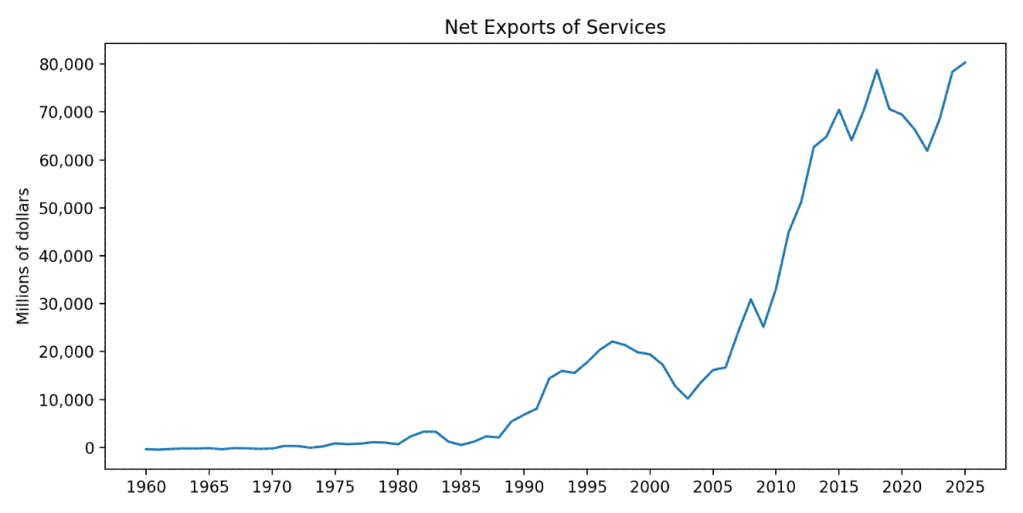

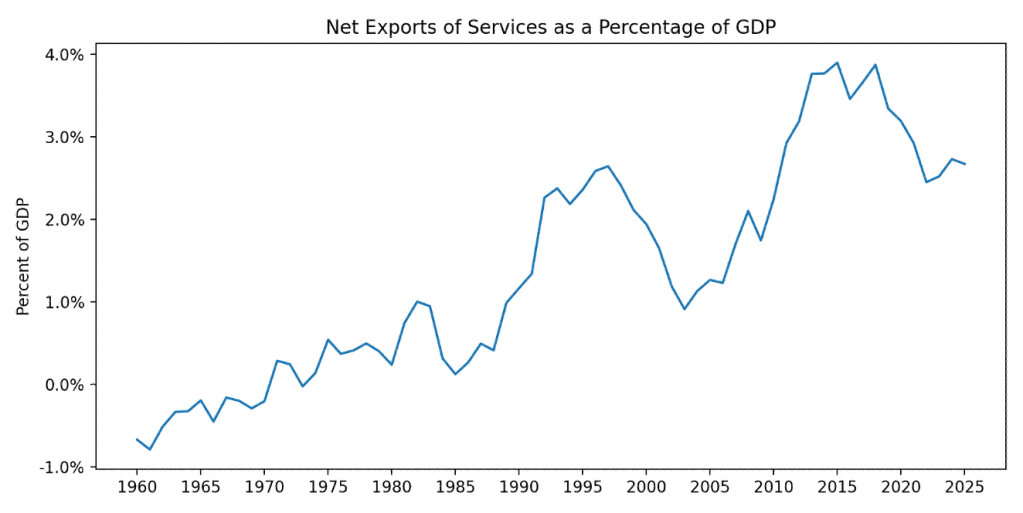

A recent post on the blog of the Federal Reserve Bank of St. Louis reminds us that although the media and some policymakers tend to focus on the fact that the United States typically runs a deficit in trade in goods, it also typically runs a surplus in trade in services. We discuss these points in Economics, Chapter 9, Section 9.1 and Chapter 28, Section 28.1 (Macroeconomics, Chapter 7, Section 7.1 and Chapter 18, Section 18.1, and Microeconomics, Section 9.1). The first of the following figures shows U.S. net exports in services in dollar terms for the period from the first quarter of 1960 through the second quarter of 2025. The second figure show U.S. net exports in services as a percentage of U.S. GDP.

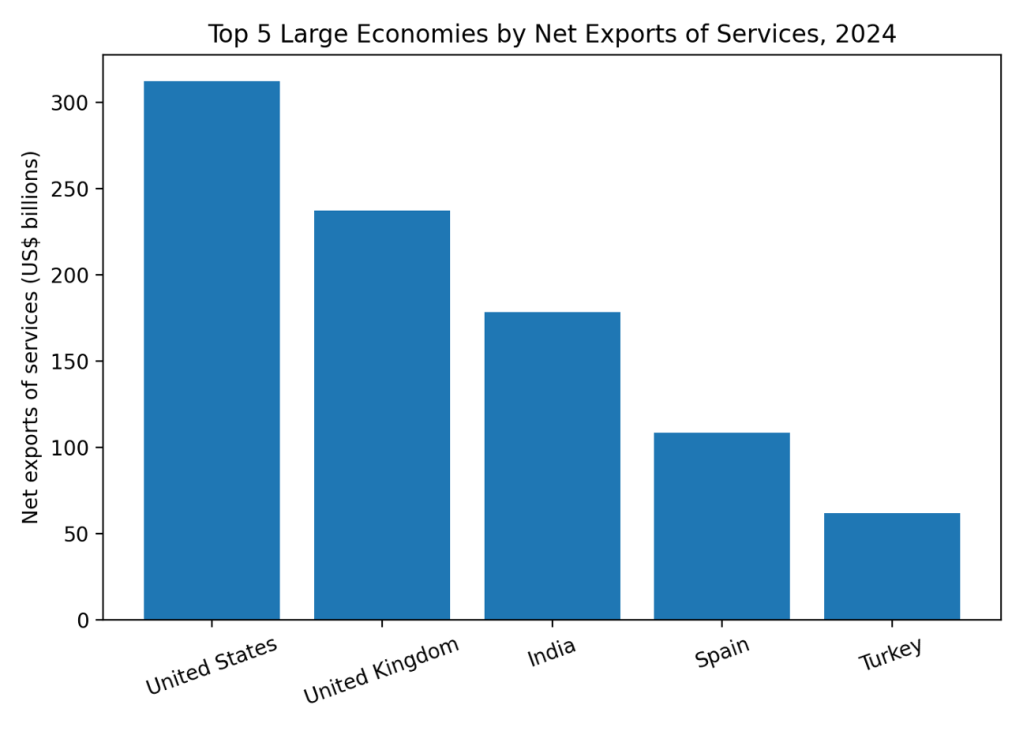

How does the United States compare to other countries? The following figure shows for 2024 the leaders in net exports of services for large economies (those with GDP of $1 trillion or more). The United States has largest value for net exports of services followed by the United Kingdom. China had negative net exports of services in 2024.

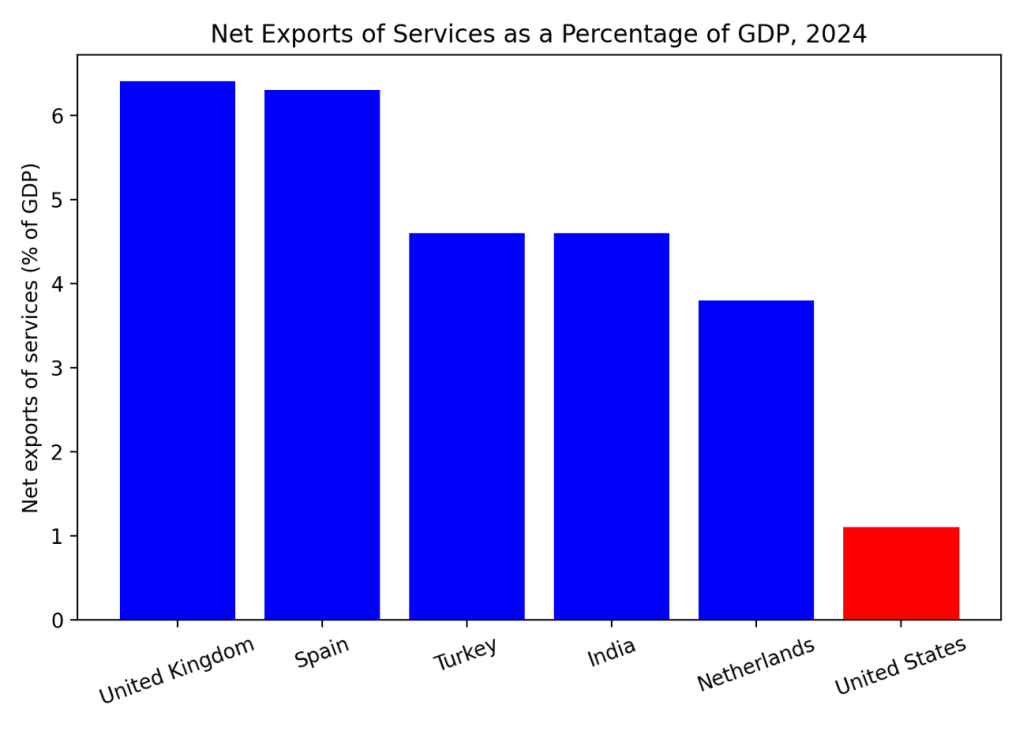

The following figure shows net exports in services as percentage of GDP among large economies. Measured this way, the largest net exporter of services is the United Kingdom, followed by Spain. The United States is included in graph (in red) for comparison and ranks ninth.

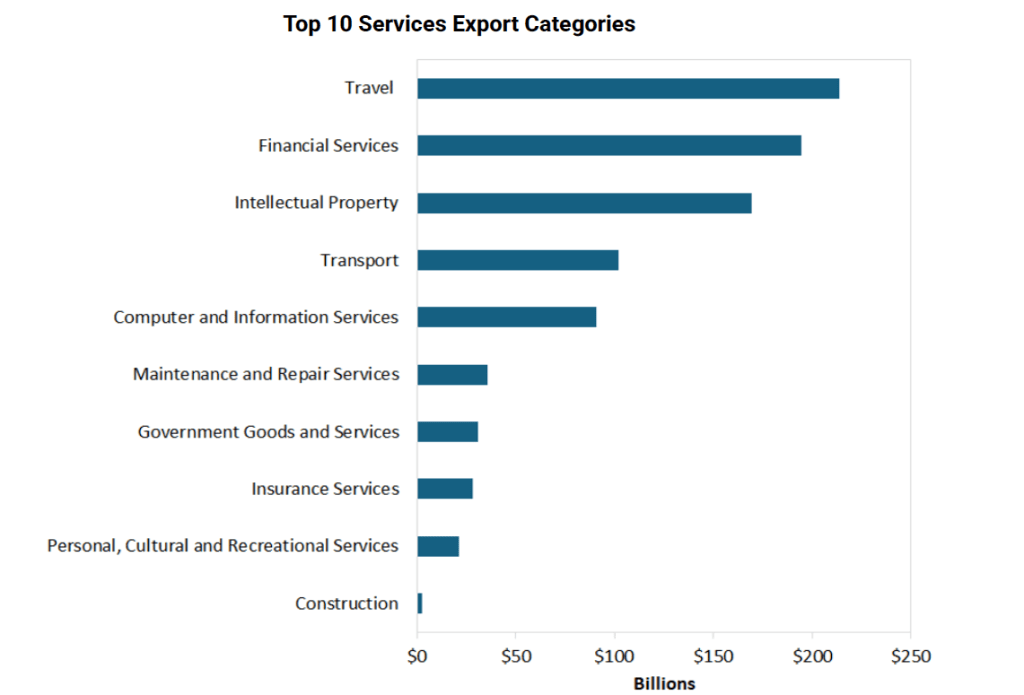

The following table from the St. Louis Fed’s blog posts shows the U.S. industries that export the most services.

The export of travel services represents largely foreign tourism in the United States. For example, if a family from France visits Walt Disney World in Florida, their spending would be included as an export of travel services.

Because of the federal government shutdown from October 1 to November 12, the regular release by the Bureau of Labor Statistics (BLS) of its monthly “Employment Situation” report (often called the “jobs report”) has been disrupted. The jobs report usually has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

Today, the BLS released a jobs report that has data from the payroll survey for both October and November, but data from the household survey only for November. Because of the government shutdown, the household survey for October wasn’t conducted.

