Image showing scientific research generated by GTP-4o

Note: The following op-ed first appeared in the Wall Street Journal.

The Trump Economic Awakening

Traditional policies like tax cuts, targeted aid and responsible spending can deliver stronger growth.

Political scientists will debate the forces that shaped Donald Trump’s victory, but one thing is clear: Americans yearn for a change in economic policy. Voters have rejected the interventionist policies that brought inflation and high deficits. They want an economic awakening, a new way forward that uses traditional economic policies to achieve Mr. Trump’s goal of more jobs for Americans whose fortunes have been harmed by technological change and globalization.

Any economic path to a successful awakening begins with growth: the engine that powers individual income and our collective ability to support the nation’s defense, economy, education and healthcare industry. To pursue this growth, the new administration should consider at least three measures:

First, by working with Congress, it should build on the successes of the Tax Cuts and Jobs Act of 2017 to make permanent the expensing of business investment. Second, it should increase support for science and defense research, which would have significant spillover to the commercial sector, particularly in space exploration. Third, it should build on this research by constructing applied research centers around the country, linked to regional university and city hubs. Like the land-grant colleges of the 19th century, these centers would generate and distribute knowledge, improving local capabilities in manufacturing and services.

Opportunity is also a pillar of the awakening. Community colleges are an underfunded source of skill-building and mobility. As Austan Goolsbee, Amy Ganz and I proposed in a 2019 report, a modest federal block grant to support community colleges on the supply side—rather than a demand-side emphasis on financial aid—can help these schools push more Americans toward better jobs by working with local employers on skill needs and curriculum development. Targeted aid to places with depressed economic activity can help distribute opportunity to communities better than one-size-fits-all Washington-directed programs.

Corporate tax reform can play a role, too, by improving incentives for companies to settle and invest in the U.S. This can magnify opportunities for Americans, all without having to rely on costly tariffs.

Working a job doesn’t merely generate income; it also promotes human dignity. Enlisting more people into the workforce is thus another element of the economic-policy awakening. While growth and opportunity policies can boost labor-force participation, strengthening the earned-income tax credit to boost the incomes of childless workers can help attract younger people to the workforce. Maintaining the child tax credit can also provide parents with easier pathways toward economic participation.

These ideas share several important themes with Mr. Trump’s campaign and the traditional conservative playbook. They emphasize that policy ideas should be practical and workable, not merely rhetorical. Each makes use of America’s federalist system and innovative ethos. Making a priority of strong local involvement in applied research centers and community colleges and as tailoring place-based aid are more effective approaches than Washington diktats. Programs need to be held accountable for results, not simply allocated money.

This economic-policy awakening requires a clear-eyed assessment of budget trade-offs. Profligate spending with little regard for debt and inflation—à la the American Rescue Plan—contributed to Mr. Trump’s victory. It is possible to accomplish the steps above in a fiscally responsible way by offsetting spending and tax changes.

Organizing for the policy awakening’s success will be essential. Lack of communication among cabinet agencies can stymie creative ideas for expanding the economic pie for American workers. Like the president’s Working Group on Financial Markets, created by Ronald Reagan in 1988 to convene disparate agencies, the new administration would benefit from a senior executive team that can coordinate economic ideas and learn from leaders in business, labor and social services. Such a body, unlike the National Economic Council, could more adeptly cut across silos related to tax, trade, regulatory and industrial policy.

Voters have signaled they’re ready for an economic awakening. The president-elect, equipped with a new playbook and vision, should seize the opportunity.

Daron Acemoglu and Simon Johnson (Credit: Acemoglu, Adam Glanzman; Johnson, courtesy of MIT, from news.mit.edu)

James Robinson (photo from news.uchicago.edu)

Many economic studies have a relatively limited objective. For instance, estimating the price elasticity of demand for soda in order to determine the incidence of a soda tax. Or estimating a Keynesian fiscal policy multiplier in order to determine the effects of a change in federal spending or taxes. (We consider the first topic in Microeconomics, Chapter 6, and the second topic in Macroeconomics, Chapter 16.)

Other economic studies consider much broader questions, such as why are some countries rich and other countries poor? As the late Nobel laureate Robert Lucas once wrote: “The consequences for human welfare involved in questions like these are simply staggering: Once one starts to think about them, it is hard to think about anything else.”

Today, the Royal Swedish Academy of Sciences awarded the 2024 Nobel Prize in Economic Sciences to Daron Acemoglu and Simon Johnson of MIT, and to James Robinson of the University of Chicago for “for studies of how institutions are formed and affect prosperity.” Acemoglu, Johnson, and Robinson (AJR) have published work highlighting the key importance of a country’s institutions in explaining whether the country has experienced sustained economic growth. Their work builds on earlier studies by the late Douglas North of Washington University in St. Louis, who received the Nobel Prize in 1993.

The institutional approach to economic growth differs from other approaches that focus on variables such as temperature, prevalence of disease, ethnic fragmentation, resource endowments, or governments adopting flawed development strategies in explaining differences in growth rates in per capita income across countries.

Two of AJR’s most discussed papers are “The Colonial Origins of Comparative Development: An Empirical Investigation,” which was published in the American Economic Review in 2001 (free download here), “Reversal of Fortune: Geography and Institutions in the Making of the Modern World Income Distribution,” which was published in the Quarterly Journal of Economics in 2002 (available here). In these papers, the authors argue that the institutions European countries established in their colonies helped determine economic growth in those countries even decades after colonization.

As with any analysis that covers many countries over long periods of time, AJR’s analysis of the effect of colonialism on economic growth has attracted critiques focused on whether the authors have gathered data properly and whether their data may be better explained with a different approach.

The authors, writing both separately and jointly, have explored many issues beyond the effects of colonialism on economic growth. The wide scope of their research can be seen by reviewing their curricula vitae, which can be found here, here, and here. The announcement by the Nobel committee can be found here.

Glenn serves on the the Grand Bargain Committee, chaired by Michael Strain of the American Enterprise Institute and Isabel Sawhill of the Brookings Institution. The committee, whose members span the political spectrum, have prepared a report that addresses some of the country’s most pressing economic and social problems.

Glenn and Michael Strain prepared the following introduction to the report. Below there is a link to the whole report.

