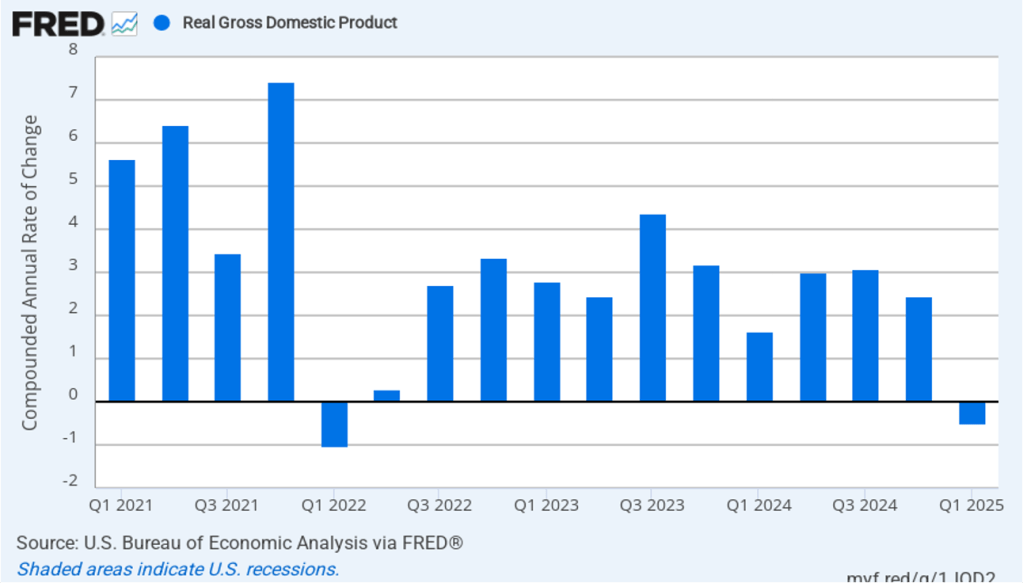

Earlier this week, the BEA released a revised estimate of real GDP growth during the first quarter of 2025—January through March. The BEA’s advance estimate, released on April 30, was that real GDP fell by 0.3 percent in the first quarter, measured at an annual rate. (We discussed the BEA’s advance estimate in this blog post.) The BEA’s revised estimate is that real GDP fell by 0.5 percent in the first quarter. The following figure shows the current estimated rates of real GDP growth in each quarter beginning in 2021.

As we noted in our post discussing the advance estimate, one way to strip out the effects of imports, inventory investment, and government purchases—which can all be volatile—is to look at real final sales to private domestic purchasers, which includes only spending by U.S. households and firms on domestic production. According to the advance estimate, real final sales to private domestic purchasers increased by 3.0 percent in the first quarter of 2025. According to the revised estimate, real final sales to private domestic purchasers increased by only 1.9 percent in the first quarter, down from 2.9 percent growth in the fourth quarter of 2024. These revised data indicate that economic growth likely slowed in the first quarter.

In summary, this week’s data provide some evidence that the inflation rate is getting close to the Fed’s 2 percent annual target and that economic growth may be slowing. Do these data make it more likely that the Fed’s policymaking Federal Open Market Committee (FOMC) will cut its target for the federal funds rate relatively soon?

Investors who buy and sell federal funds futures contracts still expect that the FOMC will leave its federal funds rate target unchanged at its next meetings on July 29–30 and September 16–17. Investors expect that the committee will cut its target at its October 28–29 meeting. (We discuss the futures market for federal funds in this blog post.) There remains a possibility, though, that future macroeconomic data releases, such as the June employment data to be released on July 3, may lead the FOMC to cut its target rate sooner.

Fed Chair Jerome Powell speaking at a press conference following a meeting of the FOMC (photo from federalreserve.gov)

Members of the Fed’s policymaking Federal Open Market Committee (FOMC) had signaled clearly before today’s (June 18) meeting that the committee would leave its target range for the federal funds rate unchanged at 4.25 percent to 4.50 percent. In the statement released after its meeting, the committee noted that a key reason for keeping its target range unchanged was that: “Uncertainty about the economic outlook has diminished but remains elevated.” Committee members were unanimous in voting to keep its target range unchanged.

In his press conference following the meeting, Fed Chair Jerome Powell indicated that a key source of economic uncertainty was the effect of tariffs on the inflation rate. Powell indicated that the likeliest outcome was that tariffs would lead to the inflation rate temporarily increasing. He noted that: “Beyond the next year or so, however, most measures of longer-term expectations [of inflation] remain consistent with our 2 percent inflation goal.”