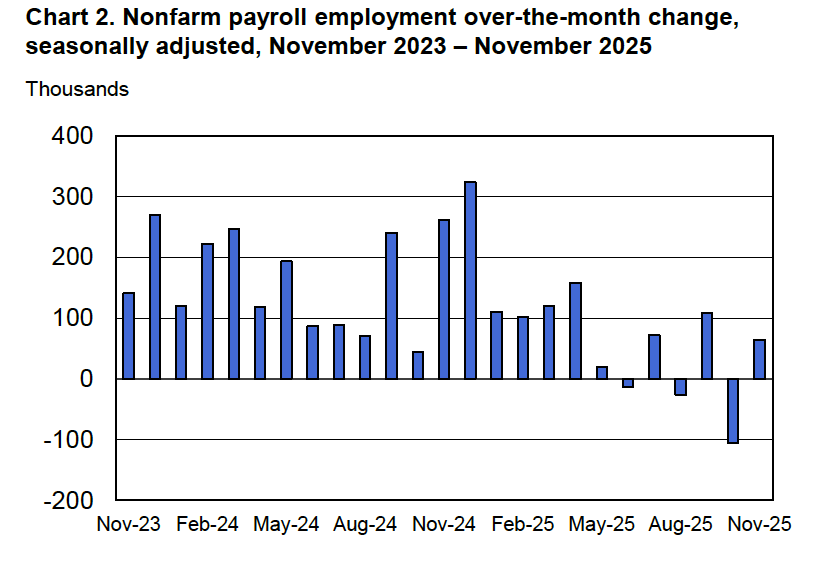

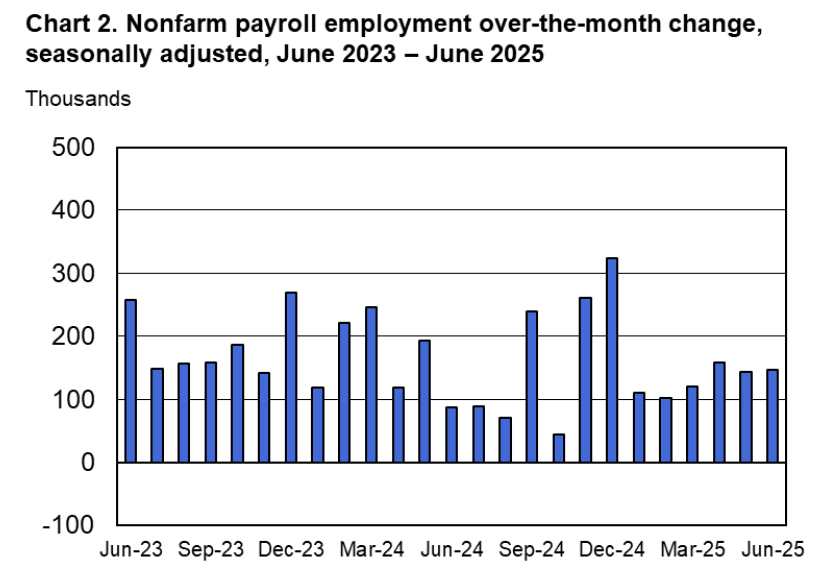

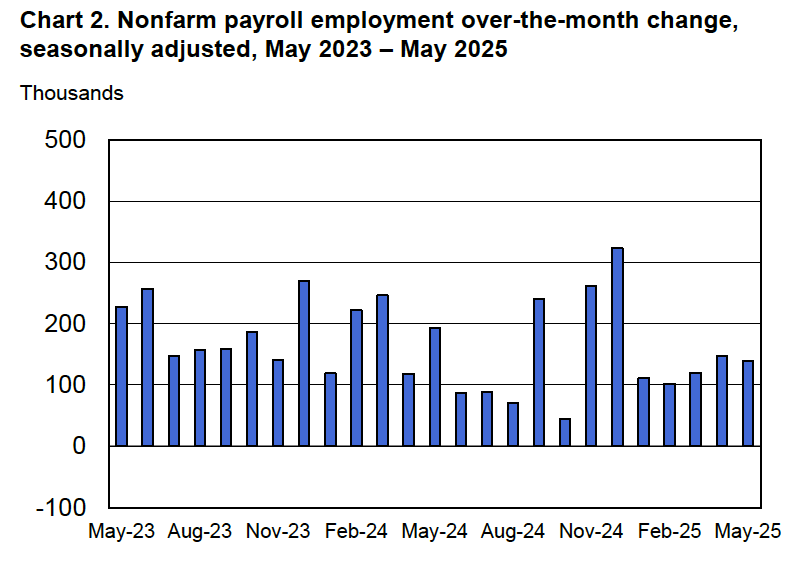

According to the establishment survey, there was a net decrease of 105,000 nonfarm jobs in October and a net increase of 64,000 nonfarm jobs in November. The increase for November was above the increase of 40,000 that economists surveyed by FactSet had forecast. Economists surveyed by the Wall Street Journal had forecast a net increase of 45,000 jobs. The BLS revised downward by a combined 33,000 jobs its previous estimates of employment in August and September. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”)

The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years. The figure illustrates that, as the BLS notes in the report, nonfarm payroll employment “has shown little net change since April.” The Trump administration announced sharp increases in U.S. tariffs on April 2. Media reports indicate that some firms have slowed hiring due to the effects of the tariffs or in anticipation of those effects. In addition, a sharp decline in immigration has slowed growth in the labor force.

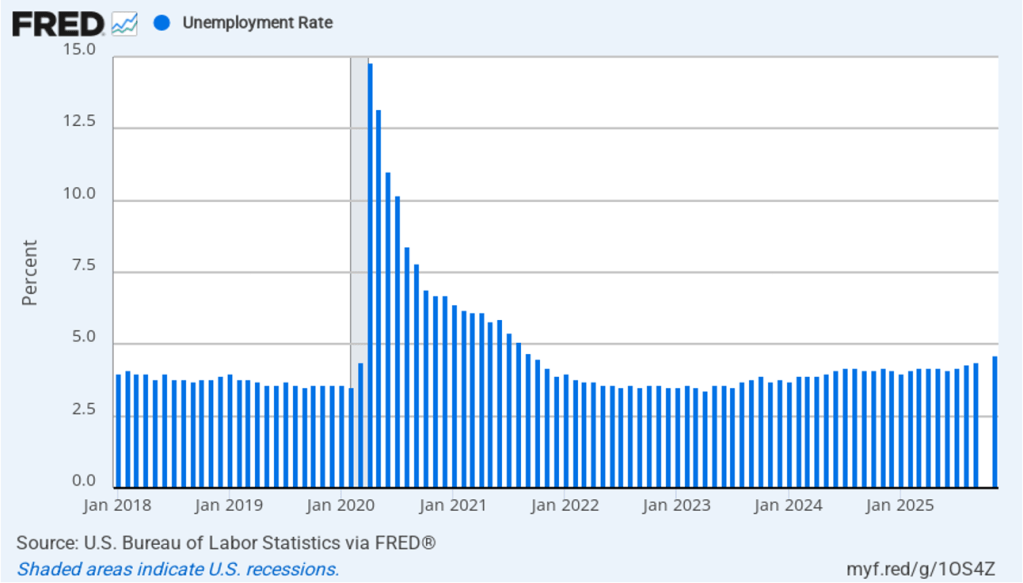

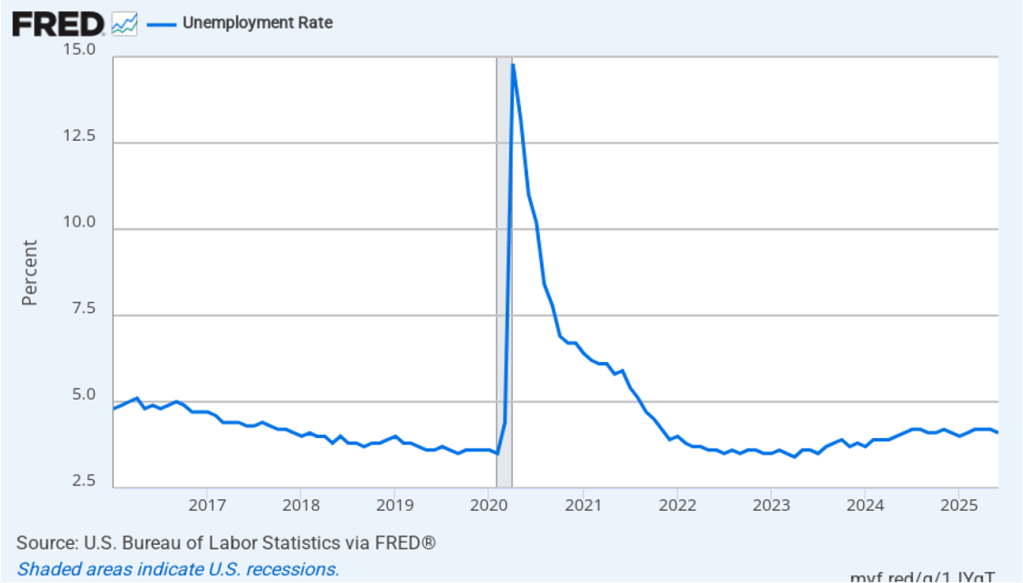

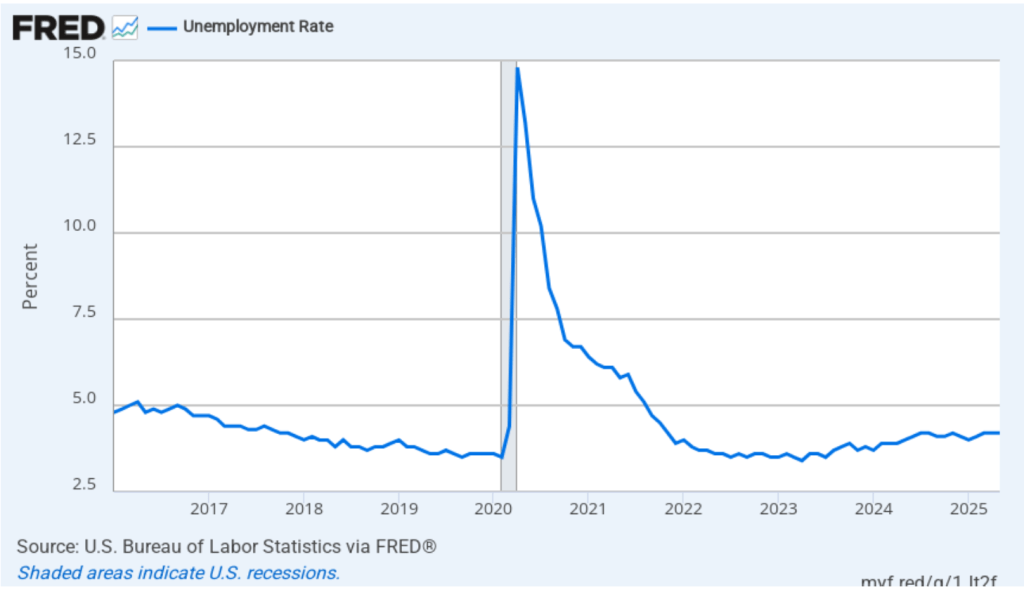

The unemployment rate estimate relies on data collected in the household survey, so there id no unemployment estimate for October. As shown in the following figure, the unemployment rate increased from 4.4 percent in September to 4.6 percent in November, the highest rate since September 2021. The unemployment rate is above the 4.4 percent rate economists surveyed by FactSet had forecast. The unemployment rate had been remarkably stable, staying between 4.0 percent and 4.2 percent in each month from May 2024 to July 2025, before breaking out of that range in August. The Federal Open Market Committee’s current estimate of the natural rate of unemployment—the normal rate of unemployment over the long run—is 4.2 percent. So, unemployment is now well above the natural rate. (We discuss the natural rate of unemployment in Macroeconomics, Chapter 9 and Economics, Chapter 19.)

