Photo from federalreserve.gov of the Pace University Fed Challenge team and their faculty advisers

Each year the Federal Reserve sponsors a competition among college student teams. As desribed on the Fed’s website, in the competition “Teams analyze economic and financial conditions and formulate a monetary policy recommendation, modeling the Federal Open Market Committee.”

This year’s winner is Pace University, representing the New York Federal Reserve District. Harvard College took second place and the University of California, Los Angeles took third place. The University of Pennsylvania, the University of Chicago, and Davidson College received honorable mentions. In 2024, the competition was won by the team from Princeton University, representing the Philadelphia Federal Reserve District.

This year, 139 colleges in 36 states participated in the competition. The rules of the competition are described here. After the competition, Federal Reserve Chair Jerome Powell noted that: “Fed Challenge offers undergraduate students an opportunity to learn firsthand about monetary policy and the work of the Federal Reserve. I thank these students for the dedication, creativity, and analytical skills they demonstrated as they grappled with real-world economic challenges.”

If not for the shutdown of the federal government, the Bureau of Labor Statistics (BLS) would have already released its “Employment Situation” report (often called the “jobs report”) for September and October by now. The September jobs report was released today based largely on data collected before the shutdown.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and Federal Reserve policymakers believe that employment data from the establishment survey provide a more accurate indicator of the state of the labor market than do the household survey’s employment data and unemployment data. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

Because the household survey wasn’t conducted in October, the data in the October report that relies on the household survey won’t be included when the BLS releases establishment employment data for October on December 16. The data for September released today showed the labor market was stronger than expected in that month.

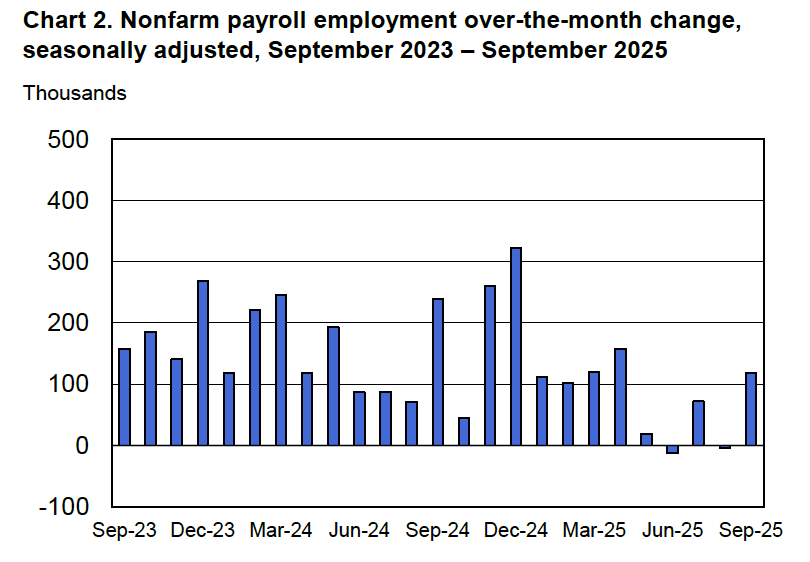

According to the establishment survey, there was a net increase of 119,00 nonfarm jobs during September. This increase was well above the increase of 50,000 that economists surveyed by FactSet had forecast. Economists surveyed by the Wall Street Journal had also forecast a net increase of 50,000 jobs. The relatively large increase in employment in September was partially offset by the BLS revising downward by a combined 33,000 jobs its previous estimates of employment in July and August. The estimate for August was revised from a net gain of 22,000 to a net loss of 4,000. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”)

The following figure from the jobs report shows the net change in nonfarm payroll employment for each month in the last two years. The figure makes clear the striking deceleration in job growth beginning in May. The Trump administration announced sharp increases in U.S. tariffs on April 2. Media reports indicate that some firms have slowed hiring due to the effects of the tariffs or in anticipation of those effects.

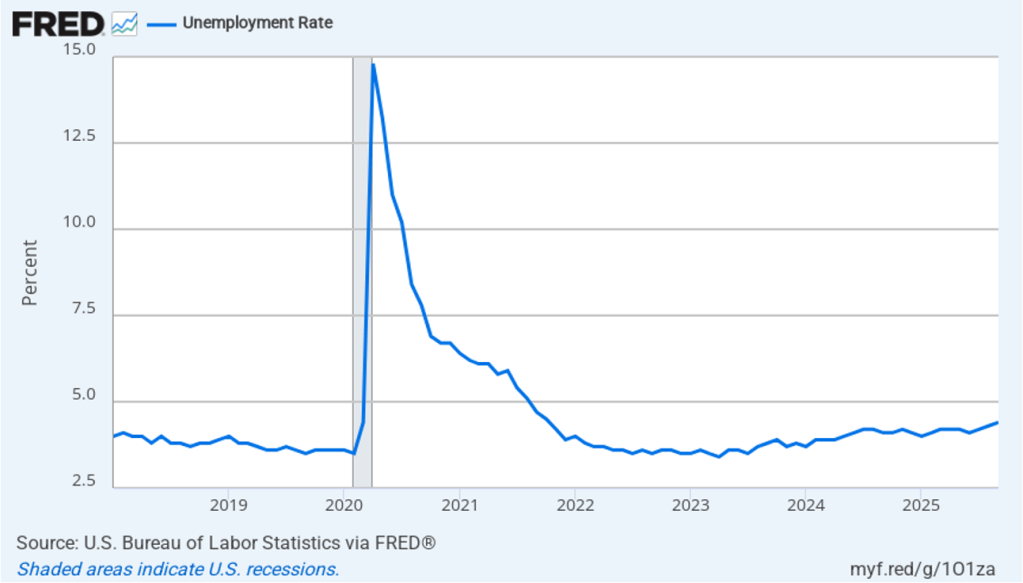

As shown in the following figure, the unemployment rate increased from 4.3 percent in August to 4.4 percent in September, the highest rate since October 2021. The unemployment rate is above the 4.3 percent rate economists surveyed by FactSet had forecast. The unemployment rate had been remarkably stable, staying between 4.0 percent and 4.2 percent in each month from May 2024 to July 2025, before breaking out of that range in August. In September, the members of the Federal Open Market Committee (FOMC) forecast that the unemployment rate during the fourth quarter of 2025 would average 4.5 percent. The FOMC’s current estimate of the natural rate of unemployment—the normal rate of unemployment over the long run—is 4.2 percent. (We discuss the natural rate of unemployment in Macroeconomics, Chapter 9 and Economics, Chapter 19.)

Each month, the Federal Reserve Bank of Atlanta estimates how many net new jobs are required to keep the unemployment rate stable. Given slower growth in the working-age population due to the aging of the U.S. population and a sharp decline in immigration, the Atlanta Fed currently estimates that the economy would have to create 111,878 net new jobs each month to keep the unemployment rate stable at 4.4 percent. If this estimate is accurate, if the average monthly net job increase from May through September of 38,600 were to continue, the result would be a rising unemployment rate.

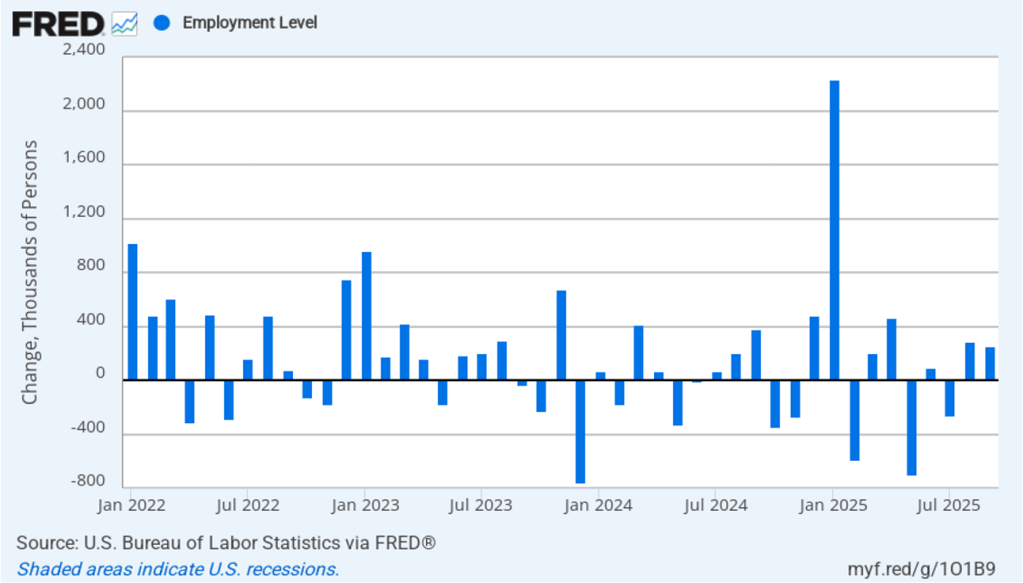

As the following figure shows, the monthly net change in jobs from the household survey moves much more erratically than does the net change in jobs from the establishment survey. As measured by the household survey, there was a net increase of 251,000 jobs in September, following a net increase of 288,000 jobs in August. As an indication of the volatility in the employment changes in the household survey note the very large swings in net new jobs in January and February. In any particular month, the story told by the two surveys can be inconsistent. as was the case in September with employment increasing much more in the household survey than in the employment survey. (In this blog post, we discuss the differences between the employment estimates in the two surveys.)

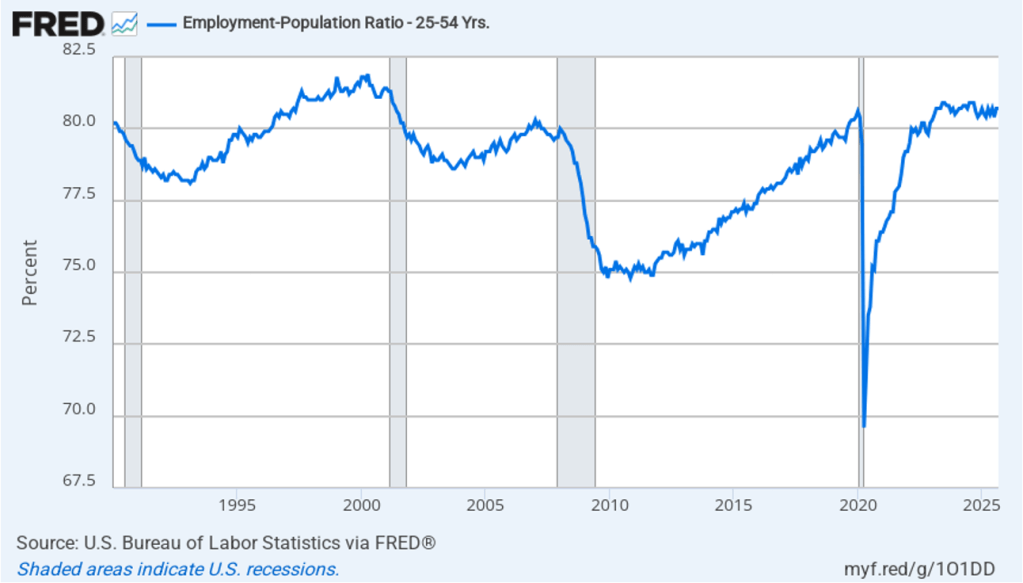

The household survey has another important labor market indicator: the employment-population ratio forprime age workers—those aged 25 to 54. In September the ratio was 80.7 percent, the same as in August. The prime-age employment-population ratio is somewhat below the high of 80.9 percent in mid-2024, but is still above what the ratio was in any month during the period from January 2008 to February 2020. The continued high levels of the prime-age employment-population ratio indicates strength in the labor market.