The views expressed in this report are those of the individual authors who collectively constitute the Grand Bargain Committee, co-chaired by Michael R. Strain and Isabel V. Sawhill. This report was sponsored by the Center for Collaborative Democracy and was prepared independent of influence from the center and from any other outside party or institution. It is being published by the Bipartisan Policy Center as an example of how people with diverse views and political leanings can find common ground. The recommendations are strictly those of the policy experts and do not necessarily reflect the views of any organization or those of the BPC. All data are current as of November 2023.

By: Eric Hanushek, G. William Hoagland, Douglas Holtz-Eakin, R. Glenn Hubbard, Maya MacGuineas, Richard V. Reeves, Robert D. Resichauer, Gerard Robinson, Isabel V. Sawhill, Diane Schanzenbach, Richard Schmalensee, Michael R. Strain, and C. Eugene Steuerle.

Introduction

The United States faces serious economic and social challenges, including:

The underlying economic growth rate has slowed, as have opportunities for people to move up the economic ladder.

Our education system fails too many children and leaves many more with fewer opportunities than they deserve.

The nation is not rising to the challenge of addressing climate change.

Both our health care system and the health of our population need improvement.

Our income tax system is broken, generating tax revenue in an inefficient and unfair manner.

And the national debt is growing at an unsustainable pace, threatening long-term economic growth, crowding out needed investments in economic opportunity, and placing the nation’s ability to respond to a future crisis at risk.

To address these problems, the Center for Collaborative Democracy commissioned subject matter experts—progressives, centrists, and conservatives—to develop a “Grand Bargain” encompassing all six issues. The policy debate typically puts these problems into silos, and within each silo, powerful forces support the status quo. This report seeks to break down these silos. Dealing with them all at once—in a Grand Bargain—is a more promising strategy than dealing with them individually, because it allows for different parties to strike deals across policy issues, not just within a single issue.

For example, implementing a carbon tax to address climate change seems impossibly difficult. So does increasing accountability for teacher performance. Trading one for the other might be easier than pursuing both in isolation. Fixing the structural budget deficit by reducing entitlement spending is an enormous political challenge. So is increasing spending on programs that advance economic opportunity. Doing both at the same time could be more politically feasible than addressing them separately.

In this context, the group of experts met for several months in 2023 to share perspectives and ideas and to come up with sensible policies in each of these areas: economic growth and mobility; education; environment; health; taxes; and the federal budget. The end result is this report, which is being published by the Bipartisan Policy Center as an example of how people with diverse views and political leanings can find common ground.

This report is short, consisting of less than 30 pages of text. Its brevity is by design. This constraint forced the group to stay focused on issues and recommendations that matter the most. The focus of the report is on concepts. It is designed to answer such questions as, “How should the nation’s approach to education or to the federal budget change? What fundamental reforms are required to increase the underlying rates of economic growth and upward mobility?” Focusing on concepts means not focusing on policy details, including the details of implementing our recommendations and of transitioning across policy regimes. Our lack of attention to policy details does not mean we do not recognize their importance. Of course, we do, and many members of the group have spent much of their careers studying and designing public policies. Instead, we focus on concepts because we believe the United States needs to return to a discussion of first principles. This report advances that objective.

Not every member of the group agrees with every recommendation in this report. That is not surprising given the diversity of views in the group, and the difficulty and complexity of many of the issues we address. Despite this disagreement, we were able to have an informed and constructive discussion about these economic issues, to find compromises, and to come up with a set of recommendations that we believe, on balance, would greatly strengthen the country and improve people’s lives.

We believe in the importance of a market economy. Free markets have led to unprecedented growth and innovation, along with rising incomes, over the past three centuries. But government also has a role to play. To unleash more growth, we need to curtail unneeded or overly costly regulations and to create a tax system that encourages investment spending and innovation. To bring prosperity to more people, we need policies that will enable more people to benefit from economic growth through investment in their education and skills. For this reason, we put a great deal of emphasis on improving education for children, on training or retraining for adult workers, and on subsidizing the earnings of low-wage workers when necessary while maintaining a safety net for those who cannot work.

Our proposals are designed to advance certain underlying values and themes: Work and savings should be rewarded, investment should be encouraged over consumption, public assistance should be better targeted to those most in need, the tax system should be more progressive, and the nation should invest relatively more in the young and spend relatively less on the elderly.

Our specific proposals in each area are as follows:

On economic growth and mobility, we recommend investing in the education and training of workers, through community colleges and apprenticeships. We call for a more skill-based immigration system and for more immigrants; for encouraging innovation by investing more in basic research; for reducing taxes on new investment; for curbing unneeded regulation; for reducing the national debt; and for encouraging participation in economic life by increasing the generosity of earnings subsidies for low-wage workers.

On education, we recommend improving the teacher workforce at the K-12 level; paying teachers more but strengthening the link between pay and performance; maintaining educational standards and accountability while narrowing gaps by race and class; expanding school choice; and recognizing the role that parents and families must play in students’ learning.

On the environment, our main recommendation is to adopt a carbon tax. We also call for reducing methane emissions; expanding federal authority in the planning, siting, and permitting of the national electric transmission system; and repealing the renewable fuel standard that requires refiners to blend corn ethanol into the fuel they sell.

On health, we call for giving more attention to the social determinants of poor health with a focus on the need for better nutrition, for rationalizing existing subsidies for health care, and for reducing health care costs.

On taxes, we call for increasing tax revenue as a share of annual gross domestic product (GDP), and for that revenue to be raised in a manner that is more progressive, efficient, and simple than under current law, while also increasing the incentive to save and invest. For the business sector, that means allowing the expensing of investment expenditures and moving toward equal treatment of the corporate and noncorporate sectors.

On the federal budget, we recommend putting the debt as a share of annual GDP on a sustainable trajectory with a comprehensive package of reforms made up of a rough balance between tax increases and spending cuts in the initial years, phasing into a much larger share of the savings coming from spending cuts over time.

Most of these recommendations are at the federal level, but some are at the state and local level, particularly our education recommendations.

