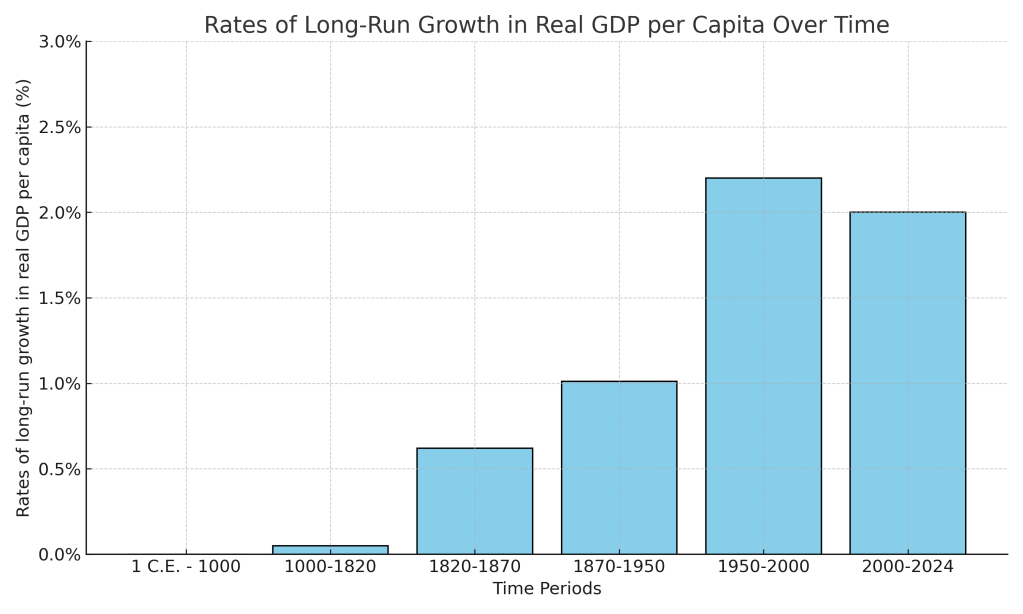

For most of human history there was little to no economic growth. Until the nineteenth century, the average person everywhere in the world lived at a subsistence level. For example, although the Roman Empire controlled most of Southern and Western Europe, the Near East, and North Africa for more than 400 years, the living standard of the average citizen of the Empire was no higher at the end of the Empire than it had been at the beginning.

Economists typically measure economic growth by the rate of increase in real GDP per capita. The following figure, updated from Chapter 11 of Macroeconomics (Chapter 21 of Economics), shows the slow pace of growth in real GDP per capita in the world economy from the year 1 to the year 1820 and the much faster rates of growth over the following periods. As discussed in Chapter 11, the figure relies on data compiled by Angus Maddison of University of Groningen in the Netherlands and—for recent years—data from the World Bank.

This year’s three Nobelists have contributed to understanding why economic growth accelerated sharply in the nineteenth century and why England was the first country to experienced sustained increases in real GDP per capita—an event labeled the Industrial Revolution. Joel Mokyr of Northwestern University has conducted decades of research into which innovations were crucial to economic growth and the institutional and economic advantages that allowed entrepreneurs in England to use those innovations to expand production much more rapidly than had happened before. Philippe Aghion of Collège de France and INSEAD and Peter Howitt of Brown University have focused on formally modeling the process of creative destruction that underlies sustained economic growth. The classic discussion of creative destruction appears in Joseph Schumpeter’s book Capitalism, Socialism, and Democracy, published in 1942.

In Macroeconomics Chapter 21, we discuss the process of creative destruction in the context of economic growth. Creative destruction occurs as technological change results in new products that drive firms producing older products out of business. Examples are automobiles driving out of business producers of horse-drawn carriages in the early twentieth century. Or Netflix and other movie streaming sites driving video rental stores out of business in more recent years.

The Nobel Committee’s announcement of the prize can be found here. A longer discussion of the Nobelists’ work can be found here. The scope of their research can be seen by reviewing their curricula vitae, which can be found here, here, and here. The amount of the prize this years is 11 million Swedish kronor (about $1.2 million). Mokyr receives half and Aghion and Howitt receive the other half.

Modern industrial capitalism’s bounty has been breathtaking globally and especially in the U.S. It’s tempting, then, to look at critics in the crowd in Monty Python’s “Life of Brian” as they ask, “What have the Romans ever do for us?,” only to be confronted with a large list of contributions. But, in fact, over time, American capitalism has been saved by adapting to big economic changes.

We’re at another turning point, and the pattern of American capitalism’s keeping its innovative and disruptive core by responding, if sometimes slowly, to structural shocks will play out as follows.

The magnitude, scope and speed of technological change surrounding generative artificial intelligence will bring forth a new social insurance aimed at long-term, not just cyclical, impacts of disruption. For individuals, it will include support for work, community colleges and training, and wage insurance for older workers. For places, it will include block grants to communities and areas with high structural unemployment to stimulate new business and job opportunities. Such efforts are a needed departure from a focus on cyclical protection from short-term unemployment toward a longer-term bridge of reconnecting to a changing economy.

These ideas, like America’s historical big responses in land-grant colleges and the GI Bill, combine federal funding support with local approaches (allowing variation in responses to local business and employment opportunities), another hallmark of past U.S. economic policy.

With a stronger economic safety net, the current push toward higher tariffs and protectionism will gradually fade. Protectionism is a wall against change, but it is one that insulates us from progress, too.

