Welcome to the first podcast for the Spring 2025 semester from the Hubbard/O’Brien Economics author team. Check back for Blog updates & future podcasts which will happen every few weeks throughout the semester.

Join authors Glenn Hubbard & Tony O’Brien as they offer thoughts on tariffs in advance of the beginning of the new administration. They discuss the positive and negative impacts of tariffs -and some of the intended consequences. They also look at the AI landscape and how its reshaping the US economy. Is AI responsible for recent increased productivity – or maybe just the impact of other factors. It should be looked at closely as AI becomes more ingrained in our economy.

A column in the New York Times made the following observations:

“The greenback has been climbing since Trump’s victory, a potential drag on multinationals’ profits. Elsewhere, the yield on the closely watched 10-year Treasury note ticked higher again on Tuesday ….”

What is a “greenback”? What does it mean to say that the greenback has been “climbing”? Climbing relative to what?

Is there a connection between the interest rate on the 10-year U.S. Treasury note increasing and the value of the greenback increasing? Briefly explain.

Why would an increase in the value of the greenback be a potential drag on the profits of U.S.-based multinationals?

Solving the Problem

Step 1: Review the chapter material. This problem is about the effect of changes in the ex-change rate, so you may want to review the section “The Foreign Exchange Market and Exchange Rates.”

Step 2: Answer part (a) by explaining what a greenback is and what it means to say that the greenback is climbing. “Greenback” is a slang term for the U.S. dollar because the back of U.S. currency is printed in green ink. The “greenback climbing” means that the U.S. dollar is increasing in value relative to other currencies—in other words, the exchange rate is increasing.

Step 3: Answer part (b) by explaining whether there is a connection between the value of the U.S. dollar increasing as the interest rate on the 10-year U.S. Treasury note is increasing. There is a connection: Higher interest rates in the United States will make investing in U.S. financial securities, such as Treasury notes, more attractive to foreign investors. Foreign investors will increase their demand for dollars, increasing the equilibrium exchange rate.

Step 3: Answer part (c) by explaining why an increase in the value of the greenback will affect the profits of U.S. multinational corporations. A U.S. multinational firm, such as Microsoft or Apple, will have operations in other countries. When, for instance, Microsoft sells access to its Office Suite to customers in France of Germany, the customers pay in euros. If the value of the dollar has risen in exchange for euros, when Microsoft converts the euros into dollars it receives fewer dollars, thereby reducing its profits.

Chicago Cubs Hall of Fame shortstop Ernie Banks was known for saying “It’s a great day for baseball. Let’s play two!” (Photo from the Baseball Hall of Fame)

First Solved Problem: Exchange Rates and Tourism

Supports: Macroeconomics, Chapter 18, Sections 18.2 and 18.6; and Economics, Chapter 28, Sections 28.2 and 28.6.

The headline of an article on nbcnews.com is: “The Fed May Soon Cut Interest Rates. That Could Make Your Next Trip Abroad More Expensive.”

Briefly explain the difference between a “strong dollar” and a “weak dollar.”

If you are going to spend two weeks on vacation in France, would you prefer that the dollar be strong or weak during that time? Briefly explain.

Briefly explain the connection between Federal Reserve monetary policy and the exchange rate between the U.S. dollar and other currencies.

Use your answers to parts a., b., and c. to explain what the headline means.

Solving the Problem

Step 1: Review the chapter material. This problem is about the effect of changes in exchange rates on import and export prices and the effect of changes in interest rates on exchange rates, so you may want to review Chapter 18, Sections 18.2 and 18.6.

Step 2: Answer part a. by explaining the difference between a “strong dollar” and a “weak dollar.” Generally, the U.S. dollar is called strong when it exchanges for more units of foreign currencies and is called weak when it exchanges for fewer units of foreign currencies. (Economists are less likely to use the phrases “strong dollar” and “weak dollar” than are members of the media.)

Step 3: Answer part b. by expalining whether you would like the U.S. dollar to be weak or strong during your vacation in France. France uses the euro as its currency. As a tourist, you will buy goods and services—such as restaurant meals and souvenirs—in euros. You would like the dollar to be strong because then you will be able to use fewer dollars to exhange for the euros you need to buy goods and services during your vacation.