In the spirit of a Grand Bargain, these recommendations advance common goals and values through compromises both within and across policy areas. For example, one of our values is reflected in the goal of refocusing government spending on those who truly need it, and another is to restore fiscal responsibility. To accomplish this, we call for slower growth in Social Security and Medicare benefits for affluent seniors to reduce the major driver of the national debt, but we also protect vulnerable seniors and spend more on the education of children and on earnings subsidies for the working poor. We recommend adopting a carbon tax because it will simultaneously advance our goals of supporting the environment, increasing tax revenue, and boosting dynamism by encouraging innovation in the energy sector.

We believe the analysis and recommendations in this report point a path forward for the nation, but we offer them in a spirit of humility, understanding that others will disagree. We hope that this report catalyzes a much needed debate about the future of our nation.

Glenn discusses Fed policy, the state of the U.S economy, economic growth, China in the world economy, industrial policy, protectionism, and other topics in this episode of the Political Economy podcast from the American Enterprise Institute.

This op-ed orginally appeared in the Wall Street Journal.

Put Growth Back on the Political Agenda

In a campaign season dominated by the past, a central economic topic is missing: growth. Rapid productivity growth raises living standards and incomes. Resources from those higher incomes can boost support for public goods such as national defense and education, or can reconfigure supply chains or shore up social insurance programs. A society without growth requires someone to be worse off for you to be better off. Growth breaks that zero-sum link, making it a political big deal.

So why is the emphasis on growth fading? More than economics is at play. While progress from technological advances and trade generally is popular, the disruption that inevitably accompanies growth and hits individuals, firms and communities has many politicians wary. Such concerns can lead to excessive meddling via industrial policy.

As we approach the next election, the stakes for growth are high. Regaining the faster productivity that prevailed before the global financial crisis requires action. The nonpartisan Congressional Budget Office estimates potential gross domestic product growth of 1.8% over the coming decade, and somewhat lower after that. Those figures are roughly 1 percentage point lower than the growth rate over the three decades before the pandemic. Many economists believe productivity gains from generative artificial intelligence can raise growth in coming decades. But achieving those gains requires an openness to change that is rare in a political climate stuck in past grievances about disruption—the perennial partner of growth.

Traditionally, economic policy toward growth emphasized support for innovation through basic research. Growth also was fostered by reducing tax burdens on investment, streamlining regulation (which has proliferated during the Biden administration) and expanding markets. These important actions have flagged in recent years. But such attention, while valuable, masks inattention to adverse effects on some individuals and communities, raising concerns about whether open markets advance broad prosperity.

This opened a lane for backward-looking protectionism and industrial policy from Democrats and Republicans alike. Absent strong national-defense arguments (which wouldn’t include tariffs on Canadian steel or objections to Japanese ownership of a U.S. steel company), protectionism limits growth. According to polls by the Chicago Council on Global Affairs, roughly three-fourths of Americans say international trade is good for the economy. Finally, protectionism belies ways in which gains from openness may be preserved, such as by simultaneously offering support for training and work for communities of individuals buffeted by trade and technological change.

On industrial policy, it is true that markets can’t solve every allocation problem. But such concerns underpin arguments for greater federal support of research for new technologies in defense, climate-change mitigation, and private activity, not micromanaged subsidies to firms and industries. If a specific defense activity merits assistance, it could be subsidized. These alternatives mitigate the problems in conventional industrial policy of “winner picking” and, just as important, the failure to abandon losers. It is policymakers’ hyperattention to those buffeted by change that hampers policy effectiveness and, worse, invites rent-seeking behavior and costly regulatory micromanagement.

Examples abound. Appending child-care requirements to the Chips Act and the inaptly named Inflation Reduction Act has little to do with those laws’ industrial policy purpose. The Biden administration’s opposition to Nippon Steel’s acquisition of U.S. Steel raises questions amid the current wave of industrial policy. How is a strong American ally’s efficient operation of an American steel company with U.S. workers an industrial-policy problem? Flip-flops on banning TikTok fuel uncertainty about business operations in the name of industrial policy.

The wrongly focused hyperattention is supposedly grounded in putting American workers first. But it raises three problems. First, the interventions raise the cost of investments, and the jobs they are to create or protect, by using mandates and generating policy uncertainty. Second, they contradict the economic freedom in market economies of voluntary transactions. Absent a strong national-security foundation, why is public policy directing investment in or ownership of assets? Such policies threaten the nation’s long-term prosperity by discouraging investment and invite rent-seeking in a way that voluntary market transactions don’t. Both problems hamstring growth.

Third, and perhaps most important, such micromanagement misses the economic and political mark of actually helping individuals and communities disrupted by growth-enhancing openness. A more serious agenda would focus on training suited to current markets (through, for example, more assistance to community colleges), on work (through expanding the Earned Income Tax Credit), and on aid to communities hit by prolonged employment loss (through services that enhance business formation and job creation). The federal government could also establish research centers around the country to disseminate ideas for businesses.

Growth matters—for individual livelihoods, business opportunities and public finances. Pro-growth policies that account for disruption’s effects while encouraging innovation, saving, capital formation, skill development and limited regulation must return to the economic agenda. A shift to prospective, visionary thinking would reorient the bipartisan, backward-looking protectionism and industrial policy that weaken growth and fail to address disruption.

Recent articles in the business press have discussed the possibility that the U.S. economy is entering a period of higher growth in labor productivity:

“US Productivity Is on the Upswing Again. Will AI Supercharge It?” (link)

“Can America Turn a Productivity Boomlet Into a Boom?” (link)

In Macroeconomics, Chapter 16, Section 16.7 (Economics, Chapter 26, Section 26.7), we highlighted the role of growth in labor productivity in explaining the growth rate of real GDP using the following equations. First, an identity:

Real GDP = Number of hours worked x (Real GDP/Number of hours worked),

where (Real GDP/Number of hours worked) is labor productivity.