A growing budget deficit and strains on public finances will lead to a reliance on consumption taxes to replace the current income tax system; continuing to raise taxes on saving and investment will arrest growth prospects. For instance, a tax on business cash flow, which places a levy on a firm’s revenue minus all expenses including investment, would replace taxes on business income. Domestic production would be enhanced by adding a border adjustment to business taxes—exports would be exempt from taxation, but companies can’t claim a deduction for the cost of imports.

That reform allows a shift from helter-skelter tariffs to tax reform that boosts investment and offers U.S. and foreign firms alike an incentive to invest in the U.S.

These ideas to retain opportunity amid creative destruction will also refresh American capitalism as the nation celebrates its 250th anniversary. They also celebrate the classical liberal ideas of Adam Smith, whose treatise “The Wealth of Nations” appeared the same year. This refresh marries competition’s role in “The Wealth of Nations” and American capitalism with the ability to compete, again a feature of turning points in capitalism in the U.S.

Decades down the road, this “Project 2026” will have preserved the bounty and mass prosperity of American capitalism.

These observations first appeared in the Wall Street Journal, along with predictions from six other economists and economic historians.

Image generated by ChatGPT 5 of a 1981 IBM personal computer.

The modern era of information technology began in the 1980s with the spread of personal computers. A key development was the introduction of the IBM personal computer in 1981. The Apple II, designed by Steve Jobs and Steve Wozniak and introduced in 1977, was the first widely used personal computer, but the IBM personal computer had several advantages over the Apple II. For decades, IBM had been the dominant firm in information technology worldwide. The IBM System/360, introduced in 1964, was by far the most successful mainframe computer in the world. Many large U.S. firms depended on IBM to meet their needs for processing payroll, general accounting services, managing inventories, and billing.

Because these firms were often reliant on IBM for installing, maintaining, and servicing their computers, they were reluctant to shift to performing key tasks with personal computers like the Apple II. This reluctance was reinforced by the fact that few managers were familiar with Apple or other early personal computer firms like Commodore or Tandy, which sold the TRS-80 through Radio Shack stores. In addition, many firms lacked the technical staffs to install, maintain, and repair personal computers. Initially, it was easier for firms to rely on IBM to perform these tasks, just as they had long been performing the same tasks for firms’ mainframe computers.

By 1983, the IBM PC had overtaken the Apple II as the best-selling personal computer in the United States. In addition, IBM had decided to rely on other firms to supply its computer chips (Intel) and operating system (Microsoft) rather than develop its own proprietary computer chips and operating system. This so-called open architecture made it possible for other firms, such as Dell and Gateway, to produce personal computers that were similar to IBM’s. The result was to give an incentive for firms to produce software that would run on both the IBM PC and the “clones” produced by other firms, rather than produce software for Apple personal computers. Key software such as the spreadsheet program Lotus 1-2-3 and word processing programs, such as WordPerfect, cemented the dominance of the IBM PC and the IBM clones over Apple, which was largely shut out of the market for business computers.

As personal computers began to be widely used in business, there was a general expectation among economists and policymakers that business productivity would increase. Productivity, measured as output per hour of work, had grown at a fairly rapid average annual rate of 2.8 percent between 1948 and 1972. As we discuss in Macroeconomics, Chapter 10 (Economics, Chapter 20 and Essentials of Economics, Chapter 14) rising productivity is the key to an economy achieving a rising standard of living. Unless output per hour worked increases over time, consumption per person will stagnate. An annual growth rate of 2.8 percent will lead to noticeable increases in the standard of living.

Economists and policymakers were concerned when productivity growth slowed beginning in 1973. From 1973 to 198o, productivity grew at an annual rate of only 1.3 percent—less than half the growth rate from 1948 to 1972. Despite the widespread adoption of personal computers by businesses, during the 1980s, the growth rate of productivity increased only to 1.5 percent. In 1987, Nobel laureate Robert Solow of MIT famously remarked: “You can see the computer age everywhere but in the productivity statistics.” Economists labeled Solow’s observation the “productivity paradox.” With hindsight, it’s now clear that it takes time for businesses to adapt to a new technology, such as personal computers. In addition, the development of the internet, increases in the computing power of personal computers, and the introduction of innovative software were necessary before a significant increase in productivity growth rates occurred in the mid-1990s.

Result when ChatGPT 5 is asked to create an image illustrating ChatGPT

The release of ChatGPT in November 2022 is likely to be seen in the future as at least as important an event in the evolution of information technology as the introduction of the IBM PC in August 1981. Just as with personal computers, many people have been predicting that generative AI programs will have a substantial effect on the labor market and on productivity.