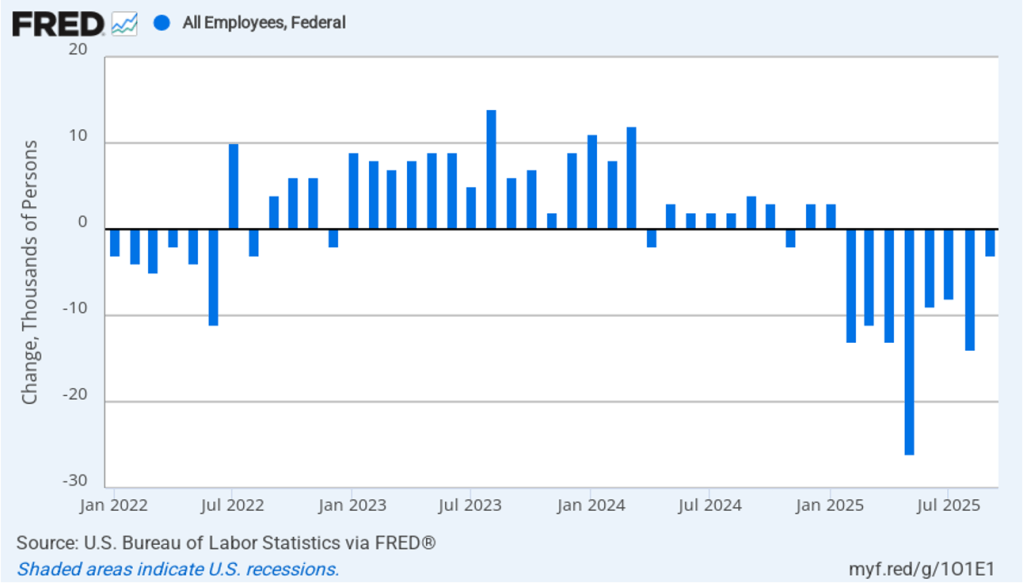

It is still unclear how many federal workers have been laid off since the Trump Administration took office. The establishment survey shows a decline in federal government employment of 3,000 in September and a total decline of 97,000 since the beginning of February 2025. However, the BLS notes that: “Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.” It’s possible that as more federal employees end their period of receiving severance pay, future jobs reports may report a larger decline in federal employment. To this point, the decline in federal employment has had only a small effect on the overall labor market.

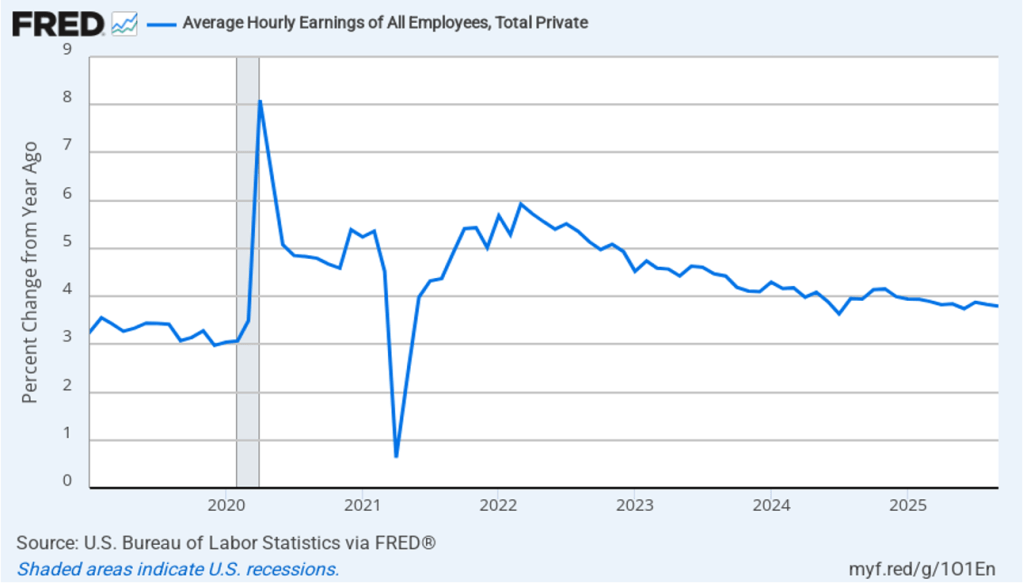

The establishment survey also includes data on average hourly earnings (AHE). As we noted in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage of being available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. The AHE increased 3.8 percent in September, the same as in August.

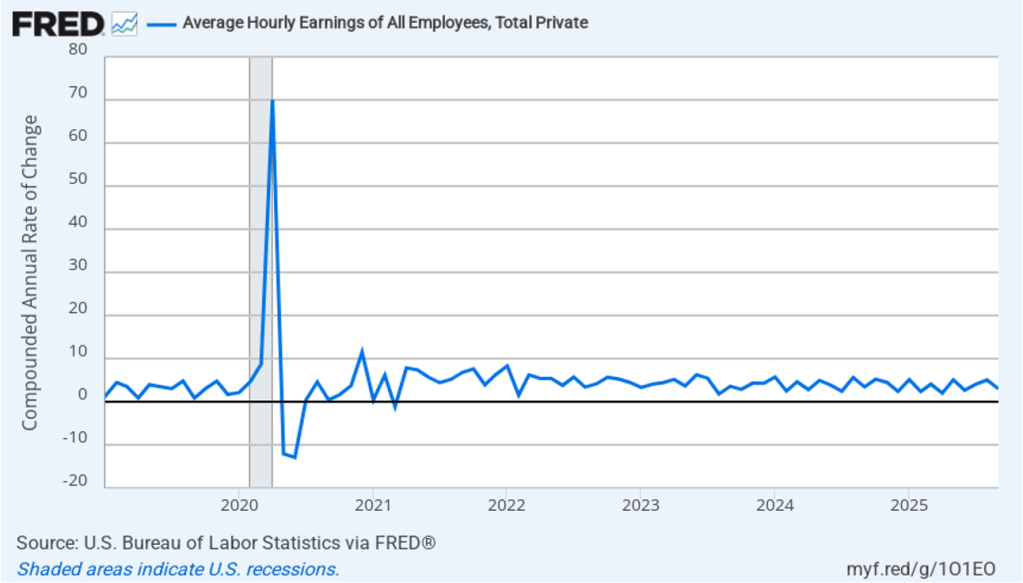

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month wage inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic. In September, the 1-month rate of wage inflation was 3.0 percent, down from 5.1 percent in August. This slowdown in wage growth may be an indication of a weakening labor market. But one month’s data from such a volatile series may not accurately reflect longer-run trends in wage inflation.

What effect might today’s jobs report have on the decisions of the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) with respect to setting its target range for the federal funds rate? The minutes from the FOMC’s last meeting on October 28–29 indicate that committee members had “strongly differing views” over whether to cut the target range by 0.25 percentage point (25 basis points) at its next meeting on December 9–10 or to leave the target range unchanged.

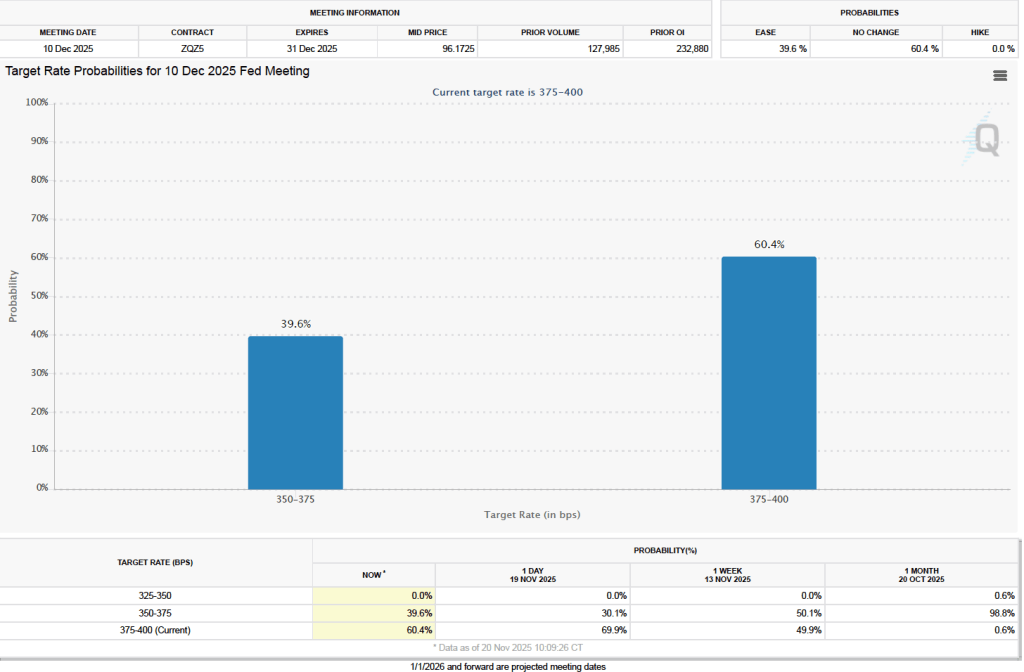

One indication of expectations of future changes in the FOMC’s target for the federal funds rate comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) A month ago, investors assigned a 98.8 percent probability of the committee cutting its target range to 3.50 percent to 3.75 percent at its December meeting. Since that time indications have increased that output and employment growth have continued to be relatively strong and that inflation is stuck above the Fed’s 2 percent annual target. This morning, as the following figure shows, investors assign a probability of 60. 4 percent to the committee keeping its target unchanged at 3.75 percent to 4.00 percent at the December meeting. Committee members will also release their Summary of Economic Projections (SEP) at that meeting. The SEP, along with Fed Chair Powell’s remarks at his press conference following the meeting, should provide additional information on the monetary policy path the committee intends to follow in the coming months.

Photo of Federal Reserve Chair Jerome Powell from federalreserve.gov

Today’s meeting of the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) occurred against a backdrop of a shutdown of the federal government that has delayed release of most government economic data. (We discuss the government shutdown here, here, and here.)

As most observers had expected, the committee decided today to lower its target for the federal funds rate from a range of 4.00 percent to 4.25 percent to a range of 3.75 percent to 4.oo percent—a cut of 0.25 percentage point, or 25 basis points. The members of the committee voted 10 to 2 for the 25 basis point cut with Governor Stephen Miran dissenting because he preferred a 50 basis point cut and Jeffrey Schmid, president of the Federal Reserve Bank of Kansas City, dissenting because he preferred that the target range be left unchanged at this meeting.