Step 4: Answer part c. by explaining how Federal Reserve monetary policy affects the exchange rate. As we discuss in Section 18.6, when the Fed wants to pursue an expansionary monetary policy, the Federal Open Market Committee (FOMC) reduces its target for the federal funds rate, which typically results in other interest rates also declining. Lower interest rates make U.S. financial asses, such as Treasury bonds, less attractive relative to foreign financial assets, such as bonds issued by the French government. As a result the demand for U.S. dollars falls relative to the demand for foreign currencies, reducing the exchange rate between the dollar and other currencies. In other words, an expansionary monetary policy will result in a weaker dollar.

Step 5: Answer part d. by using your answers to parts a., b., and c. to expalin what the headline means. The headline indicates that the Fed may soon engage in an expansionary monetary policy, which will result in lower interest rates in the United States, leading to a weaker U.S. dollar. The weaker the dollar, the more dollars you will have to exchange to receive the same number of units of a foreign currency, causing you to have to spend more dollars to pay for the same goods and services during your trip. So, the Fed taking action to reduce interest rates will make your trip abroad more expensive.

Second Solved Problem: Solved Problem: Javier Milei and Argentina’s Exchange Rate Policy

Supports: Macroeconomics, Chapter 18, Sections 18.2 and 18.3; and Economics, Chapter 28, Sections 28.2 and 28.3.

Javier Milei was elected president of Argentina in December 2023. During the presidential campaign he proposed using market-based policies to address Argentina’s economic problems, particularly high rates of inflation and low rates of economic growth. One part of his program involves moving the government away from controlling the value of the peso either by allowing it to float or by making the U.S. dollar legal tender in Argentina. Initially, however, although Milei devalued the peso against the dollar, he didn’t allow the peso to float, keeping the peso pegged against the value of the dollar. An article in the Economist states that many economists believe that the peso is overvalued. The article notes that: “A pricey peso scares off tourists, makes exports expensive and deters investors.” The article also notes that allowing the peso to float “would probably push up inflation.”

Briefly explain what it means for a government to allow its currency to float.

What does it mean to say that a county’s currency is overvalued?

What does the article mean by a “pricey peso”? Why would a pricey peso scare off tourists, make exports expensive, and deter investors?

Why would allowing the peso to float probably push up inflation?

Solving the Problem

Step 1: Review the chapter material. This problem is about exchange rates and exchange rate systems, so you may want to review Chapter 18, Sections 18.2 18.3.

Step 2: Answer part a. by explaining what it means for a government to allow its currency to float. As we discuss in Section 18.3, when a government allows its currency to float it allows the exchange rate between its currency and other currencies to be determined by demand and supply in foreign exchange markets.

Step 3: Answer part b. by expalining what it means for a country’s currency to be overvalued. A currency is overvalued if a government pegs the exchange rate above the market equilibrium exchange rate.

Step 4: Answer part c. by explaining what a “pricey peso” means and why a pricey peso might scare off tourists, make exports expensive, and deter investors. In the context of this article, a pricey peso means an overvalued peso—one that is pegged above the market equilibrium exchange rate, as we noted in the answer to part b. If the peso is overvalued relative to other currencies, then tourists from those countries will find the prices of goods and services in Argentina to be high relative to the prices of those goods and services priced in their domestic currencies. We would expect that fewer foreing tourists would visit Argentina. A pricey peso would make the prices of Argentine exports higher in terms of U.S. dollars, euros, and other currencies. Those high prices will cause a decline in Argentine exports. Finally, a pricey peso will also discourage foreign investors from investing in Argentina because they will receive fewer units of their domestic currency in exchange for the pesos they earn from their investments in Argentina.

Step 5: Answer part d. by explaining why the Argentine government allowing the peso to float would likely increase inflation. The Argentine peso is overvalued, so allowing it to float will cause the value of the peso to decline relative to other currencies. As a result, the peso price of imports will increase. The prices of imported goods and services are included in the price indexes used to measure inflation, so floating the peso will likely increase the inflation rate in Argentina.

Supports:Macroeconomics, Chapter 18, Economics, Chapter 28, and Essentials of Economics, Chapter 19.

