On September 27, the Bureau of Economic Analysis (BEA) released its “Personal Income and Outlays” report for August, which includes monthly data on the personal consumption expenditures (PCE) price index. Inflation as measured by annual changes in the consumer price index (CPI) receives the most attention in the media, but the Federal Reserve looks instead to inflation as measured by annual changes in the PCE price index to evaluate whether it’s meeting its 2 percent annual inflation target.

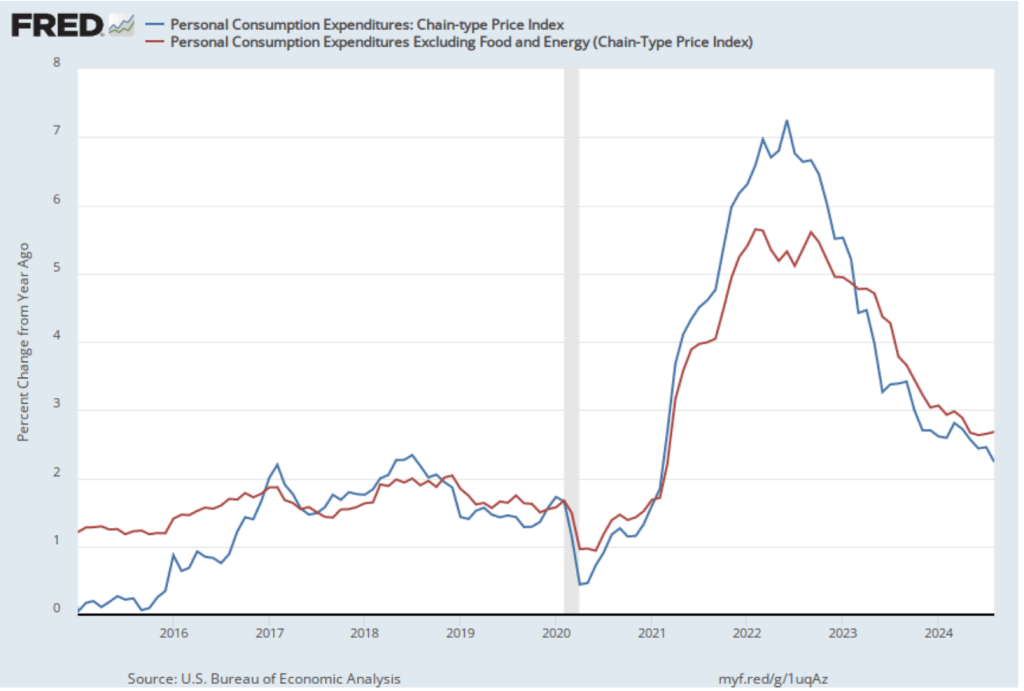

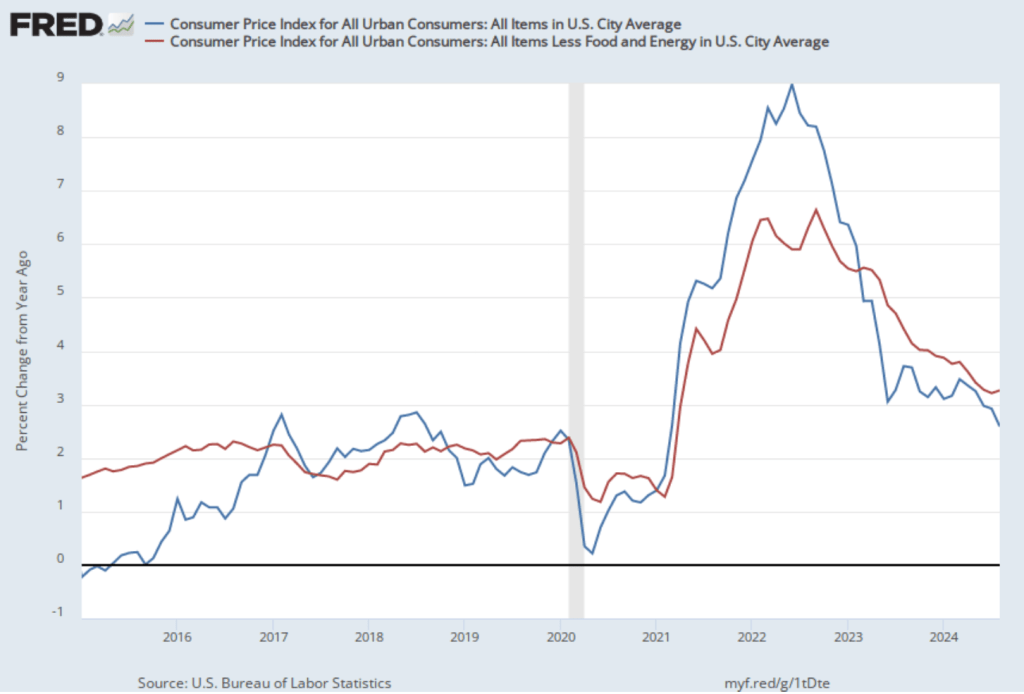

The following figure shows PCE inflation (blue line) and core PCE inflation (red line)—which excludes energy and food prices—for the period since January 2015 with inflation measured as the percentage change in the PCE from the same month in the previous year. Measured this way, PCE inflation (the blue line) was 2.2 percent in August, down from 2.7 percent in July. Core PCE inflation (the red line) ticked up in August to 2.7 percent from 2.6 percent in July.