And because an equation in which variables are multiplied together is equal to an equation in which the growth rates of these variables are added together, we have:

Growth rate of real GDP = Growth rate of hours worked + Growth rate of labor productivity

From 1950 to 2023, real GDP grew at annual average rate of 3.1 percent. In recent years, real GDP has been growing more slowly. For example, it grew at a rate of only 2.0 percent from 2000 to 2023. In February 2024, the Congressional Budget Office (CBO) forecasts that real GDP would grow at 2.0 percent from 2024 to 2034. Although the difference between a growth rate of 3.1 percent and a growth rate of 2.0 percent may seem small, if real GDP were to return to growing at 3.1 percent per year, it would be $3.3 trillion larger in 2034 than if it grows at 2.0 percent per year. The additional $3.3 trillion in real GDP would result in higher incomes for U.S. residents and would make it easier for the federal government to reduce the size of the federal budget deficit and to better fund programs such as Social Security and Medicare. (We discuss the issues concerning the federal government’s budget deficit in this earlier blog post.)

Why has growth in real GDP slowed from a 3.1 percent rate to a 2.0 percent rate? The two expressions on the right-hand side of the equation for growth in real GDP—the growth in hours worked and the growth in labor productivity—have both slowed. Slowing population growth and a decline in the average number of hours worked per worker have resulted in the growth rate of hours worked to slow substantially from a rate of 2.0 percent per year from 1950 to 2023 to a forecast rate of only 0.4 percent per year from 2024 to 2034.

Falling birthrates explains most of the decline in population growth. Although lower birthrates have been partially offset by higher levels of immigration in recent years, it seems unlikely that birthrates will increase much even in the long run and levels of immigration also seem unlikely to increase substantially in the future. Therefore, for the growth rate of real GDP to increase significantly requires increases in the rate of growth of labor productivity.

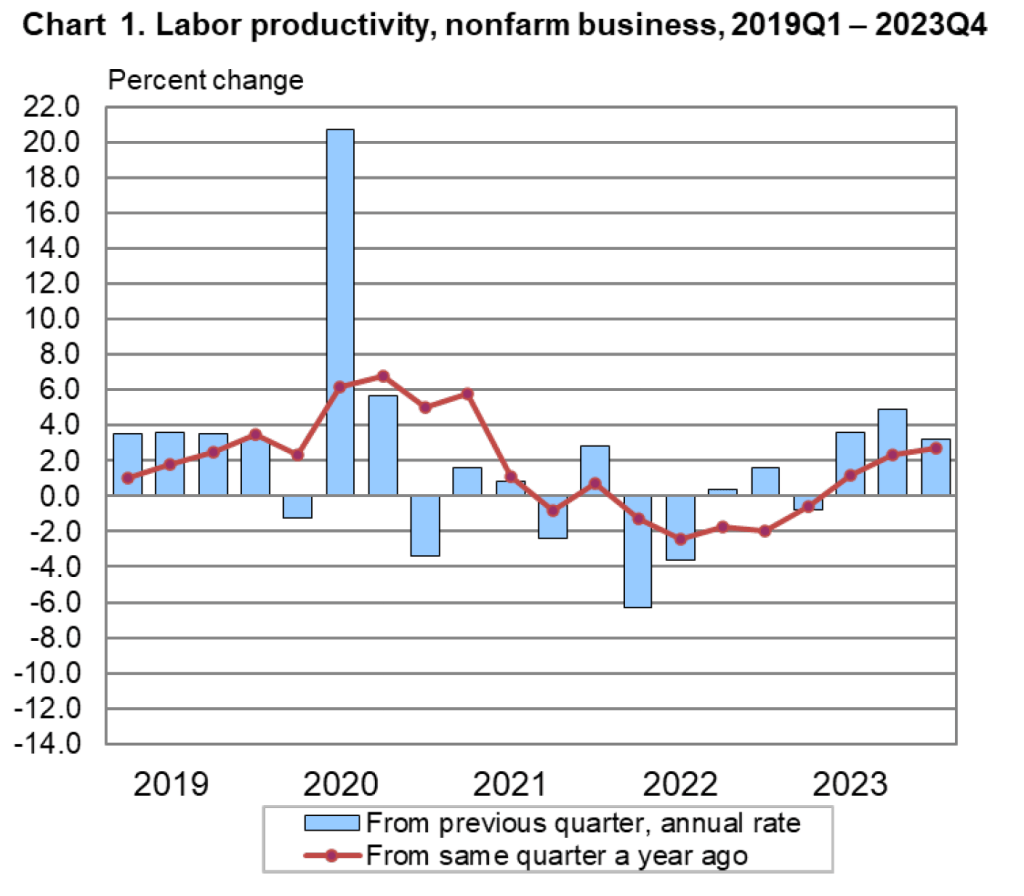

The Bureau of Labor Statistics (BLS) publishes quarterly data on labor productivity. (Note that the BLS series is for labor productivity in the nonfarm business sector rather than for the whole economy. Output of the nonfarm business sector excludes output by government, nonprofit businesses, and households. Over long periods, growth in real GDP per hour worked and growth in real output of the nonfarm business sector per hour worked have similar trends.) The following figure is taken from the BLS report “Productivty and Costs,” which was released on February 1, 2024.

Note that the growth in labor productivity increased during the last three quarters of 2023, whether we measure the growth rate as the percentage change from the same quarter in the previous year or as growth in a particular quarter expressed as anual rate. It’s this increase in labor productivity during 2023 that has led to speculation that labor productivity might be entering a period of higher growth. The following figure shows labor productivity growth, measured as the percentage change from the same quarter in the previous year for the whole period from 1950 to 2023.

The figure indicates that labor productivity has fluctuated substantially over this period. We can note, in particular, productivity growth during two periods: First, from 2011 to 2018, labor productivity grew at the very slow rate of 0.9 percent per year. Some of this slowdown reflected the slow recovery of the U.S. economy from the Great Recession of 2007-2009, but the slowdown persisted long enough to cause concern that the U.S. economy might be entering a period of stagnation or very slow growth.

Second, from 2019 through 2023, labor productivity went through very large swings. Labor productivity experienced strong growth during 2019, then, as the Covid-19 pandemic began affecting the U.S. economy, labor productivity soared through the first half of 2021 before declining for five consecutive quarters from the first quarter of 2022 through the first quarter of 2023—the first time productivity had fallen for that long a period since the BLS first began collecting the data. Although these swings were particularly large, the figure shows that during and in the immediate aftermath of recessions labor productivity typically fluctuates dramatically. The reason for the fluctuations is that firms can be slow to lay workers off at the beginning of a recession—which causes labor productivity to fall—and slow to hire workers back during the beginning of an economy recovery—which causes labor productivity to rise.