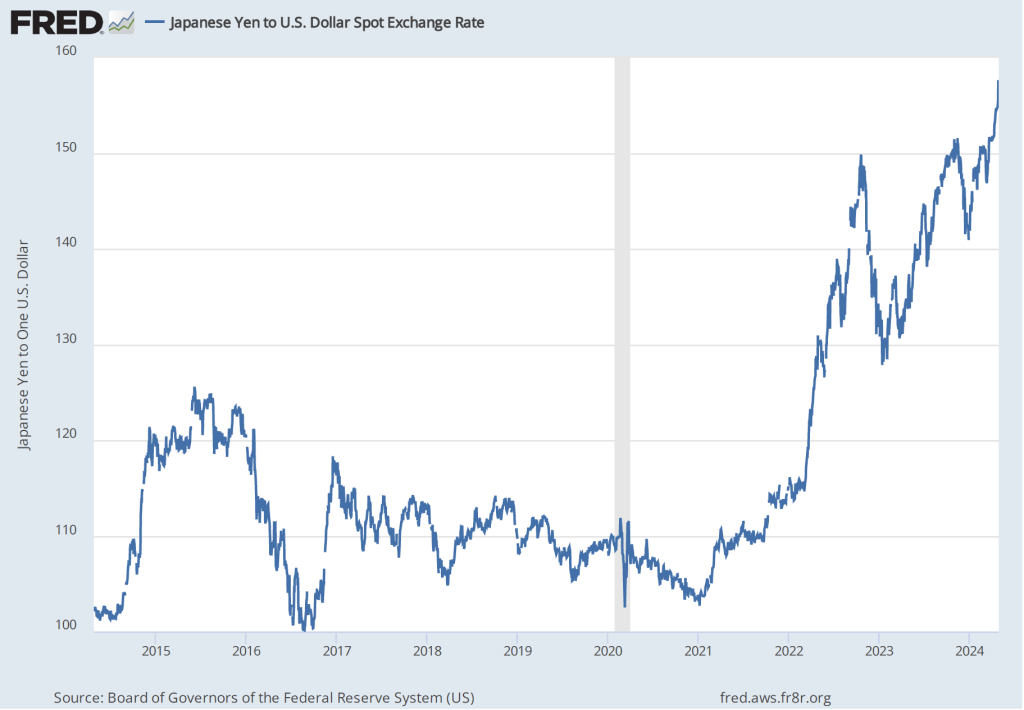

In a recent post, economics blogger Noah Smith discussed the effects on the Japanese economy of a “weaker yen”: “A weaker yen is making Japanese people feel suddenly poorer ….” But “let’s remember that a ‘weaker’ exchange rate isn’t always a bad thing.”

When the yen becomes weaker, does one yen exchange for more or fewer U.S. dollars?

Why might a weaker yen make Japanese people feel poorer?

Are there any ways that a weaker yen might help the Japanese economy? Briefly explain.

Considering your answers to parts b. and c., can you determine whether a weak yen is good or bad for the Japanese economy? Briefly explain.

Solving the Problem

Step 1:Review the chapter material. This problem is about the effect of changes in a country’s exchange rate on the country’s economy, so you may want to review Macroeconomics, Chapter 18, Section 18.2, “The Foreign Exchange Market and Exchange Rates,” (Economics, Chapter 28, Section 18.2, and Essentials of Economics, Chapter 19, Section 19.6.

Step 2:Answer part a. by explaining what a “weaker” yen means. A weaker yen will exchange for fewer U.S. dollars (or other currencies), or, equivalently, more yen will be required in exchange for a U.S. dollar. (This situation is illustrated in the figure at the top of this post, which shows the substantial weakening of yen against the dollar in the period since the end of the 2020 recession.)

Step 3: Answer part b. by explaining why a weaker yen might make people in Japan feel poorer. A weaker yen raises the yen price of imported goods. For example at an exchange rate of ¥100 = $1, a $1 Hershey candy bar imported from the United States will sell in Japan for ¥100. But if the yen becomes weaker and the exchange rate moves to ¥120 = $1, then the imported candy bar will have increased in price to ¥120. (Note that this discussion is simplified because a change in the exchange rate won’t necessarily be fully passed through to the prices of imported goods, particularly in the short run. But we would still expect that a weaker yen will result in higher yen prices of imports.) A weaker yen will require people in Japan to pay more for imports, leaving them with less to spend on other goods. Because they will be able to consume less, people in Japan will feel poorer. (As we note in Section 18.3, many goods traded internally are priced in U.S. dollars—oil being an important example. Because Japan imports nearly all of its oil and more than half of its food, a decline in the value of the yen in exchange for the dollar will increase the yen price of key consumer goods.)

