Image illustrating inflation generated by GTP-4o.

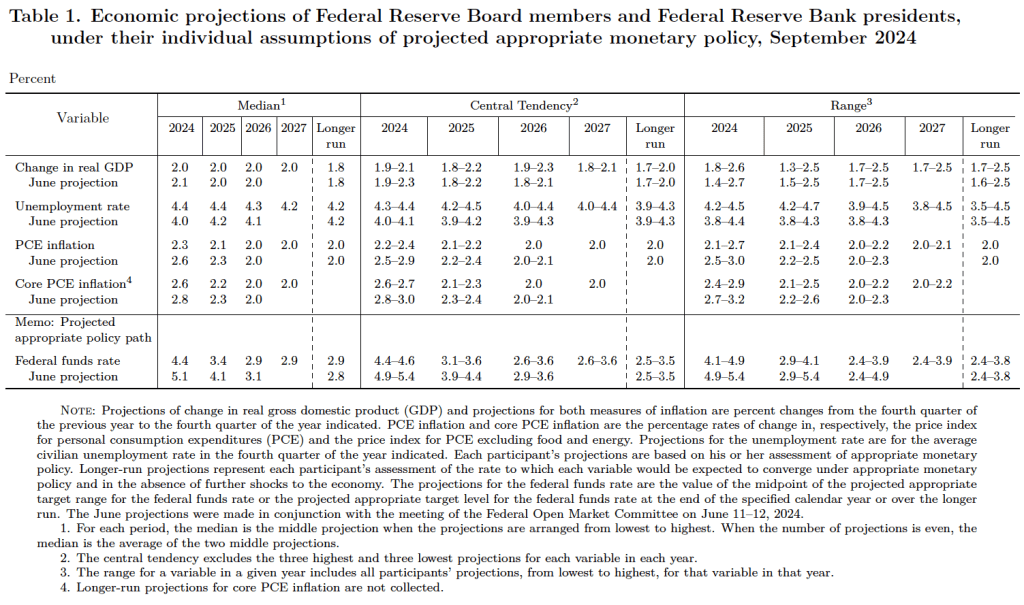

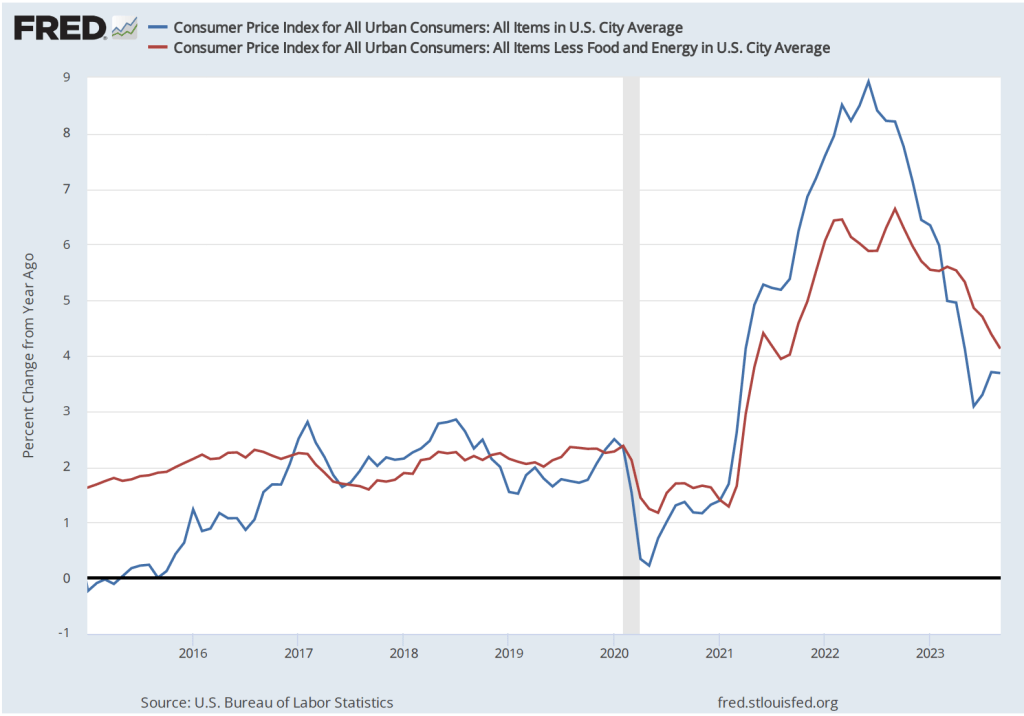

This morning (October 10), the Bureau of Labor Statistics (BLS) released its monthly report on the consumer price index (CPI). As the following figure shows, the inflation rate for September measured by the percentage change in the CPI from the same month in the previous month—headline inflation (the blue line)—was 2.4 percent down from 2.6 percent in August. That was the lowest headline inflation rate since February 2021. Core inflation (the red line)—which excludes the prices of food and energy—was unchanged at 3.3 prcent. Both headline inflation and core inflation were slightly higher than economists surveyed by the Wall Street Journal had expected.