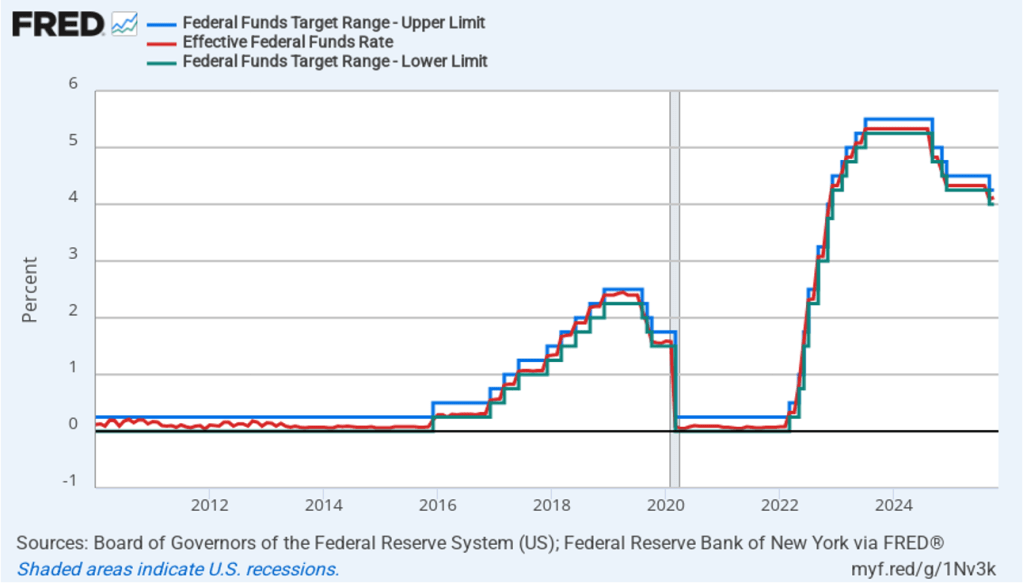

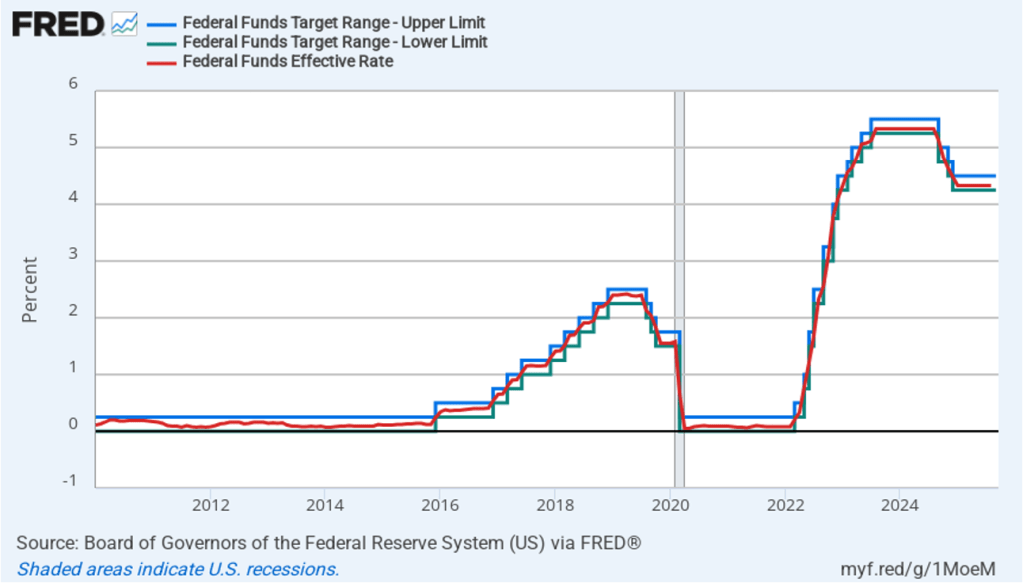

The following figure shows, for the period since January 2010, the upper bound (the blue line) and the lower bound (the green line) for the FOMC’s target range for the federal funds rate, as well as the actual values of the federal funds rate (the red line). Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

During his press conference following the meeting, Fed Chair Jerome Powell made news by stating that a further cut in the target rate at the FOMC’s meeting on December 9–10 is not a foregone conclusion. This statement came as a surprise to investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As of yesterday, investors has assigned a probability of 90.5 percent to the committee cutting its target range by another 25 basis points at the December meeting. Today that probability dropped to zero. Instead investors now assign a probability of 67.8 percent to the target remaining unchanged at that meeting, and a probability of 32.2 percent of the committee raising its target by 25 basis points.

Powell also indicated that he believes that the recent increase in inflation was largely due to the effects of the increase in tariff rates that the Trump administration began implementing in April. (We discuss the recent data on inflation in this post.) Powell indicated that committee members expect that the tariff increases will cause a one-time increase in the price level, rather than a long-term increase in the inflation rate. As a result, he said that the shift in the “balance of risks” caused the committee to believe that cutting the target for the federal funds rate was warranted to avoid the possibility of a significant rise in the unemployment rate.

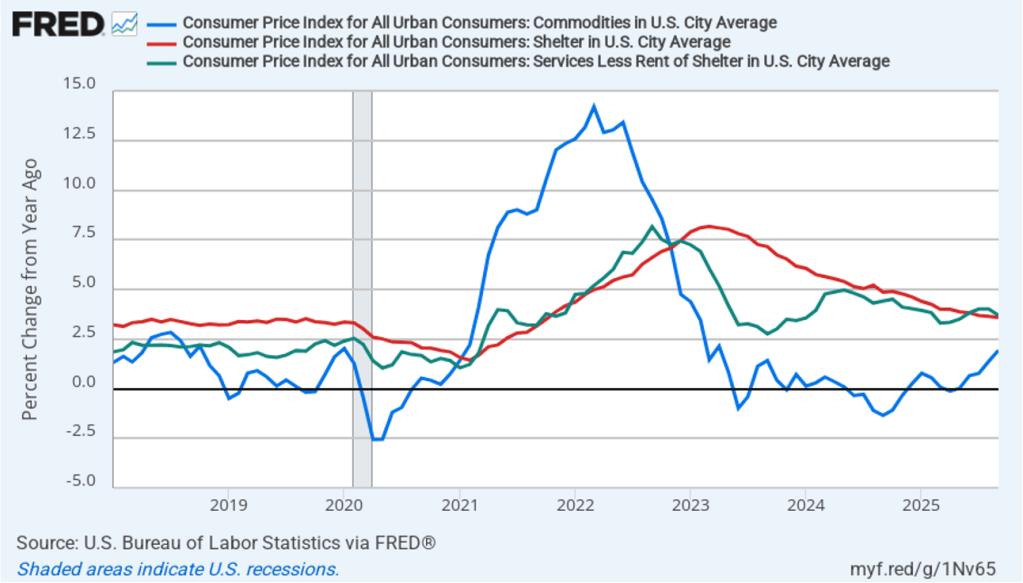

In discussing inflation, Powell highlighted three aspects of the recent CPI report: inflation in goods, inflation in shelter, and inflation in services not including shelter. (The BLS explains is measurement of shelter here.) The following figure shows inflation in each of those categories, measured as the percentage increase from the same month in the previous year. Inflation in goods (the blue line) has been trending up, reflecting the effect of increased tariffs rates. Inlation in shelter (the red line) and in services minus shelter (the green line) have generally been trending downward. Powell noted that the decline in inflation in shelter has been slower than most members of the committee had expected.

Still, Powell argued that with the downward trend in services, once the temporary inflation in goods due to the effects of tariffs had passed through the economy, inflation was likely to be close the Fed’s 2 percent annual target. He thought this was particularly likely to be true because even after today’s cut, the federal funds rate was “restrictive” because it remained above its long-run nominal and real values. A restrictive monetary policy will slow spending and inflation.

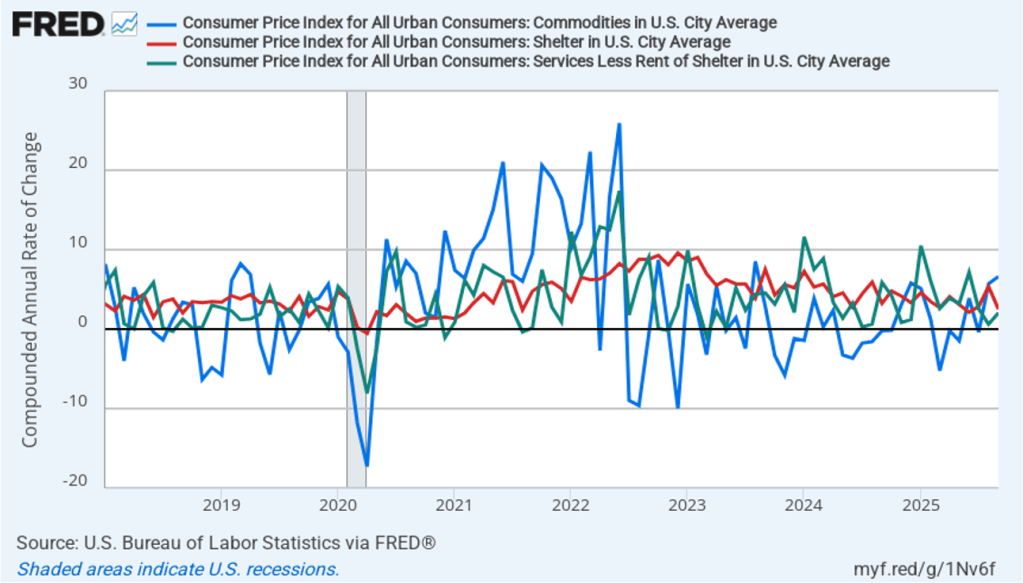

In the following figure, we look at the 1-month inflation rates—that is, the annual inflation rates calculated by compounding the current month’s rates over an entire year—for the same three categories. Calculated as the 1-month inflation rate, goods inflation (the blue line) was running at a very high 6.6 percent in September. inflation in shelter (the red line) had declined to 2.5 per cent in September. Inflation in services minus shelter rose slightly in September to 2.1 percent.

Assuming that the shutdown of the federal government ends within the next few weeks, members of the FOMC will have a great deal of data on inflation, real GDP growth, and employment to consider before their next meeting in December.

Kevin Hassett, director of the National Economic Council (photo from the AP via the Wall Street Journal)

Jerome Powell’s second term as chair of the Federal Reserve’s Board of Governor ends on May 15,2026. (Although his term as a member of the Board of Governors doesn’t end until January 31, 2028, Fed chairs have typically resigned their seats on the Board at the time that their term as chair ends.) President Trump has been clear that he won’t renominate Powell to a third term. Who will he nominate?