Step 4: Answer part c. by explaining how a weaker yen might help the Japanese economy. A weaker yen increases the yen price of Japanese imports but it also decreases the foreign currency price of Japanese exports. This effect would be the main way in which a weaker yen might help the Japanese economy but we can also note that Japanese businesses that compete with foreign imports will also be helped by the increase in import prices.

Step 5: Answer part d. by explaining that a weaker yen isn’t all bad or all good for the Japanese economy. As the answers to parts b. and c. indicate, a weaker yen creates both winners and losers in the Japanese economy. Japanese consumers lose as a result of a weaker yen but Japanese firms that export or that compete against foreign imports will be helped.

Supports:Macroeconomics, Chapter 18, Section 18.2; Economics, Chapter 28, Section 28.2; and Essentials of Economics, Chapter 19, Section 19.6.

As the figure above shows, federal government debt, sometimes called the national debt, has been increasing rapidly in the years since the 2020 Covid pandemic. (The figure show federal government debt held by the public, which excludes debt held by federal government trust funds, such as the Social Security trusts funds.) The debt grows each year the federal government runs a budget deficit—that is, whenever federal government expenditures exceed federal government revenues. The Congressional Budget Office (CBO) forecasts large federal budget deficits over the next 30 years, so unless Congress and the president increase taxes or cut expenditures, the size of the federal debt will continue to increase rapidly. (The CBO’s latest forecast can be found here. We discuss the long-run deficit and debt situation in this earlier blog post.)

When the federal government runs a budget deficit, the U.S. Treasury must sell Treasury bills, notes, and bonds to raise the funds necessary to bridge the gap between revenues and expenditures. (Treasury bills have a maturity—the time until the debt is paid off by the Treasury—of 1 year or less; Treasury notes have a maturity of 2 years to 10 years; and Treasury bonds have a maturity of greater than 10 years. For convenience, we will refer to all of these securities as “bonds.”) A recent article in the Wall Street Journal discussed the concern among some investors about the ability of the bond market to easily absorb the large amounts of bonds that Treasury will have to sell. (The article can be found here. A subscription may be required.)

According to the article, one source of demand is likely to be European and Japanese investors.

“The euro and yen are both sinking relative to the dollar, in part because the Bank of Japan is still holding rates low and investors expect the European Central Bank to slash them soon. That could increase demand for U.S. debt, with Treasury yields remaining elevated relative to global alternatives.”

a. What does the article mean by “the euro and the yen are both sinking relative to the dollar”?

b. Why would the fact that U.S. interest rates are greater than interest rates in Europe and Japan cause the euro and the yen to sink relative to the dollar?

c. If you were a Japanese investor, would you rather be invested in U.S. Treasury bonds when the yen is sinking relative to the dollar or when it is rising? Briefly explain.

Solving the Problem

Step 1:Review the chapter material. This problem is about the determinants of exchange rates, so you may want to review Macroeconomics, Chapter 18, Section 18.2, “The Foreign Exchange Market and Exchange Rates” (Economics, Chapter 28, Section 28.2; Essentials of Economics, Chapter 19, Section 19.6.)

Step 2:Answer part a. by explaining what it means that the euro and the yen “sinking relative to the dollar.” Sinking relative to the dollar means that the exchange rates between the euro and the dollar and between the yen and the dollar are declining. In other words, a dollar will exchange for more yen and for more euros.

Step 3: Answer part b. by explaining how differences in interest rates between countries can affect the exchange between the countries’ currencies. Holding other factors that can affect the attractiveness of an investment in a country’s bonds constant, the demand foreign investors have for a country’s bonds will depend on the difference in interest rates between the two countries. For example, a Japanese investor will prefer to invest in U.S. Treasury bonds if the interest rate is higher on Treasury bonds than the interest rate on Japanese government bonds. So, if interest rates in Europe decline relative to interest rates in the United States, we would expect that European investors will increase their investments in U.S. Treasury bonds. To invest in U.S. Treasury bonds, European investors will need to exhange euros for dollars, causing the supply curve for euros in exchange for dollars to shift to the right, reducing the value of the euro.