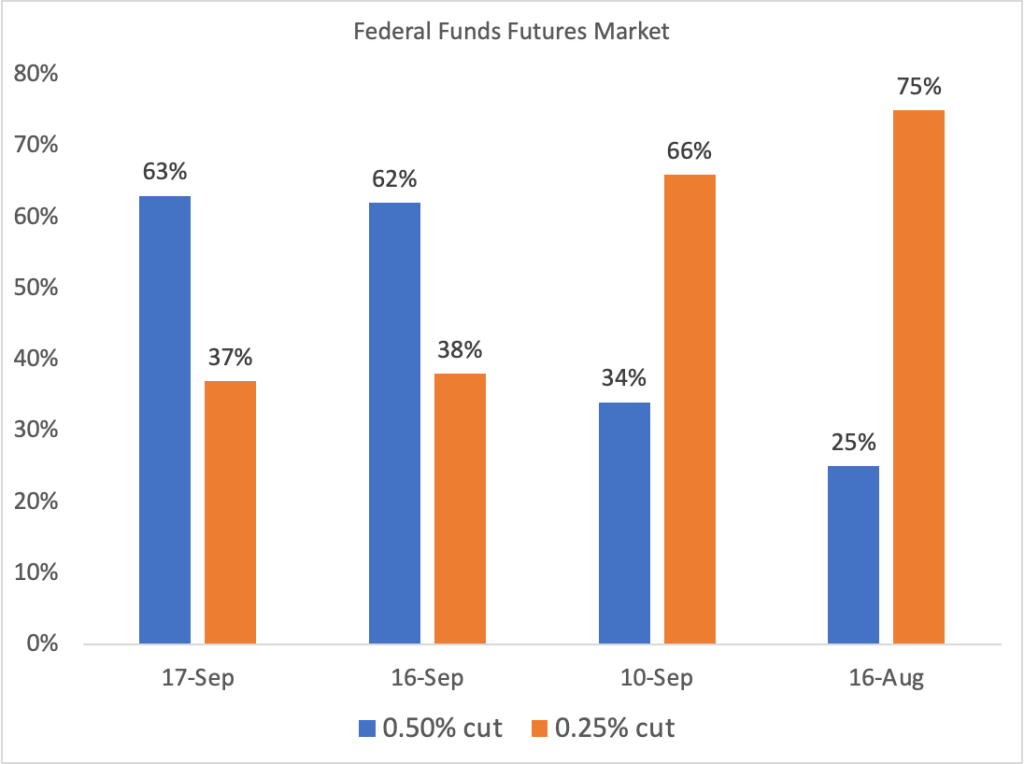

As the following figure shows, if we look at the 1-month inflation rate for headline and core inflation—that is the annual inflation rate calculated by compounding the current month’s rate over an entire year—we see that headline inflation (the blue line) decreased from 2.3 percent in August to 2.2 percent in September. Core inflation (the red line) increased from 3.4 percent in August to 3.8 percent in September.

Overall, we can say that, taking 1-month and 12 month inflation together, the U.S. economy may still be on course for a soft landing—with the annual inflation rate returning to the Fed’s 2 percent target without the economy being pushed into a recession—but the increase in 1-month core inflation is concerning because most economists believe that core inflation is a better indicator of the underlying inflation rate than is headline inflation. Of course, as always, it’s important not to overinterpret the data from a single month, although this is the second month in a row that core inflation has been well above 3 percent. (Note, also, that the Fed uses the personal consumption expenditures (PCE) price index, rather than the CPI in evaluating whether it is hitting its 2 percent inflation target.)