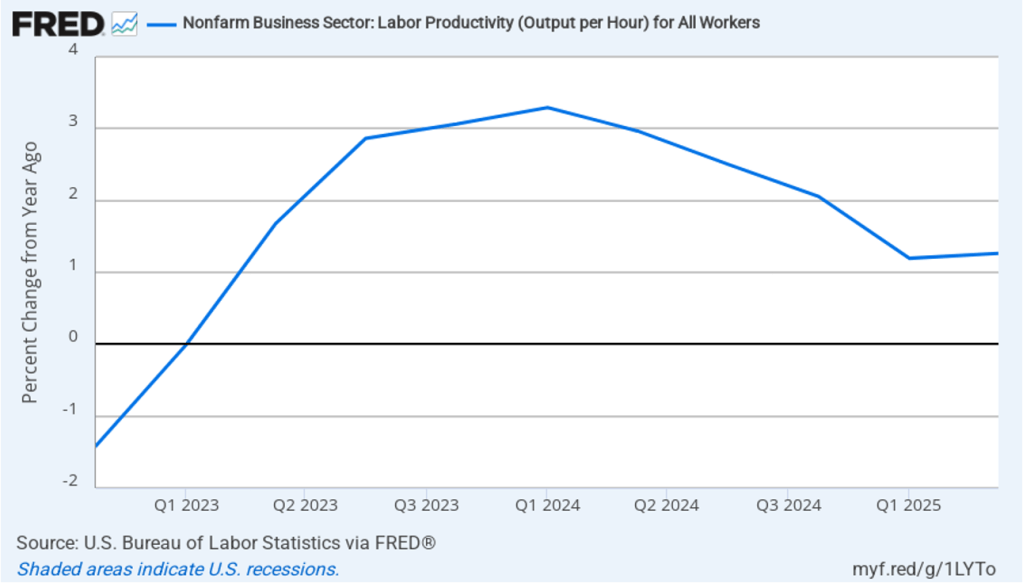

In this recent blog post, we discussed the conflicting evidence as to whether generative AI has been eliminating jobs in some occupations, such as software coding. Has AI had an effect on productivity growth? The following figure shows the rate of productivity growth in each quarter since the fourth quarter of 2022. The figure shows an acceleration in productivity growth beginning in the fourth quarter of 2023. From the fourth quarter of 2023 through the fourth quarter of 2024, productivity grew at an annual rate of 3.1 percent—higher than during the period from 1948 to 1972. Some commentators attributed this surge in productivity to the effects of AI.

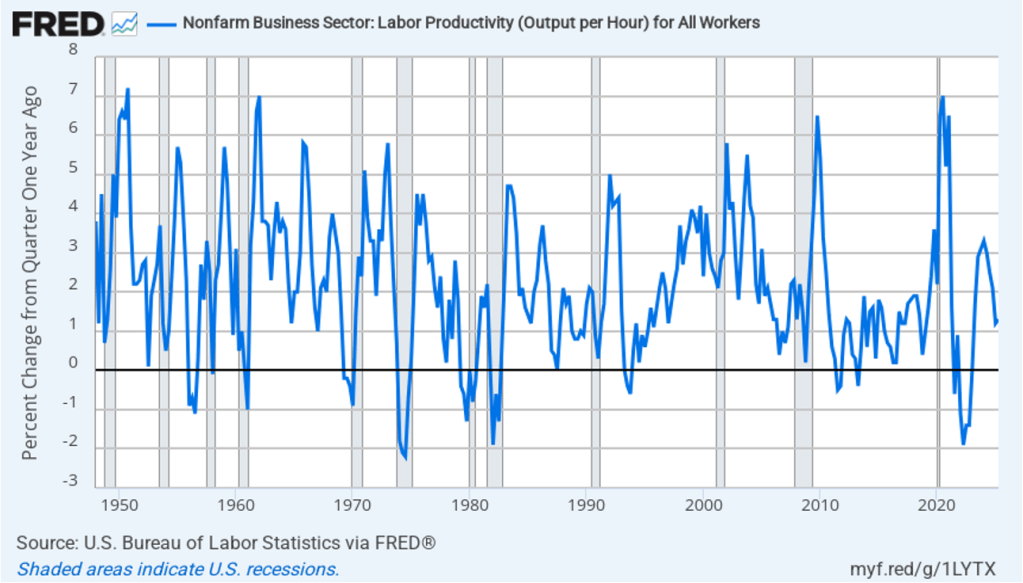

However, the increase in productivity growth wasn’t sustained, with the growth rate in the first half of 2025 being only 1.3 percent. That slowdown makes it more likely that the surge in productivity growth was attributable to the recovery from the 2020 Covid recession or was simply an example of the wide fluctuations that can occur in productivity growth. The following figure, showing the entire period since 1948, illustrates how volatile quarterly rates of productivity growth are.

How large an effect will AI ultimately have on the labor market? If many current jobs are replaced by AI is it likely that the unemployment rate will soar? That’s a prediction that has often been made in the media. For instance, Dario Amodei, the CEO of generative AI firm Anthropic, predicted during an interview on CNN that AI will wipe out half of all entry level jobs in the U.S. and cause the unemployment rate to rise to between 10% and 20%.