Does the recent increase in labor productivity growth represent a trend? Labor productivity, measured as the percentage change since the same quarter in the previous year, was 2.7 percent during the fourth quarter of 2023—higher than in any quarter since the first quarter of 2021. Measured as the percentage change from the previous quarter at an annual rate, labor productivity grew at a very high average rate of 3.9 during the last three quarters of 2023. It’s this high rate that some observers are pointing to when they wonder whether growth in labor productivity is on an upward trend.

As with any other economic data, you should use caution in interpreting changes in labor productivity over a short period. The productivity data may be subject to large revisions as the two underlying series—real output and hours worked—are revised in coming months. In addition, it’s not clear why the growth rate of labor productivity would be increasing in the long run. The most common reasons advanced are: 1) the productivity gains from the increase in the number of people working from home since the pandemic, 2) businesses’ increased use of artificial intelligence (AI), and 3) potential efficiencies that businesses discovered as they were forced to operate with a shortage of workers during and after the pandemic.

To this point it’s difficult to evaluate the long-run effects of any of these factors. Wconomists and business managers haven’t yet reached a consensus on whether working from home increases or decreases productivity. (The debate is summarized in this National Bureau of Economic Research Working Paper, written by Jose Maria Barrero of Instituto Tecnologico Autonomo de Mexico, and Steven Davis and Nicholas Bloom of Stanford. You may need to access the paper through your university library.)

Many economists believe that AI is a general purpose technology (GPT), which means that it may have broad effects throughout the economy. But to this point, AI hasn’t been adopted widely enough to be a plausible cause of an increase in labor productivity. In addition, as Erik Brynjolfsson and Daniel Rock of MIT and Chad Syverson of the University of Chicago argue in this paper, the introduction of a GPT may initially cause productivity to fall as firms attempt to use an unfamiliar technology. The third reason—efficiency gains resulting from the pandemic—is to this point mainly anecdotal. There are many cases of businesses that discovered efficiencies during and immediately after Covid as they struggled to operate with a smaller workforce, but we don’t yet know whether these cases are sufficiently common to have had a noticeable effect on labor productivity.

So, we’re left with the conclusion that if the high labor productivity growth rates of 2023 can be maintained, the growth rate of real GDP will correspondingly increase more than most economists are expecting. But it’s too early to know whether recent high rates of labor productivty growth are sustainable.

Glenn participated in this session hosted by the Society of Policy Modeling and the American Economic Association of Economic Educators and moderated by Dominick Salvatore of Fordham University. (Link to the page for this session in the ASSA program.)

Also making presentations at the session were Robert Barro of Harvard University, Janice Eberly of Northwestern University, Kenneth Rogoff of Harvard University, and John Taylor of Stanford University.

Here is the abstract for Glenn’s presentation:

Economic growth is foundational for living standards and as an objective for economic policy. The emergence of Artificial Intelligence as a General Purpose Technology, on the one hand, and a number of demographic and budget challenges, on the other hand, generate an unusually wide range of future economic outcomes. I focus on key ‘policy’ and ‘political economy’ considerations that increase the likelihood of a more favorable growth path given pre-existing trends and technological possibilities. By ‘policy,’ I consider mechanisms enabling growth through research, taxation, the scope of regulation, and competition. By ‘political economy’ factors, I consider mechanisms to increase economic participation in support of growth and policies that enhance it. I argue that both sets of mechanisms are necessary for a viable pro-growth economic policy framework.

These slides from the presentation highlight some of Glenn’s key points. (Note the cover of the new 9th edition of the textbook in slide 7!)

Bust of the Roman Emperor Vespasian. (Photo from en.wikipedia.org.)

Some people worry that advances in artificial intelligence (AI), particularly the development of chatbots will permanently reduce the number of jobs available in the United States. Technological change is often disruptive, eliminating jobs and sometimes whole industries, but it also creates new industries and new jobs. For example, the development of mass-produced, low-priced automobiles in the early 1900s wiped out many jobs dependent on horse-drawn transportation, including wagon building and blacksmithing. But automobiles created many new jobs not only on automobile assembly lines, but in related industries, including repair shops and gas stations.

Over the long run, total employment in the United States has increased steadily with population growth, indicating that technological change doesn’t decrease the total amount of jobs available. As we discuss in Microeconomics, Chapter 16 (also Economics, Chapter 16), fears that firms will permanently reduce their demand for labor as they increase their use of the capital that embodies technological breakthroughs, date back at least to the late 1700s in England, when textile workers known as Luddites—after their leader Ned Ludd—smashed machinery in an attempt to save their jobs. Since that time, the term Luddite has described people who oppose firms increasing their use of machinery and other capital because they fear the increases will result in permanent job losses.

Economists believe that these fears often stem from the lump-of-labor fallacy, which holds that there is only a fixed amount of work to be performed in the economy. So the more work that machines perform, the less work that will be available for people to perform. As we’ve noted, though, machines are substitutes for labor in some uses—such as when chatbot software replace employees who currently write technical manuals or computer code—they are also complements to labor in other jobs—such as advising firms on how best to use chatbots.

The lump-of-labor fallacy has a long history, probably because it seems like common sense to many people who see the existing jobs that a new technology destroys, without always being aware of the new jobs that the technology creates. There are historical examples of the lump-of-labor fallacy that predate even the original Luddites.

For instance, in his new book Pax: War and Peace in Rome’s Golden Age, the British historian Tom Holland (not to be confused with the actor of the same name, best known for portraying Spider-Man!), discusses an account by the ancient historian Suetonius of an event during the reign of Vespasian who was Roman emperor from 79 A.D. to 89 A.D. (p. 201):

“An engineer, so it was claimed, had invented a device that would enable columns to be transported to the summit of the [Roman] Capitol at minimal cost; but Vespasian, although intrigued by the invention, refused to employ it. His explanation was a telling one. ‘I have a duty to keep the masses fed.’”

Vespasian had fallen prey to the lump-of-labor fallacy by assuming that eliminating some of the jobs hauling construction materials would reduce the total number of jobs available in Rome. As a result, it would be harder for Roman workers to earn the income required to feed themselves.