As we’ve discussed in previous blog posts, Federal Reserve Chair Jerome Powell and his colleagues on the FOMC have been closely following inflation in the price of shelter. The price of “shelter” in the CPI, as explained here, includes both rent paid for an apartment or house and “owners’ equivalent rent of residences (OER),” which is an estimate of what a house (or apartment) would rent for if the owner were renting it out. OER is included to account for the value of the services an owner receives from living in an apartment or house.

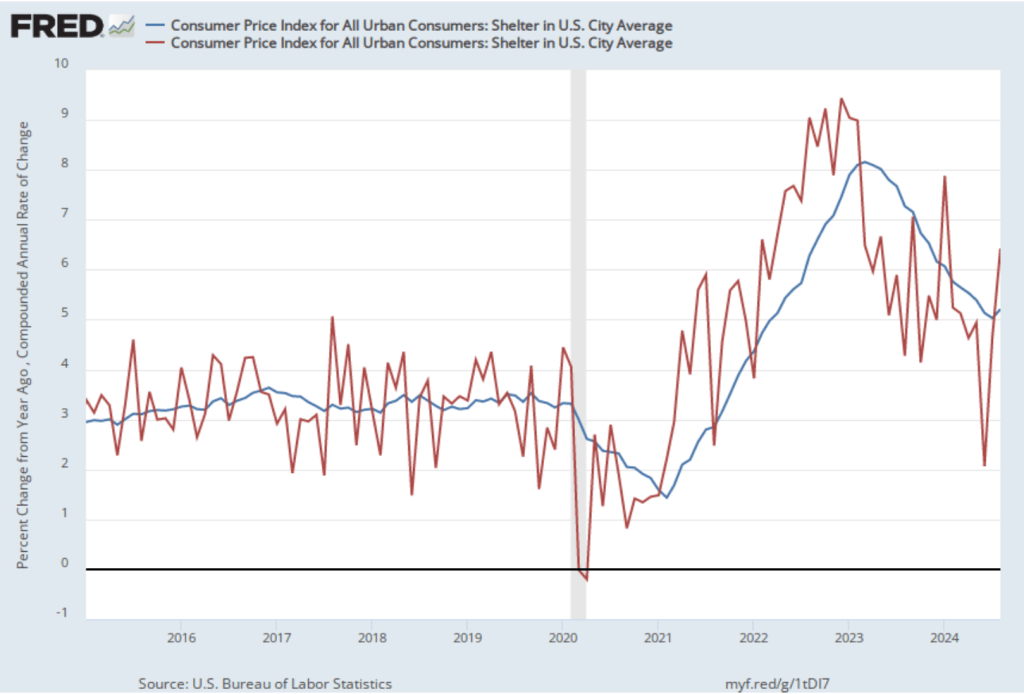

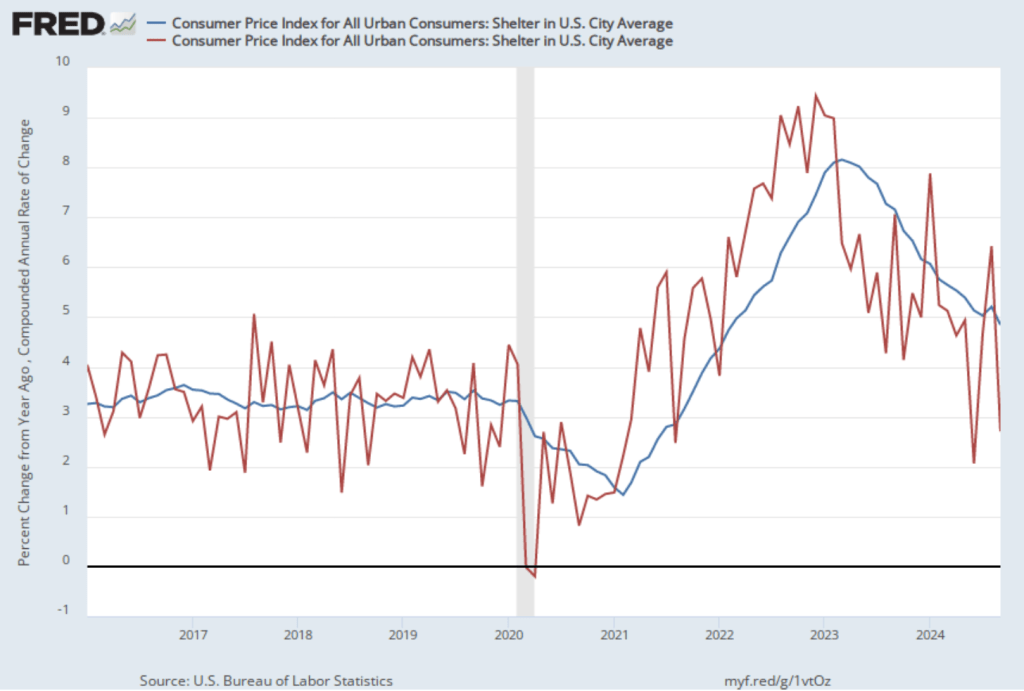

As the following figure shows, inflation in the price of shelter has been a significant contributor to headline inflation. The blue line shows 12-month inflation in shelter and the red line shows 1-month inflation in shelter. After rising in August, 12-month inflation in shelter resumed the decline that began in the spring of 2023, falling from 5.2 percent in August to 4.8 percent September. One-month inflation in shelter—which is much more volatile than 12-month inflation in shelter—declined sharply from 6.4 percent in August to 2.7 percent in September. The members of the FOMC are likely to find the decline in inflation in shelter reassuring as they consider another cut to the target for the federal funds rate at the committee’s next meeting on November 6-7. Shelter has a smaller weight of 15 percent in the PCE price index that the Fed uses to gauge whether it is hitting its 2 percent inflation target in contrast with the 33 percent weight that shelter has in the CPI.