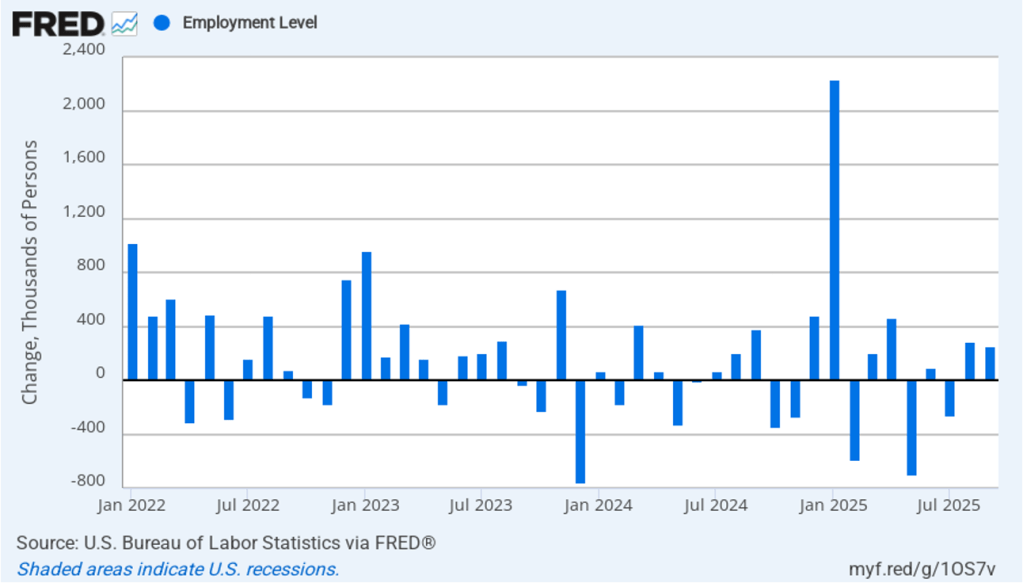

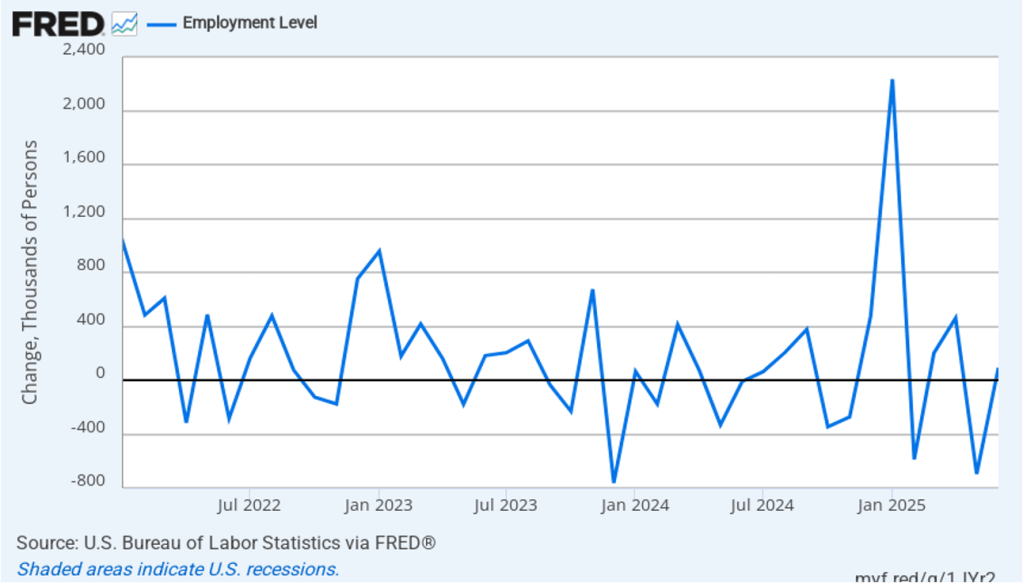

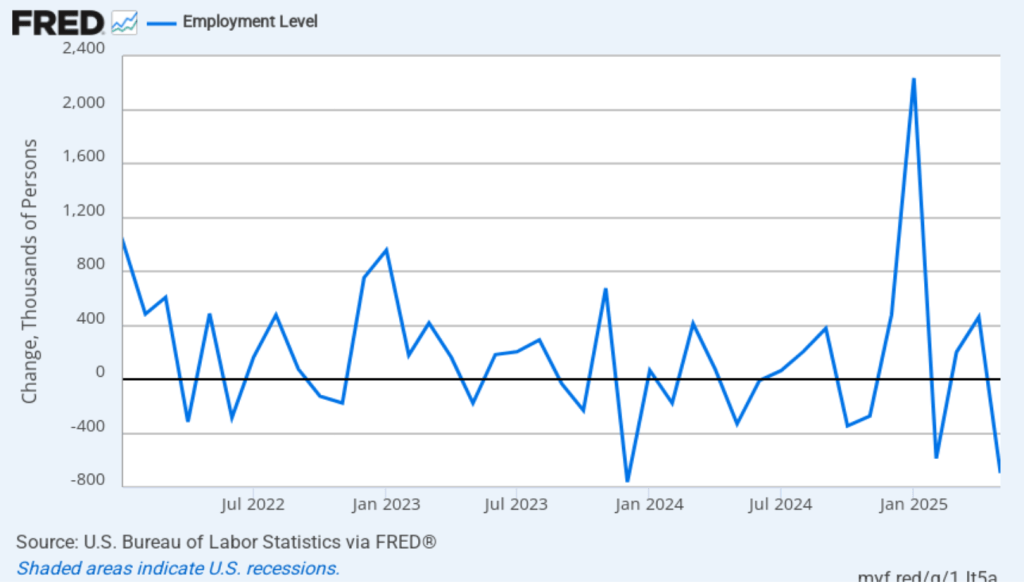

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 96,000 jobs from September to November. In the payroll survey, there was a net decrease in of 41,000 jobs from September to November. In any particular month, the story told by the two surveys can be inconsistent. In this case, we are measuring the change in jobs over a two month interval because there is no estimate from the household survey of employment in October. Over that two month period the household survey is showing more strength in the labor market than is the payroll survey. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

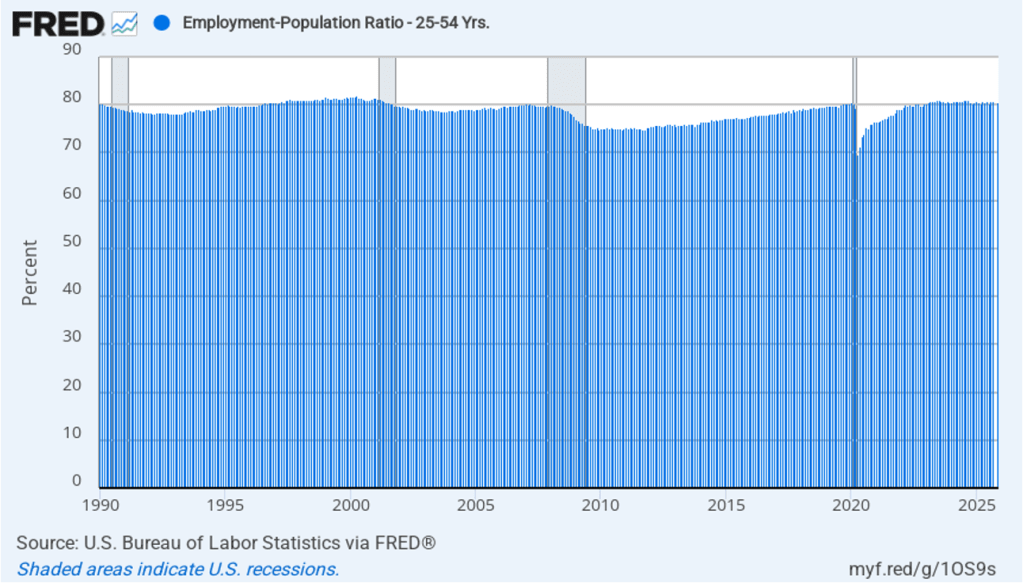

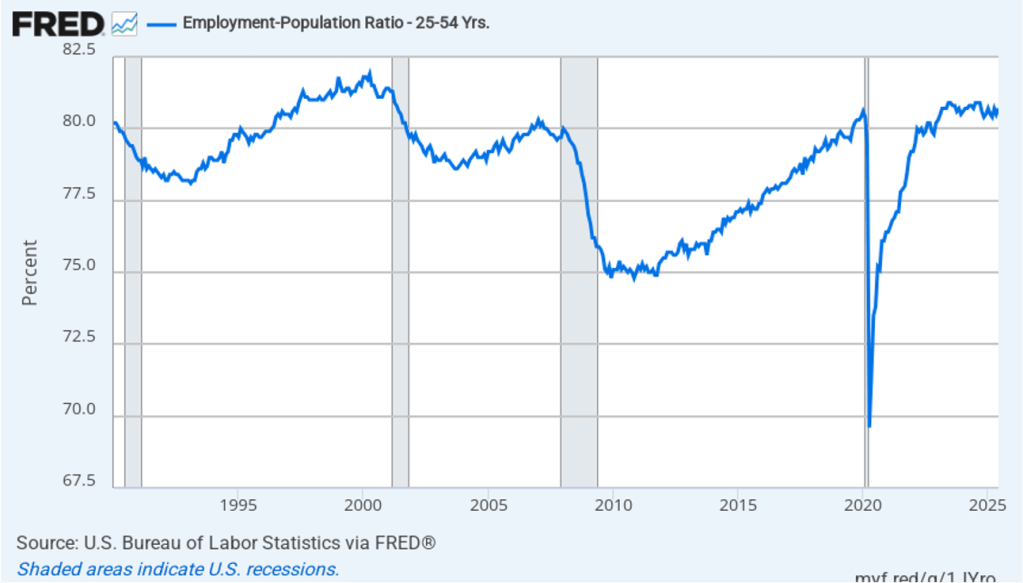

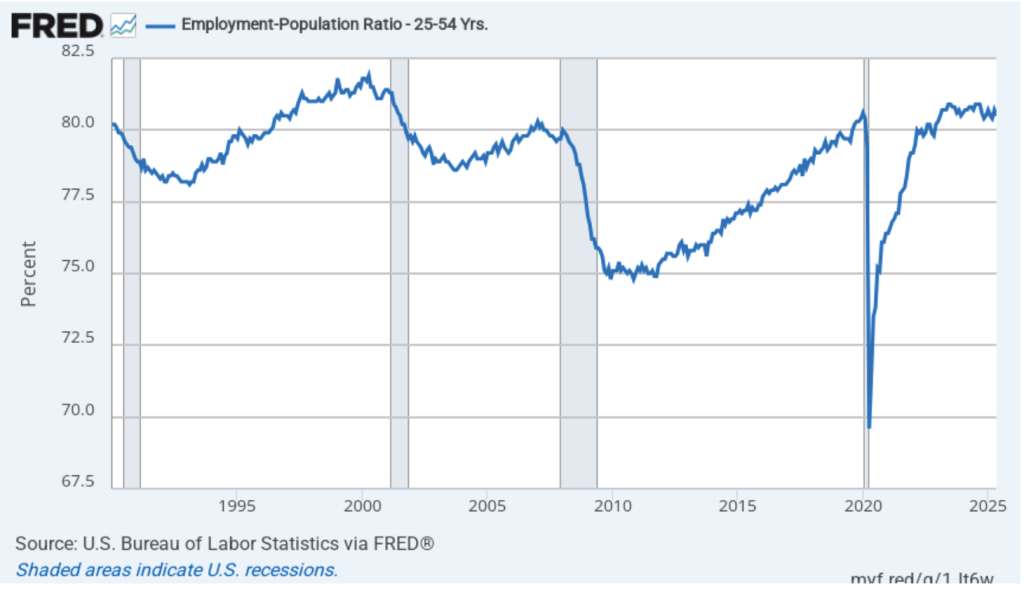

The household survey has another important labor market indicator: the employment-population ratio forprime age workers—those workers aged 25 to 54. In November the ratio was 80.6 percent, down slightly from 80.7 in September. (Again, there is no estimate for October.) The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is still above what the ratio was in any month during the period from January 2008 to February 2020. The continued high levels of the prime-age employment-population ratio indicates some continuing strength in the labor market.