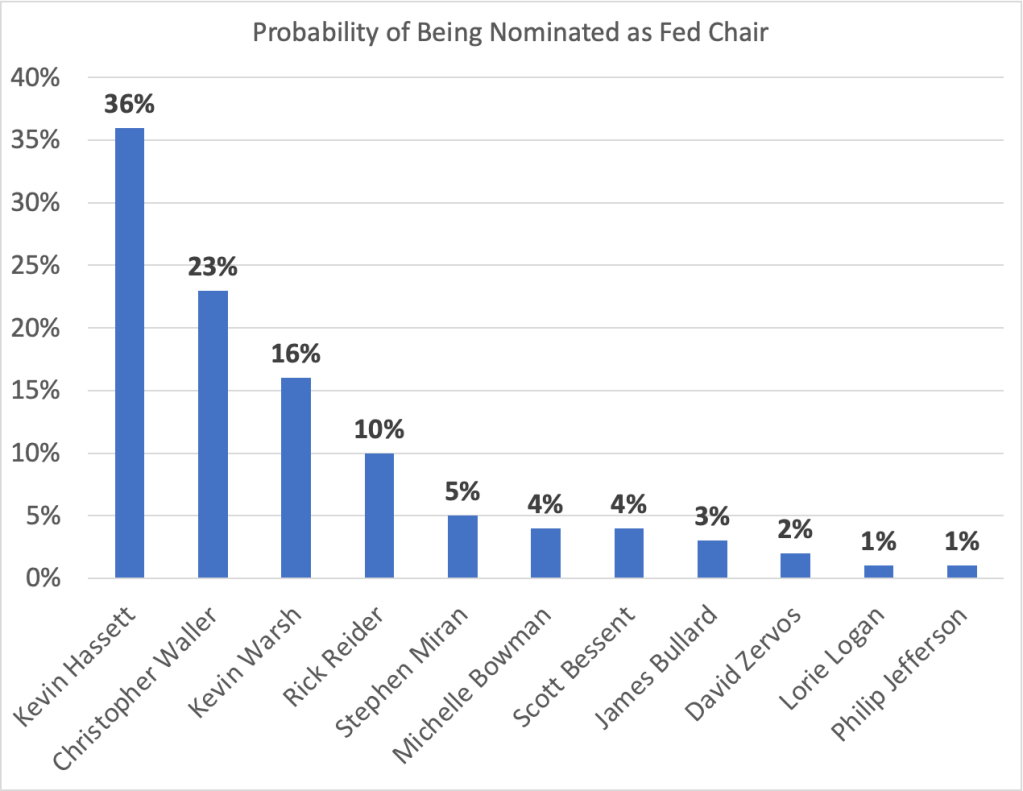

Polymarket is a site on which people can bet on political outcomes, including who President Trump will choose to nominate as Fed chair. The different amounts wagered on each candidate determine the probabilities bettors assign to that candidate being nominated. The following table shows each candidate with a probability of least 1 percent of being nominated as of 5 pm eastern time on October 27.

Kevin Hassett, who is currently the director of the National Economic Council, has the highest probability at 36 percent. Fed Governor Christopher Waller, who was nominated to the Board by President Trump in 2020, is second with a 23 percent probability. Kevin Warsh, who served on the Board from 2006 to 2011, and was important in formulating monetary policy during the financial crisis of 2007–2009, is third with a probability of 16 percent. Rick Reider, an executive at the investment company Black Rock, is unusual among the candidates in not having served in government. Bettors on Polymarket assign him a 10 percent probability of being nominated. Stephen Miran and Michelle Bowman are current members of the Board who were nominated by President Trump.

Scott Bessent is the current Treasury secretary and has indicated that he doesn’t wish to be nominated. James Bullard served as president of the Federal Reserve Bank of St. Louis from 2008 to 2023. David Zervos is an executive at the Jeffries investment bank and in 2009 served as an adviser to the Board of Governors. Lorie Logan is president of the Federal Reserve Bank of Dallas and Philip Jefferson is currently vice chair of the Board of Governors.

Today, Treasury Secretary Scott Bessent indicated that the list of candidates had been reduced to five—although bettors on Polymarket indicate that they believe these five are likely to be the first five candidates listed in the chart above, it appears that Bowman, rather than Miran, is the fifth candidate on Bessent’s lists. Bessent indicated that President Trump will likely make a decision on who he will nominate by the end of the year.

As we’ve noted in recent blog posts (here and here), the shutdown of the federal government has interrupted the release of government data, including the “Employment Situation” report prepared monthly by the Bureau of Labor Statistics (BLS). The federal government made an exception for the BLS report on the consumer price index (CPI) because annual cost-of-living increases in Social Security payments are determined by the average inflation rate in the CPI during July, August, and September.

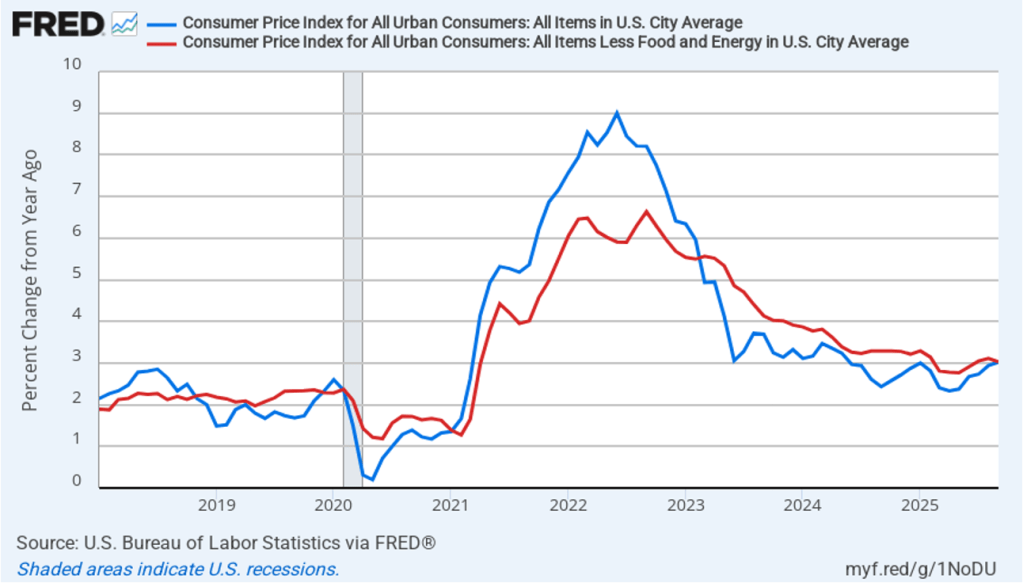

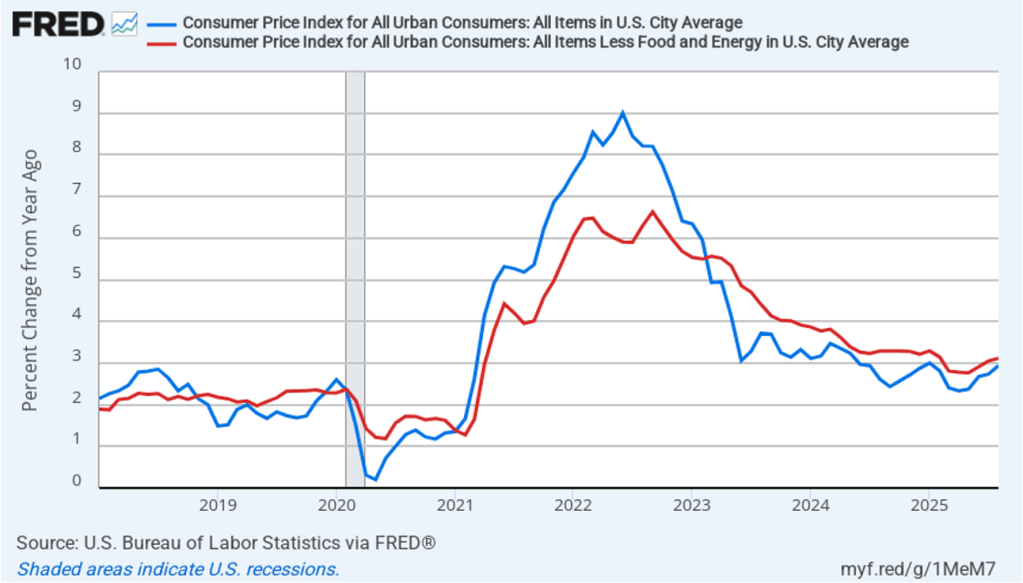

Accordingly, today (October 24), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for September. The following figure compares headline CPI inflation (the blue line) and core CPI inflation (the red line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 3.0 percent in September, up from 2.9 percent in August.

The core inflation rate,which excludes the prices of food and energy, was also 3.0 percent in September, down slightly from 3.1 percent in August.

Headline inflation and core inflation were both slightly lower than the 3.1 rate for both measures that economists had expected.

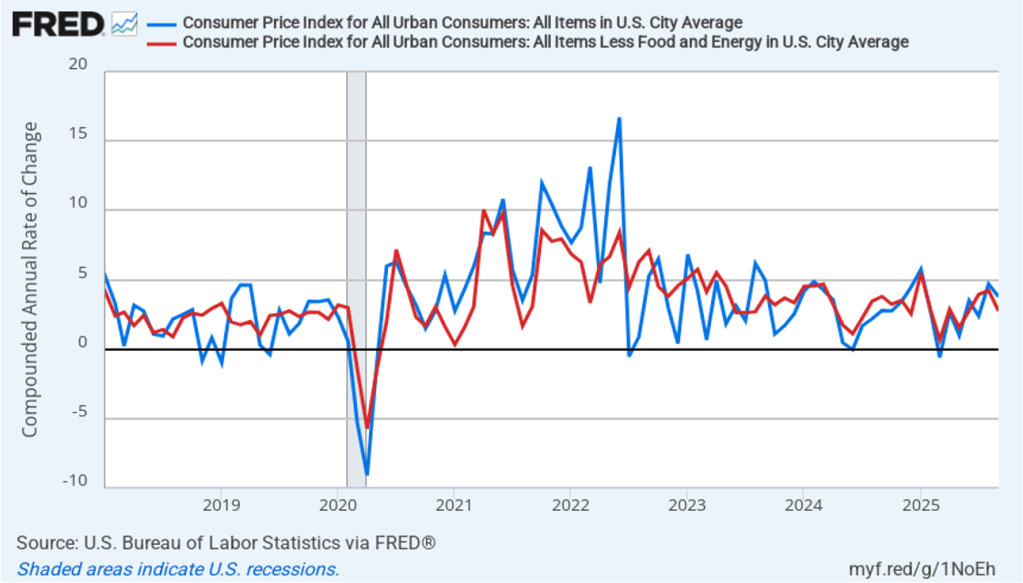

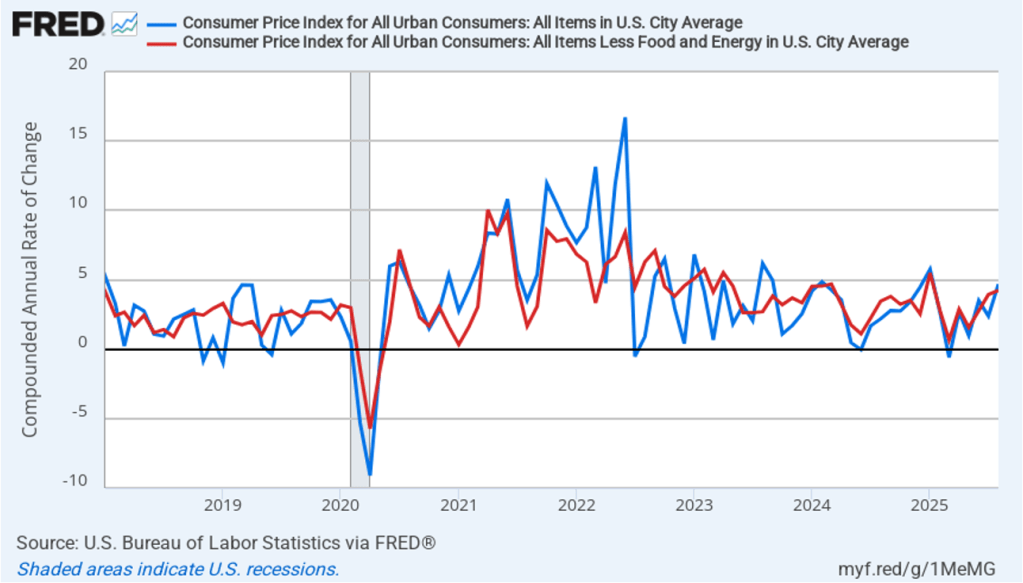

In the following figure, we look at the 1-month inflation rates for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) declined from the very high rate of 4.7 percent in August to the still high rate of 3.8 percent in September. Core inflation (the red line) declined from 4.2 percent in August to 2.8 percent in September.