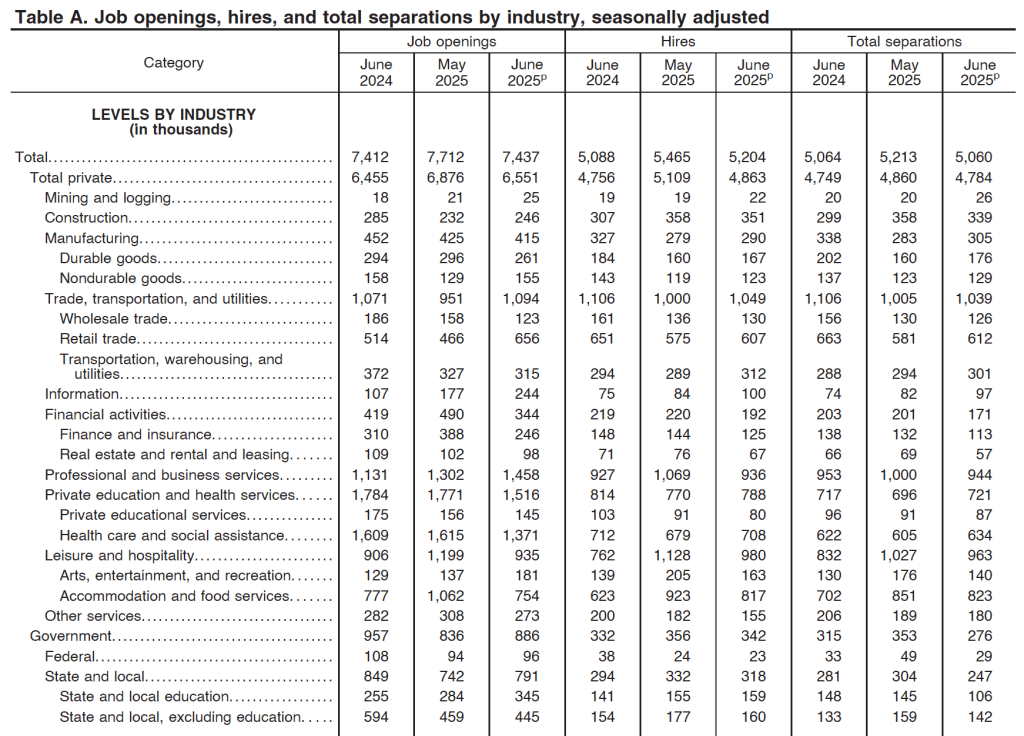

Although Amodei is likely correct that AI will wipe out many existing jobs, it’s unlikely that the result will be a large increase in the unemployment rate. As we discuss in Macroeconomics, Chapter 9 (Economics, Chapter 19 and Essentials of Economics, Chapter 13) the U.S. economy creates and destroys millions of jobs every year. Consider, for instance, the following table from the most recent “Job Openings and Labor Turnover” (JOLTS) report from the Bureau of Labor Statistics (BLS). In June 2025, 5.2 million people were hired and 5.1 million left (were “separated” from) their jobs as a result of quitting, being laid off, or being fired.

Most economists believe that one of the strengths of the U.S. economy is the flexibility of the U.S. labor market. With a few exceptions, “employment at will” holds in every state, which means that a business can lay off or fire a worker without having to provide a cause. Unionization rates are also lower in the United States than in many other countries. U.S. workers have less job security than in many other countries, but—crucially—U.S. firms are more willing to hire workers because they can more easily lay them off or fire them if they need to. (We discuss the greater flexibility of U.S. labor markets in Macroeconomics, Chapter 11 (Economics, Chapter 21).)

The flexibility of the U.S. labor market means that it has shrugged off many waves of technological change. AI will have a substantial effect on the economy and on the mix of jobs available. But will the effect be greater than that of electrification in the late nineteenth century or the effect of the automobile in the early twentieth century or the effect of the internet and personal computing in the 1980s and 1990s? The introduction of automobiles wiped out jobs in the horse-drawn vehicle industry, just as the internet has wiped out jobs in brick-and-mortar retailing. People unemployed by technology find other jobs; sometimes the jobs are better than the ones they had and sometimes the jobs are worse. But economic historians have shown that technological change has never caused a spike in the U.S. unemployment rate. It seems likely—but not certain!—that the same will be true of the effects of the AI revolution.

Which jobs will AI destroy and which new jobs will it create? Except in a rough sense, the truth is that it is very difficult to tell. Attempts to forecast technological change have a dismal history. To take one of many examples, in 1998, Paul Krugman, later to win the Nobel Prize, cast doubt on the importance of the internet: “By 2005 or so, it will become clear that the Internet’s impact on the economy has been no greater than the fax machine’s.” Krugman, Amodei and other prognosticators of the effects of technological change simply lack the knowledge to make an informed prediction because the required knowledge is spread across millions of people.

That knowledge only becomes available over time. The actions of consumers and firms interacting in markets mobilize information that is initially known only partially to any one person. In 1945, Friedrich Hayek made this argument in “The Use of Knowledge in Society,” which is one of the most influential economics articles ever written. One of Hayek’s examples is an unexpected decrease in the supply of tin. How will this development affect the economy? We find out only by observing how people adapt to a rising price of tin: “The marvel is that … without an order being issued, without more than perhaps a handful of people knowing the cause, tens of thousands of people whose identity could not be ascertained by months of investigation are made [by the increase in the price of tin] to use the material or its products more sparingly.” People adjust to changing conditions in ways that we lack sufficient information to reliably forecast. (We discuss Hayek’s view of how the market system mobilizes the knowledge of workers, consumers, and firms in Microeconomics, Chapter 2.)

It’s up to millions of engineers, workers, and managers across the economy, often through trial and error, to discover how AI can best reduce the cost of producing goods and services or improve their quality. Competition among firms drives them to make the best use of AI. In the end, AI may result in more people or fewer people being employed in any particular occupation. At this point, there is no way to know.

In June, the U.S. Census Bureau released its population estimates for 2024. Included was the following graphic showing the change in the U.S. population pyramid from 2004 to 2024. As the graphic shows, people 65 years and older have increased as a fraction of the total population, while children have decreased as a fraction of the total population. (The Census considers everyone 17 and younger to be a child.) Between 2004 and 2024, people 65 and older increased from 12.4 percent of the population to 18.0 percent. People younger than 18 fell from 25.0 percent of the population in 2004 to 21.5 percent in 2024.