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

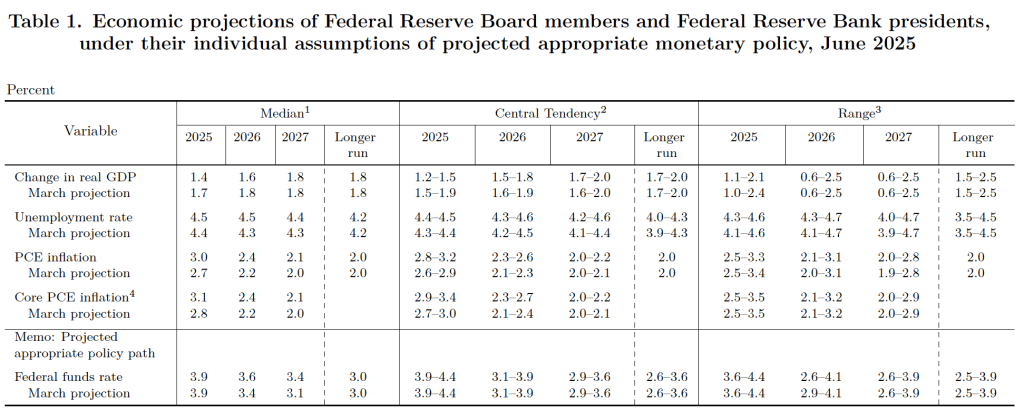

After the meeting, the committee also released a “Summary of Economic Projections” (SEP)—as it typically does after its March, June, September, and December meetings. The SEP presents median values of the 18 committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release.

There are several aspects of these forecasts worth noting:

Committee members reduced their forecast of real GDP growth for 2025 from 1.7 percent in March to 1.4 percent today. (It had been 2.1 percent in their December forecast.) Committee members also slightly increased their forecast of the unemployment rate at the end of 2025 from 4.4 percent to 4.5 percent. (The unemployment rate in May was 4.2 percent.)

Committee members now forecast that personal consumption expenditures (PCE) price inflation will be 3.0 percent at the end of 2025. In March they had forecast that it would be 2.7 percent at the end of 2025, and in December, they had forecast that it would 2.5 percent. Similarly, their forecast of core PCE inflation increased from 2.8 percent to 3.1 percent. It had been 2.5 percent in December. The committee does not expect that PCE inflation will decline to the Fed’s 2 percent annual target until sometime after 2027.

The committee’s forecast of the federal funds rate at the end of 2025 was unchanged at 3.9 percent. The federal funds rate today is 4.33 percent, which indicates that the median forecast of committee members is for two 0.25 percentage point (25 basis points) cuts in their target for the federal funds rate this year. Investors are similarly forecasting two 25 basis point cuts.

During his press conference, Powell indicated that because the tariff increases the Trump administration implemented beginning in April were larger than any in recent times, their effects on the economy are difficult to gauge. He noted that: “There’s the manufacturer, the exporter, the importer and the retailer and the consumer. And each one of those is going to be trying not to be the one to pay for the tariff, but together they will all pay together, or maybe one party will pay it all.” The more of the tariff that is passed on to consumers, the higher the inflation rate will be.

Earlier today, President Trump reiterated his view that the FOMC should be cutting its target for the federal funds rate, labeling Powell as “stupid” for not doing so. Trump has indicated that the Fed should cut its target rate by 1 percentage point to 2.5 percentage points in order to reduce the U.S. Treasury’s borrowing costs. During World War II and the beginning of the Korean War, the Fed pegged the interest rates on Treasury securities at low levels: 0.375 percent on Treasury bills and 2.5 percent on Treasury bonds. Following the Treasury-Federal Reserve Accord, reached in March 1951, the Federal Reserve was freed from the obligation to fix the interest rates on Treasury securities. (We discuss the Accord in Chapter 13 of Money, Banking, and the Financial System.) Since that time, the Fed has focused on its dual mandate of maximum employment and price stability and it has not been directly concerned with affecting the Treasury’s borrowing cost.

Barring a sharp slowdown in the growth of real GDP, a significant rise in the unemployment rate, or a significant rise in the inflation rate, the FOMC seems unlikely to change its target for the federal funds rate before its meeting on September 16–17 at the earliest.

Image generated by ChatGTP-4o of someone shopping for clothes.