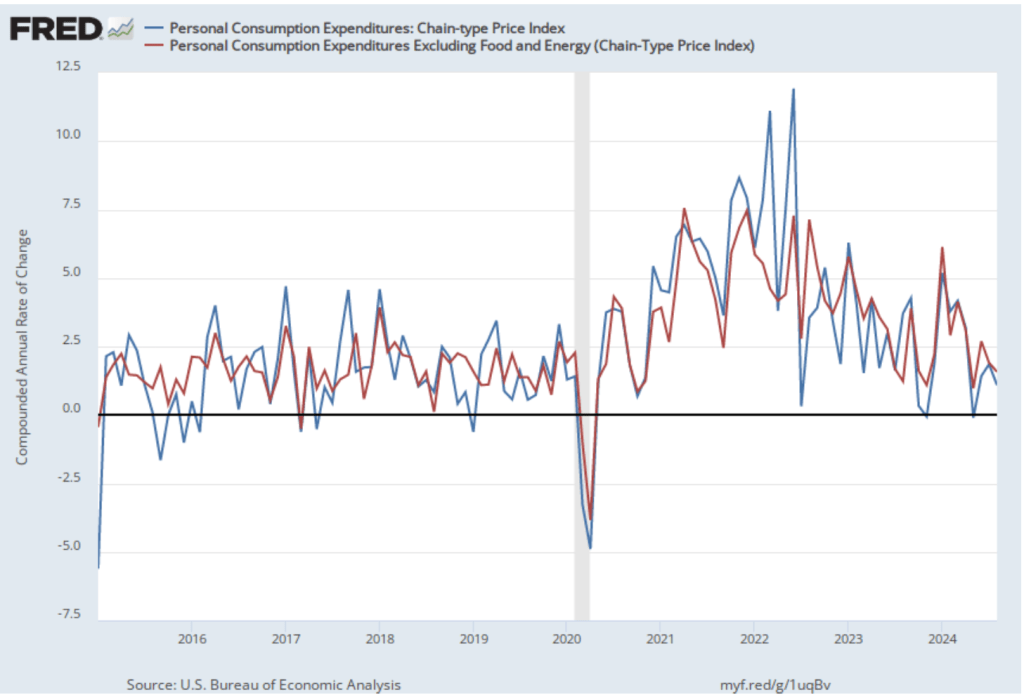

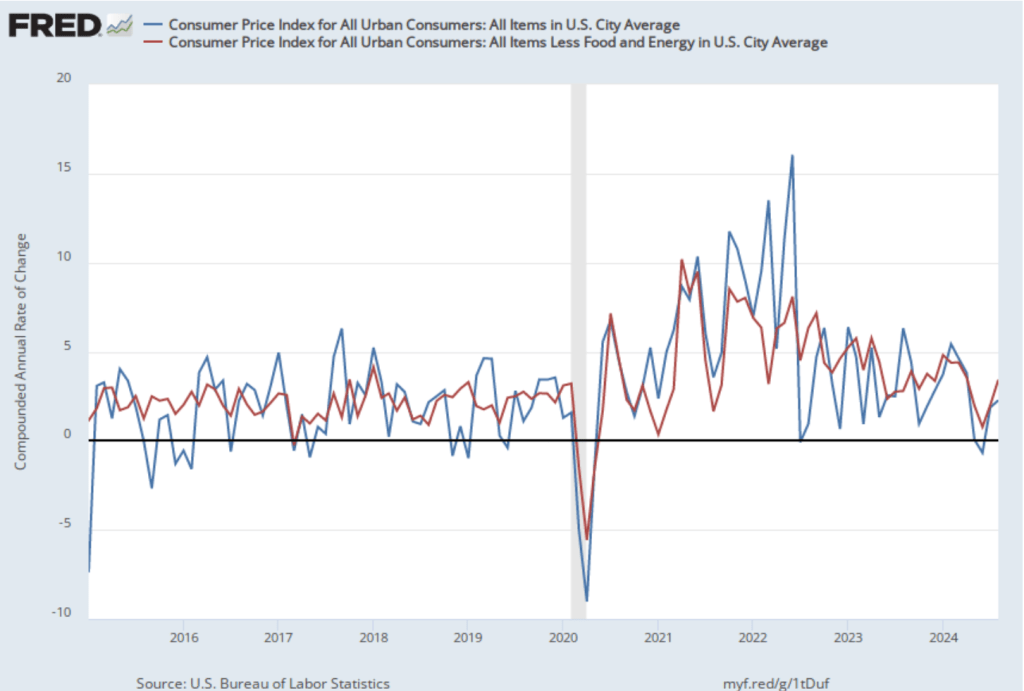

The following figure shows PCE inflation and core PCE inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month inflation, while this figure shows 1-month inflation.) Measured this way, PCE inflation declined from 1.9 percent in July to 1.1 percent in August, well below the Fed’s 2 percent inflation target. Core PCE inflation declined from 1.9 percent in July to 1.6 percent in August. Calculating inflation this way focuses only on the most recent data, and so reinforces the conclusion that inflation has slowed significantly from the higher rates seen at the beginning of this year.

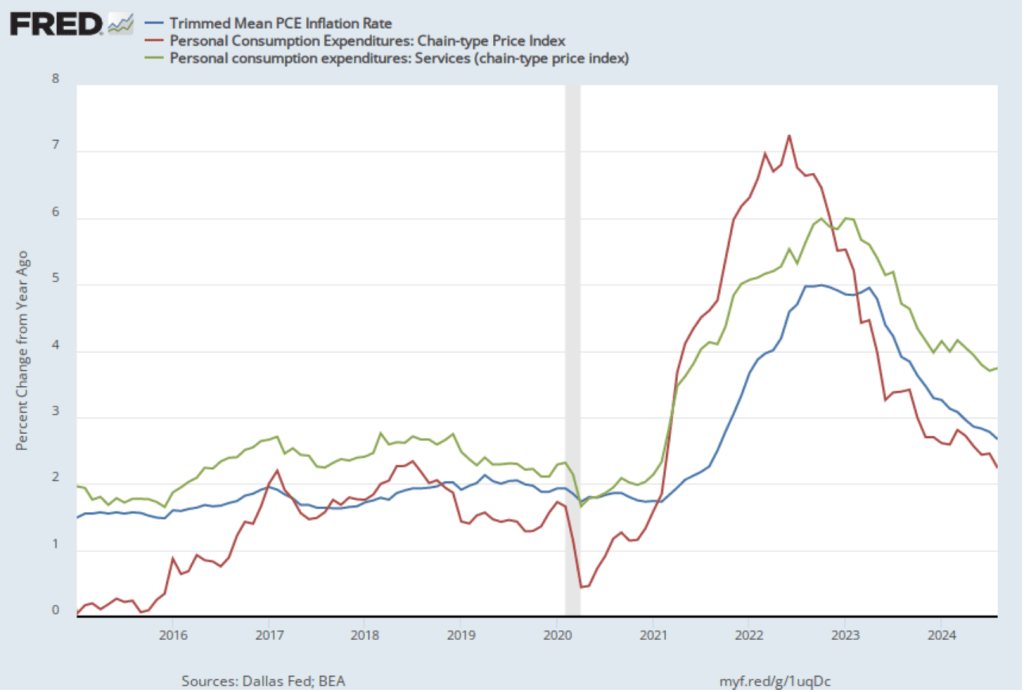

The following figure shows other ways of gauging inflation by including the 12-month inflation rate in the PCE (the same as shown in the figure above—although note that PCE inflation is now the red line rather than the blue line), inflation as measured using only the prices of the services included in the PCE (the green line), and the trimmed mean rate of PCE inflation (the blue line). Fed Chair Jerome Powell and other members of the Federal Open Market Committee (FOMC) have said that they are concerned by the persistence of elevated rates of inflation in services. The trimmed mean measure is compiled by economists at the Federal Reserve Bank of Dallas by dropping from the PCE the goods and services that have the highest and lowest rates of inflation. It can be thought of as another way of looking at core inflation by excluding the prices of goods and services that had particularly high or particularly low rates of inflation during the month.

Inflation using the trimmed mean measure was 2.7 percent in August (calculated as a 12-month inflation rate), down only slightly from 2.6 percent in July—still above the Fed’s target inflation rate of 2 percent. Inflation in services remained high in August at 3.7 percent, the same as in July.

Today’s data indicate that the economy is still on a path for a soft landing in which the inflation rate returns to the Fed’s 2 percent target without the economy slipping into a recession. Looking forward, both the Federal Bank of Atlanta’s GDPNow forecast and the Federal Reserve Bank of New York’s GDP Nowcast project that real GDP will increase at annual rate of more than 3 percent in the third quarter (which ends in three days). So, at this point there is no indication that the economy is slipping into a recession. The next Employment Situation report will be released on October 4 and will provide more information on the state of the labor market.

Image generated by GTP-4o of the U.S. Department of Labor building

The Census Bureau and the Bureau of Labor Statistics (BLS) jointly conduct the monthly Current Population Survey (CPS). As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), the BLS uses the data gathered by the CPS to calculate a number of important labor market statistics including the unemployment rate, the labor force participation rate, and the employment-population ratio.

Unfortunately, over the years Congress has not increased its appropriations for the BLS enough to cover the increasing costs of surveying 60,000 households each month. As a result, the BLS has announced that beginning in January 2025, it will be surveying fewer households in each month’s CPS.

Glenn has joined 120 other economists who have served over the years on the President’s Council of Economic Advisers (CEA) in writing a letter to Congress urging that the BLS be given sufficient funds to maintain the current size of the CPS sample and to begin steps to modernize the collection of the sample.

The letter notes that: “Reducing the CPS sample size will make its statistics less reliable…. will also hinder accurate analysis of states and local areas and subpopulations, including teenagers, seniors, veterans, people with disabilities, the self-employed, people who identify as Asian, Hispanic or Latino ethnicity, and Black or African Americans.”

Supports: Macroeconomics, Microeconomics, Economics, and Essentials of Economics, Chapter 3, Section 3.1.

Photo from theathletic.com

Caitlin Clark had a sensational college career at the University of Iowa, being named National Player of the Year in her junior and senior years. She was chosen first by the Indiana Fever in the 2024 Women’s National Basketball Association (WNBA) draft of college players. Her popularity drew large crowds to both her home and away games during the 2024 season.

In 2023, the Indiana Fever sold an average of 4,067 tickets to its home games. In 2024, with Clark on the team, the Fever sold an average of 17,036 to its home games. The average price the Fever charged per ticket increased from $60 in 2023 to $110 in 2024. As an article on theathletic.com put it: “Despite the higher price point, even more tickets were sold [by the Fever] this year.”