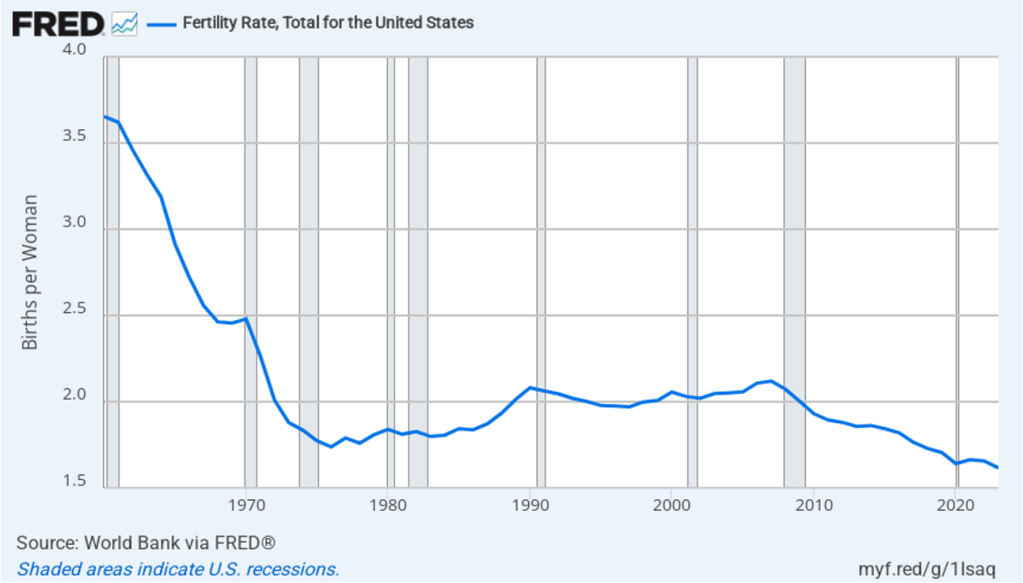

The aging of the U.S. population reflects falling birth rates. Demographers and economists typically measure birth rates as the total fertility rate (TFR), which is defined by the World Bank as: “The number of children that would be born to a woman if she were to live to the end of her childbearing years and bear children in accordance with age-specific fertility rates currently observed.” The TFR has the advantage over the simple birth rate—which is the number of live births per thousand people—because the TFR corrects for the age structure of a country’s female population. Leaving aside the effects of immigration and emigration, a TFR of 2.1 is necessary to keep a country’s population stable. Stated another way, a country needs a TFR of 2.1 to achieve replacement level fertility. A country with a TFR above 2.1 experiences long-run population growth, while a country with a TFR of less than 2.1 experiences long-run population decline.

The following figure shows the TFR for the United States for each year between 1960 and 2023. Since 1971, the TFR has been below 2.1 in every year except for 2006 and 2007. Immigration has helped to offset the effects on population growth of a TFR below 2.1.

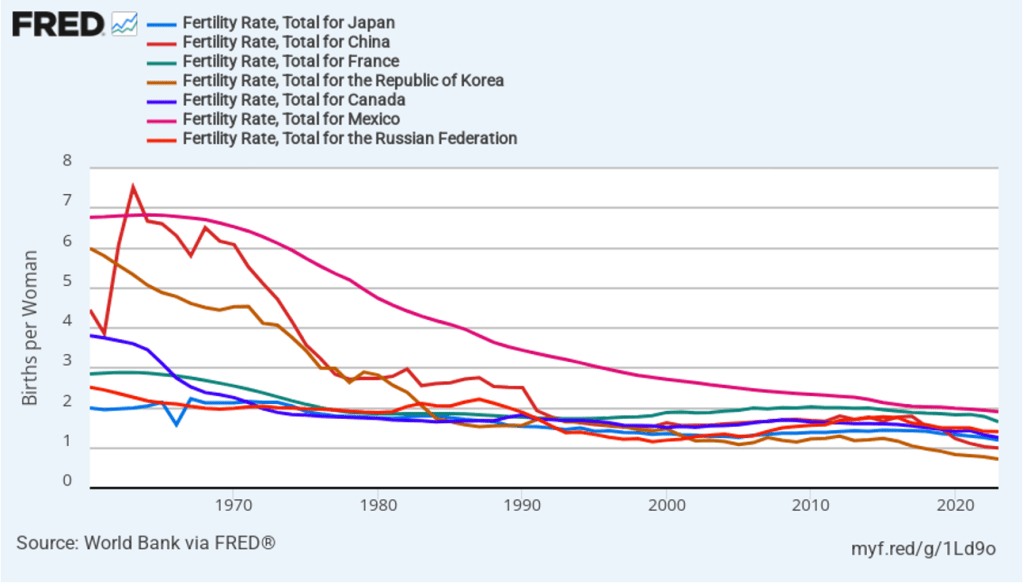

The United States is not alone in experiencing a sharp decline in its TFR since the 1960s. The following figure shows some other countries that currently have below replacement level fertility, including some countries—such as China, Japan, Korea, and Mexico—in which TFRs were well above 5 in the 1960s. In fact, only a relatively few countries, such as Israel and some countries in sub-Saharan Africa are still experiencing above replacement level fertility.

An aging population raises the number of retired people relative to the number of workers, making it difficult for governments to finance pensions and health care for older people. We discuss this problem with respect to the U.S. Social Security and Medicare programs in an Apply the Concept in Macroeconomics, Chapter 16 (Economics, Chapter 26 and Essentials of Economics, Chapter 18). Countries experiencing a declining population typically also experience lower rates of economic growth than do countries with growing populations. Finally, as we discuss in an Apply the Concept in Microeconomics, Chapter 3, different generations often differ in the mix of products they buy. For instance, a declining number of children results in declining demand for diapers, strollers, and toys.

Glenn, along with co-authors Douglas Elmendorf of Harvard’s Kennedy School and Zachary Liscow of the Yale Law School, has written a new National Bureau of Economic Research working paper: “Policies to Reduce Federal Budget Deficits by Increasing Economic Growth”

Here’s the abstract:

Could policy changes boost economic growth enough and at a low enough cost to meaningfully reduce federal budget deficits? We assess seven areas of economic policy: immigration of high-skilled workers, housing regulation, safety net programs, regulation of electricity transmission, government support for research and development, tax policy related to business investment, and permitting of infrastructure construction. We find that growth-enhancing policies almost certainly cannot stabilize federal debt on their own, but that such policies can reduce the explicit tax hikes, spending cuts, or both that are needed to stabilize debt. We also find a dearth of research on the likely impacts of potential growth-enhancing policies and on ways to design such policies to restrain federal debt, and we offer suggestions for ways to build a larger base of evidence.

