AP photo from the Wall Street Journal

Congress has given the Federal Reserve a dual mandate of high employment and price stability. In addition, though, as we discuss in Macroeconomics, Chapter 15, Section 15.1 (Economics, Chapter 25, Section 25.1) and at greater length in Money, Banking, and the Financial System, Chapter 15, Section 15.1, the Fed has other goals, including the stability of financial markets and institutions.

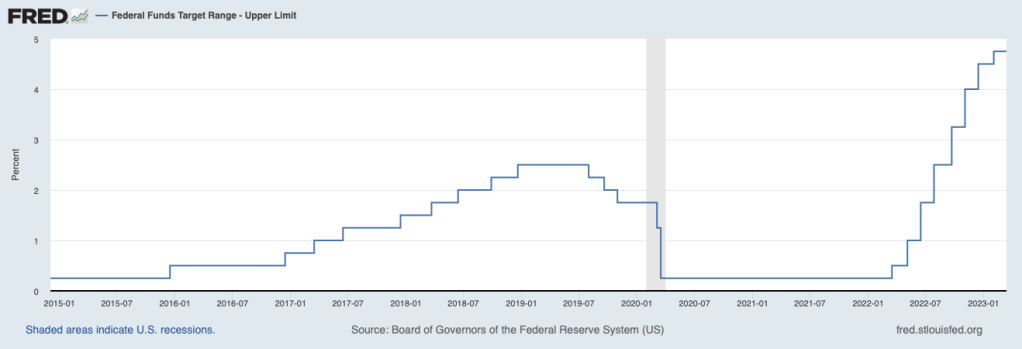

Since March 2022, the Fed has been rapidly increasing its target for the federal funds rate in order to slow the growth in aggregate demand and bring down the inflation rate, which has been well above the Fed’s target of 2 percent. (We discuss monetary policy in a number of earlier blog posts, including here and here, and in podcasts, the most recent of which (from February) can be found here.) The target federal funds rate has increased from a range of 0 percent to 0.25 percent in March 2022 to a range of 4.5 percent to 4.75 percent. The following figure shows the upper range of the target for the federal funds rate from January 2015 through March 14, 2023.

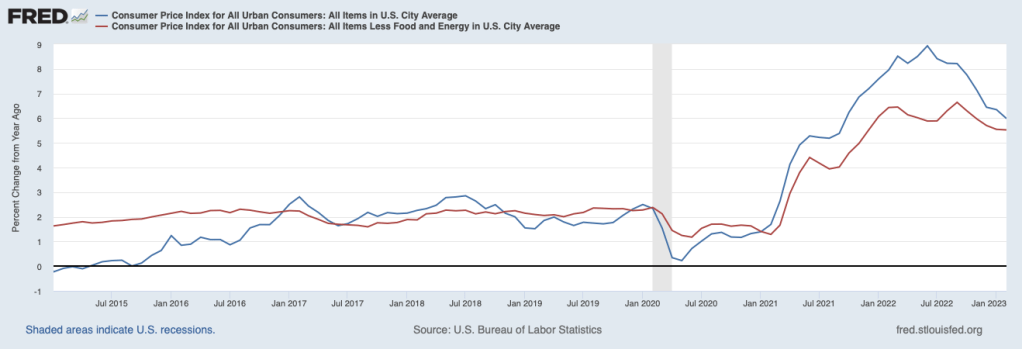

This morning (Tuesday, March 14, 2023), the Bureau of Labor Statistics (BLS) released its data on the consumer price index for February. The following figure show inflation as measured by the percentage change in the CPI from the same month in the previous year (which is the inflation measurement we use most places in the text) and as the percentage change in core CPI, which excludes prices of food and energy. (The inflation rate computed by the percentage change in the CPI is sometimes referred to as headline inflation.) The figure shows that although inflation has slowed somewhat it is still well above the Fed’s 2 percent target. (Note that, formally, the Fed assesses whether it has achieved its inflation target using changes in the personal consumption expenditures (PCE) price index rather than using changes in the CPI. We discuss issues in measuring inflation in several blog posts, including here and here.)