Can we conclude from this information that Caitlin Clark is so popular that the demance curve for Fever tickets is upward sloping? Briefly explain.

Solving the Problem Step 1: Review the chapter material. This problem is about the effect of a price change on the quantity demand of a good or service, so you may want to review Chapter 3, Section 3.1, “The Demand Side of the Market.”

Step 2: Answer the question by explaining whether it’s likely that the demand curve for tickets to Fever games is upward sloping. It’s unlikely that the demand curve for tickets to Fever games is upward sloping. The law of demand states that, holding everything else constant, when the price of a product rises, the quantity demanded of the product will decrease. When the Fever raised ticket prices from $60 in 2023 to $100 in 2024, we would expect the result to be a movement up the demand curve for tickets, resulting in fewer tickets sold, provided that everything else that would affect the demand for tickets was constant between 2023 and 2024. But everything wasn’t constant because the Fever had Clark on the team in 2024 but not in 2023. Her popularity increased the demand for tickets, shifting the demand curve to the right. In other words, the shift in demand allowed the Fever to sell more tickets at a higher price—moving from a price of $60 and a quantity of 4,067 on the 2023 demand curve to a price of $110 and a quantity of 17,036 on the 2024 demand curve.

Glenn serves on the the Grand Bargain Committee, chaired by Michael Strain of the American Enterprise Institute and Isabel Sawhill of the Brookings Institution. The committee, whose members span the political spectrum, have prepared a report that addresses some of the country’s most pressing economic and social problems.

Glenn and Michael Strain prepared the following introduction to the report. Below there is a link to the whole report.

The views expressed in this report are those of the individual authors who collectively constitute the Grand Bargain Committee, co-chaired by Michael R. Strain and Isabel V. Sawhill. This report was sponsored by the Center for Collaborative Democracy and was prepared independent of influence from the center and from any other outside party or institution. It is being published by the Bipartisan Policy Center as an example of how people with diverse views and political leanings can find common ground. The recommendations are strictly those of the policy experts and do not necessarily reflect the views of any organization or those of the BPC. All data are current as of November 2023.

By: Eric Hanushek, G. William Hoagland, Douglas Holtz-Eakin, R. Glenn Hubbard, Maya MacGuineas, Richard V. Reeves, Robert D. Resichauer, Gerard Robinson, Isabel V. Sawhill, Diane Schanzenbach, Richard Schmalensee, Michael R. Strain, and C. Eugene Steuerle.

Introduction

The United States faces serious economic and social challenges, including:

The underlying economic growth rate has slowed, as have opportunities for people to move up the economic ladder.

Our education system fails too many children and leaves many more with fewer opportunities than they deserve.

The nation is not rising to the challenge of addressing climate change.

Both our health care system and the health of our population need improvement.

Our income tax system is broken, generating tax revenue in an inefficient and unfair manner.

And the national debt is growing at an unsustainable pace, threatening long-term economic growth, crowding out needed investments in economic opportunity, and placing the nation’s ability to respond to a future crisis at risk.

To address these problems, the Center for Collaborative Democracy commissioned subject matter experts—progressives, centrists, and conservatives—to develop a “Grand Bargain” encompassing all six issues. The policy debate typically puts these problems into silos, and within each silo, powerful forces support the status quo. This report seeks to break down these silos. Dealing with them all at once—in a Grand Bargain—is a more promising strategy than dealing with them individually, because it allows for different parties to strike deals across policy issues, not just within a single issue.

For example, implementing a carbon tax to address climate change seems impossibly difficult. So does increasing accountability for teacher performance. Trading one for the other might be easier than pursuing both in isolation. Fixing the structural budget deficit by reducing entitlement spending is an enormous political challenge. So is increasing spending on programs that advance economic opportunity. Doing both at the same time could be more politically feasible than addressing them separately.

In this context, the group of experts met for several months in 2023 to share perspectives and ideas and to come up with sensible policies in each of these areas: economic growth and mobility; education; environment; health; taxes; and the federal budget. The end result is this report, which is being published by the Bipartisan Policy Center as an example of how people with diverse views and political leanings can find common ground.

This report is short, consisting of less than 30 pages of text. Its brevity is by design. This constraint forced the group to stay focused on issues and recommendations that matter the most. The focus of the report is on concepts. It is designed to answer such questions as, “How should the nation’s approach to education or to the federal budget change? What fundamental reforms are required to increase the underlying rates of economic growth and upward mobility?” Focusing on concepts means not focusing on policy details, including the details of implementing our recommendations and of transitioning across policy regimes. Our lack of attention to policy details does not mean we do not recognize their importance. Of course, we do, and many members of the group have spent much of their careers studying and designing public policies. Instead, we focus on concepts because we believe the United States needs to return to a discussion of first principles. This report advances that objective.

Not every member of the group agrees with every recommendation in this report. That is not surprising given the diversity of views in the group, and the difficulty and complexity of many of the issues we address. Despite this disagreement, we were able to have an informed and constructive discussion about these economic issues, to find compromises, and to come up with a set of recommendations that we believe, on balance, would greatly strengthen the country and improve people’s lives.

We believe in the importance of a market economy. Free markets have led to unprecedented growth and innovation, along with rising incomes, over the past three centuries. But government also has a role to play. To unleash more growth, we need to curtail unneeded or overly costly regulations and to create a tax system that encourages investment spending and innovation. To bring prosperity to more people, we need policies that will enable more people to benefit from economic growth through investment in their education and skills. For this reason, we put a great deal of emphasis on improving education for children, on training or retraining for adult workers, and on subsidizing the earnings of low-wage workers when necessary while maintaining a safety net for those who cannot work.

Our proposals are designed to advance certain underlying values and themes: Work and savings should be rewarded, investment should be encouraged over consumption, public assistance should be better targeted to those most in need, the tax system should be more progressive, and the nation should invest relatively more in the young and spend relatively less on the elderly.

Our specific proposals in each area are as follows:

On economic growth and mobility, we recommend investing in the education and training of workers, through community colleges and apprenticeships. We call for a more skill-based immigration system and for more immigrants; for encouraging innovation by investing more in basic research; for reducing taxes on new investment; for curbing unneeded regulation; for reducing the national debt; and for encouraging participation in economic life by increasing the generosity of earnings subsidies for low-wage workers.

On education, we recommend improving the teacher workforce at the K-12 level; paying teachers more but strengthening the link between pay and performance; maintaining educational standards and accountability while narrowing gaps by race and class; expanding school choice; and recognizing the role that parents and families must play in students’ learning.

On the environment, our main recommendation is to adopt a carbon tax. We also call for reducing methane emissions; expanding federal authority in the planning, siting, and permitting of the national electric transmission system; and repealing the renewable fuel standard that requires refiners to blend corn ethanol into the fuel they sell.

On health, we call for giving more attention to the social determinants of poor health with a focus on the need for better nutrition, for rationalizing existing subsidies for health care, and for reducing health care costs.

On taxes, we call for increasing tax revenue as a share of annual gross domestic product (GDP), and for that revenue to be raised in a manner that is more progressive, efficient, and simple than under current law, while also increasing the incentive to save and invest. For the business sector, that means allowing the expensing of investment expenditures and moving toward equal treatment of the corporate and noncorporate sectors.

On the federal budget, we recommend putting the debt as a share of annual GDP on a sustainable trajectory with a comprehensive package of reforms made up of a rough balance between tax increases and spending cuts in the initial years, phasing into a much larger share of the savings coming from spending cuts over time.

Most of these recommendations are at the federal level, but some are at the state and local level, particularly our education recommendations.

In the spirit of a Grand Bargain, these recommendations advance common goals and values through compromises both within and across policy areas. For example, one of our values is reflected in the goal of refocusing government spending on those who truly need it, and another is to restore fiscal responsibility. To accomplish this, we call for slower growth in Social Security and Medicare benefits for affluent seniors to reduce the major driver of the national debt, but we also protect vulnerable seniors and spend more on the education of children and on earnings subsidies for the working poor. We recommend adopting a carbon tax because it will simultaneously advance our goals of supporting the environment, increasing tax revenue, and boosting dynamism by encouraging innovation in the energy sector.