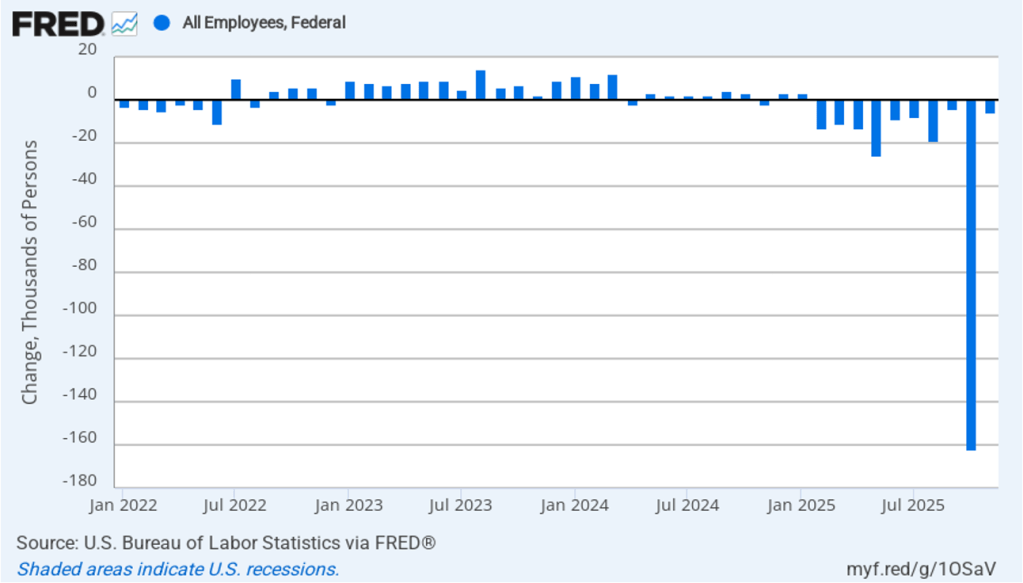

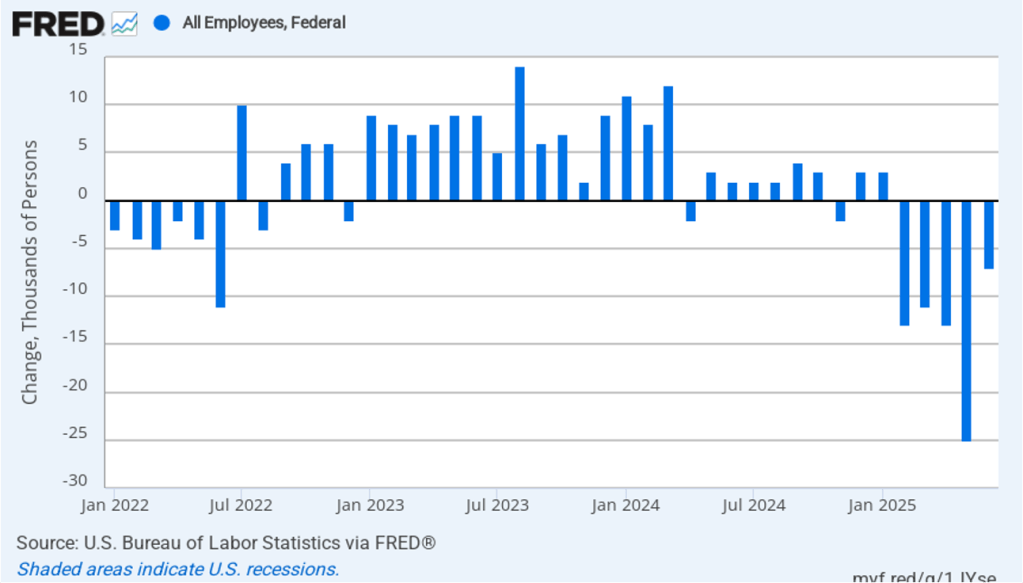

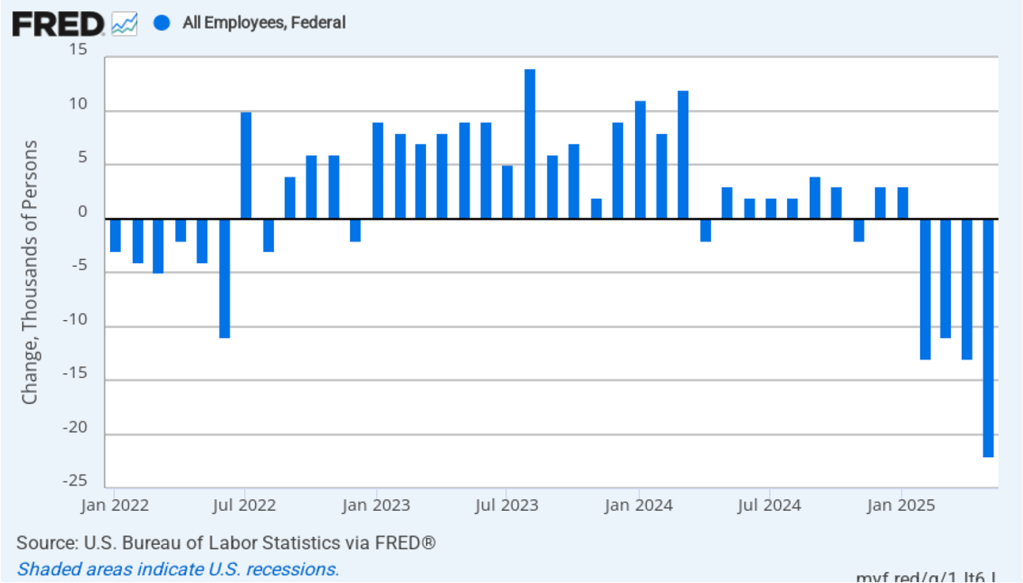

The Trump Administration’s layoffs of some federal government workers are clearly shown in the estimate of total federal employment for October, when many federal government employees exhausted their severance pay. (The BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.”) As the following figure shows, there was a decline federal government employment of 162,000 in October, with an additional decline of 6,000 In November. The total decline since the beginning of February 2025 is 271,000. At this point, we can say that the decline in federal employment has had a significant effect on the overall labor market and may account for some of the rise in the unemployment rate.

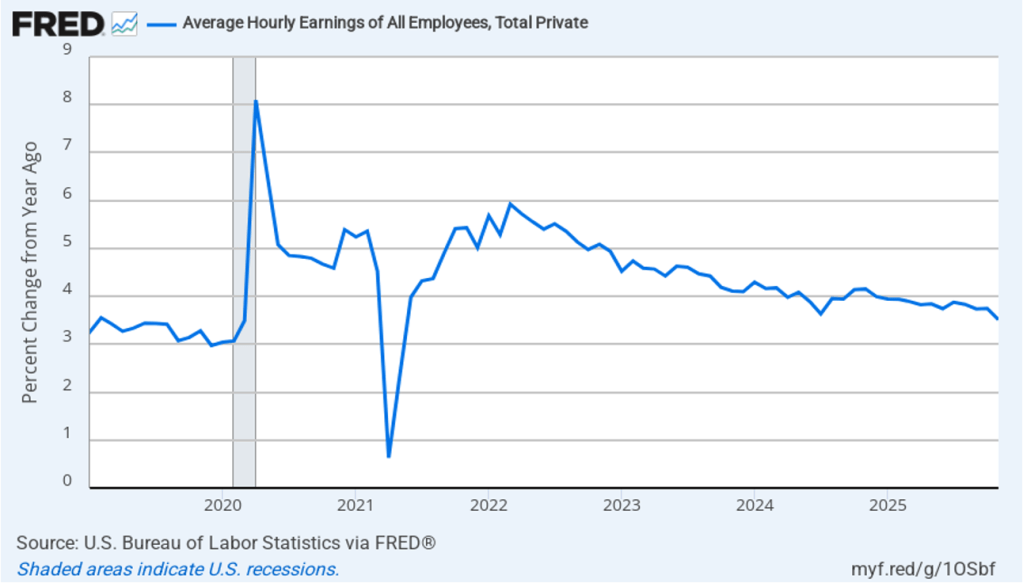

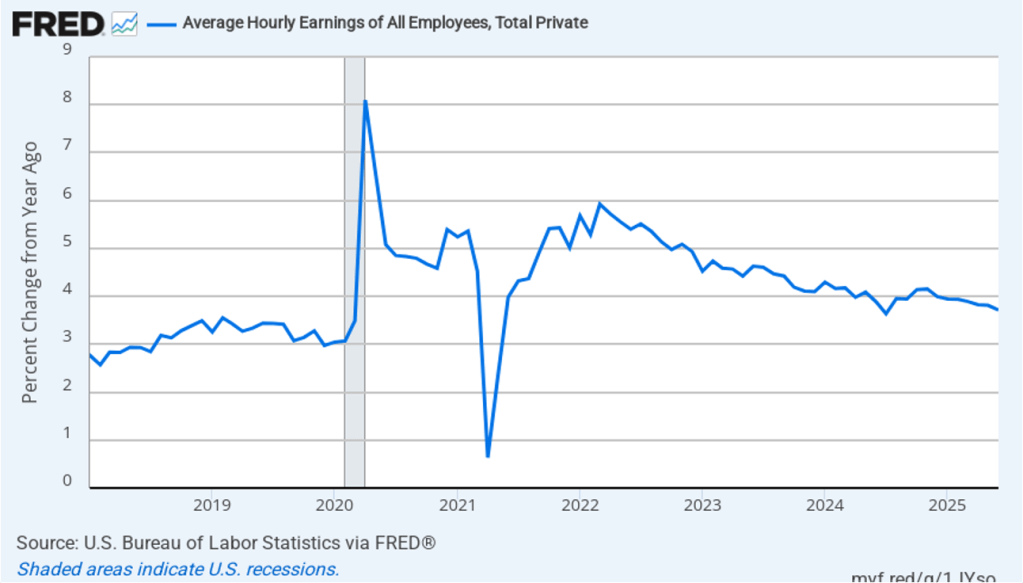

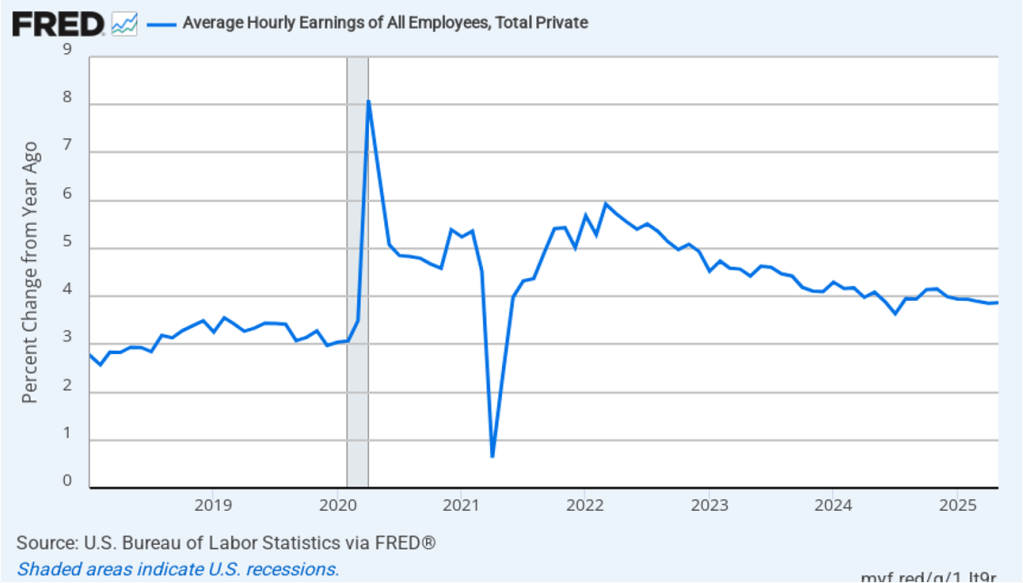

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.5 percent in November, down from 3.7 percent in October.