Today (June 11), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for May. The following figure compares headline CPI inflation (the blue line) and core CPI inflation (the green line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.4 percent in May—up slightly from 2.3 percent in April.

The core inflation rate,which excludes the prices of food and energy, was 2.9 percent in May—up slightly from 2.8 percent in April.

Headline inflation was slightly lower and core inflation was the same as what economists surveyed had expected.

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) decreased from 2.7 percent in April to 1.0 percent in May. Core inflation (the red line) decreased from 2.9 percent in April to 1.6 percent in May.

The 1-month and 12-month inflation rates are telling different stories, with 12-month inflation indicating that the rate of price increase is running slightly above the Fed’s 2 percent inflation target. The 1-month inflation rate indicates a significant slowing of inflation during May.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that the 1-month inflation rate is particularly volatile. Also note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

One of the key questions facing Federal Reserve policymakers is to what extent inflation will be affected by the increase in tariffs that the Trump administration announced on April 2. The following figure shows 12-month inflation in three categories of products whose prices are thought to be particularly vulnerable to the effects of tariffs: apparel (the blue line), toys (the red line), and motor vehicles (the green line). In May, prices of apparel fell, while the prices of toys and motor vehicles rose by less than 0.5 percent.

The following figure shows 1-month inflation in these categories. In May, the prices of apparel and motor vehicles fell, while the price of toys soared by 17.4 percent, but that followed a decline of 10.3 percent in April.

Taken together this month’s CPI data don’t show much effect of tariffs on inflation. It’s possible that some of the effects of the tariffs have been cushioned by firms increasing their inventories earlier in the year in anticipation of price increases resulting from the tariffs. If so, as firms draw down their inventories, we may see tariff-related increases in the prices of some goods later in the year.

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.0 percent in May, unchanged from April. Twelve-month median inflation (the red line) 3.5 percent in May, also unchanged from April.

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation decreased from 3.0 percent in April to 2.2. percent in May. One-month median inflation declined from 4.0 percent in April to 2.7 percent in May. These data provide some confirmation that inflation likely fell somewhat from April to May.

What are the implications of this CPI report for the actions the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) may take at its next several meetings? Investors who buy and sell federal funds futures contracts still do not expect that the FOMC will cut its target for the federal funds rate at its next two meetings. (We discuss the futures market for federal funds in this blog post.) Investors assign the highest probability to the FOMC making two 0.25 percentage point (25 basis points) cuts in its target rate by the end of the year. Those cuts would reduce the target range from the current 4.25 percent to 4.50 percent range to a range of 3.75 to 4.00 percent. The FOMC’s actions will likely depend in part on what the tariff increases will end up being following the conclusion of the current trade negotiations and what the effect on inflation from the tariff increases will be.

This morning (June 6), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for May. The data in the report show that the labor market continues to be strong. There have been many stories in the media about businesspeople becoming pessimistic as a result of the large tariff increases the Trump Administration announced on April 2—some of which have since been reduced—but we don’t see the effects in the employment data. Some firms may be maintaining employment until they receive greater clarity about where tariff rates will end up. Similarly, although there are some indications that consumer spending may be slowing, to this point, the effects are not evident in the labor market.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

According to the establishment survey, there was a net increase of 139,000 nonfarm jobs during May. This increase was above the increase of 125,000 that economists surveyed had forecast. Somewhat offsetting this increase, the BLS revised downward its previous estimates of employment in March and April by a combined 95,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years.

The unemployment rate was unchanged to 4.2 percent in May. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net decrease of 696,000 jobs in May, following an increase of 461,000 jobs in April. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, the discrepancy between the two surveys in their estimates of the change in net jobs was particularly large. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

The household survey has another important labor market indicator. The employment-population ratio for prime age workers—those aged 25 to 54—declined from 80.7 percent in April to 80.5 percent in May. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to December 2019.