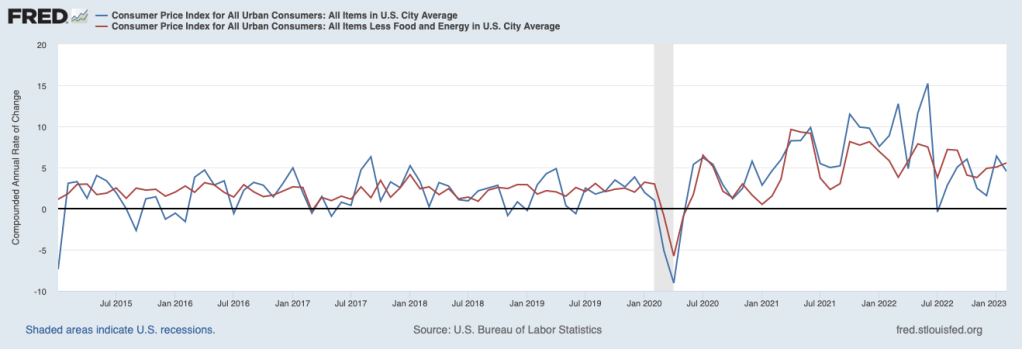

One drawback to using the percentage change in the CPI from the same month in the previous year is that it reduces the weight of the most recent observations. In the figure below, we show the inflation rate measured by the compounded annual rate of change, which is the value we would get for the inflation rate if that month’s percentage change continued for the following 12 months. Calculated this way, we get a somewhat different picture of inflation. Although headline inflation declines from January to February, core inflation is actually increasing each month from November 2022 when, it equaled 3.8 percent, through February 2023, when it equaled 5.6 percent. Core inflation is generally seen as a better indicator of future inflation than is headline inflation.

The February CPI data are consistent with recent data on PCE inflation, employment growth, and growth in consumer spending in that they show that the Fed’s increases in the target for the federal funds rate haven’t yet caused a slowing of the growth in aggregate demand sufficient to bring the inflation back to the Fed’s target of 2 percent. Until last week, many economists and Wall Street analysts had been expecting that at the next meeting of the Fed’s Federal Open Market Committee (FOMC) on March 21 and 22, the FOMC would raise its target for the federal funds rate by 0.5 percentage points to a range of 5.0 percent to 5.25 percent.

Then on Friday, the Federal Deposit Insurance Corporation (FDIC) was forced to close the Silicon Valley Bank (SVB). As the headline on a column in the Wall Street Journal put it “Fed’s Tightening Plans Collide With SVB Fallout.” That is, the Fed’s focus on price stability would lead it to continue its increases in the target for the federal funds rate. But, as we discuss in this post from Sunday, increases in the federal funds rate lead to increases in other interest rates, including the interests rates on the Treasury securities, mortgage-backed securities, and other securities that most banks own. As interest rates rise, the prices of long-term securities decline. The run on SVB was triggered in part by the bank taking a loss on the Treasury securities it sold to raise the funds needed to cover deposit withdrawals.

Further increases in the target for the federal funds rate could lead to further declines in the prices of long-term securities that banks own, which might make it difficult for banks to meet deposit withdrawals without taking losses on the securities–losses that have the potential to make the banks insolvent, which would cause the FDIC to seize them as it did SVB. The FOMC’s dilemma is whether to keep the target for the federal funds rate unchanged at its next meeting on March 21 and 22, thereby keeping banks from suffering further losses on their bond holdings, or to continue raising the target in pursuit of its mandate to restore price stability.

Some economists were urging the FOMC to pause its increases in the target federal funds rate, others suggested that the FOMC increase the target by only 0.25 percent points rather than by 0.50 percentage points, while others argued that the FOMC should implement a 0.50 increase in order to make further progress toward its mandate of price stability.

Forecasting monetary policy is a risky business, but as of Tuesday afternoon, the likeliest outcome was that the FOMC would opt for a 0.25 percentage point increase. Although on Monday the prices of the stocks of many regional banks had fallen, during Tuesday the prices had rebounded as investors appeared to be concluding that those banks were not likely to experience runs like the one that led to SVB’s closure. Most of these regional banks have many more retail deposits–deposits made be households and small local businesses–than did SVB. Retail depositors are less likely to withdraw funds if they become worried about the solvency of a bank because the depositors have much less than $250,000 in their accounts, which is the maximum covered by the FDIC’s deposit insurance. In addition, on Sunday, the Fed established the Bank Term Funding Program (BTFP), which allows banks to borrow against the holdings of Treasury and mortgage-back securities. The program allows banks to meet deposit withdrawals by borrowing against these securities rather than by having to sell them–as SVB did–and experience losses.

On March 22, we’ll find out how the Fed reacts to the latest dilemma facing monetary policy.