We believe the analysis and recommendations in this report point a path forward for the nation, but we offer them in a spirit of humility, understanding that others will disagree. We hope that this report catalyzes a much needed debate about the future of our nation.

Federal Reserve Governor Michelle Bowman (Photo from federalreserve.gov)

Federal Reserve Chairs place a high value on consensus, particularly with respect to the decisions of the Federal Open Market Committee (FOMC) setting the target for the federal funds rate. (Note that the chair of the Fed’s Board of Governors also serves as the chair of the FOMC.) As we discuss in Macroeconomics, Chapter 14, Section 14.4 (Economics, Chapter 24, Sectio 24.4), the FOMC has 12 voting members: the 7 members of the Board of Governors, the president of the Federal Reserve Bank of New York, and 4 of the other 11 District Bank presidents, who serve rotating one-year terms.

Decisions by the FOMC in setting the target for the federal funds rate are usually unanimous. Prior to the FOMC meeting on September 17-18, each vote of the committee had been unanimous since Esther George, president of the Federal Reserve Bank of Kansas City cast a dissenting vote at the meeting on June 14-15, 2022. At that meeting, the committee voted to raise its target for the federal funds rate by 0.75 percentage point (75 basis points). George voted against the move because she believed a 0.50 percentage point (50 basis points) increase would have been more appropriate.

At the September 17-18 meeting, Fed Governor Michelle Bowman voted against the decision to reduce the target for the federal funds rate by 50 basis points because she believed a cut of 25 basis point would have been more appropriate. She was the first member of the Board of Governors to cast a dissenting vote at an FOMC meeting since 2005.

Perhaps because it’s unusual for a member of the Board of Governors to dissent from an FOMC decision, Bowman issued a statement explaining her vote. In her statement, Bowman argued that although inflation has declined substantially over the past two years, she was concerned that inflation as measured by the 12-month percentage change in the core personal consumption expenditures (PCE) price index was still 2.5 percent—above the Fed’s target inflation rate of 2 percent: “Although it is important to recognize that there has been meaningful progress on lowering inflation, while core inflation remains around or above 2.5 percent, I see the risk that the Committee’s larger policy action could be interpreted as a premature declaration of victory on our price stability mandate.” (Note that the Fed uses the PCE rather than the core PCE to gauge whether it is hitting its inflation target, but core PCE is generally thought to be a better indicator of the underlying inflation rate.)

Bowman also noted the difficulty of interpreting developments in the labor market: “My reading of labor market data has become more uncertain due to increased measurement challenges and the inherent difficulty in assessing the effects of recent immigration flows.” (We discuss the effects on employment measures of differing estimates of the level of immigration in this blog post.)

Federal Reserve Chair Jerome Powell (Photo from federalreserve.gov)

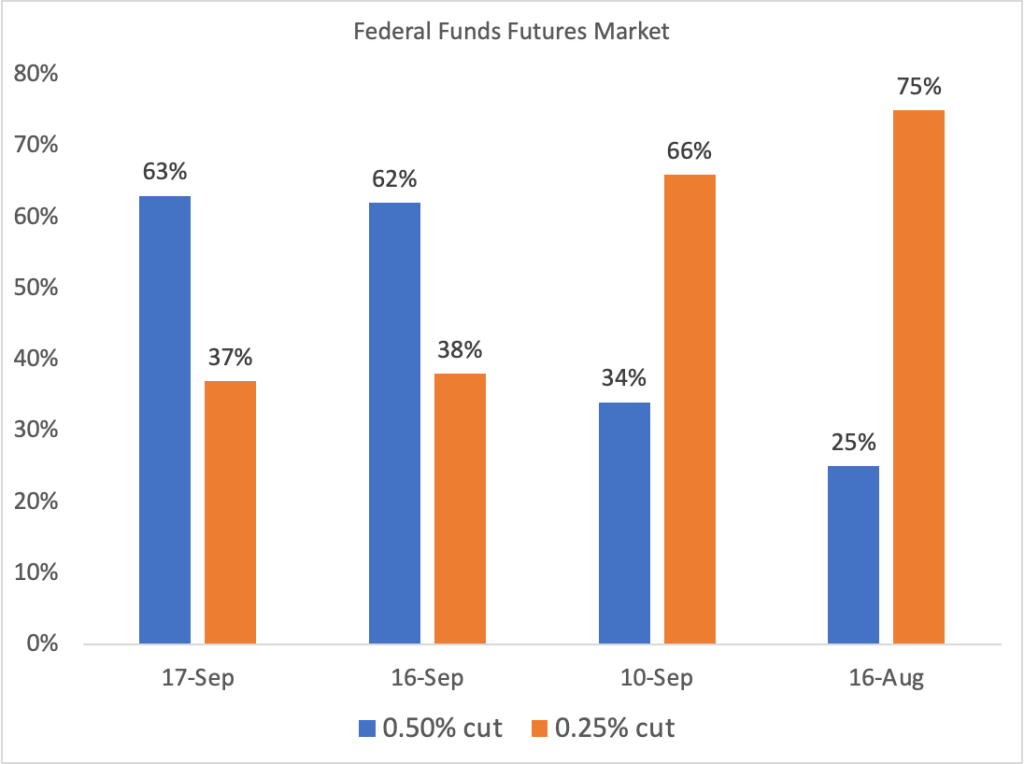

In a blog post yesterday (September 17), we noted that trading on the CME’s federal funds futures market indicated that investors assigned a probability of 63 percent to the Federal Open Market Committee (FOMC) announcing today a 0.50 percentage point (50 basis points) cut to its target range for the federal funds rate and a probability of 37 percent to a 0.25 percentage point (25 basis points) cut. (100 basis points equals 1 percentage point.) The forecast proved correct when the FOMC announced this afternoon that it was cutting its target range to 4.75 percent to 5.00 percent, from the range of 5.25 percent to 5.50 percent that had been in place since July 2023.

Congress has given the Fed a dual mandate to achieve maximum employment and price stability. In March 2022, the FOMC began responding to the surge in inflation that had begun in the spring of 2021 by raising its target for the federal funds rate. Up through its July 2024 meeting, the FOMC had been focused on the risk that the inflation rate would remain above the Fed’s target inflation rate of 2 percent. In the statement released after today’s meeting, the committee stated that it “has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance.”

In a press conference following the meeting, Fed Chair Jerome Powell indicated that with inflation close to the 2 percent target and the labor market continuing to cool “by any measure,” the committee judged that it was time to begin normalizing its target range for the federal funds rate. Powell said that: “The U.S. economy is in a good place and our action is intended to keep it there.” When asked by a reporter whether the committee cut its target by 50 basis points today to catch up for not having cut its target at its July meeting, Powell responded that: “We don’t think we’re behind [on cutting the target range]. We think this [50 basis point cut] will keep us from falling behind.”

At the conclusion of each meeting, the committee holds a formal vote on its target for the federal funds rate. The vote today was 15-1, with Governor Michelle Bowman casting the sole negative vote. She stated that she would have preferred a 25 basis point cut. Dissenting votes have been rare in recent years.