The economy and financial markets nervously await the July 8 end of the 90-day pause of the Trump administration’s “reciprocal” tariffs. But four days earlier, Republicans can allay those fears with a pro-growth policy that advances President Trump’s Made in America agenda without tariffs. The fix: tax reform.

July 4 is the date that Treasury Secretary Bessent has predicted Congress and the White House will have ready a 2.0 version of the landmark Tax Cut and Jobs Act of 2017, or TCJA. Without congressional action, some of these reforms will expire at the end of 2025, killing changes that still benefit the economy. Corporate tax changes, in particular, boosted investment and growth. These should remain the focal point of this next tax bill—for many reasons. Done right, corporate tax reform could advance President Trump’s goal to bring investment to American production without using economy-roiling tariffs. Call it TCJA+.

Renewing some parts of the original TCJA will help investment in the U.S. The 2017 reform offered incentives for investment in new businesses by allowing them to expense the cost of assets, rather than writing them off over time. But these benefits were set to be phased out from 2023 to 2026, removing a key pro-growth element of the earlier law.

Then there are two new provisions Republicans should add to secure Mr. Trump’s goal to have more made in America. Both were in the original 2016 House Republican tax reform blueprint.

First, Congress should change business taxation from the current income tax to a cash-flow tax, which taxes a firm’s revenue, minus all its expenses, including investment. Long championed by economists and tax-law experts, a cash-flow tax would allow businesses to expense investment immediately. It would also disallow nonfinancial companies from making interest deductions, because unlike an income tax, a cash-flow tax treats debt and equity the same. This removes an important tax incentive for firms to allow themselves to be leveraged. A cash-flow tax is also much simpler than a corporate income tax, which requires complex depreciation schedules. Most important, the reform would stimulate business investment.

Second, legislators should add a border adjustment to corporate taxes. That would deny companies a tax deduction for expenses of inputs imported from abroad, while exempting U.S. exports from taxation. As the Trump administration has observed, other countries already use border adjustments in their value-added taxes on consumption. America uses a similar mechanism in state and local retail taxes, too. If you buy a kitchen appliance in New York, you pay New York sales tax, even if it was made in Ohio. Sales tax applies only where the good is sold, not where it originates.

Though distinct from tariffs, border adjustments can promote domestic production. Adding a border adjustment to the federal corporate tax would eliminate any extra tax businesses suffer now simply as a consequence of producing in the U.S. Though the 2017 law made the U.S. tax system more globally competitive by lowering the corporate income tax rate from 35% to 21%, it’s still higher than in many other countries, which attract production with low cost. A border adjustment would remove this incentive for American firms to locate profits or activities abroad, while increasing incentives for non-U.S. firms to locate activities within our borders.

As with the original pro-investment features in the 2017 law, this TCJA+ reform would increase investment and incomes—and thereby revenue. For the original TCJA, when the Congressional Budget Office included the macroeconomic effects of higher incomes buoyed by the reforms’ pro-growth elements, the CBO reduced the estimated revenue loss from the tax cuts by almost 30%. Changing the corporate income tax to a cash-flow levy would similarly increase revenue by removing taxes on what economists call the “normal return” on investment, or the cost of capital. Companies would instead pay only on profits above this amount. A border adjustment can likewise raise substantial revenue over the next decade because imports (which would receive no deduction) are larger than exports (which would no longer be taxed).

The higher revenue these two TCJA+ provisions promise could be used to lower the tax rate on business cash flow or to fund other tax-policy objectives. Importantly, that revenue can replace revenue raised from the tariffs the Trump administration had planned to implement on July 8. These two tax provisions would accomplish the president’s America-first and revenue objectives without destabilizing businesses with whipsawing tariffs.

Finally, TCJA+ would offer another big benefit: It would move the U.S. toward independence from political meddling in the economy via targeted protection or subsidies. This added predictability and breathing room for investment would be one more reason to produce in America. Pluses indeed.

An image generated by GTP-4o illustrating research.

This opinion column by Glenn appeared in the Financial Times on March 10.

The Trump administration has wisely emphasised raising America’s rate of economic growth. But growth doesn’t just happen. It is the byproduct of innovation both radical (think of the emergence of generative artificial intelligence) and gradual (such as improvements in manufacturing processes or transport). Many economic factors influence innovation, but research and development is key. While this can be privately or publicly funded, the latter can support basic research with spillovers to many companies and applications.

Therein lies the rub: the new administration’s growth agenda is joined by a significant effort to reduce government spending, spearheaded by the so-called Department of Government Efficiency. Some spending restraint can enhance growth by reducing interest rates or reallocating funds towards more investment-oriented activities. But cuts to R&D, as the administration is advocating at the National Institutes of Health (NIH), National Science Foundation (NSF), Department of Energy (DoE) and NASA, are counter-productive. They will limit innovation and growth.

The link between R&D and productivity growth has a long pedigree in economics and has generally been acknowledged by US policymakers. In the mid-1950s, economist Robert Solow made the Nobel Prize-winning conclusion that sustained output growth is not possible without technological progress. Decades later, former World Bank chief economist Paul Romer added another Nobel Prize-winning insight: growth reflected the intentional adoption of new ideas, so could be affected by research incentives.

It is well known that research is undervalued by private companies. Private funders of R&D don’t capture all its benefits. The social returns of R&D are two to four times higher than private returns. These high returns are enabled in the US by federal funding. For example, publicly funded research at the NIH has been found to significantly impact private development of new drugs.