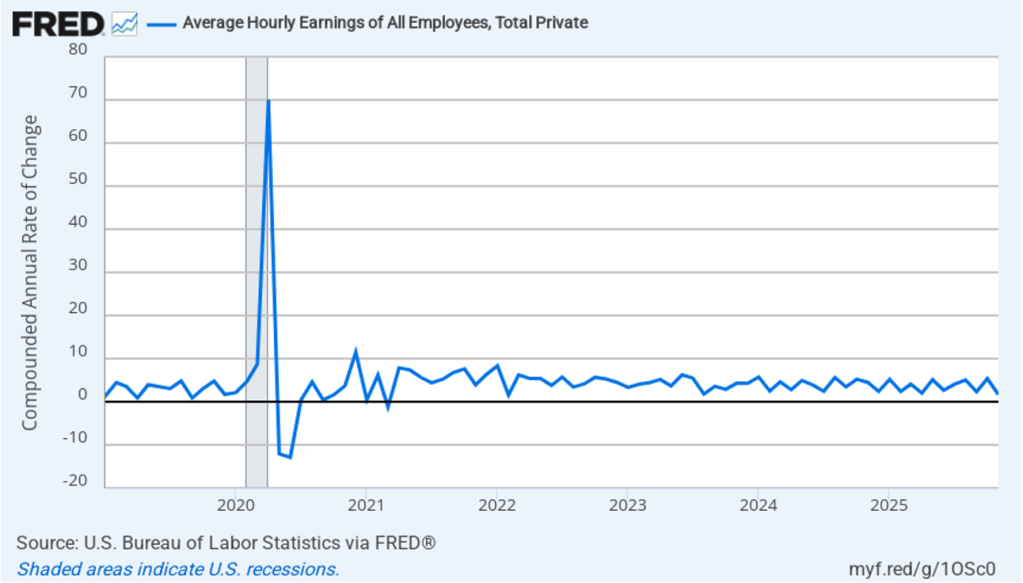

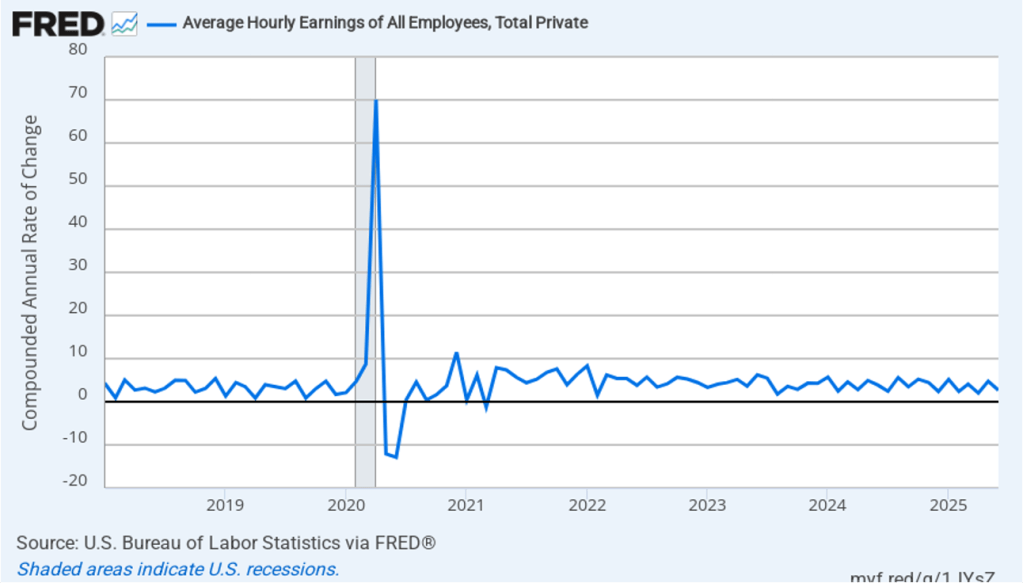

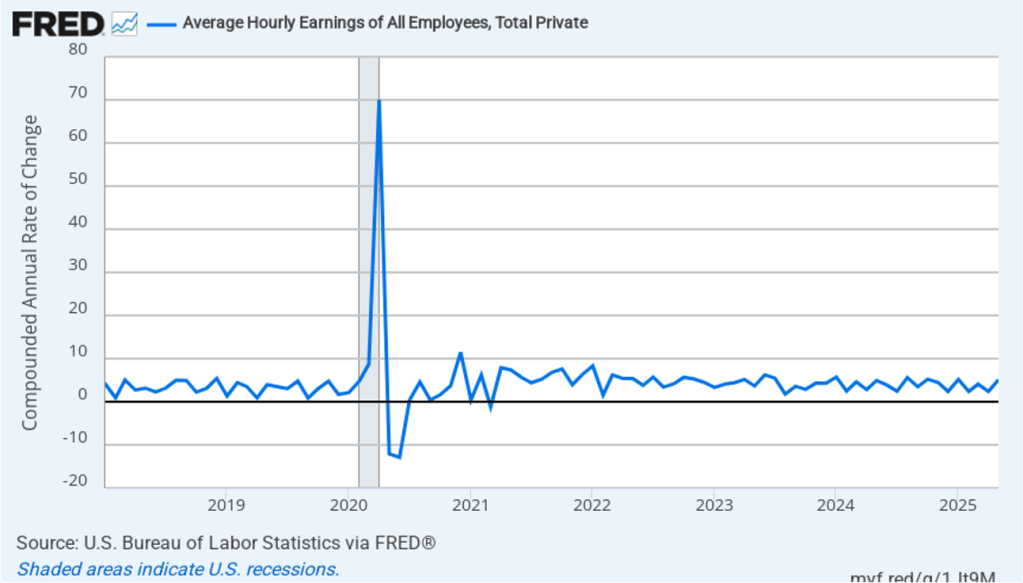

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In November, the 1-month rate of wage inflation was 1.6 percent, down from 5.4 percent in October. This slowdown in wage growth may be an indication of a weakening labor market. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

What effect might today’s jobs report have on the decisions of the Federal Open Market Committee (FOMC) with respect to setting its target range for the federal funds rate? Today’s jobs report provides a mixed take on the state of the labor market with very slow job growth—although the large decline in federal employment is a confounding factor—a continued high employment-population ratio for prime age workers, and slowing wage growth.

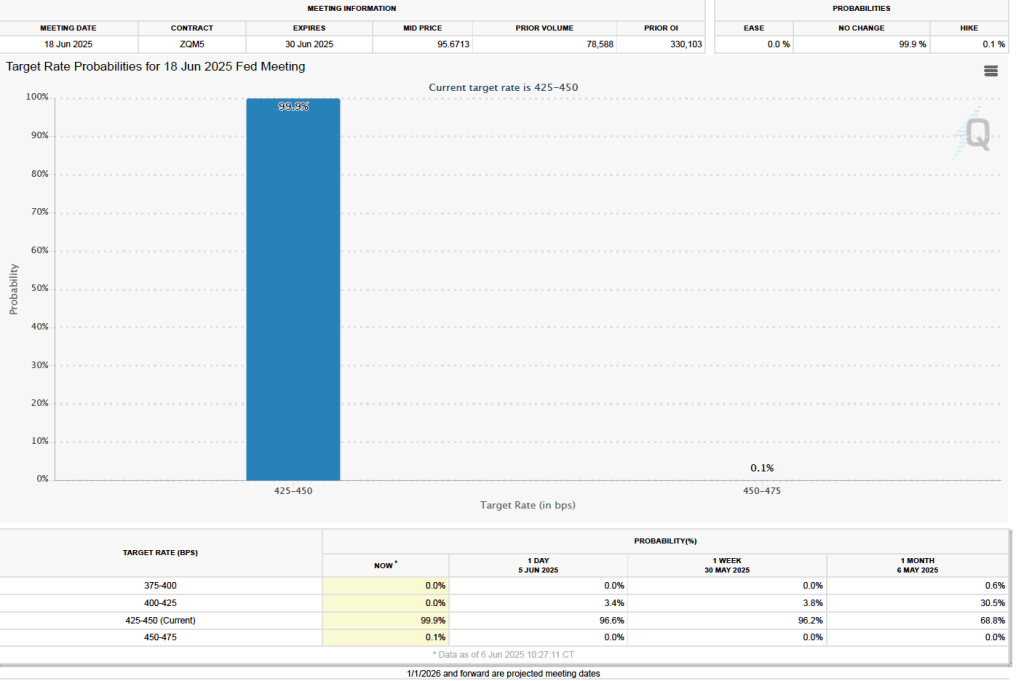

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) This morning, investors assigned a 75.6 percent probability to the committee leaving its target range unchanged at 3.50 percent to 3.75 percent at its next meeting on January 27–28. That probability is unchanged from the probability yesterday before the release of the jobs report. Investors apparently don’t see today’s report as providing much new information on the current state of the economy.

This opinion column originally ran at Project Syndicate.

While recent media coverage of the US Federal Reserve has tended to focus on when, and by how much, interest rates will be cut, larger issues loom. The selection of a new Fed chair to succeed Jerome Powell, whose term ends next May, should focus not on short-term market considerations, but on policies and processes that could improve the Fed’s overall performance and accountability.

By demanding that the Fed cut the federal funds rate sharply to boost economic activity and lower the government’s borrowing costs, US President Donald Trump risks pushing the central bank toward an overly inflationary monetary policy. And that, in turn, risks increasing the term premium in the ten-year Treasury yield—the very financial indicator that Treasury Secretary Scott Bessent has emphasized. A higher premium would raise, not lower, borrowing costs for the federal government, households, and businesses alike. Moreover, concerns about the Fed’s independence in setting monetary policy could undermine confidence in US financial markets and further weaken the dollar’s exchange rate.

But this does not imply that Trump should simply seek continuity at the Fed. The Fed, under Powell, has indeed made mistakes, leading to higher inflation, sometimes inept and uncoordinated communications, and an unclear strategy for monetary policy.

I do not share the opinion of Trump and his advisers that the Fed has acted from political or partisan motives. Even when I have disagreed with Fed officials or Powell on matters of policy, I have not doubted their integrity. However, given their mistakes, I do believe that some institutional introspection is warranted. The next chair—along with the Board of Governors and the Federal Open Market Committee—will have many policy questions to address beyond the near-term path for the federal funds rate.

Three issues are particularly important. The first is the Fed’s dual mandate: to ensure stable prices and maximum employment. Many economists (including me) have been critical of the Fed for exhibiting an inflationary bias in 2021 and 2022. The highest inflation rate in 40 years raised pressing questions about whether the Fed has assigned the right weights to inflation and employment.

Clearly, the strategy of pursuing a flexible average inflation target (implying that inflation can be permitted to rise above 2% if it had previously been below 2%) has not been successful. What new approach should the Fed adopt to hit its inflation target? And how can the Fed be held more accountable to Congress and the public? Should it issue a regular inflation report?

The second issue concerns the size and composition of the Fed’s balance sheet. Since the global financial crisis of 2008, the Fed has had a much larger balance sheet and has evolved toward an “ample reserves model” (implying a perpetually high level of reserves). But how large must the balance sheet be to conduct monetary policy, and how important should long-term Treasury debt and mortgage-backed securities be, relative to the rest of the balance sheet? If such assets are to play a central role, how can the Fed best separate the conduct of monetary policy from that of fiscal policy?

The third issue is financial regulation. What regulatory changes does the Fed believe are needed to avoid the kind of costly stresses in the Treasury market we have witnessed in recent years? How can bank supervision be improved? Given that regulation is an inherently political subject, how can the Fed best separate these activities from its monetary policymaking (where independence is critical)?

Addressing these policy questions requires a rethink of process, too. The Fed would be more effective in dealing with a changing economic environment if it acknowledged and debated more diverse viewpoints about the roles of monetary policy and financial regulation in how the economy works.

The Fed’s inflation mistakes, overconfidence in financial regulation, and other errors partly reflect the “groupthink” to which all organizations are prone. Regional Fed presidents’ views traditionally have reflected their own backgrounds and local conditions, but that doesn’t translate easily into a diversity of economic views. Instead of choosing Fed officials based on how they are likely to vote at the next rate-setting meeting, Trump should put more weight on intellectual and experiential diversity. Equally, the Fed itself could more actively seek and listen to dissenting views from academic and business leaders.

Raising questions about policy and process offers guidance about the characteristics that the next Fed chair will need to succeed. These obviously include knowledge of monetary policy and financial regulation and mature, independent judgment; but they also include diverse leadership experience and an openness to new ideas and perspectives that might enhance the institution’s performance and accountability. One hopes that Trump’s selection of the next Fed chair, and the Senate’s confirmation process, will emphasize these attributes.

This morning (July 3), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for June. The data in the report show that the labor market was stronger than expected in June. There have been many stories in the media about businesspeople becoming pessimistic as a result of the large tariff increases the Trump Administration announced on April 2—some of which have since been reduced—and some large firms—including Microsoft and Walt Disney—have announced layoffs. In addition, yesterday payroll processing firm ADP estimated that private sector employment had declined by 33,000 in June. But despite these signs of weakness in the labor market, as the headline in the Wall Street Journal put it “Hiring Defied Expectations in June.”

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

According to the establishment survey, there was a net increase of 147,000 nonfarm jobs during June. This increase was above the increase of 1115,000 that economists surveyed had forecast. In addition, the BLS revised upward its previous estimates of employment in April and May by a combined 16,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years.

The unemployment rate declined from 4.2 in May to 4.1 percent in June. Economists surveyed had forecast an increase in the unemployment rate to 4.3 percent. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In June, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.5 percent. The unemployment rate would have to rise significantly in the second half of the year for that forecast to be accurate.

Each month, the Federal Reserve Bank of Atlanta estimates how many net new jobs are required to keep the unemployment rate stable. Given a slowing in the growth of the working-age population due the aging of the U.S. population and a sharp decline in immigration, the Atlanta Fed currently estimates that the economy would have to create 113,500 net new jobs each month to keep the unemployment rate stable at 4.1 percent.

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 93,000 jobs in June, following a decrease of 696,000 jobs in May. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, the two surveys were consistent in both showing a net increase in employment. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

The household survey has another important labor market indicator. The employment-population ratio forprime age workers—those aged 25 to 54—rose from 80.5 percent in May to 80.7 percent in June. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to January 2020.