Step 4: Answer part c. by discussing whether if you were a Japanese investor, you would you rather be invested in U.S. Treasury bonds when the yen is sinking relative to the dollar or when it is rising. In answering this part, you should draw a distinction between the situation of a Japanese investor who already owns U.S. Treasury bonds and one who is considering buying U.S. Treasury bonds. A Japanese investor who already owns U.S. Treasury bonds would definitely prefer to own them when the value of the yen if falling against the dollar. In this situation, the investor will receive more yen for a given amount of dollars the investor earns from the Treasury bonds. A Japanese investor who doesn’t currently own U.S. bonds, but is thinking of buying them, would want the value of the yen to be increasing relative to the dollar because then the investor would have to pay fewer yen to buy a Treasury bond with a price in dollars, all other factors being equal. (The face value of a Treasury bond is $1,000, although at any given time the price in the bond market may not equal the face value of the bond.) If the interest rate difference between U.S. and Japanese bonds is increasing at the same time as the value of the yen is decreasing (as in the situation described in the article) a Japanese investor would have to weigh the gain from the higher interest rate against the higher price in yen the investor would have to pay to buy the Treasury bond.

Join authors Glenn Hubbard & Tony O’Brien as they discuss the economic landscape of inflation, soft-landings, and the green economy. This conversation occurred on Saturday, 9/16/23, prior to the FOMC meeting on September 19th-20th.

A food market in Mexico. (Photo from mexperience.com)

Supports:Macroeconomics, Chapter 18, Economics, Chapter 28, and Essentials of Economics, Chapter 19.

In September 2023, an article in the Los Angeles Times discussed the effects on Mexico of the “’super-peso,’ as the Mexican currency has been dubbed since steadily gaining 18% on the dollar during the last 12 months.” The article focused on the effects of the rising value of the peso on people in Mexico who receive U.S. dollars from relatives and friends working in the United States. Many of the people who receive these payments rely on them to buy basic necessities, such as food and clothing. An article in the Wall Street Journal on the effects of the rising value of the peso noted that: “The peso’s strength has helped curtail inflation ….”

Briefly explain what the Los Angeles Times article means by the peso “gaining” on the U.S. dollar? Does the peso gaining on the dollar mean that someone exchanging dollars for pesos would receive more pesos or fewer pesos?

As a result of the rising value of the peso would people in Mexico receiving dollar payments from relatives in the United States be better off or worse off? Briefly explain.

Why would the increasing strength of the peso reduce the inflation rate in Mexico?

The Los Angeles Times article also noted that: “The Bank of Mexico’s benchmark interest rate of 11.25% is more than double the U.S. Federal Reserve target …” Does this fact have anything to do with the increase in the value of the peso in exchange for the dollar? Briefly explain.

Solving the Problem

Step 1: Review the chapter material. This problem is about the effect of fluctuations in the exchange rate and the relationship between interest rates and exchange rates, so you may want to review Macroeconomics, Chapter 18, Section 8.2, “The Foreign Exchange Market and Exchange Rates,” or the corresponding sections in Economics, Chapter 28 or Essentials of Economics, Chapter 19.

Step 2:Answer part a. by explaining what it means for the peso to be “gaining” on the U.S. dollar. The peso gaining on the dollar means that someone can exchange fewer pesos to receive a dollar. Or, alternatively, someone exchanging dollars for pesos will receive fewer pesos.

Step 3: Answer part b. by explaining why people in Mexico receiving dollar payments from relatives in the United States will be worse off because of the rising value of the peso. People living in Mexico needs pesos to buy food and clothing from Mexican stores. Because people will receive fewer pesos in exchange for the dollars they receive from relatives in the United States, these people will have been made worse off by the rising value of the peso.

Step 4: Answer part c. by explaining why the increasing strength of the peso will reduce inflation in Mexico. A country’s inflation rate includes the prices of imported goods as well as the prices of domestically produced goods. A stronger peso means that fewer pesos are needed to buy the same quantity of a foreign currency, which reduces the peso price of imports from that country. For example, a stronger peso reduces the number of pesos Mexican consumers pay to buy $10 worth of cucumbers imported from the United States. Falling prices of imported goods will reduce the inflation rate in Mexico.

Step 5: Answer part d. by explaining why higher interest rates in Mexico relative to interest rates in the United States will increase the value of the peso in exchange for the U.S. dollar. If interest rates in Mexico rise relative to interest rates in the United States, Mexican financial assets, such as Mexican government bonds, will be more desirable, causing investors to increase their demand for the pesos they need to buy Mexican financial assets. The resulting shift to the right in the demand curve for pesos will cause the equilibrium exchange rate between the peso and the dollar to increase.