In a comprehensive study, Andrew Fieldhouse and Karel Mertens classify major changes in non-defence R&D funding by the DoE, Nasa, NIH and NSF over the postwar period. They estimate implied returns of as much as 200 per cent — raising US economic output by $2 per dollar of funding. This is substantially higher than recent estimates of returns to private R&D. According to the Congressional Budget Office, the high returns to public funding are more than 10 times that on public investment in infrastructure. With the higher tax revenue generated from additional GDP, an increase in R&D funding more than pays for itself.

In aggregate, productivity gains from federal R&D funding are substantial. Indeed, Fieldhouse and Mertens estimate that government-funded R&D amounts to about one-fifth of productivity growth (measured as output growth less all input growth) in the US since the second world war.

Combined with the high social returns of government-funded R&D, it is essential that policymakers in the current administration acknowledge the risks of underfunding R&D. Spending cuts are clearly harmful to productivity and even budget outcomes.

A shift towards government-financed R&D does not imply that policy in these areas should be beyond review. Some economists have questioned whether current R&D projects take sufficiently high scientific risks, particularly on the ideas of younger scholars. And policymakers can certainly investigate whether indirect cost subsidies to universities and laboratories—in addition to the direct costs of research—are set at the appropriate levels. But, if growth is the objective, the presumption must be that additional public spending on R&D is worthwhile.

Federal support for growth-oriented R&D can extend beyond research grants. Publicly supported applied research centres around the country offer a mechanism to collaborate with local universities and business networks to disseminate ideas to practice. This builds upon the agricultural and manufacturing extension services instituted by 19th-century land-grant colleges that enhanced productivity.

The Trump administration is right to promote growth as a public objective. Spending restraint and fiscal discipline can be growth-enhancing. But all spending is equal. Government-funded R&D is vitally important for innovation and productivity growth. The case is clear.

Treasury Secretary nominee Scott Bessent. (Photo from Progect Syndicate.)

By setting an ambitious 3% growth target, U.S. Treasury Secretary nominee Scott Bessent has provided the Trump administration a North Star to follow in devising its economic policies. The task now is to focus on productivity growth and avoiding any unforced errors that would threaten output.

U.S. Treasury Secretary nominee Scott Bessent is right to emphasize faster economic growth as a touchstone of Donald Trump’s second presidency. More robust growth not only implies higher incomes and living standards—surely the basic objective of economic policy—but also can reduce America’s yawning federal budget deficit and debt-to-GDP ratio, and ease the sometimes difficult trade-offs across defense, social, and education and research spending.

But faster growth must be more than just a wish. Achieving it calls for a carefully constructed agenda, based on a recognition of the channels through which economic policies can raise or reduce output. While a pro-investment tax policy might boost capital accumulation, productivity, and GDP, higher interest rates from deficit-financed tax or spending changes might have the opposite effect. Similarly, since growth in hours worked is a component of growth in output or GDP, the new administration should avoid anti-work policies that hinder full labor-force participation, as well as sudden adverse changes to legal immigration.

While recognizing that some policy shifts that increase output might adversely affect other areas of social interest (such as the distribution of income) or even national security, policymakers should focus squarely on increasing productivity. The three pillars of any productivity policy are support for research, investment-friendly tax provisions, and more efficient regulation.

Ideas drive prospects in modern economies. Basic research in the sciences, engineering, and medicine power the innovation that advances technology, improvements in business organization, and gains in health and well-being. It makes perfect sense for the federal government to support such research. Since private firms cannot appropriate all the gains from their own outlays for basic research, they have less of an incentive to invest in it. Moreover, government support in this area produces valuable spillovers, as demonstrated by the earlier Defense Department research expenditures that became catalysts for today’s digital revolution.

This being the case, cuts in federal support for basic research are inconsistent with a growth agenda. Still, policymakers should review how research funds are distributed to ensure scientific merit, and they should encourage a healthy dose of risk-taking on newer ideas and researchers.

In addition to encouraging commercialization of spillovers from basic research and defense programs, federal support for applied research centers around the country would accelerate the dissemination of new productivity-enhancing technologies and ideas. Such centers also tend to distribute the economy’s prosperity more widely, by making new ideas broadly accessible—as agricultural- and manufacturing-extension services have done historically.

To address the second pillar of productivity growth, the administration should seek to extend the pro-investment provisions of the Tax Cuts and Jobs Act that Trump signed into law in 2017. While the TCJA’s lower tax rates on corporate profits remain in place, the expensing of business investment – a potent tool for boosting capital accumulation, productivity, and incomes – was set to be phased out over the 2023-26 period. This provision could be restored and made permanent by reducing spending on credits under the Inflation Reduction Act, or by rolling back the spending – such as $175 billion to forgive student loans – associated with outgoing President Joe Biden’s executive orders.

If the new administration wanted to go further with tax policy, it could build on the 2016 House Republican blueprint for tax reform that shifted the business tax regime from an income tax to a cashflow tax. By permitting immediate expensing of investment, but not interest deductions for nonfinancial firms, this reform would stimulate investment and growth, remove tax incentives that favor debt over equity, and simplify the tax system.

That brings us to the third pillar of a successful growth strategy: efficient regulation. The issue is not “more” versus “less.” What really matters for growth is how changes in regulation can improve the prospects for growth through innovation, investment, and capital allocation, while focusing on trade-offs in risks. Those shaping the agenda should start with basic questions like: Why can’t we build better infrastructure faster? Why can’t capital markets and bank lending be nimbler? Not only do such questions identify a specific goal; they also require one to identify trade-offs.