It is still unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 7,000 in June and a total decline of 69,000 since the beginning of February. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.7 percent in June, down from an increase of 3.8 percent in May.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In June, the 1-month rate of wage inflation was 2.7 percent, down significantly from 4.8 percent in May. If the 1-month increase in AHE is sustained, it would indicate that the Fed may have an easier time achieving its 2 percent target rate of price inflation. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

Before today’s jobs reports the signs that the labor market was weakening, which we discussed earlier, had led some economists and policymakers to speculate that a weak jobs report would lead the FOMC to cut its target range for the federal funds rate at its next meeting on July 29–30. That now seems very unlikely.

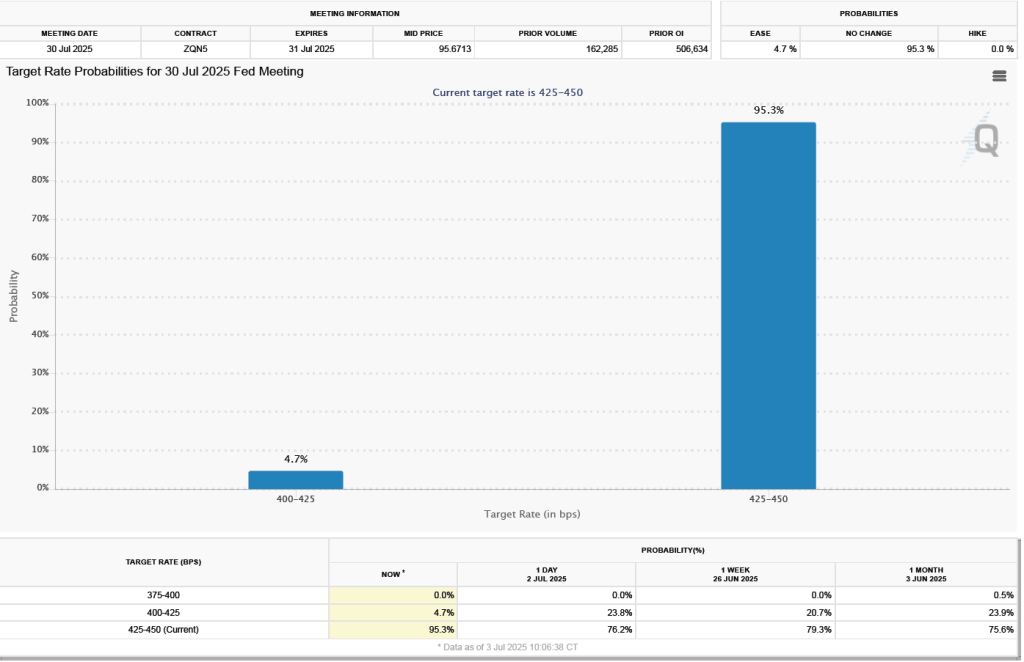

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today investors assign a 95.3 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at the July meeting.

This morning (June 6), the Bureau of Labor Statistics (BLS) released its “Employment Situation” report (often called the “jobs report”) for May. The data in the report show that the labor market continues to be strong. There have been many stories in the media about businesspeople becoming pessimistic as a result of the large tariff increases the Trump Administration announced on April 2—some of which have since been reduced—but we don’t see the effects in the employment data. Some firms may be maintaining employment until they receive greater clarity about where tariff rates will end up. Similarly, although there are some indications that consumer spending may be slowing, to this point, the effects are not evident in the labor market.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

According to the establishment survey, there was a net increase of 139,000 nonfarm jobs during May. This increase was above the increase of 125,000 that economists surveyed had forecast. Somewhat offsetting this increase, the BLS revised downward its previous estimates of employment in March and April by a combined 95,000 jobs. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”) The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years.

The unemployment rate was unchanged to 4.2 percent in May. As the following figure shows, the unemployment rate has been remarkably stable over the past year, staying between 4.0 percent and 4.2 percent in each month since May 2024. In March, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate for 2025 would average 4.4 percent.

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net decrease of 696,000 jobs in May, following an increase of 461,000 jobs in April. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent with employment increasing in one survey while falling in the other. This month, the discrepancy between the two surveys in their estimates of the change in net jobs was particularly large. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

The household survey has another important labor market indicator. The employment-population ratio for prime age workers—those aged 25 to 54—declined from 80.7 percent in April to 80.5 percent in May. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is above what the ratio was in any month during the period from January 2008 to December 2019.

It remains unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in total federal government employment of 22,000 in May and a total decline of 59,000 beginning in February. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has been too small to have a significant effect on the overall labor market.

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.9 percent in May. Movements in AHE have been remarkably stable, showing increases of 3.9 percent each month since January.

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In May, the 1-month rate of wage inflation was 5.1 percent, up sharply from 2.4 percent in April. If the 1-month increase in AHE is sustained, it would indicate that the Fed will struggle to achieve its 2 percent target rate of price inflation. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

Today’s jobs report leaves the situation facing the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) largely unchanged. Looming over monetary policy, however, is the expected effect of the Trump Administration’s tariff increases. As we note in this blog post, a large unexpected increase in tariffs results in an aggregate supply shock to the economy. In terms of the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23), an unexpected increase in tariffs shifts the short-run aggregate supply curve (SRAS) to the left, increasing the price level and reducing the level of real GDP.

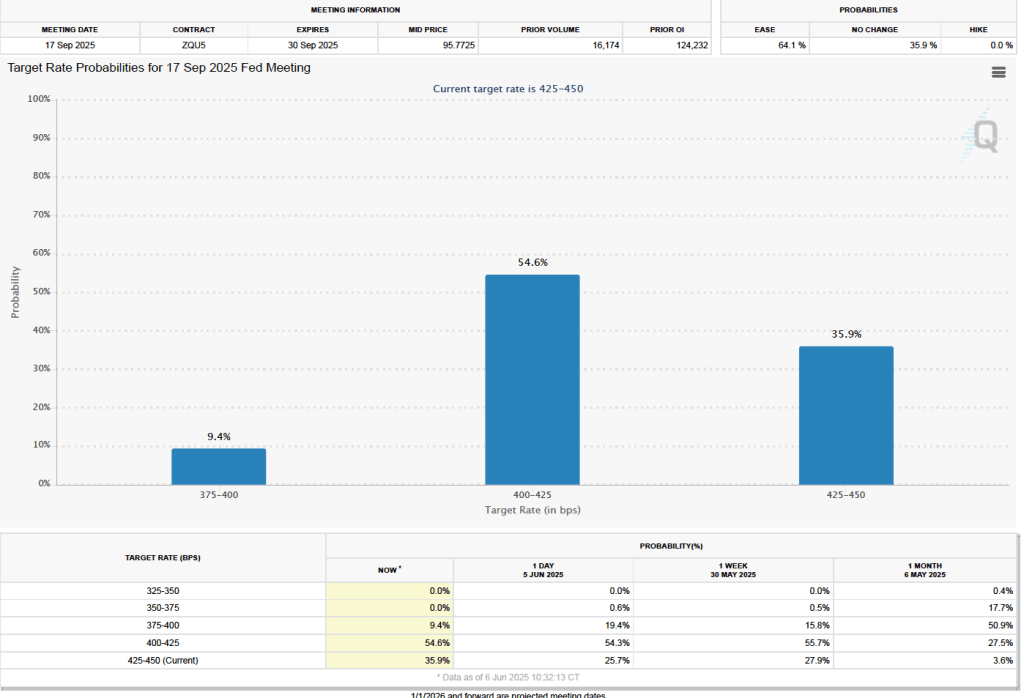

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) The data from the futures market indicate that, despite the potential effects of the tariff increases, investors don’t expect that the FOMC will cut its target for the federal funds rate at its June 17–18 meeting. As shown in the following figure, investors assign a 99.9 percent probability to the committee keeping its target unchanged at 4.25 percent to 4.50 percent at that meeting.

As the following figure shows, investors don’t expect the FOMC to cut its federal funds rate target until the committee’s September 16-17 meeting. Investors assign a probability of 54.6 percent that at that meeting the committee will cut its target range by 0.25 percentage point (25 basis points) to 4.00 percent to 4.25 percent. And a probability of 9.4 percent that the committee will cut its target rate by 50 baisis points to 3.75 percent to 4.00 percent. At 35.9 percent, investors assign a fairly high probability to the committee keeping its target range constant at that meeting.

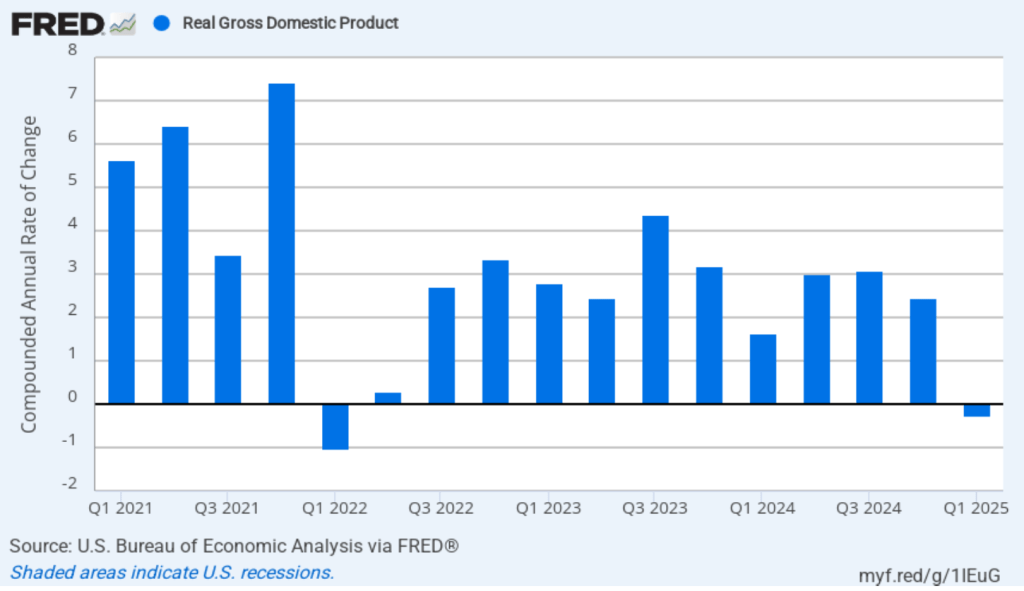

This morning (April 30), the Bureau of Economic Analysis (BEA) released its advance estimate of GDP for the first quarter of 2025. (The report can be found here.) The BEA estimates that real GDP fell by 0.3 percent, measured at an annual rate, in the first quarter—January through March. Economists surveyed had expected an 0.8 percent increase. Real GDP grew by an estimated 2.5 percent in the fourth quarter of 2024. The following figure shows the estimated rates of GDP growth in each quarter beginning in 2021.

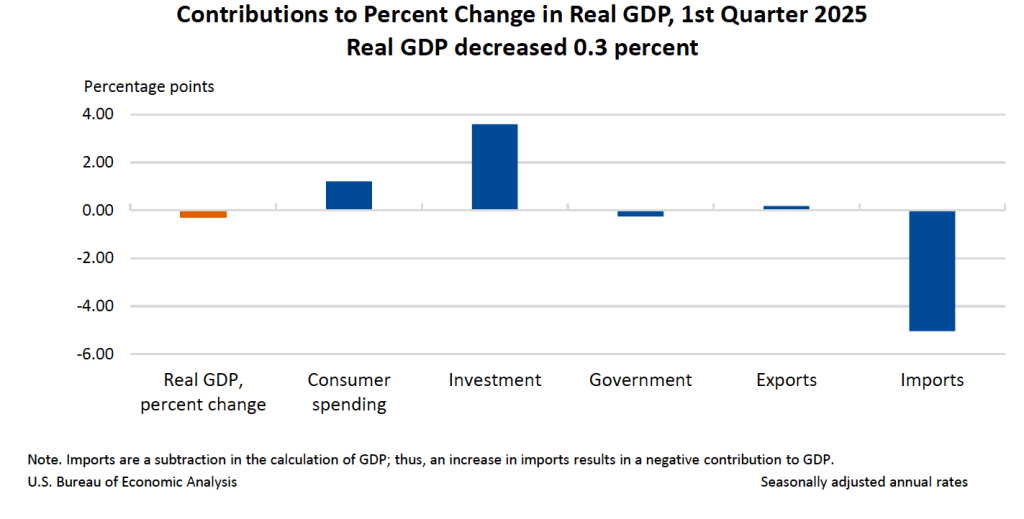

As the following figure—taken from the BEA report—shows, the increase in imports was the most important factor contributing to the decline in real GDP. The quarter ended before the Trump Administration announced large tariff increases on April 2, but the increase in imports is likely attributable to firms attempting to beat the tariff increases they expected were coming.