It remains unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 22,000 in May and a total decline of 59,000 beginning in February. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.9 percent in May. Movements in AHE have been remarkably stable, showing increases of 3.9 percent each month since January.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In May, the 1-month rate of wage inflation was 5.1 percent, up sharply from 2.4 percent in April. If the 1-month increase in AHE is sustained, it would indicate that the Fed will struggle to achieve its 2 percent target rate of price inflation. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

Today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. Looming over monetary policy, however, is the expected effect of the Trump Administration’s tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

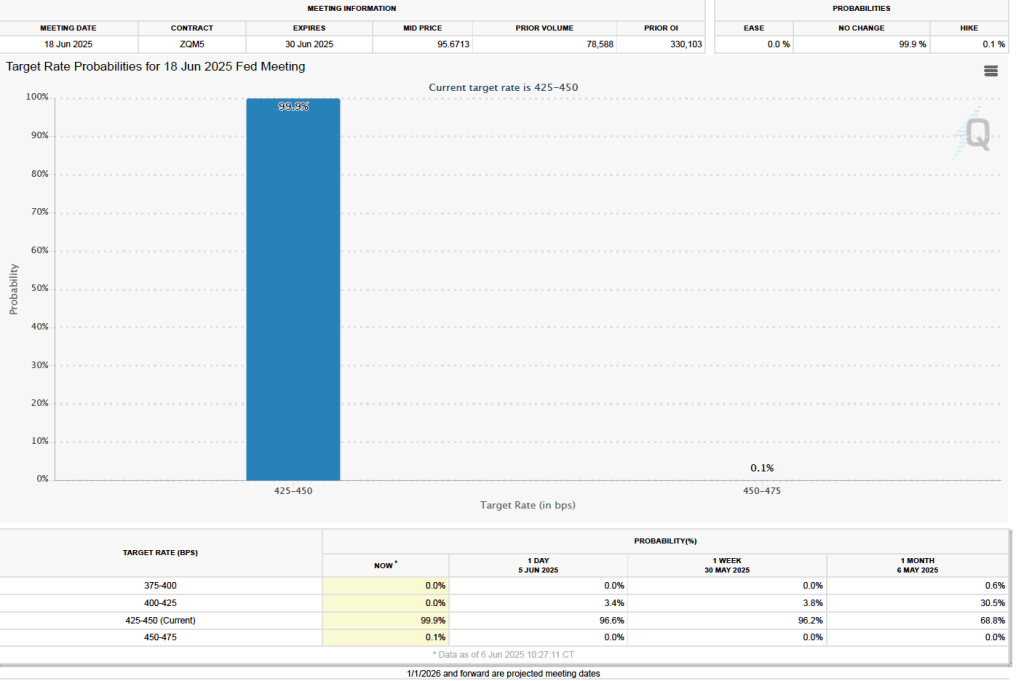

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its June 17–18 meeting. As shown in the following figure, investors assign a 99.9 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

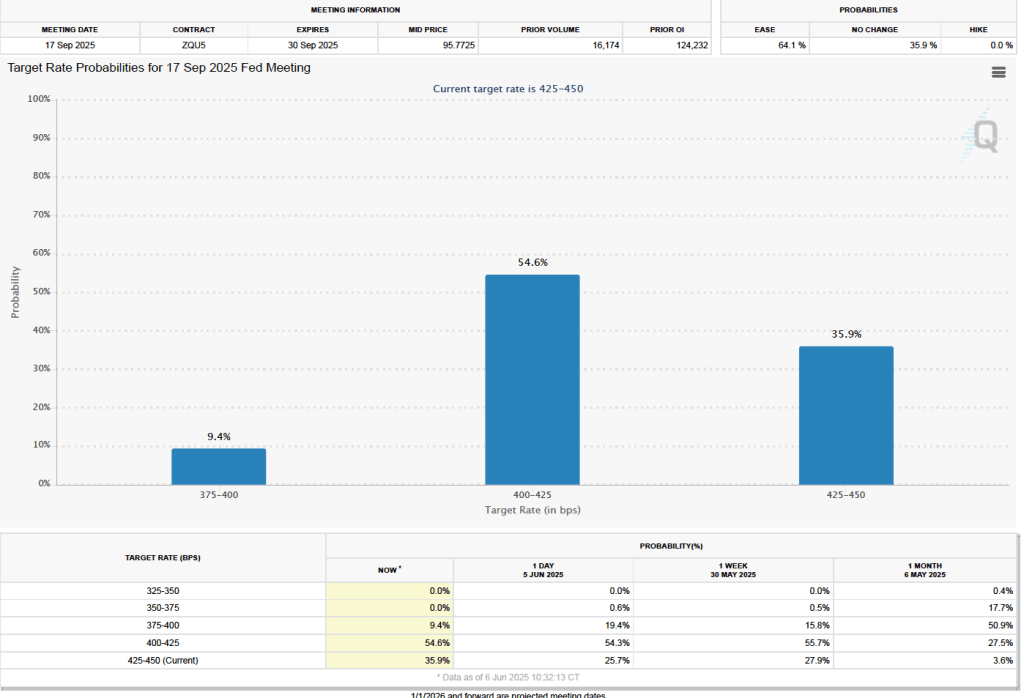

As the following figure shows, investors don’t expect the FOMC to cut its federal funds rate target until the committee’s September 16-17 meeting. Investors assign a probability of 54.6 percent that at that meeting the committee will cut its target range by 0.25 percentage point (25 basis points) to 4.00 percent to 4.25 percent. And a probability of 9.4 percent that the committee will cut its target rate by 50 baisis points to 3.75 percent to 4.00 percent. At 35.9 percent, investors assign a fairly high probability to the committee keeping its target range constant at that meeting.