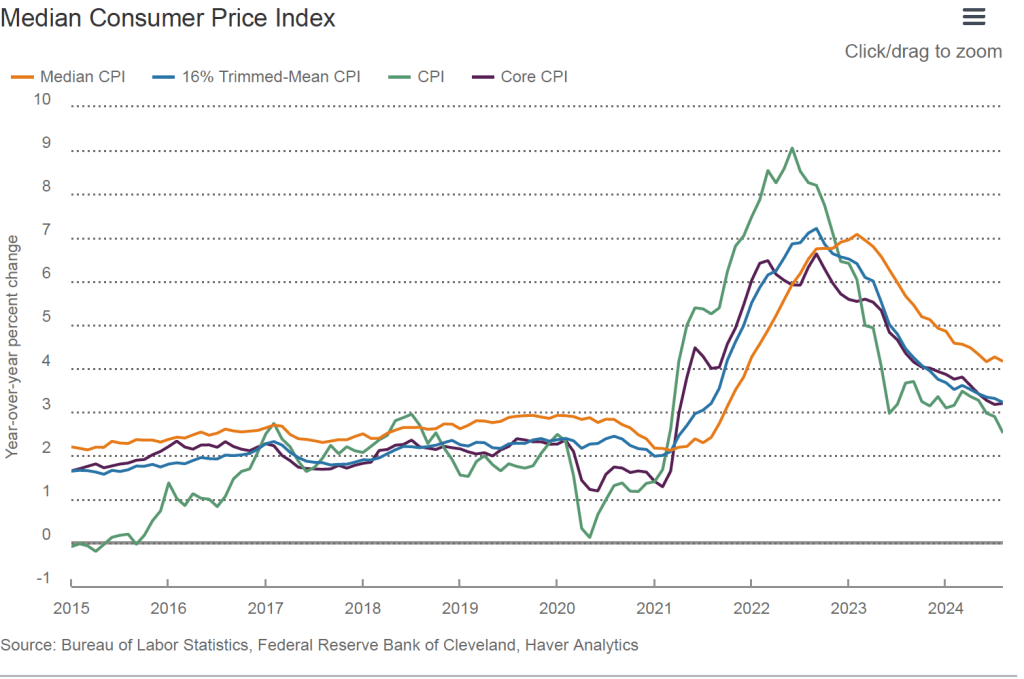

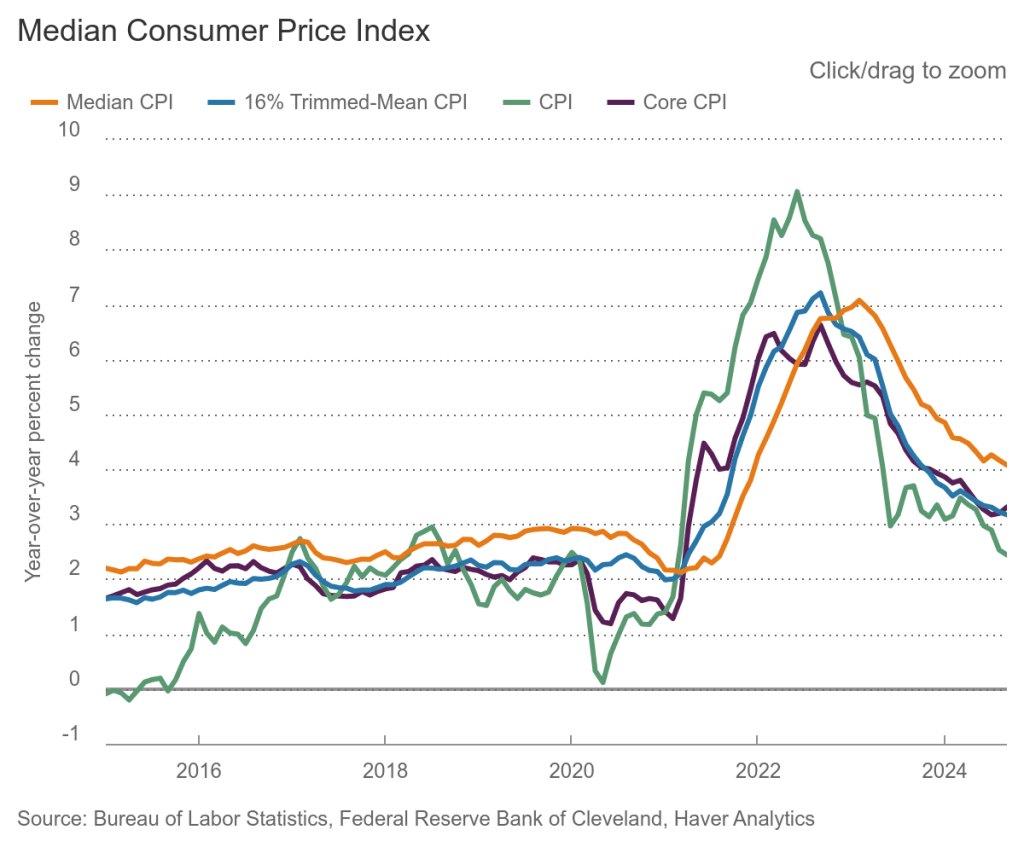

Finally, in order to get a better estimate of the underlying trend in inflation, some economists look at median inflation and trimmed mean inflation. Median inflation is calculated by economists at the Federal Reserve Bank of Cleveland and Ohio State University. If we listed the inflation rate in each individual good or service in the CPI, median inflation is the inflation rate of the good or service that is in the middle of the list—that is, the inflation rate in the price of the good or service that has an equal number of higher and lower inflation rates. Trimmed mean inflation drops the 8 percent of good and services with the higherst inflation rates and the 8 percent of goods and services with the lowest inflation rates.

As the following figure (from the Federal Reserve Bank of Cleveland) shows, median inflation (the orange line) declined slightly from 4.2 percent in August to 4.1 percent in September. Trimmed mean inflation (the blue line) was unchanged at 3.2 percent. These data provide confirmation that core CPI inflation at this point is likely running at least slightly higher than a rate that would be consistent with the Fed achieving its inflation target.