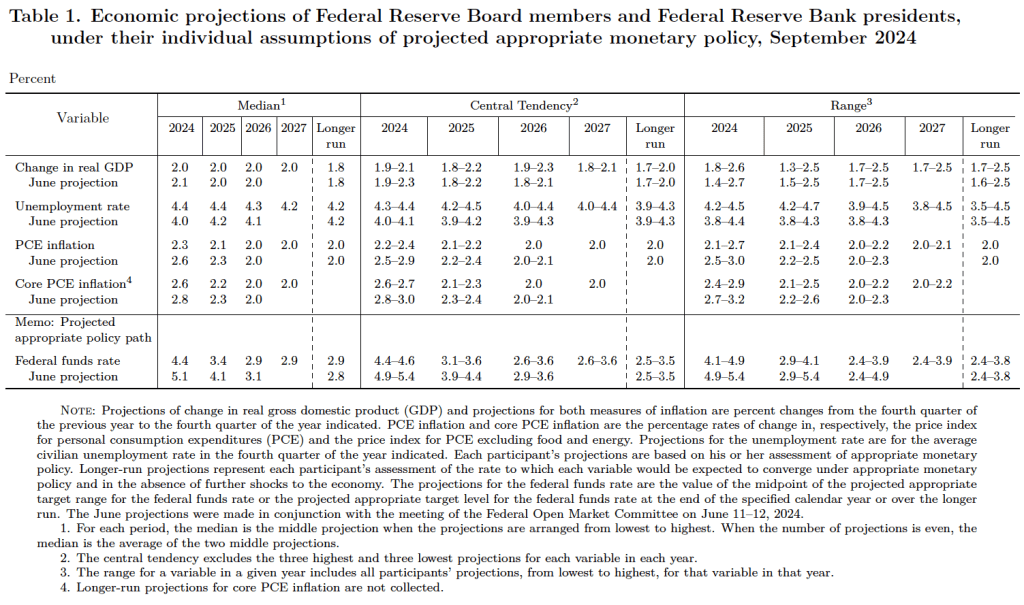

How much lower will the federal funds target range go? Typically at the FOMC’s December, March, June, and September meetings, the committee releases a “Summary of Economic Projections” (SEP), which presents median values of the committee members’ forecasts of key economic variables. The following table is from the SEP released after today’s meeting.

Looking at the values under the heading “Median” on the left side of the table, the median projection for the federal funds rate at the end of the 2024 is 4.4 percent. That projection signals that the committee will likely cut its target range by 25 basis points at each of its two remaining meetings on November 6-7 and December 17-18. The median projection for the federal funds rate at the end of 2025 is 3.4 percent, implying four additional 25 basis points cuts. In the long run, the median projection of the committee is that the federal funds rate will be 2.9 percent, which is somewhat higher than the 2.5 percent rate that the committee had projected at its December 2019 meeting before the start of the Covid pandemic.

Committee members project that the unemployment rate will end the year at 4.4 percent, up from the 4.2 percent rate in August. They expect that the unemployment rate will be 4.2 percent in the long run. The long run unemployment rate is ofter referred to as the natural rate of unemployment. (We discuss the natural rate of unemployment in Macroeconomics, Chapter 9, Section 9.2 and Economics, Chapter 19, Section 19.2.)

The median projection of the committe members is that at the end of 2024 the inflation rate, as measured by the percentage change in the personal consumption expenditures (PCE) price index, will be 2.3 percent, slightly above the Fed’s target rate. Inflation will also run slightly above the Fed’s target in 2025 at 2.1 percent before retuning to 2 percent by the end of 2026. The median projections of the inflation rate at the ends of 2024 and 2025 are lower than the median projections in the SEP that was released after the FOMC meeting on June 11-12.

Image generated by GTP-4o “illustrating interest rates.”

Tomorrow (September 18) at 2 p.m. EDT, the Federal Reserve’s policy-making Federal Open Market Committee (FOMC) will announce its target for the federal funds rate. It’s been clear since Fed Chair Jerome Powell’s speech on August 23 at the Kansas City Fed’s annual monetary policy symposium held in Jackson Hole, Wyoming that the FOMC would cut its target for the federal funds rate at its meeting on September 17-18. (We discuss Powell’s speech in this blog post.)

The only suspense has been over the size of the cut. Traditionally, the FOMC has raised or lowered its target for the federal funds rate in 0.25% (or 25 basis points) increments. Occasionally, however, either because economic conditions are changing rapidly or because the committee concludes that it has been adjusting its target too slowly (“fallen behind the curve” is the usual way of putting it) the committee makes 0.50% (50 basis points) changes to its target.

Futures markets allow investors to buy and sell futures contracts on commodities–such as wheat and oil–and on financial assets. Investors can use futures contracts both to hedge against risk—such as a sudden increase in oil prices or in interest rates—and to speculate by, in effect, betting on whether the price of a commodity or financial asset is likely to rise or fall. (We discuss the mechanics of futures markets in Chapter 7, Section 7.3 of Money, Banking, and the Financial System.) The CME Group was formed from several futures markets, including the Chicago Mercantile Exchange, and allows investors to trade federal funds futures contracts. The data that result from trading on the CME indicate what investors in financial markets expect future values of the federal funds rate to be.

The following figure summarizes the implied probabilities from federal funds rate futures trading of the FOMC cutting its target by 25 basis points (the orange bars) or 50 basis points (the blue bars) at tomorrow’s meeting. The probabilities on four days are shown—today, yesterday, one week ago, and one month ago.

The figure shows how sentiment among investors has changed over the past month. On August 16, investors assigned a 75 percent probability of a 25 basis point cut in the target range and only a 25 percent probability of a 50 basis point cut. Yesterday and today, investor sentiment has swung sharply toward expecting a 50 basis point cut. Why the shift? As the Fed attempts to fulfill its dual mandate of maximum employment and price stability, it’s focus since the spring of 2022 had been on bringing inflation back down to its 2 perecent target. But as the unemployment rate has slowly risen, output growth has cooled, and more consumers are delinquent on their auto loan and credit card payments, some members of the committee now believe that the committee made a mistake in not cutting the target range by 25 basis points at its last meeting at the end of July. For these members, a 50 basis point cut tomorrow would bring the changes in the target range back on track.

How well did investors in the federal funds futures market forecast the FOMC’s decision? If you are reading this after 2 p.m. EDT on September 18, you’ll know the answer.

Welcome to the first podcast for the Fall 2024 semester from the Hubbard/O’Brien Economics author team. Check back for Blog updates & future podcasts which will happen every few weeks throughout the semester.

Join authors Glenn Hubbard & Tony O’Brien as they provide an update on the Macroeconomy. They offer thoughts on the likelihood of a soft landing and whether the actions of the Federal Reserve helped or hindered that process. The monetary and fiscal challenges facing the new administration are real and the Fed will begin its process of rate-cutting this week in the upcoming FOMC meeting. Gain insight into this evolving situation by listening to this podcast. Click HERE to access the podcast.

Today (September 11), the Bureau of Labor Statistics (BLS) released its monthly report on the consumer price index (CPI). This report is the last one that will be released before the Fed’s policy-making Federal Open Market Committee (FOMC) holds its next meeting on September 17-18.

As the following figure shows, the inflation rate for August measured by the percentage change in the CPI from the same month in the previous month—headline inflation (the blue line)—was 2.6 percent down from 2.9 percent in July. Core inflation (the red line)—which excludes the prices of food and energy—increased slightly to 3.3 percent in August from 3.2 percent in July. Headline inflation was slightly below what economists surveyed by the Wall Street Journal had expected, while core inflation was slightly higher.

As the following figure shows, if we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—we see that both headline and core inflation increased. Headline inflation (the blue line) increased from 1.8 percent in July to 2.3 percent in August. Core inflation (the red line) jumped from 2.0 percent in July to 3.4 percent in August. Overall, we can say that, taking 1-month and 12 month inflation together, the U.S. economy may still be on course for a soft landing—with the annual inflation rate returning to the Fed’s 2 percent target without the economy being pushed into a recession—but the increase in 1-month inflation is concerning. Of course, as always, it’s important not to overinterpret the data from a single month. (Note, also, that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI in evaluating whether it is hitting its 2 percent inflation target.)

As we’ve discussed in previous blog posts, Federal Reserve Chair Jerome Powell and his colleagues on the FOMC have been closely following inflation in the price of shelter. The price of “shelter” in the CPI, as explained here, includes both rent paid for an apartment or house and “owners’ equivalent rent of residences (OER),” which is an estimate of what a house (or apartment) would rent for if the owner were renting it out. OER is included to account for the value of the services an owner receives from living in an apartment or house.