Photo of the Federal Reserve Bank of Dallas from federalreservehistory.org.

The unusual structure of the Federal Reserve System reflects the political situation at the time that Congress passed the Federal Reserve Act in 1913. As we discuss in Money, Banking, and the Financial System, Chapter 13, at that time, many members of Congress believed that a unified central bank based in Washington, DC would concentrate too much economic power in the hands of the officials running the bank. So, the act divided economic power within the Federal Reserve System in three ways: among bankers and business interests, among states and regions, and between the federal government and the private sector.

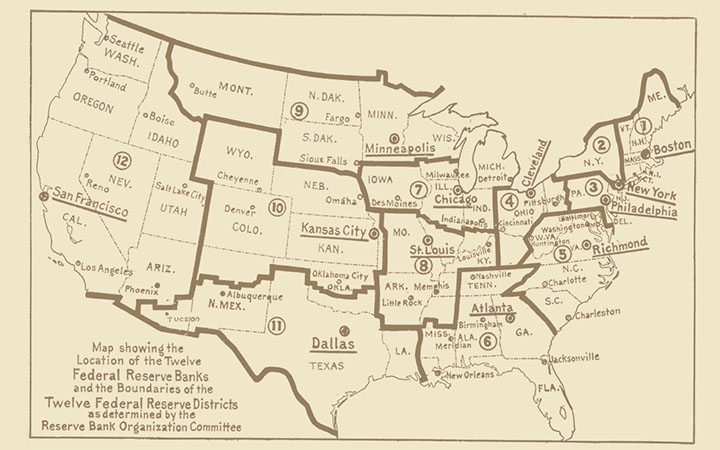

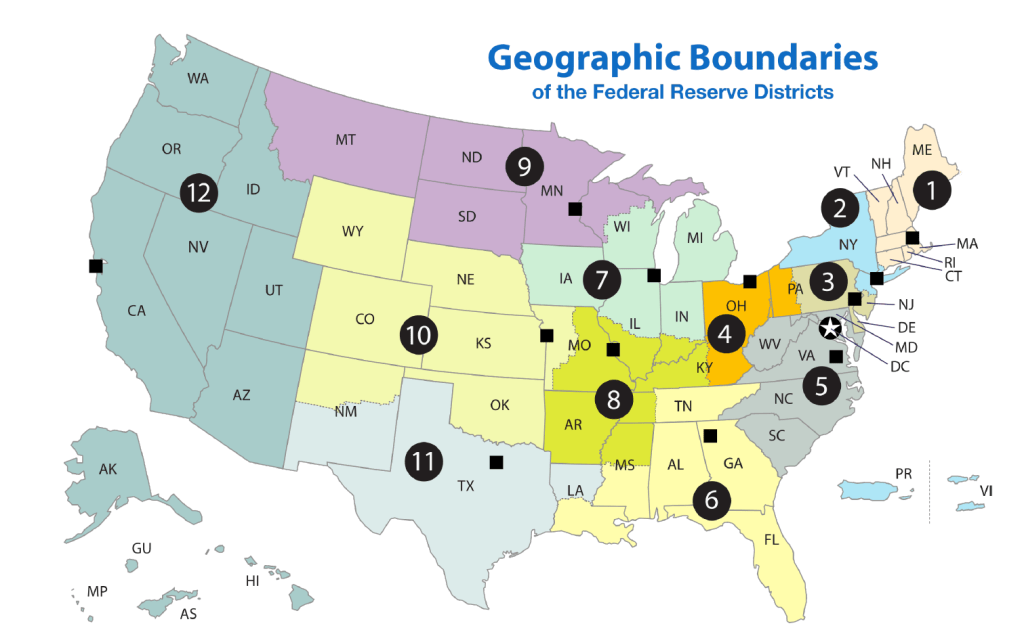

As part of its plan to divide authority within the Federal Reserve System, Congress decided not to establish a single central bank with branches, which had been the structure of both the First and Second Banks of the United States—which were the two attempts by Congress during the period from 1791 to 1836 to establish a central bank. Instead, the Federal Reserve Act divided the United States into 12 Federal Reserve districts, each of which has a Federal Reserve Bank in one city (and, in most cases, additional branches in other cities in the district). The following figure is the original map drawn by the Federal Reserve Organizing Committee in 1913 showing the 12 Federal Reserve Districts. Congress adopted the map with a few changes, following which the areas of the 12 districts have remained largely unchanged down to the present.