The 1-month and 12-month inflation rates are both indicating that inflation remains well above the Fed’s 2 percent annual inflation target in September. Core inflation—which is often a good indicator of future inflation—in particular has been running well above target during the last three months.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that the 1-month inflation rate is particularly volatile. Also note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

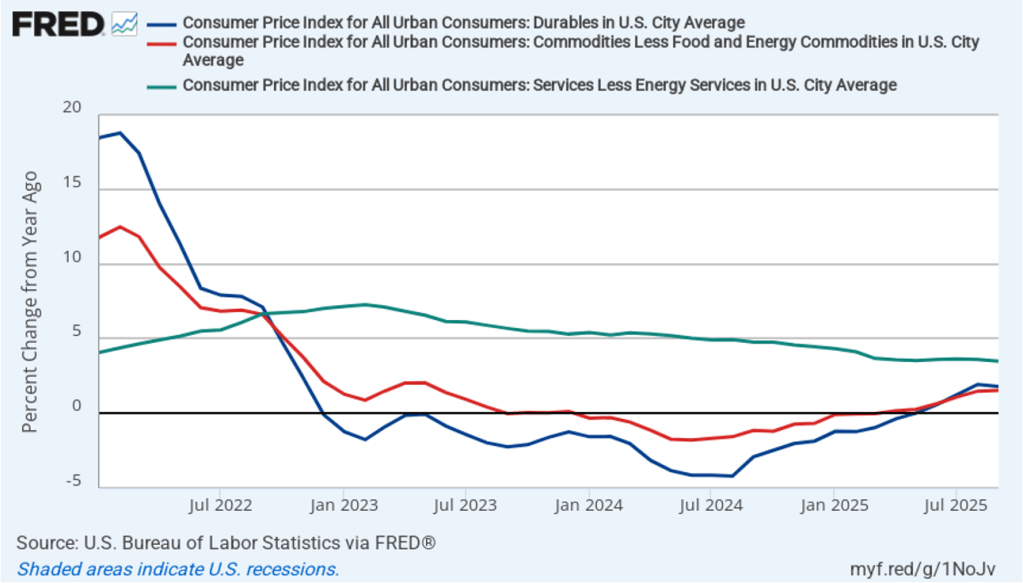

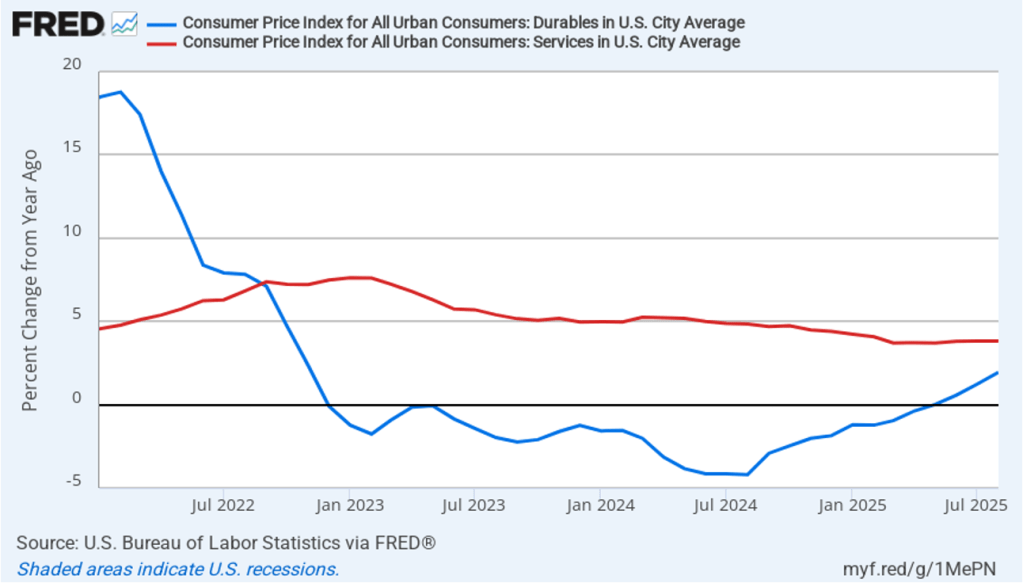

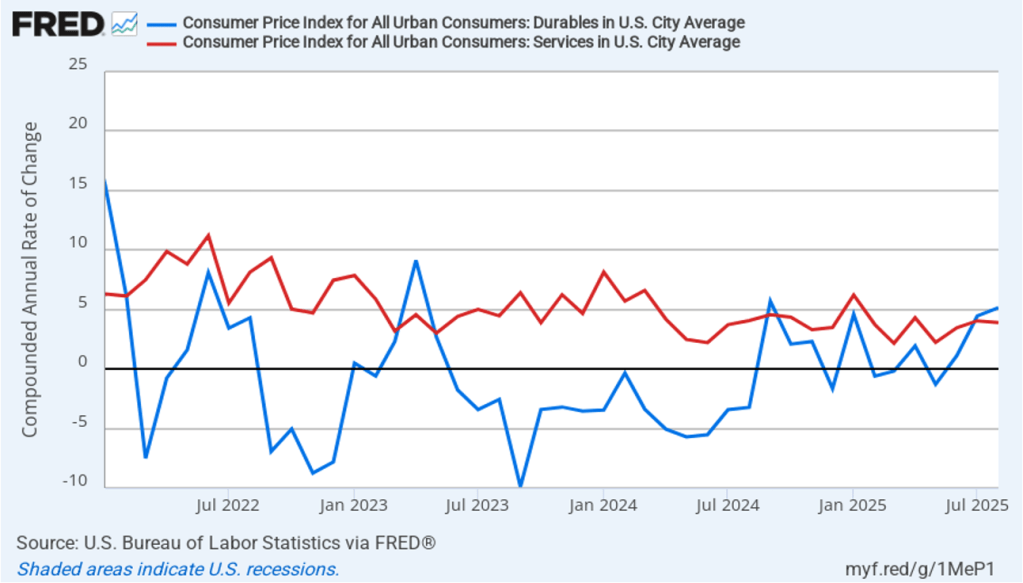

Does the increase in inflation represent the effects of the increases in tariffs that the Trump administration announced on April 2? (Note that many of the tariff increases announced on April 2 have since been reduced.) The following figure shows 12-month inflation in durable goods—such as furniture, appliances, and cars—which are likely to be affected directly by tariffs, all core goods, and core services. Services are less likely to be affected by tariffs.. To make recent changes clearer, we look only at the months since January 2022. In August, inflation in durable goods declined slightly to 1.8 percent in September from 1.9 percent in August. Inflation in core goods was unchanged in September at 1.5 percent. Inflation in core services fell slightly in September to 3.5 percent from 3.6 percent in August.

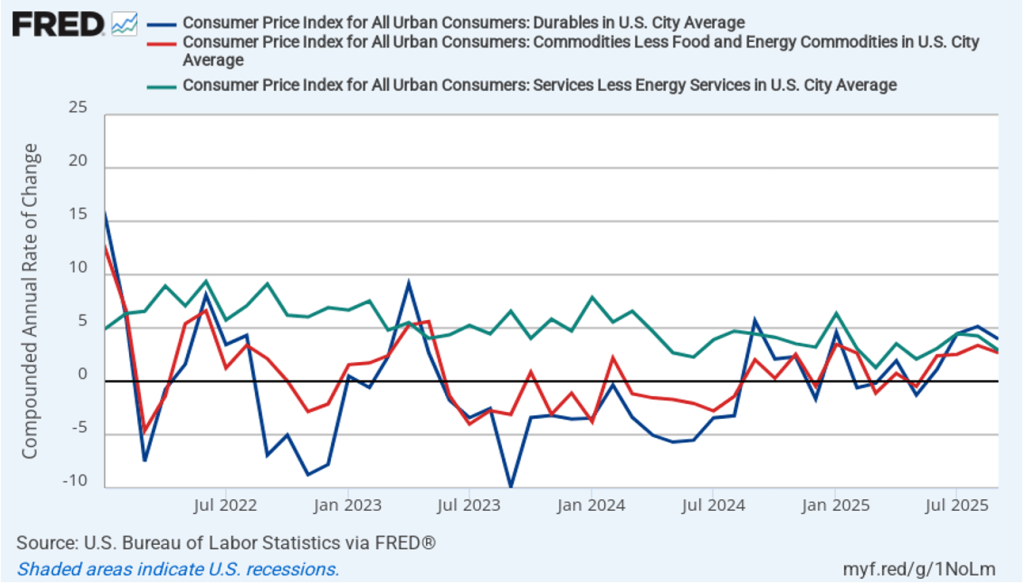

The following figure shows 1-month inflation in the prices of these products, which may makes clearer the effects of the tariff increases. In September, durable goods inflation was a high 4.0 percent, although down from 5.1 percent in August. Core goods inflation in September was 2.7 percent, down from 3.4 percent in August. Core service inflation was 2.9 percent in August, down from 4.3 percent in August.