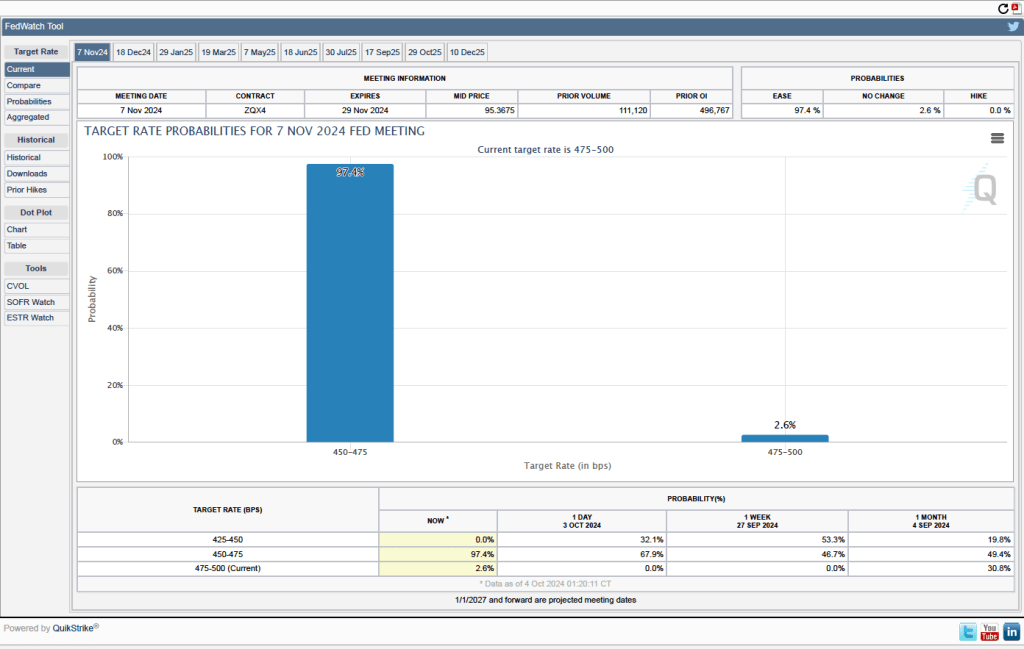

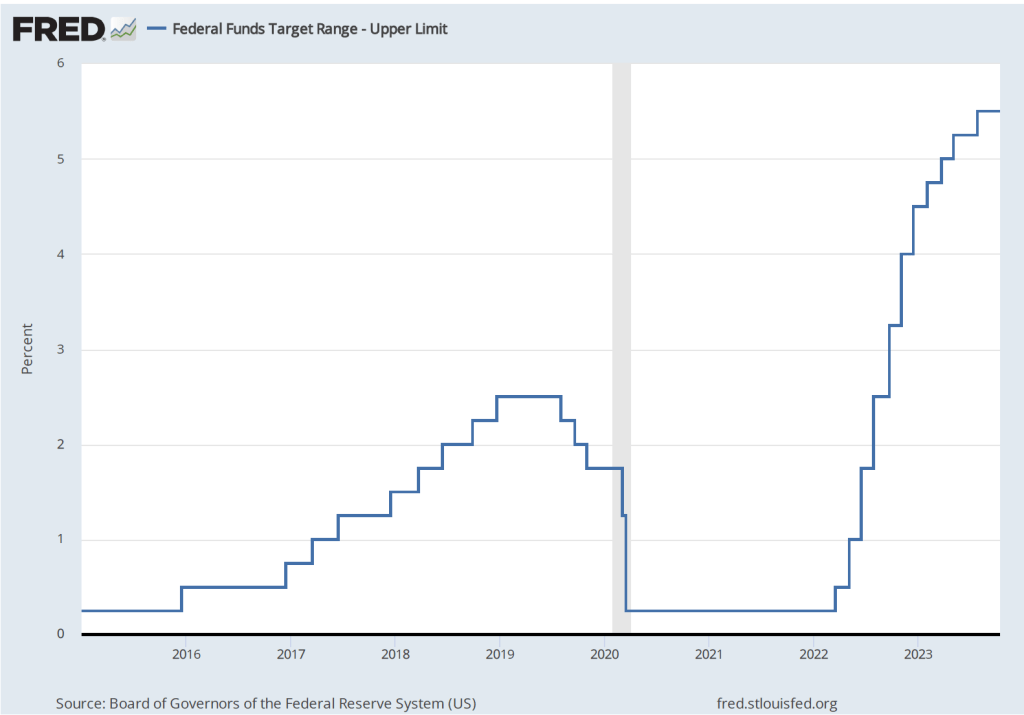

The FOMC cut its target for the federal funds rate by 0.50 percentage point (50 basis points) from 5.50 percent to 5.25 percent to 5.00 percent to 4.75 percent at its last meeting on September 17-18. Some economists and investors believed that the FOMC might cut its target by another 50 basis points at its next meeting on November 6-7. This inflation report makes that outcome less likely. In addition, the release of the minutes from the September 17-18 meeting revealed that a significant number of committee members may have preferred a 25 basis point cut rather than a 50 basis point cut at that meeting:

“However, noting that inflation was still somewhat elevated while economic growth remained solid and unemployment remained low, some participants observed that they would have preferred a 25 basis point reduction of the target range at this meeting, and a few others indicated that they could have supported such a decision.”