As the following figure shows, inflation in the price of shelter has been a significant contributor to headline inflation. The blue line shows 12-month inflation in shelter and the red line shows 1-month inflation in shelter. Twelve-month inflation in shelter reversed the decline that began in the spring of 2023, rising from 5.0 percent in July to 5.2 percent August. One-month inflation in shelter—which is much more volatile than 12-month inflation in shelter—increased from 4.6 percent in July to 5.2 percent in August, continuing an increase that began in June. The increase in 1-month inflation in shelter may concern the members of the FOMC, as may, to a lesser extent, the increase in 12-month inflation in shelter. Shelter has a smaller weight of 15 percent in the PCE price index that the Fed uses to gauge whether it is hitting its 2 percent inflation target in contrast with the 33 percent weight that shelter has in the CPI. But persistent shelter inflation in the 5 percent range would make a soft landing more difficult.

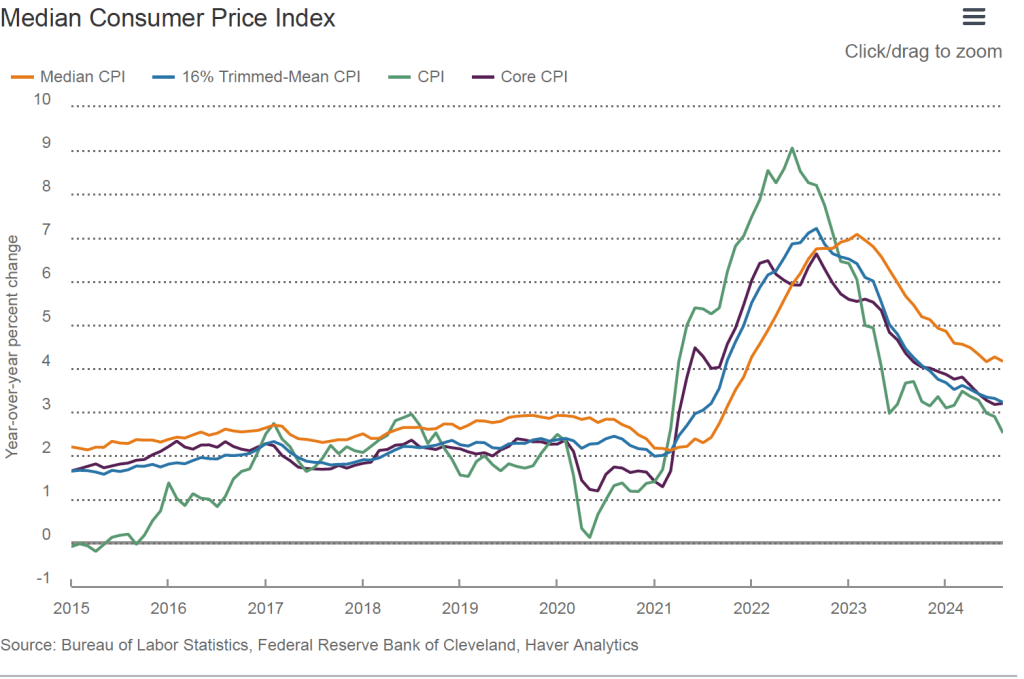

Finally, in order to get a better estimate of the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation. Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates. Trimmed mean inflation drops the 8 percent of good and services with the higherst inflation rates and the 8 percent of goods and services with the lowest inflation rates.

As the following figure (from the Federal Reserve Bank of Cleveland) shows, median inflation (the orange line) declined slightly from 4.3 percent in July to 4.2 percent in August. Trimmed mean inflation (the blue line) also declined slightly from 3.3 in July to 3.2 percent in August. These data provide confirmation that core CPI inflation is likely running higher than a rate that would be consistent with the Fed achieving its inflation target.

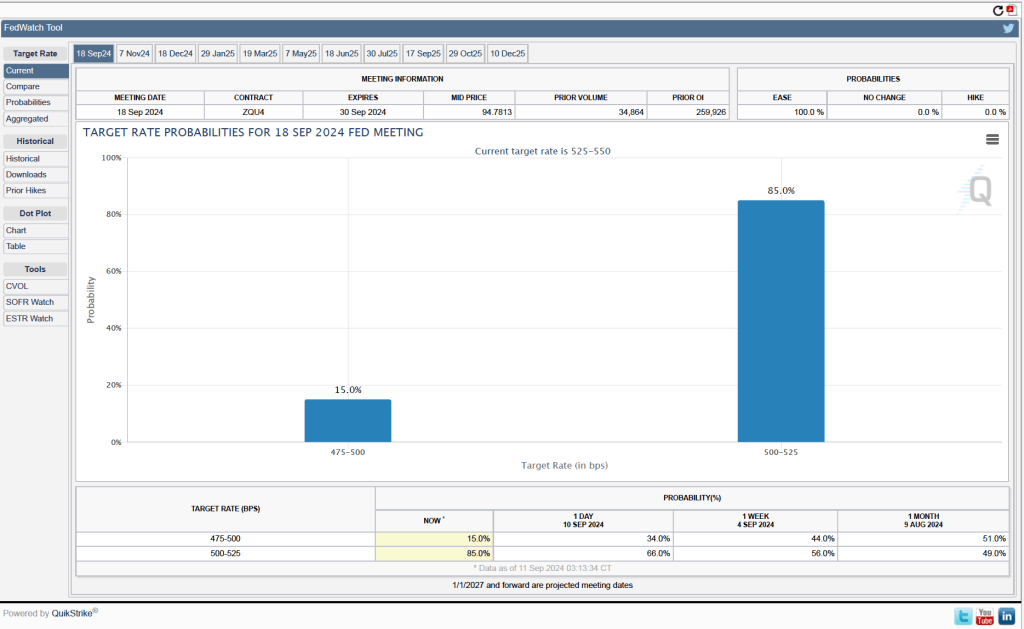

For the past few weeks Fed officials have been indicating that the FOMC is likely to cut its target for the federal funds at its next meeting on Septembe 17-18. Investors who buy and sell federal funds futures contracts expect that the FOMC will cut its target for the federal funds rate by 0.25 percentage point from the current range of 5.50 percent to 5.25 percent. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 85.0 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point at its next meeting and a probability of only 15.0 percent that the cut will be 0.50 percentage point.

The FOMC has to balance the risk of leaving its target for the federal funds rate at its current level for too long—increasing the risk of slowing demand so much that the economy slips into recession—against the risk of cutting its target too soon—increasing the risk that inflation persists above the Fed’s 2 percent target. We’ll see at the committee’s next meeting how Fed Chair Jerome Powell and the other members assess the current state of the economy as they consider when and by how much to cut their target for the federal funds rate.

The “Employment Situation” report (often referred to as the “jobs report”), which is released monthly by the Bureau of Labor Statistics (BLS), is always closely followed by economists and policymakers because it provides important insight in the current state of the U.S. economy. This month’s report is considered particularly important because last month’s report indicated that the labor market might be weaker than most economists had believed. As we discussed in a recent blog post, late last month Fed Chair Jerome Powell signaled that the Fed’s policy-making Federal Open Market Committee (FOMC) was likely to cut its target for the federal funds rate at its next meeting on September 17-18.

Economists and investment analysts had speculated that following August’s unexpectedly weak jobs report, another weak report might lead the FOMC to cut its federal funds target by 0.50 percentage rate rather than by the more typical 0.25 percent point. The jobs report the BLS released this morning (September 6) was mixed, showing a somewhat lower than expected increase in employment as measured by the establishment survey, but higher wage growth.

The jobs report has two estimates of the change in employment during the month: one estimate from the establishment survey, often referred to as the payroll survey, and one from the household survey. As we discuss in Macroeconomics, Chapter 9, Section 9.1 (Economics, Chapter 19, Section 19.1), many economists and policymakers at the Federal Reserve believe that employment data from the establishment survey provides a more accurate indicator of the state of the labor market than do either the employment data or the unemployment data from the household survey. (The groups included in the employment estimates from the two surveys are somewhat different, as we discuss in this post.)