It’s notable that the change in real private inventories was a large $140 billion, which contributed 2.3 percentage points to the change in real GDP. Again, it’s likely that the large increase in inventories represented firms stockpiling goods in anticipation of the tariff increases.

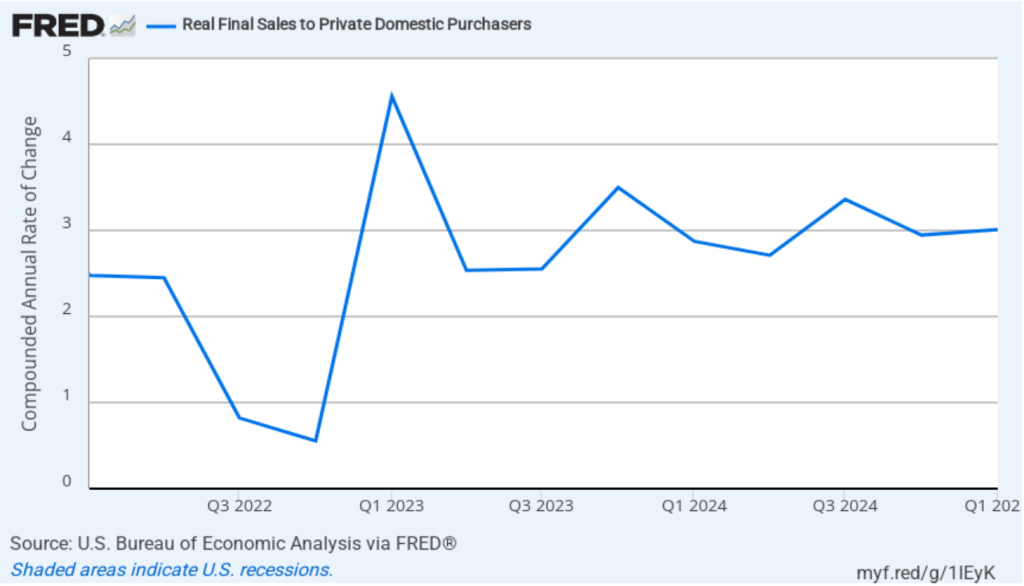

One way to strip out the effects of imports, inventory investment, and government purchases—which can also be volatile—is to look at real final sales to domestic purchasers, which includes only spending by U.S. households and firms on domestic production. As the following figure shows, real final sales to domestic purchasers increase by 3.0 percent in the first quarter of 2024, which was a slight increase from the 2.9 percent increase in the fourth quarter of 2024. The large difference between the change in real GDP and the change in real final sales to domestic purchasers is an indication of how strongly this quarter’s national income data were affected by businesses anticipating the tariff increases.

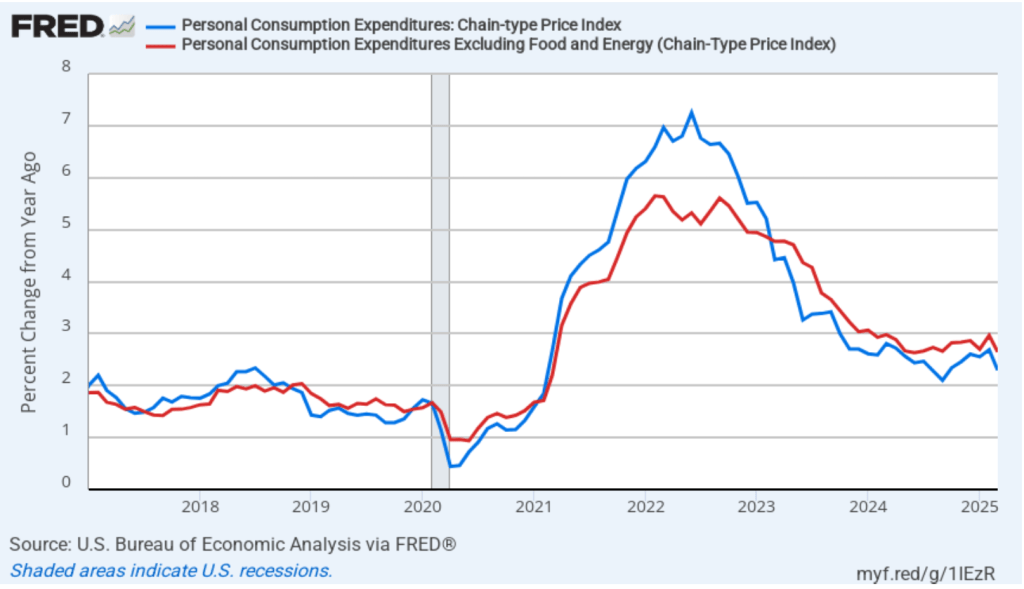

In the separate “Personal Income and Outlays” report that the BEA also released this morning, the bureau reported monthly data on the personal consumption expenditures (PCE) price index. The Fed relies on annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target. The following figure shows PCE inflation (the blue line) and core PCE inflation (the red line)—which excludes energy and food prices—for the period since January 2017 with inflation measured as the percentage change in the PCE from the same month in the previous year. In March, PCE inflation was 2.3 percent, down from 2.7 percent in February. Core PCE inflation in March was 2.6 percent, down from 3.0 percent in February. Both headline and core PCE inflation were higher than the forecasts of economists surveyed.

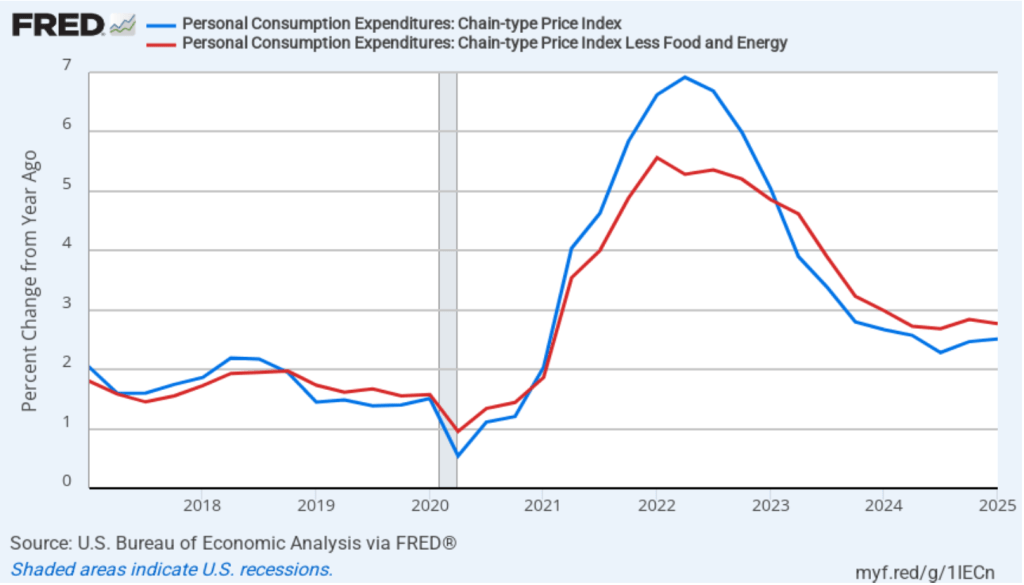

The BEA also released quarterly PCE data as part of its GDP report. The following figure shows quarterly headline PCE inflation (the blue line) and core PCE inflation (the red line). Inflation is calculated as the percentage change from the same quarter in the previous year. Headline PCE inflation in the first quarter was 2.5 percent, unchanged from the fourth quarter of 2025. Core PCE inflation was 2.8 percent, also unchanged from the fourth quarter of 2025. Both measures were still above the Fed’s 2 percent inflation target.

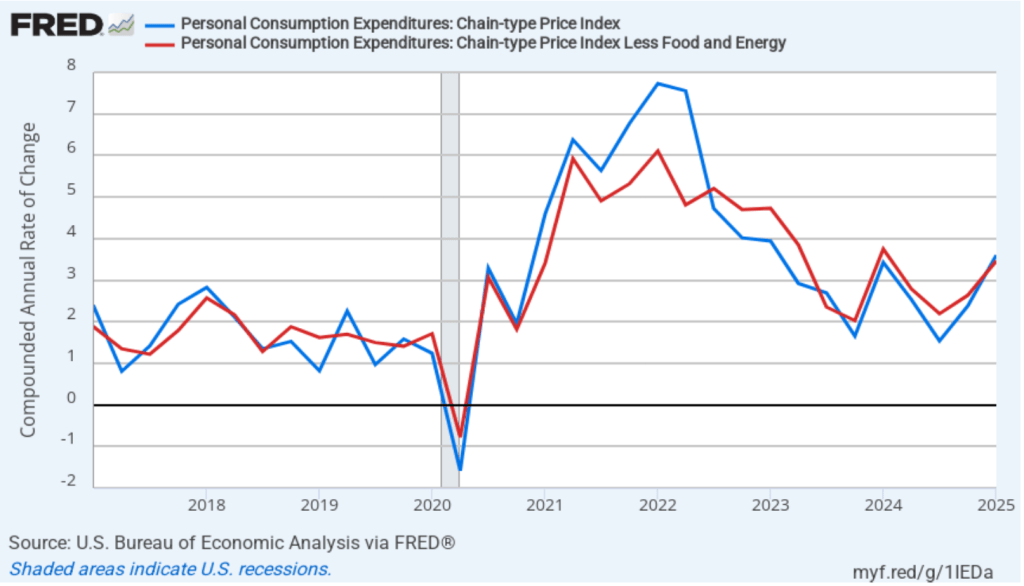

The following figure shows quarterly PCE inflation and quarterly core PCE inflation calculated by compounding the current quarter’s rate over an entire year. Measured this way, headline PCE inflation increased from 2.4 percent in the fourth quarter of 2024 to 3.6 percent in the first quarter of 2025. Core PCE inflation increased from 2.6 percent in the fourth quarter of 2024 to 3.5 percent in the first quarter of 2025. Clearly, the quarterly data show significantly higher inflation than do the monthly data. As we discuss in this blog post, tariff increases result in an aggregate supply shock to the economy. As a result, unless the current and scheduled tariff increases are reversed, we will likely see a significant increase in inflation in the coming months. So, neither the monthly nor the quarterly PCE data may be giving a good indication of the course of future inflation.

What should we make of today’s macro data releases? First, it’s important to remember that these data will be subject to revisions in coming months. If we are heading into a recession, the revisions may well be very large. Second, we are sailing into unknown waters because the U.S. economy hasn’t experienced tariff increases as large as these since passage of the Smoot-Hawley Tariff in 1930. Third, at this point we don’t know whether some, most, all, or none of the tariff increases will be reversed as a result of negotiations during the coming weeks. Finally, on Friday, the Bureau of Labor Statistics will release its “Employment Situation Report” for March. That report will provide some additional insight into the state of the economy—as least as it was in March before the full effects of the tariffs have been felt.

A tariff is a tax a government imposes on imports. Since the end of World War II, high-income countries have only occasionally used tariffs as an important policy tool. The following figure shows how the average U.S. tariff rate, expressed as a percentage of the value of total imports, has changed in the years since 1790. The ups and downs in tariff rates reflect in part political disa-greements in Congress. Generally speaking, through the early twentieth century, members of Congress who represented areas in the Midwest and Northeast that were home to many manufacturing firms favored high tariffs to protect those industries from foreign competition. Members of Congress from rural areas opposed tariffs, because farmers were primarily exporters who feared that foreign governments would respond to U.S. tariffs by imposing tariffs on U.S. agricultural exports. From the pre-Civil War period until after World War II the Republicans Party generally favored high tariffs and the Democratic Party generally favored low tariffs, reflecting the economic interests of the areas the parties represented in Congress. (Note: Because the tariffs that the Trump Administration will end up imposing are still in flux, the value for 2025 in the figure is only a rough estimate.)

By the end of World War II in 1945, government officials in the United States and Europe were looking for a way to reduce tariffs and revive international trade. To help achieve this goal, they set up the General Agreement on Tariffs and Trade (GATT) in 1948. Countries that joined the GATT agreed not to impose new tariffs or import quotas. In addition, a series of multilateral negotiations, called trade rounds, took place, in which countries agreed to reduce tariffs from the very high levels of the 1930s. The GATT primarily covered trade in goods. A new agreement to cover services and intellectual property, as well as goods, was eventually negotiated, and in January 1995, the GATT was replaced by the World Trade Organization (WTO). In 2025, 166 countries are members of the WTO.

As a result of U.S. participation in the GATT and WTO, the average U.S. tariff rate declined from nearly 20% in the early 1930s to 1.8% in 2018. The first Trump Administration increased tariffs beginning in 2018, raising the average tariff rate to 2.5%. (The Biden Administration continued most of the increases.) In 2025, the second Trump Administration’s substantial increases in tariffs raised the average tariff rate to the highest level since the 1940s.