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

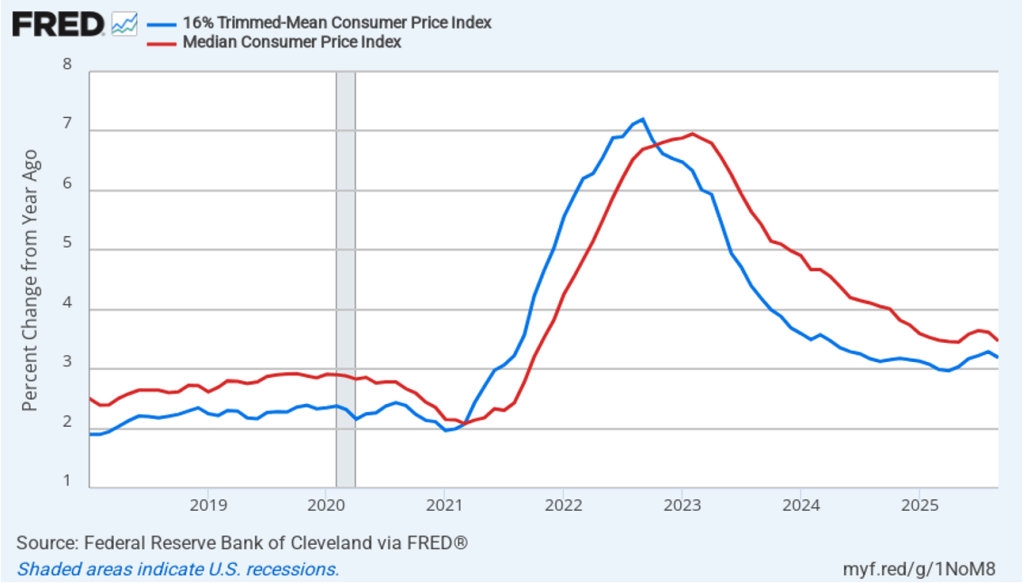

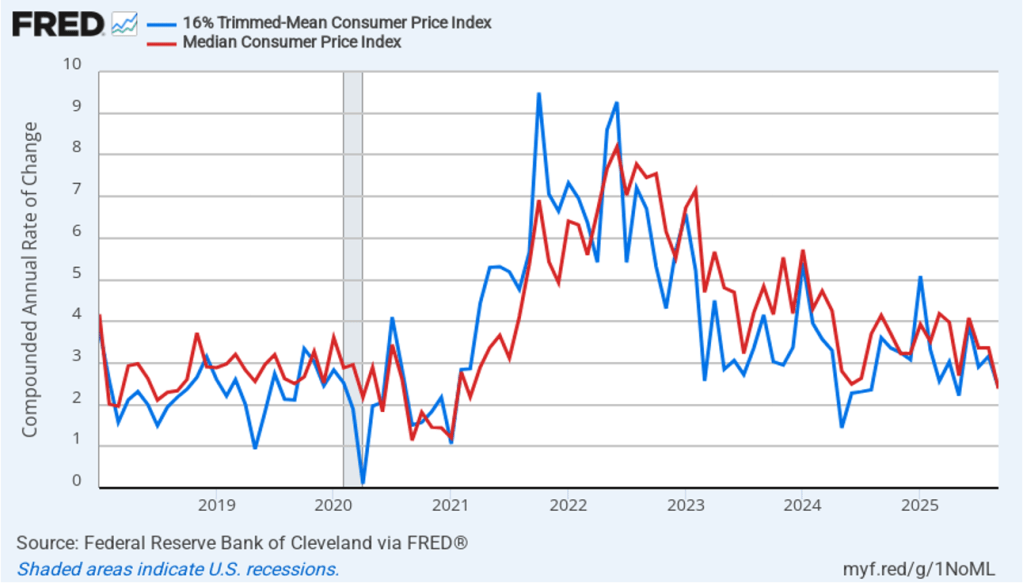

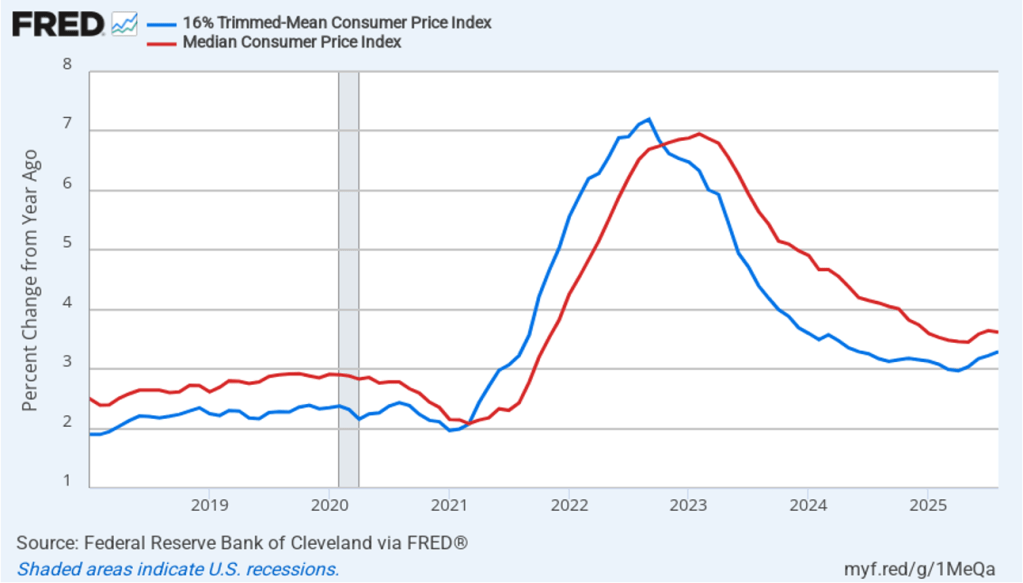

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.2 percent in September, down slightly from 3.3 August. Twelve-month median inflation (the red line) 3.5 percent in September, down slightly from 3.6 in August.

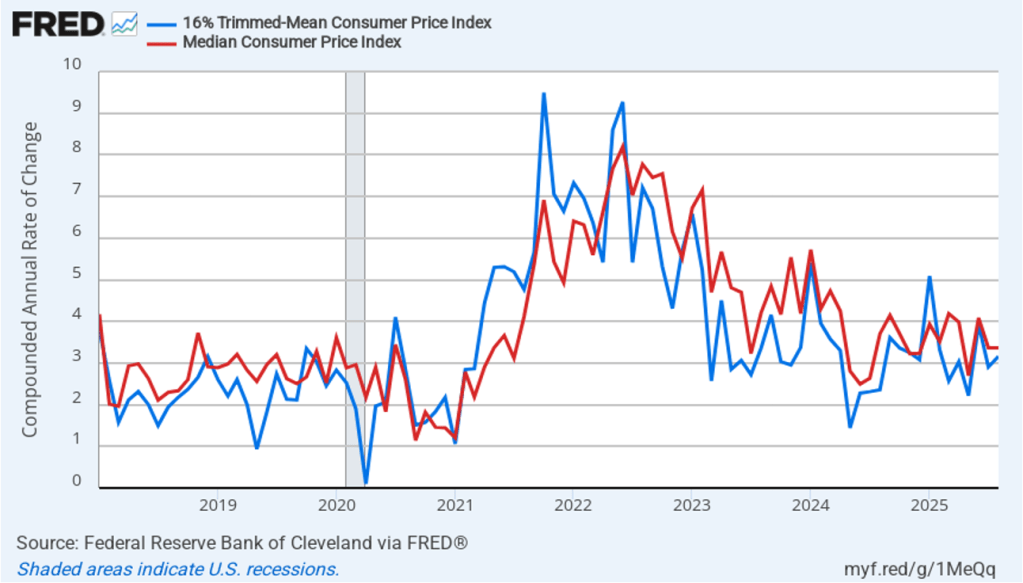

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation declined from 3.2 percent in August to 2.4 percent in September. One-month median inflation declined from 3.4 percent in August to 2.4 percent in September. These data are consistent with the view that inflation is still running above the Fed’s 2 percent target.

With inflation running above the Fed’s 2 percent annual target, we wouldn’t typically expect that the Fed’s policymaking Federal Open Market Committee (FOMC) would cut its target for the federal funds rate at its October 28–29 meeting. At this point, though, it seems likely that the FOMC will “look through” the higher inflation rates of the last few months because the higher rates may be largely attributable to one-time price increases caused by tariffs. Committee members have signaled that they are likely to cut their target for the federal funds rate by 0.25 percentage point (25 basis points) at the conclusion of next week’s meeting.

This morning, investors who buy and sell federal funds futures contracts assign a probability of 96.7 percent to the FOMC cutting its target for the federal funds rate at that meeting by 25 basis points from its current target range of 4.00 percent to 4.25 percent. Investors assign a 95.9 percent probability of the committee cutting its target by an additional 25 basis points to 3.50 percent to 3.75 percent at its December 9–10 meeting. If persistently high inflation rates reflect more than just the temporary effects of tariffs, these rate cuts will make it unlikely that the Fed will reach its 2 percent inflation target anytime soon.

Fed Governor Christopher Wallace on October 21, 2025 at the Fed’s Payment Innovation Conference (photo from federalreserve.gov)

The current partial shutdown of the federal government has delayed the release by the Bureau of Labor Statistics (BLS) of its “Employment Situation” report (often called the “jobs report”). The report had originally been scheduled to be released on October 3. In a recent blog post we discussed how well the employment data collected by the private payroll processing firm Automatic Data Processing (ADP) serves as an alternative measure of the state of the labor market. In that post we showed that ADP data on total private payroll employment tracks fairly well the BLS data on total private employment from its establishment survey (often called the payroll survey) .

An article in today’s Wall Street Journal reports that ADP has stopped providing the Fed with early access to its data. Apparently, as a public service ADP had been providing its data to the Fed a week before the data was publicly released. The article notes that ADP stopped providing the data soon after this speech delievered by Fed Governor Christopher Wallace in late August. In a footnote to the speech Wallace refers to “data that Federal Reserve staff maintains in collaboration with the employment services firm ADP.” The article points out, though, that Waller’s speech was only one of several times since 2019 that a Fed official has publicly mentioned receiving data from ADP.

Losing early access to the ADP data comes at a difficult time for the Fed, given that the BLS employment data are not available. In addition, the labor market has shown signs of weakening even though growth has remained strong in measures of output. If payroll employment has been falling, rather than growing slowly as it was in the August jobs report, that knowledge would affect the deliberations of the Fed’s policymaking Federal Open Market Committee (FOMC) at its next meeting on October 28–29. Serious deterioration in the labor market could lead the FOMC to cut its target for the federal funds rate by more than the expected 0.25 percentage point (25 basis points).

In a speech in 2019, Fed Chair Jerome Powell noted that the Fed staff had used ADP data to develop a new measure of payroll employment. Had that measure been available in 2008, Powell argued, the FOMC would have realized earlier than it did that employment was being severely affected by the deepening of the financial crisis:

“[I]n the first eight months of 2008, as the Great Recession was getting underway, the official monthly employment data showed total job losses of about 750,000. A later benchmark revision told a much bleaker story, with declines of about 1.5 million. Our new measure, had it been available in 2008, would have been much closer to the revised data, alerting us that the job situation might be considerably worse than the official data suggested.”

The Wall Street Journal article notes that Powell has urged ADP to resume sharing its employment data with the Fed.

Supports:Macroeconomics, Chapter 13, Section 13.3; Economics, Chapter 23, Section 23.3; and Essentials of Economics, Chapter 15, Section 15.3

Image generated by ChatGPT

A recent article on axios.com made the following observation: “The mainstream view on the Federal Open Market Committee is based on risk management—that the possibility of a further downshift in the job market appears to be the more pressing concern than the chance that inflation will spiral higher.” The article also notes that: “Tariffs’ effects on inflation are probably a one-time bump.”

a. What is the dual mandate that Congress has given the Federal Reserve?

b. In what circumstances might the Federal Open Market Committee (FOMC) be faced with a conflict between the goals in the dual mandate?

c. What does the author mean by tariffs’ effects on inflation being a “one-time bump”?

d. What does the author mean by the FOMC engaging in “risk management”? What is a “downshift” in the labor market? If the FOMC is more concerned about a downshift in the labor market than about inflation, will the committee raise or lower its target for the federal funds rate? Briefly explain.

Solving the Problem Step 1: Review the chapter material. This problem is about the policy dilemma the Fed can face when the unemployment rate and the inflation rate are both rising, so you may want to review Macroeconomics, Chapter 13, Section 13.3, “Macroeconomic Equilibrium in the Long Run and the Short Run.”

Step 2: Answer part a. by explaining what the Fed’s dual mandate is. Congress has given the Fed a dual mandate of achieving price stability and maximum employment.

Step 3: Answer part b. by explaining when the FOMC may face a conflict with respect to its dual mandate. When the FOMC is faced with rising unemployment and falling inflation, its preferred policy response is clear: The committee will lower its target for the federal funds rate in order to increase the growth of aggregate demand, which will increase real GDP and reduce unemployment. When the FOMC is faced with falling unemployment and rising inflation, its preferred policy response is also clear: The committee will raise its target for the federal funds rate in order to slow the growth of aggregate demand, which will reduce the inflation rate.