Note that, as we discuss in Macroeconomics, Chapters 10 and 11 (also Economics, Chapter 20 and 21), over the long-run, in any economy technological change is the main source of rising incomes. Technological change increases the productivity of workers and the only way for the average worker to consume more output is for the average worker to produce more output. In other words, most economists agree that the main reason that the wages—and, therefore, the standard of living—of the average worker today are much higher than they were in the past is that workers today are much more productive because they have more and better capital to work with.

Although the Roman Empire controlled most of Southern and Western Europe, the Near East, and North Africa for more than 400 years, the living standard of the average citizen of the Empire was no higher at the end of the Empire than it had been at the beginning. Efforts by emperors such as Vespasian to stifle technological progress may be part of the reason why.

Adam Smith bronze statue on Royal Mile Market square in front of Saint Gilles Cathedral in Edinburgh, Scotland.

Growth matters. A lot. A slightly higher rate of economic growth, sustained over time, can make the difference between a big increase in living standards and relative stagnation. Whether we can still generate strong and steady growth is a “$64,000 question” for the economy — the question. Nobel Prize–winning economist Robert Lucas famously observed that once economists think of long-term growth, it is hard to think of anything else. A pro-growth policy agenda is a good idea because growth is a good idea.

But a deeper question remains: Is public support for growth guaranteed? Oren Cass of American Compass refers to growth and economists’ fealty to economic participation for all as “economic piety.” This critique resonates for a simple reason: Forces that propel growth invariably leave a wake of economic disruption for people in many places and political disruption for the nation. A serious discussion of pro-growth policy must account for that disruption.

A conventional pro-growth policy agenda can be enhanced by support for openness to markets, ideas, and new ways of doing things, and for the ability of firms to adapt to change. Such an enhanced agenda would center on infrastructure broadly defined, development and dissemination of better management practices, and reduced barriers to competition.

Yet the political process, and even many a conservative, is openly skeptical of such an agenda. This skepticism is rooted not in disagreement over the future of scientific advances or of organizational adaptation — but in a concern that growth’s benefits be shared broadly. Addressing this skepticism head-on is essential for rebuilding social support for growth and for countering well-meaning but potentially harmful policies.

The system that needs defending is a mature and successful one. Adam Smith, the great proponent of the “invisible hand” (not the visible hand of a state-directed economy), saw openness and competition as worth the candle. His 1776 publication of The Wealth of Nations came before what we would recognize today as industrial capitalism, though technological change and globalization were features of economic debates in the aftermath of Smith’s ideas.

Smith’s radical insight is central to economic policy today: National prosperity (the “wealth of a nation”) is represented by consumption of goods and services by its people — i.e., their living standards. The goal of the economy in Smith’s telling was to make the economic pie as large as possible. His advocacy of free markets and competition rested on their ability to boost consumption possibilities.

Two centuries later, Nobel laureates Kenneth Arrow and Gérard Debreu added the jargon and mathematics of contemporary economics to formalize Smith’s intuition. While individuals and firms act independently, competitive markets lead to an efficient allocation of resources and a maximized economic pie. Friedrich Hayek, another Nobel laureate, hailed the virtue of a decentralized competitive price system in maximizing economic activity.

Smith’s radicalism draws from his attack on mercantilism—the economic orthodoxy of the day—which stressed a zero-sum view of trade and state intervention to promote and protect certain firms and industries. (Sound familiar?) His second radical insight was that the “nation” did not mean the sovereign and the well-connected. In Smith’s view, individuals as consumers—all people—were kings. Finally, channeling the sympathetic concern espoused in his earlier classic, The Theory of Moral Sentiments, Smith championed mass participation in the productive economy as a precondition for human flourishing.

It is fair to say that Smith lacked a theory of per capita growth in the economy over time; indeed, he wrote before the massive increase in living standards attendant upon the Industrial Revolution. After 1800, per capita income in the United Kingdom — and the United States — witnessed a 30-fold increase. There have also been major improvements in the quality of goods and services that such a statistic doesn’t quite capture. And, of course, many of today’s offerings — from smartphones to computers to air-conditioning — were not available even in 1900, let alone 1800.

That lacuna in Smith’s theory partly reflects technical difficulties in modeling growth. Higher output can come from growth in inputs such as labor and capital, but what determines their growth? Today’s economists highlight population growth and society’s willingness to work, save, and invest. Still more important is growth in productivity, or the efficiency with which inputs are used to produce goods and services.

Smith’s pin-factory example — in which output rose with the specialization of tasks — links how things are done with the level of productivity. But what factors determine productivity growth over time? Today’s economic analysis focuses on technology and the process of generating ideas. Since economic growth is still crucial for people seemingly marginalized by capitalism, it’s worth asking whether the economic foundations expressed in The Wealth of Nations are still relevant today. Where does growth come from now? And do those sources still require openness and competition?

The short answer is that they do, but to see why, we need to focus on the ideas of two prominent economists after 1800: Edmund Phelps and Deirdre Nansen McCloskey.

Phelps, a Nobel laureate, has done much to connect growth to Smith’s foundational ideas. He starts with Smith’s emphasis on a great many individuals (not the state or privileged firms) searching for new and better ways of doing things. This relentless search produces innovative ideas, processes, and goods that drive growth — but only if the political economy allows openness. Smith’s messy, “bottom up” version of the market therefore puts mass innovation at the heart of economic growth. Phelps’s argument reflects how Smithian societies committed to openness are best able to prosper and promote growth.

This argument has two important applications. The first is to debunk the sometimes fashionable view of secular productivity decline — that we have run short of new things to discover and exploit. The second is to give an answer to economies struggling with growth in a period of structural changes from technology and globalization. Slowdowns in innovation are likely not due to scientific barrenness but to walls against openness and change — that is, fears of disruption.

Phelps’s concern with economic dynamism draws him to Smith’s arguments against mercantilist tinkering in the economy. Like Smith, he worries about the hidden costs of tinkering with competition by blocking change from the outside and by enabling rent-seeking on the inside. These “corporatist” policies — fashionable among some conservatives at present — inevitably embolden vested interests and cronyism, slowing change and growth. Even seemingly small interventions can subtly diminish innovation, a point to which I’ll return.