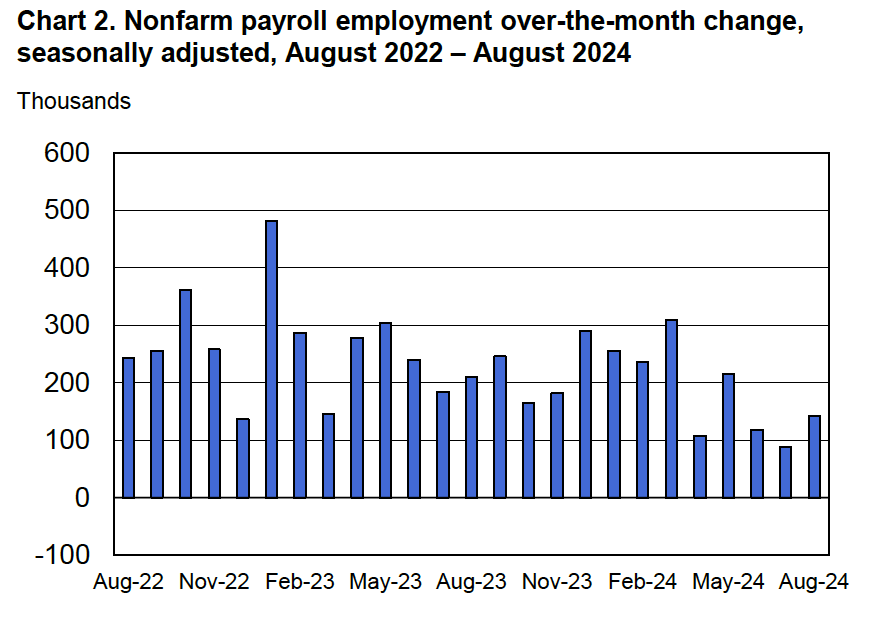

According to the establishment survey, there was a net increase of 142,000 jobs during August. This increase was below the increase of 161,000 that economists had forecast in a survey by the Wall Street Journal. The following figure, taken from the BLS report, shows the monthly net changes in employment for each month during the past two years. The BLS revised lower its estimates of the net increase in jobs during June and July by a total of 86,000. (The BLS notes that: “Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.”)

The BLS’s estimate of average monthly job growth during the last three months is now 116,000, a significant decline from an average of 211,000 per month during the previous three months and 251,000 per month during 2023.

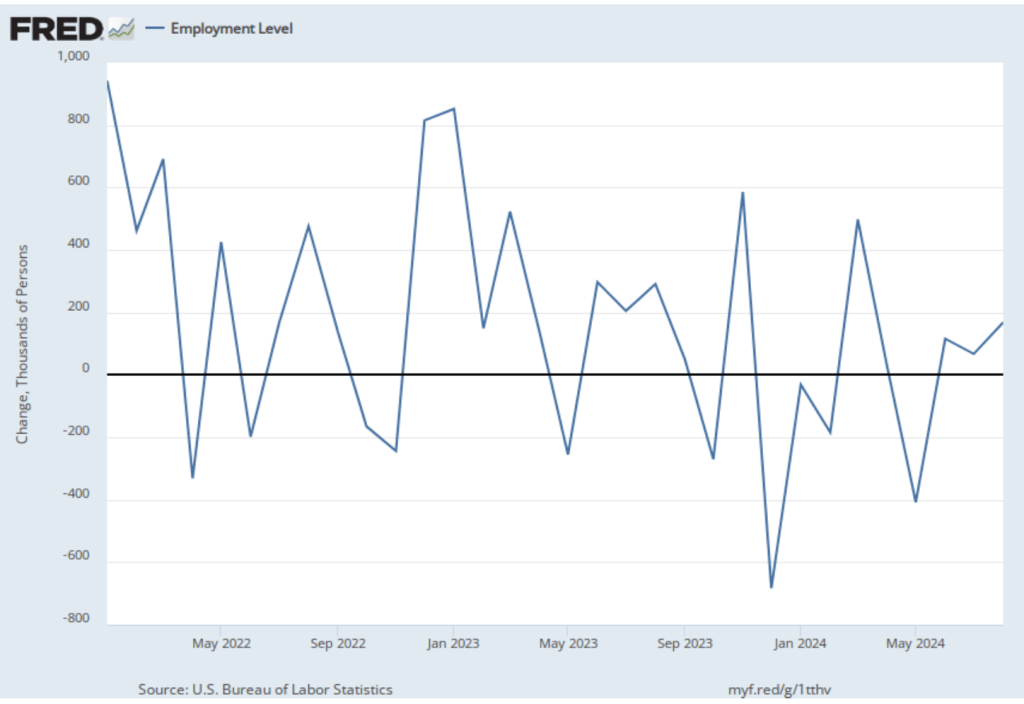

As the following figure shows, the net change in jobs from the household survey moves much more erratically than does the net change in jobs in the establishment survey. The net change in jobs as measured by the household survey increased from 67,000 in July to 168,000 in August. So, in this case the direction of change in the two surveys was the same—an increase in the net number of jobs created in August compared with July.

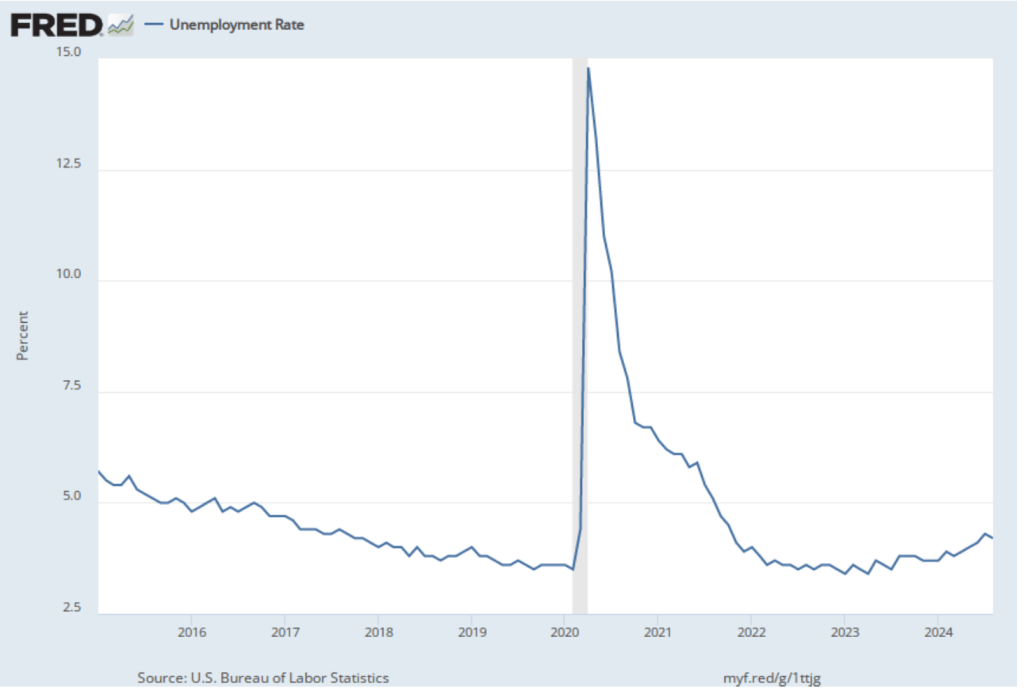

As the following figure shows, the unemployment rate, which is also reported in the household survey, decreased from 4.3 percent to 4.2 percent—breaking what had been a five month string of unemployment rate increases.