Fortunately, financial regulation under the new administration is likely to improve capital allocation and the prospects for growth, given the leadership appointments already announced at the Securities and Exchange Commission and the Federal Reserve. But policymakers also will need to improve the climate for building infrastructure and enhancing the country’s electricity grids to support the data centers needed for generative artificial intelligence. This will require a sharper focus on cost-benefit analysis at the federal level, as well as better coordination with state and local authorities on permitting. Using federal financial support programs as carrots or sticks can be part of such a strategy.

Bessent’s emphasis on economic growth is spot on. By setting an ambitious 3% target for annual growth, he has provided the new administration a North Star to follow in devising its economic policies.

Welcome to the first podcast for the Spring 2025 semester from the Hubbard/O’Brien Economics author team. Check back for Blog updates & future podcasts which will happen every few weeks throughout the semester.

Join authors Glenn Hubbard & Tony O’Brien as they offer thoughts on tariffs in advance of the beginning of the new administration. They discuss the positive and negative impacts of tariffs -and some of the intended consequences. They also look at the AI landscape and how its reshaping the US economy. Is AI responsible for recent increased productivity – or maybe just the impact of other factors. It should be looked at closely as AI becomes more ingrained in our economy.

Image generated by GTP-4o illustrating labor productivity

Several articles in the business press have discussed the recent increases in labor productivity. For instance, this article appeared in this morning’s Wall Street Journal (a subscription may be required).

The most widely used measure of labor productivity is output per hour of work in the nonfarm business sector. The BLS calculates output in the nonfarm business sector by subtracting from GDP production in the agricultural, government, and nonprofit sectors. (The definitions used by the Bureau of Labor Statistics (BLS) in estimating labor productivity are discussed in the “Technical Notes” that appear at the end of the BLS’s quarterly “Productivity and Costs” releases.) The blue line in the following figure shows the annual growth rate in labor productivity in the nonfarm business sector as measured by the percentage change from the same quarter in the previous year. The green line shows labor productivity growth in manufacturing.

As the figure shows, both labor productivity growth in the nonfarm business sector and labor productivity growth in manufacturing are volatile. The business press has focused on the growth of productivity in the nonfarm business sector during the period from the third quarter of 2023 through the third quarter of 2024. During this time, labor productivity has grown at an average annual rate of 2.5 percent. That growth rate is notably higher than the growth rate that many economists are expecting over the next 10 years. For instance, the Congressional Budget Office (CBO) has forecast that labor productivity will grow at an average annual rate of only 1.6 percent over the period from 2025 to 2034.

The CBO forecasts that the total numbers of hours worked in the economy will grow at an average annual rate of 0.5 percent. Combining that estimate with a 2.5 percent annual rate of growth of labor productivity results in output per person—a measure of the standard of living—increasing by 34 percent by 2034. If labor productivity increases at a rate of only 1.6 percent, then output per person will have increased by only 23 percent by 2034.

The standard of living of the average person in United States increasing 11 percent more would make a noticeable difference in people’s lives by allowing them to consume and save more. Higher rates of labor productivity growth leading to a faster growth rate of income and output would also increase the federal government’s tax revenues, helping to decrease federal budget deficits that are currently forecast to be historically large. (We discuss the components of long-run economic growth in Macroeconomics, Chapter 16, Section 16.7; Economics, Chapter 26, Section 26.7, and the economics of long-run growth in Macroeconomics, Chapter 11; Economics, Chapter 21.)

Can the recent growth rates in labor productivity be maintained over the next 10 years? There is an historical precedent. Labor productivity in the nonfarm business sector grew at an average annual rate of 2.6 percent between 1950 and 1973. But growth rates that high have proven difficult to achieve in more recent years. For instance, from 2008 to 2023, labor productivity grew at an average annual rate of only 1.5 percent. (We discuss the debate over future growth rates in Macroeconomics, Chapter 11, Section 11.3; Economics, Chapter 21, Section 21.3.)

The Wall Street Journal article we cited earlier provides an overview of some of the factors that may account for the recent increase in labor productivity growth rates. The 2020 Covid pandemic may have led to some increases in labor productivity. Workers who temporarily or permanently lost their jobs as businesses closed during the height of the pandemic may have found new jobs that better matched their skills, making them more productive. Similarly, businesses that were forced to operate with fewer workers, may have found ways to restore their previous levels of output with lower levels of employment. These changes may have led to one-time increases in labor productivity at some firms, but are unlikely to result in increased rates of labor productivity growth in the future.

Some businesses have used newly available generative artificial intelligence (AI) software to increase labor productivity by, for instance, using software to replace workers who previously produced marketing materials or responded to customer questions or complaints. It will take at least several years before generative AI software spreads throughout the economy, so it seems too early for it to have had a broad enough effect on the economy to be visible in the productivity data.

Note also that, as the green line in the figure above shows, manufacturing productivity has been lagging recently. From the third quarter of 2023 to the third quarter of 2024, labor productivity in manufacturing has increased at an annual average rate of only 0.4 percent. This slowdown is surprising given that over the long run productivity in manufacturing has typically increased faster than has productivity in the overall economy. It seems unlikely that labor productivity in the overall economy can sustain its recent growth rates if labor productivity growth in manufacturing continues to lag.

Finally, the productivity data are subject to revision as better estimates of output and of hours worked become available. It’s possible that what appear to be rapid rates of productivity growth during the last five quarters may turn out to have been less rapid following data revisions.

So, while the recent increase in the growth rate of labor productivity is an encouraging sign of the strength of the U.S. economy, it’s too soon to tell whether we have entered a sustained period of higher productivity growth.