Yet such a critique must acknowledge the political consequences of disruption. Dynamism is messy. It creates growth in the aggregate, but with many individual losers as well as individual gainers.

McCloskey, an economic historian, has similarly identified the continuous, large-scale, voluntary, and unfocused search for betterment as the source of new ideas that can produce economic growth. She sees this “innovism” as primarily a cultural force, preferring the term to the more familiar “capitalism,” and connects innovism to economic liberalism. Echoing Smith, she emphasizes how an open economy allows individuals—from the moderately to the spectacularly talented—to “have a go.” This economic liberalism allows competition to enshrine liberty and mass flourishing.

In McCloskey’s telling, growth depends on a liberal tolerance and openness to change, which encourage many people to be alert to opportunity. Sustaining that tolerance as structural shifts bring economic misfortune to many individuals, however, requires more than devotion to Smith.

Therein lies the current economic-policy rub. Economists’ theories of growth bring to mind a coin: Sunny descriptions of growth and dynamism are “heads,” and hand-wringing over disruption is “tails.” As I observed earlier, growth is messy. It can push some individuals, firms, and even industries off well-worn and comfortable paths.

But Smith offers more in defense of growth than paeans to laissez-faire. Though he is sometimes caricatured as being anti-government in all cases, Smith was principally opposed to mercantilist privileges for specific businesses and industries and to the governmentalization of social affairs. He wanted government to provide what economists today call “public goods,” such as national defense, the criminal-justice system, and enforcement of property rights and contracts the institutional underpinnings of commerce and trade. He also favored support for infrastructure to keep commerce flowing freely.

But Smith went further: To prepare workers and enrich their lives, he called for government to provide universal education, and he drew a connection between education and liberty as well as work in a free society. But boosting participation in today’s economy—participation that provides support for growth—will require a bit more.

Not surprisingly, political reaction to economic disruption brings about — pardon the econ-speak—a “demand” for and “supply” of policy actions. Job losses, firm failures, and diminished industry fortunes bring about a demand for help, for adaptation. The political process responds with a supply of ideas in one of two forms: walls or bridges. Walls are protections against disruption or change. Bridges, ways to get somewhere or back, prepare individuals for the changed economy and help those whose economic participation has been disrupted reenter the workforce.

Proposals for walls are familiar. They can be physical, of course, but they needn’t be. Conservative populists advocate limits on trade and technology, in order to advance industrial policy. Some progressives advocate universal basic income. All these policies would diminish the prospects for economic advances.

The most prominent sort of wall today is what I call “modern corporatism.” It assumes that Smith was wrong: The “wealth of a nation” lies not in consumption or living standards (and so ultimately in growth) but in jobs, good jobs, even particular good jobs, with good manufacturing jobs the very paradigm. The sort of tinkering with the market that drew Smith’s ire may actually be a necessary way of recentering economic policy on jobs, so the theory goes. Opportunities for work, and for the dignity it can bring, are surely important.

A gentle industrial policy devised by social scientists who are worried about jobs is not the answer. It results in state tinkering for special interests, precisely the kind of thing that prompted Smith’s criticism of mercantilism. Moreover, as University of Chicago economist Luigi Zingales argues in A Capitalism for the People, it risks a vicious cycle: A little bit of tinkering becomes a lot of tinkering—and anyone who cannot justify special privileges is left out, calling into question social support for growth. Nevertheless, industrial policy has caught the attention of elected officials on the right, from Donald Trump to Josh Hawley to Marco Rubio. While national security and the border can be exceptions as concerns, advice from Milton Friedman to the party of Ronald Reagan this is not.

That said, economists’ invocation of Smith as a proponent of let-’er-rip laissez-faire is neither faithful to Smith nor particularly helpful to individuals and communities buffeted by disruption. With today’s rapid and long-lasting technological change and globalization, “having a go” requires support for acquiring new skills when they are needed.

That is why we need more bridges. Bridges take us somewhere and bring us back. The journey to somewhere is about preparation for new opportunities. The journey back is about reconnecting to the productive economy when economic forces beyond our control have knocked us away.

Economic bridges have three features. The first is that they help people overcome a specific challenge on their way to economic flourishing — they don’t provide that outcome directly. The second is that wider society builds the bridge, through private organizations, governments, or public–private partnerships, as globalization and technological change have introduced significant risks that individuals by themselves cannot avoid. The third feature is that they avoid restraints on openness to changes in markets and ideas.

We once did better, much better. During the Civil War, President Abraham Lincoln worked with Congress to pass the Morrill Act, directing resources to the development of land-grant colleges around the country, extending higher education to citizens of modest means, and enabling workers to develop skills for new industries, particularly in manufacturing. As World War II drew to a close, President Franklin D. Roosevelt and Congress came together to enact the G.I. Bill, helping to educate returning troops for a changing economy.

Supporting economic growth and undergirding broad participation in the economy require similarly bold ideas. To begin, community colleges are the logical workhorses of skill development and retraining, and their presence in regional economies makes them attractive partners for employers. Yet community colleges have seen their state-level public support wither. The Biden administration calls for free tuition, which would boost demand but provide no support for community college to offer a practical education and an emphasis on completion. Amy Ganz, Austan Goolsbee, Melissa Kearney, and I proposed an alternative approach based on the land-grant-college model. We proposed a supply-side program of federal grants to strengthen community colleges — contingent on improved degree-completion rates and labor-market outcomes. To further encourage training, the federal government could offer a tax credit to compensate firms for the risk of losing trained workers. It could also increase the earned-income tax credit for workers with or without children.

New ideas are also needed to promote workers’ reentry into the workforce. Personal reemployment accounts, for example, would support dislocated workers and offer them a reemployment bonus if they found a new job within a certain period of time. The “personal” refers to individuals’ choosing from a range of training and support services. Another idea is to beef up support for place-based assistance to areas with stubbornly high rates of long-term nonemployment. Such support could be integrated with an increase in the earned-income tax credit and the supply-side investment in community colleges. Building on the decentralized approach in the land-grant colleges and grants to community colleges, expanded place-based aid would be delivered via flexible block grants encouraging business and employment.