Sources: Patrick J. McDonnell, “Mexico’s Peso Is Soaring. That’s Bad News for People Who Rely on Dollars Sent from the U.S.,” Los Angeles Times, September 5, 2023; and Anthony Harrup, “Mexico’s Peso Surges to Strongest Level Since 2015,” Wall Street Journal, July 13, 2023.

Novo Nordisk production facility in Denmark (Photo from Bloomberg News via the Wall Street Journal.)

Like most other small European countries, imports and exports are more important in the Danish economy than in the U.S. economy. In 2022, imports were 59 percent of Danish GDP and exports were 70 percent. In contrast, in 2022 imports were only 16 percent of U.S. GDP and exports were only 12 percent.

The Danish company Novo Nordisk makes the weight-loss prescription injections Ozempic and Wegovy. Because these and related pharmaceuticals are the first to result in significant weight loss among patients, demand for them has been very strong. (Note that some researchers believe that is not yet clear whether long-term use of these drugs might have side effects.) Demand has been so strong that Novo Nordisk’s market cap—the total value of its outstanding shares of stock—is now larger than Denmark’s GDP. According to the Wall Street Journal, Novo Nordisk now has the second largest market cap in Europe, behind only luxury good manufacturer LVMH Moët Hennessy Louis Vuitton

Most of Novo Nordisk’s customers are outside of Denmark, so to buy Ozempic or Wegovy, these customers much exchange their domestic currency—for example, euros, U.S. dollars, pounds, or yen—for Danish kroner. This increase in demand, increases the value of kroner relative to dollars, euros, and other currencies. (We discuss the effects of changes in demand and supply of a currency relative other currencies in Macroeconomics, Chapter 18, Section 18.2, Economics, Chapter 28, Section 28.2, and Essentials of Economics, Chapter 19, Section 19.6.)

Denmark has been a member of the European Union (EU), since the EU’s formation in 1991. But it is one of two EU countries (Sweden is the other) that has retained its own currency rather than using the euro. Because most of Denmark’s trade has traditionally been with other countries in the EU, the Danmarks Nationalbank, Denmark’s central bank, has pegged the value of the krone to the euro. Pegging makes it easier for Danish firms to plan because they know the prices their goods and services will sell for in eurozone countries. In addition, Danish firms that borrow in euros know how much in interest they will be paying in kroner. Finally, if the krone rises in value against other currencies, prices of imported goods and services will increase, raising the Danish inflation rate. (We discuss currency pegs in Macroeconomics, Chapter 18, Section 18.3, and Economics, Chapter 28, Section 28.3.) Inflation is a significant concern in Denmark because, as the following figure shows, the inflation rate reached 10.1 percent in October 2022. Although by July 2023, the inflation rate had decline to 3.1 percent, that rate was still above the Nationalbank’s inflation target of 2 percent.

Source: Statistics Denmark, dst.dk.

To keep the the krone pegged against the euro, the Nationalbank has to reduce the demand for the krone. The key tool that a central bank has to reduce demand for its country’s currency is interest rates. If the Nationalbank keeps interest rates in Denmark below interest rates in eurozone countries, investors will demand fewer kroner in exchange for euros. Accordingly, the Nationalbank as kept its key monetary policy rate below the corresponding rate set by the European Central Bank. In August the ECB’s policy rate was 3.75 percent, whereas the Nationalbank’s corresponding policy rate was 3.35 percent.

It’s unusual even for a small country that its central bank has to take steps to respond to a surge in demand for a single product. But that was the situation of the Danish central bank in 2023.

Sources: Joseph Walker, Dominic Chopping, and Sune Engel Rasmussen Wall Street Journal, August 17, 2023; Matthew Fox, “America’s Favorite Weight Loss Drugs Are Impacting Denmark’s Currency and Interest Rates,” finance.yahoo.com, August 18, 2023; Christian Weinberg, “Novo’s Value Surpasses Denmark GDP After Obesity Drug Boost,” bloomberg.com, August 9, 2023; Tom Fairless, “European Central Bank Raises Rates, Says Pausing Is an Option” Wall Street Journal, July 27, 2023; and “Official Interest Rates,” nationalbanken.dk.