The map is from federalreservehistory.org.

The following map shows the current boundaries of the Federal Reserve Districts.

The map is reproduced from the working paper discussed below.

All national banks—commercial banks with charters from the federal government—were required to join the Federal Reserve System. State banks—commercial banks with charters from state governments—were given the option to join. Congress intended that the primary function of each of the Federal Reserve Banks would be to make discount loans to member banks in its region. These loans were to provide liquidity to banks, thereby fulfilling in a decentralized way the system’s role as a lender of last resort.

When banks join the Federal Reserve System, they are required to buy stock in their Federal Reserve Bank, which pays member banks a dividend on this stock. So, in principle, the private commercial banks in each district that are members of the Federal Reserve System own the District Bank. In fact, each Federal Reserve Bank is a private–government joint venture because the member banks enjoy few of the rights and privileges that shareholders ordinarily exercise. For example, member banks do not have a legal claim on the profits of the District Banks, as shareholders of private corporations do.

On paper, the Federal Reserve System is a decentralized organization with a public-private structure. In practice, power within the system is concentrated in the seven member Board of Governors in Washington, DC. Control over the most important aspect of monetary policy—setting the target for the federal funds rate—is vested in the Federal Open Market Committee (FOMC). The voting membership of the FOMC consists of the seven member of the Board of Governors, the president of the Federal Reserve Bank of New York and four other district bank presidents on a rotating basis (although all 12 district presidents participate in committee discussions). The district bank presidents are elected by the boards of directors of the district banks, but the Board of Governors has final say on who is chosen as a district bank president.

Given these considerations, does the structure of the Fed matter or is it an unimportant historical curiosity? There are reasons to think the Fed’s structure does still matter. First, as we discuss in this blog post, in a recent decision, the U.S. Supreme Court implied—but didn’t state explicitly—that, because of the Fed’s structure, U.S. presidents will likely not be allowed to remove Fed chairs except for cause. That is, if presidents disagree with monetary policy actions, they will not be able to remove Fed chairs on that basis.

Second, as Michael Bordo of Rutgers University and the late Nobel Laureate Edward Prescott argue, the decentralized structure of the Fed has helped increase the variety of policy views that are discussed within the system:

“What is unique about the Federal Reserve, at least compared with other entities created by the federal government, is that the Reserve Banks’ semi-independent corporate structure allows for ideas to be communicated to the System . . . . Moreover, it also allows for new and sometimes dissenting views to develop and gestate within the System without being viewed as an expression of disloyalty that undermines the organization as a whole, as would be more likely within a government bureau.”

Finally, recent research by Anton Bobrov of the University of Michigan, Rupal Kamdar of Indiana University, and Mauricio Ulate of the Federal Reserve Bank of San Francisco indicates that the FOMC votes of the district bank presidents reflect economic conditions in those districts. This result indicates that the district bank presidents arrive at independent judgements about monetary policy rather than just reflecting the views of the Board of Governors, which has to approve the appointment of the presidents. The authors analyze the 896 dissenting votes district bank presidents (other than the president of the NY Fed) cast during the period from 1990 to 2017. A dissenting vote is one in which the district bank president voted to either increase or decrease the target for the federal funds relative to the target the majority of the committee favored.

The authors’ key finding is that the FOMC votes of district bank presidents are influenced by the level of unemployment in the district: “a 1 percentage point higher District unemployment rate increases the likelihood that the respective District president will dissent in favor of looser policy [that is, a lower federal funds rate target than the majority of the committee preferred] at the FOMC by around 9 percentage points.” The authors note that: “The influence of local economic conditions on dissents by District presidents reflects the regional structure of the Federal Reserve System, which was designed to accommodate diverse views across the nation.” (The full text of the paper can be found here. A summary of the paper’s findings by Ulate and Caroline Paulson and Aditi Poduri of the San Francisco Fed can be found here.)