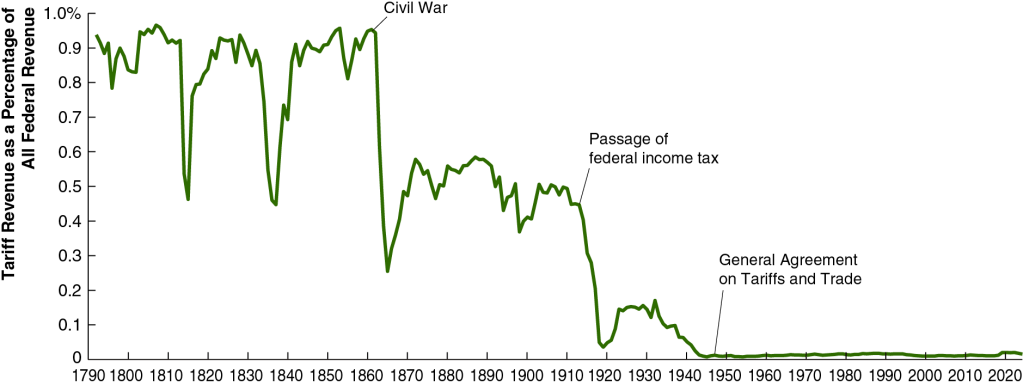

Until the enactment in 1913 of the 16th Amendment to the U.S. Constitution, which allowed for a federal income tax, tariffs were an important source of revenue to the federal government. As the following figure shows, in the early years of the United States, more than 90% of federal government revenues came from the tariff. As tariff rates declined and federal income and payroll taxes increased, tariffs declined to only 2% of federal government revenue. It’s unclear yet how much tariff’s share of federal government revenue will rise as a result of the Trump Administration’s tariff increases.

The effect of tariff increases on the U.S. economy are complex and depend on the details of which tariffs are increased, by how much they are increased, and whether foreign governments raise their tariffs on U.S. exports in response to U.S. tariff increases. We can analyze some of the effects of tariffs using the basic aggregate demand and aggregate supply model that we discuss in Macroeconomics, Chapter 13 (Economics, Chapter 23). We need to keep in mind in the following discussion that small increases in tariffs rates—such as those enacted in 2018—will likely have only small effects on the economy given that net exports are only about 3% or U.S. GDP.

An increase in tariffs intended to protect domestic industries can cause the aggregate demand curve to shift to the right if consumers switch spending from imports to domestically produced goods, thereby increasing net exports. But this effect can be partially or wholly offset if trading partners retaliate by increasing tariffs on U.S. exports. When Congress passed the Smoot-Hawley Tariff in 1930, which raised tariff rates to historically high levels, retaliation by U.S. trading partners contributed to a sharp decline in U.S. exports during the early 1930s.

International trade can increase a country’s production and income by allowing a country to specialize in the goods and services in which it has a comparative advantage. Tariffs shift a country’s allocation of labor, capital, and other resources away from producing the goods and services it can produce most efficiently and toward producing goods and services that other countries can produce more efficiently. The result of this misallocation of resources is to reduce the productive capacity of the country, shifting the long-run aggregate supply curve (LRAS) to the left.

Tariffs raise the prices of U.S. imports. This effect can be partially offset because tariffs increase the demand for U.S. dollars relative to trading partners’ currencies, increasing the dollar exchange rate. Because a tariff effectively acts as a tax on imports, like other taxes its incidence—the division of the burden of the tax between sellers and buyers—depends partly on the price elasticity of demand and the price elasticity of supply, which vary across the goods and services on which tariffs are imposed. (We discuss the effects of demand and supply elasticity on the incidence of a tax in Microeconomics, Chapter 17, Section 17.3.)

About two-thirds of U.S. imports are raw materials, intermediate goods, or capital goods, all of which are used as inputs by U.S. firms. For example, many cars assembled in the United States contain imported parts. The popular Ford F-Series pickup trucks are assembled in the United States, but more than two-thirds of the parts are imported from other countries. That fact indicates that the automobile industry is one of many U.S. industries that depend on global supply chains that can be disrupted by tariffs. Because tariffs on imported raw materials, parts and other intermediate goods, and capital goods increase the production costs of U.S. firms, tariffs reduce the quantity of goods these firms will produce at any given price. In terms of the aggregate demand and aggregate supply model , a large unexpected increase in tariffs results in an aggregate supply shock to the economy, shifting the short-run aggregate supply curve (SRAS) to the left.

Our thanks to Fernando Quijano for preparing the two figures.

Welcome to the first podcast for the Spring 2025 semester from the Hubbard/O’Brien Economics author team. Check back for Blog updates & future podcasts which will happen every few weeks throughout the semester.

Join authors Glenn Hubbard & Tony O’Brien as they offer thoughts on tariffs in advance of the beginning of the new administration. They discuss the positive and negative impacts of tariffs -and some of the intended consequences. They also look at the AI landscape and how its reshaping the US economy. Is AI responsible for recent increased productivity – or maybe just the impact of other factors. It should be looked at closely as AI becomes more ingrained in our economy.

A column in the New York Times made the following observations:

“The greenback has been climbing since Trump’s victory, a potential drag on multinationals’ profits. Elsewhere, the yield on the closely watched 10-year Treasury note ticked higher again on Tuesday ….”

What is a “greenback”? What does it mean to say that the greenback has been “climbing”? Climbing relative to what?

Is there a connection between the interest rate on the 10-year U.S. Treasury note increasing and the value of the greenback increasing? Briefly explain.

Why would an increase in the value of the greenback be a potential drag on the profits of U.S.-based multinationals?

Solving the Problem

Step 1: Review the chapter material. This problem is about the effect of changes in the ex-change rate, so you may want to review the section “The Foreign Exchange Market and Exchange Rates.”

Step 2: Answer part (a) by explaining what a greenback is and what it means to say that the greenback is climbing. “Greenback” is a slang term for the U.S. dollar because the back of U.S. currency is printed in green ink. The “greenback climbing” means that the U.S. dollar is increasing in value relative to other currencies—in other words, the exchange rate is increasing.

Step 3: Answer part (b) by explaining whether there is a connection between the value of the U.S. dollar increasing as the interest rate on the 10-year U.S. Treasury note is increasing. There is a connection: Higher interest rates in the United States will make investing in U.S. financial securities, such as Treasury notes, more attractive to foreign investors. Foreign investors will increase their demand for dollars, increasing the equilibrium exchange rate.

Step 3: Answer part (c) by explaining why an increase in the value of the greenback will affect the profits of U.S. multinational corporations. A U.S. multinational firm, such as Microsoft or Apple, will have operations in other countries. When, for instance, Microsoft sells access to its Office Suite to customers in France of Germany, the customers pay in euros. If the value of the dollar has risen in exchange for euros, when Microsoft converts the euros into dollars it receives fewer dollars, thereby reducing its profits.

Chicago Cubs Hall of Fame shortstop Ernie Banks was known for saying “It’s a great day for baseball. Let’s play two!” (Photo from the Baseball Hall of Fame)

First Solved Problem: Exchange Rates and Tourism

Supports: Macroeconomics, Chapter 18, Sections 18.2 and 18.6; and Economics, Chapter 28, Sections 28.2 and 28.6.

The headline of an article on nbcnews.com is: “The Fed May Soon Cut Interest Rates. That Could Make Your Next Trip Abroad More Expensive.”

Briefly explain the difference between a “strong dollar” and a “weak dollar.”

If you are going to spend two weeks on vacation in France, would you prefer that the dollar be strong or weak during that time? Briefly explain.

Briefly explain the connection between Federal Reserve monetary policy and the exchange rate between the U.S. dollar and other currencies.

Use your answers to parts a., b., and c. to explain what the headline means.

Solving the Problem

Step 1: Review the chapter material. This problem is about the effect of changes in exchange rates on import and export prices and the effect of changes in interest rates on exchange rates, so you may want to review Chapter 18, Sections 18.2 and 18.6.

Step 2: Answer part a. by explaining the difference between a “strong dollar” and a “weak dollar.” Generally, the U.S. dollar is called strong when it exchanges for more units of foreign currencies and is called weak when it exchanges for fewer units of foreign currencies. (Economists are less likely to use the phrases “strong dollar” and “weak dollar” than are members of the media.)

Step 3: Answer part b. by expalining whether you would like the U.S. dollar to be weak or strong during your vacation in France. France uses the euro as its currency. As a tourist, you will buy goods and services—such as restaurant meals and souvenirs—in euros. You would like the dollar to be strong because then you will be able to use fewer dollars to exhange for the euros you need to buy goods and services during your vacation.

Step 4: Answer part c. by explaining how Federal Reserve monetary policy affects the exchange rate. As we discuss in Section 18.6, when the Fed wants to pursue an expansionary monetary policy, the Federal Open Market Committee (FOMC) reduces its target for the federal funds rate, which typically results in other interest rates also declining. Lower interest rates make U.S. financial asses, such as Treasury bonds, less attractive relative to foreign financial assets, such as bonds issued by the French government. As a result the demand for U.S. dollars falls relative to the demand for foreign currencies, reducing the exchange rate between the dollar and other currencies. In other words, an expansionary monetary policy will result in a weaker dollar.

Step 5: Answer part d. by using your answers to parts a., b., and c. to expalin what the headline means. The headline indicates that the Fed may soon engage in an expansionary monetary policy, which will result in lower interest rates in the United States, leading to a weaker U.S. dollar. The weaker the dollar, the more dollars you will have to exchange to receive the same number of units of a foreign currency, causing you to have to spend more dollars to pay for the same goods and services during your trip. So, the Fed taking action to reduce interest rates will make your trip abroad more expensive.

Second Solved Problem: Solved Problem: Javier Milei and Argentina’s Exchange Rate Policy

Supports: Macroeconomics, Chapter 18, Sections 18.2 and 18.3; and Economics, Chapter 28, Sections 28.2 and 28.3.

Javier Milei was elected president of Argentina in December 2023. During the presidential campaign he proposed using market-based policies to address Argentina’s economic problems, particularly high rates of inflation and low rates of economic growth. One part of his program involves moving the government away from controlling the value of the peso either by allowing it to float or by making the U.S. dollar legal tender in Argentina. Initially, however, although Milei devalued the peso against the dollar, he didn’t allow the peso to float, keeping the peso pegged against the value of the dollar. An article in the Economist states that many economists believe that the peso is overvalued. The article notes that: “A pricey peso scares off tourists, makes exports expensive and deters investors.” The article also notes that allowing the peso to float “would probably push up inflation.”

Briefly explain what it means for a government to allow its currency to float.

What does it mean to say that a county’s currency is overvalued?

What does the article mean by a “pricey peso”? Why would a pricey peso scare off tourists, make exports expensive, and deter investors?

Why would allowing the peso to float probably push up inflation?

Solving the Problem

Step 1: Review the chapter material. This problem is about exchange rates and exchange rate systems, so you may want to review Chapter 18, Sections 18.2 18.3.

Step 2: Answer part a. by explaining what it means for a government to allow its currency to float. As we discuss in Section 18.3, when a government allows its currency to float it allows the exchange rate between its currency and other currencies to be determined by demand and supply in foreign exchange markets.

Step 3: Answer part b. by expalining what it means for a country’s currency to be overvalued. A currency is overvalued if a government pegs the exchange rate above the market equilibrium exchange rate.

Step 4: Answer part c. by explaining what a “pricey peso” means and why a pricey peso might scare off tourists, make exports expensive, and deter investors. In the context of this article, a pricey peso means an overvalued peso—one that is pegged above the market equilibrium exchange rate, as we noted in the answer to part b. If the peso is overvalued relative to other currencies, then tourists from those countries will find the prices of goods and services in Argentina to be high relative to the prices of those goods and services priced in their domestic currencies. We would expect that fewer foreing tourists would visit Argentina. A pricey peso would make the prices of Argentine exports higher in terms of U.S. dollars, euros, and other currencies. Those high prices will cause a decline in Argentine exports. Finally, a pricey peso will also discourage foreign investors from investing in Argentina because they will receive fewer units of their domestic currency in exchange for the pesos they earn from their investments in Argentina.

Step 5: Answer part d. by explaining why the Argentine government allowing the peso to float would likely increase inflation. The Argentine peso is overvalued, so allowing it to float will cause the value of the peso to decline relative to other currencies. As a result, the peso price of imports will increase. The prices of imported goods and services are included in the price indexes used to measure inflation, so floating the peso will likely increase the inflation rate in Argentina.