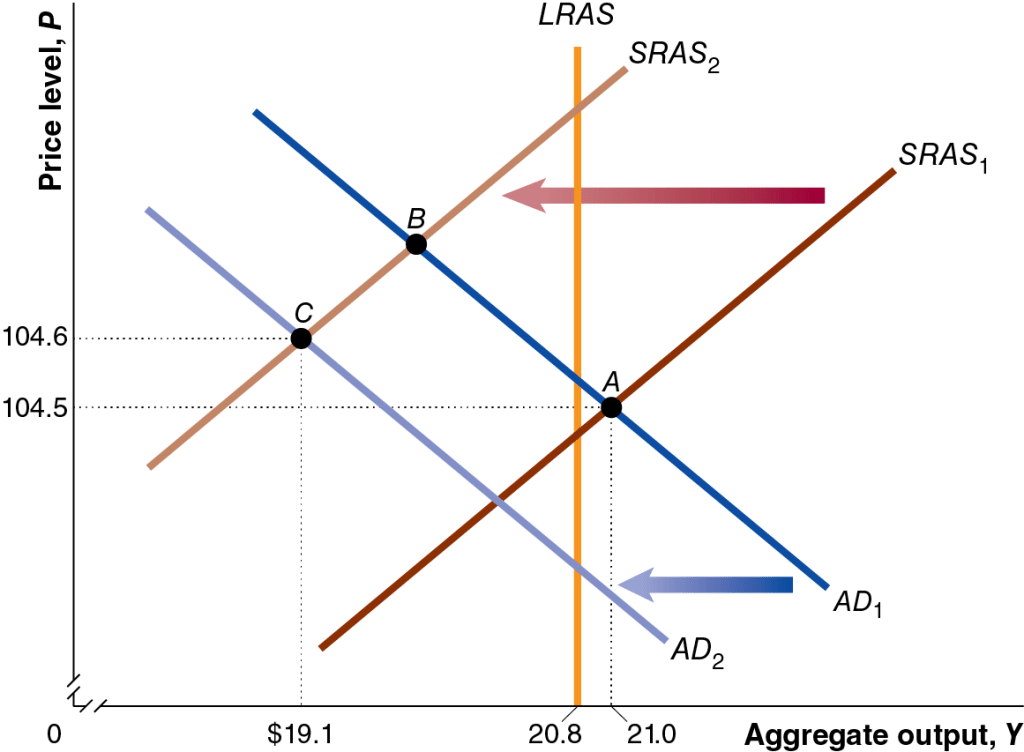

But when the Fed faces an aggregate supply shock, its preferred policy response is unclear. An aggregate supply shock, such as the U.S. economy experienced during the Covid pandemic and again with the tariff increases that the Trump administration began implementing in April, will shift the short-run aggregate supply curve (SRAS) will shift to the left, causing an increase in the price level, along with a decline in real GDP and employment. This combination of rising unemployment and inflation is called stagflation. In this situation, the FOMC faces a policy dilemma: Raising the target for the federal funds rate will help reduce inflation, but will likely increase unemployment, while lowering the target for the federal funds rate will lead to lower unemployment, but will likely increase inflation. The following figure shows the situation during the Covid pandemic when the economy experienced both an aggregate demand and aggregate supply shock. The aggregate demand curve and the aggregate supply curve both shifted to the left, resulting in falling real GDP (and employment) and a rising price level.

Step 4: Answer part c. by explaining what it means to refer to the effect of tariffs on inflation being a “one-time bump.” Tariffs cause the aggregate supply curve to shift to the left because by increasing the prices of raw materials and other inputs, they increase the production costs of some businesses. Assuming that tariffs are not continually increasing, their effect on the price level will end once the production costs of firms stop rising.

Step 5: Answer part d. by explaining what the author means by the FOMC engaing in “risk management,” explaining what a “downshift” in the labor is, and whether if the FOMC is more concerned about a downshift in the labor market than in inflation, it will raise or lower its target for the federal funds rate. The article refers to the “possibility” of a further downshift in the labor market. A downshift in the labor market means that the demand for labor may decline, raising the unemployment rate. Managing the risk of this possibility would involve concentrating on the maximum employment part of the Fed’s dual mandate by lowering its target for the federal funds rate. Note that the expectation that the effect of tariffs on the price level is a one-time bump makes it easier for the committee to focus on the maximum employment part of its mandate because the increase in inflation due to the tariff increases won’t persist.

Photo of Fed Chair Jerome Powell from federalreserve.gov

Today’s meeting of the Federal Reserve’s policymaking Federal Open Market Committee (FOMC) occurred against a backdrop of President Trump pressuring the committee to reduce its target for the federal funds rate. In a controversial move, Trump nominated Stephen Miran, chair of Council of Economic Advisers (CEA), to fill an open seat on the Fed’s Board of Governors. Miran took a leave of absence from the CEA rather than resign his position, which made him the first member of the Board of Governors in decades to maintain an appointment elsewhere in the executive branch while serving on the Board. In addition, Trump had fired Governor Lisa Cook on the grounds that she had committed fraud in applying for a mortgage at a time before her appointment to the Board. Cook denied the charge and a federal appeals court sustained an injunction allowing her to participate in today’s meeting.

As most observers had expected, the committee decided today to lower its target for the federal funds rate from a range of 4.25 percent to 4.50 percent to a range of 4.00 percent to 4.25 percent—a cut of 0.25 percentage point, or 25 basis points. The members of the committee voted 11 to 1 for the 25 basis point cut with Miran dissenting because he preferred a 50 basis point cut.

The following figure shows, for the period since January 2010, the upper bound (the blue line) and lower bound (the green line) for the FOMC’s target range for the federal funds rate and the actual values of the federal funds rate (the red line) during that time. Note that the Fed has been successful in keeping the value of the federal funds rate in its target range. (We discuss the monetary policy tools the FOMC uses to maintain the federal funds rate in its target range in Macroeconomics, Chapter 15, Section 15.2 (Economics, Chapter 25, Section 25.2).)

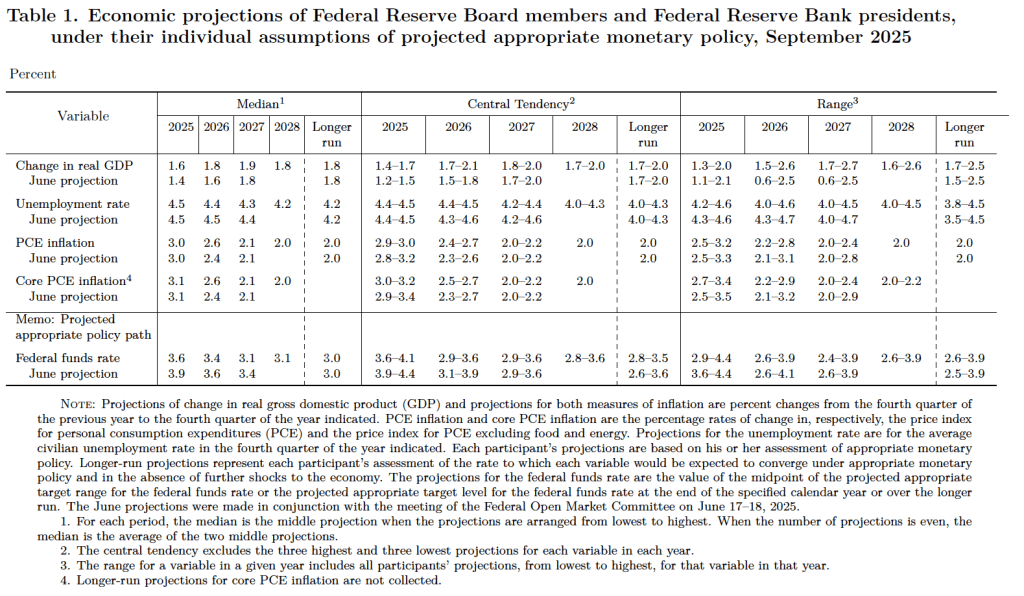

After the meeting, the committee also released a “Summary of Economic Projections” (SEP)—as it typically does after its March, June, September, and December meetings. The SEP presents median values of the 19 committee members’ forecasts of key economic variables. The values are summarized in the following table, reproduced from the release. (Note that only 5 of the district bank presidents vote at FOMC meetings, although all 12 presidents participate in the discussions and prepare forecasts for the SEP.)

There are several aspects of these forecasts worth noting:

Committee members slightly increased their forecasts of real GDP growth for each year from 2025 through 2027. Committee members also slightly decreased their forecasts of the unemployment rate in 2026 and 2027. They left their forecast of unemployment in the fourth quarter of 2025 unchanged at 4.5 percent. (The unemployment rate in August was 4.3 percent.)

Committee members left their forecasts for personal consumption expenditures (PCE) price inflation unchanged for 2025 and 2026, while raising their forecast for 2026 from 2.4 percent to 2.6 percent. Similarly, their forecasts of core PCE inflation were unchanged for 2025 and 2027 but increased from 2.4 percent to 2.6 percent for 2026. The committee does not expect that PCE inflation will decline to the Fed’s 2 percent annual target until 2028.

The committee’s forecast of the federal funds rate at the end of 2025 was lowered from 3.9 percent in June to 3.6 percent today. They also lowered their forecast for federal funds rate at the end of 2026 from 3.6 percent to 3.4 pecent and at the end of 2027 from 3.4 percent to 3.1 percent.

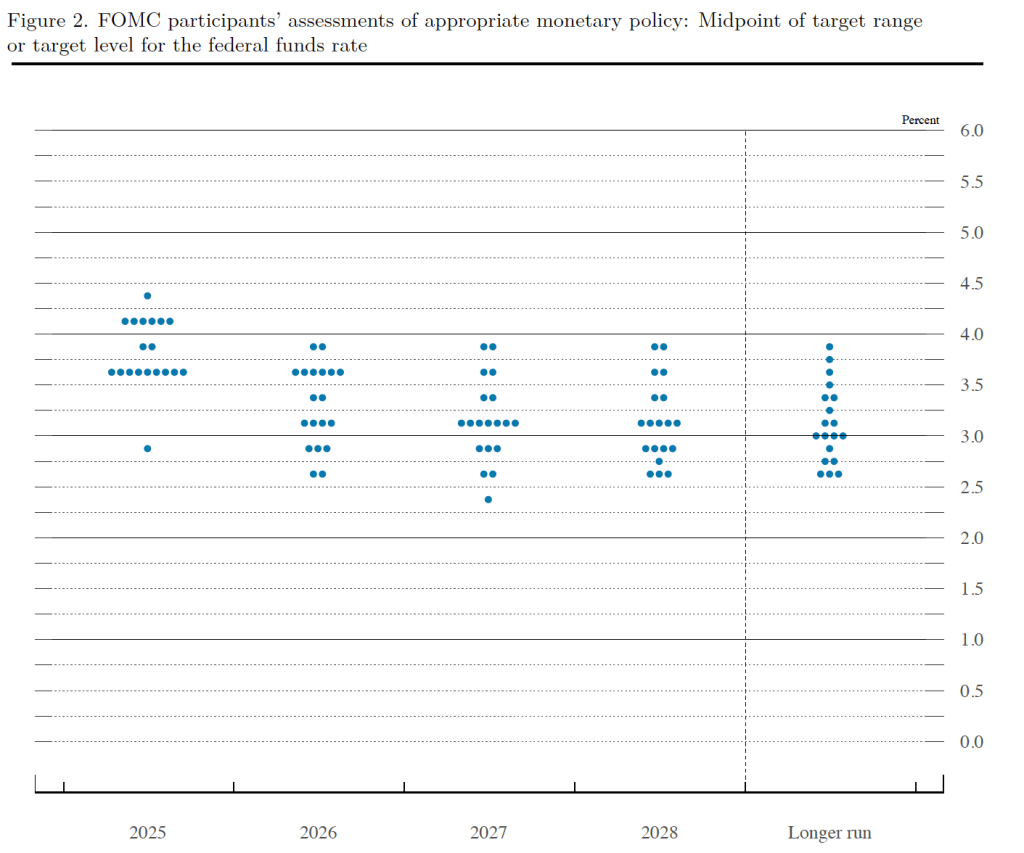

Prior to the meeting there was much discussion in the business press and among investment analysts about the dot plot, shown below. Each dot in the plot represents the projection of an individual committee member. (The committee doesn’t disclose which member is associated with which dot.) Note that there are 19 dots, representing the 7 members of the Fed’s Board of Governors and all 12 presidents of the Fed’s district banks.