Join authors Glenn Hubbard & Tony O’Brien as they discuss the state of the landing the economy will achieve – hard vs. soft – or “no landing”. Also, they address the debt ceiling and the barriers it might present to a recovery. We also delve into the Chips Act and what economics has to say about the subsidy of a particular industry. Gain insights into today’s economy through our final podcast of the 2022-2023 academic year! Our discussion covers these points but you can also check for updates on our blog post that can be found HERE .

Argentina’s Argentina’s Economy Minister Sergio Massa coming from a meeting in Washington, DC with the International Monetary Fund to discuss the country’s hyperinflation. Photo from the Wall Street Journal.

Argentina has been through several periods of hyperinflation during with the price level has increased more than 50 percent per month. The following figure shows the inflation rate as measured by the percentage change in the consumer price index from the previous month for since the beginning of 2018. The inflation rate during these years has been volatile, being greater than 50 percent per month during several periods, including staring in the spring of 2022. High rates of inflation have become so routine in Argentina that an article in the Wall Street Journal quoted on store owner as saying, “Here 40% [inflation] is normal. And when we get past 50%, it doesn’t scare us, it simply bothers us.”

As we discuss in Macroeconomics, Chapter 14, Section 14.5 (Economics, Chapter 24, Section 24.5 ), when an economy experiences hyperinflation, consumers and businesses hold the country’s currency for as brief a time as possible because the purchasing power of the currency is declining rapidly. As we noted in the chapter, in some countries experiencing high rates of inflation, consumers and businesses buy and sell goods using U.S. dollars rather than the domestic currency because the purchasing power of the dollar is more stable. This demand for dollars in countries experiencing high inflation rates is one reason why an estimated 80 percent of all $100 bills circulate outside of the United States.

The increased demand for U.S. dollars by people in Argentina is reflected in the exchange rate between the Argentine peso and the U.S. dollar. The following figure shows that at the beginning of 2018, one dollar exchanged for about 18 pesos. By November 2022, one dollar exchanged for about 159 pesos. The exchange rate shown in the figure is the official exchange rate at which people in Argentina can legally exchange pesos for dollars. In practice, it is difficult for many individuals and small firms to buy dollars at the official exchange rate. Instead, they have to use private currency traders who will make the exchange at an unofficial—or “blue”—exchange rate that varies with the demand and supply of pesos for dollars. A reporter for the Economist described his experience during a recent trip to Argentina: “Walk down Calle Lavalle or Calle Florida in the centre of Buenos Aires and every 20 metres someone will call out ‘cambio’ (exchange), offering to buy dollars at a rate that is roughly double the official one.”

People in Argentina are reluctant to deposit their money in banks, partly because the interest rates banks pay typically are lower than the inflation rate, causing the purchasing power of money deposited in banks to decline over time. People are also afraid that the government might keep them from withdrawing their money, which has happened in the past. As an alternative to depositing their money in banks, many people in Argentina buy more goods than they can immediately use and store them, thereby avoiding future price increases on these goods. The Wall Street Journalquoted a university student as saying: “I came to this market and bought as much toilet paper as I could for the month, more than 20 packs. I try to buy all [the goods] I can because I know that next month it will cost more to buy.”

Devon Zuegel, a U.S. software engineer and economics blogger who travels frequently to Argentina, has observed one unusual way that some people in Argentina save while experiencing hyperinflation:

“Bricks—actual bricks, not stacks of cash—are another common savings mechanism, especially for working-class Argentinians. The value of bricks is fairly stable, and they’re useful to a family building out their house. Argentina doesn’t have a mortgage industry, and thus buying a pallet of bricks each time you get a paycheck is an effective way to pay for your home in installments. (Bricks aren’t fully monetized, in that I don’t think people buy bricks and then sell them later, so people only use this method of saving when they actually have something they want to use the bricks for.)”

Sources: “Sergio Massa Is the Only Thing Standing Between Argentina and Chaos,” economist. com, October 13, 2022; Devon Zuegel, “Inside Argentina’s Currency Exchange Black Markets,” devonzuegel.com, September 10, 2022; Silvina Frydlewsky and Juan Forero, “Inflation Got You Down? At Least You Don’t Live in Argentina,” Wall Street Journal, April 25, 2022; and Federal Reserve Bank of St. Louis, FRED data set.