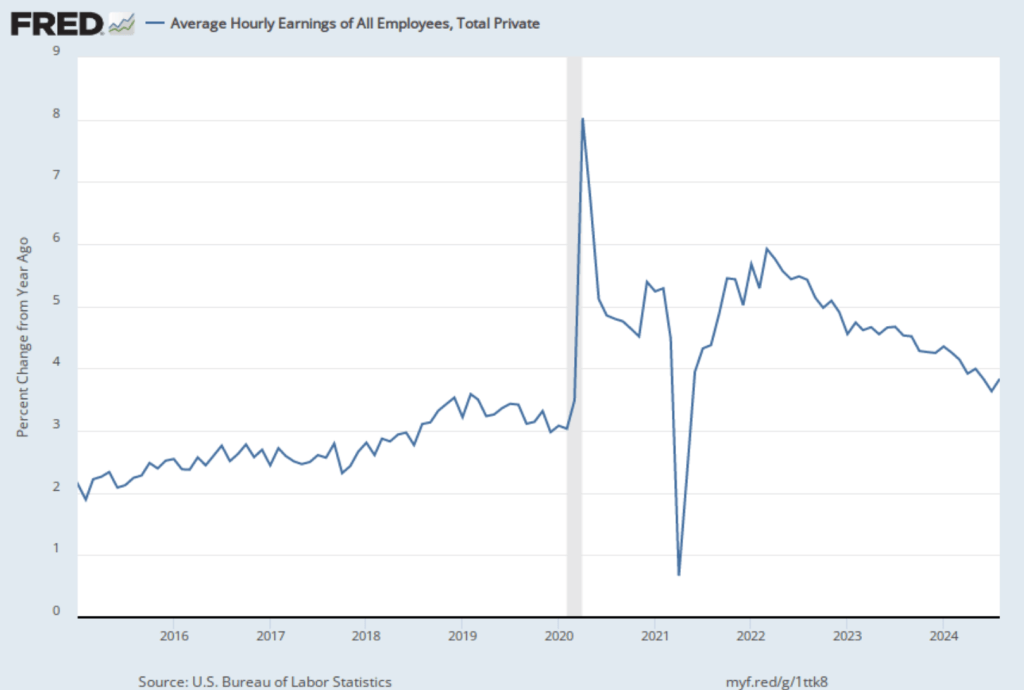

The establishment survey also includes data on average hourly earnings (AHE). As we note in this post, many economists and policymakers believe the employment cost index (ECI) is a better measure of wage pressures in the economy than is the AHE. The AHE does have the important advantage that it is available monthly, whereas the ECI is only available quarterly. The following figure shows the percentage change in the AHE from the same month in the previous year. AHE increased 3.8 percent in August, up from a 3.6 percent increase in July.

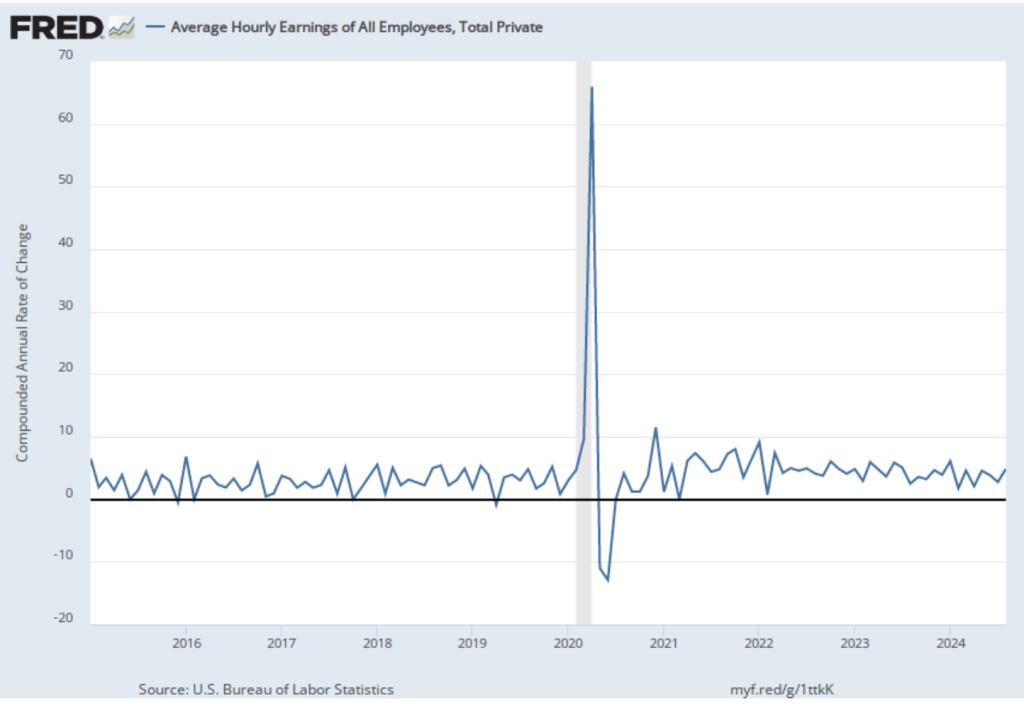

The following figure shows wage inflation calculated by compounding the current month’s rate over an entire year. (The figure above shows what is sometimes called 12-month wage inflation, whereas this figure shows 1-month wage inflation.) One-month wage inflation is much more volatile than 12-month inflation—note the very large swings in 1-month wage inflation in April and May 2020 during the business closures caused by the Covid pandemic.

The 1-month rate of wage inflation of 4.9 percent in August is a significant increase from the 2.8 percent rate in July, although it’s unclear whether the increase represented renewed upward wage pressure in the labor market or reflected the greater volatility in wage inflation when calculated this way.

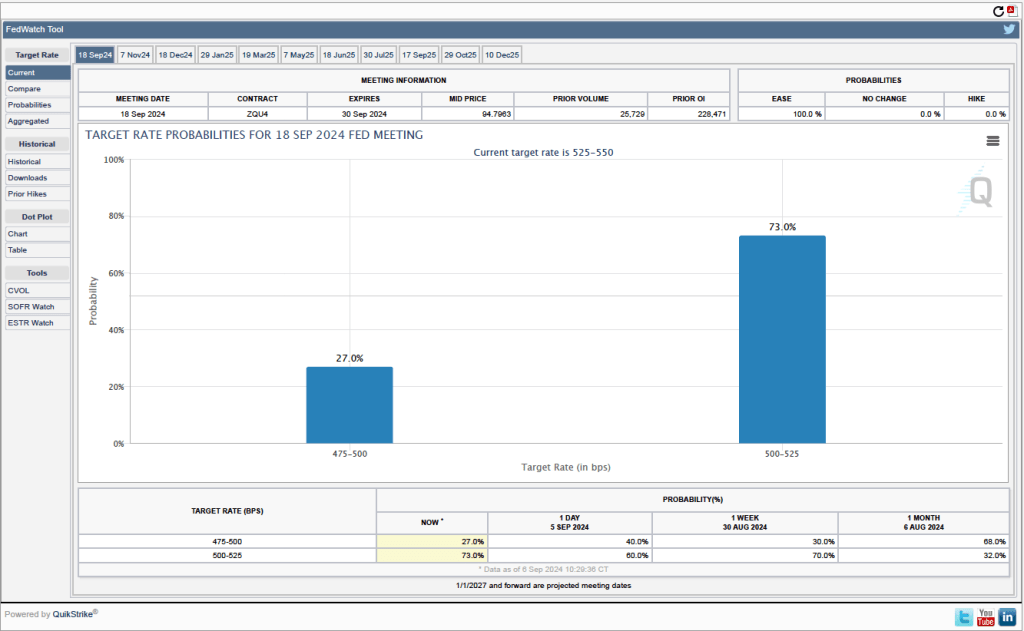

What effect is this jobs report likely to have on the FOMC’s actions at its September meeting? One indication comes from investors who buy and sell federal funds futures contracts. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 73.0 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point at its next meeting and a probability of only 27.0 percent that the cut will be 0.50 percentage point. In contrast, after the last jobs report was interpreted to indicate a dramatic slowing of the economy, investors assigned a probability of 79.5 percent to a 0.50 cut in the federal funds rate target.

It seems most likely following today’s mixed job report that the FOMC will cut its target for the federal funds rate by 0.25 percent point from the current target range of 5.25 percent to 5.50 percent to a range of 5.00 percent to 5.25 percent. The report doesn’t indicate the significant weakening in the labor market that was probably needed to push the committee to cutting its target by 0.50 percent point.