The plots on the far left of the figure represent the projections of each of the 19 members of the value of the federal funds rate at the end of 2025. Ten of the 19 members expect that the committee will cut its target range for the federal funds rate by at least 50 basis points in its two remaining meetings this year. That narrow majority makes it likely that an unexpected surge in inflation during the next few months might result in the target range being cut by only 25 basis points or not cut at all. Members of the business press and financial analysts are expecting tht the committee will implement a 25 basis point cut in each of its last two meetings this year.

During his press conference following the meeting, Powell indicated that the recent increase in inflation was largely due to the effects of the increase in tariff rates that the Trump administration began implementing in April. (We discuss the recent data on inflation in this post.) Powell indicated that committee members expect that the tariff increases will cause a one-time increase in the price level, rather than causing a long-term increase in the inflation rate. Powell also noted recent slow growth in real GDP and employment. (We discuss the recent employment data in this blog post.) As a result, he said that the shift in the “balance of risks” caused the committee to believe that cutting the target for the federal funds rate was warranted to avoid the possibility of a significant rise in the unemployment rate.

The next FOMC meeting is on October 28–29 by which time the status of Lisa Cook on the committee may have been clarified. It also seems likely that President Trump will have named the person he intends to nominate to succeed Powell as Fed chair when Powell’s term ends on May 15, 2026. (Powel’s term on the Board doesn’t end until January 31, 2028, although Fed chairs typically resign from the Board if they aren’t reappointed as chair). And, of course, additional data on inflation and unemployment will also have been released.

Today (September 11), the Bureau of Labor Statistics (BLS) released its report on the consumer price index (CPI) for August. The following figure compares headline CPI inflation (the blue line) and core CPI inflation (the red line).

The headline inflation rate, which is measured by the percentage change in the CPI from the same month in the previous year, was 2.9 percent in August, up from 2.7 in July.

The core inflation rate,which excludes the prices of food and energy, was 3.1 percent in August, up slightly from 3.0 percent in July.

Headline inflation and core inflation were both the same as economists surveyed had expected.

In the following figure, we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year. Calculated as the 1-month inflation rate, headline inflation (the blue line) jumped from 2.4 percent in July to 4.7 percent in August. Core inflation (the red line) increased from 3.9 percent in July to 4.2 percent in August.

The 1-month and 12-month inflation rates are both indicating that inflation accelerated in August. Core inflation—which is often a good indicator of future inflation—in particular has been running well above the Fed’s 2 percent inflation target during the last two months.

Of course, it’s important not to overinterpret the data from a single month. The figure shows that the 1-month inflation rate is particularly volatile. Also note that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI, to evaluate whether it is hitting its 2 percent annual inflation target.

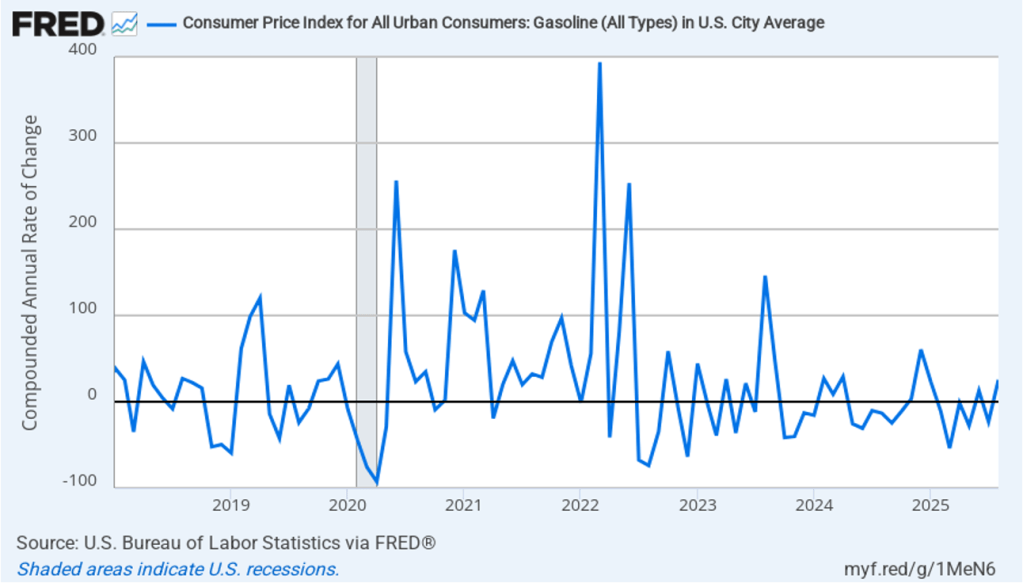

Core inflation had been running significantly higher than headline inflation in the past few months because gasoline prices had generally been falling since February. Gasoline prices turned around in August, however, increasing at a 25.5 percent annual rate. As shown in the following figure, 1-month inflation in gasoline prices moves erratically—which is the main reason that gasoline prices aren’t included in core inflation.

Does the increase in inflation represent the effects of the increases in tariffs that the Trump administration announced on April 2? (Note that many of the tariff increases announced on April 2 have since been reduced) The following figure shows 12-month inflation in durable goods—such as furniture, appliances, and cars—which are likely to be affected directly by tariffs, and services, which are less likely to be affected by tariffs.. To make recent changes clearer, we look only at the months since January 2022. In August, inflation in durable goods increased to 1.9 percent from 1.2 percent in July. Inflation in services in August was 3.8 percent, unchanged from July.

The following figure shows 1-month inflation in the prices of these products, which may make the effects of tariffs clearer. In August, durable goods inflation was 5.1 percent up from 4.5 percent in July. Service inflation was 3.9 percent in August, down slightly from 4.0 percent in July. Inflation in goods and services both running well above 2 percent is not good news for inflation falling back to the Fed’s 2 percent target in the near future.

To better estimate the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation.

Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates.

Trimmed-mean inflation drops the 8 percent of goods and services with the highest inflation rates and the 8 percent of goods and services with the lowest inflation rates.

The following figure shows that 12-month trimmed-mean inflation (the blue line) was 3.3 percent in August, up slightly from 3.2 July. Twelve-month median inflation (the red line) 3.6 percent in August, unchanged from July.

The following figure shows 1-month trimmed-mean and median inflation. One-month trimmed-mean inflation rose from 2.9 percent in July to 3.2 percent in August. One-month median inflation remained unchanged at 3.4 percent in August. These data are consistent with the view that inflation is running above the Fed’s 2 percent target.

The CPI inflation data combined with the recent jobs data (which we discuss here and here), indicate that the U.S. economy may be entering a period of stagflation—a combination of rising inflation with falling, or stagnating, output. Stagflation poses a policy dilemma for the Fed’s policymaking Federal Open Market Committee (FOMC) because cutting its target for the federal funds rate to increase economic growth and employment may worsen inflation. At this point, it seems likely that the FOMC will “look through” this month’s rising inflation because it may be largely due to one-time price increases caused by tariffs. Committee members have signaled that they are likely to cut their target for the federal funds rate by 0.25 percent (25 basis points) at the conclusion of their meeting on September 16–17 and again at the conclusion of the following meeting on October 28–29.

Today (September 9), the Bureau of Labor Statistics (BLS) issued revised estimates of the increase in employment, as measured by the establishment survey, over the period from April 2024 through March 2025. The BLS had initially estimated that during that period net employment had increased by a total of 1,758,000 or an average of 147,000 jobs per month. The revision lowered this estimate by more than half to a total of 839,000 jobs or an average of only 70,000 net new jobs created per month. The difference between those two monthly averages means that the U.S. economy had generated a total of 919,000 fewer jobs during that period. The revision was larger than the downward revision of 800,000 jobs forecast by economists at Wells Fargo, Comerica Bank, and Pantheon Macroeconomics.

Why does the BLS have to revise its employment estimates? As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1) the initial estimates that the BLS issues each month in its “Employment Situation” reports are based on a sample of 121,000 businesses and government agencies representing 631,000 worksites or “establishments.” The monthly data also rely on estimates of the number of employees at establishments that opened or closed during the month and on employment changes at establishments that failed to respond to the survey. In August or September of each year, the BLS issues revised employment estimates based on data from the Quarterly Census of Employment and Wages (QCEW), which relies on state unemployment insurance tax records. The unemployment tax records are much more comprehensive than the original sample of establishments because nearly all employers are included.

In today’s report, the BLS cited two likely sources of error in their preliminary estimates:

“First, businesses reported less employment to the QCEW than they reported to the CES survey (response error). Second, businesses who were selected for the CES survey but did not respond reported less employment to the QCEW than those businesses who did respond to the CES survey (nonresponse error).”

The preliminary benchmark estimates the BLS released today will be revised again and the final estimates for these months will be released in February 2026. The difference between the preliminary and final benchmark estimates can be substantial. For example, last year, the BLS’s initially preliminary benchmark estimate indicated that the net employment increase from April 2023 to March 2024 had been overestimated by 818,000 jobs. In February 2025, the final benchmark estimate reduced this number to 598,000 jobs.

Although this year’s revision is particularly large in absolute terms—the largest since at least 2001—it still represents only about 0.56 percent of the more than 159.5 million people employed in the U.S. economy. Still the size of this revision is likely to increase political criticism of the BLS.

How will this revision affect the decision by the Federal Open Market Committee (FOMC) at its next meeting on September 16-17 to cut or maintain its target for the federal funds rate? The members of the committee were probably not surprised by the downward revision in the employment estimates, although they may have anticipated that the revision would be smaller. In six of the past seven years, the BLS has revised its estimates of payroll employment downward in its annual preliminary benchmark revision.

As we noted in this recent post, even before the BLS revised its employment estimates downward, recent monthly net employment increases were well below the increases during the first half of the year. There was already a high likelihood that the FOMC intended to cut its target for the federal funds rate at its meeting on September 16–17. The substantial downward revision in the employment data makes a cut at the September meeting nearly a certainty and increases the likelihood that the FOMC will implement a second cut in its target for the federal funds rate at the committee’s meeting on October 28–29.