Broad public support required for growth and dynamism requires both bridge-building and a political language that frames it. Growth, opportunity, and participation are good, and we do not need a new economics. But phrases like “transition cost” and “inevitable economic forces” must give way to bridges of preparation and reconnection.

‘Why did nobody see it coming?” a quizzical Queen of England questioned a quorum of economists at the London School of Economics about the global financial crisis as it emerged in late 2008. How could major disruptive forces build up over time and yet escape the attention of experts and leaders?

Of the disruptive structural changes accompanying economic dynamism, one might ask a similar question. Growth matters. But that growth is one side of a coin whose flip side is disruption is known, certainly to economists. Why has our political discourse not emphasized this basic point?

Why did we not see fatigue with change coming among the people who most had to bear its ill effects?

However foolishly, we did not. Some so-called conservatives today have responded by saying that we should limit change. Surely a better response is that we should seek ever more growth by allowing unfettered change, but also facilitate the establishing of ever more connections in a growing economy. That classical-liberal answer has the better place in American conservatism — and in American economic life.

— This essay is sponsored by National Review Institute.Originally published here.

On Tuesday, March 1, Glenn and Tony will record a podcast on the economic consequences of the Russian invasion of Ukraine. The recording will be posted to this blog and also available through iTunes.

Some useful links

General information on developments (political and military, as well as economic):

Updates on the website of the Financial Times (note that the FT has dropped its paywall to allow non-subscribers to read this content). This article on the possible effects on the global economy is particularly worth reading.

The Twitter feed of Max Seddon, the FT’s Moscow bureau chief, is here.

The website of the New York Times has an extensive series of updates focused on military and political developments (subscription may be required).

Streaming updates on the website of the Wall Street Journal (subscription may be required).

A Twitter feed that provides timely updates on the military situation.

An article in the New Yorker discussing Russian President Vladimir Putin’s claims about the historical relationship between Russia and Ukraine.

A pessimistic blog post by a retired U.S. Army Colonel on whether the U.S. military is equipped to fight a war in Europe.

Discussions focused on economics:

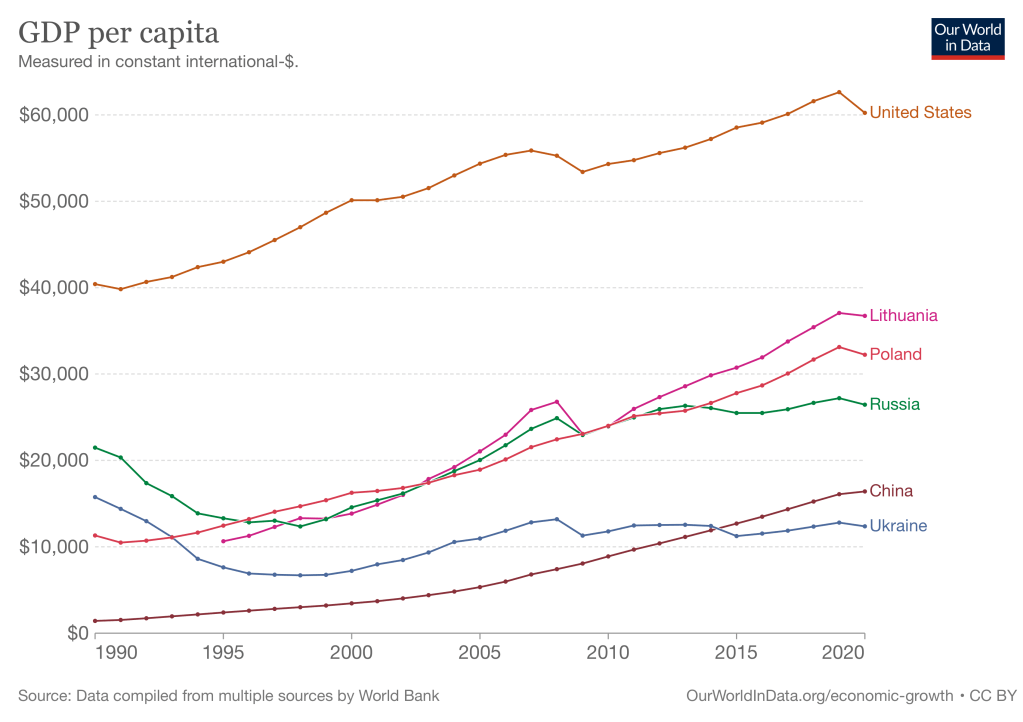

As background, the following figure from the Our World in Data site shows the growth in real GDP per capita for several countries. The underlying data were compiled by the World Bank and are measured in constant international dollars, which means that they are corrected for inflation and for variations across countries in the purchasing power of the domestic currency.

In 2020, Russian GDP per capita was less than half that of U.S. GDP per capita although about 50 percent greater than GDP per capita in China. GDP per capita in Lithuania, part of the Soviet Union until 1991, and Poland, part of the Soviet bloc until 1989, are significantly higher than in Russia. These two countries have become integrated into the European economy and have grown more rapidly than has Russia, which continues to rely heavy on exports of oil, natural gas, and other commodities. Ukraine is not as well integrated into the European economy as are Poland and Lithuania and Ukraine experienced little economic growth since attaining independence in 1991. In fact, Ukraine’s real GDP per capita was lower in 2020 than it had been in 1991.

Here is a transcript of President Joe Biden’s speech imposing sanctions on Russia.

Informative Full Stack Economics blog post by Alan Cole explaining the likely reasons why U.S. and European sanctions on Russia excluded energy. Useful explanation of the role of correspondent banking in international trade.

An article in the Economist discussing sanctions (subscription may be required).

An article in the New York Times discussing the SWIFT (Society for Worldwide Interbank Financial Telecommunications) service, which is based in Belgium, and is a key component of the international financial system. Some policymakers have proposed cutting Russia off from SWIFT. The article discusses why some countries have been opposed to taking that step (subscription may be required).

An opinion column by Justin Fox on bloomberg.com examines in what sense the United States is energy independent and the economic reasons that the U.S. still imports some oil from Russia (subscription may be required).

Blog post by economic writer Noah Smith on the possible effects of the invasion on the post-World War II international economic system.