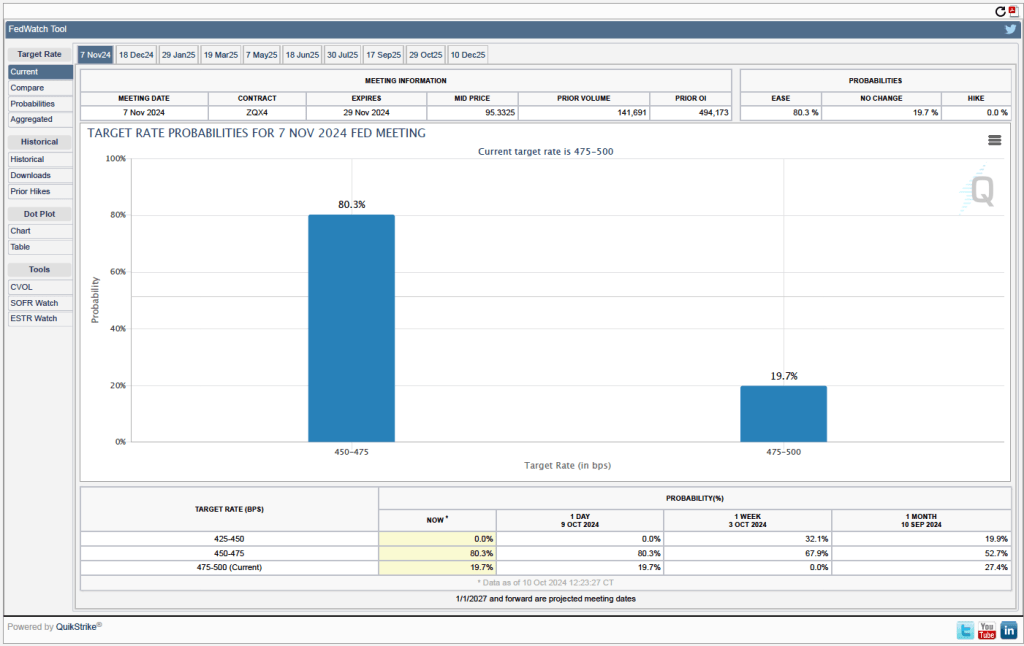

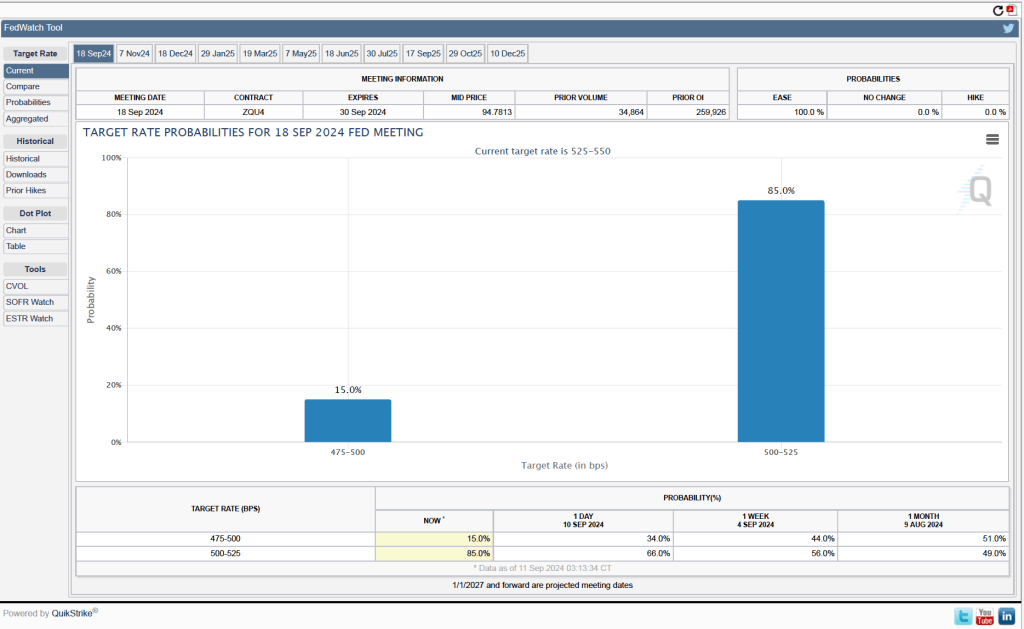

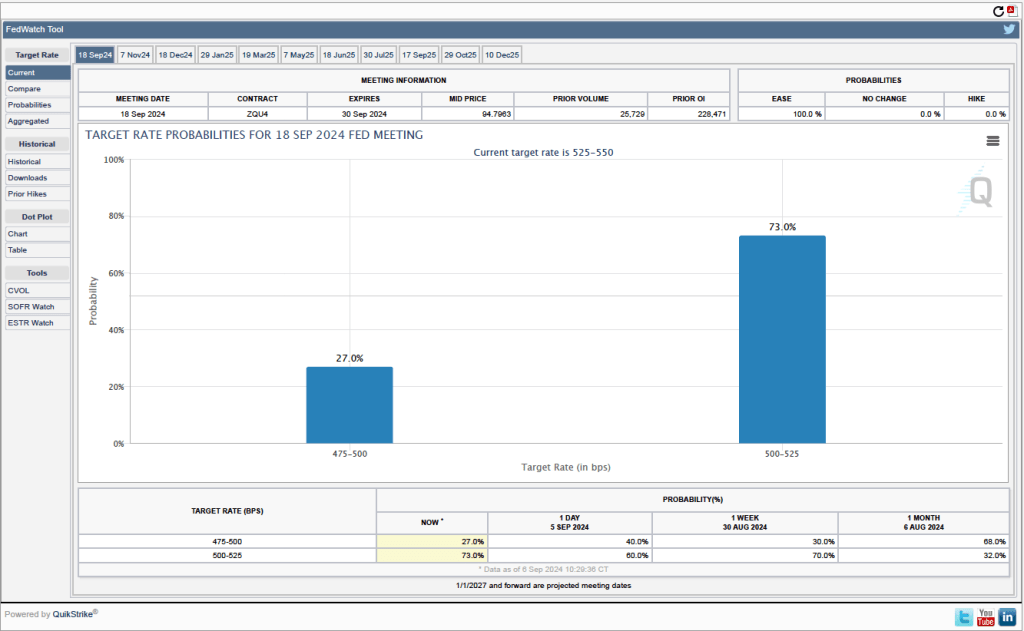

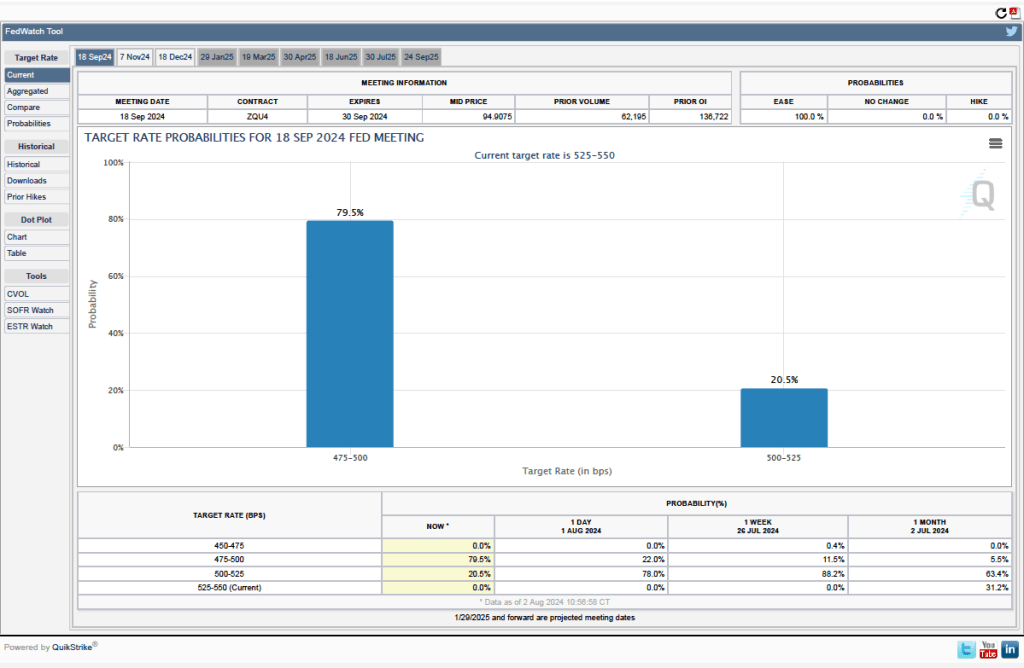

Investors who buy and sell federal funds futures contracts expect that the FOMC will cut its target for the federal funds rate by 0.25 percentage point at its November meeting. (We discuss the futures market for federal funds in this blog post.) As shown in the following figure, today these investors assign a probability of 80.3 percent to the FOMC cutting its target for the federal funds rate by 0.25 percentage point and a probability of 19.7 percent to the committee leaving its target unchanged.